Non-Dairy Cheese Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.79 Billion |

| Market Size (2031) | USD 5.75 Billion |

| Growth Rate (2026 - 2031) | 15.63% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

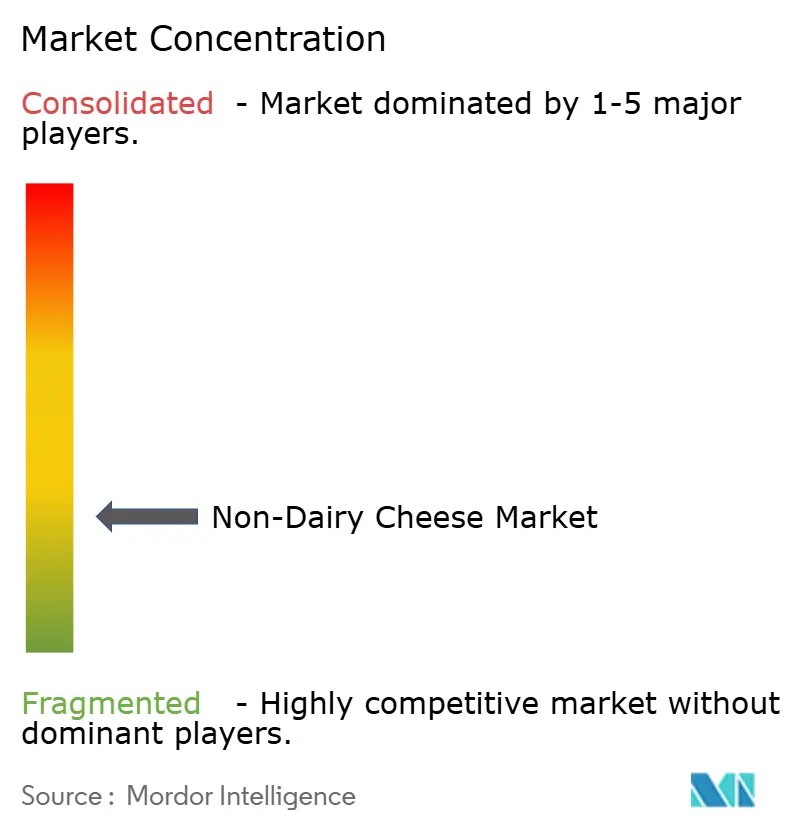

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Non-Dairy Cheese Market Analysis by Mordor Intelligence

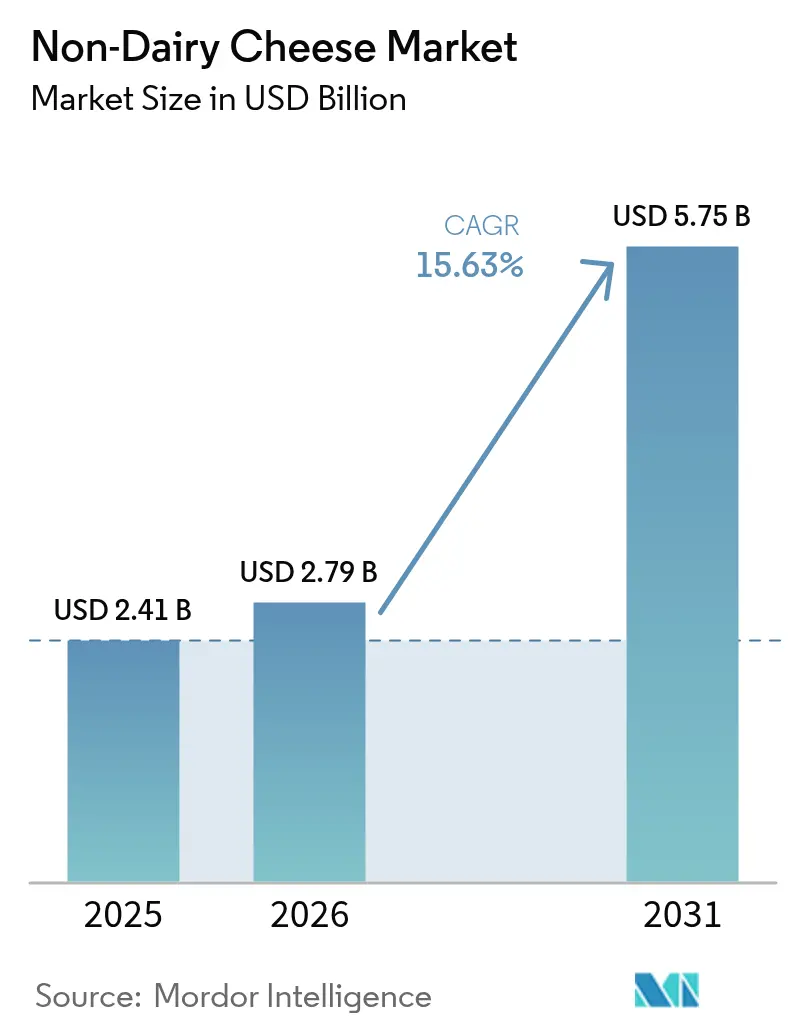

The non-dairy cheese market size is expected to grow from USD 2.41 billion in 2025 to USD 2.79 billion in 2026 and is forecast to reach USD 5.75 billion by 2031 at 15.63% CAGR over 2026-2031. Consumer adoption of plant-based cheese is increasing as health-conscious and environmentally conscious consumers seek dairy alternatives. Manufacturers are using precision fermentation and data-driven formulation to improve product characteristics like melting, stretching, and texture. Flexitarian consumers, who reduce rather than eliminate animal products, represent a key market segment. In response, manufacturers are optimizing recipes and expanding product formats to meet taste expectations while managing costs. The competitive landscape centers on ingredient selection, with soy maintaining the largest market share due to established supply chains. However, oat-based alternatives show the highest growth rates, driven by their neutral taste profile and environmental benefits. The retail presence of plant-based cheese is expanding as retailers enhance their carbon reduction goals and cold storage capabilities, enabling manufacturers to increase production and work toward achieving cost competitiveness with traditional dairy products.

Key Report Takeaways

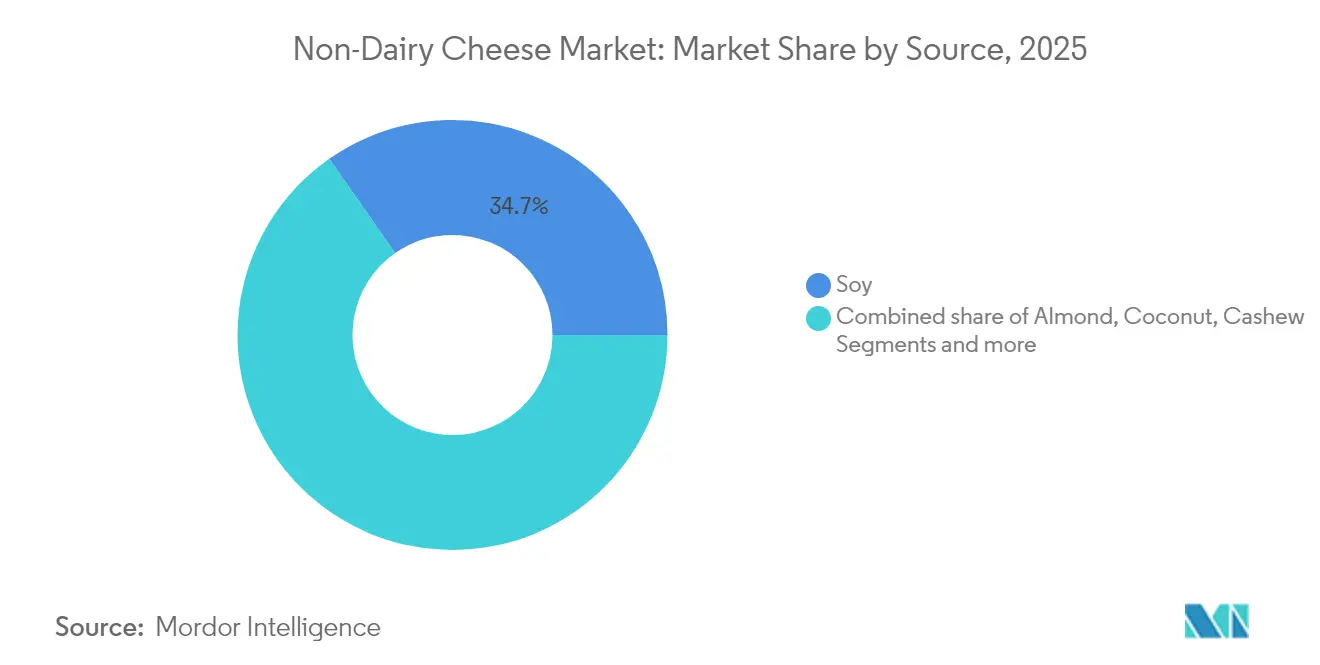

- By source, soy led with 34.72% revenue share in 2025; oat is forecasted to expand at an 18.74% CAGR through 2031.

- By form, blocks and slices segment held 40.12% of the non-dairy cheese market share in 2025, while shreds and grated recorded the highest projected CAGR at 18.26% through 2031.

- By distribution channel, the supermarkets/hypermarkets channel captured 55.48% revenue in 2025; online retail is growing at a 17.02% CAGR through 2031.

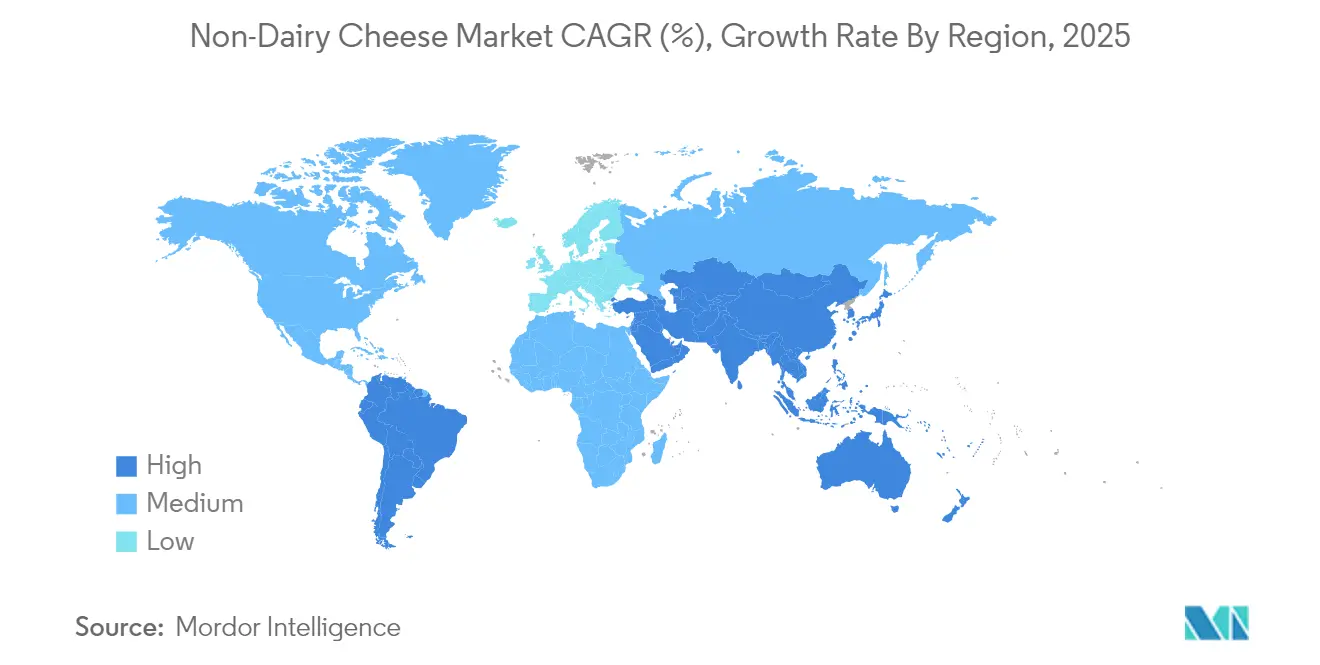

- By geography, Europe commanded a 42.35% share of the market in 2025, while Asia-Pacific is the fastest-growing region at 16.88% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Non-Dairy Cheese Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flexitarian diet uptake in cheese-consuming households | +4.2% | North America, Europe | Medium term (3-4 years) |

| Product innovation and better taste/texture | +3.8% | Global | Medium term (3-4 years) |

| Sustainable and ethical concerns | +2.5% | Europe, Urban North America | Long term (≥5 years) |

| Rising lactose-intolerance diagnosis | +2.1% | Asia-Pacific | Short term (≤2 years) |

| Expanding flavor varieties and formats are broadening consumer appeal | +1.8% | Global, with higher impact in mature markets | Medium term (3-4 years) |

| Greater retail and foodservice presence is enhancing product visibility and accessibility | +1.5% | Global, with early gains in urban centers | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Flexitarian Influence Drives Innovation in Plant-Based Cheese Market

The growth of flexitarian diets influences the plant-based cheese market, as these consumers emphasize taste preferences over ethical factors. The International Food Information Council (IFIC) Food and Health Survey in 2024 indicated that approximately 5% of Americans followed a flexitarian diet[1]Source: International Food Information Council, "2024 Food And Health Survey", foodinsight.org/2024-foodhealth-survey. Manufacturers are adapting to these consumer preferences by improving the sensory qualities of non-dairy cheese products. Their focus is on enhancing meltability, stretch, and umami flavor profiles to match traditional dairy cheese characteristics. These quality improvements are essential for attracting flexitarian consumers who expect taste parity with conventional cheese products. With the evolving preference, consumers view non-dairy cheese as complementary options rather than substitutes, aligning with flexitarian dietary practices. Moreover, millennials and generation Z consumers are choosing non-dairy cheese alternatives due to health consciousness, preference for plant-based foods, and environmental concerns. These consumers select products that match their values, including ethical sourcing and environmental sustainability.

Product Innovation and Better Taste/Texture

Advances in precision fermentation, data-driven recipe development, and enzyme modification enable manufacturers to reduce their dependence on coconut oil while achieving dairy-like stretch and melt properties. For instance, in March 2024, New Culture, a California-based food technology company, received pre-launch commitments exceeding USD 5 million from US pizza restaurants for its mozzarella cheese, which is produced using precision-fermented casein without animal inputs. Initial trials combining pulse protein isolates with specialized fats have demonstrated mouthfeel characteristics comparable to dairy mozzarella in blind tastings. This improvement has encouraged restaurant chains to introduce vegan pizzas and quesadillas across their locations. These implementations provide two key benefits: they generate consistent production volume to offset bioreactor investments and showcase plant-based cheese products to mainstream consumers. Additionally, menu placement serves as a marketing channel, encouraging retail consumers to purchase these products for home consumption.

Sustainable and Ethical Concerns

Life-cycle analyses demonstrate that plant-based cheese production generates lower greenhouse gas emissions and requires less land compared to conventional dairy cheese manufacturing. Manufacturers now display carbon scores on their packaging to inform consumers about the environmental impact of their products. Retailers incorporate verified environmental certifications in their category reviews to ensure accurate product claims. Retail buyers use these environmental metrics to differentiate products in their assortment. This approach benefits plant-based cheese manufacturers by helping them obtain shelf space in competitive retail environments. Additionally, investors focused on decarbonization view plant-based cheese as an investment opportunity, particularly considering potential climate regulations affecting animal agriculture. This combination of environmental benefits and market opportunities is reshaping the food industry. Moreover, consumer awareness about environmental sustainability and animal welfare is driving the growth of non-dairy cheese. According to the International Food Information Council (IFIC) Food and Health Survey in 2024, approximately 33% of consumers follow vegan, vegetarian, or plant-based eating patterns due to animal welfare concerns, while 26% make these choices to support environmental sustainability [2]Source: International Food Information Council, "2024 Food And Health Survey", foodinsight.org/2024-foodhealth-survey.

Rising Lactose-Intolerance Diagnosis

A significant portion of the global adult population has lactose intolerance, and lactose testing has become more accessible, especially in East and Southeast Asia. According to data from MedlinePlus, which is part of the National Institutes of Health (NIH), approximately 65% of the global population has a reduced ability to digest lactose after infancy. The condition, known as lactase nonpersistence, affects 70-100% of people of East Asian descent. The condition is also highly prevalent among people of West African, Arab, Jewish, Greek, and Italian descent [3]Source: MedlinePlus, “Lactose Intolerance: MedlinePlus Genetics”, medlineplus.gov. Medical professionals frequently recommend dairy-free diets to patients experiencing chronic gastrointestinal issues, directing them to plant-based cheese alternatives. The products with "easy to digest" labels achieve higher household penetration rates, indicating the continued importance of health-related claims. Retailers have adapted by implementing lactose-free and vegan indicators on shelf labels, simplifying product selection for consumers following medical recommendations. For instance, Walmart offers a wide selection of vegan cheeses, including Daiya and Follow Your Heart, among others.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High prices compared to dairy cheese | -3.5% | Global | Short term (≤2 years) |

| Limited nutritional parity with dairy | -2.2% | Global | Medium term (3-4 years) |

| Use of allergens like nuts or soy in formulations can restrict consumer base | -1.7% | Global, with higher impact in regions with allergen awareness | Medium term (3-4 years) |

| Regulatory restrictions on labeling can hinder marketing and product clarity | -1.4% | Europe, North America | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

High Prices Compared to Dairy Cheese

Plant-based cheese products maintain higher price points compared to traditional dairy cheese, creating a significant barrier to market growth. In developing countries, the cost factor particularly impacts market expansion, as economic constraints limit consumers' ability to purchase alternative dairy options. The substantial price difference between non-dairy and conventional cheese products often discourages potential buyers. Limited product availability in local markets compounds this challenge, restricting consumer access to non-dairy cheese options. The price disparity primarily results from specialized production methods, premium ingredient requirements, and reduced economies of scale in plant-based manufacturing. However, recent advancements in ingredient diversification and fermentation processes are reducing unit production costs. These improvements allow manufacturers to incorporate various plant-based ingredients, enhancing both taste and texture profiles while lowering production expenses. Decreasing production costs are attracting price-sensitive consumers to plant-based cheese alternatives. This development mirrors trends in other alternative protein categories, where improved affordability and product variety have driven increased consumer acceptance.

Limited Nutritional Parity with Dairy

Plant-based cheese alternatives have distinct nutritional profiles compared to dairy cheese, particularly regarding protein content and bioavailable calcium. These alternatives typically contain lower nutritional diversity, with high levels of saturated fat from coconut oil, but lack the protein and micronutrient density of dairy products. Manufacturers use oils and starches to replicate the creamy texture and flavor characteristics of traditional dairy cheese. This formulation approach results in lower protein content compared to dairy cheese, creating challenges for health-conscious consumers, athletes, bodybuilders, and individuals with specific dietary needs. The protein content gap influences purchasing decisions, especially among consumers who prioritize protein intake. Products labeled as "complete protein" sources that contain all essential amino acids demonstrate strong performance in natural food stores, with increased sales indicating consumer demand for nutritionally balanced plant-based alternatives that combine traditional cheese characteristics with adequate nutritional content.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Soy Dominates While Oat Accelerates

Soy-based formulations account for 34.72% of the non-dairy cheese market in 2025, leveraging established supply chains, competitive pricing, and versatile functional properties. Oat-based alternatives demonstrate strong growth with an 18.74% CAGR (2026-2031), driven by their neutral flavor profile and lower water consumption compared to nut-based options. This growth reflects the broader consumer shift toward oat-based dairy alternatives.

Chickpea emerged as a notable ingredient when ChickP, a food technology startup, developed cheese alternatives using 90% protein isolate with enhanced nutritional and functional properties in March 2023. Almond-based products retain a significant market share due to consumer familiarity. However, coconut-based alternatives show declining demand as manufacturers reduce their use due to high saturated fat content, despite their dairy-like texture. Precision fermentation technology advances the market through the production of dairy-identical proteins without animal inputs. Companies such as NewMoo and DairyX produce casein proteins through fermentation processes, enabling the development of plant-based cheeses that match dairy functionality.

By Distribution Channel: Supermarkets Dominate as E-commerce Gains Momentum in Non-Dairy Cheese Market

Supermarkets and hypermarkets dominate the plant-based cheese distribution landscape, accounting for 55.48% of sales in 2025. Their market leadership results from extensive consumer reach and the ability to display plant-based options alongside conventional dairy products, which increases product visibility and consumer trial.

Online retail demonstrates the highest growth rate at 17.02% CAGR (2026-2031). This growth is driven by increased e-commerce adoption following the pandemic and the platform's capacity to provide comprehensive product information and consumer reviews. The digital platform particularly benefits premium and specialty plant-based cheese brands by enabling detailed communication of their product attributes, surpassing the limitations of physical retail shelf space.

Specialty stores hold a notable market position, particularly in the distribution of artisanal and premium plant-based cheese products. These stores cater to dedicated plant-based consumers seeking high-quality and innovative options. The foodservice sector presents expanding opportunities as restaurants incorporate more plant-based alternatives. Brands such as Miyoko's and Follow Your Heart have established foodservice partnerships with establishments including Mellow Mushroom and Veggie Grill.

By Form: Blocks and Slices Lead While Shreds Gain Momentum

Blocks and slices constitute 40.12% of the plant-based cheese market in 2025, due to their convenience and versatility in both household and food service applications. Blocks offer flexibility for slicing, grating, or shredding, adapting to various cooking needs. Pre-cut slices are commonly used in sandwiches, burgers, and pizzas, providing ease of use for consumers.

Shreds and grated varieties are experiencing the highest growth rate at 18.26% CAGR (2026-2031), due to their cooking convenience and enhanced melting properties from improved formulations. Spreads and dips retain a substantial market share, as manufacturers face fewer technical challenges in developing these formats compared to products requiring melting capabilities. Follow Your Heart's introduction of dairy-free Bleu Cheese Crumbles, the first such product in the market, indicates continued product development beyond conventional slices and shreds. In September 2024, Armored Fresh's patent application for specialized plant-based grated cheese production highlights the strategic importance of this segment. Their technology aims to replicate the texture and appearance of traditional grated aged cheese, meeting consumer demand for authentic alternatives.

Geography Analysis

Europe dominates the plant-based cheese market with a 42.35% share in 2025, supported by the region's strong vegan movement, environmental consciousness, and established plant-based food ecosystem. The market's growth is driven by the country's large consumer base of vegetarians and flexitarians seeking alternatives to conventional cheese products. The availability of vegan cheese brands through supermarkets and specialty stores has contributed to market expansion. Major restaurant chains in the UK, including Pizza Hut, Domino's, McDonald's, Greggs, and Subway, have added vegan dishes with dairy-free cheese to their menus, increasing market penetration.

Asia-Pacific shows the highest growth rate at 16.88% CAGR (2026-2031), driven by increasing lactose intolerance awareness, health consciousness, and rising disposable incomes. China and Japan lead the regional growth, while South Korea has become a significant market due to its innovative food culture and acceptance of plant-based alternatives. India demonstrates broader plant-based food acceptance that benefits the cheese alternative segment. North America holds a substantial market share, with the United States driving innovation through startups like Climax Foods, which uses AI to develop plant-based cheeses that replicate traditional dairy varieties. The region's growth continues through strong retail distribution and increasing consumer acceptance. South America and the Middle East and Africa present emerging opportunities, with Brazil and the UAE demonstrating promise due to increasing health consciousness and expanding retail distribution networks for plant-based products. These regions face challenges including limited consumer awareness, price sensitivity, and underdeveloped cold chain infrastructure.

Regulatory Landscape

Regulation for non-dairy cheese is shaped by rules on the use of dairy designations, allergen statements, and novel ingredient approvals, with meaningful divergence across major markets. In the European Union, Regulation (EU) No 1308/2013 reserves dairy terms (including "cheese") for milk products, which continues to constrain front-of-pack naming for purely plant-based analogs even when clarifying descriptors are used. In the United States, the FDA issued draft guidance in January 2025 for labeling plant-based alternatives to animal-derived foods (other than milk), signaling closer scrutiny of how plant-based products use standardized dairy names and how labeling communicates product differences.

International standard-setting activity also affects cross-border trade and labeling strategies. The International Dairy Federation (IDF) published Bulletin N 541/2026 (June 2026) discussing the Codex General Standard for the Use of Dairy Terms and its implications for restricting dairy names on non-dairy products, and the FAO/WHO Codex Alimentarius Commission held its 49th session in July 2026 to adopt new food standards. Against this backdrop, national measures such as France's decree restricting the use of animal-derived product names for vegetable-protein-based foods (subject to ongoing legal challenges) reinforce the need for market-by-market packaging, claims, and product naming plans for global brand rollouts.

Value Chain Analysis

The non-dairy cheese value chain starts with agricultural and specialty input suppliers providing plant proteins (soy, pulses, oats, nuts), plant oils and fats, starches and hydrocolloids, flavors, and cultures, followed by ingredient processing and functionalization (protein isolation, fractionation, and texturization). Manufacturers then carry out formulation and blending, emulsification and thermal treatment, and in some cases fermentation to build flavor and structure, before forming into blocks, slices, shreds, or spreads, packaging, and distributing through cold-chain logistics. Downstream, scale depends on supermarkets/hypermarkets, specialty retail, online, and foodservice buyers (notably pizza and fast-casual), where consistent melt and stretch performance drives repeat ordering.

A parallel, faster-evolving branch of the chain is precision fermentation for animal-free casein, which brings biotechnology platforms, fermentation capacity, and regulatory clearance workflows into sourcing and manufacturing. In June 2026, Formo progressed its US pathway by submitting an FDA GRAS notice (GRN 1312) for recombinant alpha-S1-casein, while New Culture received US Patent No. 12,635,703 in July 2026 covering an animal-free mozzarella formulation containing precision-fermented alpha-S1-casein. These developments point to key bottlenecks (taste/texture parity, cost of fermentation scale-up, and novel-ingredient compliance), and they also show how startups are using partnerships and existing fermentation assets to reduce capital intensity and shorten time to commercial supply for food manufacturers and foodservice operators.

Competitive Landscape

The plant-based cheese market demonstrates a fragmented structure, consisting of specialized plant-based manufacturers, established dairy companies, and emerging startups. The fragmented market structure drives innovation as companies work to improve taste and texture characteristics. The major players in the non-dairy cheese market include Otsuka Holdings Co., Ltd. (Daiya Foods Inc.), Danone S.A., and Saputo Inc., among others. The key players are adopting various strategies such as product innovations, partnerships, expansions, mergers, and acquisitions.

Strategic partnerships are transforming the competitive landscape, as traditional dairy companies partner with or acquire plant-based specialists. Bel's collaboration with Climax in May 2022 has resulted in product prototypes, including vegan Babybel cheeses, scheduled for market release in the fourth quarter of 2024. In July 2024, Leprino Foods partnered with Fooditive Group to develop animal-free casein through precision fermentation for non-dairy cheese applications.

Technology-focused startups are emerging as market disruptors. Climax Foods utilizes data science and machine learning to analyze plant ingredient combinations for optimal taste and texture. In July 2024, NewMoo, Ltd. entered the market using plant molecular farming (PMF) technology to produce casein proteins for cheese production.

Non-Dairy Cheese Industry Leaders

-

Otsuka Holdings Co, Ltd. (Daiya Foods Inc.)

-

Saputo Inc. (Vitalite)

-

Danone S.A. (Follow Your Heart)

-

Miyoko’s Creamery PBC

-

Flora Food Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Foodservice-led volume remains a clear commercialization lane for non-dairy cheese, especially for mozzarella-style applications where melt, stretch, and browning are decisive. Recent activity in precision-fermented casein reinforces this opportunity: Those Vegan Cowboys raised 12.25 million euros in March 2026 to scale animal-free casein and cited work with multiple food companies (including Hochland and Westland Kaas), and New Culture secured a mozzarella-focused patent in July 2026 aimed at the US pizza channel. For brands and ingredient developers, this channel offers a route to higher throughput and faster iteration cycles than retail-only launches, while also building consumer familiarity through menu exposure.

Capacity expansion and technology licensing create additional whitespace as manufacturers move from pilot outputs toward repeatable, commercial-scale supply. In March 2026, Quevana opened a 2,400-square-meter cashew cheese facility in Vallelado, Spain, with capacity stated at over 400,000 units per month, reflecting investment in European-scale production of plant-based cheese formats. In January 2026, Finland-based Mo Foods raised 2.4 million euros to scale oat-based cheese technology with a licensing model geared to established European producers, pointing to a pathway where process know-how and formulations are deployed via partners rather than solely through owned factories. Alongside these moves, navigating differing regulatory pathways (notably US GRAS processes versus EFSA-facing approvals for novel proteins) creates a practical opening for co-manufacturers and ingredient suppliers that can provide validated compliance packages, documentation, and standardized specifications for multi-country product rollouts.

Recent Industry Developments

- July 2026: New Culture was granted US Patent No. 12,635,703 covering a mozzarella formulation that includes precision-fermented alpha-S1-casein. The patent strengthens protectable differentiation around melt and stretch performance, supporting partnerships and supply discussions with high-volume pizza and foodservice operators.

- May 2025: Daiya introduced dairy-free cream cheese in 1oz packets targeted at foodservice operators. Portion-controlled formats simplify back-of-house handling and broaden usage occasions, helping plant-based cheese suppliers secure repeat orders in restaurants and catering.

- October 2024: Protein Industries Canada announced a project with partners including Daiya Foods, Ingredion, Ingredion Plant Based Specialties (IPBPS), and Lovingly Made Flour Mills to develop plant-based cheeses and new pulse-based protein ingredients using Canadian pea and fava inputs. The initiative supports localized ingredient supply and formulation improvements that address cost and functional performance constraints in mainstream plant-based cheese formats.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of non-dairy cheese sold for consumption, where the product is made from plant-based inputs and is intended to mimic dairy cheese in taste, texture, and melt performance across retail and food service.

Scope exclusions: We exclude lactose-reduced animal-milk cheeses, cultured animal protein dairy, and plant-based foods that are not positioned and consumed as cheese alternatives.

Segmentation Overview

-

By Source

- Soy

- Almond

- Coconut

- Cashew

- Oat

- Pea Protein

- Other Sources

-

By Form

- Blocks and Slices

- Shreds and Grated

- Spreads and Dips

- Other Forms

-

By Distribution Channel

-

Off-Trade

- Supermarkets/Hypermarkets

- Specialty Stores

- Convenience Stores

- Online Retail

- Other Distribution Channels

- On-Trade

-

Off-Trade

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research builds a clean starting view of dairy alternatives and packaged foods, then narrows it to cheese-style substitutes. We rely on public datasets such as USDA and ERS food availability series, FAOSTAT food and agriculture statistics, UN Comtrade trade flows for relevant HS codes, and EU Eurostat food and retail indicators, plus country statistical offices where the category is separately reported.

We then review how products are described and sold, using sources such as FDA labeling guidance and EU food information rules. We also use trade association publications for plant-based foods and peer-reviewed food science journals that track ingredient and formulation shifts (for example, oils, starches, and protein bases). Company annual reports, investor presentations, and credible press are used to cross-check pricing direction and channel mix changes. Paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export datasets are used to validate the supply-side and trade-side signals behind the model. These sources are illustrative, and many other public references were also reviewed to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary interviews and surveys are used to verify what desk sources cannot fully quantify, especially price ladders by format, retail versus food-service split, and how quickly trial converts to repeat purchase. We engaged a mix of ingredient-side participants, brand and private-label teams, distributors, and retail and food-service buyers across APAC, EMEA, and the Americas. Their inputs were used to tighten assumptions and resolve gaps.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 14% | APAC: 45% |

| Mid tier: 56% | Functional/Unit leaders: 42% | EMEA: 37% |

| Smaller Players: 19% | Managers: 44% | Americas: 18% |

Market-Sizing & Forecasting

Market sizing starts with a top-down build where consumption and spending signals for plant-based dairy are translated into a realistic demand pool for non-dairy cheese by region and channel, then reconciled to observed pricing. When the build is done carefully, the main totals fall into place at the end, because the demand pool, channel split, and price points are constrained by real-world indicators.

To keep the model repeatable, we track a practical set of market inputs. These include retail price ranges and promotion intensity, the mix shift across slices, shreds, blocks, and spreads, food-service menu penetration for cheese-style applications, ingredient base mix changes (such as coconut, soy, and nuts), and country-level plant-based adoption indicators. We then corroborate the results with selective bottom-up approximations such as sampled average selling price times estimated volumes by channel, plus limited supplier and distributor checks. This helps correct any region that looks overstated based on the top-down build.

For forecasting, we use scenario analysis supported by multivariate regression checks, where growth is linked to variables such as plant-based household penetration, real food price inflation, and expansion of distribution in supermarkets and online retail. When bottom-up signals are incomplete for a country or a channel, gaps are handled through conservative range setting, then tightened through follow-up validation focused on pricing and volume direction.

Data Validation & Update Cycle

Validation is completed in several passes so unusual results are surfaced early and corrected before sign-off. Model outputs are compared against independent signals such as trade momentum, retail pricing movement, and region-level plant-based category growth. Any large variance is then traced back to the exact assumption that created it.

A second analyst reviews the calculation chain, and sharp jumps trigger re-contacts with selected interviewees to confirm what changed on the ground, for example a price reset, a new listing win, or a short-term supply constraint. Reports are refreshed annually, and interim updates are made when material events can move demand or pricing. Before delivery, an analyst performs a final pass so clients receive the latest updated view.

Mordor Intelligence's Non Dairy Cheese Market Estimate Compared With Other Published Estimates

Published market sizes for non-dairy cheese often differ because each publisher sets its own rules on what counts as cheese, which channels are included, and which year is treated as the starting point. Currency conversion timing, how price progression is handled, and whether adoption is modeled conservatively or aggressively can also widen the spread.

Some estimates lean more heavily on retail-only channel tracking and a 2025 base year, which can keep the near-term value lower if food-service demand and format-level price mix are not fully reflected. In Mordor Intelligence's 2026 sizing, retail and food-service sales value are both counted, and lactose-reduced dairy cheese and other non-cheese plant-based items are excluded so adjacent categories do not inflate the total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.79 B (2026) | |

| Global Consultancy A | USD 2.15 B (2025) | Uses a 2025 base year and may under-represent food-service sales value and format-driven price mix, which can reduce the stated market value versus a combined channel view. |

| Industry Publisher B | USD 2.12 B (2025) | Often anchors sizing to distribution-channel reporting and a longer 2026 to 2034 forecast window, and differences in channel inclusion and currency timing can shift the starting value. |

The table suggests the main drivers of the spread are base-year selection, channel coverage, and how pricing is normalized across formats. By tying the totals to repeatable indicators such as channel split, price ranges, and adoption signals, the output stays transparent and can be re-created when inputs are refreshed.

Key Questions Answered in the Report

What is the current plant-based cheese market size?

The global plant-based cheese market size is USD 2.79 billion in 2026 and is forecast to reach USD 5.75 billion by 2031.

Which ingredient source holds the largest market share?

Soy maintains the largest market share at 34.72% in 2025, driven by established supply chains and proven functional performance.

Which region holds the largest plant-based cheese market share?

Europe accounts for 42.35% of the market share in 2025, driven by increasing vegan product consumption and supportive regulatory environment.

What factors drive the high CAGR of the plant-based cheese industry?

Core drivers include precision-fermentation innovation, expanding flexitarian diets, rising lactose-intolerance diagnosis, and verified sustainability advantages.

Page last updated on: