Mozzarella Cheese Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

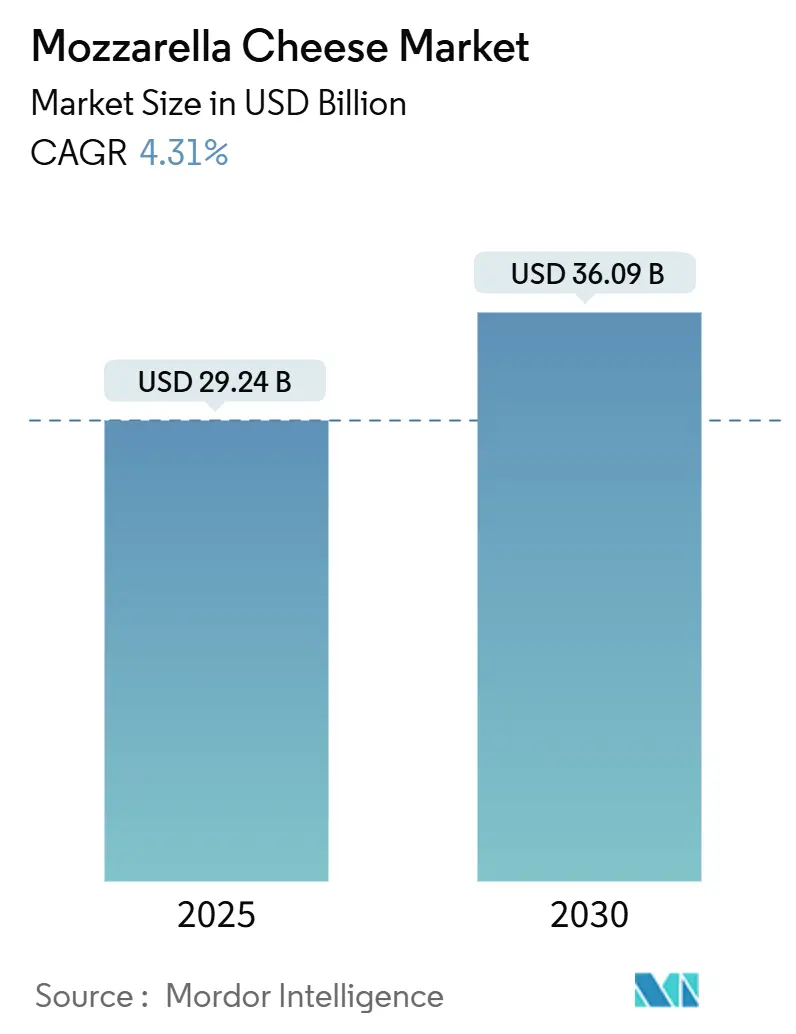

| Market Size (2025) | USD 29.24 Billion |

| Market Size (2030) | USD 36.09 Billion |

| Growth Rate (2025 - 2030) | 4.31% CAGR |

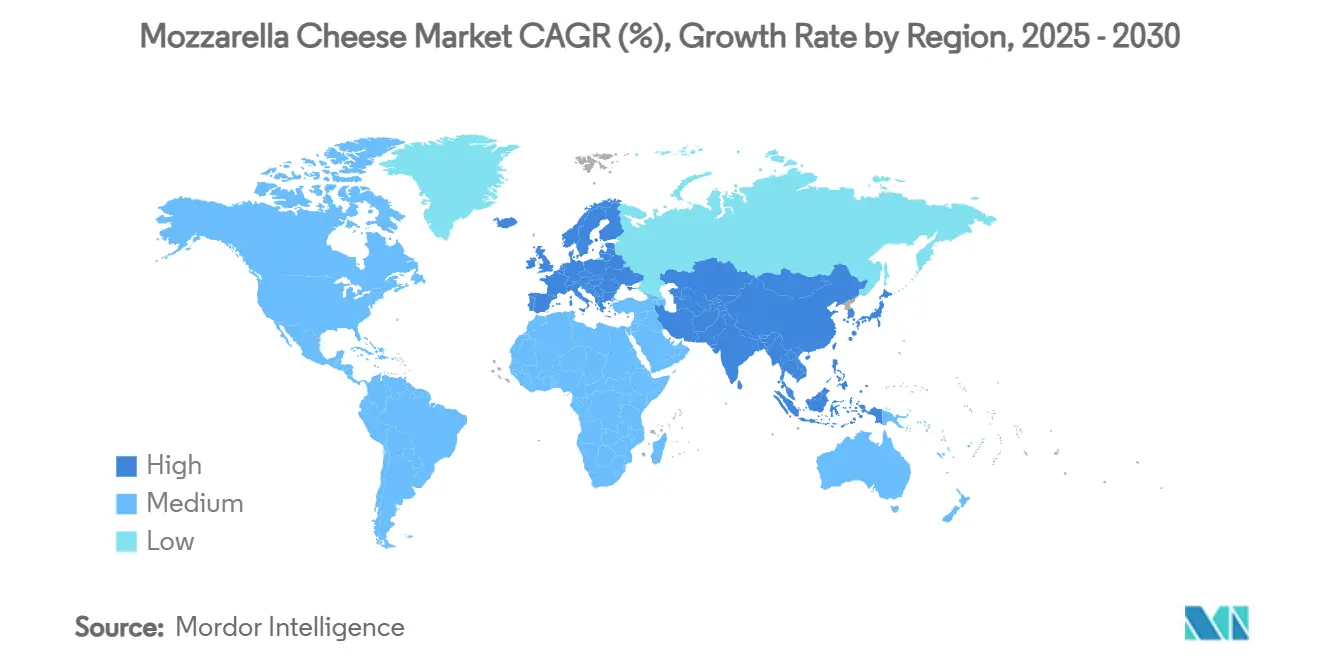

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mozzarella Cheese Market Analysis by Mordor Intelligence

The global mozzarella cheese market size is set to grow steadily, reaching USD 36.09 billion by 2030 from USD 29.24 billion in 2025, at a CAGR of 4.31%. A booming fast-food industry and a worldwide love for Italian cuisine largely fuel this growth trajectory. Central to pizza production, mozzarella dominates cheese usage in both quick-service restaurants and the frozen food sector. Major foodservice chains, such as Domino’s and Pizza Hut, leverage mozzarella’s unique melting properties and stretchability, ensuring product consistency and heightened customer satisfaction. Furthermore, as premium home-cooking experiences gain traction, there's a notable uptick in demand for fresh mozzarella varieties like bocconcini and ovolini. Consumers are increasingly aiming for restaurant-quality meals in their kitchens. Retail sales are witnessing a boost, with brands rolling out convenient, pre-shredded, or diced mozzarella formats, catering to the fast-paced meal prep culture. This trend is especially pronounced in the Asia-Pacific region, where rapid urbanization, rising middle-class incomes, and a surge of Western-style fast-food chains are driving up mozzarella consumption. In India, local pizza brands and fusion cuisines are embracing mozzarella, while Japan and South Korea are seeing a growing appetite for cheese-infused bakery items and ready meals, highlighting a significant shift in regional dairy preferences.

Key Report Takeaways

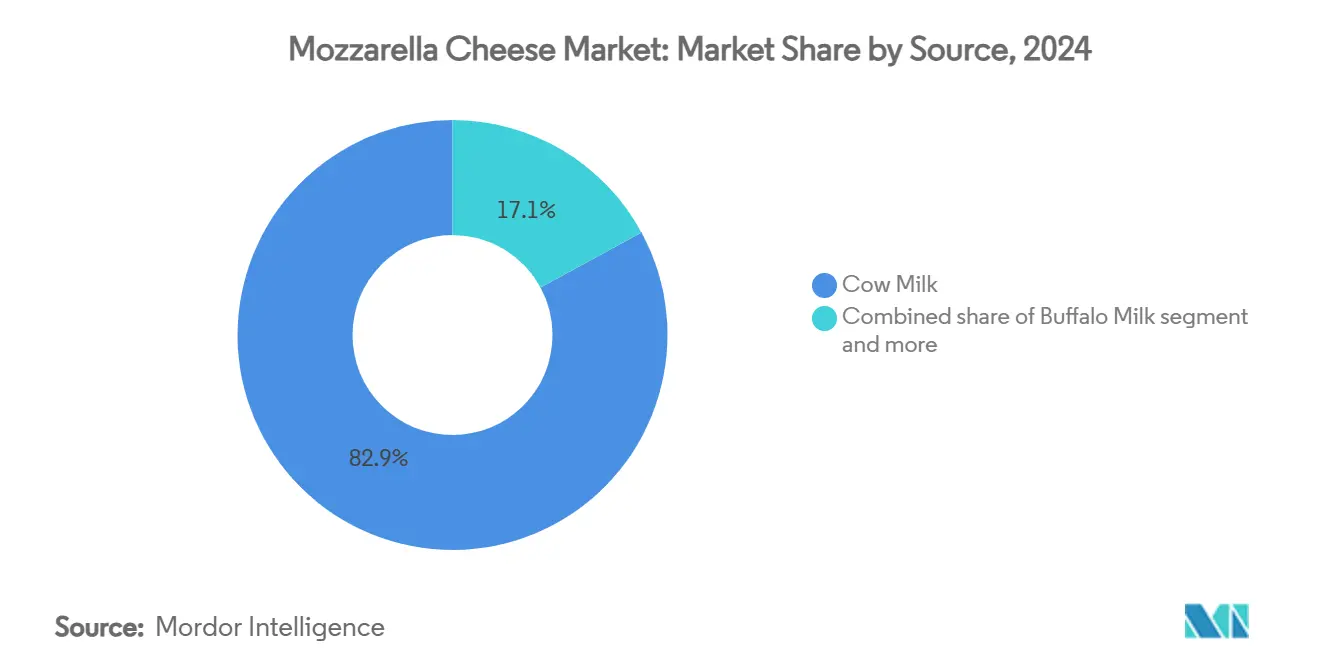

- By source, cow milk retained 82.90% of the mozzarella cheese market share in 2024; buffalo milk is forecast to expand at a 6.50% CAGR to 2030.

- By product type, processed offerings led with 67.43% revenue share in 2024; fresh variants are projected to advance at a 5.40% CAGR.

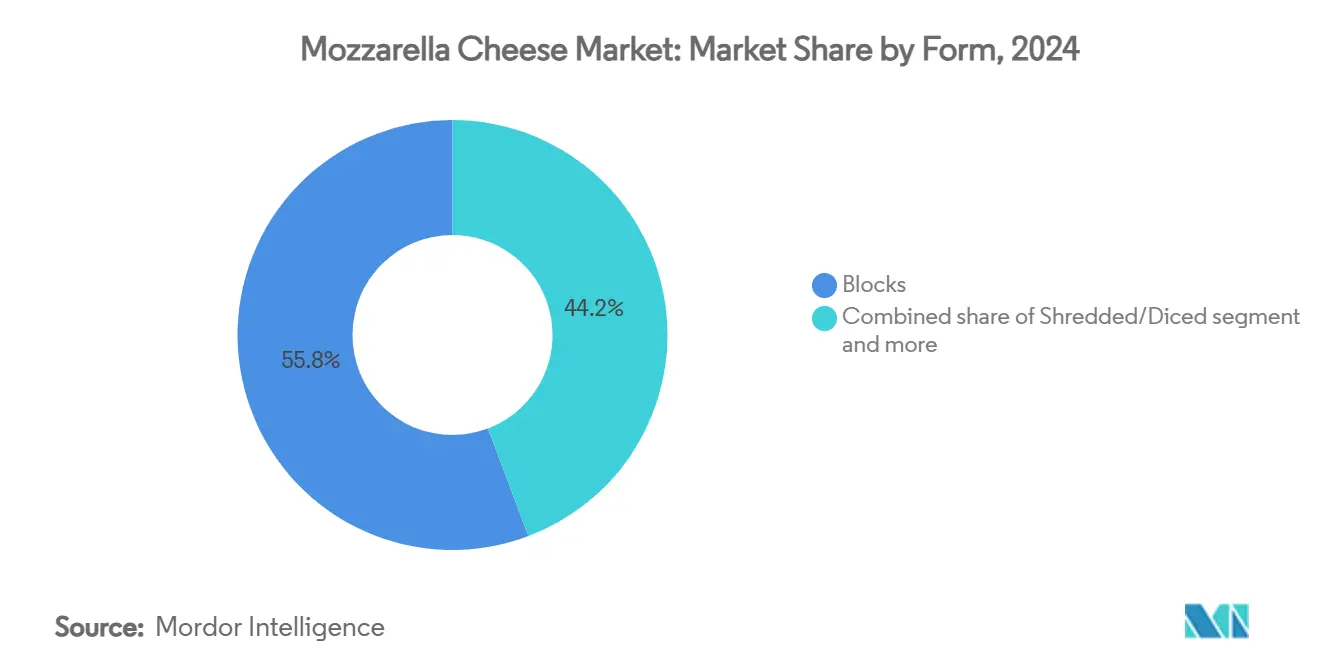

- By form, blocks accounted for 55.76% of the mozzarella cheese market size in 2024, while shredded/diced formats should rise at a 6.90% CAGR through 2030.

- By distribution channel, HoReCa held 64.45% share in 2024; retail sales are expected to climb at a 10.80% CAGR as at-home cooking persists.

- By geography, Europe commanded 48.60% share in 2024; Asia-Pacific is set to register the fastest 6.30% CAGR through 2030.

Global Mozzarella Cheese Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fast food expansion and global pizza affinity | +1.5% | Asia-Pacific, North America, Global | Medium term (2-4 years) |

| Health-oriented demand for low-fat and organic mozzarella | +0.8% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Rise of gourmet and artisanal cheeses | +0.6% | Europe, North America | Medium term (2-4 years) |

| Home-cooking culture post-pandemic | +0.4% | Global | Short term (≤ 2 years) |

| Production and packaging innovation | +0.3% | Developed markets | Long term (≥ 4 years) |

| Expanding omnichannel distribution | +0.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fast Food Expansion and Global Love for Pizza and Italian Cuisine

The global demand for mozzarella cheese is being significantly driven by the ongoing expansion of the quick-service restaurant (QSR) segment. The International Franchise Association’s 2024 Franchising Economic Outlook projects a 2.2% growth in the total number of franchised QSR units, reaching 199,808 in 2024. This marks an addition of 4,301 new outlets compared to 2023 [1]Source: International Franchise Association, “2024 Franchising Economic Outlook,” franchise.org. A major player in this expansion is the aggressive global outreach of pizza chains, especially Pizza Hut. By 2025, Pizza Hut will boast over 19,000 restaurants in more than 100 countries, utilizing both traditional and non-traditional franchise formats. This expansive presence underscores the global affinity for pizza and Italian cuisine, directly elevating the demand for mozzarella, the cheese of choice for most pizzas. Moreover, Pizza Hut’s menu innovations, including region-specific toppings and enhanced cheese blends, further spotlight mozzarella's versatility. Italian chains, notably Papa John’s and Little Caesars, are also ramping up their global footprint. Papa John’s has unveiled plans for over 1,100 new international stores by 2026, while Little Caesars is making significant strides in Asia and Latin America. As these international QSR and Italian chains adapt their menus to local tastes while expanding, the consumption of mozzarella surges, cementing its status as both a fundamental ingredient and a catalyst for innovation.

Health-Conscious Consumer Preferences Driving Low-Fat Mozzarella

Health-conscious consumers are reshaping the mozzarella cheese market, fueling demand for low-fat and nutrient-enriched variants. As consumers prioritize clean labels, balanced nutrition, and functional benefits, brands are innovating products to meet these evolving expectations. For instance, Arla Foods rolled out a light mozzarella, boasting reduced fat and no artificial additives, specifically targeting health-aware families and fitness enthusiasts. In a similar vein, Galbani debuted low-fat mozzarella slices across Europe, catering to calorie-conscious consumers desiring guilt-free indulgence. This trend is especially evident among millennials and Gen Z, who prioritize high-protein, low-sodium snacks and actively pursue healthier alternatives without sacrificing taste. The 2024 IFIC Food & Health Survey underscores these trends: 62% of consumers identified healthfulness as a top purchase driver, and 37% linked “healthy” foods with being protein-rich, mirroring mozzarella's nutritional shift [2]Source: IFIC, “2024 Food & Health Survey,” ific.org. Furthermore, innovations like protein-enriched and low-sodium mozzarella are broadening its appeal, making it a favored ingredient in health-centric snacks, salads, and meal kits. These developments elevate mozzarella from merely a flavor enhancer to a functional, nutrient-rich staple in contemporary diets.

Growth of Gourmet and Artisanal Cheeses with Minimal Processing

Consumers are increasingly favoring authentic, minimally processed cheeses, driving the growth of gourmet and artisanal mozzarella. While water buffalo mozzarella remains a niche, its richer texture and flavor profile are winning over discerning buyers. The Protected Designation of Origin (PDO) status for Mozzarella di Bufala Campana further enhances its allure, guaranteeing consumers its regional authenticity and artisanal quality. This trend is evident in retail, with major supermarkets like Whole Foods, Eataly, and Waitrose expanding their premium offerings. These stores now feature small-batch, fresh mozzarella balls, often highlighted with labels such as “hand-stretched,” “farmstead,” or “locally sourced.” Brands like Lioni Latticini and BelGioioso are capitalizing on this trend, presenting artisanal mozzarella with regional branding and cues of a short shelf-life, appealing to connoisseurs who prioritize freshness and origin. This move dovetails with a broader premiumization trend, where consumers view cheese not merely as a commodity but as a centerpiece of elevated culinary experiences.

Rising Demand for Home Cooking Culture, Boosting Mozzarella Demand

As consumers increasingly replicate restaurant-style meals at home, the demand for mozzarella has surged. Lifestyle changes during the pandemic have solidified home cooking as a lasting preference, fueling interest in high-quality ingredients like mozzarella. In response, retail brands have broadened their offerings, introducing pre-shredded, sliced, and portion-controlled mozzarella formats that prioritize convenience. Major dairy players, including Kraft Heinz and Belgioioso, have rolled out mozzarella packs specifically designed for pizza, pasta, and snacks, streamlining meal prep without sacrificing quality. E-commerce and grocery delivery platforms have democratized access to gourmet mozzarella varieties, previously confined to foodservice. Brands such as Galbani and FreshDirect now provide ready-to-use mozzarella pearls and sliced logs, appealing to those desiring premium cheese for salads, baked dishes, and appetizers. Consequently, mozzarella has transitioned from a mere pizza topping to a versatile household staple, reflecting the evolving preferences of home chefs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plant-based or vegan cheese substitutes | -0.7% | North America, Europe, Global | Medium term (2-4 years) |

| Cheaper processed cheese alternatives | -0.5% | Price-sensitive markets | Short term (≤ 2 years) |

| Fluctuating milk prices impacting production costs | -0.4% | Global | Short term (≤ 2 years) |

| Logistics and supply-chain disruptions | -0.3% | Trade-dependent regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Plant-Based or Vegan Cheese Alternatives

As global consumer demand surges, driven by health concerns, ethical considerations, and lactose intolerance, competition intensifies among plant-based and vegan cheese alternatives. Mozzarella-style vegan cheeses, prized for their adaptability in pizza, pasta, and snacks, have led brands such as Violife and Miyoko’s Creamery to innovate. These brands are crafting coconut oil- and nut-based shreds that boast enhanced melt and stretch properties. Countries with notable vegan populations, India and Mexico (both at 9%), Israel (5%), Canada (4.6%), and Ireland (4.1%) are emerging as pivotal growth markets [3]Source: World Population Review, “Veganism by Country 2025,” worldpopulationreview.com. In 2024, the U.S. plant-based food sector achieved sales of USD 8.1 billion, underscoring a growing retail footprint and evolving dietary trends [4]Source: Good Food Institute, “U.S. Plant-Based Food Retail Sales 2024,” gfi.org. Companies like Perfect Day are leveraging precision fermentation technologies, creating dairy-identical proteins for vegan cheese without any animal inputs. Urban, health-conscious consumers, prioritizing sustainability and clean labels, are increasingly gravitating towards these premium products, thereby siphoning some demand from traditional dairy mozzarella.

Availability of Cheaper Processed Cheese Options

In price-sensitive regions, the mozzarella market grapples with competition from cheaper processed cheese options. In many developing markets, consumers often prioritize cost over quality. As a result, they are turning to processed cheese products that visually resemble mozzarella, even if they don't match its taste or functionality. Brands such as Amul, Britannia, and Kraft are marketing processed cheese slices and blocks at prices that are significantly lower than those of fresh or premium mozzarella. This pricing strategy makes processed cheese more appealing to budget-conscious consumers. Additionally, large retail chains like Walmart, Big Bazaar, and Tesco are amplifying this trend by prominently featuring private-label cheese alternatives. These retailers are championing value-oriented cheese blends that challenge the traditional pricing of mozzarella. Although these alternatives don't possess the signature melt and stretch of authentic mozzarella, consumers using them for budget-friendly applications, like sandwiches, snacks, or home meals, often overlook these differences. This shift not only limits the market's broader penetration but also diminishes the pricing leverage of genuine mozzarella products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Buffalo Milk Drives Premium Positioning

In 2024, cow milk firmly holds its ground in the mozzarella market, commanding a dominant 82.90% share of the global value. This supremacy is largely attributed to cow milk's widespread availability, cost-effective production, and a robust supply infrastructure. Major brands, including Kraft Heinz, Galbani, and BelGioioso, favor cow milk for their large-scale commercial mozzarella production, catering to both retail and foodservice sectors. Cow milk mozzarella's consistent quality and processing ease make it the go-to for mass-market formats like shredded, sliced, and block varieties, reinforcing its global leadership.

On the other hand, while buffalo milk mozzarella occupies a smaller market share, it's the segment on the rise, with projections indicating a robust 6.50% CAGR growth rate through 2030. This surge is fueled by an increasing appetite for premium, authentic Italian-style cheeses, particularly in gourmet retail and upscale foodservice arenas. Offerings such as Mozzarella di Bufala Campana and artisanal products from brands like Lioni Latticini are drawing in consumers with their promise of richer flavors, softer textures, and a touch of heritage. The market's premium segment thrives on this authenticity and quality, making buffalo milk mozzarella a distinguished player in the upscale cheese landscape.

By Product Type: Fresh Mozzarella Gains Momentum

In 2024, processed mozzarella commands a dominant 67.43% market share, thanks to its long shelf life, consistent quality, and versatility in both industrial and foodservice applications. It's the top choice for frozen foods, fast-food outlets, and ready-to-eat meals, with major brands like Saputo, Lactalis, and Amul leading the way in large-scale distribution. Low-moisture mozzarella, a prominent type of processed cheese, is particularly sought after for pizzas. Its superior meltability and low moisture release ensure the crust remains intact in baked dishes.

Conversely, fresh mozzarella is the segment on the rise, projected to grow at a 5.40% CAGR until 2030. This surge is fueled by consumers' increasing desire for restaurant-quality dining at home and a heightened interest in artisanal cooking. Brands like Galbani, Lioni Latticini, and Maplebrook Farm have broadened their retail range, offering fresh mozzarella balls, pearls, and logs, typically found in premium deli or specialty sections. With its creamy texture and clean label allure, fresh mozzarella is a favored ingredient in salads, appetizers, and main dishes. Current innovations are honing in on enhancing shelf stability and portion control, aiming to boost its presence in retail outlets.

By Form: Convenience Drives Shredded Growth

In 2024, blocks dominate the mozzarella packaging landscape, commanding a 55.76% market share. Their versatility makes them a favorite in both foodservice and retail. Offering cost efficiency and flexibility, blocks cater to professional kitchens, bulk cooking needs, and value-driven consumers who appreciate customizable portions. Major players like Saputo, Lactalis, and Mother Dairy supply bulk mozzarella blocks, targeting pizza chains, bakeries, and institutions where manual shredding or slicing is feasible.

On the other hand, shredded and diced mozzarella formats are on a growth trajectory, boasting a projected CAGR of 6.90% through 2030. This surge is driven by a growing appetite for convenience. These ready-to-use formats resonate with busy consumers, especially for pizza, baked dishes, and quick meals. Retail giants like Kraft Heinz, Galbani, and Amul are amplifying their shredded mozzarella lines, frequently utilizing modified atmosphere packaging to enhance shelf life and mitigate clumping. The added processing and packaging elevate this format's value, justifying its premium pricing. Moreover, innovations like single-serve and portion-controlled packs cater to smaller households and health-conscious consumers, emphasizing reduced food waste and consumption control.

By Distribution Channel: Retail Transformation Accelerates

In 2024, HoReCa channels command a dominant 64.45% share of the mozzarella distribution market. This prominence is largely attributed to mozzarella's pivotal role in beloved dishes like pizza and pasta, especially within full-service restaurants, quick-service restaurants (QSRs), and catering services. Renowned for its meltability and subtle flavor, mozzarella has become a kitchen essential. Major players, including Domino’s, Pizza Hut, and Olive Garden, favor bulk formats for enhanced operational efficiency. Leading foodservice suppliers, such as Saputo Foodservice and Leprino Foods, dominate the arena, providing tailored solutions that cater to both volume and performance demands, especially in high-heat cooking scenarios.

On the other hand, retail channels are emerging as the fastest-growing segment, with projections indicating a robust 10.80% CAGR expansion through 2030. This surge is fueled by a growing trend of consumers crafting restaurant-quality dishes in their kitchens. At the same time, supermarkets and hypermarkets spearhead distribution, online platforms like BigBasket, FreshDirect, and Amazon Fresh are carving out a significant niche. Their rise can be attributed to advancements in cold chain logistics and a heightened demand for premium dairy offerings. Brands such as Galbani, Amul, and BelGioioso are tapping into this trend, rolling out convenient formats like shredded packs and mozzarella pearls.

Geography Analysis

In 2024, Europe commands a dominant 48.60% share of the global mozzarella market, a testament to its rich cheese-making heritage, robust regulatory frameworks, and streamlined supply chains. Italy, with its artisanal prowess and products like Mozzarella di Bufala Campana enjoying Protected Designation of Origin (PDO) status, stands as the undisputed leader. Germany, with its strong export game, secures the second spot. Meanwhile, France, Spain, and the United Kingdom bolster regional demand, offering both mass-market and premium mozzarella. Prominent brands like Galbani, Zanetti, and Arla Foods further cement Europe's supremacy in retail and foodservice.

Asia-Pacific emerges as the fastest-growing region, eyeing a 6.30% CAGR through 2030. This surge is attributed to urbanization, Western dietary trends, and the proliferation of quick-service restaurants. In China, cheese consumption is set to rise at a 9.1% CAGR, with mozzarella taking center stage in pizzas and baked goods. South Korea showcases its Western culinary embrace, with mozzarella imports surpassing its total cheese intake. Meanwhile, Japan leans towards premium retail, India drives volume-led growth, and Australia and New Zealand focus on exports, all contributing to a broader regional demand.

North America, anchored by giants like Leprino Foods and Saputo, maintains a steady mozzarella share, bolstered by entrenched consumption habits and substantial production. South America, with Brazil and Argentina at the helm, charts a steady expansion.In the Middle East and Africa, nations like Saudi Arabia, United Arab Emirates, and South Africa are swiftly integrating mozzarella into their diets, thanks to a growing affinity for Western cuisine, both in dining and retail settings.

Competitive Landscape

The mozzarella cheese market is fragmented. The mozzarella cheese market sees a blend of global dairy giants and niche regional producers vying for dominance in both volume and premium segments. Leading the charge is Leprino Foods Company, the world's top mozzarella manufacturer. With expansive facilities both in the U.S. and internationally, Leprino caters to major quick-service restaurants (QSRs) and food processors. Other notable players like Lactalis Group, Saputo Inc., and Arla Foods harness vast distribution networks and diverse dairy portfolios to stay globally relevant. On the other hand, regional names like BelGioioso Cheese and Grande Cheese carve out a niche by emphasizing premium offerings and forging strong foodservice collaborations, presenting a high-quality, traditionally crafted mozzarella.

Both production scaling and tech investments fuel growth in the sector. Grande Cheese's USD 60 million plant expansion in Wisconsin, alongside Lactalis's USD 75 million U.S. facility investment, highlight a collective industry drive to boost output, refine operations, and create jobs. These initiatives echo the surging demand for both industrial-grade and artisanal mozzarella. Companies are also diving into mergers and acquisitions, alongside innovative strategies, to tap into burgeoning demand, especially in rapidly expanding regions and specialized formats.

The merging realms of traditional dairy and biotechnology hint at a seismic shift in the competitive arena, with sustainability, functionality, and innovative processes taking center stage. While established players delve into next-gen protein technologies, others, like Fonterra with its “Naked Mozz” initiative, focus on streamlining processes, having done away with superfluous cardboard packaging.

Mozzarella Cheese Industry Leaders

Leprino Foods Company

Lactalis Group

Saputo Inc.

Arla Foods amba

Fonterra Co-operative Group Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Lactalis Group allocated USD 75 million to expand New York mozzarella lines, safeguarding 800 jobs while adding 50 positions.

- June 2025: Kirtland Capital Partners acquired Galati Cheese Company to scale premium mozzarella production in Ontario.

- May 2025: Sabelli acquired Stella Bianca to deepen its Italian mozzarella capabilities.

- August 2024: Grande Cheese started a USD 60 million Wisconsin plant expansion, enlarging capacity for mozzarella shreds.

Global Mozzarella Cheese Market Report Scope

| Cow Milk |

| Buffalo Milk |

| Goat Milk |

| Sheep Milk |

| Fresh Mozzarella |

| Processed Mozzarella |

| Blocks |

| Shredded/Diced |

| Slices |

| HoReCA | Full Service-Restuarents |

| Quick Service Restaurants | |

| Cafes and Bars | |

| Retail | Supermarket/Hypermarket |

| Convience/Grocery Stores | |

| Online Retail Stores | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Source | Cow Milk | |

| Buffalo Milk | ||

| Goat Milk | ||

| Sheep Milk | ||

| By Product Type | Fresh Mozzarella | |

| Processed Mozzarella | ||

| By Form | Blocks | |

| Shredded/Diced | ||

| Slices | ||

| By Distribution Channel | HoReCA | Full Service-Restuarents |

| Quick Service Restaurants | ||

| Cafes and Bars | ||

| Retail | Supermarket/Hypermarket | |

| Convience/Grocery Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the mozzarella cheese market?

The mozzarella cheese market size is USD 29.24 billion in 2025 and is forecast to reach USD 36.09 billion by 2030 at a 4.31% CAGR.

Which milk source is growing the fastest?

Buffalo milk mozzarella, prized for rich butterfat and PDO authenticity, is expanding at a 6.50% CAGR through 2030.

Why are shredded formats gaining popularity?

Shredded and diced mozzarella post a 6.90% CAGR because time-pressed consumers and foodservice kitchens value ready-to-use convenience and consistent portioning.

Which region is the primary growth engine?

Asia-Pacific leads with a 6.30% CAGR, driven by rapid urbanization, rising disposable incomes, and pizza’s mainstream acceptance in China, South Korea, and India.

Page last updated on: