Middle East Dairy Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

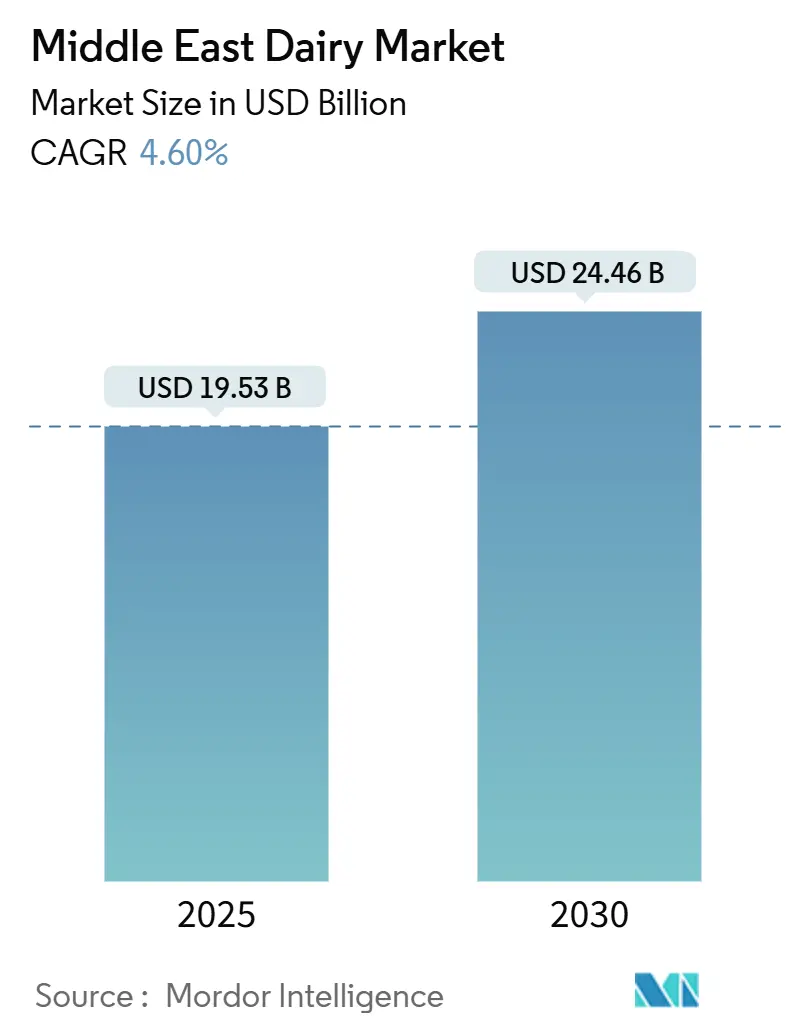

| Market Size (2025) | USD 19.53 Billion |

| Market Size (2030) | USD 24.46 Billion |

| Growth Rate (2025 - 2030) | 4.60% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East Dairy Market Analysis by Mordor Intelligence

The Middle East dairy market size stands at USD 19.53 billion in 2025 and is forecast to reach USD 24.46 billion by 2030, reflecting a 4.60% CAGR. This growth is driven by the region's youthful population, increasing demand for functional dairy products, and improvements in cold-chain logistics. While milk remains the largest contributor in terms of value, yogurt is gaining traction due to probiotic innovations and convenient formats. The expansion of modern retail channels is complemented by a recovery in tourism hubs, which is boosting premium dairy consumption. Governments in the region, particularly in Saudi Arabia and the United Arab Emirates, are actively promoting healthier diets. Through public campaigns, subsidies, and incentives, they are encouraging manufacturers to produce fortified and functional dairy products, resulting in increased market consumption and greater consumer awareness. Saudi Arabia leads the market with its focus on scale and food-security investments, while the United Arab Emirates leverages its emphasis on organic products and its position as a trade hub. The shift from traditional sales channels to modern retail formats—such as supermarkets, hypermarkets, and online platforms—enhances consumer accessibility and convenience. Although challenges like water scarcity and rising feed costs affect production, government nutrition programs are creating stable institutional demand and supporting the growth of domestic processing capabilities.

Key Report Takeaways

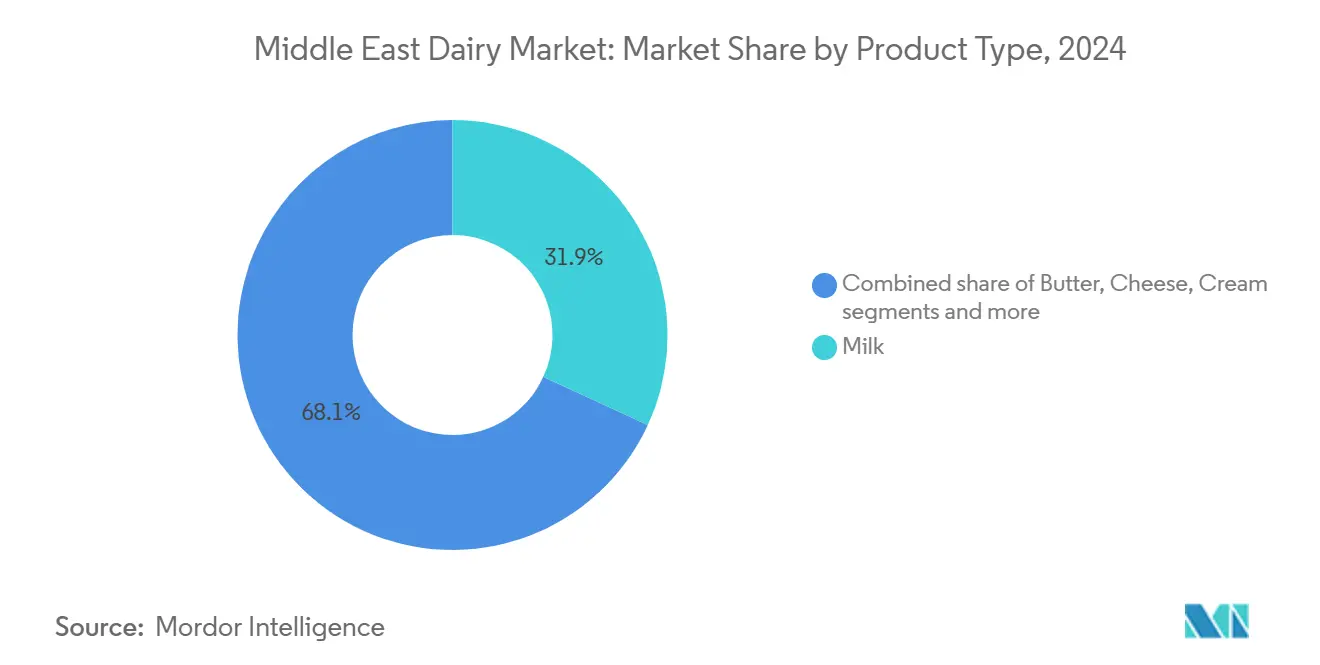

- By product type, milk commanded 31.87% share of the Middle East dairy market size in 2024, while yogurt is advancing at a 4.97% CAGR through 2030.

- By distribution channel, off-trade accounted for 66.23% of the Middle East dairy market size in 2024, and on-trade is registering the highest projected CAGR at 4.86% through 2030.

- By geography, Saudi Arabia held 32.56% of the Middle East dairy market share in 2024, while the United Arab Emirates segment is projected to expand at a 5.24% CAGR to 2030.

Middle East Dairy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for functional/fortified dairy (probiotics, lactose-free) | +0.8% | United Arab Emirates, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Rising consumer interest in convenience and ready-to-eat dairy products | +0.7% | Global, strongest in United Arab Emirates and Saudi Arabia | Short term (≤ 2 years) |

| Rapid growth of modern grocery retail and cold-chain logistics | +0.9% | Saudi Arabia, United Arab Emirates, Qatar | Long term (≥ 4 years) |

| Expansion of school milk and nutrition programmes | +0.6% | Regional, with early gains in Iraq, Yemen | Medium term (2-4 years) |

| Government-led health and wellness campaigns | +0.5% | Saudi Arabia, United Arab Emirates, Bahrain | Medium term (2-4 years) |

| Diversification of flavor, format, and health benefit claims | +0.4% | Saudi Arabia, United Arab Emirates, Qatar | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for functional / fortified dairy (probiotics, lactose-free)

In Gulf markets, increasing health consciousness among consumers is driving the demand for probiotic and lactose-free dairy products. Regulatory frameworks are progressively validating health-related claims, further promoting the adoption of functional dairy. For instance, the United Arab Emirates is set to launch Meliha organic laban in February 2025, targeting health-conscious consumers who prioritize the nutritional and digestive benefits of traditional fermented milk, now offered in convenient, modern packaging. Similarly, Saudi Arabia's local production of Actimel probiotic products highlights the cost efficiencies achieved through large-scale functional dairy manufacturing. Additionally, camel milk is gaining traction as a premium alternative, supported by industrial-scale operations catering to niche consumer preferences. Halal certification requirements, while posing entry barriers for some players, also safeguard domestic producers from non-compliant imports. This regulatory framework underscores the growing recognition that demand for functional dairy products is surpassing the certified supply capacity. Consequently, this supply-demand gap presents a significant opportunity for regional producers to differentiate themselves through quality and compliance, enabling them to capture a larger market share.

Rapid growth of modern grocery retail and cold-chain logistics

Infrastructure investments in temperature-controlled distribution networks are unlocking access to previously untapped market segments, particularly in secondary cities where traditional retail is prevalent. The United Arab Emirates cold-chain market has experienced significant growth, with Dubai and Abu Dhabi accounting for two-thirds of the region's facilities. At the same time, Saudi Arabia is leading the cold-chain expansion across the broader MENA region. The completion of Etihad Rail is transforming the transportation of temperature-sensitive goods across the United Arab Emirates. This development not only reduces logistics costs but also enables smaller producers to reach wider distribution networks without requiring substantial investments in cold storage. Al Dahra's 300,000 metric ton storage facility in Fujairah, along with its partnership with Etihad Rail, highlights how optimizing the feed supply chain enhances the dairy sector's resilience by reducing input volatility. The expansion of modern retail is driving demand for premium packaging formats. Tetra Pak's USD 11.5 million investment in the Mleiha facility in Sharjah reflects the confidence of technology providers in the adoption of sustainable packaging across the region's dairy operations.

Expansion of school milk and nutrition programmes

Government nutrition initiatives establish predictable demand channels through institutional procurement. This strategy not only avoids retail margin pressures but also enhances local production capacity. Government procurement specifications frequently prioritize local suppliers with recognized quality certifications. This approach provides domestic producers with a competitive advantage while reducing reliance on imports. In the United Arab Emirates, strategic food commodity stockpile legislation requires the Ministry of Economy to monitor dairy consumption trends and supplier obligations, highlighting the government's active role in maintaining market stability and supply security. In Saudi Arabia, the Ministry of Education has emphasized the impact of its nationwide school nutrition initiative. Serving 5.2 million students across 35,000 schools, this program has created a steady institutional demand, valued at approximately USD 400 million in 2024[1]Source: Ministry of Education in Saudi Arabia, "Data and Statistics", moe.gov.sa. Designed to combat childhood malnutrition, the initiative mandates the daily provision of milk to students. Additionally, it supports local dairy producers through preferential procurement policies, ensuring domestic suppliers benefit. The program has also expanded to include fortified milk variants enriched with nutrients such as calcium, vitamin D, and iron. These fortified options address specific nutritional deficiencies identified in national health surveys, aiming to improve students' overall health outcomes.

Government-led health and wellness campaigns

Public health campaigns are influencing consumer preferences toward dairy products with verified nutritional benefits, creating opportunities for producers with strong health-focused positioning. Saudi Arabia's "Healthy Habits" campaign addresses poor dietary habits through education, while the UAE's "Food for Life" initiative, supported by the National Nutrition Strategy 2030 framework, promotes healthier diets from sustainable food systems. In 2024, the federal government allocated AED 5 billion to healthcare, as reported by the United States-United Arab Emirates Business Council[2]Source: The U.S.-U.A.E. Business Council, "U.A.E. Healthcare & Life Sciences Sector", usuaebusiness.org. Abu Dhabi's Nutri-Mark labeling scheme introduces an A-E grading system for packaged foods, including dairy products, fostering transparency that rewards higher-quality formulations with better shelf positioning and consumer recognition. The United Arab Emirates National Survey for Health and Nutrition 2024 provides a foundation for evidence-based interventions targeting vitamin D deficiency and anemia, conditions where fortified dairy products offer practical solutions. These public health campaigns are driving measurable shifts in demand toward products with substantiated health claims, benefiting producers who focus on nutritional enhancements and regulatory compliance rather than commodity positioning. Messaging around obesity and non-communicable diseases encourages the adoption of reduced sugar, lower-fat, and functional dairy options. Producers are responding with low-fat milks, reduced-sugar yogurts, and fortified beverages designed to align with dietary guidelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water scarcity and high feed-import costs | -1.2% | Saudi Arabia, United Arab Emirates, regional spillover | Long term (≥ 4 years) |

| Growing preference for plant-based alternatives | -0.3% | United Arab Emirates, Qatar, urban centers | Medium term (2-4 years) |

| Retail listing fees and price-promotion race squeezing producer margins | -0.5% | Regional, concentrated in modern retail | Short term (≤ 2 years) |

| Rising geopolitical freight risk on imported dairy inputs | -0.4% | Regional, affecting import-dependent markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Water scarcity and high feed-import costs

The region's arid climate and limited renewable water resources significantly increase production costs, posing challenges to the scalability of dairy production. Producing one liter of milk in the country requires approximately 1,000 liters of water, surpassing the global average of 700 liters. This higher water consumption is primarily attributed to the cooling requirements driven by the region's extreme temperatures. To address these issues, leading dairy producers are implementing advanced water recycling technologies and precision irrigation systems. For example, Almarai, a key market player, has established advanced treatment facilities, achieving a 56% water recycling rate. Furthermore, the Saudi government is actively conserving water resources by discontinuing wheat production and redirecting agricultural support toward cultivating more water-efficient crops. These initiatives aim to enhance productivity and reduce emissions, demonstrating a regional focus on balancing operational efficiency with resource constraints.

Growing preference for plant-based alternatives

In the Middle East, cultural preferences for traditional dairy products have slowed the growth of alternative protein adoption. However, urban consumers are increasingly exploring plant-based options due to health and sustainability concerns. As of 2024, 10% of Saudi Arabia's population identifies as vegetarian or vegan, according to Farmlandgrab[3]Source: Farmlandgrab, "Down on the farm", farmlandgrab.org. The limited production of plant-based alternatives locally has created a reliance on imports, which reduces competitive pressure on domestic dairy producers. Additionally, halal certification requirements for plant-based products add challenges for international brands entering the market. While regional food system assessments highlight sustainability and resilience, factors that could support plant-based options in resource-constrained settings, current consumption patterns still favor dairy. Initiatives such as Sharjah's Mleiha farm in the United Arab Emirates reflect a defensive strategy, addressing sustainability concerns while maintaining the dairy sector's dominance. Despite the availability of alternative proteins, government nutrition campaigns promote balanced diets rather than plant-based substitutions, indicating a policy environment that continues to support dairy consumption growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Milk Dominance Faces Yogurt Innovation

Milk retains a dominant 31.87% market share in 2024, driven by institutional demand and household consumption. Fresh milk benefits from school nutrition programs and government procurement that prioritize local suppliers, with the United Arab Emirates's Mleiha organic milk distinguishing itself through A2A2 protein content and a premium 4% fat level. UHT milk's extended shelf life and wider distribution are crucial, particularly for camel milk products targeting international markets. Camelicious, for instance, has achieved EU export approval and Malaysian halal certification, enabling global expansion. Condensed and powdered milk address food service needs and emergency stockpiling, while flavored milk varieties, including chocolate, date, and strawberry options, appeal to younger consumers.

Yogurt, driven by probiotic advancements and convenient packaging, stands out as the fastest-growing segment, with a 4.97% CAGR projected through 2030. This growth reflects increasing health awareness, with drinkable yogurts competing with traditional spoonable options for on-the-go consumption. In the cheese segment, natural varieties such as cheddar and parmesan cater to food services, while processed cheeses focus on retail convenience. Dairy desserts, particularly ice cream, benefit from the recovery of tourism and the expansion of the hospitality sector. Cream products, including fresh, cooking, and whipping varieties, support growth in the food service sector. Sour milk drinks retain cultural importance, though their growth trails behind innovative yogurt formulations with functional benefits. The butter segment, despite competition from imports, sustains its market presence through local production advantages and halal certification compliance.

By Distribution Channel: Off-Trade Leadership Meets On-Trade Recovery

Modern retail channels, such as supermarkets, hypermarkets, and convenience stores, hold a 66.23% market share in 2024. These channels provide temperature-controlled storage and a diverse range of products. Supermarkets and hypermarkets are expanding, supported by investments in cold-chain infrastructure and growing consumer preference for one-stop shopping. For instance, Union Coop has introduced Sharjah's organic dairy products across its Dubai branches. Online retail is also gaining traction, driven by last-mile delivery capabilities and subscription models. However, the need for temperature control in certain products has limited its growth compared to ambient grocery categories. Specialist retailers focus on premium and organic products, while convenience stores cater to impulse purchases and immediate consumption needs.

On-trade segments are experiencing a strong 4.86% CAGR growth, driven by the recovery of the hospitality sector and the expansion of tourism, which are boosting premium consumption. This growth highlights the revival of the hospitality industry and the broader development of food services. Mazoon Dairy's participation in HORECA 2024 demonstrates the industry's emphasis on hotels, restaurants, and café channels. The food service sector prioritizes consistent quality, competitive pricing, and reliable supply chains, favoring established producers with scale advantages. The growth of tourism in the United Arab Emirates and Saudi Arabia is increasing demand for premium dairy products in hospitality settings. Additionally, the expanding café culture is driving the need for high-quality milk and cream in specialty coffee. Emerging distribution channels, such as warehouse clubs and gas stations, combine convenience with bulk purchasing options. However, their market penetration remains lower compared to traditional retail formats.

Geography Analysis

Saudi Arabia holds a 32.56% market share in 2024, driven by its strong domestic production and strategic emphasis on food security. The kingdom has attained self-sufficiency in dairy and is actively diversifying into poultry, seafood, and red meat, supported by Almarai's extensive USD 4.8 billion investment program. However, water scarcity is prompting structural changes. The National Water Strategy 2030 limits fodder cultivation, increasing reliance on imported feed. This shift raises costs, making integrated operations and supply chain efficiency more advantageous. The government supports feed importers while promoting sustainability. The Ministry of Environment, Water, and Agriculture is encouraging livestock farmers to adopt compound feed through extension services.

The United Arab Emirates is experiencing rapid growth, with a 5.24% CAGR projected through 2030. Leveraging its position as a trade hub and innovation leader, the United Arab Emirates is targeting premium market segments through organic dairy initiatives and camel milk industrialization. For example, Sharjah's Mleiha organic dairy farm has invested USD 11.5 million in technology, establishing the United Arab Emirates's first integrated organic production capabilities. It's A2A2 protein milk, with 4% fat content, is positioned as a premium product in Dubai's retail market. Additionally, the Emirates Industry for Camel Milk Products operates the world's first advanced camel milking facility with EU export approval. The company aims to expand its Camelicious brand to 30 global markets by 2030. The United Arab Emirates's food commodity legislation reflects systematic government support, requiring monitoring of dairy consumption and supplier obligations to ensure market stability and supply security. Furthermore, with two-thirds of the region's cold-chain infrastructure located in Dubai and Abu Dhabi, temperature-sensitive products can be distributed across wider geographic areas.

Qatar, Bahrain, Oman, Kuwait, and Iran, while holding smaller market shares, remain strategically significant due to their specialized production capabilities and regional trade connections. Qatar's Baladna has rapidly achieved self-sufficiency, supported by USD 3.5 billion in Algerian investments and USD 250 million in Syrian operations. Oman's Mazoon Dairy leverages local production advantages to reduce transportation times and improve product freshness. The company is also targeting growth in the hospitality sector by participating in HORECA 2024. In Iran, government policies and subsidy frameworks influence dairy consumption patterns and shape import substitution strategies.

Competitive Landscape

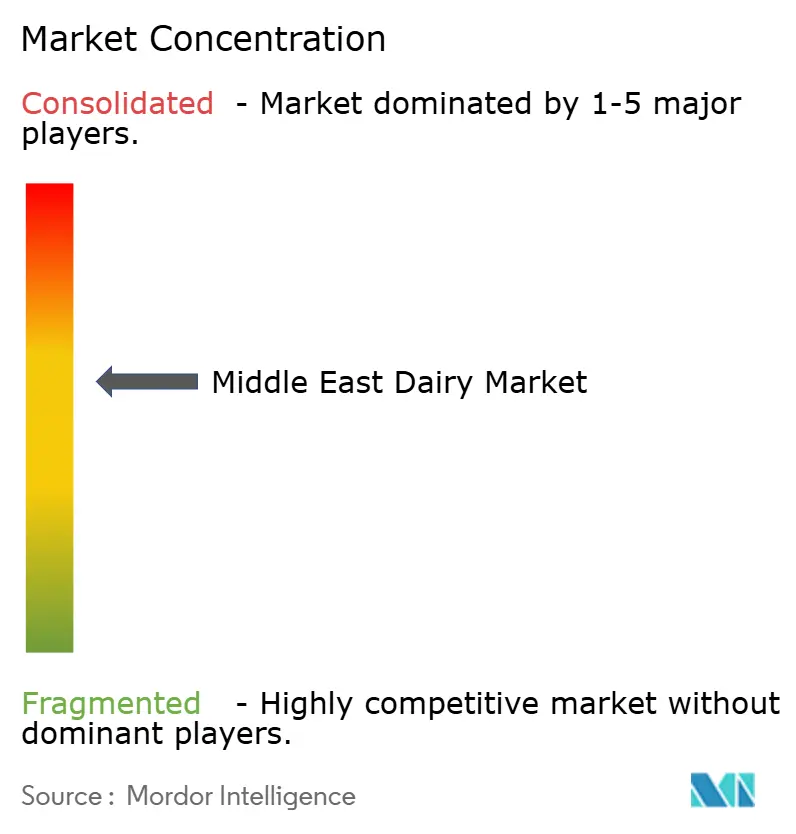

The Middle East dairy market exhibits moderate concentration, with established players employing vertical integration strategies. Simultaneously, emerging organic and specialty producers are challenging traditional competitors by emphasizing sustainability and premium product differentiation. Almarai leverages its scale and diversification to maintain its competitive position. Technology adoption is advancing through collaborations with equipment suppliers. For example, Tetra Pak invested USD 11.5 million in the Mleiha facility in Sharjah to improve sustainable packaging and processing automation. Growth opportunities are evident in functional dairy products, organic production, and camel milk industrialization, where regulatory approvals and specialized infrastructure offer advantages to early entrants.

Key players in the market include Almarai Company, Arla Foods AmbA, Danone SA, Saudia Dairy and Foodstuff Company (SADAFCO), and The National Agricultural Development Company (NADEC). The Saudi Arabian dairy market comprises a mix of domestic and international companies employing various strategies. Companies are focusing on product innovation, emphasizing clean-label products, organic options, and functional dairy offerings to meet shifting consumer preferences. Digital transformation is driving operational improvements. Additionally, firms are expanding production capacities by constructing new facilities, upgrading existing ones, and strengthening distribution networks to improve market penetration and product availability.

Emerging disruptors are leveraging sustainability and direct-to-consumer strategies to capture premium market segments. For example, Mleiha organic dairy, supported by the Sharjah government, has achieved a first in the United Arab Emirates by integrating farm-to-retail operations, bypassing traditional distribution channels. Halal certification requirements from organizations like Dar El Fatwa create barriers to entry, granting market access to compliant regional producers while limiting international competition. This is illustrated by UTRIX, which obtained certification in December 2024, enabling its Lebanese feed additives to enter the Middle Eastern market. Competitive dynamics increasingly favor producers with strong ESG compliance. Almarai exemplifies this with its comprehensive sustainability policies, which address animal welfare, environmental stewardship, and ethical sourcing, aligning with international standards and the government's Vision 2030 objectives. Supply chain resilience is becoming a critical differentiator, as geopolitical freight risks and water scarcity reward integrated operations with diverse sourcing and operational flexibility.

Middle East Dairy Industry Leaders

-

Almarai Company

-

Arla Foods Amba

-

Danone SA

-

Saudia Dairy and Foodstuff Company (SADAFCO)

-

The National Agricultural Development Company (NADEC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Sawani, backed by the Public Investment Fund and owner of the NOUG brand, collaborated with GEA, a German specialist in modern milking systems, to establish its model farm. This cutting-edge facility produces 500,000 liters of camel milk monthly.

- January 2025: Almarai, the largest dairy producer in Saudi Arabia, is poised for substantial growth, unveiled a USD 4.8 billion investment as part of its new five-year strategic blueprint. This move underscores Almarai's dedication to bolstering Saudi Arabia's Vision 2030 ambition: attaining food self-sufficiency and curbing the nation's import dependencies.

- November 2024: Savola Group has announced the distribution of a 34.52% stake in Almarai to its shareholders, a transaction valued at SAR 12.8 billion, signifying a major ownership restructuring in the Kingdom's largest dairy company.

Middle East Dairy Market Report Scope

| Butter | ||

| Cheese | Natural Cheese | Cheddar |

| Cottage | ||

| Ricotta | ||

| Parmesan | ||

| Others | ||

| Processed Cheese | ||

| Cream | Fresh Cream | |

| Cooking Cream | ||

| Whippng Cream | ||

| Others | ||

| Dairy Desserts | Ice Cream | |

| Cheesecakes | ||

| Frozen Desserts | ||

| Others | ||

| Milk | Condensed milk | |

| Flavored Milk | ||

| Fresh Milk | ||

| UHT Milk (Ultra-high temperature milk) | ||

| Powdered Milk | ||

| Yogurt | Drinkable | |

| Spoonable | ||

| Sour Milk Drinks | ||

| On-trade | |

| Off-trade | Convenience Stores |

| Specialist Retailers | |

| Supermarkets and Hypermarkets | |

| On-line Retail | |

| Others |

| United Arab Emirates |

| Qatar |

| Saudi Arabia |

| Bahrain |

| Oman |

| Kuwait |

| Iran |

| Rest of the Middle East |

| By Product Type | Butter | ||

| Cheese | Natural Cheese | Cheddar | |

| Cottage | |||

| Ricotta | |||

| Parmesan | |||

| Others | |||

| Processed Cheese | |||

| Cream | Fresh Cream | ||

| Cooking Cream | |||

| Whippng Cream | |||

| Others | |||

| Dairy Desserts | Ice Cream | ||

| Cheesecakes | |||

| Frozen Desserts | |||

| Others | |||

| Milk | Condensed milk | ||

| Flavored Milk | |||

| Fresh Milk | |||

| UHT Milk (Ultra-high temperature milk) | |||

| Powdered Milk | |||

| Yogurt | Drinkable | ||

| Spoonable | |||

| Sour Milk Drinks | |||

| By Distribution Channel | On-trade | ||

| Off-trade | Convenience Stores | ||

| Specialist Retailers | |||

| Supermarkets and Hypermarkets | |||

| On-line Retail | |||

| Others | |||

| By Country | United Arab Emirates | ||

| Qatar | |||

| Saudi Arabia | |||

| Bahrain | |||

| Oman | |||

| Kuwait | |||

| Iran | |||

| Rest of the Middle East | |||

Key Questions Answered in the Report

How large is the Middle East dairy market in 2025?

It is valued at USD 19.53 billion and is projected to reach USD 24.46 billion by 2030 at a 4.60% CAGR.

Which country leads regional dairy revenue?

Saudi Arabia holds 32.56% share, benefiting from large-scale integrated farms and Vision 2030 food-security investments.

Which product category grows the fastest?

Yogurt registers a 4.97% CAGR owing to probiotic formulas and on-the-go drinkable packs.

Which distribution channel grows the fastest?

On-trade segments are experiencing a strong 4.86% CAGR growth.

Page last updated on: