Cheese Analogue Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

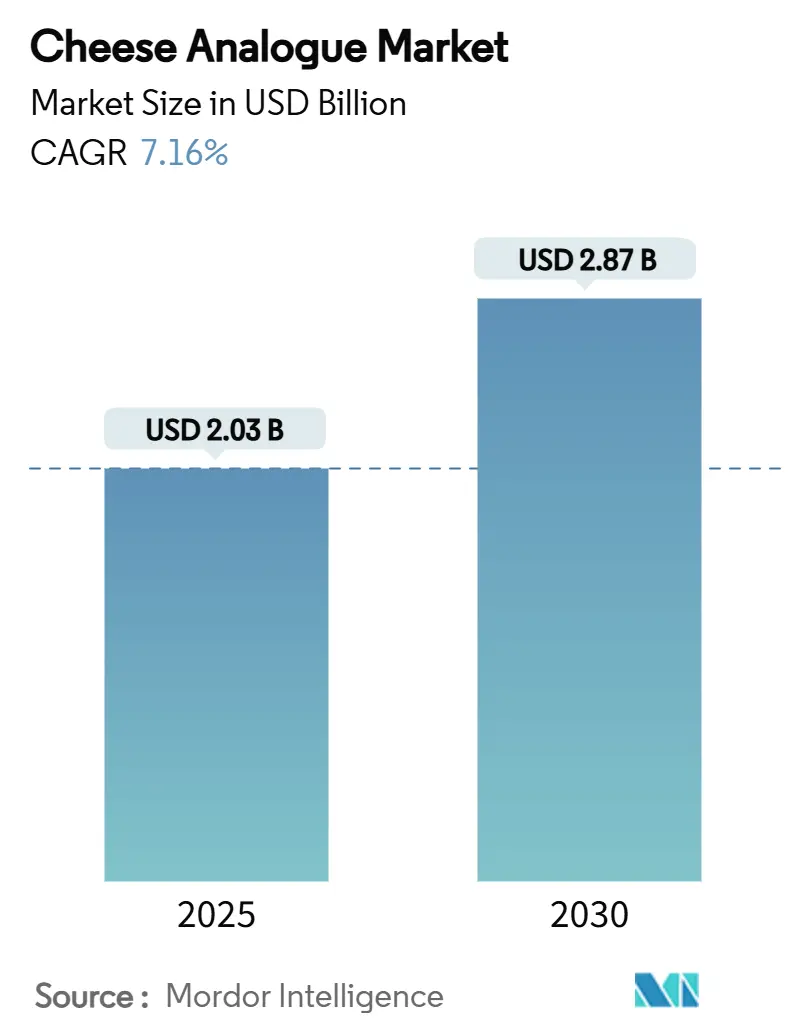

| Market Size (2025) | USD 2.03 Billion |

| Market Size (2030) | USD 2.87 Billion |

| Growth Rate (2025 - 2030) | 7.16% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cheese Analogue Market Analysis by Mordor Intelligence

The cheese analogue market size, valued at USD 2.03 billion in 2025, is expected to grow to USD 2.87 billion by 2030, registering a CAGR of 7.16%. This growth is driven by increasing health awareness, advancements in precision fermentation, and the implementation of clearer labeling regulations, which are attracting both consumers and investors. The rising popularity of flexitarian diets is fueling demand, while innovations in nut-based and coconut-based formulations are diversifying product offerings. Investments in fermentation technologies are significantly reducing production costs, and retailers are allocating more shelf space for chilled cheese analogue products. Additionally, collaborations between established food companies and biotech startups are addressing challenges like achieving authentic meltability, which has been a key barrier to mainstream adoption. In the United States, venture capital funding and improved regulatory clarity are accelerating product launches, setting new global benchmarks for the cheese analogue market.

Key Report Takeaways

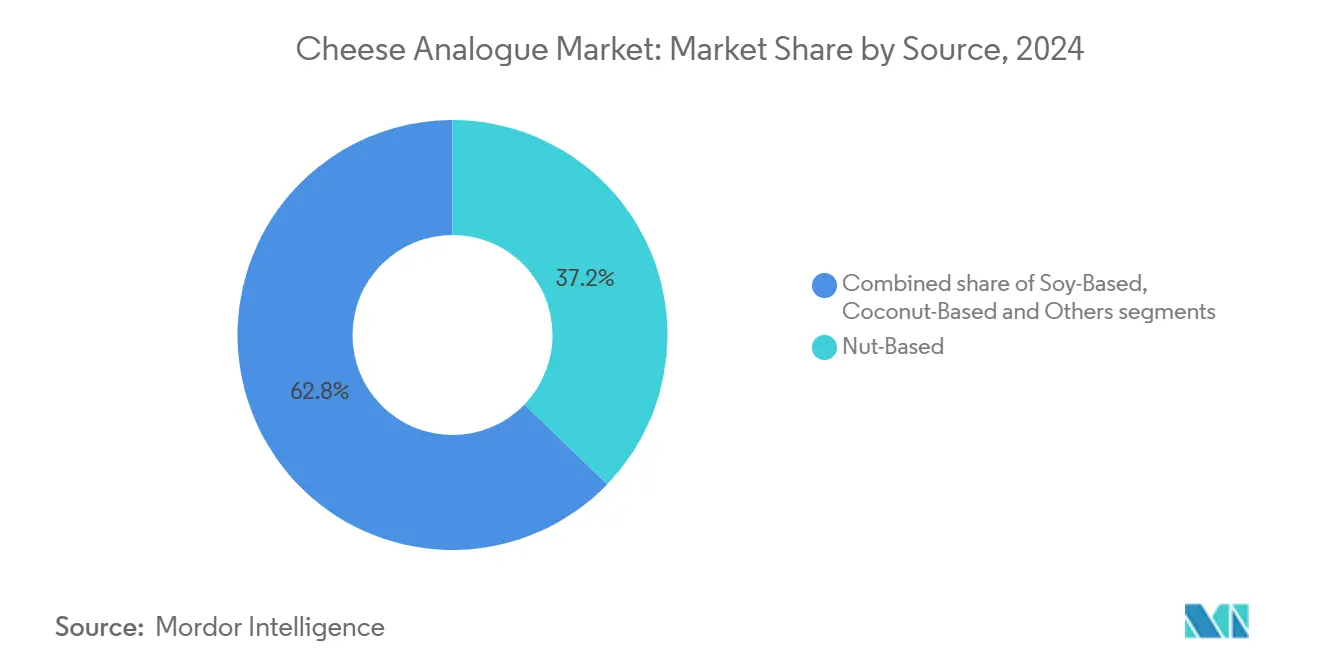

- By source, nut-based products captured 37.21% of cheese analogue market share in 2024; coconut-based alternatives are forecast to expand at a 7.66% CAGR through 2030.

- By category, the conventional segment held 73.44% share of the cheese analogue market size in 2024, while specialty variants are advancing at an 8.03% CAGR through 2030.

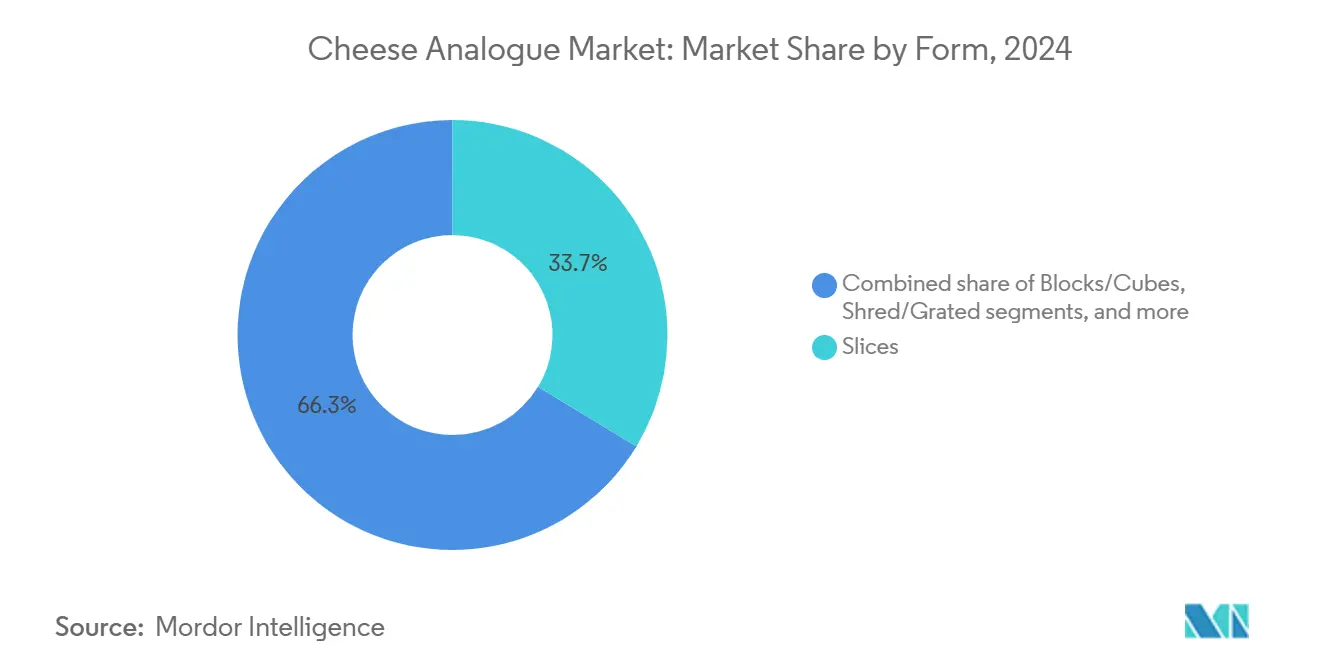

- By form, slices commanded a 33.67% share of the cheese analogue market size in 2024 and spreadables are projected to rise at a 9.21% CAGR to 2030.

- By distribution, off-trade channels accounted for 63.26% of cheese analogue market share in 2024; on-trade channels are growing at a 7.59% CAGR through 2030.

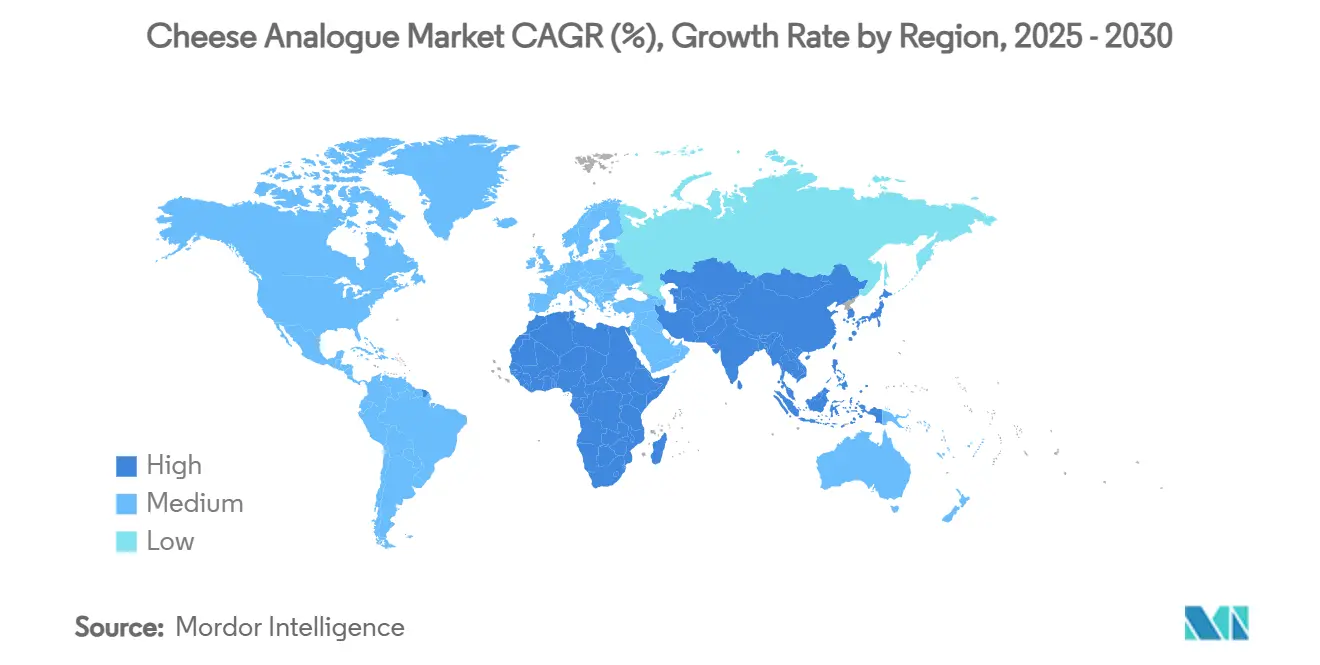

- By region, North America led with 36.69% revenue share in 2024; Asia-Pacific records the highest projected CAGR at 8.94% to 2030.

Global Cheese Analogue Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Lactose Intolerance and Dairy Allergies | +1.2% | Global, with higher impact in Asia-Pacific | Medium term (2-4 years) |

| Growth of Plant-Based and Vegan Diets | +1.8% | North America and Europe core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Increasing Popularity of Processed and Convenience Foods | +1.0% | Global, particularly urban centers | Short term (≤ 2 years) |

| Product Innovation in Taste and Texture | +1.5% | North America and Europe, with technology transfer to Asia | Medium term (2-4 years) |

| Increasing Demand for Fortified Cheese Analogue with Functional Ingredients | +0.8% | Global, premium segments leading | Long term (≥ 4 years) |

| Expansion of E-commerce and Online Retail | +0.9% | Global, accelerated in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising incidence of lactose intolerance and dairy allergies

Lactose intolerance impacts approximately 65% of the global adult population, with prevalence rates as high as 90% in certain Asian countries. This condition has emerged as a significant factor driving the growth of the cheese analogue market, particularly in regions where genetic predispositions have historically restricted dairy consumption[1]National Library of Medicine, "Lactose Intolerance", ncbi.nlm.nih.gov. The alignment between the geographic prevalence of lactose intolerance and the expanding cheese analogue market underscores that biological necessity, rather than lifestyle preferences, is the primary catalyst for growth in this market. Additionally, growing awareness within the medical community about dairy sensitivities has led to an increase in diagnoses, further broadening the consumer base. This shift has expanded the market beyond traditional vegan consumers to include individuals seeking functional, health-focused alternatives to address digestive challenges. These trends collectively highlight the robust growth potential of the cheese analogue market, driven by evolving consumer needs and increasing demand for dairy-free solutions.

Growth of plant-based and vegan diets

The plant-based movement has evolved from a niche dietary choice to a mainstream consumption trend. The fastest-growing segment now comprises vegan and vegetarian consumers who seamlessly integrate plant-based options into their diets. Data from USA Data Hub reveals that in 2023, about 4.2% of the U.S. population identified as vegetarians, while 1.5% embraced veganism[2]USA Data Hub, "Global Trends In Vegetarianism And Veganism Index 2024", usadatahub.com. This demographic shift has fueled a consistent demand for cheese alternatives that blend effortlessly into traditional meals, sparing consumers from major lifestyle adjustments. Environmental concerns play a pivotal role in this transition, with many consumers becoming increasingly aware of the resource-intensive nature and carbon footprint of dairy production. In light of this, the precision fermentation industry has risen to the challenge, crafting animal-free dairy proteins that not only mimic the taste and texture of their conventional counterparts but also boast an impressive 85% reduction in environmental impact. This momentum is further bolstered by the food service sector, as prominent restaurant chains adopt plant-based cheese options, aligning with sustainability objectives and catering to changing consumer preferences.

Increasing popularity of processed and convenience foods

The growing convenience food sector is driving the integration of cheese analogues, particularly in applications such as ready-to-eat meals, frozen pizzas, and snacks. Advanced formulation techniques enable these analogues to replicate the functionality of traditional cheese effectively. Manufacturers are responding to this trend by developing innovative products tailored for food service applications. For instance, Daiya introduced its first-to-market dairy-free cream cheese packets in May 2025, specifically targeting restaurant operators to meet their evolving needs. Additionally, the processed food industry's scale economics allow cheese analogue manufacturers to achieve significant cost efficiencies through bulk ingredient procurement and standardized production processes. The increasing prevalence of urban lifestyles, which prioritize convenient meal solutions, further fuels the demand for plant-based cheese ingredients. These ingredients are designed to endure processing, storage, and reheating without compromising on sensory qualities, making them a preferred choice in the evolving food landscape.

Product innovation in taste and texture

Technological advancements in precision fermentation and plant protein modification are addressing critical barriers that have historically hindered the adoption of cheese analogues. Companies like DairyX are utilizing lab-synthesized casein proteins to replicate the melting and stretching properties of dairy cheese, effectively resolving texture-related consumer concerns. Advanced fermentation techniques employing microbial cultures are producing complex, dairy-like flavor profiles, while innovations such as ChickP's 90% chickpea protein isolate provide neutral-tasting, high-protein bases that enhance both nutritional value and product functionality. The convergence of biotechnology and food science is enabling manufacturers to deliver plant-based cheeses that closely mimic the sensory and functional attributes of dairy. Consumer acceptance studies indicate that these advancements are achieving taste parity with traditional dairy products, further driving adoption. Additionally, industry investments in Research and Development are accelerating innovation, exemplified by Plonts securing USD 12 million in 2024 in seed funding to develop aged plant-based cheeses with textures and characteristics comparable to dairy. These developments are positioning the cheese analogue market for robust growth in the coming years.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain and distribution fluctuations | -0.7% | Global, particularly affecting emerging markets | Short term (≤ 2 years) |

| Regulatory and labeling challenges | -0.5% | Europe and Asia-Pacific, with varying national interpretations | Medium term (2-4 years) |

| Difficulty in achieving technological parity | -0.9% | Global, with higher impact in price-sensitive segments | Long term (≥ 4 years) |

| Quality and standardization problems | -0.6% | Global, particularly affecting smaller manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply chain and distribution fluctuations

Cheese analogues face notable challenges due to their reliance on cold chain distribution, unlike shelf-stable plant-based products. This dependency limits market penetration, particularly in regions with inadequate refrigeration infrastructure. A 2025 University of Antwerp study identified flame retardants and plasticizers in plant-based cheese products, with coconut oil flagged as a contamination source. This highlights critical supply chain quality control issues that must be addressed to ensure safety and maintain consumer trust. Additionally, sourcing specialized ingredients like plant proteins and fermentation-derived components is costly due to limited supplier networks, unlike widely available commodity dairy ingredients. The European listeriosis outbreak, linked to imported vegan cheese products, further emphasized that plant-based alternatives face similar food safety risks as dairy products. This incident demonstrated the need for stringent hygiene standards and pasteurization processes comparable to those in dairy production. Moreover, weak distribution partnerships in many markets restrict retail availability, increasing logistical costs and reducing price competitiveness. Addressing these issues is essential for the plant-based cheese market to achieve sustainable growth and broader acceptance.

Regulatory and labeling challenges

The European Union's restrictions on dairy terminology for plant-based products are causing market fragmentation and consumer confusion due to inconsistent labeling requirements across member states. Turkey enforces the strictest regulations, banning the production and sale of vegan cheese resembling dairy, while other regions permit terms like “cheese alternative.” In the United States, the FDA's January 2025 draft guidance seeks to clarify regulations by requiring plant source identification in product names while allowing cheese-related terminology[3]FAIRR Initiative, "Alternative Proteins Regulations", fairr.org. However, uncertainty around implementation timelines continues to challenge manufacturers. These regulatory inconsistencies increase compliance costs, delay product launches, and hinder companies operating across multiple jurisdictions. The lack of harmonized international standards further restricts trade and prevents manufacturers from leveraging economies of scale, limiting cost reductions and market accessibility. Addressing these disparities is essential to support growth and innovation in the plant-based product market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Nut-Based Leadership Meets Coconut Innovation

In 2024, nut-based cheese analogues capture a commanding 37.21% market share, leveraging their superior protein content and the consumer's growing familiarity with almond and cashew alternatives. This segment's dominance is rooted in the nutritional benefits and processing advantages of nuts, which naturally offer fats and proteins that closely resemble dairy cheese, often needing minimal modification. Recent innovations highlight the segment's dynamic nature, with fermented cashew cheese now enhanced with seaweeds like Chondrus crispus and Porphyra sp., boosting mineral content while retaining familiar taste profiles. While the segment enjoys the advantages of established supply chains and consumer acceptance, its price premiums compared to other plant sources pose challenges for broader market penetration. Furthermore, nut-based formulations effectively tackle protein deficiency issues in plant-based alternatives, with cashew products boasting a complete amino acid profile that rivals the nutritional density of dairy cheese.

Meanwhile, coconut-based alternatives are set to experience the fastest growth, projected at a 7.66% CAGR through 2030. This surge is attributed to advancements in processing techniques that have rectified earlier texture issues and the growing availability of refined coconut ingredients. Yet, the segment grapples with notable challenges. A 2025 study from the University of Antwerp flagged coconut oil as a potential contamination source for flame retardants and plasticizers in plant-based cheese, with contamination levels averaging 1,155 ng/g for plasticizers. Despite these red flags, coconut-based products are gaining popularity, thanks to their natural saturated fat content, which offers superior melting characteristics over other plant sources. The segment's rapid growth is also a testament to enhanced sourcing practices and processing technologies that mitigate the off-flavors often linked to coconut-based dairy alternatives. However, the industry faces mounting pressure for responsible sourcing practices, especially in light of sustainability concerns surrounding coconut oil production.

By Category: Conventional Dominance Faces Specialty Acceleration

In 2024, conventional cheese analogues command a 73.44% market share, underscoring a widespread consumer preference for familiar products that don't tout specialized dietary claims or premium pricing. This dominance suggests that basic plant-based alternatives have reached quality and price points competitive with traditional cheese in everyday uses. Leveraging economies of scale and established distribution ties, the conventional category offers competitive pricing. Manufacturers prioritize enhancing basic sensory attributes over incorporating functional ingredients. While the segment's market control highlights its broad appeal and accessibility, a surge in competition from specialty variants intensifies the push for continual enhancement of core product attributes.

Specialty variants, which include gluten-free, organic, reduced fat, and fortified formulations, are on track for a robust 8.03% CAGR growth through 2030. This surge is driven by manufacturers honing in on specific consumer needs and health considerations. DSM-Firmenich is at the forefront, offering ingredient solutions tailored to the specialty market. Their vitamin blends and nutrient systems aim to fill nutritional voids when compared to dairy cheese. Additionally, their natural colorants and flavor enhancers elevate sensory appeal. Within this specialty category, fortified products are a standout growth driver. Manufacturers are enriching these products with vitamins B12, D, and calcium, striving to match or surpass the nutritional profile of dairy cheese. This move directly addresses health-conscious consumers' concerns about the sufficiency of a plant-based diet. The specialty segment's growth trajectory is a testament to the evolving consumer landscape, with many now willing to pay a premium for added functional benefits. Notably, organic and reduced-fat variants are seeing heightened interest, especially among health-focused demographics.

By Form: Slice Leadership Challenged by Spreadable Innovation

In 2024, cheese slices command a dominant market share of 33.67%, buoyed by their prevalent use in sandwiches and ingrained consumer preferences for convenient, portion-controlled formats. Their widespread acceptance in meal routines, coupled with manufacturing efficiencies, allows slices to be competitively priced against more intricate cheese forms. The slice segment enjoys the advantages of established packaging technologies and distribution networks tailored for refrigerated items. However, challenges in achieving genuine melting and browning effects limit its growth in culinary applications. Consumers' familiarity with processed cheese slices paves the way for acceptance of plant-based versions that mimic basic functionalities. Moreover, the straightforward nature of slices simplifies manufacturing, especially when juxtaposed with aged or cultured cheese alternatives. This segment's leadership underscores that in the realm of plant-based adoption, convenience and familiarity often eclipse sensory nuances.

Spreadable cheese analogues are set to experience the most rapid expansion, with a projected CAGR of 9.21% through 2030. These products are seizing opportunities during breakfast and snack times, where texture demands are less stringent than in melting applications. Nature's Fynd's dairy-free cream cheese, powered by Fy Protein, exemplifies the segment's innovative trajectory. It boasts environmental advantages, consuming less land and water, all while delivering familiar taste profiles at just 80 calories per serving with 7g of total fat. Tirlán's Oat-Standing™ Functional Oat Flour is tailored for cream cheese, ensuring excellent spreadability and addressing the common challenge of syneresis. The swift ascent of the spreadable segment is attributed to both its technical edge and strategic market positioning. Manufacturers can prioritize taste and nutrition, sidestepping the complexities of melting performance. This format not only allows for premium artisanal presentations and diverse flavors but also benefits from reduced manufacturing costs when compared to aged or cultured counterparts.

By Distribution Channel: Off-Trade Control Meets On-Trade Momentum

In 2024, off-trade channels account for 63.26% of cheese analogue distribution, underscoring a consumer shift towards home preparation and the retail sector's adeptness at handling refrigerated plant-based products. Supermarkets and hypermarkets, at the forefront of off-trade distribution, harness their vast cold chain capabilities and promotional strategies to fuel category growth. Their scale not only bolsters competitive pricing but also propels market expansion. This off-trade segment, riding on established consumer shopping habits, adeptly uses packaging and in-store displays to educate shoppers about plant-based alternatives. Meanwhile, online retail in this domain is surging, thanks to e-commerce platforms refining cold chain logistics and subscription models boosting purchase frequency. However, it's worth noting that delivery costs for these refrigerated items outstrip those for shelf-stable goods. The segment's stronghold is a testament to both its infrastructural edge and a consumer inclination towards home consumption of cheese across various meals.

On-trade channels, however, are set to outpace with a projected 7.59% CAGR through 2030. This growth is largely attributed to foodservice operators increasingly incorporating plant-based options, aligning with both sustainability goals and rising consumer demand. A case in point: Daiya's debut of dairy-free cream cheese packets, tailored for foodservice, highlights the segment's shift towards products that cater to operational needs. These 1-ounce packets not only reduce waste but also ensure freshness. The on-trade segment's rapid ascent signals a transition from niche specialty retail to mainstream foodservice, with eateries now viewing plant-based cheese as a staple rather than an afterthought. This channel enjoys fatter margins than its retail counterpart, and the culinary world often enhances the sensory appeal of these cheeses, sidestepping any texture concerns. As dining experiences evolve, so do consumer expectations for plant-based offerings, fueling a demand surge that outstrips retail growth.

Geography Analysis

In 2024, North America holds a dominant 36.69% market share, driven by established regulatory frameworks and a consumer base receptive to product commercialization and retail expansion. This regional supremacy is underscored by early market development and robust infrastructure, notably advanced cold chain distribution networks and strategic foodservice partnerships, ensuring widespread product access. The FDA's 2025 draft guidance on plant-based food labeling offers North American manufacturers a competitive edge. Simultaneously, established venture capital funding fuels ongoing innovation in precision fermentation and product development. Major metropolitan areas in the United States drive regional growth, boasting plant-based adoption rates that outpace national figures.

Asia-Pacific is set to be the fastest-growing region, boasting an 8.94% CAGR through 2030. This growth is spurred by heightened awareness of lactose intolerance, swift urbanization, and supportive government initiatives for alternative protein development. As demographic shifts lean towards plant-based consumption, nations like India and China are recognizing increased sensitivity to dairy, broadening the market appeal beyond just traditional vegan consumers. Research highlights a pronounced enthusiasm for animal-free dairy in India, with a striking 93.4% of respondents eager to sample precision fermentation cheese. Markets in East and Southeast Asia, with a preference for soft textures and subtle flavors, present a canvas for manufacturers to craft region-specific products, leveraging polysaccharides and plant proteins. In South America, Brazil stands out with 92% of its consumers open to trying animal-free dairy cheese. In contrast, Europe grapples with regulatory hurdles that restrict dairy terminology for plant-based items, leading to fragmentation and compliance challenges across its member states.

Despite facing regulatory hurdles, Europe's established market showcases steady growth. These constraints limit the use of dairy terminology for plant-based products, and differing national interpretations complicate compliance for manufacturers operating across borders. Driven by a deep-rooted environmental consciousness, the region consistently demands sustainable alternatives. Moreover, premium positioning strategies allow for higher margins, helping to counterbalance the costs of regulatory compliance. Meanwhile, the Middle East and Africa present untapped potential. While current market penetration is limited, there's a burgeoning awareness of lactose intolerance and the advantages of plant-based nutrition. For the region to realize its development potential, it must focus on expanding its cold chain infrastructure and establishing a regulatory framework. Such measures would ensure product quality and safety standards align with those of more developed markets.

Competitive Landscape

The cheese analogue market features a blend of global brands and numerous regional players, all vying for dominance across diverse product formats and dietary niches. While top companies command significant market shares, the rise of plant-based ingredients and the surging demand for vegan and allergen-free options are luring in new competitors. This competitive landscape not only drives pricing strategies but also enhances product variety and spurs innovations in texture, flavor, and nutrition. Key players shaping the market include Flora Food Group B.V. (Violife), Daiya Foods Inc., Miyoko’s Creamery, Kite Hill, and Danone S.A.

Strategic maneuvers predominantly revolve around vertical integration and forging partnerships. Companies are keen on controlling essential production inputs or tapping into specialized technologies to address sensory challenges. A case in point is New Culture's alliance with CJ CheilJedang, which melds biotechnological advancements with a seasoned fermentation framework, targeting cost parity with traditional mozzarella in a three-year window. Meanwhile, Bel Group's tie-up with Standing Ovation underscores a pivotal shift: traditional dairy giants now view precision fermentation as a strategic asset, not a competitive hurdle, allowing them to diversify their portfolios while capitalizing on their cheese-making heritage.

Foodservice applications present untapped potential, with operational needs diverging from retail demands. Daiya's tailored packet formats, designed for portion control and waste minimization, highlight this opportunity. The sector's primary focus lies in refining fermentation methods, enhancing ingredient functionality, and streamlining supply chains. This emphasis underscores a collective drive to surmount core product challenges, paving the way for wider market acceptance, rather than diverting energies towards marketing or distribution advancements.

Cheese Analogue Industry Leaders

-

Flora Food Group B.V (Violife)

-

Daiya Foods Inc

-

Miyoko’s Creamery

-

Kite Hill

-

Danone S.A (Follow Your Heart)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Miyoko’s Creamery has launched a new dairy-free Jalapeño Cheese Spread, expanding its line of plant-based cheese alternatives for 2025. According to the brand, it is crafted from organic cultured cashew milk, the spread delivers a creamy texture and bold jalapeño flavor, catering to consumers seeking both taste and plant-based ingredients.

- January 2025: JULIENNE BRUNO has debuted Mozzafiore Pearls, claimed to be the world’s first commercial dairy-free mozzarella pearl-style cheese alternative, at Whole Foods Market United Kingdom. According to the brand, the product is made from fermented soybeans, free of dairy, nuts, gluten, and artificial flavorings, making it suitable for people with diverse dietary needs.

- September 2024: Formo has secured USD 61 million in a Series B funding round to accelerate its production and commercialization of animal-free cheese made with precision-fermented Koji. The company’s new Koji cheese products have now launched in select supermarkets, marking a major step in bringing fermentation-based, sustainable cheese alternatives to mainstream retail.

Global Cheese Analogue Market Report Scope

| Soy-Based |

| Nut-Based |

| Coconut-Based |

| Others |

| Conventional |

| Specialty |

| Slices |

| Blocks/Cubes |

| Shred/Grated |

| Spreadable |

| Others |

| On-trade (HoReCa) | |

| Off-trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online retail stores | |

| Other distribution channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Source | Soy-Based | |

| Nut-Based | ||

| Coconut-Based | ||

| Others | ||

| By Category | Conventional | |

| Specialty | ||

| By Form | Slices | |

| Blocks/Cubes | ||

| Shred/Grated | ||

| Spreadable | ||

| Others | ||

| By Distribution Channel | On-trade (HoReCa) | |

| Off-trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online retail stores | ||

| Other distribution channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the cheese analogue market in 2030?

The cheese analogue market size is expected to reach USD 2.87 billion by 2030 at a 7.16% CAGR.

Which region shows the fastest demand growth for cheese analogues?

Asia-Pacific leads in growth, expanding at an 8.94% CAGR through 2030 due to rising lactose intolerance awareness and supportive government policies.

Why do nut-based cheese analogues dominate the source segment?

Nut formulations mimic dairy fat and protein profiles, giving them a 37.21% share of cheese analogue market size while sustaining premium positioning.

Which product form is expanding the quickest?

Spreadable cheese analogues log the highest CAGR at 9.21% because taste expectations are easier to meet and they fit popular snacking occasions.

Page last updated on: