Cheddar Cheese Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

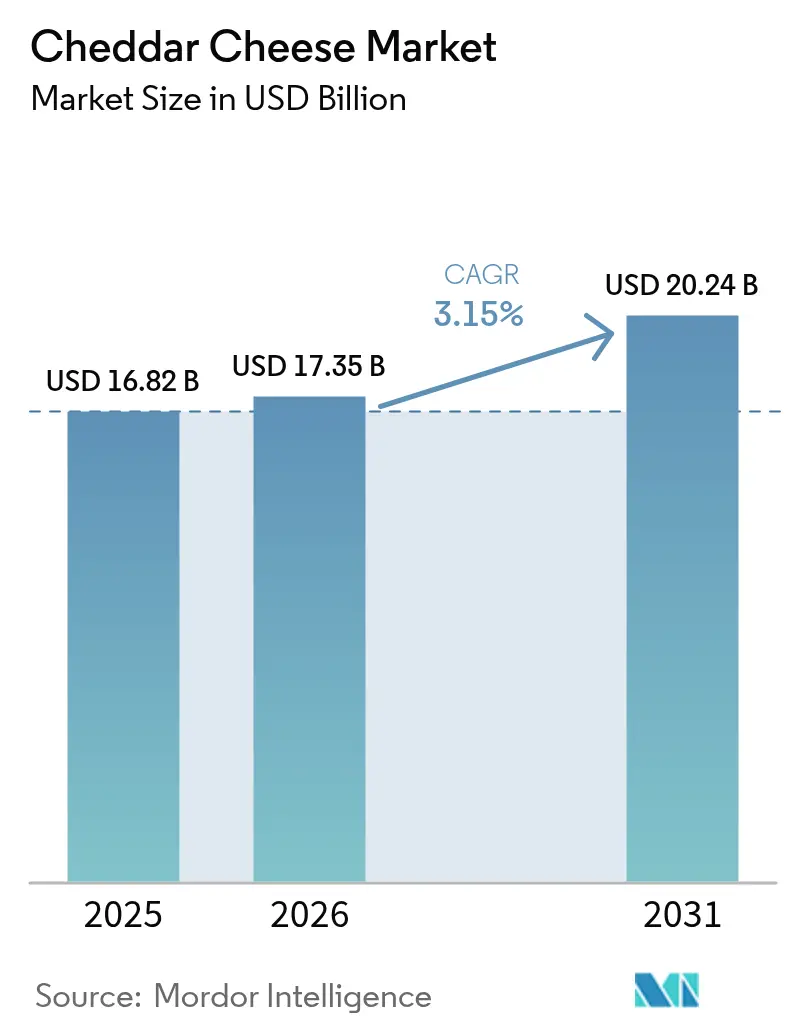

| Market Size (2026) | USD 17.35 Billion |

| Market Size (2031) | USD 20.24 Billion |

| Growth Rate (2026 - 2031) | 3.15% CAGR |

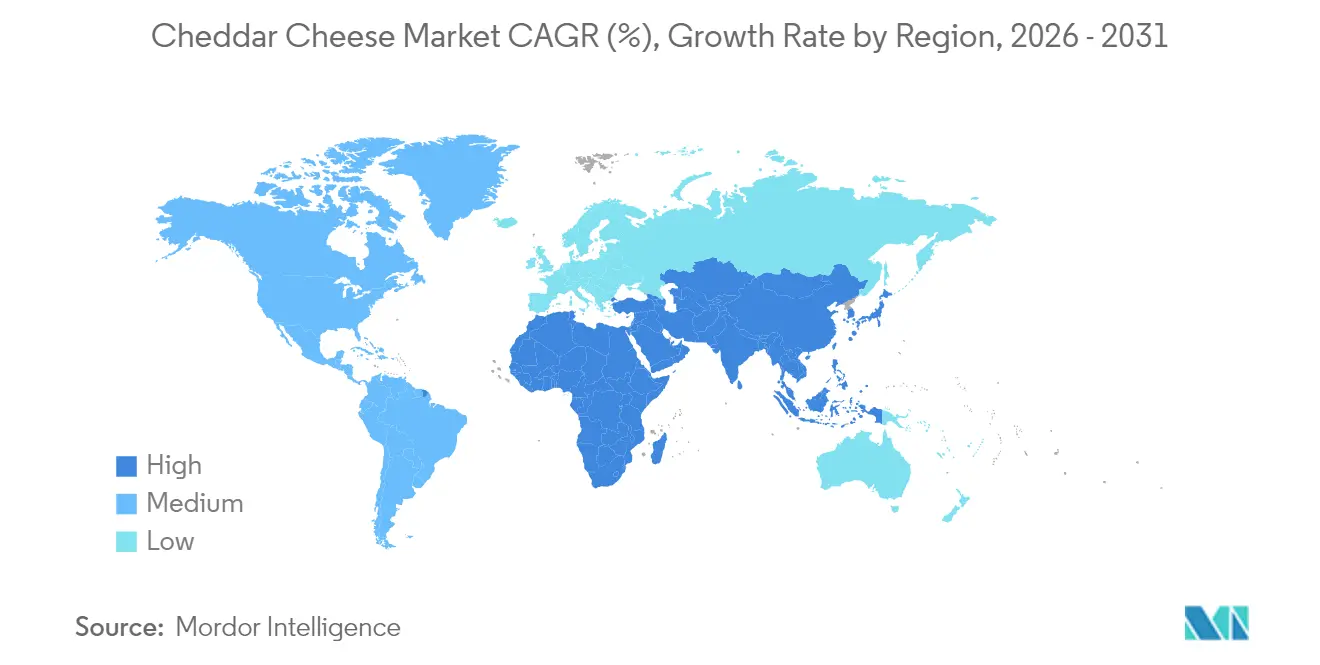

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cheddar Cheese Market Analysis by Mordor Intelligence

The cheddar cheese market size is expected to grow from USD 16.82 billion in 2025 to USD 17.35 billion in 2026 and is forecast to reach USD 20.24 billion by 2031 at 3.15% CAGR over 2026-2031. This growth is primarily driven by factors such as the premiumization of cheese products, the introduction of innovative menu options in quick-service restaurants, and advancements in convenience-focused packaging solutions. North America remains the dominant region in terms of volume; however, the Asia-Pacific region is anticipated to contribute significantly to future growth. This is attributed to the increasing adoption of Western-style dining habits and substantial investments in cold-chain infrastructure, which are enhancing the distribution and storage of cheddar cheese. The recovery of the foodservice sector is playing a pivotal role in driving demand, with more cheddar cheese being utilized in pizzas, burgers, and hot snacks, as opposed to being stocked in retail refrigerators. Additionally, natural cheese variants are gaining popularity over processed formats, a trend fueled by stricter compositional standards and a growing preference for health-oriented products among consumers. While multinational corporations are accelerating consolidation efforts to strengthen their market positions, niche segments such as grass-fed and regenerative cheese offerings are attracting attention from agile regional players, who are leveraging these opportunities to carve out a competitive edge in the market.

Key Report Takeaways

- By product type, natural cheddar captured 58.86% of global revenue in 2025 while also registering the fastest 3.21% CAGR through 2031.

- By form, block products led with 41.78% of cheddar cheese market share in 2025, whereas shredded and sliced formats are expanding at a 3.86% CAGR to 2031.

- By packaging, bulk formats accounted for 43.25% of 2025 sales, yet single-serve packs are rising at a 3.58% CAGR on portion-control demand.

- By distribution channel, off-trade outlets held 67.12% value in 2025, but on-trade foodservice is set to grow faster at a 4.15% CAGR.

- By geography, North America commanded 54.79% value in 2025, while Asia-Pacific is forecast to post the strongest 4.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cheddar Cheese Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer preference for convenient, ready-to-eat cheddar cheese products | +0.6% | Global, with North America and Europe leading adoption; Asia-Pacific emerging | Medium term (2-4 years) |

| Rising demand for healthier cheddar options | +0.5% | North America and Europe core; spill-over to urban Asia-Pacific | Long term (≥ 4 years) |

| Growing popularity of cheese-based snacks and meals | +0.7% | Global, particularly strong in North America foodservice and Asia-Pacific QSR | Short term (≤ 2 years) |

| Advances in dairy processing and packaging technologies | +0.4% | Global, with early adoption in North America and Europe; gradual diffusion to emerging markets | Medium term (2-4 years) |

| Increasing interest in premiumization | +0.5% | North America and Europe dominant; selective uptake in affluent Asia-Pacific urban centers | Long term (≥ 4 years) |

| Product innovation in flavors and formats broadening market | +0.3% | Global, with North America and Europe as innovation hubs; Asia-Pacific adapting to local palates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing consumer preference for convenient, ready-to-eat cheddar cheese products

Consumers with busy lifestyles are increasingly opting for single-serve and snackable cheddar formats, shifting their purchasing behavior from bulk buying to grab-and-go convenience. This shift corresponds with the growing consumption of ready-to-eat foods and a heightened preference for convenient cheddar cheese products. In 2024, the Wholesale Price Index for processed ready-to-eat foods in India reached 146.3, according to the Office of Economic Adviser[1]Source: Office of Economic Adviser, "Annual Average of Monthly Index", eaindustry.nic.in. To capitalize on the portable snacking market, Sartori Company introduced its Cheese Bites in April 2025. These individually wrapped aged cheddar portions, which can remain unrefrigerated for short periods, are designed for on-the-go consumption. Similarly, in 2024, Volpi Foods launched snack cups combining cheddar with cured meats, leveraging the protein-forward snacking trend. This trend has driven U.S. cheese snack sales to grow faster than traditional block formats. The rise of these new formats represents more than just a packaging innovation; it signifies a strategic move toward higher-margin, portion-controlled SKUs. These formats not only support premium pricing but also minimize household waste, aligning with both profitability objectives and sustainability goals.

Rising demand for healthier cheddar options

Health-conscious reformulation is driving a split between reduced-fat options and nutrient-rich full-fat offerings, each catering to distinct consumer segments. As health-conscious individuals seek better food choices, cheddar cheese stands out as an excellent option for those preferring low-fat and nutrients variants. For instance, as of March 2024, 12.2% of Japanese consumers chose health foods labeled as "foods with nutrient function claims" (FNFC), according to the Consumer Affairs Agency[2]Source: Consumer Affairs Agency, "Consumer survey on food labeling", caa.go.jp. In 2024, Cathedral City introduced a high-protein, 30% reduced-fat cheddar, positioning it as a muscle-recovery snack for active consumers while retaining the brand's signature sharpness through extended aging. Similarly, Organic Valley launched its Flavor Favorites line in 2024, featuring organic cheddar made from pasture-raised cows, aligning with the clean-label movement that emphasizes ingredient transparency and animal welfare. Notably, emerging research suggests that regular-fat cheddar may not pose a cardiovascular risk due to the dairy matrix effect, where calcium and bioactive peptides influence fat absorption. A 2024 meta-analysis published in the European Journal of Nutrition found no significant connection between full-fat cheese consumption and coronary heart disease. This finding could help reduce the stigma around traditional cheddar, enabling marketers to position indulgence as acceptable within a balanced diet.

Growing popularity of cheese-based snacks and meals

Cheddar demand is increasing, driven by the recovery in foodservice and the growth of quick-service restaurants (QSRs). On-trade channels are growing faster than off-trade, with a one percentage point higher CAGR. The expanding use of cheddar in QSRs is a significant factor contributing to this market growth. In 2024, the International Franchise Association reported that the United States had 199,931 QSR franchise establishments [3]Source: International Franchise Association, "2025 Franchising Economic Outlook", franchise.org. Demonstrating the global scale of QSR cheese procurement, Fonterra Co-operative Group stated that its foodservice division is expanding at an annual rate of approximately 8%. The company supplies cheddar and cheddar blends to Yum! Brands' Pizza Hut and KFC outlets across more than 30 countries. The pizza and burger segments account for a substantial share of foodservice cheese volume, driving demand for shredded and sliced cheddar formats. These formats ensure uniform melting and consistent flavor across millions of daily servings. Convenience-store chains are also adapting to this trend. For example, 7-Eleven Japan offers cheddar-topped rice bowls and pasta dishes, leveraging cheddar's umami depth to enhance the flavor of grab-and-go meals. Meal-kit providers such as HelloFresh and Blue Apron include pre-portioned shredded cheddar in their recipe boxes. This approach reduces preparation time and waste while introducing home cooks to premium cheddar varieties, potentially encouraging future retail purchases.

Advances in dairy processing and packaging technologies

Cheddar producers are expanding their reach to distant markets while simultaneously reducing their environmental impact, driven by advancements in shelf-life extension and sustainable packaging. In 2024, Cabot Creamery introduced packaging containing 30% post-consumer recycled content, aligning with retailer sustainability goals and consumer preferences for circular-economy practices. Premium cheddar brands are adopting high-pressure processing technology, which eliminates spoilage microorganisms without heat damage. This innovation extends refrigerated shelf life from 90 to 120 days, reducing retailer markdowns and enabling longer export distribution windows. In Europe, aseptic and extended-shelf-life systems are gaining momentum under EU Regulation No 1308/2013, which permits novel processing methods as long as they preserve taste and nutritional value. Artisanal cheddar wheels are being coated with edible layers made from whey protein and chitosan, replacing traditional wax and plastic wraps. These biodegradable alternatives appeal to eco-conscious consumers while maintaining effective moisture barriers. However, the adoption of these technologies is uneven; larger cooperatives and multinationals have the resources to invest in pilot lines and scale-up infrastructure, whereas smaller regional creameries often face financial constraints, creating a competitiveness gap that could drive industry consolidation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating milk and dairy raw material prices | -0.4% | Global, with acute sensitivity in regions dependent on imported feed and energy | Short term (≤ 2 years) |

| Growing health concerns related to saturated fat content and calories | -0.3% | North America and Europe primary; emerging in affluent Asia-Pacific urban markets | Medium term (2-4 years) |

| Supply chain challenges and potential disruptions | -0.3% | Global, particularly acute in regions with underdeveloped cold-chain infrastructure | Short term (≤ 2 years) |

| Perishability of cheese products imposing challenges | -0.2% | Global, with heightened impact in tropical and subtropical climates lacking robust refrigeration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fluctuating milk and dairy raw material prices

Milk price volatility poses the greatest margin risk for cheddar processors. In the U.S., Class III and Class IV milk prices experience cyclical fluctuations, reducing profitability during price increases and creating inventory write-down risks during price declines. The U.S. Department of Agriculture's 2025 dairy outlook forecasts modest growth in milk production. However, tight global dairy supply has kept prices above the 2019-2023 average. This has compelled processors to either absorb higher costs or pass them on to retailers and foodservice operators. Feed costs, which account for 40% to 50% of dairy farm operating expenses, are influenced by grain and soybean meal prices. These prices are subject to changes driven by weather, energy markets, and geopolitical factors. In 2024, the U.S. initiated a modernization process for the Federal Milk Marketing Order to revise cheese pricing formulas, ensuring they better reflect current manufacturing costs. However, this transition introduces uncertainty for processors, who must hedge against potential formula changes that could impact their contract costs.

Growing health concerns related to saturated fat content and calories

Although new scientific evidence challenges the direct association between dairy fat and heart disease, concerns about saturated fat continue to suppress full-fat cheddar consumption. Public health guidelines in many regions still recommend limiting saturated fat intake to less than 10% of daily calories, framing cheddar as more of an occasional indulgence than a dietary staple. However, a 2024 systematic review in the European Journal of Nutrition reported no link between cheese consumption, including full-fat varieties, and an increased risk of coronary heart disease. The review attributed this finding to the "dairy matrix effect," where elements like calcium, protein, and bioactive peptides influence lipid metabolism and gut microbiome composition. Despite this emerging evidence, mainstream dietary guidelines and consumer perceptions remain largely unchanged. This creates a challenging environment for cheddar marketers, who must address lingering health concerns while cautiously promoting research-backed counter-narratives. In response to these health narratives, reduced-fat and low-sodium cheddar options have gained traction. However, these reformulated products often compromise on flavor and texture, limiting their appeal to traditional cheddar enthusiasts and confining them to a niche health-focused market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Natural Cheddar Captures Both Share and Growth Momentum

Natural cheddar accounted for 58.86% of the global market value in 2025 and is projected to grow at a 3.21% CAGR through 2031. This growth surpasses that of processed formats, despite natural cheddar's higher production costs and shorter shelf life. This trend highlights a consumer shift toward authenticity and ingredient transparency. Natural cheddar benefits from regulatory definitions, particularly those established by the FDA in 21 CFR 133.113, which outline specific moisture, fat, and aging requirements. In contrast, processed cheddar uses emulsifying salts and thermal treatments to achieve uniform melting and extended shelf life. While it maintains a strong presence in foodservice, valued for its consistency and cost efficiency, its growth is slower due to health-conscious consumers associating processing with reduced nutritional value.

Grass-fed and organic cheddar varieties within the natural segment are experiencing significant growth, driven by health and environmental narratives that resonate with affluent urban consumers. For example, Pastureland's Irish grass-fed cheddar emphasizes its higher omega-3 and conjugated linoleic acid content, supported by peer-reviewed nutritional research. Meanwhile, processed cheddar remains popular in emerging markets, particularly in the Asia-Pacific region, due to its milder flavor and longer shelf life, which suit local preferences less familiar with sharper, aged cheeses. However, as cold-chain infrastructure improves and Western food culture becomes more prevalent in Asia-Pacific, natural cheddar is expected to gain market share. This transition, however, is likely to occur gradually over several years rather than within a short timeframe.

By Form: Shredded and Sliced Formats Outpace Blocks on Convenience Premium

Block cheddar accounted for 41.78% of the market's value in 2025. While block cheddar remains favored in bulk-buying channels and by culinary enthusiasts for its customizable shred size and thickness, its declining market share signals a structural shift. This trend mirrors a societal move towards time-saving culinary solutions. Formats like shredded and sliced cheddar are projected to grow at a 3.86% CAGR through 2031. This growth is fueled by the rising popularity of meal kits, standardization in food services, and a general consumer push for reduced meal prep times. In 2024, Kraft Heinz rolled out "Signature Shreds", boasting restaurant-quality thick-cut shreds. These shreds are crafted for optimal melt and stretch, appealing to home cooks desiring quick-service restaurant (QSR) quality. Shredded and sliced cheddars command a price premium of 15% to 25% per pound over their block counterparts. This premium reflects the additional labor and packaging efforts, yet consumers readily pay for the convenience and precise portion control these formats offer.

Crumbled cheddar, while a smaller player, is carving out a niche in salad kits and ready-to-eat meals. Its even dispersion and anti-clumping properties elevate product quality. Spreadable cheddar, often mixed with cream cheese or whey for a smooth texture, is positioning itself as a breakfast and snack staple. It competes with butter and margarine on toast, boasting a protein edge. Regulatory standards also influence cheddar's form. For instance, shredded cheddar requires anti-caking agents like cellulose or potato starch to avoid clumping. However, these ingredients face scrutiny from some clean-label proponents. This skepticism has birthed a market for "no-additive" shredded cheddars, which, while accepting a shorter shelf life, prioritize ingredient transparency.

By Packaging: Single-Serve Formats Gain Ground on Portion Control and Snacking Trends

Bulk packaging represented 43.25% of the market value in 2025, highlighting its cost-effectiveness for foodservice and large-household retail purchases. However, single-serve formats are growing at a 3.58% CAGR through 2031, driven by evolving consumption trends that prioritize portion control and on-the-go snacking. Babybel expanded its variety pack in 2024 to include white cheddar, leveraging its strong single-serve brand equity. Similarly, Sargento's Fun! snack packs, which combine cheddar sticks with crackers, provide a portable snacking option that competes with traditional salty snacks. Although single-serve formats are priced higher than bulk options, consumers are willing to pay for the convenience, reduced waste, and calorie transparency they offer. Individually wrapped portions not only meet these demands but also act as built-in portion-control tools, aligning with health and wellness objectives.

Vacuum-sealed formats, designed to extend shelf life by eliminating oxygen and inhibiting microbial growth, are gaining popularity in both bulk and single-serve segments. This trend is particularly evident in export markets, where longer distribution timelines and inconsistent cold-chain reliability present challenges. Bulk packaging continues to dominate the foodservice sector, where operators purchase 5-pound and 10-pound blocks or bags to lower per-serving costs. However, this segment is also witnessing innovation, with resealable bulk bags featuring zip closures replacing traditional film wraps. These advancements help reduce waste and maintain freshness across multiple service periods. Meanwhile, regulatory pressures are reshaping the packaging landscape. Policies such as the European Union's Single-Use Plastics Directive, along with similar initiatives in North America, are pushing manufacturers toward compostable and biodegradable films. These emerging technologies, while promising, come with higher costs that could either compress profit margins or lead to price increases.

By Distribution Channel: On-Trade Recovery Outpaces Retail as Foodservice Demand Rebounds

Off-trade channels, including supermarkets, hypermarkets, convenience stores, specialty retailers, and online platforms, accounted for 67.12% of the market value in 2025. Meanwhile, on-trade channels catering to foodservice and institutional buyers are expected to grow at a 4.15% CAGR through 2031, driven by a post-pandemic recovery in dining and menu innovations. The pizza and burger segments lead foodservice cheese consumption, driving cheddar demand while protecting it from retail price volatility and private-label competition. Quick-service restaurants prioritize consistency, melt properties, and cost predictability, favoring large-scale suppliers with strong quality controls and the ability to fulfill multi-year contracts.

Online retail, though starting from a small base, is the fastest-growing segment within off-trade channels. This growth is fueled by increasing e-commerce grocery penetration and changing consumer perceptions about purchasing perishable dairy products online. Supermarkets and hypermarkets, the dominant players in the off-trade segment, utilize their cold-chain infrastructure and promotional strategies to increase sales. However, they face margin challenges due to the rise of private-label cheddar. Specialty stores and cheese boutiques, while holding a smaller market share, offer premium artisanal and imported cheddar selections, appealing to culinary enthusiasts willing to pay for quality. Convenience stores are shifting from being primarily snack destinations to becoming providers of complete meal solutions. Regulatory factors also influence the on-trade and off-trade dynamics; foodservice operators often benefit from bulk pricing and exemptions from certain labeling requirements, enabling them to offer lower menu prices to consumers.

Geography Analysis

North America represented 54.79% of the global cheddar market value in 2025, highlighting the region's strong cultural connection to the cheese and its dominance in retail and foodservice channels. Cheddar is the preferred cheese in the U.S. for pizzas, burgers, sandwiches, and snacks. However, as per-capita consumption levels off, the market is shifting its focus to premium and specialty segments. In Canada, supply-management policies ensure stable milk prices but limit production flexibility in the cheddar market. This has opened opportunities for imported artisanal varieties, which are commanding premium prices in urban areas. Mexico is emerging as a key growth area in the North American cheddar market, driven by increasing incomes, urbanization, and the expansion of quick-service restaurants featuring cheddar-heavy menus. Notably, Mexico's per capita cheese consumption remains lower than that of the U.S. and Canada, indicating significant growth potential.

Asia-Pacific is poised to lead global cheddar growth with a projected CAGR of 4.19% through 2031. This growth is driven by the region's adoption of Western food culture, the expansion of quick-service restaurants, and increasing protein consumption. In China, natural cheddar's market penetration is limited by low consumer awareness and an underdeveloped cold-chain infrastructure in smaller cities. However, urban centers like Shanghai, Beijing, and Shenzhen are seeing rapid growth in cheddar adoption, supported by the expansion of international QSR chains and the rising popularity of Western dining. India's cheddar market is still developing, with consumption concentrated in major cities and skewed toward processed formats. However, the country's large youth population and growing middle class present a significant growth opportunity if producers can address price sensitivity and adapt flavors to local tastes. Japan and South Korea have higher cheddar consumption per capita compared to other Asia-Pacific markets, reflecting earlier adoption of Western cuisine and well-established retail cold chains. However, growth in these markets is slowing as they mature. Australia and New Zealand are major producers and consumers of cheddar, with export-driven dairy industries supplying cheddar to Asia-Pacific and Middle Eastern markets.

In 2024, Europe held a significant share of the cheddar market, with the UK, Germany, France, and Italy leading consumption. The UK cheddar market is mature and highly competitive, with strong private-label presence and a clear division between commodity and premium segments. Germany and France have lower cheddar consumption per capita compared to the UK, as local preferences lean toward cheeses like Gouda and Emmental. However, cheddar is gaining traction in foodservice, particularly with the growth of burger and pizza chains. Eastern Europe, including Poland and Russia, is emerging as a growth area for cheddar, driven by rising incomes and increasing adoption of Western food culture. However, geopolitical tensions and trade restrictions pose challenges. In Latin America, countries like Brazil, Argentina, and Chile are experiencing growth in the cheddar market, supported by urbanization and the expansion of quick-service restaurants. However, the market remains fragmented and price-sensitive. The Middle East and Africa, despite having the lowest per-capita cheddar consumption globally, are seeing growing demand in urban centers like Dubai, Riyadh, and Johannesburg. This demand is driven by expatriates and affluent locals seeking Western food options, although challenges such as hot climates, cultural preferences for fresh dairy, and price sensitivity persist.

Regulatory Landscape

Cheddar cheese is shaped by compositional standards, safety rules, and border-control requirements that affect formulation and cross-border sales. In the United States, the FDA standard of identity for cheddar cheese under 21 CFR 133.113 sets core parameters, including moisture and milkfat-in-solids requirements. This reinforces the market distinction between clearly defined natural cheddar and processed alternatives that use added ingredients and operate under different regulatory frameworks.

For international trade lanes, alignment with Codex (Codex General Standard for Cheese, CXS 283-1978, amended through December 2024) supports harmonized expectations for composition and additives, with additional country-specific compliance layers. China regulates cheese under its National Food Safety Standard GB 5420-2021, including microbiological and raw material requirements. In the European Union, border and official-control requirements under Regulation (EU) 2017/625 remain a key gatekeeper for imports. Commission Implementing Regulation (EU) 2026/551 (issued March 13, 2026, applying from October 1, 2026) updates the lists of animal-origin products subject to official controls at border control posts, which can affect establishment listing and shipment clearance processes for exporters.

Value Chain Analysis

The cheddar value chain begins with dairy farming, where feed and energy costs influence milk production economics, then moves through milk collection and quality testing. Processing standardizes, pasteurizes, cultures, curdles, cheddars, mills, salts, presses, and ages the product. After aging, cheddar is converted into consumer and foodservice formats, including blocks, shredded, sliced, crumbled, and spreadable, then packaged into bulk, vacuum-sealed, or single-serve options before reaching off-trade retail, e-commerce fulfillment, and on-trade foodservice channels via cold-chain logistics.

Processing capacity and downstream use of co-products are central economic levers in this chain. Whey valorization links cheddar production with sports and medical nutrition ingredients, improving plant economics and encouraging processors to prioritize cheese output. On the infrastructure side, the United States has seen a major processing buildout, with Dairy Herd reporting over USD 11 billion in capital invested into new and expanded processing facilities, including projects cited such as Leprino Foods in Lubbock, Texas, and Hilmar Cheese in Dodge City, Kansas. Trade and standards coordination bodies such as the International Dairy Federation (IDF) and the U.S. Dairy Export Council (USDEC) support cross-border movement through technical alignment and market access, while cold-chain performance remains a differentiator for servicing distant Asia-Pacific and Middle East and Africa demand centers.

Competitive Landscape

The global cheddar market is moderately fragmented, with the top 10 players collectively accounting for a significant share of the market value. However, a substantial portion of the market remains distributed among regional cooperatives, private-label manufacturers, and artisanal producers. This fragmentation highlights cheddar's dual role as both a commodity staple and a premium specialty product. This unique positioning creates opportunities for differentiation across various factors, including aging processes, geographic provenance, organic certifications, and innovative flavor profiles. These elements allow producers to cater to diverse consumer preferences and establish distinct market positions.

White-space opportunities are emerging in niche segments such as grass-fed cheddar, A2/A2 protein variants, and products aligned with regenerative agriculture practices. Smaller players like Pastureland, Rumiano, and Organic Valley are leveraging these trends to carve out specialized niches. Larger incumbents face challenges in replicating these efforts without making significant changes to their supply chains and renegotiating farmer contracts. Meanwhile, technological advancements are reshaping the competitive landscape. Leading companies such as Fonterra Cooperative Group, Arla Foods Limited, and Lactalis Group are implementing high-pressure processing, aseptic extended-shelf-life systems, and real-time cold-chain monitoring. These innovations help reduce waste, extend product shelf life, and expand distribution capabilities. In contrast, smaller producers often rely on conventional pasteurization methods and manual quality control, which limit their ability to compete in e-commerce and export markets.

Global foodservice partnerships are proving to be a strategic advantage for major players. For instance, Fonterra supplies cheddar to Yum! Brands' Pizza Hut and KFC outlets in over 30 countries, ensuring volume stability and providing insulation from retail price wars and private-label competition. While patent activity in cheese processing remains relatively modest compared to other food categories, there is growing interest in innovations such as edible coatings, biodegradable packaging, and microbial cultures designed to accelerate aging. These advancements indicate that intellectual property could become a critical differentiator, particularly in premium market segments, as producers seek to enhance product quality and sustainability.

Cheddar Cheese Industry Leaders

-

Arla Foods Limited

-

Dairy Farmers of America

-

Fonterra Cooperative Group

-

Koninklijke Friesland Campina N.V

-

The Kraft Heinz Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are clustering around throughput expansion, efficiency upgrades, and higher-value formats that fit foodservice and snacking demand. In the United Kingdom, multiple processors have disclosed capacity-linked investments that raise the ceiling for cheddar output and support broader export and private-label supply. First Milk announced a GBP 16.8 million investment at its Lake District Creamery to replace existing cheese vats with larger equipment and lift capacity by 20%, while Arla Foods highlighted a GBP 144 million investment at Lockerbie covering an upgraded cheddar facility with latest-generation vats and an on-site anaerobic digestion plant. These actions create room for suppliers of cultures, automation, and packaging systems that reduce losses and help stabilize quality across longer distribution windows.

A second opportunity area is process and formulation innovation aimed at reducing resource intensity while expanding consumer accessibility, including protein-forward, lactose-free, and portion-controlled cheddar. IFF introduced its CHOOZIT LIFT culture (June 2025) for semi-hard cheese production designed to eliminate curd washing, which offers a route to lower water and energy use per kilogram in relevant production lines. On the product side, recent launches in high-protein sticks and lactose-free cheddar in mainstream portfolios point to a pathway for incremental volume and margin capture through differentiated claims, supported by improving cold-chain capabilities and extended-shelf-life packaging that makes single-serve and export SKUs more workable for retailers and e-commerce operators.

Recent Industry Developments

- May 2026: Kraft Natural Cheese expanded its portfolio with a lactose-free line that includes Mild Cheddar and Mozzarella varieties. The company targets shoppers managing lactose intolerance while keeping the product within mainstream natural cheese usage occasions, strengthening shelf presence against private label and specialty lactose-free brands.

- April 2025: Sartori Company introduced Cheese Bites, individually wrapped portions of aged cheddar positioned for lunchboxes, travel, and workplaces with limited refrigeration access. The format supports portion control and on-the-go consumption, shifting mix toward higher-margin snacking SKUs versus commodity blocks.

- September 2024: RELCO (a Kovalus company) entered a strategic partnership with Milky Mist Dairy Food Private Limited to establish Indias largest cheddar cheese manufacturing plant. The project reflects investment into local processing scale and cold-chain compatible supply, expanding domestic availability beyond imported and processed-cheese-heavy consumption patterns.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the cheddar cheese market is defined as the value of cheddar cheese sold across retail and foodservice channels, covering natural and processed cheddar in common consumer and bulk formats, measured in USD.

Scope exclusions: This sizing does not count non-cheddar cheese varieties, cheese analogs not sold as cheddar, or upstream dairy farming and raw milk production value.

Segmentation Overview

-

By Product Type

- Natural

- Processed

-

By Form

- Block

- Shredded/Sliced

- Crumbled

- Spreadable

-

By Packaging

- Bulk

- Single-Serve

- vacuum-sealed formats

-

By Distribution Channel

- On-Trade

-

Off-Trade

- Supermarkets and Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retail Stores

- Other Off-trade Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Sweden

- Belgium

- Poland

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Thailand

- Singapore

- Indonesia

- South Korea

- Australia

- New Zealand

- Rest of Asia-Pacific

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Saudi Arabia

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping where cheddar volume and value can be observed in public statistics, and then turning those indicators into clean inputs for the model. We typically refer to sources such as USDA dairy and cold storage data, FAOSTAT supply and utilization series, UN Comtrade trade flows, Eurostat agri-food statistics, and national customs or agriculture ministry releases for major producing and consuming countries.

To convert these indicators into market value, secondary references are added, including company annual reports and investor presentations, retailer and foodservice price monitoring in reputed press, and selected peer-reviewed nutrition and dairy science papers for processing and yield assumptions. In a few places, paid subscriptions are used only for company financials, patent lookups, and shipment-level trade checks so gaps in public data can be explained. The sources listed here are illustrative, and many other public and paid references were also used to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work is used to pressure test the desk assumptions with people who see pricing, volumes, and channel movement directly, including dairy processors, ingredient buyers, distributors, and foodservice category managers. We also speak with regional experts across APAC, EMEA, and the Americas so local packaging shifts, import reliance, and private label intensity are reflected consistently in the final numbers.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 12% | APAC: 51% |

| Mid tier: 50% | Functional/Unit leaders: 41% | EMEA: 30% |

| Smaller Players: 17% | Managers: 47% | Americas: 19% |

Market-Sizing & Forecasting

Sizing begins with a top-down build that reconstructs cheddar demand from cheese consumption indicators, production and trade balances, and channel mix, then converts volumes into value using region-specific average selling prices (ASPs). Once the first view is ready, it is corroborated with selective bottom-up approximations such as supplier roll ups by major producing regions, sampled pack-price checks converted to per kilogram equivalents, and distributor feedback on foodservice versus retail splits.

Key model inputs include milk availability and utilization into cheese, cheddar versus total cheese share where published, import and export direction by region, foodservice recovery signals, and packaged format shifts (block versus shredded or sliced) that change realized ASPs. Forecasts are run using scenario analysis anchored to expected changes in consumption habits, trade policies, and input cost pass-through, then adjusted where expert feedback suggests slower or faster pricing normalization. Where bottom-up evidence is thin, we keep assumptions conservative, document the gap, and rely on cross-checks against independent consumption and trade signals.

Data Validation & Update Cycle

Outputs are checked in several steps so the final series remains consistent across history and the forecast window. We compare implied per capita consumption, trade intensity, and ASP movement against independent public signals, then investigate outliers that sit outside expected ranges for a region or channel.

Before sign-off, the model and key assumptions go through internal analyst reviews, and follow-up calls are triggered when a variance cannot be explained through the source trail. Reports are refreshed annually, and interim updates are made when material events occur, such as sharp milk price moves, trade restrictions, or major demand shocks. Right before delivery, a fresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's Cheddar Cheese Market Size Compared With Other Published Estimates

It is normal to see different market sizes for cheddar because each publisher draws the boundary differently and uses different price timing and conversion choices. The spread also increases when some models lean more on broad cheese proxies, while others isolate cheddar and then rebuild value from specific supply and channel signals.

In this study, the gap is often explained by how the price basis is refreshed and converted into USD, since monthly dairy price swings can materially shift ASP-based totals, a step kept in check through scheduled reviews and variance flags before the number is finalized at Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 16.82 B (2025) | |

| Trade Publisher A | USD 3.71 B (2025) | Uses a narrower value pool that appears closer to packaged retail cheddar, with limited visibility into bulk and foodservice volumes, which can understate total market value. |

| Global Publisher B | USD 3.40 B (2024) | Carries a smaller base year total and a different year, and it likely applies a broader average price set that does not fully reflect regional cheddar mix, bulk pricing, and on-trade recovery timing. |

Taken together, the table shows that scope and pricing mechanics drive most of the variance, more than the growth math itself. By keeping the demand pool tied to production and trade signals and then aligning ASP timing to the modeled year, our series stays easier to reconcile with observable market indicators.

Key Questions Answered in the Report

How large is the cheddar cheese market in 2026?

It is valued at USD 17.35 billion, with a forecast to reach USD 20.24 billion by 2031.

Which region will grow fastest in cheddar demand through 2031?

Asia-Pacific is projected to lead with a 4.19% CAGR, driven by QSR expansion and rising Western-style eating.

What product segment is gaining both share and growth momentum?

Natural cheddar tops revenue at 58.86% and is also the fastest-growing variant at 3.21% CAGR.

Why are shredded and sliced forms expanding quickly?

Meal-kit adoption, foodservice consistency needs, and home-cooking convenience push shredded and sliced formats to a 3.86% CAGR.

Page last updated on: