United States Butter Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 11.86 Billion |

| Market Size (2026) | USD 12.43 Billion |

| Market Size (2031) | USD 15.97 Billion |

| Growth Rate (2026 - 2031) | 5.14% CAGR |

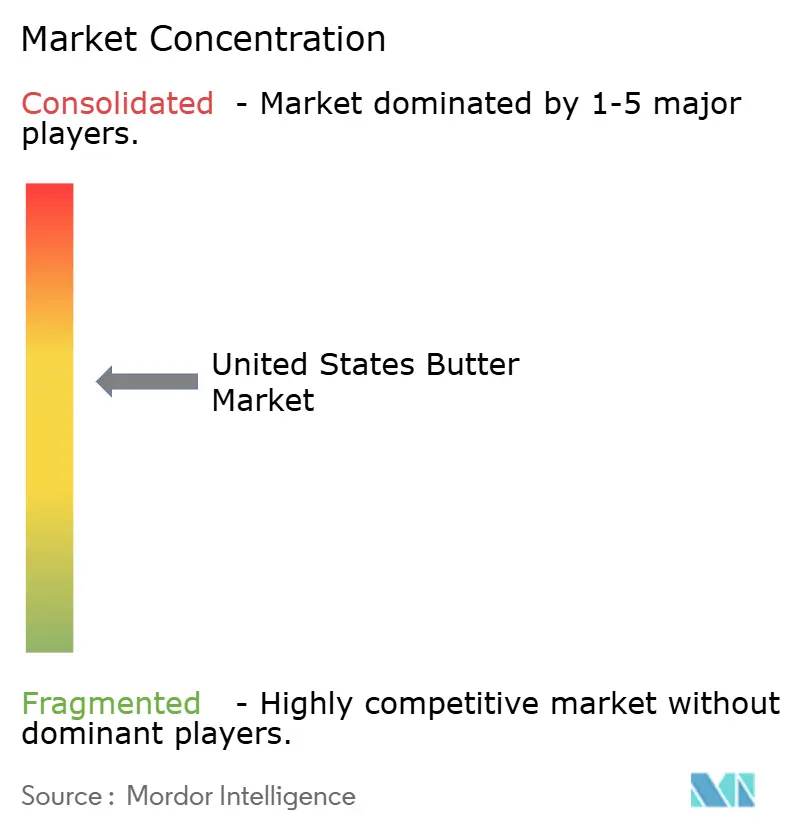

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Butter Market Analysis by Mordor Intelligence

The United States butter market was valued at USD 11.86 billion in 2025 and is projected to grow to USD 12.43 billion in 2026, reaching USD 15.97 billion by 2031, with a CAGR of 5.14% during the forecast period of 2026–2031. This growth is primarily driven by increasing consumer preference for natural, minimally processed, and clean-label dairy products, as buyers prioritize simple ingredients, authentic taste, and high-quality food options. Additionally, the rising demand for premium dairy products, characterized by richer textures, enhanced flavor profiles, and traditional production methods, is further boosting market growth. Shifting dietary preferences and the growing acceptance of full-fat dairy products are also contributing to market expansion, as consumers place greater emphasis on ingredient quality and personalized nutrition.

Key Report Takeaways

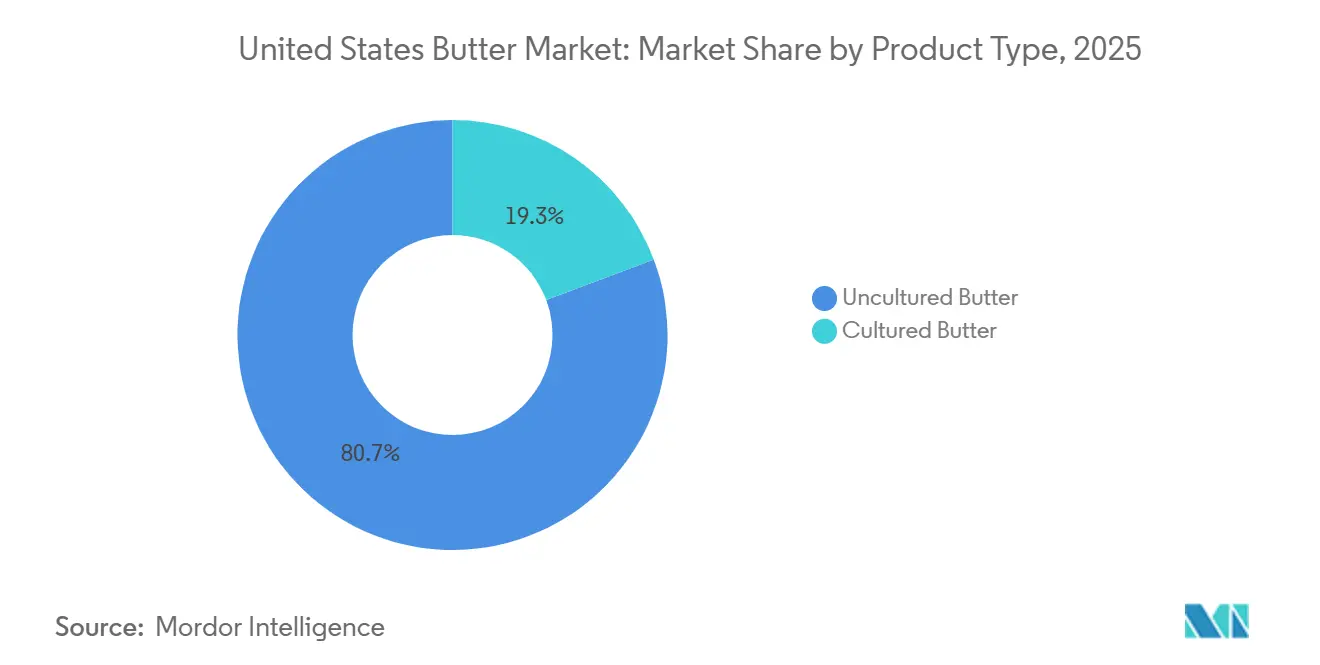

- By product type, uncultured butter held 80.71% of the United States butter market share in 2025, while cultured butter is forecast to expand at a 5.81% CAGR through 2031.

- By source, animal-based butter held 93.21% of the United States butter market share in 2025, while plant-based butter analogs are projected to grow at a 7.03% CAGR through 2031.

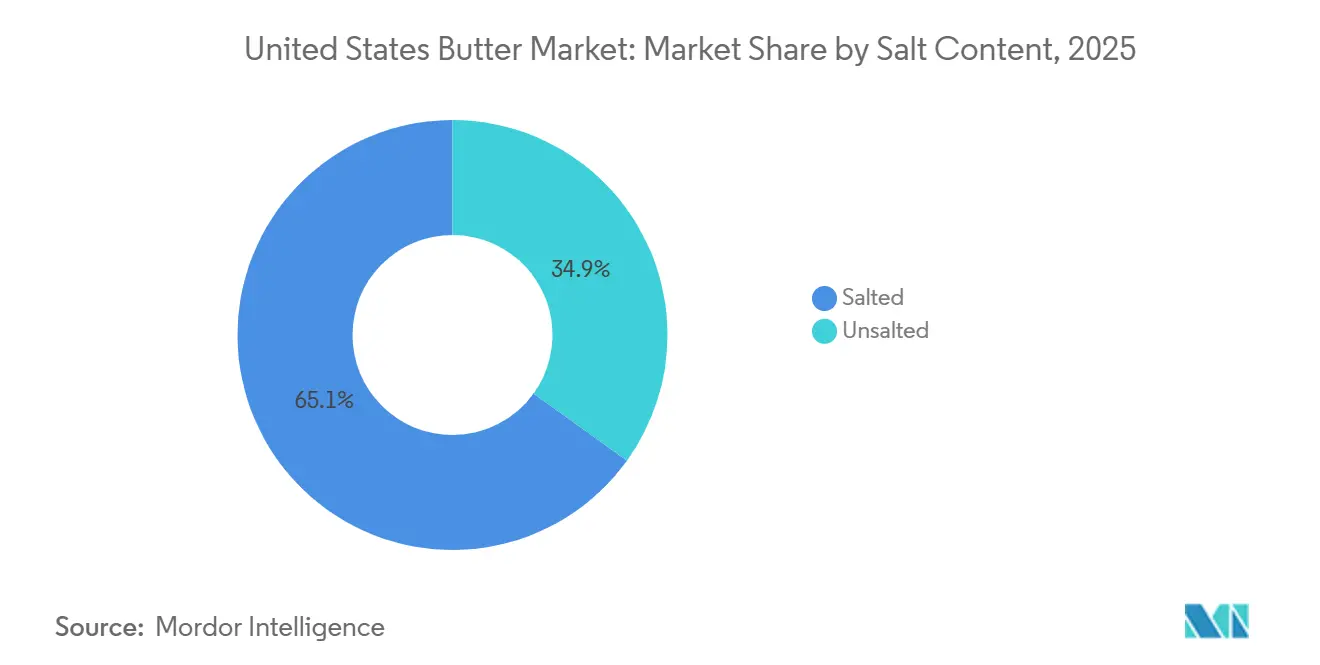

- By salt content, salted butter accounted for 65.06% share of the United States butter market size in 2025, while unsalted butter is set to advance at a 6.33% CAGR through 2031.

- By packaging type, blocks and cubes represented 46.45% share of the United States butter market size in 2025, while plastic boxes and tubs are projected to grow at a 6.81% CAGR through 2031.

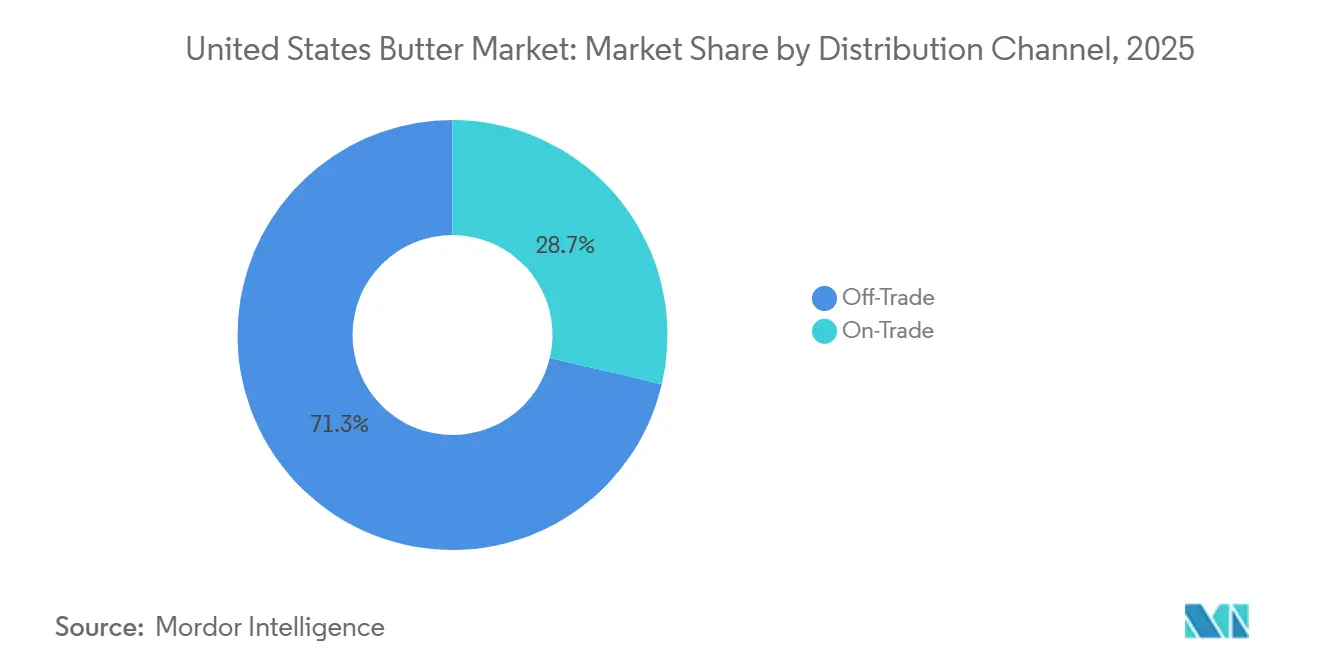

- By distribution channel, off-trade channels accounted for 71.32% share of the United States butter market size in 2025, while on-trade channels are forecast to expand at a 5.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Butter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preference for natural and minimally processed dairy products | +1.2% | National, with above-average intensity in urban and coastal markets | Medium term (2–4 years) |

| Demand for premium and specialty butter products | +0.9% | National, strongest in Northeast, West Coast, and major metro areas | Medium term (2–4 years) |

| Popularity of high-fat and low-carbohydrate diet trends | +0.7% | National, with early concentration in health-focused suburban and digital-native consumer segments | Short term (≤ 2 years) |

| Adoption of grass-fed and organic dairy products | +0.6% | National, with above-average penetration in natural food retail chains | Long term (≥ 4 years) |

| Product innovation and flavor diversification | +0.5% | National, with early adoption in specialty retail and premium foodservice | Medium term (2–4 years) |

| Increasing home cooking and baking trends | +0.4% | National, sustaining across income groups following pandemic-era behavior shifts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Preference for natural and minimally processed dairy products

The growing preference for natural and minimally processed dairy products is driving butter demand, as consumers increasingly prioritize products with simple ingredients, authentic taste, and fewer artificial additives. Butter’s traditional image as a recognizable dairy product made primarily from cream aligns with the rising clean-label movement and the demand for less-processed food options. According to the United States Department of Agriculture (USDA), per capita butter consumption increased to 6.8 pounds per person in 2024, up from 6.5 pounds per person in 2023, highlighting sustained consumer interest in real dairy-based products [1]Source: United States Department of Agriculture (USDA), "Per capita consumption of butter in the United States ", usda.gov. The shift away from highly processed alternatives, coupled with rising demand for premium, organic, grass-fed, and specialty butter varieties, continues to strengthen butter’s appeal among consumers seeking natural and high-quality dairy options.

Demand for premium and specialty butter products

The growing demand for premium and specialty butter products is driving market growth as consumers prioritize enhanced taste, superior quality, and unique dairy experiences. Increased interest in products like cultured butter, European-style butter, grass-fed butter, organic options, and flavored butter has prompted manufacturers to expand their premium product portfolios. Consumers are placing greater importance on attributes such as richer texture, higher butterfat content, traditional production methods, and distinctive flavor profiles, contributing to a shift from conventional butter to value-added varieties. Furthermore, the rising preference for artisanal and clean-label dairy products is fostering innovation in specialty formulations. Improvements in packaging and product positioning are also enhancing consumer engagement with premium butter categories.

Popularity of high-fat and low-carbohydrate diet trends

The increasing popularity of high-fat and low-carbohydrate diet trends is driving butter consumption as consumers shift toward natural, whole-food-based fat sources. The adoption of ketogenic, low-carb, and high-fat dietary lifestyles has enhanced the perception of butter due to its high fat content, low carbohydrate profile, and simple ingredient composition. Changing views on dietary fats are prompting consumers to prefer traditional dairy fats over highly processed spreads and artificial substitutes, boosting demand for full-fat dairy products. Furthermore, a growing emphasis on clean-label nutrition, ingredient transparency, and premium-quality food choices is increasing the preference for grass-fed, organic, and higher butterfat varieties. As consumers prioritize products that align with personalized nutrition and natural eating habits, butter remains well-positioned within these evolving dietary trends.

Adoption of grass-fed and organic dairy products

The rising demand for grass-fed and organic dairy products is driving butter consumption as consumers increasingly prioritize ingredient quality, natural production methods, and premium dairy experiences. Greater awareness of clean-label products, animal welfare, and sustainable farming practices has reinforced consumer preference for butter made from organically sourced and responsibly produced dairy ingredients. In response, manufacturers are introducing premium products emphasizing authenticity, superior texture, and enhanced flavor. For example, in November 2024, Nancy’s Probiotic Foods expanded its dairy portfolio by launching Cultured European-Style Organic Butter in Sea Salted and Unsalted varieties. This product offers a rich, velvety texture and complex flavor profile, earning international recognition. Such innovations underscore the growing demand for high-quality organic butter and support the continued growth of premium dairy categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns related to saturated fat consumption | -0.8% | National, most acute among cardiovascular risk-sensitive demographics in all major markets | Long term (≥ 4 years) |

| Increasing cases of lactose intolerance and dairy sensitivities | -0.5% | National, highest impact in Hispanic, African American, and Asian American communities | Medium term (2–4 years) |

| Volatility in milk supply and dairy raw material availability | -0.6% | National, with upstream impacts concentrated in Midwest and Pacific Northwest dairy regions | Short term (≤ 2 years) |

| Fluctuating butter prices due to supply chain instability | -0.7% | National, most acute for foodservice and industrial buyers with limited hedging capacity | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health concerns related to saturated fat consumption

Health concerns related to saturated fat consumption are limiting butter demand as consumers increasingly focus on dietary choices linked to heart health and overall wellness. Butter contains a high level of saturated fat, prompting health-conscious individuals to reduce consumption or opt for alternatives considered healthier. Greater awareness of nutritional labeling, fat content, and guidelines to limit saturated fat intake has significantly influenced purchasing behavior, particularly among those prioritizing balanced diets and preventive health measures. This shift in perception has driven the adoption of reduced-fat spreads, plant-based alternatives, and other substitute products, intensifying competition for traditional butter. As consumers continue to emphasize healthier eating habits and fat intake management, concerns about saturated fat remain a significant challenge for the butter market.

Increasing cases of lactose intolerance and dairy sensitivities

The rising prevalence of lactose intolerance and dairy sensitivities is limiting butter demand, as more consumers reduce their consumption of dairy-based products due to digestive issues, dietary restrictions, and evolving attitudes toward dairy. Growing awareness of lactose-related discomfort and food sensitivities has driven consumers to seek dairy-free alternatives and plant-based substitutes, intensifying competition for traditional butter products. This trend is particularly pronounced among younger demographics. According to the International Food Information Council (IFIC), in 2024, Gen Z consumers in the United States reported the highest reduction in milk consumption, with approximately 36% indicating they had decreased their milk intake [2]Source: International Food Information Council (IFIC), "Share of consumers who have reduced their milk consumption in the U.S.", ific.org. The growing preference for lactose-free, vegan, and alternative dairy options continues to pose challenges to the growth of conventional dairy-based butter categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Uncultured Butter Dominates, While Cultured Formats Command Disproportionate Value

Uncultured butter accounted for 80.71% of the 2025 market value, driven by its widespread consumer acceptance, familiar taste profile, and strong positioning as a traditional dairy product. Its mild flavor, smooth texture, and consistent quality have reinforced consumer preference, making it a favored choice over specialty butter varieties. The segment benefits from a simple production process, broader availability, and alignment with consumer demand for natural and minimally processed dairy products. Furthermore, the increasing preference for clean-label foods with recognizable ingredients continues to support uncultured butter consumption. Its versatility, established consumption patterns, and ability to meet evolving preferences for authentic dairy experiences further solidify its dominance in the United States butter market.

Cultured butter is the fastest-growing product type, projected to grow at a 5.81% CAGR through 2031. This growth is driven by increasing consumer preference for premium dairy products with enhanced flavor, texture, and traditional processing methods. The fermentation process used in cultured butter creates a richer taste profile, improved creaminess, and distinctive characteristics that appeal to consumers seeking elevated food experiences. Rising interest in artisanal and specialty dairy products is bolstering the segment’s growth as consumers increasingly value authenticity, craftsmanship, and differentiated offerings. Additionally, the growing focus on natural ingredients and traditional dairy preparation techniques supports the adoption of cultured butter.

By Source: Animal-Based Dominance is Structural, but Plant-Based Analogs Open New Demand Architecture

Animal-based butter accounted for 93.21% of the 2025 market value, driven by the established tradition of dairy consumption, strong consumer trust, and the consistent availability of milk-based ingredients. This segment's dominance is further supported by a robust dairy production infrastructure. According to the United States Department of Agriculture (USDA), the nationwide average number of licensed dairy operations was 23,609 in 2025, ensuring a stable supply of dairy inputs for butter production. Consumer preference for authentic dairy taste, natural fat composition, and familiar product characteristics continues to bolster demand for animal-based butter. Additionally, advancements in dairy farming practices, product quality, and processing efficiency are enhancing production reliability.

Plant-based butter analogs represent the fastest-growing source segment, with a projected CAGR of 7.03% through 2031. This growth is driven by the increasing shift toward dairy-free alternatives and evolving consumer preferences for plant-derived ingredients. Rising awareness of sustainability, animal welfare, and diverse dietary needs is encouraging consumers to opt for alternatives made from sources such as nuts, seeds, and vegetable oils. The segment's growth is further supported by advancements in taste, texture, and formulation technologies, enabling plant-based butter analogs to closely mimic the sensory qualities of traditional dairy butter. Additionally, the growing demand for allergen-friendly, lactose-free, and clean-label products is accelerating adoption among a broader consumer base.

By Salt Content: Salted Formats Anchor Household Demand While Unsalted Captures Professional and Health Segments

Salted butter accounted for 65.06% of the projected 2025 market value, driven by strong consumer preference, its enhanced flavor profile, and its long-standing role in everyday dairy consumption. The addition of salt enhances taste consistency, balances the richness of butter, and improves overall sensory appeal, making it a preferred choice among consumers. Additionally, salt contributes to product stability and freshness, aligning with consumer demand for convenient and reliable butter options. The growing popularity of flavorful, ready-to-use dairy products and the continued preference for traditional butter varieties further reinforce salted butter’s market dominance.

Unsalted butter is the faster-growing segment, with a projected CAGR of 6.33% through 2031. This growth is driven by increasing consumer demand for greater ingredient transparency, customization, and healthier dairy options. Awareness of sodium reduction and a preference for products with fewer added ingredients are encouraging a shift toward unsalted varieties. The segment is gaining popularity as consumers seek butter with a pure dairy taste, fresh cream characteristics, and a natural flavor profile without added seasoning. Rising interest in premium dairy products and minimally processed foods further supports demand, as unsalted butter is often associated with higher-quality formulations and authentic taste.

By Packaging Type: Blocks Define Volume Logistics, Plastic Boxes Drive Consumer-Facing Innovation

Blocks and cubes accounted for 46.45% of the 2025 market share by packaging type, driven by strong consumer acceptance, convenience, and their ability to preserve butter's original texture and quality. This segment benefits from consumer preference for traditional butter formats that offer easy portioning, handling, and storage flexibility. Blocks and cubes are widely preferred due to their straightforward packaging design, ability to maintain freshness, and appeal to consumers seeking minimally processed dairy products. The availability of various sizes and portion options has further enhanced their attractiveness by accommodating changing household consumption patterns and minimizing product wastage. Additionally, the rising demand for premium and specialty butter varieties has supported the adoption of block formats, as they are often associated with authenticity, craftsmanship, and high-quality dairy experiences.

Plastic box and tub formats represent the fastest-growing packaging segment, with a projected CAGR of 6.81% through 2031. This growth is driven by increasing consumer preference for convenience, ease of use, and improved product storage. These formats are gaining traction due to their resealable designs, which help maintain freshness, reduce exposure to external elements, and enhance the overall user experience. The growing demand for practical and ready-to-use packaging solutions is encouraging the adoption of tubs, as they provide easier handling, better portion control, and improved storage efficiency compared to traditional formats. The segment's growth is further supported by innovations in lightweight, durable, and user-friendly packaging that align with evolving consumer lifestyles. Additionally, the increasing preference for spreadable butter products and value-added dairy formats is accelerating demand for plastic boxes and tubs.

By Distribution Channel: Off-Trade Infrastructure Anchors Volume, On-Trade Unlocks Value Premiums

Off-trade channels accounted for 71.32% of the 2025 market value, driven by consumer preference for convenience, wider product availability, and diverse retail purchasing formats. This segment benefits from the increasing tendency of consumers to purchase butter for regular household use, supported by access to multiple product choices, various packaging sizes, and specialty variants. The availability of premium, organic, grass-fed, flavored, and alternative butter options through retail channels has enhanced consumer engagement and encouraged repeat purchases. Additionally, improved product visibility, organized shelf placement, promotional activities, and expanded refrigerated storage have contributed to an enhanced shopping experience. The growing adoption of digital grocery platforms and evolving retail strategies emphasizing convenience, freshness, and accessibility continue to reinforce the dominance of off-trade channels.

On-trade channels represent the fastest-growing distribution segment, with a projected CAGR of 5.63% through 2031. This growth is driven by the increasing use of butter in commercial food preparation and a focus on delivering premium taste, texture, and quality experiences. The segment's expansion is further supported by the rising number of foodservice outlets. For instance, the International Franchise Association reported nearly 279,553 quick-service restaurant franchise establishments in the United States in 2025, creating a broader consumption base for dairy ingredients [3]Source: The International Franchise Association, "Number of quick service restaurant (QSR) franchise establishments in the United States", franchise.org . The growing demand for consistent flavor enhancement, premium-quality ingredients, and differentiated menu offerings is driving the adoption of butter in professional food environments.

Geography Analysis

The Western region, particularly California, holds a significant position in the United States butter market due to its large-scale dairy production capabilities, advanced processing infrastructure, and the strong presence of dairy manufacturing facilities. California's well-established milk supply chain ensures consistent cream availability for butter production. Additionally, the increasing focus on sustainable dairy farming, product quality improvements, and premium dairy innovation continues to drive market growth. Consumer preferences for organic, grass-fed, and clean-label dairy products further bolster demand in this region.

The Midwestern states, including Wisconsin, Minnesota, and Iowa, are major contributors to the butter market's growth, supported by their long-standing dairy heritage, robust farming networks, and extensive dairy processing capacity. Wisconsin, renowned for its dairy specialization, benefits from high-quality milk production and expertise in value-added dairy manufacturing. The rising demand for traditional, premium, and specialty butter varieties has prompted processors in these states to prioritize product innovation, enhance production efficiency, and improve quality standards.

The Northeastern and Southern states, including New York, Pennsylvania, Texas, and Florida, are witnessing increasing butter demand driven by shifting consumer preferences and the expanding availability of dairy products. New York and Pennsylvania leverage their strong dairy farming traditions and processing capabilities, while Texas and Florida are experiencing growth due to evolving food preferences and the rising availability of premium dairy options. Enhancements in distribution networks, cold-chain systems, and product accessibility across these regions continue to support the growth of the butter market.

Competitive Landscape

The market exhibits a moderately concentrated competitive structure, dominated by key players such as Dairy Farmers of America, Inc., Land O'Lakes, Inc., California Dairies, Inc., Saputo Inc., and Lactalis Group. These companies maintain strong positions through extensive dairy processing capabilities, diverse product portfolios, and well-established distribution networks. To meet evolving consumer preferences for high-quality and value-added dairy products, companies are focusing on product differentiation by offering premium butter varieties, including cultured, organic, grass-fed, and specialty formulations.

Technology is becoming a critical competitive factor as manufacturers invest in advanced processing methods, formulation enhancements, and innovative packaging solutions. Precision fermentation techniques, which ensure consistent flavor development in cultured butter, and improved cold-chain packaging solutions that enhance freshness and extend shelf life for tub formats, are providing competitive advantages to producers leveraging food technology. Additionally, companies are prioritizing operational efficiency, quality consistency, and enhanced production capabilities to strengthen their market position.

Significant growth opportunities exist in underdeveloped premium segments, particularly within the professional foodservice sector. Cultured butter, compound butter, and specialty formats have considerable potential for expansion compared to the more mature retail premium category. Manufacturers are increasingly targeting these opportunities through innovation-driven strategies, customized butter solutions, and premium positioning. Ongoing investments in product development, sustainability initiatives, and differentiated offerings are expected to influence competitive dynamics among leading market players.

United States Butter Industry Leaders

-

Dairy Farmers of America, Inc.

-

Land O'Lakes, Inc.

-

California Dairies, Inc.

-

Saputo Inc.

-

Lactalis Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Flora Food Group, which includes Country Crock, has launched an 84% butterfat American-made butter called Red Barn. This marks a significant shift for a company traditionally known for vegetable oil spreads and plant-based alternatives.

- August 2025: Kerrygold introduced sweet butter sticks in 3.5 oz sizes, made from grass-fed milk sourced from Irish family dairy farms that are part of farmer-owned local milk cooperatives.

- April 2025: Challenge introduced Challenge Butter Cubes, a new cube-shaped butter format designed for convenient measuring and reduced mess during cooking. Each cube is individually wrapped and pre-portioned into four tablespoons.

United States Butter Market Report Scope

The butter market is segmented by product type, source, salt content, packaging type, and distribution channel. Based on product type, the market is segmented into cultured butter and uncultured butter. Based on source, the market is segmented into animal-based butter and plant-based butter analogs. The animal-based segment is further categorized into cow-milk, buffalo-milk, goat and sheep-milk, and other animal-based sources. Based on salt content, the market is segmented into salted and unsalted butter. Based on packaging type, the market is segmented into blocks/cubes, plastic boxes, and others. Based on distribution channel, the market is segmented into off-trade and on-trade channels. The off-trade segment is further categorized into supermarkets/hypermarkets, convenience and grocery stores, specialty stores, online retail stores, and other distribution channels. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

| Cultured Butter |

| Uncultured Butter |

| Animal Based | Cow-milk |

| Buffalo-milk | |

| Goat and Sheep-milk | |

| Other Animal Based | |

| Plant-based Butter Analogs |

| Salted |

| Unsalted |

| Blocks/Cubes |

| Plastic Boxes |

| Others (Sheet/slabs, cartons, etc.) |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience and Grocery Stores | |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| On-Trade |

| By Product Type | Cultured Butter | |

| Uncultured Butter | ||

| By Source | Animal Based | Cow-milk |

| Buffalo-milk | ||

| Goat and Sheep-milk | ||

| Other Animal Based | ||

| Plant-based Butter Analogs | ||

| By Salt Content | Salted | |

| Unsalted | ||

| By Packaging Type | Blocks/Cubes | |

| Plastic Boxes | ||

| Others (Sheet/slabs, cartons, etc.) | ||

| By Distribution Channel | Off-Trade | Supermarkets/Hypermarkets |

| Convenience and Grocery Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| On-Trade | ||

Key Questions Answered in the Report

What is the 2031 outlook for butter demand in the United States?

The United States butter market is forecast to reach USD 16 billion by 2031 from USD 12.4 billion in 2026, growing at a 5.1% CAGR over 2026-2031.

Which product type leads butter sales in the United States?

Uncultured butter led the category with 80.7% of 2025 value, supported by broad use in households, food manufacturing, and institutional buying.

Which source segment is growing fastest in butter alternatives?

Plant-based butter analogs are the fastest-growing source segment, with a projected 7% CAGR through 2031, although animal-based butter still held 93.2% of 2025 value.

Why are premium and specialty butter products gaining traction?

Premium growth is being supported by stronger demand for grass-fed, cultured, and provenance-led products that offer clearer taste and quality differentiation than standard commodity butter.

Page last updated on: