Lactose-Free Butter Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

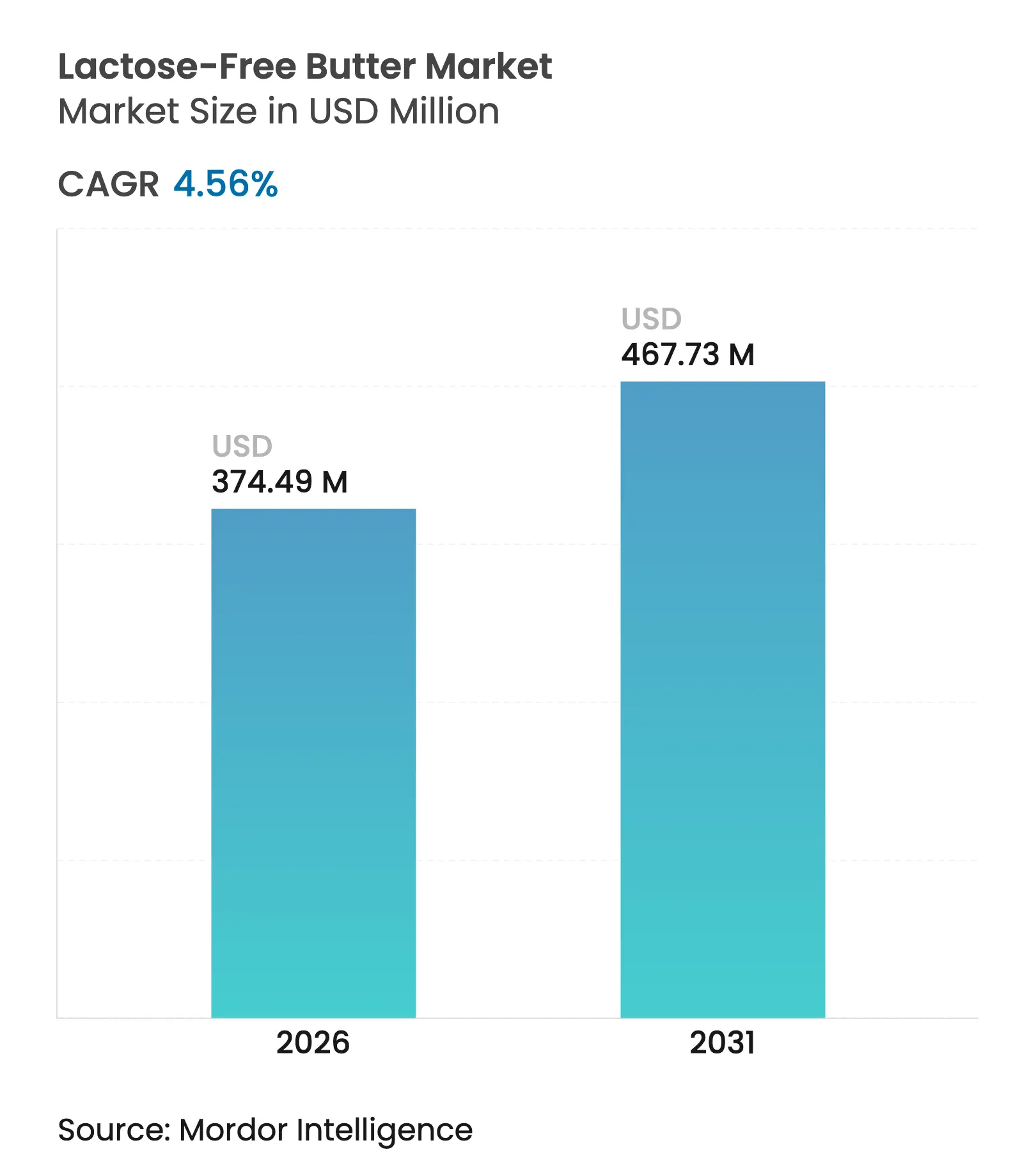

| Market Size (2026) | USD 374.49 Million |

| Market Size (2031) | USD 467.73 Million |

| Growth Rate (2026 - 2031) | 4.56 % CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Lactose-Free Butter Market Analysis by Mordor Intelligence

The lactose-free butter market size was valued at USD 358.16 million in 2025 and estimated to grow from USD 374.49 million in 2026 to reach USD 467.73 million by 2031, at a CAGR of 4.56% during the forecast period (2026-2031). Clinical recognition that lactose malabsorption affects 68% of the global population, together with enzyme technologies that remove lactose while preserving taste, underpins steady demand growth. Mature food-safety rules in North America, halal standardization in the Gulf states, and the European Union’s authorization of beta-galactosidase applications create regulatory clarity that encourages capacity expansion. Premium pricing remains stable because consumers now view lactose-free butter as a functional upgrade rather than a compromise, while off-trade channels and spreadable formats widen household penetration. Momentum is strongest in emerging urban centers where rising incomes, health awareness, and Western baking habits converge, although cold-chain gaps and compliance costs limit conversion in rural areas.

Key Report Takeaways

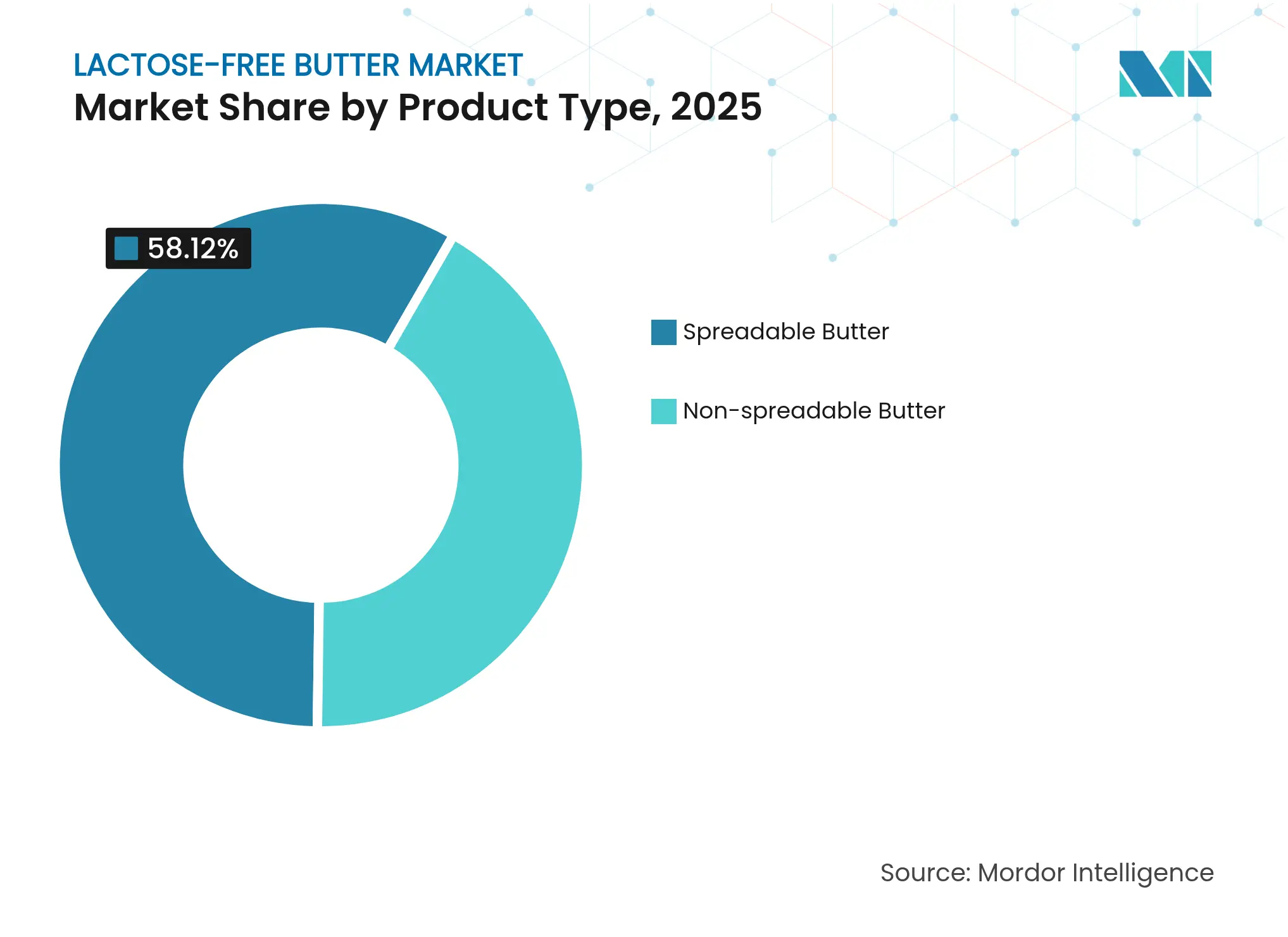

- By product type, spreadable butter led with a 58.12% revenue share in 2025; non-spreadable formats are projected to expand at a 5.21% CAGR to 2031.

- By source, cow milk accounted for 87.34% of the lactose-free butter market share in 2025, while alternatives from goat, buffalo, and sheep milk are advancing at a 5.52% CAGR through 2031.

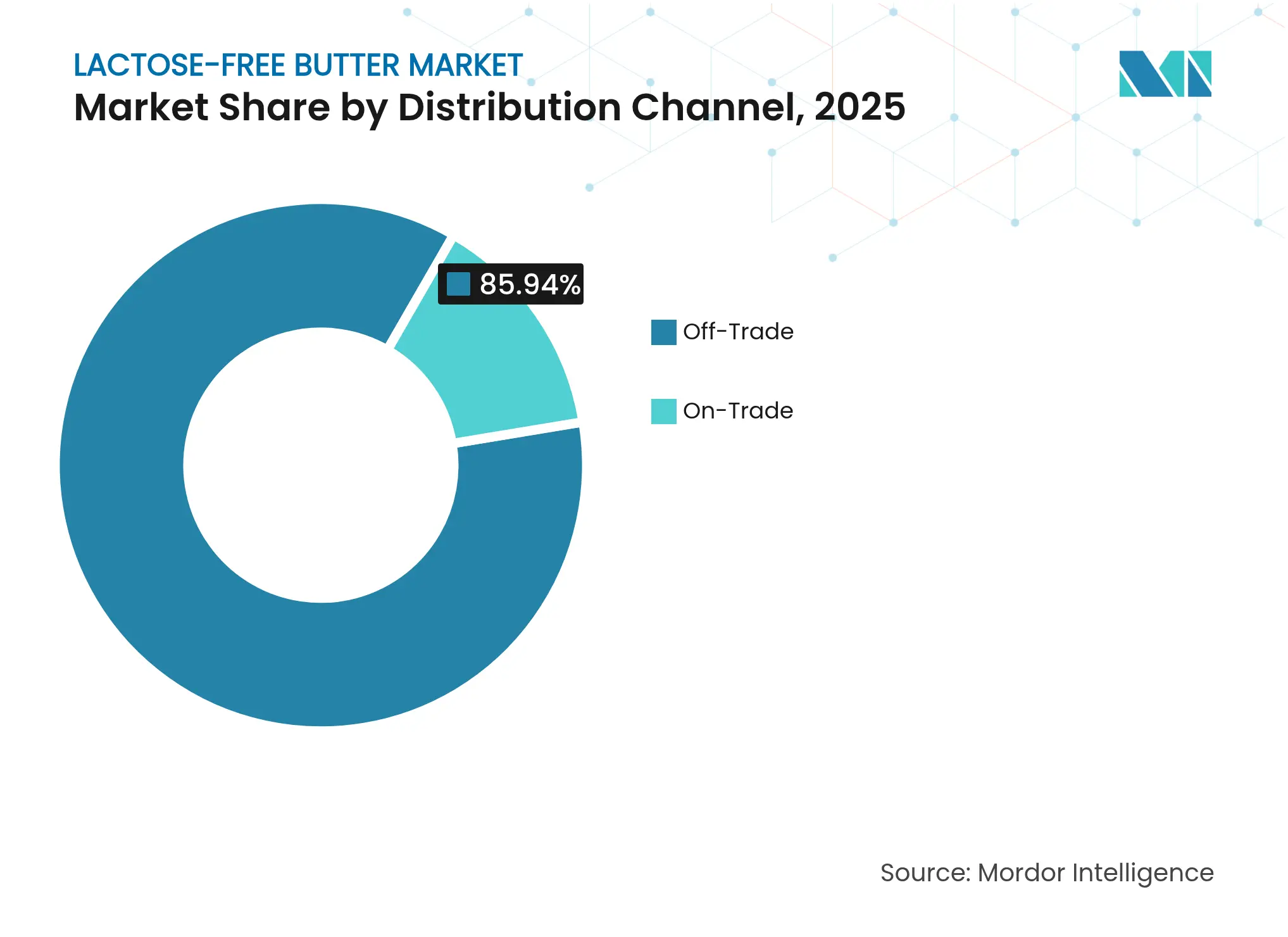

- By distribution channel, off-trade outlets commanded 85.94% of sales in 2025; on-trade recovery is proceeding at a 4.91% CAGR as food service reopens.

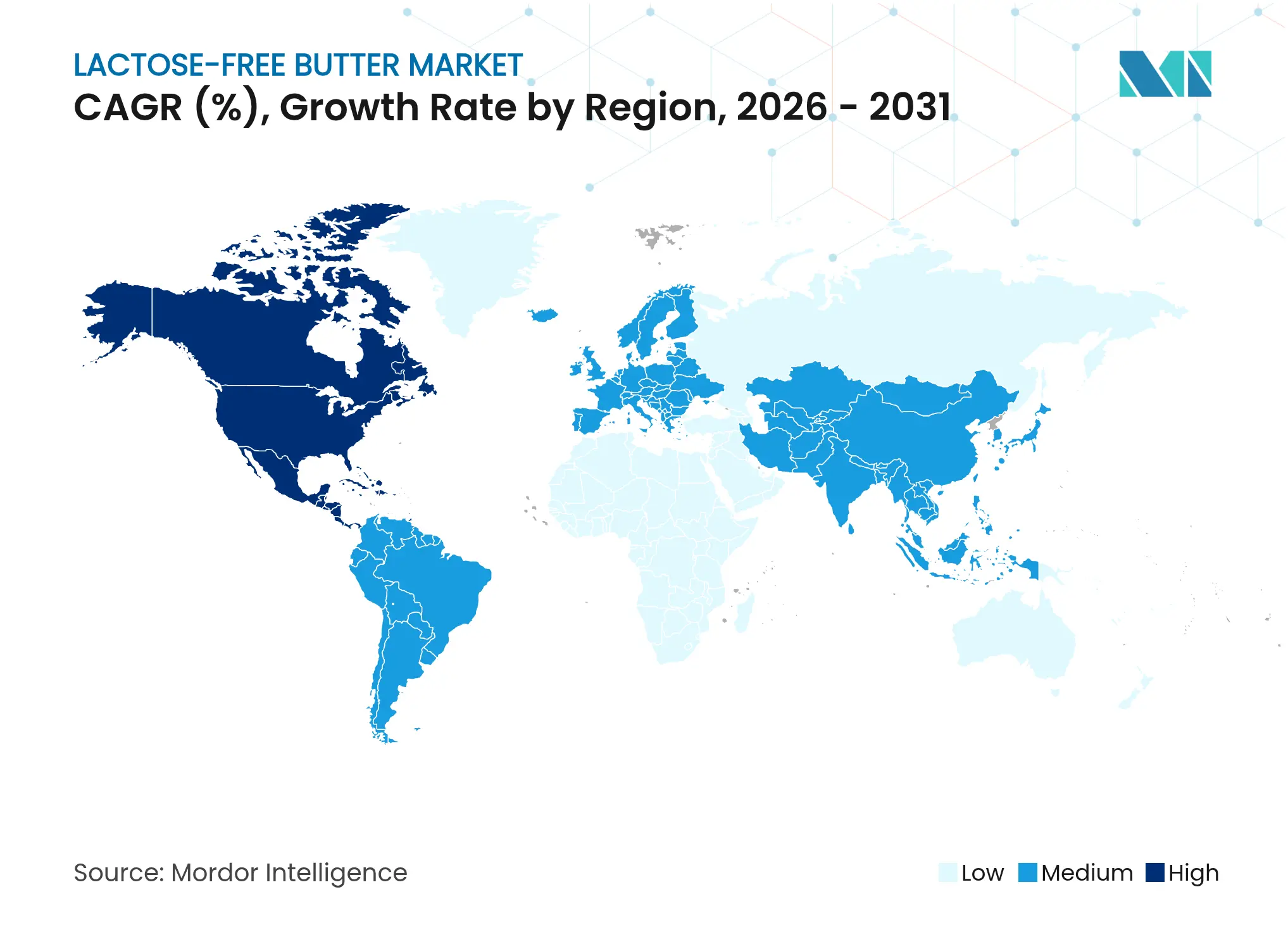

- By geography, North America held 38.12% of global revenue in 2025, whereas the Middle East and Africa region is set to grow at the fastest 6.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lactose-Free Butter Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising prevalence of lactose intolerance and dairy allergies globally Rising prevalence of lactose intolerance and dairy allergies globally | +1.2% | Global, with highest concentration in Asia, Africa, and South America | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:Global, with highest concentration in Asia, Africa, and South America | Impact Timeline:Long term (≥ 4 years) |

Expansion of clean-label and natural ingredient trends in dairy Expansion of clean-label and natural ingredient trends in dairy | +0.8% | North America and Europe, spill-over to urban centers in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) | |||

Growing health consciousness and demand for digestive-friendly dairy products Growing health consciousness and demand for digestive-friendly dairy products | +1.0% | Global, particularly urban populations in developed and emerging markets | Medium term (2-4 years) | |||

Increasing vegan and flexitarian consumer adoption of lactose-free options Increasing vegan and flexitarian consumer adoption of lactose-free options | +0.9% | North America, Europe, Asia-Pacific urban cores (Japan, South Korea, Australia) | Short term (≤ 2 years) | |||

Premium pricing acceptance among health-focused premium segments Premium pricing acceptance among health-focused premium segments | +0.6% | North America, Western Europe, Gulf Cooperation Council states | Short term (≤ 2 years) | |||

Product innovation in taste and texture matching traditional butter Product innovation in taste and texture matching traditional butter | +0.7% | Global, with early commercial adoption in Europe and North America | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising prevalence of lactose intolerance and dairy allergies globally

Rising prevalence of lactose intolerance and dairy allergies globally drives the lactose-free butter market as, according to the National Institute of Health in 2024, 65% to 70% of the world's population exhibits lactose intolerance[1]Source: National Institute of Health, “Lactose Intolerance”, ncbi.nlm.nih.gov, prompting widespread demand for accessible dairy alternatives. Heightened awareness through medical diagnoses and consumer education accelerates adoption among affected demographics, particularly in high-incidence regions like Asia, Africa, and parts of Europe. Foodservice operators and households seek butter substitutes that maintain culinary performance without digestive discomfort, expanding retail and institutional channels. Regulatory labeling mandates enhance visibility, enabling informed purchasing in supermarkets and online platforms. Wellness trends amplify this shift, positioning lactose-free butter as essential for inclusive menus and family nutrition.

Expansion of clean-label and natural ingredient trends in dairy

Expansion of clean-label and natural ingredient trends in dairy propels the lactose-free butter market as consumers demand transparent formulations free from artificial additives and excessive processing. According to research by CBI Ministry of Foreign Affairs, clean-label products are projected to constitute over 70% of portfolios in 2025 and 2026, increasing from 52% in 2021[2]Source: CBI Ministry of Foreign Affairs, "Which trends offer opportunities," cbi.eu. Lactose-free processing via natural lactase enzymes aligns perfectly with "minimal intervention" claims, differentiating products from synthetic dairy alternatives. Brands emphasize short ingredient lists typically just milk, cultures, and lactase appealing to health-conscious shoppers scanning labels for purity. This trend coincides with rising scrutiny of ultra-processed foods, positioning lactose-free butter as a premium, trustworthy option in refrigerated dairy cases. Retailers dedicate expanded shelf space to clean-label dairy, boosting visibility alongside organic and grass-fed variants.

Growing health consciousness and demand for digestive-friendly dairy products

Growing health consciousness and demand for digestive-friendly dairy products drive the lactose-free butter market as consumers prioritize gut health amid rising awareness of lactose-related discomforts like bloating and IBS. The World Health Organization's emphasis on microbiome health in its 2024 dietary guidelines has amplified awareness of lactose intolerance management as a component of overall wellness[3]Source: World Health Organization, "Healthy Diet", who.int. This shift reflects broader wellness movements emphasizing proactive digestion management through everyday staples rather than restrictive diets. Lactose-free butter enables seamless integration into baking, cooking, and spreading without compromising flavor or texture, appealing to families and food enthusiasts. Clinical endorsements and influencer advocacy amplify visibility, positioning the category as essential for inclusive meal planning. Retailers expand chilled dairy sections with prominent digestive health claims to capture impulse buys. Manufacturers respond with fortified variants incorporating prebiotics for enhanced gut support, justifying premium pricing.

Increasing vegan and flexitarian consumer adoption of lactose-free options

Increasing vegan and flexitarian consumer adoption of lactose-free options drives the lactose-free butter market as these groups seek dairy-like products without animal-derived lactose, expanding the addressable consumer base beyond intolerance sufferers. Flexitarians, representing 30-40% of Western demographics, favor occasional dairy alternatives that maintain culinary versatility in plant-forward diets. Vegan butter innovations using lactase-treated dairy or plant blends bridge ethical and health preferences, capturing premium shelf space. Retailers position lactose-free alongside vegan spreads to capitalize on crossover demand in wellness aisles. Manufacturers innovate with hybrid formulations cow milk with canola or almond oil appealing to semi-vegetarian lifestyles prioritizing sustainability and digestion. E-commerce subscriptions and meal kit integrations accelerate trial among younger flexitarians influenced by social media.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Limited consumer awareness in non-urban and emerging markets Limited consumer awareness in non-urban and emerging markets | -0.5% | Rural areas in South Asia, Sub-Saharan Africa, interior South America | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:-0.5% | Geographic Relevance:Rural areas in South Asia, Sub-Saharan Africa, interior South America | Impact Timeline:Long term (≥ 4 years) |

Perception of inferior taste or mouthfeel versus regular butter Perception of inferior taste or mouthfeel versus regular butter | -0.4% | Global, particularly among traditional dairy consumers in Europe and North America | Medium term (2-4 years) | |||

Shorter shelf life due to processing sensitivities Shorter shelf life due to processing sensitivities | -0.3% | Global, with acute impact in regions lacking cold-chain infrastructure (Africa, Southeast Asia) | Medium term (2-4 years) | |||

Stringent food safety and labeling compliance burdens Stringent food safety and labeling compliance burdens | -0.4% | Global, disproportionately affecting small and medium producers in emerging markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Limited consumer awareness in non-urban and emerging markets

Limited consumer awareness in non-urban and emerging markets restrains the lactose-free butter market, as rural populations and developing regions often lack education on lactose intolerance symptoms and available solutions. Traditional dietary habits prioritize conventional dairy staples, viewing lactose-free variants as unnecessary premiums rather than essential alternatives. Low penetration of health media and medical outreach in areas like rural Asia, Africa, and Latin America perpetuates undiagnosed intolerance, suppressing demand volumes. Retail infrastructure gaps few supermarkets stocking specialized dairy compound visibility challenges, confining sales to urban elites. Cultural stigma around digestive issues further discourages trial among price-sensitive households. Manufacturers face high marketing costs for grassroots campaigns, delaying category mainstreaming in high-growth demographics.

Perception of inferior taste or mouthfeel versus regular butter

Perception of inferior taste or mouthfeel versus regular butter restrains the lactose-free butter market, as consumers associate lactase processing with altered creaminess, sweetness, or aftertaste that fails to replicate traditional butter's indulgent profile. Early formulations often suffered from residual enzyme bitterness or watery texture, fostering skepticism among trial users and limiting repeat purchases. Sensory panels confirm that 25-30% of tasters detect differences in spreadability and melt characteristics, deterring premium positioning in baking and gourmet applications. This barrier persists despite technological advances in lactase timing and fat crystallization, as legacy perceptions linger through word-of-mouth and online reviews. Retailers hesitate to allocate prime shelf space to products vulnerable to comparison shopping. Manufacturers invest heavily in blind taste tests and reformulations, yet overcoming entrenched biases slows mainstream adoption.

Segment Analysis

By Product Type: Spreadable Formats Drive Convenience Premium

Spreadable butter dominated the lactose-free butter market in 2025, capturing a significant 58.12% share. This dominance reflects strong consumer preference for convenience, as spreadable butter offers refrigerator-to-table usability without the need for softening before application. Its creamy texture and ease of use make it highly favored for everyday consumption, including bread spreads and general cooking. The product’s consistent quality and availability in retail formats support widespread adoption. Additionally, lifestyle trends emphasizing quick meal preparation drive demand for spreadable butter. As a result, this segment maintains a robust presence, catering largely to household consumers seeking practicality and immediate usability.

Non-spreadable butter, while occupying a smaller market share, is experiencing growth at a compound annual growth rate (CAGR) of 5.21%. This growth is largely attributed to food service operators and home bakers who prefer its distinct functional advantages. Non-spreadable butter offers superior performance in culinary applications requiring precise control of fat content and texture, such as laminated pastries and sauces. In these contexts, the modified texture of spreadable butter can compromise product quality and outcome consistency. As artisanal baking and professional cooking demand finer ingredient precision, the importance of non-spreadable butter rises.

Note: Segment shares of all individual segments available upon report purchase

By Source: Cow Milk Dominance Faces Niche Alternatives

Cow milk dominated lactose-free butter production in 2025, commanding 87.34% of the total volume. This overwhelming share stems from well-established supply chains that ensure reliable sourcing and scalability for manufacturers. Consumer familiarity with cow milk-based products fosters trust and repeat purchases in retail settings. Regulatory frameworks worldwide are optimized specifically for bovine dairy processing, streamlining certification and compliance processes. These factors collectively enable cow milk to maintain consistent quality and broad availability across global markets. As the foundational source in lactose-free butter, cow milk benefits from decades of technological advancements in lactase treatment and flavor neutralization.

Alternative milk sources, including goat, buffalo, and sheep, represent the fastest-growing segment in lactose-free butter production, expanding at a compound annual growth rate (CAGR) of 5.52% through 2031. This growth is propelled by niche consumer segments prioritizing unique flavor profiles that offer subtle tanginess or richness distinct from cow milk varieties. These alternatives naturally contain marginally lower lactose levels, appealing to highly sensitive individuals seeking minimal processing. Rising interest in artisanal and premium dairy products drives demand among gourmet consumers and specialty retailers. Diversification in farm sourcing enhances resilience against cow milk supply fluctuations caused by feed costs or disease outbreaks.

By Distribution Channel: Off-Trade Dominance with On-Trade Recovery

Off-trade channels dominated the lactose-free butter market's distribution in 2025, capturing 85.94% of the total share. This commanding position reflects the product's status as a household staple, routinely purchased for home consumption. Supermarkets and hypermarkets serve as primary touchpoints, offering extensive shelf space and promotional visibility to drive impulse buys. Increasingly, online retail platforms contribute to this growth, providing convenience through subscription models and home delivery services. Consumer behavior favors bulk purchasing and stockpiling in these channels, ensuring steady demand volumes. The off-trade dominance underscores lactose-free butter's integration into everyday grocery routines across diverse demographics.

On-trade channels, comprising just 14.06% of distribution share in 2025, represent the fastest-growing segment with a compound annual growth rate (CAGR) of 4.91% through 2031. This recovery follows pandemic-era disruptions that severely impacted institutional food service operations worldwide. Operators in hotels, restaurants, and catering are now rebounding, incorporating lactose-free butter into standard menu offerings to accommodate dietary restrictions. Rising awareness of lactose intolerance among diners prompts menu diversification, boosting on-trade procurement. Professional kitchens value the product's reliability in high-volume preparation, from baking to table service.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America commanded the largest share of the global lactose-free butter market in 2025, accounting for 38.12% of total revenue. The region benefits from mature dairy industries, advanced production technologies, and strong consumer awareness of lactose intolerance and related dietary needs. Robust regulatory frameworks and established organic and specialty product certifications enhance market penetration. Additionally, widespread retail infrastructure, including supermarkets and online platforms, supports extensive availability. High per-capita income and health-conscious lifestyles drive consistent demand for lactose-free dairy alternatives. North America’s leadership is further affirmed by innovation in lactose-free product formulations and marketing strategies targeting both functional and indulgence-oriented consumers.

The Middle East and Africa represent the fastest-growing region in the lactose-free butter market, projected to expand at a compound annual growth rate (CAGR) of 6.05% through 2031. This growth is fueled by increasing consumer awareness of lactose intolerance and rising disposable incomes, particularly in urban centers. Expansion of modern retail chains and improving cold-chain logistics enable wider product distribution. Growth in the hospitality and food service sectors further bolsters demand. Government initiatives promoting healthier food options and dietary diversification support market development in these emerging economies. Collectively, these factors position the Middle East and Africa for significant market advances in the lactose-free dairy segment.

Asia-Pacific, Europe, and South America also contribute meaningfully to the lactose-free butter market’s global dynamics. Asia-Pacific benefits from rising population health awareness and increasing penetration of western dietary habits, alongside expanding dairy processing capacities. Europe holds a significant market share due to established lactose intolerance rates and highly regulated food safety standards fostering consumer trust. South America shows steady growth driven by expanding dairy sectors in countries like Brazil and Argentina, alongside growing exports. These regions reflect diverse market maturity stages, with opportunities for both premium product adoption and broader accessibility.

Competitive Landscape

Market Concentration

The lactose-free butter market displays moderate fragmentation, characterized by a competitive environment where large multinational dairy cooperatives operate alongside specialized ingredient suppliers and regional processors. This structure reflects the complexity of the dairy supply chain and the diverse consumer demands across global markets. Multinational cooperatives leverage extensive production capacities, advanced technological capabilities, and robust distribution networks to deliver consistent product quality at scale. Their presence ensures broad market coverage and the ability to meet regulatory requirements in multiple jurisdictions, reinforcing consumer trust in lactose-free dairy alternatives.

Alongside these large players, specialized ingredient suppliers play a crucial role by providing innovative lactase enzymes and other functional additives that enable the production of lactose-free butter with enhanced taste and texture. These suppliers contribute to product differentiation and help manufacturers meet increasing demand for high-quality, clean-label lactose-free dairy goods. Their focus on research and development fosters continuous improvements in lactose reduction techniques, shelf-life extension, and nutrient retention, driving market competitiveness through innovation.

Regional processors also form a significant component of the market, capitalizing on local consumer preferences and supply chain efficiencies. These players often operate in niche markets or emerging regions, tailoring products to specific taste profiles and cultural dietary requirements. Their agility enables rapid response to evolving consumer trends, such as organic certification or artisanal product positioning. The coexistence of global cooperatives, ingredient specialists, and agile regional processors creates a dynamic market landscape, fostering diversity of options and opportunities for new entrants willing to innovate and build localized supply chains.

Lactose-Free Butter Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Fonterra, in line with its strategic investments highlighted in its FY25 Annual Results, announced a USD 75 million investment aimed at expanding butter production at its Clandeboye facility in South Canterbury. This move marked a significant step in the Co-operative's efforts to enhance its production capabilities and meet growing demand.

- July 2024: Challenge Butter, the flagship brand of Challenge Dairy Products, has launched national distribution for its Spreadable Lactose Free Clarified Butter with Canola Oil. Formulated specifically for individuals with lactose intolerance, it removes lactose and milk solids while retaining the rich flavor and versatility of clarified butter.

- January 2024: Upfield, under its Flora Plant brand, launched the world's first plastic-free, recyclable paper tub for butters and spreads. This innovative packaging was initially introduced in Austria, marking a significant step toward sustainable solutions in the food industry.

Table of Contents for Lactose-Free Butter Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising prevalence of lactose intolerance and dairy allergies globally

- 4.2.2Expansion of clean-label and natural ingredient trends in dairy

- 4.2.3Growing health consciousness and demand for digestive-friendly dairy products

- 4.2.4Increasing vegan and flexitarian consumer adoption of lactose-free options

- 4.2.5Premium pricing acceptance among health-focused premium segments

- 4.2.6Product innovation in taste and texture matching traditional butter

- 4.3Market Restraints

- 4.3.1Limited consumer awareness in non-urban and emerging markets

- 4.3.2Perception of inferior taste or mouthfeel versus regular butter

- 4.3.3Shorter shelf life due to processing sensitivities

- 4.3.4Stringent food safety and labeling compliance burdens

- 4.4Supply Chain Analysis

- 4.5Regulatory Landscape

- 4.6Porter's Five Forces

- 4.6.1Bargaining Power of Buyers/Consumers

- 4.6.2Bargaining Power of Suppliers

- 4.6.3Threat of New Entrants

- 4.6.4Threat of Substitute Products

- 4.6.5Intensity of Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Product Type

- 5.1.1Spreadable Butter

- 5.1.2Non-Spreadable Butter

- 5.2By Source

- 5.2.1Cow Milk

- 5.2.2Other Milk Source (Goat, Buffalo, Sheep)

- 5.3By Distribution Channel

- 5.3.1Off-Trade

- 5.3.1.1Supermarkets/Hypermarkets

- 5.3.1.2Convenience Stores

- 5.3.1.3Online Retail Stores

- 5.3.1.4Other Distribution Channels

- 5.3.2On-Trade

- 5.4By Region

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.1.4Rest of North America

- 5.4.2Europe

- 5.4.2.1United Kingdom

- 5.4.2.2Germany

- 5.4.2.3France

- 5.4.2.4Spain

- 5.4.2.5Italy

- 5.4.2.6Netherlands

- 5.4.2.7Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Thailand

- 5.4.3.7Rest of Asia-Pacific

- 5.4.4South America

- 5.4.4.1Brazil

- 5.4.4.2Argentina

- 5.4.4.3Rest of South America

- 5.4.5Middle East and Africa

- 5.4.5.1Saudi Arabia

- 5.4.5.2United Arab Emirates

- 5.4.5.3South Africa

- 5.4.5.4Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1Arla Foods amba

- 6.4.2Challenge Dairy Products, Inc.

- 6.4.3Upfield Canada Inc.

- 6.4.4Valio Ltd

- 6.4.5Fonterra Co-operative Group

- 6.4.6Agropur Co-operative

- 6.4.7Lactalis Group

- 6.4.8Redwood Hill Farm & Creamery (Green Valley)

- 6.4.9Kraft Heinz Co.

- 6.4.10Land O'Lakes, Inc.

- 6.4.11General Mills Inc.

- 6.4.12Hain Celestial Group

- 6.4.13Fage International S.A.

- 6.4.14DMK Deutsches Milchkontor GmbH

- 6.4.15Parmalat S.p.A.

- 6.4.16Butterfields Butter LLC

- 6.4.17Molkerei Biedermann AG

- 6.4.18OMIRA GmbH

- 6.4.19Organic Valley

- 6.4.20Miyoko's Creamery

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Global Lactose-Free Butter Market Report Scope

The lactose free butter market is segmented by type, by distribution channel and by geography. By type, the market is segmented into salted and unsalted butter. By distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, convenience store, online retail stores and others. Furthermore, the report also takes into consideration the market for gummy vitamins in established and emerging economies, including North America, Europe, Asia-Pacific, South America, and Middle East & Africa.