West Africa Shea Butter Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

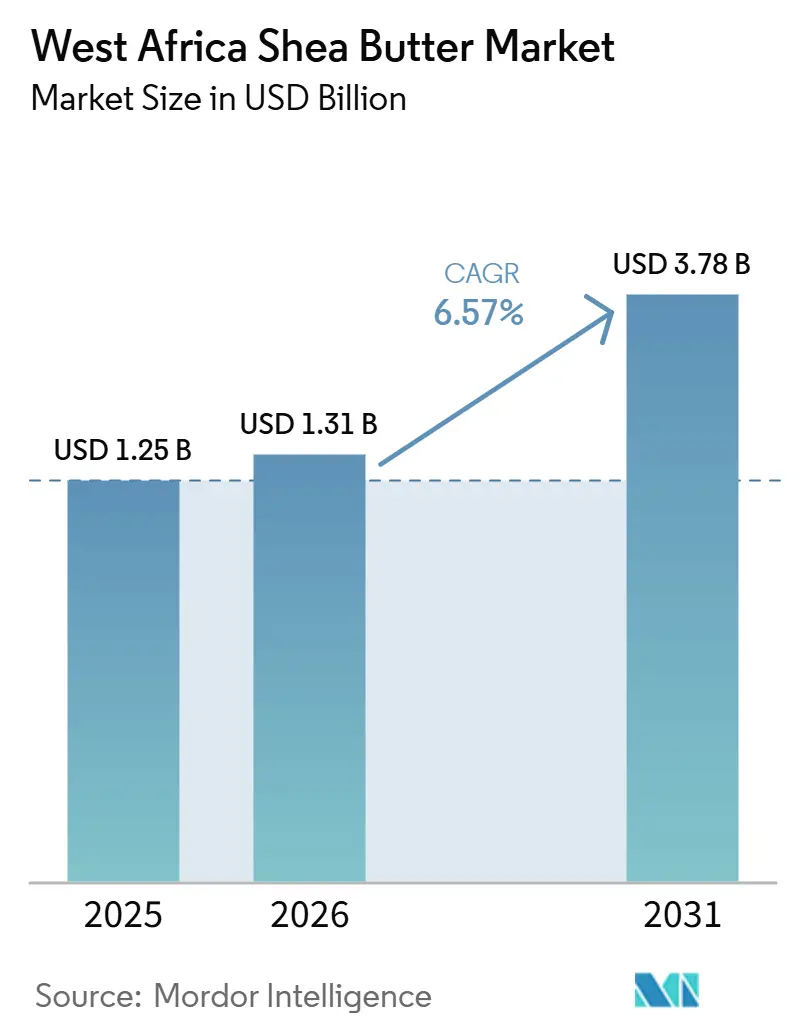

| Base Year Market Size (2025) | USD 1.25 Billion |

| Market Size (2026) | USD 1.31 Billion |

| Market Size (2031) | USD 3.78 Billion |

| Growth Rate (2026 - 2031) | 6.57% CAGR |

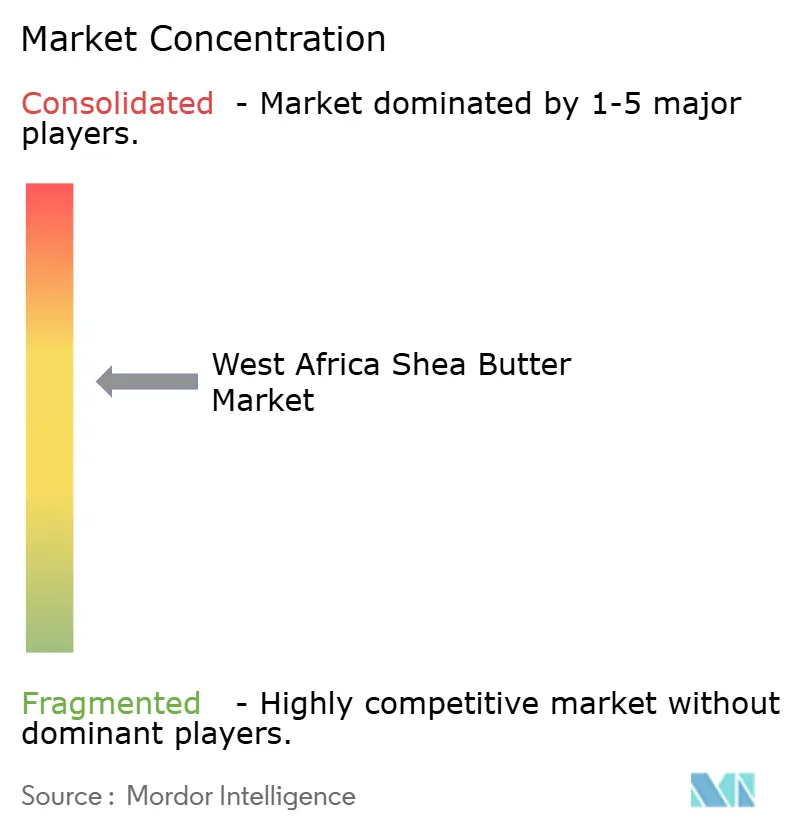

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

West Africa Shea Butter Market Analysis by Mordor Intelligence

The West Africa Shea Butter market size was valued at USD 1.25 billion in 2025 and is estimated to grow from USD 1.31 billion in 2026 to reach USD 3.78 billion by 2031, at a CAGR of 6.57% during the forecast period (2026-2031). The West Africa Shea Butter market is gaining support from global buyers that are shifting toward plant-based ingredients in both cosmetics and food applications, which is widening the demand base beyond its traditional skincare use. Demand also strengthened after the cocoa supply shock in 2024 and 2025 pushed confectionery manufacturers to use shea-derived cocoa butter equivalents more actively to protect product margins and maintain texture consistency. The West Africa Shea Butter market is also being reshaped by export controls on raw shea nuts across key producing countries, which are pushing more value addition into origin markets and changing the balance between nut exports and butter exports. Certified and traceable supply is becoming more important because major buyers now need clearer proof on sustainability, wild collection practices, and supply chain visibility, especially in Europe. Climate variability remains a constraint for the West Africa Shea Butter market because irregular wet seasons and the long maturity period of shea trees limit how quickly supply can respond to stronger global demand.

Key Report Takeaways

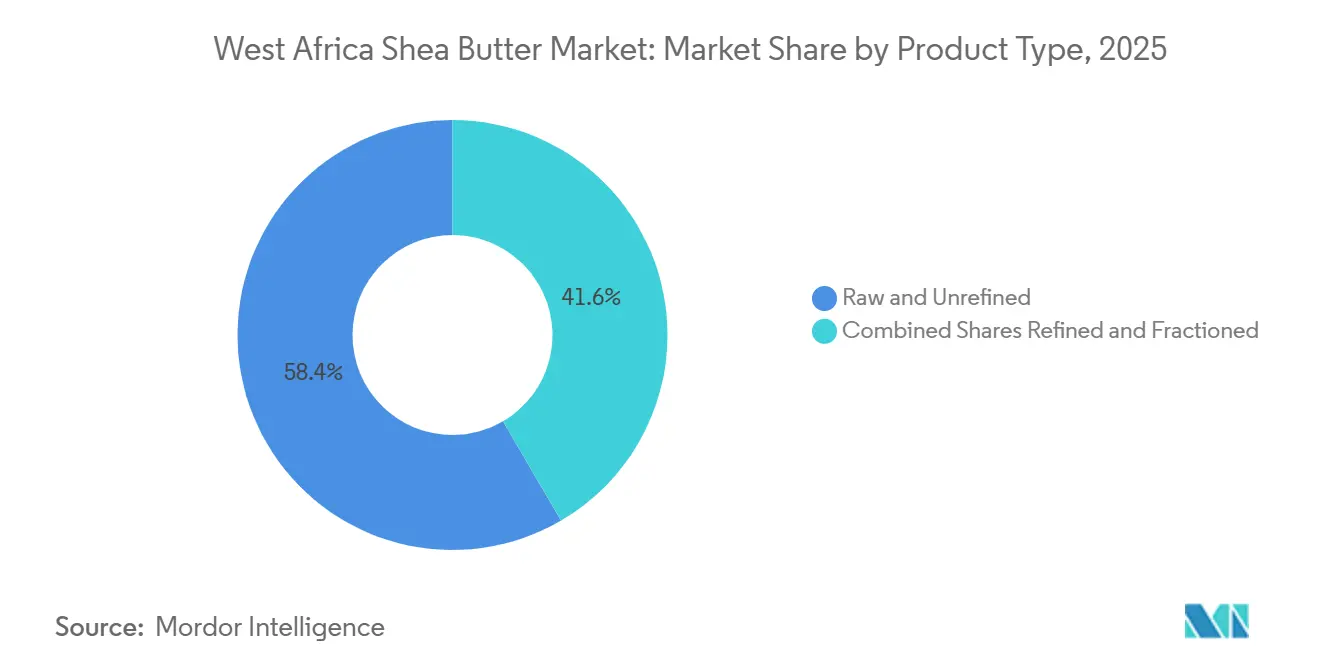

- By type, raw and unrefined held 58.42% of the West Africa Shea Butter market share in 2025, while unrefined is projected to expand at an 8.21% CAGR through 2031.

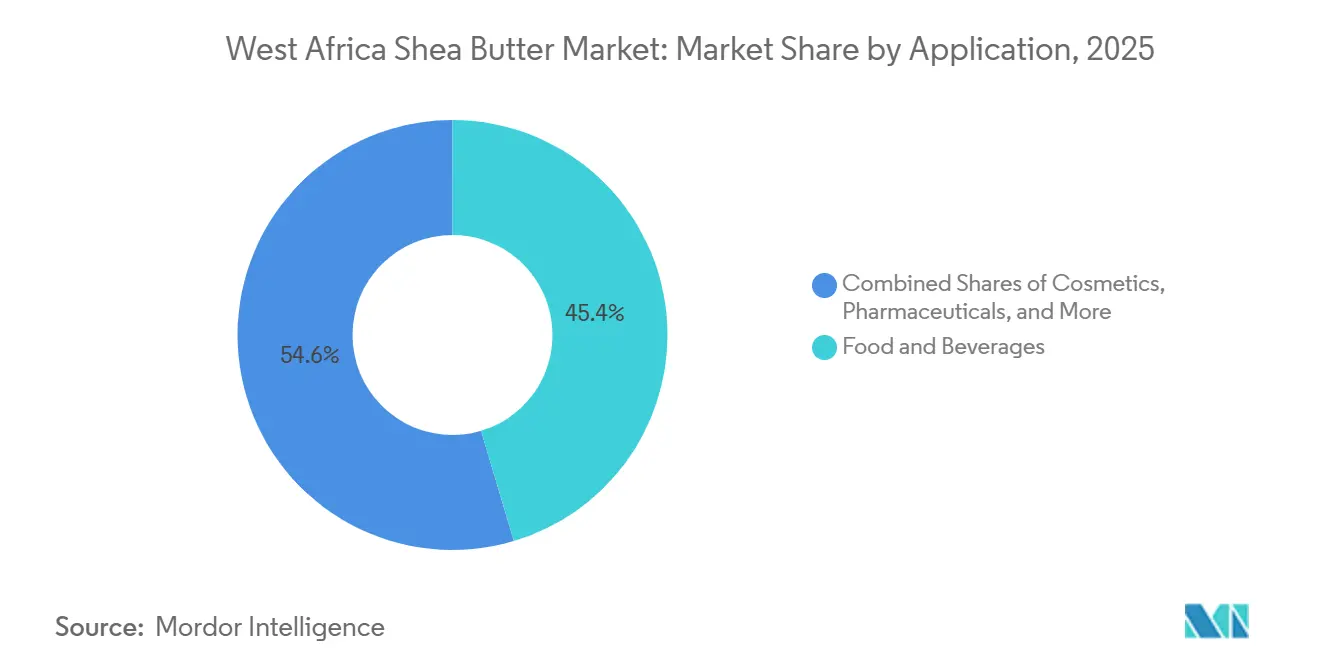

- By application, food and beverages accounted for 45.38% of the West Africa Shea Butter market size in 2025, while cosmetics and personal care is forecast to grow at a 7.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

West Africa Shea Butter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion Of Clean-Label And Plant-Based Beauty Formulations | +1.5% | Global, led by EU and North America with growing APAC uptake | Medium term (2-4 years) |

| Cocoa Butter Equivalent Demand In Confectionery And Food Processing | +1.2% | EU and North America, with spill-over to APAC confectionery hubs | Medium term (2-4 years) |

| Processing Localization And Value Retention In Origin Markets | +1.0% | Ghana, Nigeria, Burkina Faso | Long term (≥ 4 years) |

| Traceability Premium For Certified West African Supply | +0.8% | EU, UK, North America | Long term (≥ 4 years) |

| Preference For Sustainable And Ethically Sourced Raw Materials | +0.7% | Global, concentrated in EU and North America | Medium term (2-4 years) |

| Improved Pit-Fermentation And Mechanised Presses Boosting Supply Quality | +0.5% | West Africa, especially Ghana, Burkina Faso, Nigeria | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion Of Clean-Label And Plant-Based Beauty Formulations

The West Africa Shea Butter market is benefiting from a steady move by skincare and haircare brands toward simpler ingredient lists and plant-based inputs. Buyers in Europe and North America are using more shea butter because unrefined material retains triterpene alcohols, tocopherols, and phenolic compounds that support moisturization and anti-inflammatory performance in finished products. This makes unrefined shea harder to replace at the same cost with synthetic emollients when brands want both functional performance and a natural ingredient story. The shift is also changing buying behavior because brands are now asking for certified and traceable supply rather than standard commodity-grade material, which reduces open-market availability and favors contracted sourcing programs[1]Source: Centre for the Promotion of Imports, “The European Market Potential for Nilotica Shea Butter,” CBI, cbi.eu. The West Africa Shea Butter market is therefore seeing stronger demand not only for volume, but also for premium grades that carry clear sustainability and sourcing credentials.

Cocoa Butter Equivalent Demand In Confectionery And Food Processing

The West Africa Shea Butter market is also being supported by the rise in shea-based cocoa butter equivalents in confectionery and food processing. Cocoa supply stress in West Africa lifted cocoa butter prices sharply in 2024 and 2025, which pushed manufacturers to look for technically reliable alternatives that could hold texture and product quality. Research published in Food Biophysics showed that shea butter stearin blends can maintain solid fat content and sensory properties at controlled substitution ratios, which supports larger commercial use in chocolate applications. The FDA strengthened this demand path when it issued a GRAS "No Questions" letter in July 2024 for shea stearin, which reopened a regulated growth path in North American food use after a long gap[2]Source: U.S. Food and Drug Administration, “GRAS Notice Inventory, Shea Stearin,” FDA, fda.gov. The West Africa Shea Butter market is gaining most from this shift in processors that can produce refined and fractionated grades, especially stearin, at food-grade standards.

Processing Localization And Value Retention In Origin Markets

The West Africa Shea Butter market is being altered by policy moves that aim to keep more value inside producing countries. Governments in several producing markets have restricted or discouraged raw nut exports since late 2024, which reflects a clear preference for exporting processed butter instead of lower-value kernels[3]Source: PBS NewsHour, “Nigeria Bans Exports of Raw Shea Nuts Used for Cosmetic Products,” PBS NewsHour, pbs.org. This policy direction is encouraging new refinery, warehousing, logistics, and skills investments in origin countries, especially Ghana and Nigeria. AAK’s February 2026 agreement with Ghana’s Ministry of Food and Agriculture added USD 90 million to this transition and tied the investment to local processing, supply chain infrastructure, and skills development. The West Africa Shea Butter market is likely to reward buyers with long-term sourcing relationships because spot access to raw nuts is becoming less dependable as more butter extraction happens near origin.

Traceability Premium For Certified West African Supply

The West Africa Shea Butter market is moving toward a more visible premium for traceable and certified supply. Buyers are asking for standards that go beyond a basic fair-trade claim and include proof of wild harvesting practices, environmental stewardship, and product-level traceability. FairWild certification became more important after AAK’s Kolo Nafaso program received that status in October 2025, and the accreditation was later extended to the company’s personal care shea-based emollients portfolio in March 2026. This supports a higher-value supply tier because certified grades can help buyers meet sourcing disclosure needs while also supporting product claims in cosmetics and personal care. The West Africa Shea Butter market is therefore seeing stronger competition for organized sourcing networks that can link women collectors, cooperatives, processors, and export buyers through one auditable chain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Nut Export Restrictions Disrupting Trade Flows | -0.7% | Ghana, Nigeria, Burkina Faso, Mali, Côte d'Ivoire, Togo | Short term (≤ 2 years) |

| Seasonal Supply Tightness And Long Shea Tree Maturity Cycles | -0.5% | West Africa, across producing countries | Long term (≥ 4 years) |

| Quality Inconsistency And Adulteration In Fragmented Collection Networks | -0.4% | Nigeria, Mali, Togo | Medium term (2-4 years) |

| High Compliance Cost For Organic, Fairtrade, And Food-Safety Standards | -0.3% | Global, with origin burden concentrated in West Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw Nut Export Restrictions Disrupting Trade Flows

The West Africa Shea Butter market is facing short-term disruption because raw nut export restrictions are moving faster than local processing capacity in several countries. Nigeria’s export ban shows the main problem clearly because the policy was meant to support domestic processing, but early implementation left many collectors with fewer immediate buyers during the harvest season. This raises procurement risk for international buyers that used to depend on flexible nut purchases and then process material outside the region. It also raises working capital needs because buyers now need longer-term contracts for butter supply instead of open-market nut purchases. The West Africa Shea Butter market will remain exposed to this pressure until new extraction and refining capacity can absorb a larger share of local harvests in real time.

Seasonal Supply Tightness And Long Shea Tree Maturity Cycles

The West Africa Shea Butter market also remains limited by the biology of the shea tree and by weather volatility across the shea belt. Shea trees typically need 15 to 20 years before they reach bearing maturity, which means supply cannot expand quickly even when demand improves. Irregular wet seasons are already affecting nut development and harvest timing, which reduces annual supply predictability and increases seasonal price swings for buyers that rely on spot volumes. This matters because the parkland production model does not allow the kind of rapid plantation-style expansion seen in other tropical oils. The West Africa Shea Butter market is therefore likely to see continued competition for multi-season supply contracts as buyers try to protect themselves from repeated seasonal shortages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Raw Form Holds Value, Fractionation Broadens Use

Raw and unrefined shea butter held 58.42% of market value in 2025, which made it the largest type in the West Africa Shea Butter market. This lead reflects sustained demand from cosmetics buyers that want the full unsaponifiable profile because it supports emollient, antioxidant, and skin barrier functions that are reduced by heavier processing. Refined material is also the fastest-growing type, with the West Africa Shea Butter market size for this segment projected to rise at an 8.21% CAGR through 2031. This combination of scale and growth shows that buyers are treating unrefined shea as both a volume material and a premium ingredient linked to natural positioning and traceable sourcing.

Refined shea butter serves applications where color, odor, and food-grade consistency matter more than a full natural profile. That keeps it relevant in confectionery, neutral cosmetic bases, and other uses where technical performance must remain stable across large batches. Fractionated shea has become more important because stearin is being used more actively in cocoa butter equivalent formulations, and published research supports its functional compatibility at controlled blend ratios. The West Africa Shea Butter market is therefore creating more value for processors that can handle extraction, refining, and fractionation close to origin rather than shipping lower-value raw material abroad.

By Application: Food Supports Volume, Cosmetics Lifts Premium Demand

Food and beverages accounted for 45.38% of the 2025 value, which made it the largest application in the West Africa Shea Butter market. The segment benefits from strong demand for refined and fractionated shea, especially in confectionery, where cocoa butter substitution became more attractive after cocoa price pressure intensified in 2024 and 2025. The West Africa Shea Butter market size for food-linked refined and fractionated output should remain important because this application absorbs large commercial volumes. Pharmaceutical use is smaller, but it is still supporting investment in better food-safety and quality systems as buyers ask for more controlled excipient and topical-use inputs.

Cosmetics and personal care is the fastest-growing application in the West Africa Shea Butter market, with a 7.77% CAGR through 2031. Brands are using shea more deliberately as a main functional ingredient in skincare, haircare, and lip care rather than as a background carrier oil. This is helping certified unrefined grades because premium cosmetic channels increasingly ask for FairWild, Fairtrade, or organic compliance when they source from West Africa. Industrial use remains smaller, but it still provides an outlet for stearin and olein fractions that come out of broader processing activity.

Geography Analysis

Ghana holds the strongest competitive position in the West Africa Shea Butter market because it combines processing capacity, export organization, and a wide certification base. The country also has one of the most developed cooperative systems in the region, which helps global buyers secure traceable supply through structured sourcing programs. Ghana’s policy direction now supports more value-added output because the government has backed stronger local processing and signed a USD 90 million agreement with AAK to support factories, logistics, warehousing, and skills development. This makes Ghana a preferred origin for both personal care and food-grade supply. The West Africa Shea Butter market is likely to keep viewing Ghana as the most balanced origin between premium certification and industrial scaling.

Nigeria has the largest shea tree coverage and one of the largest harvest bases in the region, but for many years it captured limited processed value from that position PBS.ORG. The export ban introduced in August 2025 was meant to change that pattern by forcing more local conversion of nuts into butter and other processed forms. That shift creates opportunity for processors, but it also creates near-term risk for collectors when processing capacity and farmgate demand do not rise at the same pace. Burkina Faso remains important because of its strong cooperative base and its long-standing role in certified shea supply for premium export channels.

Mali and Côte d’Ivoire remain important swing origins in the West Africa Shea Butter market because both influence regional availability and buyer routing decisions. Mali’s continued policy restrictions and landlocked trade structure add complexity for exporters that depend on cross-border aggregation and transport links. Côte d’Ivoire is important for a different reason because it sits close to the cocoa value chain, which gives it strategic relevance when shea is used in cocoa butter equivalent applications. Smaller origins such as Togo and Benin remain attractive to niche buyers that need traceable and premium small-batch supply, but climate pressure across the whole shea belt will continue to limit how quickly regional output can rise

Competitive Landscape

The West Africa Shea Butter market has a moderately consolidated processing and export layer, while the collection layer remains highly fragmented across millions of rural women working through cooperatives and local aggregators. This structure gives global processors an advantage because they can combine financing, certification systems, and direct sourcing relationships in ways that smaller entrants struggle to match. AAK, Cargill, and Bunge remain central reference points in the West Africa Shea Butter market because scale, buyer relationships, and origin infrastructure matter as much as pure product quality in this business. The competitive gap is most visible in the middle of the chain, where artisanal groups often lack the capital and equipment needed to move into larger-scale extraction and refining. That leaves room for players that can build organized regional processing while still staying close to cooperative supply networks.

AAK has taken one of the clearest strategic positions in the West Africa Shea Butter market through its Kolo Nafaso sourcing network, FairWild-linked certification work, and the USD 90 million Ghana investment plan announced in 2026. Manorama Industries also moved to deepen its origin presence through its August 2025 agreement with Burkina Faso for a new processing factory. L’Occitane has kept a different but still important strategy by reinforcing long-term cooperative relationships in Burkina Faso that support fair-trade sourcing and community-linked brand positioning. These moves show that companies are not competing only on purchase price, but also on access, traceability, and reliability of origin supply.

Technology is becoming more important in the West Africa Shea Butter market because yield, consistency, and traceability now affect competitiveness directly. Research from the University of Liège shows large differences between traditional extraction and improved mechanical or assisted extraction methods, which means processing technology can change the economics of butter output in a meaningful way. Downstream ingredient companies such as Croda are also helping move value beyond commodity butter by placing shea inside higher-margin cosmetic ingredient portfolios. The West Africa Shea Butter market should therefore continue to reward firms that combine origin relationships, process capability, and premium product positioning in one integrated model.

West Africa Shea Butter Industry Leaders

AAK AB

Cargill, Incorporated

Fuji Oil Holdings Inc.

BASF SE

Olvea Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: AAK extended FairWild certification, obtained at programme level in October 2025, to its full personal care shea-based emollients portfolio, enabling customers to apply verified FairWild claims in consumer communications for both segregated and mass-balance supply chain options.

- February 2026: AAK signed a USD 90 million MoU with Ghana's Ministry of Food and Agriculture to invest in local shea processing, expand the Kolo Nafaso programme to 300,000+ women collectors, establish an innovation academy for SME skills development, and upgrade logistics and warehousing infrastructure.

- August 2025: Manorama Industries Limited signed a Memorandum of Understanding with the Government of Burkina Faso to establish a new factory for shea nut and mango kernel processing through a wholly owned subsidiary, Manorama Burkina Industries SA, as part of a broader Africa-anchored backward integration strategy.

West Africa Shea Butter Market Report Scope

| Raw / Unrefined |

| Refined |

| Fractionated (stearin, olein) |

| Food and Beverages |

| Cosmetics and Personal Care |

| Pharmaceuticals |

| Industrial (bio-lubes, candles, etc.) |

| By Type | Raw / Unrefined |

| Refined | |

| Fractionated (stearin, olein) | |

| By Application | Food and Beverages |

| Cosmetics and Personal Care | |

| Pharmaceuticals | |

| Industrial (bio-lubes, candles, etc.) |

Key Questions Answered in the Report

How large is the West Africa Shea Butter space in 2026 and 2031?

The West Africa Shea Butter market stood at USD 1.31 billion in 2026 and is forecast to reach USD 3.78 billion by 2031 at a 6.57% CAGR.

Which type leads revenue and which type is growing the fastest?

Raw and unrefined led with 58.42% of 2025 value, and unrefined is also the fastest-growing type with an 8.21% CAGR through 2031.

Why is food and beverages important for shea butter suppliers?

Food and beverages held 45.38% of 2025 value because refined and fractionated shea is being used more in confectionery, especially after cocoa price pressure increased interest in substitution.

Which countries matter most in the regional supply chain?

Ghana remains the strongest processing and certification hub, Nigeria has the largest resource base and a stronger domestic processing push, and Burkina Faso remains important for premium cooperative-based supply.

Page last updated on: