Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

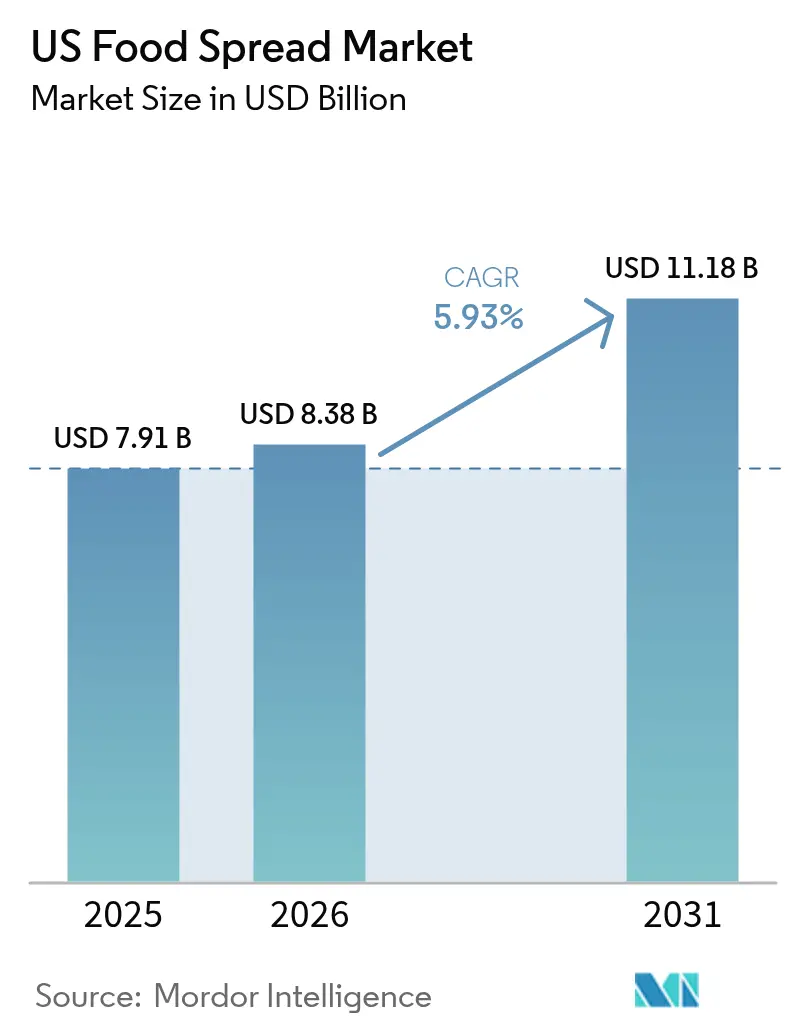

| Base Year Market Size (2025) | USD 7.91 Billion |

| Market Size (2026) | USD 8.38 Billion |

| Market Size (2031) | USD 11.18 Billion |

| Growth Rate (2026 - 2031) | 5.93% CAGR |

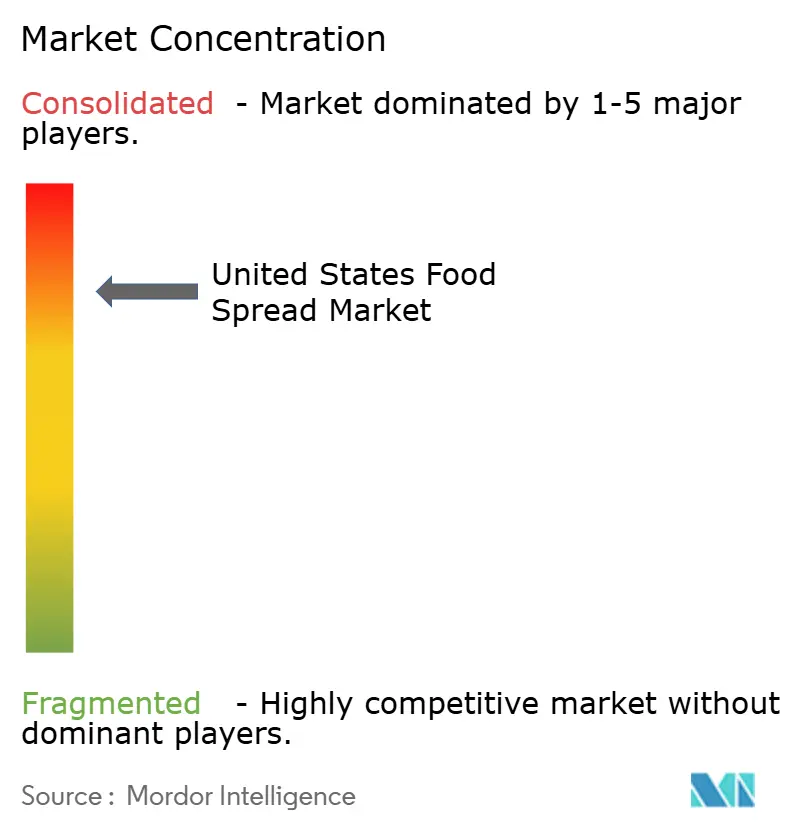

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

US Food Spread Market Analysis by Mordor Intelligence

The United States food spread market size is expected to grow from USD 7.91 billion in 2025 to USD 8.38 billion in 2026 and is forecast to reach USD 11.18 billion by 2031 at 5.93% CAGR over 2026-2031. The market expansion is driven by increasing consumer preference for healthier alternatives, particularly the shift toward peanut-based spreads over traditional options like jam or butter. Consumer behavior demonstrates a clear trend toward premium, organic, and functionally enhanced spreads, supported by growing awareness of nutritional benefits and ingredient transparency. The market growth is further strengthened by consumers adopting low-calorie diets due to lifestyle-related health concerns, along with the development of innovative packaging solutions that improve product accessibility and shelf life. As health consciousness continues to influence purchasing decisions, the market is expected to maintain its growth trajectory, with manufacturers focusing on product innovation and healthier formulations to meet evolving consumer demands.

Key Report Takeaways

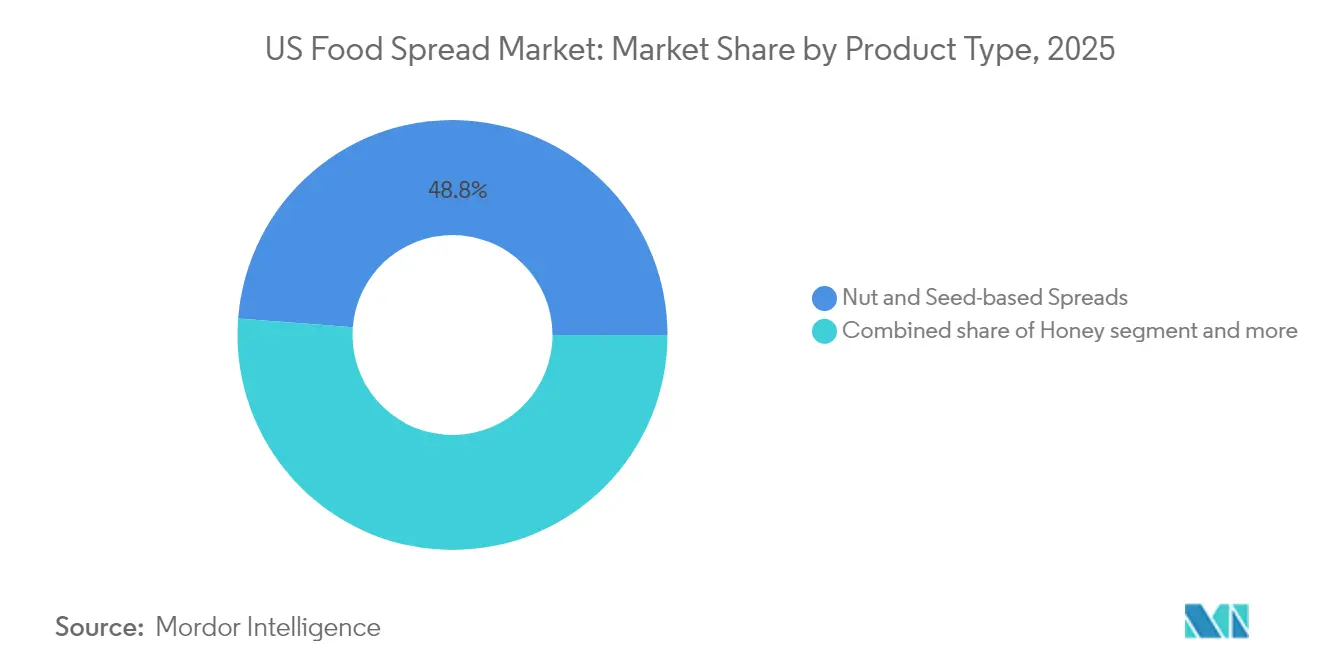

- By product type, nut and seed-based spreads captured 48.77% of food spreads market share in 2025 and are projected to advance at a 6.18% CAGR through 2031.

- By nature, conventional variants retained a 69.42% hold on the food spreads market size in 2025, while the organic segment is accelerating at a 9.45% CAGR between 2026-2031.

- By packaging type, jars dominated with 41.88% share in 2025; sachets and pouches represent the fastest track, expanding 7.21% annually during the forecast window.

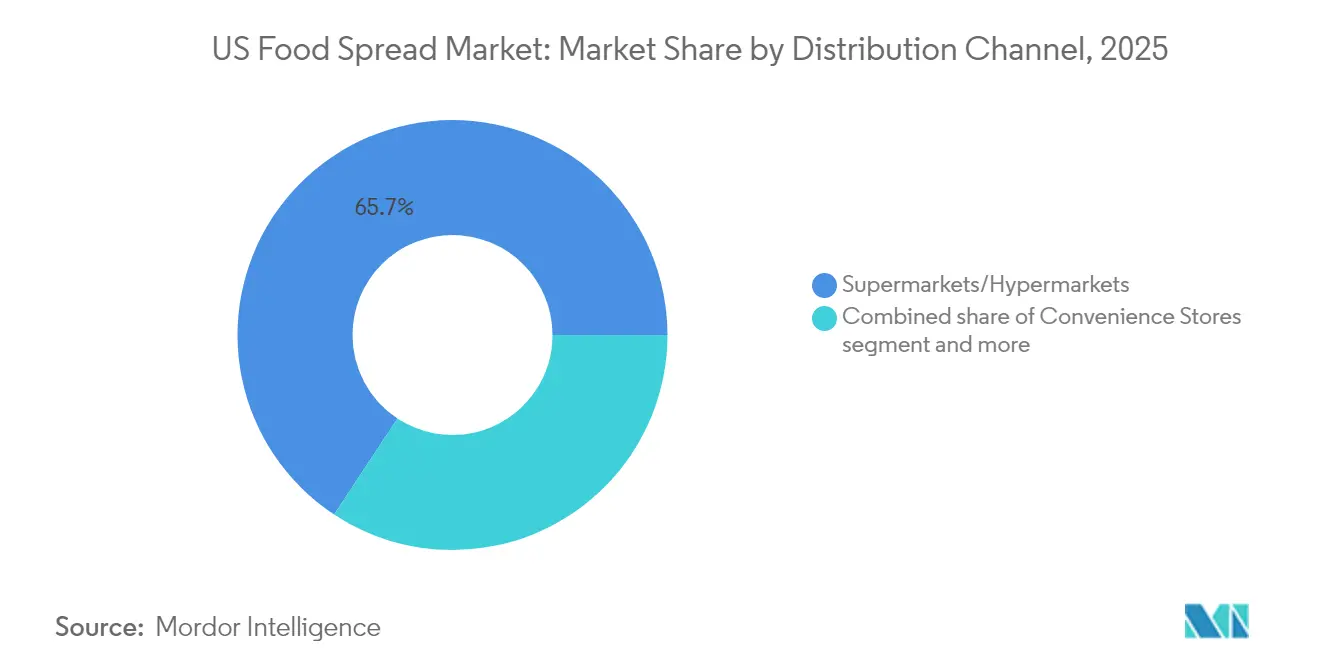

- By distribution channel, supermarkets and hypermarkets accounted for 65.72% of the 2025 market; online retail is registering the highest trajectory at 11.65% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Food Spread Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising health consciousness boosting demand for natural and organic spreads | +1.3% | Nationwide, with early gains in California, Northeast corridor, and Pacific Northwest | Medium term (2-4 years) |

| Increasing consumer preference for convenient and ready-to-eat food options | +1.0% | Urban centers nationwide, particularly strong in New York, Los Angeles, Chicago metropolitan areas | Short term (≤ 2 years) |

| Growing popularity of plant-based and vegan spreads | +1.6% | Coastal states and urban markets, with concentration in California, New York, Washington, Oregon | Long term (≥ 4 years) |

| Expansion of product variety with innovative flavors and formulations | +0.9% | National, with premium positioning in affluent suburban markets across all regions | Medium term (2-4 years) |

| Rising disposable incomes supporting premium and gourmet spread purchases | +0.8% | High-income metropolitan areas, particularly Northeast, West Coast, and affluent Southern markets | Long term (≥ 4 years) |

| Growing awareness about the nutritional benefits of fortified spreads | +0.7% | National, with regulatory support from FDA and state-level health initiatives | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising health consciousness boosting demand for natural and organic spreads

Growing consumer health awareness is fundamentally reshaping food spread formulations in the United States, with natural and organic variants experiencing increased adoption. The FDA's February 2025 food labeling criteria established stricter nutritional standards that disqualify highly sweetened products while enabling nutrient-dense alternatives to qualify for health claims [1]Source: Food & Drug Administration, “Food Labeling: Nutrient Content Claims; Definition of Term Healthy", federalregister.gov. This regulatory change has accelerated product reformulations towards natural and organic ingredients, as demonstrated by As Ever's launch of natural raspberry spreads in March 2025. Consumers are actively seeking natural and organic alternatives to conventional spreads, driven by concerns about artificial ingredients, preservatives, and processed foods. This shift is evident in the growing shelf space dedicated to organic nut butters, fruit spreads without added sugars, and plant-based alternatives in retail stores. Manufacturers are leveraging clean-label positioning to justify premium pricing, with the expanding application of natural sweeteners in food spread formulations reflecting this shift. The demand for clean-label spreads with minimal ingredients has prompted manufacturers to expand their natural and organic product portfolios, contributing to market growth.

Increasing consumer preference for convenient and ready-to-eat food options

The rise in fast-paced lifestyles across the United States has expanded the role of food spreads beyond traditional uses, aligning with busy lifestyles and on-the-go snacking occasions. The demand for convenience is particularly significant in dual-income households where time constraints increase the appeal of easy-to-use products. This trend is supported by rising household incomes, as evidenced by the U.S. Census Bureau's report of a 4.0% increase in real median household income to USD 80,610 in 2023 from USD 77,540 in 2022 [2]Source: U.S. Census Bureau, “Income in the United States: 2023”, census.gov. Product innovations featuring multiple applications, such as spreads that function as dips, toppings, or cooking ingredients, have broadened the category's appeal across different meal occasions and consumer groups. Food spreads, including nut butter, chocolate spreads, and fruit preserves, offer convenient breakfast and snacking options that require minimal preparation time. The versatility of these products in various applications, from sandwiches to baked goods, makes them an attractive choice for consumers seeking quick meal solutions. This adaptability, combined with longer working hours and increasingly busy schedules, has positioned food spreads as essential items in American households, particularly for those requiring convenient and ready-to-eat food options.

Growing popularity of plant-based and vegan spreads

The plant-based movement is transforming the United States food landscape, with vegan food spreads emerging as a rapidly growing segment in the market. This growth extends beyond strict vegans to include flexitarians and health-conscious consumers seeking alternatives to traditional dairy-based spreads. Retailers are expanding their plant-based offerings, with products like almond butter, cashew spreads, and chickpea-based alternatives gaining significant market share. According to World Population Review, vegans constituted approximately 1.5% of the U.S. population in 2025, indicating a substantial consumer base for plant-based products [3]Source: World Population Review, "Veganism by Country 2025", worldpopulationreview.com. The increasing adoption of these alternatives is primarily driven by health consciousness, environmental awareness, and animal welfare concerns among consumers. Recent technological advancements in ingredient formulation have significantly enhanced the taste and texture profiles of plant-based spreads, enabling them to compete effectively with conventional alternatives based on sensory attributes rather than ethical considerations alone. These innovations, coupled with enhanced nutritional profiles, continue to attract both vegan and flexitarian consumers, contributing to the overall growth of the plant-based spreads market in the United States.

Expansion of product variety with innovative flavors and formulations

Flavor innovation is accelerating beyond traditional profiles, with manufacturers introducing bold combinations that cater to adventurous consumer palates and cultural fusion trends. The market growth is primarily driven by better-for-you options, plant-based ingredients, unique flavor combinations, varied textures, and natural clean labels, reflecting a comprehensive approach to product differentiation. Companies are developing distinctive combinations like chocolate-hazelnut spreads, fruit-based variants, and specialty nut butters to attract health-conscious consumers, while also incorporating functional ingredients such as probiotics, protein fortification, and superfoods to enhance nutritional value. For instance, in May 2024, Jif introduced its first significant flavor innovation in nearly 10 years with a chocolate and peanut butter spread, containing 50% less sugar compared to the leading hazelnut spread with cocoa. The market has witnessed an increase in plant-based and organic spreads, catering to the rising vegan and health-focused population, while the introduction of sugar-free, low-calorie, and allergen-free variants has expanded the market reach to consumers with specific dietary requirements. These product developments focus on creating sensory experiences and emotional connections, which significantly influence consumer purchase decisions in the food spread segment.

Restraints Impact Analysis*

| Restraint | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Intense competition from alternative snack and condiment options | -0.9% | National, particularly intense in mature markets like Midwest and Northeast | Short term (≤ 2 years) |

| Regulatory challenges regarding labeling and health claims | -0.7% | Federal level with state variations, particularly stringent in California, New York, and health-focused states | Medium term (2-4 years) |

| Consumer concerns over sugar, fat, and additive content in spreads | -1.2% | National, with heightened awareness in health-conscious markets like California, Colorado, Vermont | Long term (≥ 4 years) |

| Fluctuations in raw material prices affecting production costs | -1.0% | National impact, with supply chain vulnerabilities affecting Midwest manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intense competition from alternative snack and condiment options

Significant competition emerges from diverse snacking alternatives and condiment options, creating substantial pressure on traditional spread manufacturers. The market faces competition from protein bars, ready-to-eat snacks, functional beverages, nuts, fresh fruits, and alternative condiments like hummus, guacamole, and plant-based dips. Health-conscious consumers increasingly gravitate toward specialized snacking solutions that offer enhanced convenience and improved nutritional profiles over conventional spread applications. The rise of quick-service restaurants and ready-to-eat meals further impacts the at-home consumption of traditional spreads. This shift in consumer preferences toward alternative snacking formats and healthier options directly affects the consumption patterns of conventional spreads. The competitive landscape intensifies with the introduction of innovative spreads featuring unique flavors and health-focused formulations, compelling established manufacturers to adapt their product offerings. These market dynamics collectively create significant substitution pressure and pose a notable restraint on the expansion of the food spreads market, requiring manufacturers to continuously evolve their strategies to maintain market share.

Consumer concerns over sugar, fat, and additive content in spreads

Rising health consciousness and diabetes-related concerns are reshaping the United States food spreads market, as consumers increasingly scrutinize traditional spread formulations due to their high sugar and fat content. This heightened awareness is supported by concerning health statistics, including the US Department of Health and Human Services' report of 22.4 diabetes-related deaths per 100,000 people in 2023 [4]Source: U.S. Department of Health & Human Services, “National Diabetes Statistics Update 2024”, hhs.gov. Consumer behavior, particularly among health-conscious millennials and Generation Z, reflects a growing trend of carefully examining product labels and actively reducing intake of spreads high in sugar and saturated fats. These shifts have created significant challenges for manufacturers, who must now balance consumer health demands with taste expectations. While companies are responding by reformulating products with natural ingredients and developing low-sugar, low-fat alternatives, many consumers report dissatisfaction with the flavor profiles of these healthier options. The pressure for healthier formulations comes not only from consumer preferences but also from regulatory bodies, compelling manufacturers to innovate while maintaining product appeal. This complex dynamic of health consciousness, regulatory requirements, and consumer taste preferences continues to impact market growth and product development strategies in the food spreads industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Nut and Seed-Based Spreads Dominate Innovation

Nut and seed-based spreads command a 48.77% market share in 2025 and are projected to grow at a 6.18% CAGR during 2026-2031. The category's dominance reflects its alignment with health trends and protein demand, allowing manufacturers to implement premium pricing strategies. Consumer shift toward plant-based protein sources has increased demand for almond, cashew, and sunflower seed spreads. Justin's recent expansion in March 2025 includes a new crunchy peanut butter formulation featuring a no-stir consistency and a specific grinding process that preserves ingredient quality.

The market's innovation landscape focuses on premium positioning and health-conscious reformulations across various spread categories. While honey spreads benefit from their natural positioning, fruit-based spreads experience moderate growth by appealing to consumers seeking reduced sugar alternatives. New processing technologies are being developed to preserve the nutritional content of spreads while extending shelf life. The market also witnesses increased product development in specialized dietary segments, including keto-friendly and allergen-free spreads. The incorporation of functional ingredients and superfoods into spreads further enhances their nutritional profile and appeals to health-conscious consumers seeking additional health benefits.

By Nature: Organic Segment Accelerates Despite Conventional Dominance

Conventional nut and seed-based spreads dominate the market with a 69.42% share in 2025, primarily due to established consumer preferences and price sensitivity. The segment's widespread availability and competitive pricing continue to drive its market leadership position. These traditional spreads maintain their strong market presence through established distribution channels and consumer familiarity with the products. The conventional segment demonstrates consistent market stability through diverse product offerings and flavor innovations. Additionally, economies of scale in production and established supplier relationships contribute to maintaining attractive price points in the market.

Organic spreads are experiencing significant growth at 9.45% CAGR (2026-2031), driven by increasing consumer preference for premium, health-focused alternatives. The segment benefits from USDA organic certification standards, which enhance consumer confidence and justify price premiums that offset higher production and certification costs. The growth is further supported by expanding retail distribution networks and increasing shelf space allocation in mainstream supermarkets. The organic segment also benefits from rising consumer awareness about environmental sustainability and clean-label ingredients, particularly among millennial and Gen Z consumers.

By Distribution Channel: Supermarkets Dominate While Online Retail Surges

Supermarkets and hypermarkets dominate the market with a 65.72% share in 2025, driven by their extensive product assortments, competitive pricing, and established consumer shopping patterns favoring in-person food selection. These retail formats benefit from economies of scale, allowing them to offer diverse product ranges while maintaining profit margins. Their ability to provide one-stop shopping experiences continues to attract consumers who value convenience and product variety. While convenience stores maintain a steady presence through impulse purchases and single-serve formats, online retail exhibits remarkable growth at 11.65% CAGR during 2026-2031, reflecting increased digital adoption and convenience preferences.

The distribution landscape also includes specialty food stores, and health food retailers, each developing specialized product assortments for specific consumer needs. These specialized retailers focus on premium, organic, and health-focused products, creating distinct market niches. This retail transformation has led to the adoption of omnichannel strategies, which have become crucial for manufacturers seeking comprehensive market coverage and enhanced consumer accessibility across all distribution channels. The integration of physical and digital retail platforms enables retailers to capture consumer data and provide personalized shopping experiences, while manufacturers benefit from increased visibility and market penetration across multiple touchpoints.

By Packaging Type: Jars Lead While Sachets/Pouches Show Fastest Growth

Jars dominate the nut and seed-based spreads market with a 41.88% share in 2025, as consumers prefer traditional packaging that preserves product quality while enabling portion control and resealing convenience. Tubs maintain a steady presence, while other formats, including cups, cans, and tetra packs, serve specialized distribution channels. The widespread acceptance of jars stems from their proven track record in maintaining product freshness and preventing spoilage, particularly important for preserving the natural oils in nut-based spreads. Additionally, the transparent nature of glass jars allows consumers to visually inspect the product before purchase, enhancing trust and confidence in the brand.

Sachets/pouches demonstrate the fastest growth at 7.21% CAGR during 2026-2031, driven by on-the-go consumption patterns and portion control benefits that align with health-conscious consumer behavior. This format caters to individual and small household needs, while PET jars gain traction due to price sensitivity considerations, with sustainability increasingly influencing packaging decisions across all formats. The rise in e-commerce sales has further boosted the demand for sachets and pouches, as their lightweight nature reduces shipping costs. The format's convenience factor particularly resonates with millennials and Gen Z consumers, who prioritize portable and easy-to-use packaging solutions in their purchasing decisions.

Geography Analysis

The market for spreads exhibits robust growth driven by evolving consumer preferences toward health-conscious, convenient, and premium food options. The industry benefits from established distribution infrastructure, strong brand loyalty, and increasing acceptance of innovative formulations that cater to dietary restrictions and wellness trends. Organic spreads represent a rapidly growing category segment, supported by comprehensive USDA certification standards that enhance consumer confidence in product quality and sourcing practices. Manufacturers like crofter's organic have responded to this trend by expanding their organic product portfolios and investing in sustainable sourcing practices. Additionally, the market sees continuous innovation in packaging designs that emphasize convenience and portion control.

Regional consumption patterns reveal significant variations across the United States. Coastal markets demonstrate higher adoption rates for premium, organic, and plant-based alternatives, while traditional heartland regions maintain preference for established brands and conventional formulations. State-level health initiatives influence institutional demand for nutritious spread options, further shaping market dynamics. Market research indicates a gradual shift in consumer behavior across all regions, with increasing awareness of health benefits driving product selection. The influence of local food cultures and dietary preferences continues to impact regional product development strategies.

E-commerce transformation continues to accelerate across all regions in the spreads category. Urban markets lead digital adoption, while suburban and rural areas show increasing acceptance of online grocery shopping for shelf-stable products like spreads. This digital shift enhances market accessibility and distribution efficiency across diverse geographical segments. Mobile applications and subscription-based delivery services are becoming increasingly important channels for spread products. The integration of digital platforms has also enabled better inventory management and demand forecasting for retailers and manufacturers.

Regulatory Landscape

Food spreads sold in the United States are regulated primarily under the Federal Food, Drug, and Cosmetic Act and implemented through FDA rules on labeling and standards of identity, with USDA requirements also applicable to certain fat-based products. Standards of identity affect dairy and cheese spreads, including pasteurized process cheese spread requirements under 21 CFR 133.179, which set composition and performance attributes (a homogeneous, spreadable mass at 70 degrees Fahrenheit) and allow defined emulsifying agents. This framework shapes formulation choices and quality-control programs.

Compliance expectations for traceability and labeling are also tightening. The FSMA Food Traceability Rule requires covered entities that manufacture, process, pack, or hold foods on the Food Traceability List to maintain key data elements at defined critical tracking events, which raises the bar for record-keeping and recall readiness. Separately, the Food Labeling Modernization Act of 2026 (H.R. 8385) was introduced with provisions aimed at strengthening disclosure of fats on labels, and the FDA Human Foods Program set 2026 priority deliverables that emphasize more data-driven oversight of the food supply chain.

Competitive Landscape

The market for food spreads in United States is characterized by high consolidation, with major players like The J.M. Smucker Company, Ferrero International S.A, Conagra Brands Inc., and Unilever PLC dominating the landscape. These established companies maintain their market positions through extensive distribution networks, substantial marketing investments, and brand equity developed over decades of consumer engagement. The competitive environment is further shaped by private label offerings from major retailers, which compete primarily on price points. Regional manufacturers also contribute to market dynamics by catering to local taste preferences and maintaining strong relationships with regional retailers.

Market competition continues to evolve through strategic acquisitions and facility expansions. For instance, Flora Food Group's acquisition of a new facility in Southwestern Kansas in September 2024 demonstrates this trend. The facility serves as a production center for creams and cream cheeses, catering to markets across the Americas region. Companies are also focusing on product innovation and health-conscious reformulations to address changing consumer preferences. Manufacturing efficiency improvements and supply chain optimization remain key priorities for market participants. The integration of advanced production technologies has enabled companies to maintain quality while improving cost structures.

The market presents opportunities in specialized segments, particularly in allergen-free formulations and dietary-specific products. Emerging brands are successfully challenging traditional players by focusing on niche markets and implementing innovative distribution strategies, including direct-to-consumer capabilities that bypass traditional retail channels while securing higher margins. The growth of e-commerce platforms has provided these specialized manufacturers with expanded market access and improved consumer reach. Consumer demand for transparent ingredient sourcing and sustainable packaging solutions continues to influence product development and marketing strategies in this segment.

US Food Spread Industry Leaders

-

The J.M. Smucker Company

-

Unilever PLC

-

Ferrero International S.A.

-

Conagra Brands Inc.

-

Hormel Foods Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Clean-label reformulation and premiumization continue to create room for growth across core spread categories, especially in nut and seed-based spreads, which already lead the US market by share. In March 2026, The J.M. Smucker Co. expanded the Jif franchise with Jif Simply Unsweetened Creamy, positioned on a three-ingredient formulation. The launch reinforces demand signals for simplified ingredient decks and supports line extensions across pack sizes and channels.

Product-format innovation in convenient packaging remains another commercialization lever, supported by the category's momentum toward portable use occasions. In chocolate and nut-based spreads, localization of manufacturing and ingredient sourcing is increasingly used as a competitive lever to support faster innovation cycles and retailer programs. Ferrero invested USD 75 million to enable US production for Nutella Peanut at its Franklin Park, Illinois facility, and it opened a new production line in May 2026 using US-grown peanuts and hazelnuts. This increases domestic capacity for differentiated flavors and can improve service levels for national retail accounts. Regulatory activity also adds a practical opportunity for brands that can operationalize compliant digital product content, as the FDA Human Foods Program scheduled draft guidance in 2026 related to food labeling for online grocery shopping, increasing the importance of accurate and updated product data across ecommerce and omnichannel retail.

Recent Industry Developments

- May 2026: Ferrero inaugurated a new Nutella production line at the Franklin Park, Illinois facility after a USD 75 million investment to enable US-sourced peanuts and hazelnuts. The expansion increases domestic capacity for Nutella and supports faster supply to national retailers.

- October 2025: Hormel Foods entered a strategic partnership with Forward Consumer Partners for the Justin's brand, transitioning it into a standalone entity owned 51% by Forward and 49% by Hormel. The structure supports dedicated investment and sharper brand focus in premium nut and seed-based spreads while keeping Hormel economically tied to the franchise.

- October 2024: Crofter's Organic launched an organic fruit spread in squeezable pouches at national scale, positioned with real fruit and 33% less sugar than standard preserves. This packaging shift targets portability and portion control, adding competitive pressure on jar-dominant fruit spread formats.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the United States food spreads market is defined as the value of retail and foodservice sales of edible spreads used as toppings or fillings, including fruit spreads, nut and seed spreads, honey, chocolate spreads, and cheese-based spreads.

Scope exclusions: We exclude meat pates, spreads sold mainly as cooking fats, and industrial bulk ingredients that are not sold as consumer-ready spreads.

Segmentation Overview

-

By Product Type

- Honey

- Chocolate-based Spreads

- Fruit-based Spreads

- Nuts and Seed-based Spreads

- Dairy and Cheese Spreads

- Other Product Types

-

By Nature

- Conventional

- Organic

-

By Packaging Type

- Jars

- Tubs

- Sachets/Pouches

- Others

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the market boundaries and build the first draft of the demand and pricing picture across the United States. We rely on public statistics and reference sources such as USDA data, US Census Bureau and Bureau of Labor Statistics series, USITC trade data, and FDA labeling and compliance guidance to understand category definitions and shifts that can affect consumption and pricing.

To pressure-test the above, we also review company annual filings, investor presentations, retailer category pages, and public price listings, along with reputable press coverage of new launches and promotions. Where it helps the model, a paid subscription for company financials and news intelligence is used to standardize revenue cues and timeline events, and a paid patent database is used to track whether innovation themes are rising or fading. These desk sources are illustrative, and many other public and paid references were used to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work is used to confirm what is actually selling, how realized pricing is changing, and which channels are gaining share, since spreads can behave very differently across household use and foodservice. We speak with manufacturers, ingredient and packaging participants, distributors, retail category teams, and foodservice stakeholders across the United States, and then we close gaps from desk findings through follow-up checks and short surveys.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | |

| Mid tier: 49% | Functional/Unit leaders: 33% | |

| Smaller Players: 18% | Managers: 53% |

Market-Sizing & Forecasting

The sizing starts with a top-down build where national demand is reconstructed using category consumption cues and retail turnover signals, then translated into value using observed price points and mix. To keep the totals realistic, we corroborate them with selective bottom-up checks, such as sampled brand and private label volumes by channel, distributor sense-checks, and an ASP times volume approach for key spread types.

A few market fingerprints that shape the model include household penetration and usage frequency for spreads, shifts between branded and private label share, pack size changes, and promo intensity that affects realized pricing. We also monitor input-cost pass-through patterns that show up in shelf prices over time. When a data point is not directly visible, we treat it as a range and narrow it using primary responses and adjacent public indicators, before it is carried into the final worksheet.

For forecasting, we use scenario analysis anchored in observed price progression and expected category volume trends, then align scenarios with expert views on how consumer health preferences and convenience-led snacking are changing. Assumptions are documented at the variable level so the same steps can be repeated in future refreshes without needing proprietary datasets.

Data Validation & Update Cycle

Outputs are validated in several steps, starting with internal consistency checks across value, volume, and implied pricing, followed by variance reviews against public signals such as food CPI movements and retail promotion cycles. When the model indicates a break from expected patterns, we re-check the input trail, confirm the calculation logic, and re-contact relevant interviewees if the change looks structural rather than seasonal.

Before sign-off, the model and narrative go through multi-step analyst review so assumptions, units, and time alignment are consistent across the full report. Reports are refreshed annually, and interim updates are made when material events occur, such as sharp commodity swings or major channel disruptions. Right before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's United States Food Spreads Market Market Size Measured Against Other Published Estimates

Published numbers for US food spreads often do not match, and the differences usually come from what gets counted as a spread, which selling channels are included, and how price is treated over time. Timing also matters because food categories can show quick price swings from promotions and input-cost changes, and those swings alter value sizing even when volumes are steady.

A refresh-led gap is common, where older pricing assumptions and fixed currency timing are carried forward without being re-checked against recent shelf prices and channel mix. In our work, the implied ASP trend is re-validated around the base year using spot checks and interview feedback before totals are finalized. That update cadence is a key reason the 2025 value differs for Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.91 B (2025) | |

| Global Consultancy A | USD 30.40 B (2024) | This figure appears to use a wider boundary that blends spreads with adjacent categories like syrups and some broader spreadable fats, and it also anchors the value to an earlier year where pricing and channel mix are different. |

| Industry Publisher B | USD 5.90 B (2025) | This estimate is closer in size but likely applies a narrower product scope and may lean more heavily on a conservative price realization path, which can understate value when promotions and pack-size shifts are changing the average selling price. |

Taken together, the spread comes mainly from scope control and how price is refreshed at the base year. By keeping inclusions clear and by tying the value build to observable demand and price signals that can be re-checked each year, the market size remains traceable and easier to replicate when new data arrives.

Key Questions Answered in the Report

What is the current size of the U.S. food spreads market?

The food spreads market is valued at USD 8.38 billion in 2026, with a projected rise to USD 11.18 billion by 2031.

Which product type leads the category?

Nut & seed-based spreads hold the largest 2025 share at 48.77% and are forecast to grow 6.18% annually.

How fast is online retail for spreads growing?

Online channels are expanding at a 11.65% CAGR from 2026-2031 as consumers embrace digital grocery shopping.

What packaging innovation is most popular?

Sachets and pouches are the fastest-growing format, advancing 7.21% yearly due to convenience and portion control.

Page last updated on: