Almond Butter Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

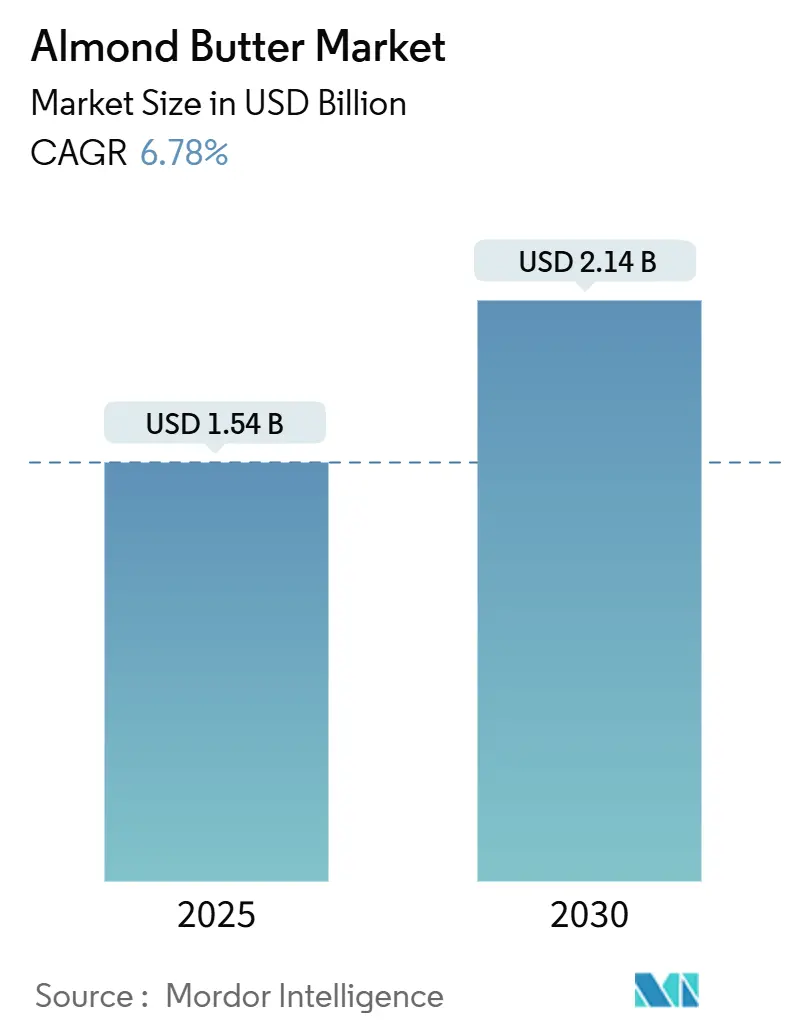

| Market Size (2025) | USD 1.54 Billion |

| Market Size (2030) | USD 2.14 Billion |

| Growth Rate (2025 - 2030) | 6.78% CAGR |

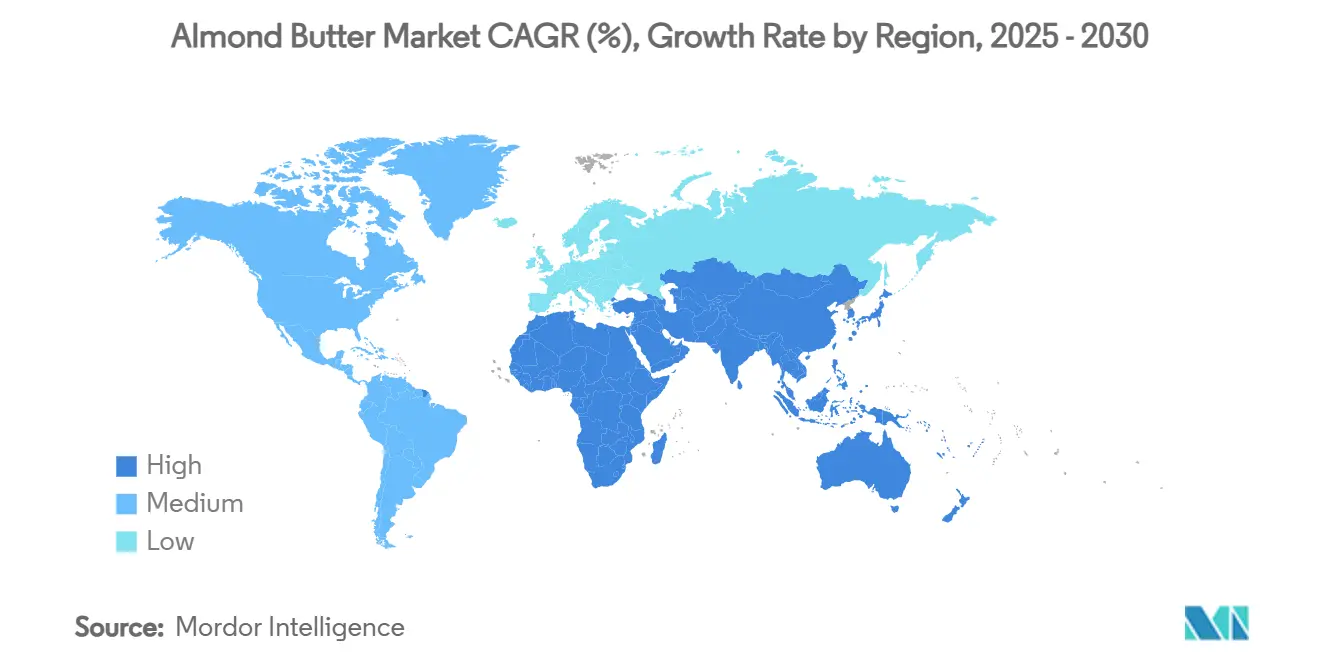

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Almond Butter Market Analysis by Mordor Intelligence

The almond butter market size is estimated to be USD 1.54 billion in 2025 and is forecast to reach USD 2.14 billion by 2030, advancing at a CAGR of 6.78%. Heightened consumer focus on plant-based proteins, escalating concerns over peanut allergies, and the widespread availability of e-commerce grocery channels are sustaining volume growth even as California’s drought-related production challenges tighten raw-nut supply. Besides, North America retains demand leadership by pairing its dominant almond farming base with mature retail distribution, while Asia-Pacific’s rapidly urbanizing middle class is driving the fastest incremental gains. Additionally, product development is tilting toward flavored and organic variants, and brands are increasingly shifting to flexible pouches to balance convenience with sustainability. Competitive intensity remains moderately fragmented, enabling smaller entrants that emphasize clean labels and direct-to-consumer (DTC) fulfilment to chip away at shelf space traditionally held by legacy spreads.

Key Report Takeaways

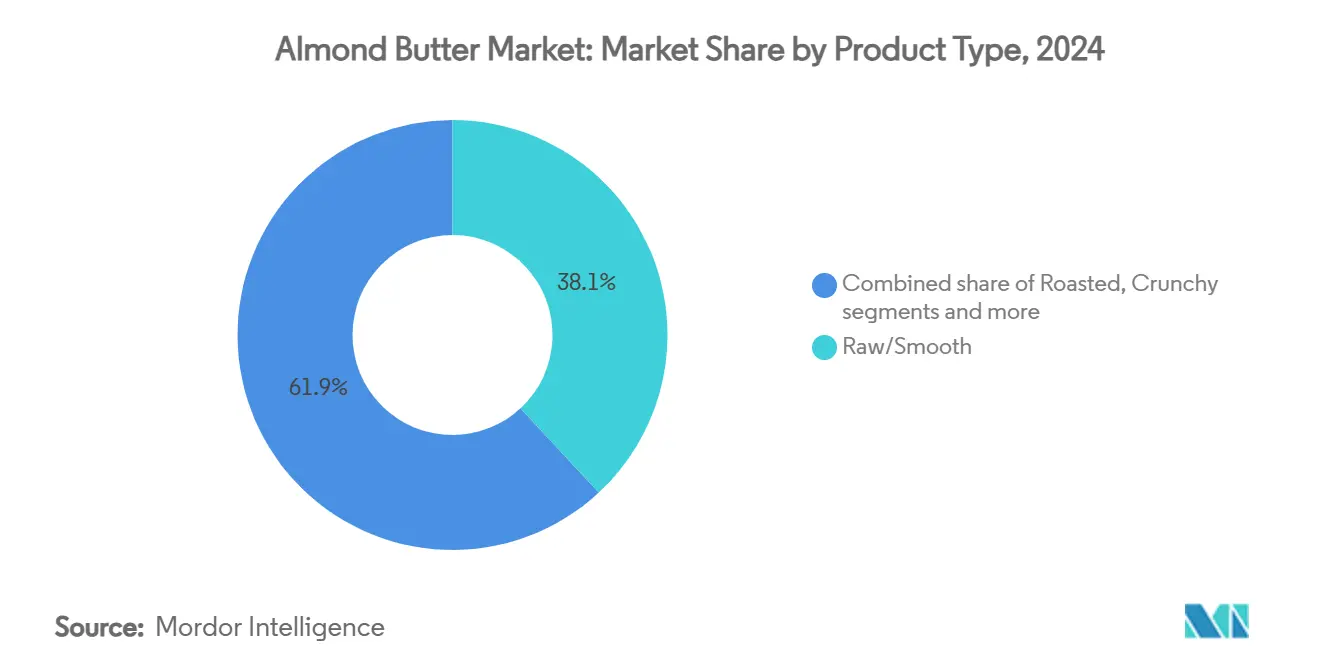

- By product type, the raw/smooth segment led with 38.09% revenue share in 2024, while flavored variants are projected to expand at an 8.23% CAGR to 2030.

- By nature, conventional offerings captured 71.53% of category revenue in 2024; organic alternatives are forecast to grow at an 8.90% CAGR through 2030.

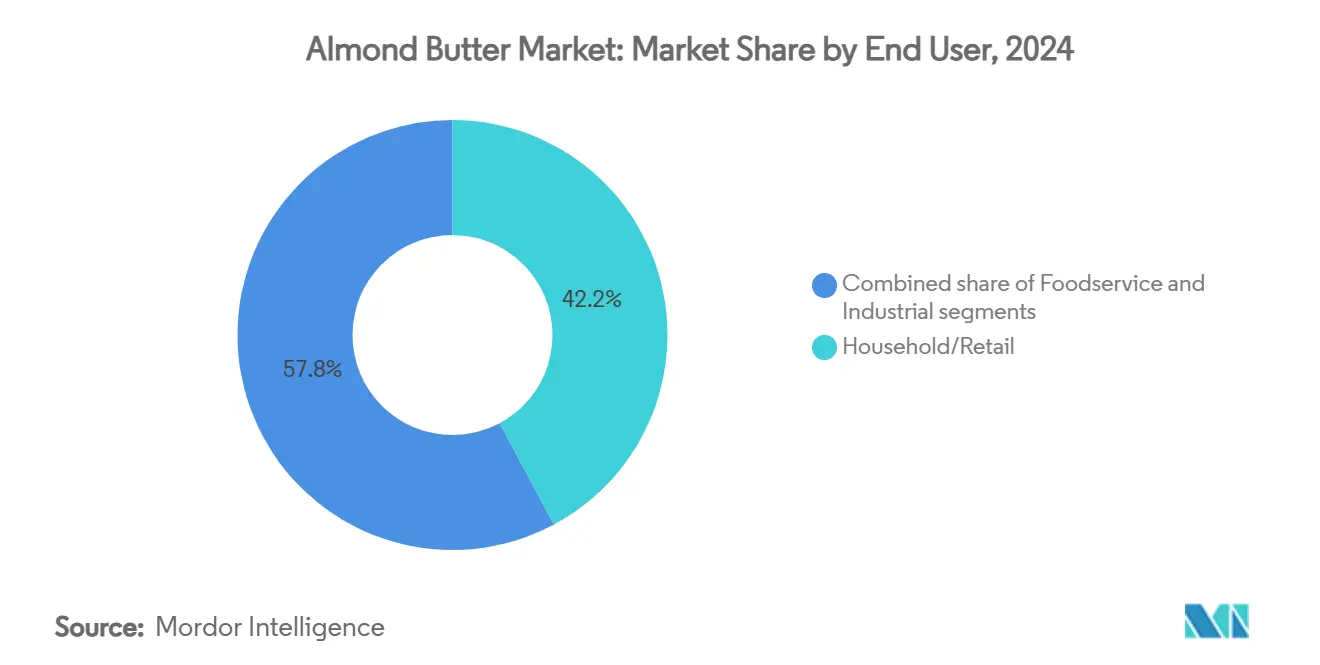

- By end user, household/retail held 42.18% of market share in 2024, whereas foodservice uses are poised for a 7.14% CAGR to 2030.

- By packaging, traditional jars, and tubs controlled 54.62% of sales in 2024; squeeze packs and pouches are expected to climb 7.89% CAGR to 2030.

- By geography, North America commanded 37.51% of volume in 2024, while Asia-Pacific is projected to accelerate at a 9.01% CAGR through 2030.

Global Almond Butter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in the popularity of plant-based diets | +1.8% | Global, with the strongest impact in North America and Europe | Medium term (2-4 years) |

| Rising prevalence of peanut allergies and dairy intolerance | +1.2% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Expansion of e-commerce grocery and DTC nut-butter brands | +1.5% | Global, led by North America and Asia-Pacific urban centers | Short term (≤ 2 years) |

| Clean-label and organic product positioning | +1.1% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Product innovation in flavors and formats | +0.9% | Global, with early adoption in North America | Short term (≤ 2 years) |

| Growing health consciousness boosting almond butter demand | +1.3% | Global, strongest in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in the popularity of plant-based diets

The global almond butter market is undergoing substantial transformation due to increasing consumer adoption of plant-based diets, with almond butter recording significant growth in foodservice and retail segments. The expansion of the plant-based food market indicates rising consumer demand for non-animal product alternatives. Almond butter's functionality serves as a key ingredient in bakery products, confectionery items, and specialty beverages. In the foodservice industry, companies utilize almond butter to develop vegan, allergen-friendly, and clean-label menu items that address diverse consumer requirements. For instance, the Veganuary initiative in January 2023 validated this market shift, with 707,000 participants globally selecting a vegan diet, demonstrating increased market acceptance of plant-based products [1]Source: Veganuary, "The Official Veganuary 2023 Participant Survey", veganuary.com. The introduction of plant-based spreads in retail operations and the implementation of almond butter in foodservice establishments strengthen its market position as a nutritious and sustainable alternative. These market factors, combined with increased health consciousness and product development, continue to drive expansion in the global almond butter market across consumer and institutional channels.

Rising prevalence of peanut allergies and dairy intolerance

The market demand for almond butter is increasing due to rising cases of peanut allergies and dairy intolerance. The product's compatibility with dairy-, soy-, and gluten-free formulations makes it valuable for manufacturers adapting products to meet allergen and dietary requirements. The processing of almond butter maintains its allergenic stability, making it a safer option for individuals with tree nut sensitivities compared to peanut-based products. According to the Australasian Society of Clinical Immunology and Allergy (ASCIA) in 2023, approximately 3% of children have peanut allergies, with even minimal exposure presenting significant risks [2]Source: Australasian Society of Clinical Immunology and Allergy (ASCIA), "Peanut Allergy - Fast Facts", allergy.org.au. Moreover, research published in the American Journal of Clinical Nutrition indicates that regular almond consumption increases butyrate levels in the colon, supporting digestive health - a key consideration for health-conscious consumers and parents seeking specialized nutrition for their children. The protein content and nutritional composition of almond butter make it an effective substitute for children with multiple food allergies, such as peanut allergy. These combined factors of health benefits and allergen safety are driving almond butter's market growth, as foodservice operators and consumers seek allergen-friendly, nutritious alternatives that maintain taste and versatility.

Expansion of e-commerce grocery and DTC nut-butter brands

E-commerce platforms and direct-to-consumer (DTC) distribution channels are transforming almond butter sales across household/retail and foodservice segments. Digital platforms have reduced market entry barriers, allowing smaller brands like Wild Friends Foods and Pip & Nut to offer specialized products, including organic varieties and unique flavors, through their online stores and subscription services. For instance, Pip & Nut manufactures almond butter in multiple varieties, including classic smooth, crunchy almond, and coconut-flavored almond butter. The products contain no palm oil or added sugar and serve as a source of protein and Vitamin E. All varieties are plant-based. Additionally, in Asia-Pacific, digital platforms enable consumers to access imported and specialty almond butter products, expanding market reach beyond traditional retail channels. E-commerce platforms provide consumers with diverse product options, while DTC models enable brands to build customer relationships and gather consumer preference data. Furthermore, foodservice businesses benefit from simplified online bulk purchasing processes, supporting menu development and kitchen operations. DTC brands are establishing market positions through premium offerings and subscription programs, contributing to market growth and product premiumization in the global almond butter market.

Product innovation in flavors and formats

Product manufacturers are experiencing significant growth in flavored almond butter varieties, achieving an 8.23% CAGR, surpassing traditional offerings. Consumers are increasingly seeking nutritious alternatives to conventional spreads, prompting manufacturers to expand their product portfolios. Companies like American Dream Nut Butter are responding to this demand by introducing diverse flavors, including cookies & cream, confetti cake pop, chocolate brownie, mint chocolate and dream, and cinnamon toast, etc. According to the Almond Board of California, almonds were used in 14,000 new food products in 2023, demonstrating their importance in product development [3]Source: Almond Board of California, "2024 State of the Almond Industry: Well-Positioned for Growth", almonds.com. In the almond butter market, manufacturers are introducing diverse flavor combinations, incorporating spices and fruits, and developing new packaging solutions like single-serve packets. Also, improvements in processing technology, specifically in particle size reduction, are enhancing product texture and smoothness. These technical advances improve both the sensory qualities and potential nutritional benefits, including better lipid absorption and nutrient availability. Besides, manufacturers are combining innovative flavors and advanced processing methods to establish unique market positions. Thus, retailers and foodservice operators are leveraging this trend by offering products that feature bold flavors and clean-label ingredients. These developments are strengthening almond butter's position as a premium option in the spreads category, appealing to consumers who prioritize both health and taste.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile almond prices driven by climate risk | -1.4% | Global, with strongest impact in North America production regions | Short term (≤ 2 years) |

| Competition from other nut and seed butters | -0.8% | Global, most intense in North America and Europe | Medium term (2-4 years) |

| High price compared to conventional spreads | -0.6% | Global, particularly in price-sensitive emerging markets | Long term (≥ 4 years) |

| Sustainability and water-use concerns in almond farming | -0.5% | North America production regions, spreading to consumer markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile almond prices driven by climate risk

Price volatility in almonds, primarily caused by climate-related risks, affects supply stability and value chain costs in almond butter production. In 2024, wholesale almond prices demonstrated substantial fluctuation, initially dropping to their lowest levels in 20 years before increasing by 24.42% year-over-year due to supply constraints, according to USDA data. Climate change continues to affect almond farming through higher temperatures, irregular rainfall patterns, and altered bloom periods, which impact crop cycles and pollination efficiency. These conditions create cost pressures for almond butter manufacturers, particularly affecting smaller companies that lack robust price hedging capabilities. Manufacturers often transfer these increased costs to consumers, which can reduce market accessibility for price-sensitive consumers and restrict product innovation. The ongoing price instability may lead to industry changes in raw material sourcing strategies and market consolidation, while creating challenges for manufacturers to maintain profitable almond butter production in an increasingly climate-affected environment.

Competition from other nut and seed butters

Market competition has intensified as manufacturers introduce diverse nut and seed butter alternatives, requiring almond butter brands to adapt their strategies to maintain market share. While peanut butter remains dominant in mass-market segments due to its lower cost, consumers are increasingly choosing alternatives such as cashew butter, sunflower seed butter, and hazelnut butter, each offering unique nutritional benefits and taste profiles. Sunflower seed butter has emerged as a significant competitor in the allergy-friendly category, providing an option for consumers with tree nut allergies. Additionally, the introduction of hybrid spreads combining almond butter with legumes or seeds helps brands optimize costs while enhancing nutritional value. This competitive environment has pushed almond butter manufacturers to focus on product differentiation through new flavors, clean-label products, and functional ingredients that target health-conscious consumers. Continuous investment in product development has become crucial, especially as private labels and startups use e-commerce platforms to market premium and specialized products. The expanding nut and seed butter market is driving innovation in the almond butter segment, emphasizing the importance of premium positioning and adaptation to consumer preferences.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flavored Varieties Drive Innovation

The raw/smooth segment holds a dominant 38.09% market share in 2024, driven by industrial and consumer demand for versatile, unprocessed almond butter across multiple applications. Flavored varieties are growing at 8.23% CAGR through 2030, as consumers seek healthy alternatives to conventional spreads. The Almond Board of California's November 2024 collaboration with Ecole Chocolat highlights the industry's focus on chocolate-almond butter applications in premium confectionery. Besides, roasted varieties remain popular in foodservice, particularly in bakery applications, while crunchy textures attract consumers looking for textural variety.

Meanwhile, manufacturers are incorporating functional ingredients to enhance nutritional value and market appeal. Roasting processes improve flavor and texture while preserving nutritional content, with dry-roasted almonds having reduced moisture content for better stability. The growth in flavored varieties reflects the premiumization of spreads, where consumers accept higher prices for distinctive flavors. Companies use natural flavoring ingredients such as honey, maple, and sea salt to develop premium products that maintain clean-label standards.

By Nature: Organic Segment Accelerates

The market share of conventional almond butter reached 71.53% in 2024, supported by established supply networks and economies of scale that provide cost advantages for large-scale producers. The conventional segment maintains strong market penetration through mass-market retail and foodservice channels, reaching broad consumer segments through competitive pricing and wide distribution. Major producers like Blue Diamond Growers leverage these advantages to maintain their conventional almond butter products' presence across supermarkets, wholesale outlets, and international markets.

The organic almond butter segment is experiencing a CAGR of 8.90% through 2030, surpassing the overall market growth rate. This increase indicates consumer willingness to purchase certified organic spreads without pesticides and synthetic additives, despite higher prices. Companies like MaraNatha have developed clean-label and sustainably sourced almond butters to meet demand from health-conscious consumers and specialty retail channels. The organic segment's expansion demonstrates market demand for products with transparent sourcing and quality certifications.

By End User: Foodservice Applications Expand

Household/retail segment accounts for 42.18% of the market in 2024, as consumers increasingly adopt almond butter as a nutritious pantry staple and breakfast spread alternative. Consumer health awareness drives market growth, with almond butter offering protein, healthy fats, and dairy-free properties. The product's versatility and suitability for various dietary preferences strengthen its presence in households and retail outlets. Companies such as Justin's meet consumer demand through product diversification, including organic varieties, flavored options, and protein-enhanced formulations.

The foodservice segment is experiencing rapid growth, with a projected CAGR of 7.14% through 2030, due to increased menu innovation in bakery and confectionery applications. Almond butter's properties, including its creamy texture, flavor, and nutritional benefits, enable chefs and food developers to create premium, plant-based, and allergen-friendly products that align with consumer preferences. This growth is prominent in cafes and specialty bakeries, where almond butter enhances smoothies, pastries, and energy bars. Wild Friends Foods demonstrates successful integration across retail and foodservice channels by showcasing almond butter's versatility, strengthening its position in the global market. Moreover, the functional properties of almond butter, including emulsification and protein fortification, enable manufacturers to develop clean-label products for industrial applications that align with consumer preferences for natural ingredients.

By Packaging: Convenience Formats Gain Traction

The market share of traditional jars and tubs accounts for 54.62% of almond butter sales in 2024. This dominance stems from familiar packaging formats, efficient storage capabilities, and established manufacturing processes. The format enables competitive pricing and quality consistency, making it the standard choice for major brands like Justin's and MaraNatha. Also, glass and durable plastic containers enhance product visibility and perceived quality, driving consistent sales across retail and household segments.

Meanwhile, squeeze packs and pouches represent the fastest-growing packaging segment, with a projected CAGR of 7.89% through 2030. These formats provide convenience for on-the-go consumption and portion control, meeting consumer demand for healthy, portable snacks. Companies like Spread The Love have introduced single-serve almond butter packs designed for travel, lunchboxes, and gym bags. The growing consumer preference for flexible packaging continues to drive product development and premium offerings in the market. Moreover, advancements in packaging materials focus on enhanced barrier properties that prevent lipid oxidation, helping maintain almond butter quality and extend shelf life for better consumer acceptance.

Geography Analysis

The North American almond butter market holds a 37.51% share in 2024, driven by its proximity to California's almond production and strong consumer demand. The market growth stems from expanded retail presence in natural and specialty stores, with significant sales through club retailers like Costco. Canada emerges as a strategic growth market for Blue Diamond Growers as the company pursues international expansion to counter domestic market saturation. However, the region faces supply chain disruptions and climate-related risks, evidenced by California's declining almond acreage over three consecutive years through 2024. While Mexico presents growth opportunities, potential tariff impacts may affect market development, though its dependence on U.S. almonds limits alternative sourcing options.

The Asia-Pacific almond butter market is projected to grow at a CAGR of 9.01% through 2030. This growth stems from urbanization, health awareness, and changing dietary preferences in China, India, and Australia. The increasing adoption of plant-based foods has enhanced consumer interest in almond butter as a nutritious spread. The expansion of e-commerce platforms and improved availability of almond butter products are driving market growth. The region's urban consumers are showing increased demand for almond butter, making Asia-Pacific a significant contributor to the global market's expansion.

Europe maintains steady growth through established organic and natural food distribution networks, with California remaining the EU's primary tree nut supplier. Western Europe recorded a 15.6% decline in almond imports in 2025 due to economic pressures and supply chain disruptions, according to Select Harvest USA. The Middle East shows robust growth potential, with Turkey sustaining significant almond imports despite implementing 10% retaliatory tariffs on U.S. products, as reported by the U.S. Department of Agriculture. Additionally, Saudi Arabia exhibits notable market strength, combining local almond cultivation with import demand and traditional preferences for almond-based products in the hospitality sector. Furthermore, South America and Africa present developing market opportunities, with Latin American regions experiencing growth driven by competitive pricing and increasing health consciousness, though these markets remain in early development phases compared to established regions.

Competitive Landscape

The global almond butter market shows moderate fragmentation, with multinational companies and specialty brands competing for market share. Blue Diamond Growers, The J.M. Smucker Company, and Hormel Foods Corporation (through Justin's) maintain their market leadership in the almond butter segment through established distribution networks, retail partnerships, and brand recognition. These companies utilize their operational scale to introduce new flavors, packaging formats, and product variants aligned with consumer preferences for clean labels and plant-based nutrition. Their investments in research and development and marketing strengthen customer relationships while facilitating expansion into new markets. The companies' retail presence across premium grocery chains and online platforms ensures broad product accessibility. This combination of market presence and adaptability enables them to maintain competitive advantages over smaller manufacturers and serve diverse consumer segments worldwide.

Smaller and emerging almond butter manufacturers differentiate themselves through organic certifications, distinctive flavors, and direct-to-consumer (DTC) strategies. These companies utilize e-commerce platforms and social media to target health-conscious consumers seeking clean-label, allergy-friendly, and artisanal products. Their rapid product development capabilities, including protein-enhanced and dessert-inspired varieties, help establish brand loyalty among specific consumer segments.

The market's competitive dynamics intensify as traditional peanut butter manufacturers expand into the almond butter segment, targeting premium nut butter consumers through existing supply chains and retail partnerships. Industry consolidation continues, as demonstrated by Once Again Nut Butter's acquisition of Big Tree Organic Farms in 2024. This consolidation trend enables companies to enhance market positions, expand product lines, and manage price fluctuations through vertical integration and supply chain optimization. These developments indicate an evolving competitive environment in the global almond butter industry.

Almond Butter Industry Leaders

-

Blue Diamond Growers

-

The J.M. Smucker Company

-

Hormel Foods Corporation

-

The Hain Celestial Group, Inc.

-

Barney Butter, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Wilkin and Sons, based in Tiptree, launched its first Tiptree Nut Butters range. The range included smooth peanut butter, crunchy peanut butter, and almond butter. The peanut butter varieties were available in 270-gram jars priced at GBP 3.29, while the almond butter came in a 180-gram jar priced at GBP 3.99.

- April 2024: SkinnyDipped initiated a brand transformation that included a new logo and packaging design. The company expanded its product portfolio with a nut butter line launching in the fall. The latest product range offered 16-ounce jars in three varieties: Lemon Bliss, Classic Almond, and Maple Kiss. Each product contained 6 grams of protein and incorporated natural flavors.

- January 2024: ManiLife, known for its peanut butter products, expanded its portfolio with a new range of small-batch almond butters. The sustainably sourced almond butters, available in smooth and crunchy varieties, were distributed through Tesco stores nationwide and the ManiLife website.

Global Almond Butter Market Report Scope

| Raw/Smooth |

| Roasted |

| Flavored (Chocolate, Honey, Maple, etc.) |

| Crunchy |

| Organic |

| Conventional |

| Foodservice | |

| Household/Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channel | |

| Industrial | Bakery and Confectionery |

| Nutraceutical and Sports Nutrition | |

| Cosmetics and Personal Care | |

| Other Industrial Uses |

| Jars and Tubs |

| Squeeze Packs and Pouches |

| Bulk Containers (more than 5 kg) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Raw/Smooth | |

| Roasted | ||

| Flavored (Chocolate, Honey, Maple, etc.) | ||

| Crunchy | ||

| By Nature | Organic | |

| Conventional | ||

| By End User | Foodservice | |

| Household/Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| Industrial | Bakery and Confectionery | |

| Nutraceutical and Sports Nutrition | ||

| Cosmetics and Personal Care | ||

| Other Industrial Uses | ||

| By Packaging | Jars and Tubs | |

| Squeeze Packs and Pouches | ||

| Bulk Containers (more than 5 kg) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the almond butter market?

The almond butter market size is valued at USD 1.54 billion in 2025 and is projected to reach USD 2.14 billion by 2030.

Which region is growing the fastest in almond butter sales?

Asia-Pacific is expected to record the quickest growth with a 9.01% CAGR through 2030, driven by rising disposable income and health awareness.

Which product type is expanding most rapidly?

Flavored almond butter varieties are projected to advance at an 8.23% CAGR to 2030, outpacing raw, roasted, and crunchy formats.

What share does organic almond butter hold and how fast is it growing?

Conventional SKUs dominate with 71.53% share in 2024 while organic alternatives are growing at an 8.90% CAGR, reflecting strong demand for clean-label spreads.

Page last updated on: