Robotic Surgical Procedures Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

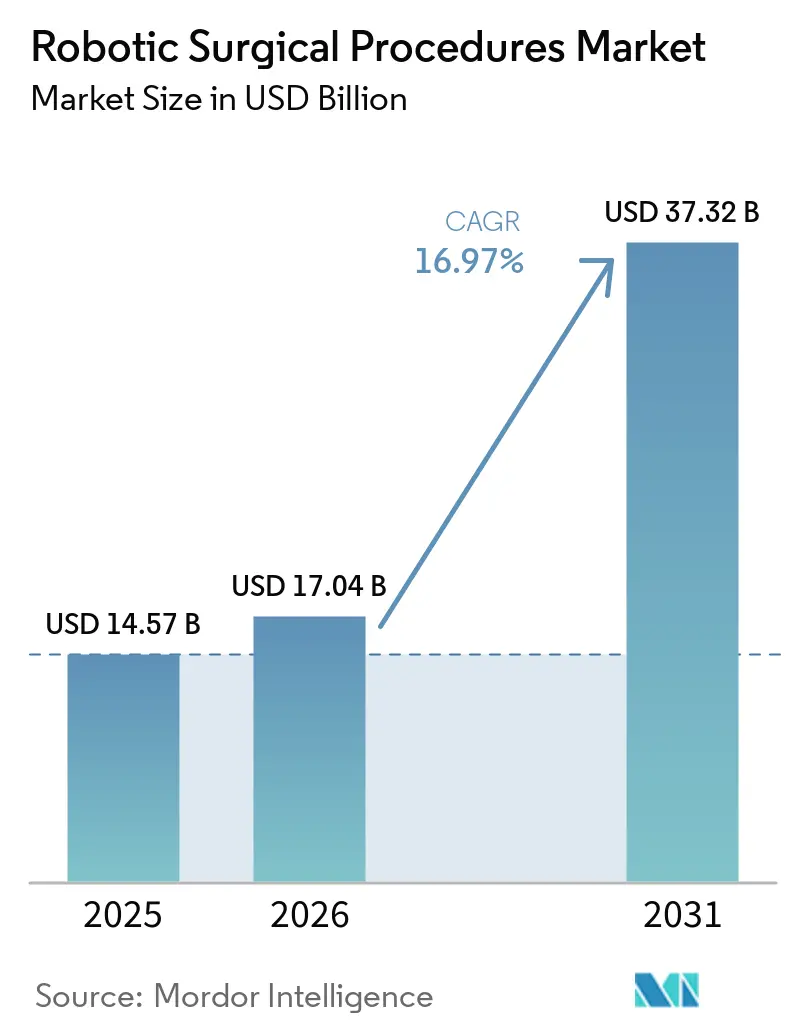

| Market Size (2026) | USD 17.04 Billion |

| Market Size (2031) | USD 37.32 Billion |

| Growth Rate (2026 - 2031) | 16.97% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Robotic Surgical Procedures Market Analysis by Mordor Intelligence

The Robotic Surgical Procedures Market size was valued at USD 14.57 billion in 2025 and is estimated to grow from USD 17.04 billion in 2026 to reach USD 37.32 billion by 2031, at a CAGR of 16.97% during the forecast period (2026-2031).

As populations age and conditions like cancer, benign prostatic hyperplasia, and joint degeneration become more prevalent, the demand for robotic assistance in surgeries is increasing. Hospitals are supporting robotic surgical procedures due to consistent minimally invasive workflows and reduced conversion rates, which help lower complications and the need for repeat care. In 2025, over 3.2 million procedures were conducted using Intuitive Surgical platforms, marking a 19% increase from 2024.[1]Intuitive Surgical, “Intuitive Announces Preliminary Fourth Quarter and Full Year 2025 Results,” Investor Relations Press Release, intuitive.com This growth highlights the rising utilization and broader clinical adoption of robotic surgeries. Recent developments, such as Medtronic’s Stealth AXiS clearance, Johnson & Johnson’s OTTAVA filing, and Medtronic’s expansion of its Hugo platform in the U.S., signal intensified competition and expanded specialty coverage in the robotic surgical market. With increasing case volumes, diverse platform options, and outcome-driven commercial models, the market is set for new applications, outpatient growth, and deeper hospital integration.

Key Report Takeaways

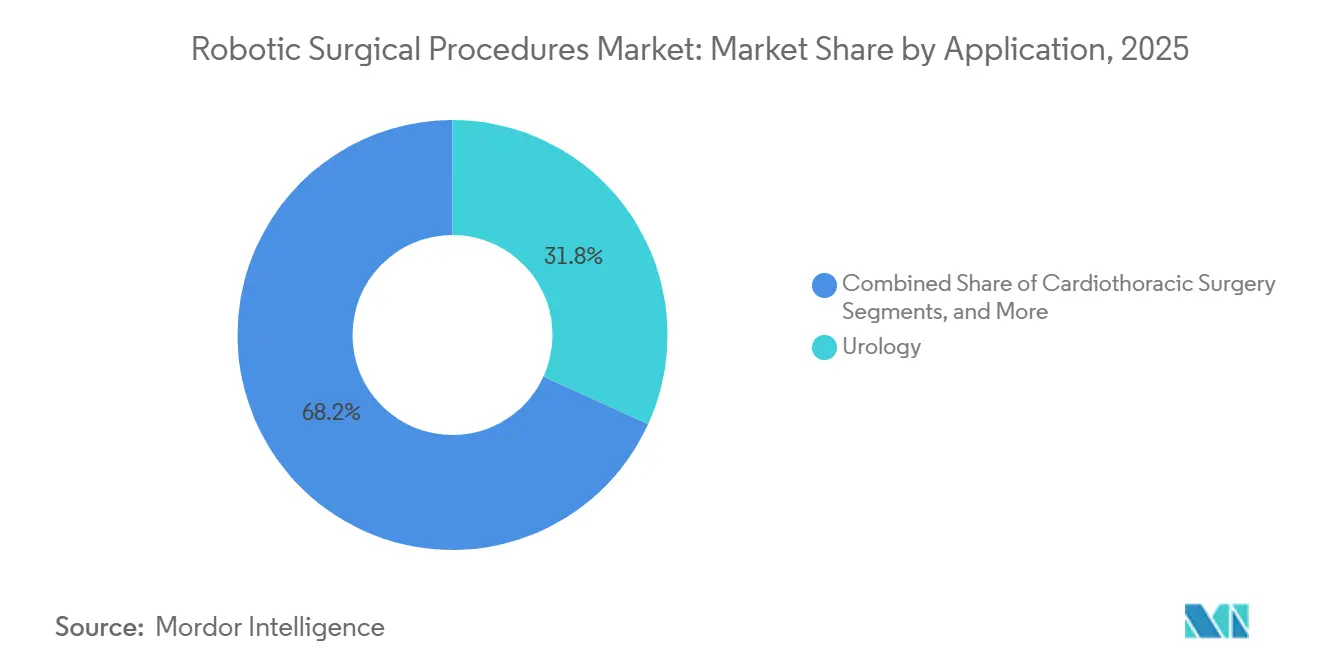

- By application, urology led with 31.76% revenue share in 2025, while orthopedics is projected to expand at a 17.90% CAGR through 2031.

- By procedure type, minimally invasive laparoscopic robotic-assisted procedures held 26.87% revenue share in 2025, while endoscopic robotic procedures are projected to grow at an 18.25% CAGR through 2031.

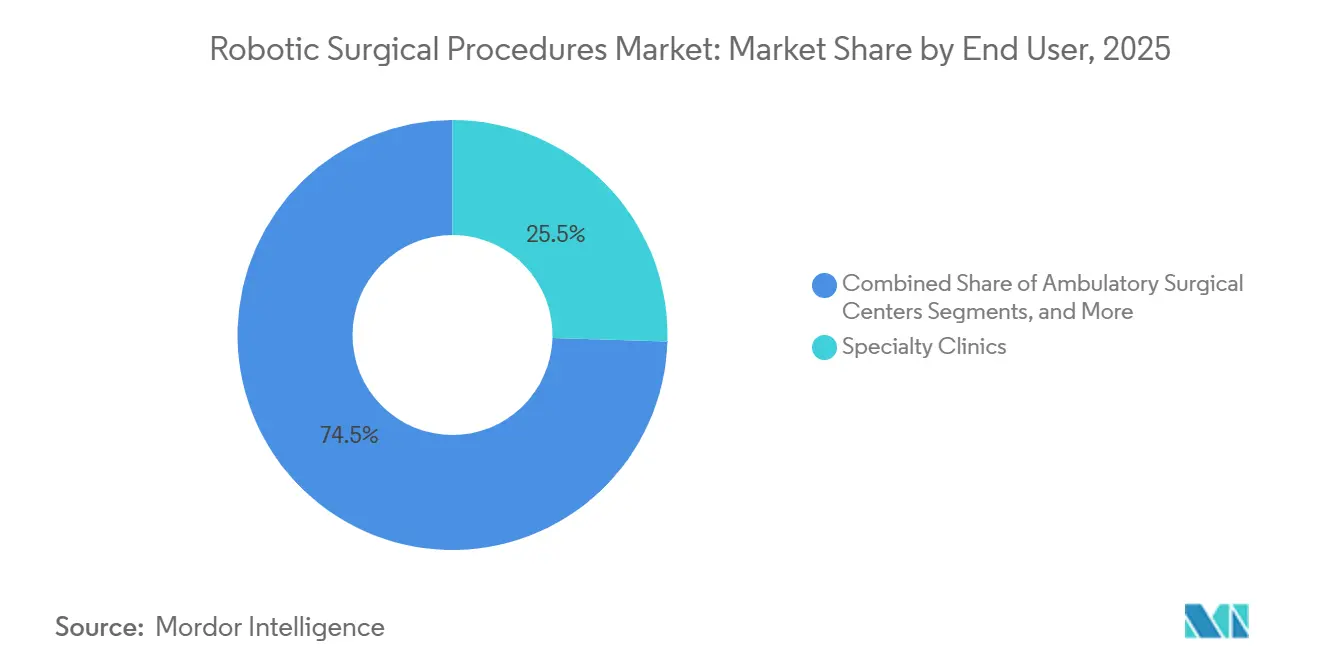

- By end user, specialty clinics held 25.45% revenue share in 2025, while ambulatory surgical centers are forecast to expand at a 17.69% CAGR through 2031.

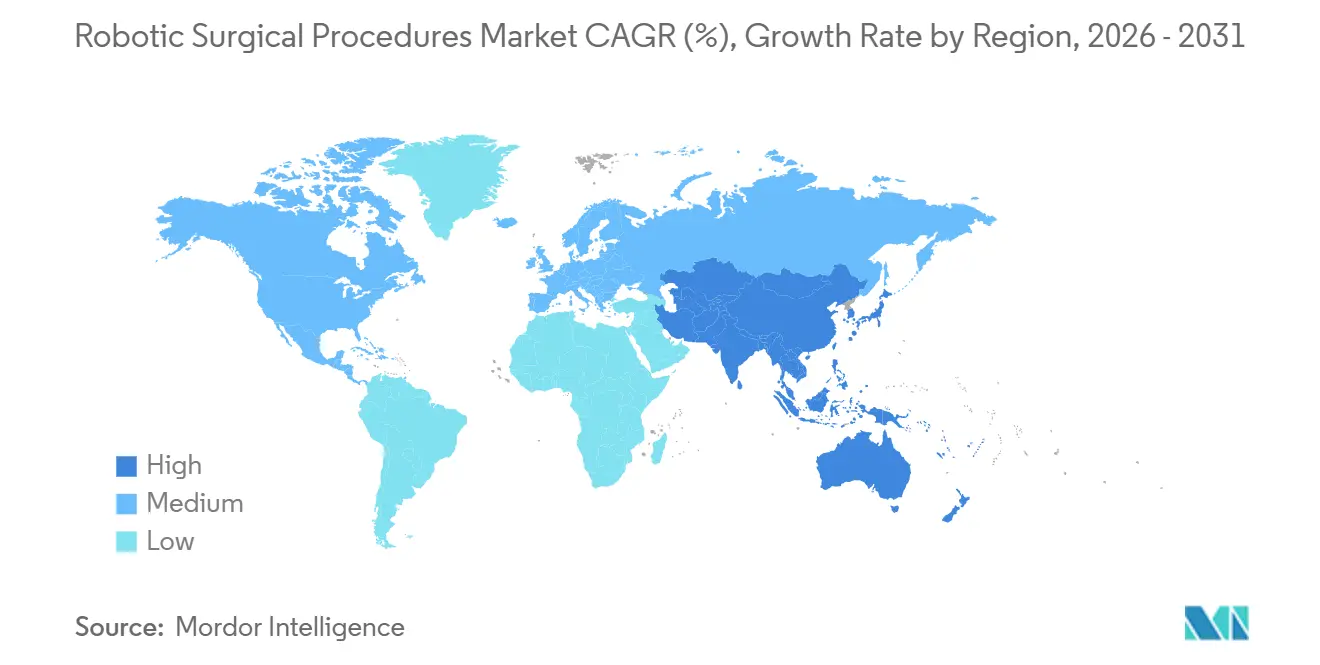

- By geography, North America held 43.55% of revenue in 2025, while Asia-Pacific is projected to expand at a 17.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Robotic Surgical Procedures Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Expanded clinical validation beyond urology | +3.2% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Ambulatory surgical center platform fit and throughput | +2.8% | North America primary, with spillover to Asia-Pacific and Middle East and Africa | Short term (≤ 2 years) |

| AI-enabled surgical planning and workflow standardization | +3.5% | Global | Medium term (2-4 years) |

| Value-based procurement tied to measurable outcomes | +2.4% | North America and Europe | Medium term (2-4 years) |

| Multi-specialty utilization of single robotic platforms | +2.1% | Global, strongest in emerging Asia-Pacific markets | Long term (≥ 4 years) |

| Surgeon retention and talent attraction through robotics | +1.6% | North America and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanded Clinical Validation Beyond Urology

The robotic surgical procedures market is transitioning from its reliance on urology to broader adoption across multiple specialties. In 2026, enhanced guidelines for Aquablation increased confidence in robotic treatments for benign prostatic hyperplasia, driving its use in urology. General surgery and gynecology are also gaining traction, with Johnson & Johnson's FORTE study meeting safety and performance benchmarks in a 30-patient gastric bypass cohort. Stable robotic performance in complex bariatric cases is expected to encourage payers and providers to extend adoption to related procedures, expanding the market's potential.

AI-Enabled Surgical Planning and Workflow Standardization

Artificial intelligence is transforming the robotic surgical procedures market from hardware-driven purchases to workflow-focused models. Medtronic’s Stealth AXiS system, cleared by the FDA in February 2026 and CE Mark in April 2026, integrates planning, navigation, and robotic execution into a single platform. Moon Surgical’s Maestro Software Version 2.7, launched in June 2026, introduced automated operating room setup, navigation, and post-procedure documentation. These advancements simplify operations, making robotic systems more appealing to facilities previously deterred by staffing complexities.

Ambulatory Surgical Center Platform Fit and Throughput

Ambulatory surgical centers (ASCs) are reshaping the robotic surgical procedures market, challenging the dominance of large hospitals. Stryker’s Mako RPS, launched in February 2026, targets total knee arthroplasty in outpatient settings with limited space and staffing. Similarly, Smith+Nephew’s CORI XT handheld robotics platform completed its first clinical cases in June 2026 at an ASC in Arizona. These innovations highlight the market's shift toward compact, multi-procedure systems, with vendors focusing on smaller setups and faster room turnovers to meet ASC demands.

Value-Based Procurement Tied to Measurable Outcomes

Procurement strategies in the robotic surgical procedures market are evolving, with hospitals prioritizing systems that enhance efficiency, throughput, and outcomes over upfront costs. Platforms with proven efficacy in specific procedures are gaining preference, while leasing and usage-based models are becoming more popular. These flexible options enable hospitals to align robotic adoption with case volumes and procedural needs, lowering barriers for mid-sized facilities to enter the market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High capital and recurring per-procedure cost burden | -2.5% | Global, most acute in Asia-Pacific and Middle East and Africa | Short term (≤ 2 years) |

| Or integration complexity and staff training dependencies | -1.8% | Global, strongest in smaller hospital systems | Medium term (2-4 years) |

| Cybersecurity and software validation requirements | -1.4% | Global, with stronger regulatory influence in North America and Europe | Medium term (2-4 years) |

| Uneven reimbursement and procedure economics | -2.0% | Europe and Asia-Pacific, with localized pressure in North America for non-urology indications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital and Recurring Per-Procedure Cost Burden

Robotic surgical procedures grapple with significant cost hurdles, hindering their uptake beyond major medical centers. The financial strain extends beyond just acquiring the robotic system; costs for instruments, disposables, and upgrades play a pivotal role in the economics of each procedure. This challenge intensifies when insurers don't offer premium reimbursements for robotic surgeries compared to their laparoscopic counterparts. Consequently, medical providers are left to advocate for robotic adoption based on efficiency and patient outcomes rather than direct financial incentives. A case in point is Smith+Nephew’s CORI XT platform, which, while expanding capabilities to shoulder surgeries, introduces a substantial capital challenge for facilities still ramping up their orthopedic volumes. Consequently, adoption of robotic procedures is largely confined to tertiary hospitals, specialized clinics, and a select few busy outpatient centers.

OR Integration Complexity and Staff Training Dependencies

Adoption of robotic surgical procedures is further hampered as facilities grapple with integrating these systems into established operating room protocols. Smaller surgical teams, with limited capacity, find it challenging to accommodate training sessions, staff rotations, and the inevitable temporary dips in productivity. This challenge is magnified in ambulatory settings, where streamlined staffing is crucial for cost management, leaving little room for redundancy during training. Thus, the market for robotic surgical procedures hinges not just on advanced devices, but also on simplified setups, optimized workflows, and effective team training. If any of these elements falter, hospitals might postpone adopting the technology, even with a clear clinical interest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Urology Anchors Revenue as Orthopedics Accelerates

In 2025, urology accounted for 31.76% of the robotic surgical procedures market, maintaining its position as the leading application segment. This dominance stems from the widespread adoption of robotic prostatectomies and faster clinical acceptance compared to other specialties. The growing guideline support for Aquablation in 2026 further strengthened robotic urologic care's role in the market. Hospitals find this segment appealing as they can increase procedure volumes without creating new clinical categories.

Orthopedics is the fastest-growing segment, with a forecast CAGR of 17.90% through 2031. Recent advancements have reduced system footprints, image dependency, and setup challenges, enabling orthopedic robots to move into outpatient settings. Stryker’s Mako RPS and Smith+Nephew’s CORI XT exemplify this shift. General surgery and gynecology are also expanding, with OTTAVA’s FDA submission in January 2026 and positive gastric bypass study results signaling broader platform applications. Neurosurgery and spine remain smaller segments, but Medtronic’s Stealth AXiS demonstrates how shared platforms can enhance hospitals' capital efficiency.

By Procedure Type: Endoscopic Gains Ground as Minimally Invasive Core Holds

Minimally invasive laparoscopic robotic-assisted procedures held 26.87% of market revenue in 2025, maintaining their leadership position. This reflects the established history of robotic surgeries in urology, gynecology, and general surgery. Intuitive Surgical reported a 12% year-over-year increase in globally installed da Vinci systems, reaching 11,395 units by March 2026. The company’s Q1 2026 revenue of USD 2.77 billion, with a 23% rise in instruments and accessories sales, underscores the segment's financial stability driven by recurring procedures. The laparoscopic core remains robust due to its scale, training base, and reimbursement familiarity.

Endoscopic robotic procedures are the fastest-growing segment, with a projected CAGR of 18.25% through 2031. Miniaturized tools are driving growth by enabling natural-orifice and transluminal procedures that older systems could not address effectively. Percutaneous and catheter-based robotic procedures are gaining traction in cardiology and interventional oncology, while open-assisted hybrid procedures remain relevant in lower-resource settings. Over time, the market is expected to integrate laparoscopic, endoscopic, and hybrid workflows as vendors develop broader platform families.

By End User: Specialty Clinics Lead While ASCs Redefine the Growth Frontier

Specialty clinics accounted for 25.45% of the robotic surgical procedures market in 2025, making them the leading end-user segment. Their dominance is driven by high-volume urologic and orthopedic procedures, where robotic use is justified by throughput and patient acquisition. Focused outpatient practices align surgeon specialization, case flow, and equipment utilization more effectively than diversified hospital operating rooms, making robotic investments sustainable for procedures like robotic prostatectomies and knee arthroplasties. Standalone and private hospitals remain key buyers but face increasing pressure to demonstrate cost control and improved outcomes.

Ambulatory surgical centers (ASCs) are the fastest-growing end-user segment, with a forecast CAGR of 17.69% through 2031. The market is expanding into ASCs due to systems designed for smaller spaces, reduced staffing needs, and faster room turnovers. Stryker’s Mako RPS was used for the first total knee arthroplasty at the Surgery Center at Pelham in early 2026, showcasing the ASC robotics model. Similarly, Smith+Nephew’s CORI XT cases in Arizona ASCs highlight the growing adoption of outpatient orthopedic robotics. While large hospitals will continue to handle complex multi-specialty robotic procedures, future growth is expected to shift toward ASCs and specialty clinics.

Geography Analysis

In 2025, North America accounted for 43.55% of the robotic surgical procedures market, maintaining its position as the largest regional contributor. The region benefits from strong reimbursement frameworks in robotic urology, higher utilization rates per installed system, and a well-established training base for surgeons and care teams. Intuitive reported a 15% increase in US da Vinci procedures in 2025, alongside a 31% rise in after-hours procedure utilization in Q1 2026. This indicates that market growth is driven by better utilization of existing systems rather than solely by new installations. While Canada and Mexico are progressing, the US continues to lead the region in terms of volume, reimbursement, and platform approvals.

Europe held the second-largest share in the robotic surgical procedures market. The region benefits from strong clinical research, universal healthcare systems, and a significant manufacturing presence. However, reimbursement remains less consistent compared to North America, exposing hospitals to higher economic risks when robotic benefits are not fully covered under existing payment structures. Despite this, Europe is advancing through selective platform adoption, particularly in orthopedic and minimally invasive applications, which support long-term utilization. Success in Europe under tighter budget constraints strengthens vendors' prospects for broader global adoption.

Asia-Pacific is projected to witness the fastest growth in the robotic surgical procedures market, with a CAGR of 17.45% through 2031. The region is transitioning from import reliance to stronger domestic competition, especially in China. Da Vinci procedures in Southeast Asia grew by 24% in 2025, reflecting increased utilization even in markets with smaller installed bases compared to North America and Europe. China's domestic surgical robot market is gaining traction, potentially reshaping pricing and platform access. India and South Korea contribute to regional growth through rising chronic disease burdens and private hospital investments, while the Middle East, Africa, and South America remain in early stages, focusing on medical tourism, hospital modernization, and selective platform adoption.

Competitive Landscape

Intuitive Surgical continues to lead the robotic surgical procedures market with its da Vinci and Ion platforms. In 2025, over 3.2 million procedures were performed using Intuitive's systems. By early 2026, the company had 11,395 da Vinci systems installed globally, reflecting its strong procedural and training foundation. Intuitive's competitive edge lies in surgeon familiarity, service depth, and utilization history, which are difficult for new entrants to replicate quickly. However, competition is intensifying as rivals adopt more focused, specialty-specific strategies.

Medtronic and Johnson & Johnson are making notable advancements in the robotic surgical procedures market. Medtronic received FDA clearance for its Hugo system in urologic procedures in December 2025 and filed 510(k) applications in June 2026 to expand into general surgery and gynecology, signaling its intent to dominate the laparoscopic space. Johnson & Johnson submitted its OTTAVA system to the FDA in January 2026 and reported positive pivotal study results for gastric bypass in May 2026, positioning it as a strong contender in soft-tissue surgery. Both companies are targeting high-volume procedures that have historically driven robotic surgery adoption, shifting competition toward evidence-based strategies and specialty expansions.

The market is also creating opportunities for focused competitors who do not aim to dominate all categories. PROCEPT BioRobotics has established a niche with its Aquablation system, performing 12,200 US procedures in Q1 2026, showcasing the strength of a specialized approach. In orthopedics, Stryker and Smith+Nephew are driving growth by introducing compact systems into outpatient settings, diverging from the large soft-tissue platform race. Emerging players like CMR Surgical, Distalmotion, SS Innovations, Moon Surgical, and Cornerstone Robotics are increasing competition by focusing on workflow simplicity, reduced capital requirements, or targeted clinical applications. While the market is becoming more diverse, established players with significant installed bases and training ecosystems continue to dominate.

Robotic Surgical Procedures Industry Leaders

Intuitive Surgical, Inc.

Johnson & Johnson

Medtronic plc

Stryker Corporation

CMR Surgical Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Medtronic filed 510(k) applications in the U.S. to expand the Hugo Robotic-Assisted Surgery system to general surgery and gynecology, building on its global use in over 35 countries and aiming to compete with Intuitive Surgical’s da Vinci system.

- June 2026: Smith+Nephew completed the first clinical cases using the CORI XT Handheld Robotics Platform for knee and shoulder arthroplasty, designed for both hospital and ambulatory surgery center environments.

- June 2026: Moon Surgical launched Maestro Software Version 2.7, transforming the platform into a multi-model physical AI system with features like automated OR setup, intraoperative navigation, and post-procedure documentation.

- May 2026: Johnson & Johnson presented positive clinical results for the OTTAVA Robotic Surgical System, meeting safety and performance benchmarks in a 30-patient IDE study for Roux-en-Y gastric bypass, supporting its FDA De Novo application.

- May 2026: Cornerstone Robotics received EU CE Mark MDR approval for its Sentire Endoscopic Surgical System, enabling access to European markets for minimally invasive procedures in general surgery, gynecology, thoracic, and urology.

- May 2026: PROCEPT BioRobotics completed enrollment for the WATER IV study comparing Aquablation therapy with radical prostatectomy and received FDA IDE approval for a study comparing Aquablation with active surveillance in prostate cancer.

Global Robotic Surgical Procedures Market Report Scope

As per the scope of the report, robotic surgical procedures, or robot-assisted surgeries, use advanced mechanical arms and computers to help surgeons perform complex operations. The robot does not work on its own. Instead, a trained surgeon controls every movement from a computer screen.

The robotic surgical procedures market is segmented by application, procedure type, end-user, and geography. By application, the market includes urology, general surgery, gynecology, orthopedics, cardiothoracic surgery, neurosurgery, ear, nose, and throat surgery, bariatric and metabolic surgery, and other applications. By procedure type, the market is segmented into minimally invasive laparoscopic robotic-assisted procedures, percutaneous and catheter-based robotic procedures, endoscopic robotic procedures, open-assisted hybrid procedures, and other procedure types. By end-user, the market is categorized into large hospital systems, standalone and private hospitals, ambulatory surgical centers, and specialty clinics. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Urology |

| General Surgery |

| Gynecology |

| Orthopedics |

| Cardiothoracic Surgery |

| Neurosurgery |

| Ear, Nose, and Throat Surgery |

| Bariatric and Metabolic Surgery |

| Other Applications |

| Minimally Invasive Laparoscopic Robotic-Assisted Procedures |

| Percutaneous and Catheter-Based Robotic Procedures |

| Endoscopic Robotic Procedures |

| Open-Assisted Hybrid Procedures |

| Other Procedure Types |

| Large Hospital Systems |

| Standalone and Private Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Urology | |

| General Surgery | ||

| Gynecology | ||

| Orthopedics | ||

| Cardiothoracic Surgery | ||

| Neurosurgery | ||

| Ear, Nose, and Throat Surgery | ||

| Bariatric and Metabolic Surgery | ||

| Other Applications | ||

| By Procedure Type | Minimally Invasive Laparoscopic Robotic-Assisted Procedures | |

| Percutaneous and Catheter-Based Robotic Procedures | ||

| Endoscopic Robotic Procedures | ||

| Open-Assisted Hybrid Procedures | ||

| Other Procedure Types | ||

| By End User | Large Hospital Systems | |

| Standalone and Private Hospitals | ||

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the robotic surgical procedures market size in 2026 and 2031?

The robotic surgical procedures market size is USD 17.04 billion in 2026 and is forecast to reach USD 37.32 billion by 2031, with a CAGR of 16.97%.

Which application leads revenue in robotic surgical procedures?

Urology leads with a 31.76% revenue share in 2025, supported by strong procedure adoption and broader support for Aquablation in benign prostatic hyperplasia care.

Which procedure type is growing the fastest in robotic-assisted surgery?

Endoscopic robotic procedures are the fastest-growing procedure type, with a projected CAGR of 18.25% through 2031.

Why are ambulatory surgical centers becoming important for robotic platforms?

Ambulatory surgical centers are projected to grow at a 17.69% CAGR through 2031 because newer systems are smaller, easier to deploy, and better matched to outpatient workflows.

Which region leads revenue and which region is growing fastest?

North America led with 43.55% of revenue in 2025, while Asia-Pacific is expected to post the fastest growth at a 17.45% CAGR through 2031.

Which companies are shaping competition in robotic surgical procedures?

Intuitive Surgical remains the leading platform player, while Medtronic, Johnson & Johnson, PROCEPT BioRobotics, Stryker, and Smith+Nephew are expanding competition through specialty-focused and outpatient-oriented strategies.

Page last updated on: