Handheld Surgical Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

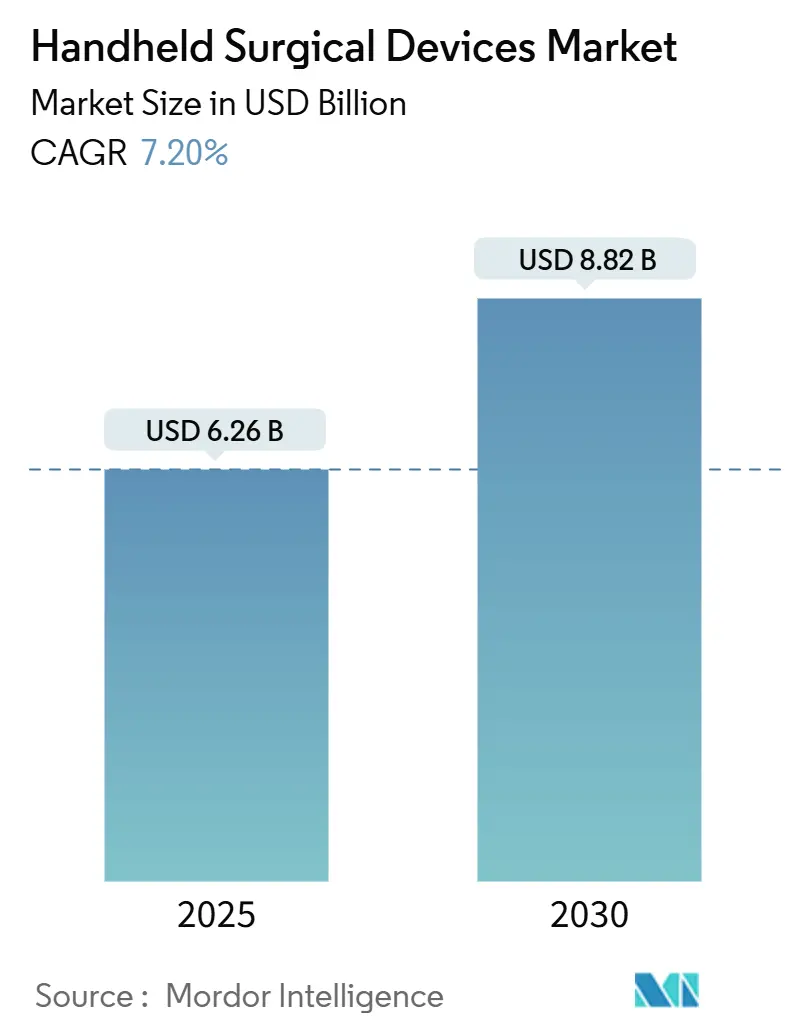

| Market Size (2025) | USD 6.26 Billion |

| Market Size (2030) | USD 8.82 Billion |

| Growth Rate (2025 - 2030) | 7.20% CAGR |

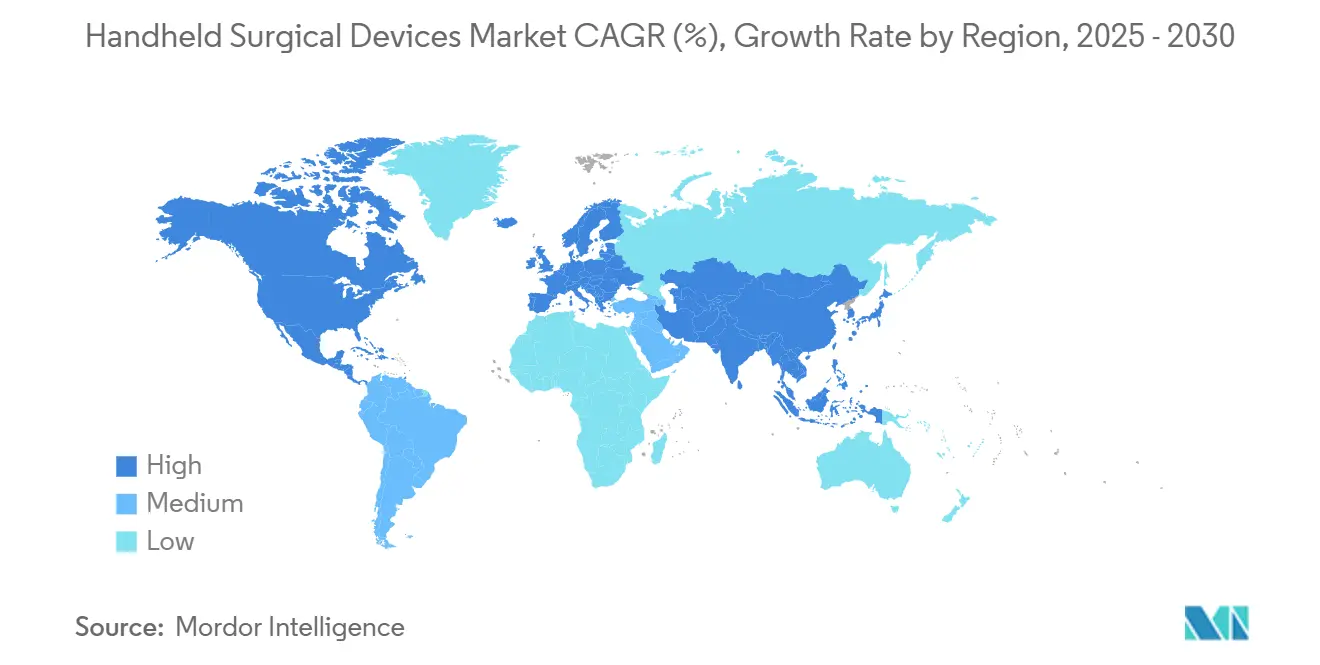

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Handheld Surgical Devices Market Analysis by Mordor Intelligence

The handheld surgical devices market size stood at USD 6.26 billion in 2025 and is forecast to reach USD 8.82 billion by 2030, advancing at a 7.2% CAGR during the period. Continued growth in minimally invasive procedures, rapid uptake of single-use tools for infection control, and investments in ergonomic designs keep demand resilient, even as supply chains for surgical-grade metals remain volatile. Major manufacturers now bundle force-sensing, AI-enabled feedback and multi-energy capabilities to differentiate portfolios, while hospitals accelerate device replacement cycles to comply with new U.S. Quality Management System Regulation requirements effective 2026. Expansion of outpatient surgery centers, particularly in orthopedics, offers a new volume tier that favors compact, battery-powered equipment and is reshaping distribution strategies. North America retains clear leadership thanks to high procedure volumes and Medicare spending on ambulatory surgical centers, but price-sensitive Asia Pacific shows the fastest unit growth, aided by volume-based procurement and regulatory streamlining in China.

Key Report Takeaways

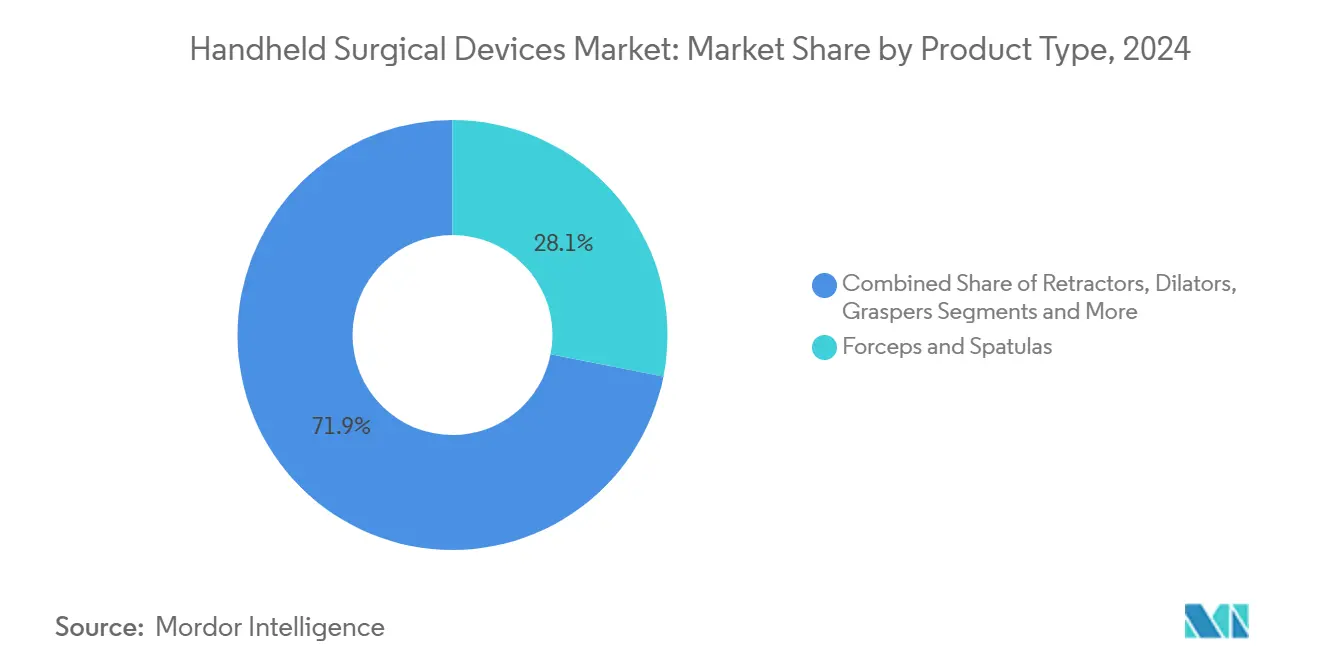

- By product type, forceps and spatulas led with 28.1% revenue share in 2024, while disposable laparoscopic scissors are projected to expand at an 8.9% CAGR through 2030.

- By application, laparoscopic surgery captured 24.5% of the handheld surgical devices market share in 2024; orthopedic surgery is forecast to post the highest CAGR at 9.8% to 2030.

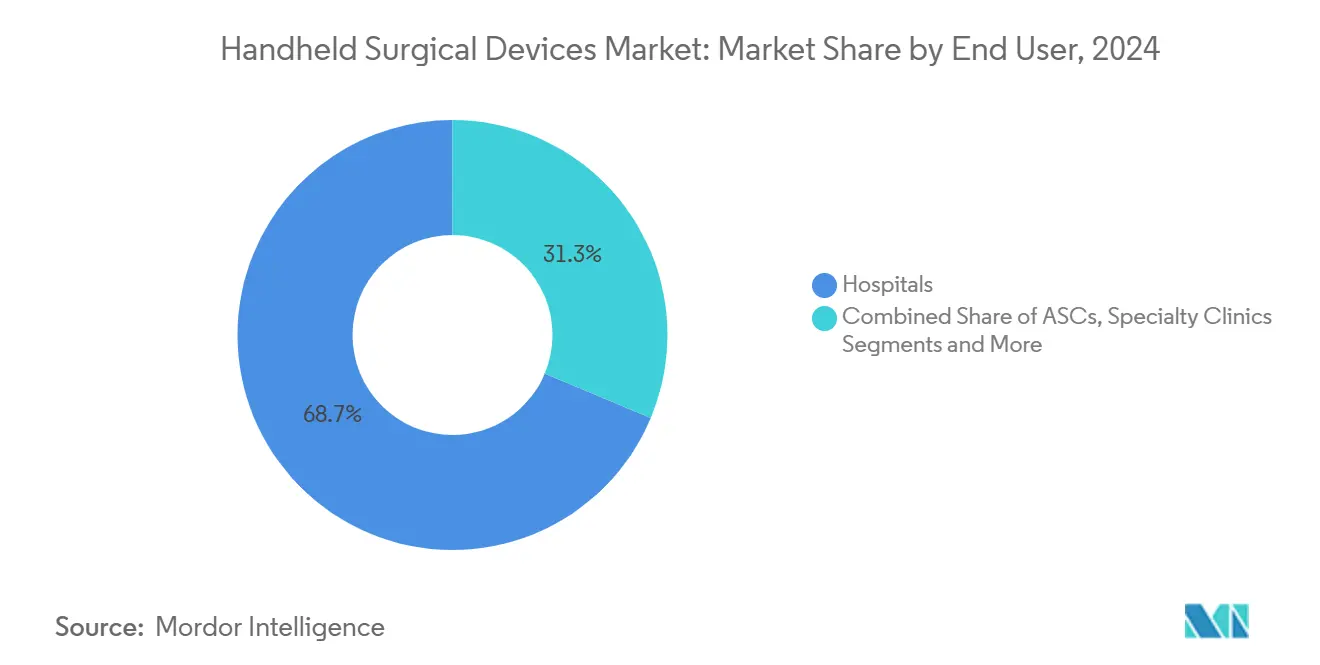

- By end user, hospitals accounted for 68.7% of the handheld surgical devices market size in 2024, whereas ambulatory surgical centers are expected to grow at an 8.4% CAGR during the outlook period.

- By region, North America commanded a 55.3% share in 2024, and Asia Pacific is projected to register a 7.4% CAGR from 2025 to 2030.

Global Handheld Surgical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of minimally invasive surgeries | 1.80% | North America & Europe, expanding worldwide | Medium term (2-4 years) |

| Growing geriatric population & chronic disease burden | 1.20% | Global, led by North America & APAC | Long term (≥ 4 years) |

| Technological advances in ergonomic & powered handheld tools | 1.00% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Increasing preference for single-use instruments | 0.90% | Global, fastest in post-pandemic systems | Short term (≤ 2 years) |

| AI-enabled sensing for real-time intra-operative feedback | 0.70% | North America & EU, selective in APAC | Long term (≥ 4 years) |

| Growth of outpatient surgery centers | 0.60% | North America, emerging in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Minimally Invasive Surgeries

Procedure counts for laparoscopic and robot-assisted operations are climbing steadily, with 2.63 million U.S. robotic cases in 2024 reflecting a 17% yearly rise.[1]American Hospital Association, “3 Ways Robotic Surgery Is Changing Health Care This Year,” aha.org This momentum underpins unit demand across the handheld surgical devices market as surgeons require slimmer, precision-engineered tools that navigate small access ports. Orthopedics shows the sharpest shift, highlighted by AI-equipped robotic systems such as Mako that refine bone-cut accuracy and shorten rehabilitation times. Vendors are miniaturizing graspers, retractors, and clip appliers while embedding haptic cues for safer tissue handling. Emerging African health networks, led by Egypt and South Africa, are starting to pilot laparoscopic suites, signaling early penetration potential despite infrastructure gaps.

Growing Geriatric Population & Chronic Disease Burden

An aging demographic generates heavier caseloads in orthopedics, cardiovascular and neurosurgery, each reliant on high-precision handheld systems. The global surgical robotics sector—valued at USD 3.92 billion in 2024—is projected to almost double by 2030 as hospitals target better outcomes for older patients. Longer operative times and complex anatomies push designers toward lighter, ergonomic handles that mitigate surgeon fatigue. Elevated Medicare reimbursements for joint replacements and spine fusion further amplify instrument turnover in North America, while APAC hospitals invest in powered saws and modular screwdrivers to tackle rising hip and knee revisions.

Technological Advances in Ergonomic & Powered Handheld Tools

Manufacturers now integrate multiple energy modalities within a single generator, exemplified by Johnson & Johnson MedTech’s DUALTO platform that trims operating-room footprint by 46% and permits dual-surgeon workflows. Cordless ultrasonic shears ease cable clutter and improve room sterility, with clinical trials showing performance parity to wired models. New handle geometries cut wrist hyper-flexion, and flex-articulated mechanical devices replicate robotic dexterity at a fraction of the cost. Powered screwdrivers and battery-assisted staplers are also gaining adoption in busy trauma centers that seek efficiency gains.

Increasing Preference for Single-Use Instruments for Infection Control

Post-COVID infection-control protocols have accelerated the swing toward disposables, the fastest-growing branch of the handheld surgical devices market. Eliminating reprocessing lowers per-case costs by more than USD 400 and removes sterilization bottlenecks. Surveyed scrub nurses frequently report debris on reprocessed devices, reinforcing safety concerns. Clarified FDA guidance on remanufacturing single-use items now outlines validation requirements, nudging facilities to reassess economic break-even points. Alberta Health Services and other health systems have banned the reuse of critical single-use devices, a policy likely to ripple outward.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pricing pressure from group-purchasing consolidation | -0.80% | North America & Europe, expanding globally | Short term (≤ 2 years) |

| Stringent reprocessing regulations raise ownership cost | -0.60% | Developed markets worldwide | Medium term (2-4 years) |

| Supply-chain volatility in surgical-grade steel & titanium | -0.50% | North America & Europe | Short term (≤ 2 years) |

| Emerging energy-based cutting modalities | -0.40% | North America & Europe, selective in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pricing Pressure from Group-Purchasing Consolidation

Six dominant GPOs control almost 90% of U.S. hospital purchasing volume, driving average 13.1% supply-cost cuts but squeezing device margins. Studies show some GPO contracts exceed direct-vendor prices for large systems, prompting selective side deals.[2]U.S. Government Accountability Office, “Group Purchasing Organizations: Services Provided to Customers,” gao.gov Administrative fees and formulary locks can slow the introduction of innovative handheld units, forcing smaller brands to seek alternative channels.

Stringent Reprocessing Regulations Raise Ownership Cost

New FDA QMSR rules harmonize with ISO 13485, compelling manufacturers to overhaul documentation and validation processes by 2026.[3]Food and Drug Administration, “Medical Devices; Quality System Regulation Amendments,” fda.gov Parallel policies covering ethylene-oxide sterilization and the definition of “remanufacturing” broaden liability for hospitals that refurbish devices, elevating lifecycle costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Forceps Remain Core as Disposable Scissors Accelerate

Forceps and spatulas controlled 28.1% of 2024 revenue, underscoring their ubiquity in virtually every surgical specialty. Hospitals routinely replenish these staples, and design tweaks—such as micro-serrated jaws and non-glare coatings—prolong their dominance. Disposable laparoscopic scissors, in contrast, are rocketing at an 8.9% CAGR as infection-control policies tighten; their unit economics improve further when factoring in sterilization room staffing cuts. Graspers now integrate capacitive sensors that translate tissue stiffness into tactile cues, while powered retractors with LED illumination help visualize deep cavities. Energy-based knives nibble at scalpel volumes, yet metal blades continue to play a role in skin incisions and micro-vascular graft prep. Front-line surgeons also adopt needle holders with ergonomic pistol-grip handles that lower forearm EMG activity, minimizing fatigue during lengthy micro-anastomoses.

Retractors and dilators retain a steady niche in the handheld surgical devices market, buoyed by neurosurgical and spinal applications where precise exposure is paramount. Hooks, probes, and suction lines occupy specialty micro-segments but collectively represent meaningful aftermarket revenue via tip disposables and single-use filters. Looking ahead, hybrid polymer-metal composites should help vendors offset metal-price shocks and enable lighter-weight tools that lessen hand strain during complex laparoscopic suturing.

By Application: Laparoscopy Dominates While Orthopedics Posts Fastest Pace

Laparoscopic surgery held a commanding 24.5% share in 2024, a testament to its cross-specialty utility and high patient acceptance. Surgeons rely on slim graspers, clip appliers, and scopes that integrate seamlessly with insufflation systems, driving consistent procurement cycles. Orthopedics, aided by robotic platforms and 3-D printed trial components, is projected to expand at a 9.8% CAGR, elevating the handheld surgical devices market size within joint arthroplasty suites. General surgery maintains healthy volumes through appendectomies and cholecystectomies, whereas cardiovascular teams invest in ultra-fine forceps and titanium micro-needle holders for valve repairs. Neurosurgery adopts AI-assisted micro-scissors paired with fluorescence imaging, and ENT clinics experiment with plasma-wand tonsillectomy devices that curtail post-op pain. Veterinary surgery emerges as a boutique segment, mirroring human trends in single-use packs but at lower price points.

Integration of AI decision-support is particularly pronounced in orthopedic operating rooms, where pre-op imaging feeds robotic saws and navigated screwdrivers. This data loop reduces alignment errors and drives follow-up demand for torque-limited hex drivers and cannulated reamers. As orthopedic ASCs proliferate, vendors bundle implants and disposable instrumentation to streamline case carts, boosting recurring revenue.

By End User: Hospitals Still Rule as ASCs Capture Momentum

Hospitals represented 68.7% of 2024 sales, reflecting their role as full-service surgical hubs with capital budgets for both reusable trays and advanced electrosurgery consoles. Complex oncology and trauma cases—often requiring instrument sets exceeding 120 pieces—anchor steady restock orders. Ambulatory surgical centers, however, are posting an 8.4% CAGR, siphoning volume from inpatient settings by focusing on high-throughput orthopedic and GI procedures. ASC operators seek turnkey kits that minimize room turnover times, steering growth toward modular, color-coded packs of clamps, scissors, and hemostats. Specialty clinics (e.g., fertility, ophthalmology) purchase niche micro-forceps, whereas academic institutions adopt sensor-enabled prototypes for skill-lab curricula, subtly shaping future demand.

ASC expansion is further propelled by payer incentives that favor outpatient settings for lower complication rates and shorter stays. Vendors, therefore, tailor marketing messages around reduced sterilization logistics, offering pre-sterile, procedure-specific sets that cut setup times by 15%. Hospitals respond by upgrading central sterile departments and piloting RFID-tagged trays to track instrument utilization and prevent loss.

By Usability: Reusable Dominance Faces Rising Disposable Wave

Reusable tools still command 72.8% of the handheld surgical devices market share, leveraging embedded sterilization infrastructure and long service life that withstands thousands of autoclave cycles. High-value sets such as orthopedic saws and cranial drills remain largely reusable due to precision components and purchase cost. Yet disposables—growing at 8.9% CAGR—gain ground wherever infection risk or reprocessing cost tilts the ROI equation toward single-use. Evidence shows hospitals can shave USD 400 per case by skipping re-sterilization labor, closing the total-cost gap even when unit price is higher. FDA guidance clarifying what constitutes remanufacturing has removed ambiguity and nudges providers to adopt validated disposable lines when reprocessing complexity rises. Innovations such as rigid polymer-based laparoscopic shears, once limited by blade durability, now incorporate ceramic edges that maintain sharpness for single-case use, opening doors to orthopedic knee balancers and hip reamers designed explicitly for one-time deployment.

Geography Analysis

North America generated 55.3% of 2024 revenue, powered by 2.63 million annual robotic procedures and Medicare’s USD 6.1 billion spend on ambulatory surgical center services. Mature reimbursement channels encourage hospitals to trial AI-integrated forceps and powered staplers, while supply contracts lock in multiyear pricing. Electrosurgery device sales alone are forecast to exceed USD 1.7 billion in the United States by 2032, supporting ancillary purchases of disposable pencil tips, bipolar forceps, and smoke evacuation tubing.

Asia Pacific represents the fastest-growing slice of the handheld surgical devices market at a 7.4% CAGR, buttressed by large patient pools and pro-innovation policies. China’s volume-based procurement programs pressure pricing but also force efficiencies that expand domestic manufacturing capacity and export potential. Regulatory reforms promise to chop device approval lead times by half, accelerating access for laparoscopic sets and energy generators. India, Thailand, and Indonesia are scaling surgical infrastructure via public-private partnerships, with rising middle-class insurance coverage swelling case volumes in uterine, gallbladder, and bariatric surgery.

Europe retains substantial share through robust hospital networks and leading OEM clusters in Germany and Switzerland. Harmonized CE MDR pathways gradually stabilize submission queues, allowing steady rollouts of next-gen ergonomic handles and single-use kits. Latin America and Middle East & Africa trail but post double-digit volume growth in select urban centers; Saudi Arabia’s Vision 2030 hospital build-out and Egypt’s medical tourism drive should spur incremental orders for general-surgery trays. Supply-chain constraints on titanium nevertheless hit these import-dependent regions hardest, occasionally delaying instrument replenishment cycles.

Competitive Landscape

The handheld surgical devices market is moderately consolidated, with Johnson & Johnson’s Ethicon unit holding roughly 12-13% share, followed by Medtronic at 4.6% and Stryker near 3%. Remaining demand fragments across dozens of regional or specialty manufacturers, giving buyers leverage but also creating whitespace for differentiated platforms. Recent M&A underscores a push into articulation and sensing: Medtronic bought Fortimedix Surgical to obtain single-port, articulating instruments, while Karl Storz moved to acquire Asensus Surgical to deepen robotics competencies. Teleflex’s USD 827 million purchase of BIOTRONIK’s vascular unit extends its reach into drug-coated balloons, signaling convergence between handheld devices and catheter-based therapies.

Technology roadmaps now emphasize haptic feedback and AI-driven decision support. Intuitive’s Force Feedback platform illustrates first-mover advantage, reducing tissue stress and sharpening surgeon perception. Patent filings for removable infinite-roll handles and embedded touch sensors hint at next-gen ergonomic leaps. Pricing pressure from GPOs fuels cost-optimized variants, prompting OEMs to bolster aftermarket revenue via proprietary single-use inserts and subscription analytics. Diversified supply strategies counter raw-material volatility, with large players dual-sourcing titanium from Asia and South America while exploring polymer-ceramic hybrids.

Competitive success increasingly hinges on digital ecosystems: cloud-based instrument-tracking dashboards, predictive maintenance for powered tools, and surgeon training portals integrated with VR modules. Those capabilities raise switching barriers and embed vendors deeper into hospital workflows. Smaller innovators focus on ultra-niche instruments—such as micro-vascular anastomotic couplers—banking on acquisition exits.

Handheld Surgical Devices Industry Leaders

Medtronic plc

Johnson & Johnson

Stryker Corporation

B. Braun Melsungen AG

Smith & Nephew plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Medtronic acquired Fortimedix Surgical, a company specializing in articulating surgical instruments, to enhance its surgical portfolio and strengthen offerings in minimally invasive surgical solutions

- August 2025: CooperSurgical expanded its portfolio by acquiring obp Surgical, enhancing its offerings in the handheld surgical devices market and reflecting ongoing consolidation within the industry.

- June 2024: Karl Storz agreed to acquire Asensus Surgical, consolidating resources and technologies to enhance its product portfolio and competitive positioning in the surgical instruments sector.

Global Handheld Surgical Devices Market Report Scope

| Forceps & Spatulas |

| Retractors |

| Dilators |

| Graspers |

| Scalpels & Blades |

| Scissors |

| Needle Holders |

| Hooks & Probes |

| Suction Tubes |

| Others |

| General Surgery |

| Orthopedic Surgery |

| Cardiovascular Surgery |

| Neurosurgery |

| Gynecology & Obstetrics |

| ENT Surgery |

| Plastic & Reconstructive Surgery |

| Urology Surgery |

| Veterinary Surgery |

| Other Applications |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Academic & Research Institutions |

| Reusable Instruments |

| Disposable Instruments |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Forceps & Spatulas | |

| Retractors | ||

| Dilators | ||

| Graspers | ||

| Scalpels & Blades | ||

| Scissors | ||

| Needle Holders | ||

| Hooks & Probes | ||

| Suction Tubes | ||

| Others | ||

| By Application | General Surgery | |

| Orthopedic Surgery | ||

| Cardiovascular Surgery | ||

| Neurosurgery | ||

| Gynecology & Obstetrics | ||

| ENT Surgery | ||

| Plastic & Reconstructive Surgery | ||

| Urology Surgery | ||

| Veterinary Surgery | ||

| Other Applications | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Academic & Research Institutions | ||

| By Usability | Reusable Instruments | |

| Disposable Instruments | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What was the worldwide revenue for handheld surgical tools in 2025?

The handheld surgical devices market size reached USD 6.26 billion in 2025.

Which product category currently leads sales?

Forceps and spatulas hold the top slot with 28.1% share of 2024 revenue.

Why are ambulatory surgical centers attracting vendors?

ASCs are expected to grow at an 8.4% CAGR, driven by cost advantages and payer support for outpatient orthopedic procedures.

Which region is expanding fastest?

Asia Pacific is projected to post a 7.4% CAGR between 2025 and 2030 as infrastructure and regulatory reforms accelerate device uptake.

How will new FDA QMSR rules affect manufacturers?

The 2026 alignment with ISO 13485 will raise compliance costs but streamline global submissions, benefiting companies with robust quality systems.

Are disposable or reusable instruments gaining ground?

Reusable tools still dominate, yet disposable variants are the fastest-growing, propelled by infection-control savings of more than USD 400 per case.

Page last updated on: