Disposable Surgical Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

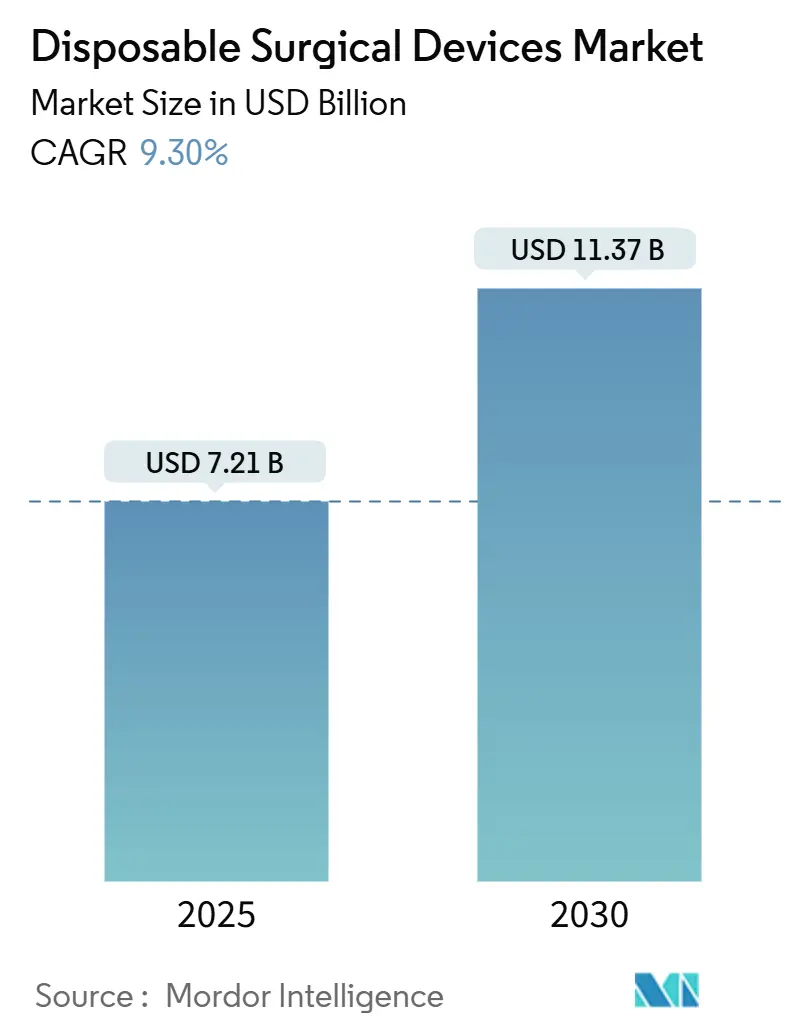

| Market Size (2025) | USD 7.21 Billion |

| Market Size (2030) | USD 11.37 Billion |

| Growth Rate (2025 - 2030) | 9.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Disposable Surgical Devices Market Analysis by Mordor Intelligence

The disposable surgical devices market size stands at USD 7.21 billion in 2025 and, at a forecast CAGR of 9.30%, is projected to reach USD 11.37 billion by 2030. Rising demand for infection-free interventions, quicker operating-room turnover, and lower sterilization overheads position single-use instruments as default choices in modern surgery. Hospitals in mature economies increasingly treat disposables as compliance tools in value-based reimbursement settings, while ambulatory surgical centers (ASCs) adopt them for lean, high-throughput care models. Concurrently, breakthroughs in high-precision polymer molding and RFID tracking embed digital traceability, easing inventory accounting and recall management. Regulatory momentum—most visibly Article 17 of the EU Medical Device Regulation—strips reprocessing of economic appeal, keeping the disposable surgical devices market on a durable growth path.

Key Report Takeaways

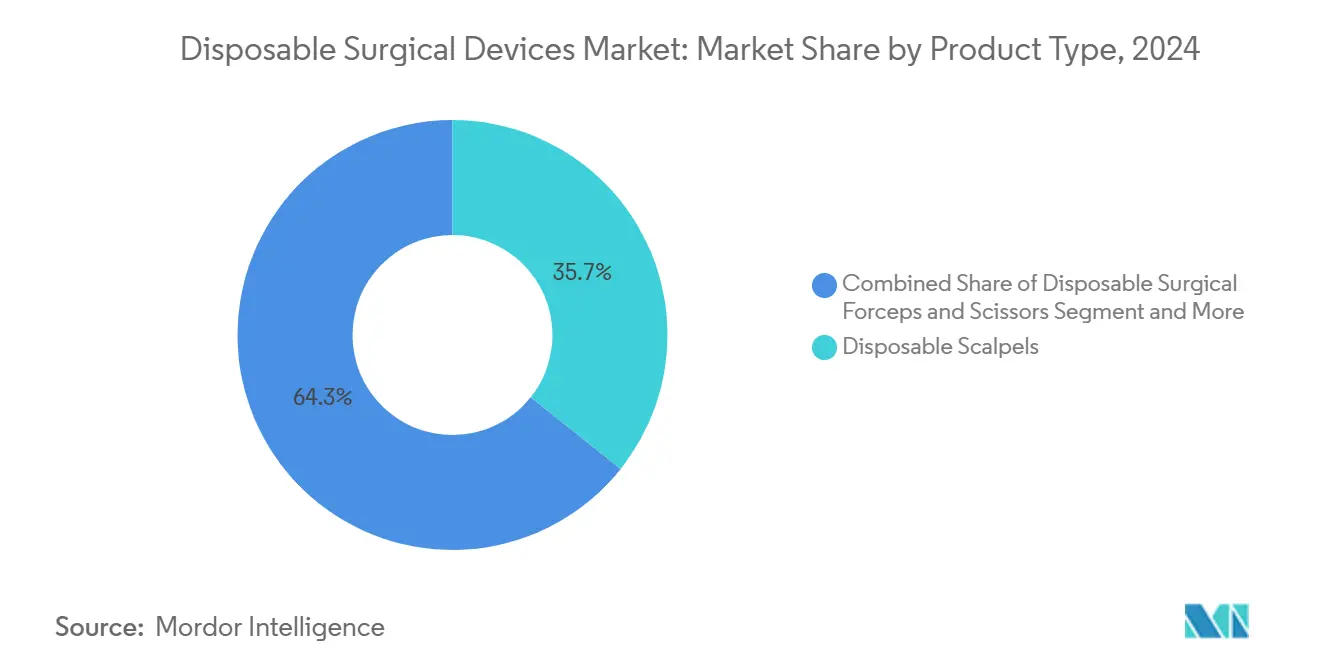

- By product type, disposable scalpels held 35.7% revenue share in 2024, whereas disposable staplers are set to expand at an 8.9% CAGR through 2030.

- By application, general surgery commanded 42.3% of the disposable surgical devices market share in 2024; bariatric surgery is advancing at a 10.2% CAGR through 2030.

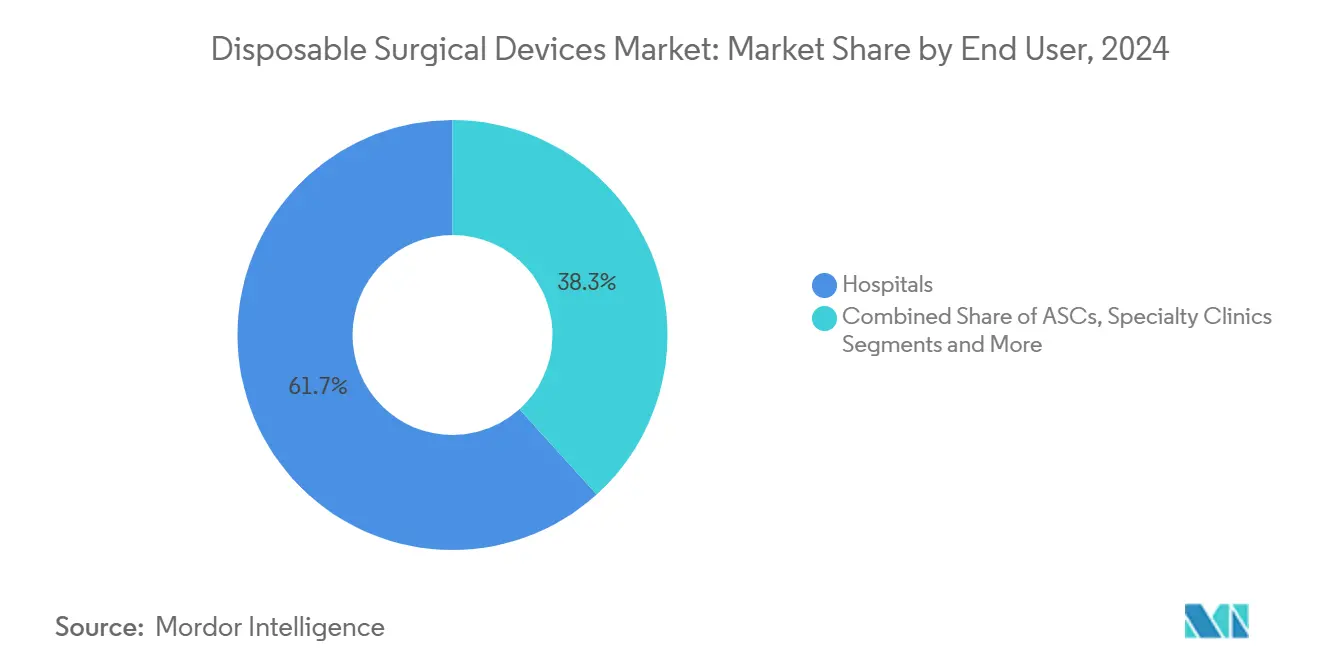

- By end user, hospitals retained a 61.7% share of the disposable surgical devices market in 2024; ASCs exhibit the fastest growth at a 9.1% CAGR to 2030.

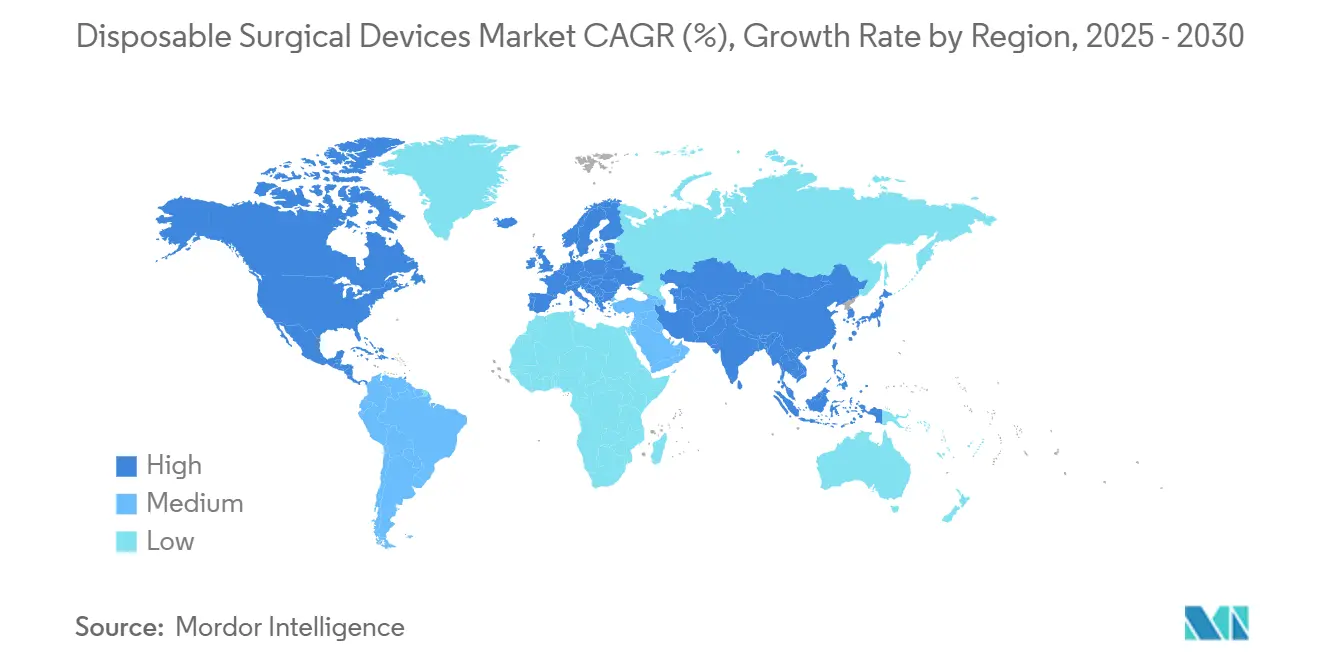

- By geography, North America led with 45.8% market share in 2024, while Asia Pacific is forecast to post the highest regional CAGR of 9.40% through 2030.

Global Disposable Surgical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Surgical Procedure Volume | +2.10% | Global | Long term (≥ 4 years) |

| Growing Focus On Infection-Control Boosting Single-Use Adoption | +1.80% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Technological Innovations In High-Precision Disposable Tools | +1.20% | Global, with early gains in North America, Europe | Medium term (2-4 years) |

| Surge In Minimally-Invasive & Outpatient Surgeries | +0.90% | Global, led by North America & Europe | Short term (≤ 2 years) |

| RFID-Enabled Inventory & Traceability Solutions Gaining Traction | +0.70% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Emergence Of Carbon-Neutral Single-Use Instruments | +0.60% | EU & North America, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Surgical Procedure Volume

Rapid procedure growth in aging OECD populations converges with expanded insurance coverage in emerging economies to create a rising floor for instrument demand. Health systems embracing value-based care reward shorter operating times, an area where disposables eliminate the reprocessing queue and lower instrument miscount risk. India’s medical device market is expected to jump from USD 11 billion in 2024 to USD 50 billion by 2025, confirming the long-run pull on single-use supplies.[1]Indian Embassy in Moscow, “Indian Medical Device Sector – An Overview,” indianembassy-moscow.gov.inCoupled with demographic surges, these forces ensure the disposable surgical devices market maintains double-digit volume growth well into the next decade.

Growing Focus on Infection-Control Boosting Single-Use Adoption

Healthcare-associated infections cost developed systems USD 28–45 billion annually, turning contamination control from a clinical nicety into a budget imperative. The CDC underscores that a single-use device “should be used once and discarded with routine waste”.[2]Centers for Disease Control and Prevention, “Best Practices for Single-Use (Disposable) Devices,” cdc.govPost-pandemic protocols raise penalties for breaches, tilting purchasing toward disposables that guarantee sterility. Europe’s MDR further restricts reprocessing pathways, locking in demand for original single-use instruments across regulated markets.

Technological Innovations in High-Precision Disposable Tools

Advanced polymer blends and micro-molding now deliver blade sharpness, ergonomic balance, and tactile feedback on par with premium reusables. Integrated RFID chips achieve 100% usage tracking accuracy and trim counting time by up to 87% in trial ORs. Verathon’s video laryngoscope, built with 80% bio-based resin, slashes its carbon footprint by 74%, proving that sustainability and performance can coexist in high-acuity devices.

Surge in Minimally Invasive & Outpatient Surgeries

ASCs now conduct 72% of U.S. surgeries, delivering 45–60% cost savings and 20% faster scheduling than hospitals. Their economics hinge on near-zero turnover delays, a feat possible only with ready-to-go disposables. Medicare’s 2025 data show ASCs treated 3.4 million beneficiaries, up 2.5% year-over-year, validating the outpatient momentum. As robotic and laparoscopic techniques proliferate, they demand single-use staplers and trocars engineered for precise deployment in tight anatomical windows, reinforcing the disposable surgical devices market growth curve.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Medical-Waste Legislation & Sustainability Scrutiny | -1.40% | EU & North America, expanding globally | Medium term (2-4 years) |

| Cost Pressures In Low-Resource Healthcare Settings | -0.80% | APAC emerging markets, MEA, South America | Long term (≥ 4 years) |

| Breakthroughs In In-House Sterilization Extending Life Of Reusables | -0.60% | Global, with higher impact in cost-sensitive markets | Medium term (2-4 years) |

| Supply-Chain Volatility For Specialty Medical-Grade Polymers | -0.50% | Global, acute in Asia Pacific manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Medical-Waste Legislation & Sustainability Scrutiny

Hospitals generate 5.9 million tons of waste each year, much of it single-use plastics.[3]Journal of Cleaner Production, “Sustainable Healthcare and Environmental Life-Cycle Impacts of Disposable Supplies,” sciencedirect.com European procurement guidelines increasingly demand life-cycle assessments, pressuring buyers to justify every disposable purchase. FDA-validated reprocessing programs cut costs by up to 60%, challenging original manufacturers to innovate or lose share. Response strategies include hybrid “Resposable” platforms that reduce waste by 70% and carbon emissions by 80 tons per facility annually.

Cost Pressures in Low-Resource Healthcare Settings

In price-sensitive markets across APAC, MEA, and South America, disposable kits compete against bulk-purchased reusables amortized over years. Supply-chain shocks, from polymer shortages to shipping delays, further inflate landed costs. Some facilities adopt enhanced in-house sterilization, extending reusable life cycles and delaying disposable conversion. Nonetheless, tightening infection-control norms in urban tertiary centers should gradually override the cost hurdle, widening the addressable base for the disposable surgical devices industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Scalpels Lead While Staplers Accelerate

Disposable scalpels accounted for 35.7% of the disposable surgical devices market share in 2024, underscoring their indispensable role across virtually every procedure. Segment volumes move in lockstep with overall case counts, ensuring predictable baseline demand. Staplers, by contrast, represent only a mid-teen percentage of current revenues yet are projected to log the highest 8.9% CAGR, propelled by bariatric, colorectal, and thoracic minimally invasive operations that require precision closure at depth. The disposable surgical devices market size for staplers is forecast to reach USD 3.9 billion in 2030, more than doubling its 2025 contribution. RFID-enabled cartridge recognition, ergonomic reload handles, and bio-absorbable staple lines offer competitive edges for suppliers focused on next-generation closure.

Refinements in scissor metallurgy substitute hardened tungsten inserts with composite silicone-carbide edges, granting single-case sharpness without grinders. Forceps makers integrate molded finger stops to reduce pinch injuries and fatigue on high-volume shift days. Trocar innovations emphasize bladeless tips and integrated smoke evacuation, meeting laparoscopic visibility standards without reusable filter add-ons. Each micro-improvement nudges surgeons toward disposables perceived as premium yet predictable, reinforcing the dominant scalpels franchise while accelerating stapler uptake.

By Application: General Surgery Dominance Meets Bariatric Surge

General surgery captured 42.3% of 2024 revenue, effectively anchoring the disposable surgical devices market size at USD 3.0 billion that year. Universal instrument lists—scalpels, clamps, pestles, and needle drivers—translate any uptick in appendectomies, cholecystectomies, or hernia repairs into proportional device pull-through. Nevertheless, bariatric procedures, growing at 10.2% CAGR, will expand their slice from USD 0.6 billion in 2025 to nearly USD 1.0 billion by 2030. Sleeve gastrectomy popularity and robotic system penetration (16.7% of Roux-en-Y gastric bypass by 2024) make gastric stapling cartridges the hero SKU.

Cardiovascular and orthopedic lines show mid-single-digit gains, as cross-clamp disposables and bone saw blades shift to single-use to curb prion disease fears. Gynecology maintains a steady mid-teens unit share: disposable hysteroscopic scissors and energy devices address infection-risk aversion in fertility clinics. Importantly, application overlap means one procedure may consume a multi-instrument tray, compounding revenue yield for vendors able to offer full disposable portfolios.

By End User: Hospital Dominance Challenged by ASC Growth

Hospitals held 61.7% of the disposable surgical devices market share in 2024, equal to USD 4.4 billion in revenue. Integrated supply chains and purchasing consortia drive bulk deals, while enterprise tracking systems embed RFID tags into instrument labels for closed-loop post-operative reconciliation. Yet ASCs, expanding at 9.1% CAGR, should raise their draw from USD 1.7 billion in 2025 to USD 2.8 billion by 2030. Payors redirect elective ortho and GI cases to outpatient settings, where 20-minute room-turn targets demand grab-and-go sterile kits. Specialty clinics—especially dermatology and ophthalmology—adopt compact disposable sets conforming to office-based surgery policies, incrementally enlarging the demand pie.

ASCs’ lean staffing magnifies the value of all-in-one procedure packs: one nurse can flip rooms without central sterile support. Manufacturers capturing this segment design color-coded packaging and QR-linked instructions for rapid verification, mirroring consumer packaging cues to simplify clinical workflows. The hospital franchise remains stable, but ASC expansion injects high-growth momentum, supporting the broader disposable surgical devices market trajectory.

Geography Analysis

North America represented 45.8% of global revenue in 2024, translating to a disposable surgical devices market size of USD 3.3 billion. CMS reimbursement models reward reduced infection-related readmissions, and U.S. Joint Commission audits reference disposable options as mitigation levers, spurring adoption in high-acuity centers. Canada mirrors this stance, with provincial authorities funding ASC expansions to offload elective waitlists and favoring single-use kits to minimize cross-province sterilization logistics. Supply resilience initiatives drive near-shoring of polymer molding, granting regional players cost and lead-time advantages.

Europe contributed a steady mid-20% share, buoyed by stringent MDR oversight and climate strategies that paradoxically stimulate premium “green” disposables. Hospitals deploy life-cycle assessment dashboards to justify purchases, prompting suppliers to document CO₂ savings via bio-based plastics. Programs like the U.K. National Health Service's “Net-Zero Supplier Roadmap” stipulate carbon disclosure by 2027, so European manufacturers emphasize neutral production pipelines to safeguard tenders.

Asia Pacific, the fastest-growing territory at 9.40% CAGR, is on course to double its disposable surgical devices market size from USD 1.3 billion in 2025 to USD 2.6 billion by 2030. China’s tier-three hospitals standardize single-use laparoscopic kits to gain JCI accreditation and attract medical tourism. India’s burgeoning insurance penetration and Make-in-India incentives encourage domestic production, countering import dependence while amplifying surgical device volumes. ASEAN states roll out universal health schemes, and private hospital chains specify disposables to comply with international infection-control norms sought by expatriate patients.

Middle East & Africa and South America account for a combined sub-10% share yet post mid-single-digit CAGRs. Gulf Cooperation Council members channel oil windfalls into flagship hospital projects stocked almost entirely with single-use kits. In Brazil, Anvisa reforms shorten device approval lead times, widening market access but cost constraints keep reusables relevant in public facilities. Overall, geographic diversification dilutes concentration risk and cushions vendors against region-specific regulatory shocks.

Competitive Landscape

The disposable surgical devices market features a moderate Herfindahl-Hirschman index; the top five suppliers control an estimated 52% share, leaving ample runway for midsized innovators. Incumbents defend their share via vertically integrated polymer compounding and cartridge stamping, locking in cost efficiencies. Medtronic’s late-2024 acquisition of Fortimedix extended its access port portfolio, an example of bolt-on deals filling perioperative white spaces. Smith & Nephew’s USD 3.92 billion medtech budget earmarks USD 70 million for robotic disposable lines, signaling heavyweight commitment to next-gen automation.

Technology pipelines emphasize RFID-labeled handles, optical UDI scanners, and sensor-embedded tips measuring real-time tissue impedance for energy devices. Google’s “sterile field interactive control display” patent foreshadows touch-less screen panels enabling surgeons to manipulate imaging without breaking sterility, positioning disposables as data carriers inside interconnected OR ecosystems. Sustainability turns into a differentiator: Verathon’s 80% bio resin laryngoscope and Elemental Healthcare’s Resposable range headline marketing narratives centered on carbon metrics, resonating with European tenders.

Supply-chain vulnerabilities remain the Achilles’ heel. Specialty polymer granule shortages inflated input costs by up to 20% in 2024. Manufacturers respond through dual-sourced feedstocks, vendor-managed inventories, and on-site compounding to buffer disruptions. Resulting consolidation should incrementally lift average selling prices, cushioning margin erosion while bolstering after-sales support capabilities.

Disposable Surgical Devices Industry Leaders

Johnson & Johnson

Medtronic plc

Stryker Corporation

Becton, Dickinson and Company

B. Braun Melsungen AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Verathon launched Spectrum QC eco, the first bio-based single-use video laryngoscope, cutting carbon emissions by 74%.

- November 2024: Medtronic acquired Fortimedix, strengthening its minimally invasive tool lineup.

- September 2024: Spartan Medical broadened its single-use sterile instrument portfolio.

- June 2024: Olympus America introduced CELERIS, the world’s first disposable sinus debrider, enabling treatment room procedures.

Global Disposable Surgical Devices Market Report Scope

| Disposable Scalpels |

| Disposable Surgical Forceps |

| Disposable Surgical Scissors |

| Disposable Surgical Staplers |

| Disposable Trocars & Cannulas |

| Others |

| General Surgery |

| Gynecological Surgery |

| Cardiovascular Surgery |

| Orthopedic Surgery |

| Other Surgeries |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Disposable Scalpels | |

| Disposable Surgical Forceps | ||

| Disposable Surgical Scissors | ||

| Disposable Surgical Staplers | ||

| Disposable Trocars & Cannulas | ||

| Others | ||

| By Application | General Surgery | |

| Gynecological Surgery | ||

| Cardiovascular Surgery | ||

| Orthopedic Surgery | ||

| Other Surgeries | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the disposable surgical devices market?

The disposable surgical devices market size is USD 7.2 billion in 2025 and is on track to hit USD 11.3 billion by 2030.

Which region leads adoption of single-use surgical tools?

North America holds 45.8% market share, driven by strict infection-control norms and high procedure volumes.

Which product category is growing the fastest?

Disposable staplers are advancing at an 8.9% CAGR through 2030 as minimally invasive surgeries proliferate.

Why are ambulatory surgical centers important for future growth?

ASCs rely on ready-to-use kits to meet rapid turnover targets, propelling a 9.1% CAGR in disposable demand from this channel.

How are sustainability concerns being addressed?

Vendors introduce bio-based plastics, hybrid Resposable, designs, and life-cycle transparency to meet tightening environmental procurement rules.

What impact does RFID technology have on the market?

RFID-embedded instruments provide 100% usage visibility and cut counting time by up to 87%, boosting hospital efficiency and strengthening the value proposition for disposables.

Page last updated on: