Microsurgery Robot Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

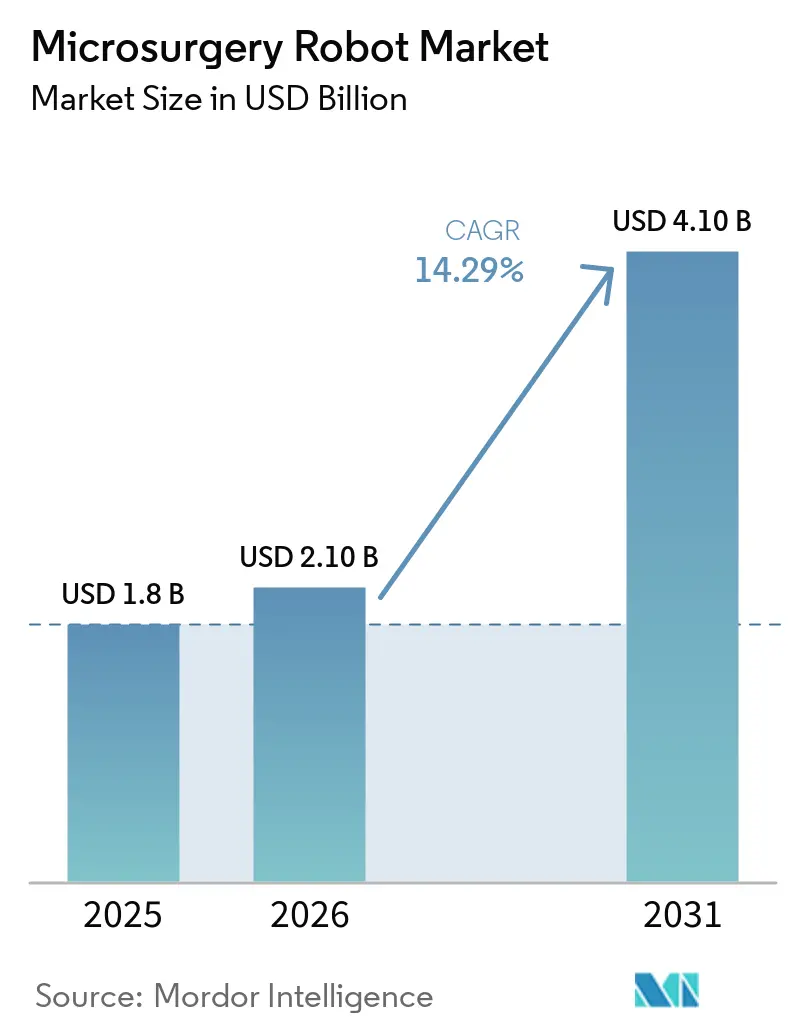

| Market Size (2026) | USD 2.10 Billion |

| Market Size (2031) | USD 4.10 Billion |

| Growth Rate (2026 - 2031) | 14.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microsurgery Robot Market Analysis by Mordor Intelligence

The Microsurgery Robot Market size is projected to expand from USD 1.8 billion in 2025 and USD 2.10 billion in 2026 to USD 4.10 billion by 2031, registering a CAGR of 14.29% between 2026 to 2031.

Hospitals are accelerating robot purchases to close a widening skill gap in supermicrosurgery, where fewer than 200 Nort.h American surgeons can reliably execute sub-millimeter anastomoses unaided. The April 2024 De Novo authorization of the Symani system validated motion-scaling and tremor-filtration technologies that cut hand tremor by up to 90% in bench testing[1]U.S. Food and Drug Administration, “De Novo Classification Request for Symani Surgical System,” fda.gov. Oncology remains the revenue anchor, yet reconstructive procedures linked to secondary lymphedema are expanding faster as CPT codes and payer policies mature. Vendors that combine robotic data capture with vision augmentation tools are differentiating on productivity, shortening operative times by more than 20% in early U.S. experience.

Key Report Takeaways

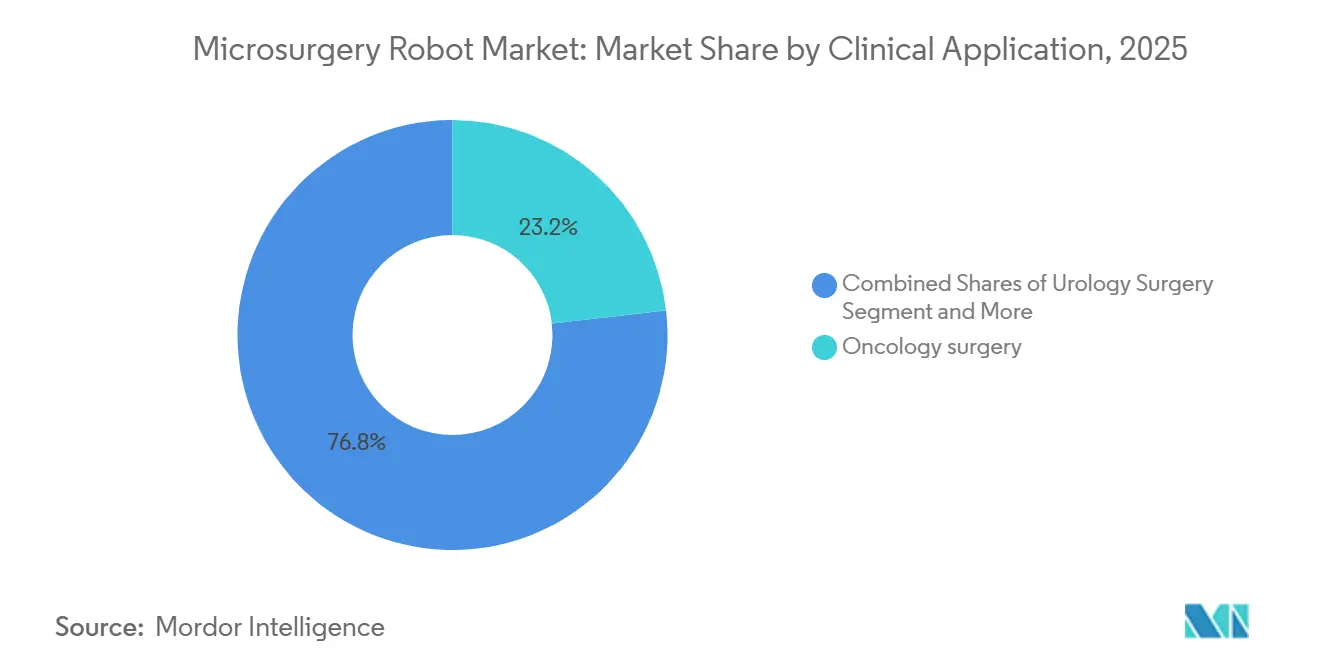

- By clinical application, oncology surgery led with 23.18% of the microsurgery robot market share in 2025, while reconstructive surgery is forecast to post the highest 16.56% CAGR through 2031.

- By technology, teleoperated multi-arm platforms held 58.16% share of the microsurgery robot market size in 2025, whereas semi-autonomous systems are projected to grow at a 17.12% CAGR over 2026-2031.

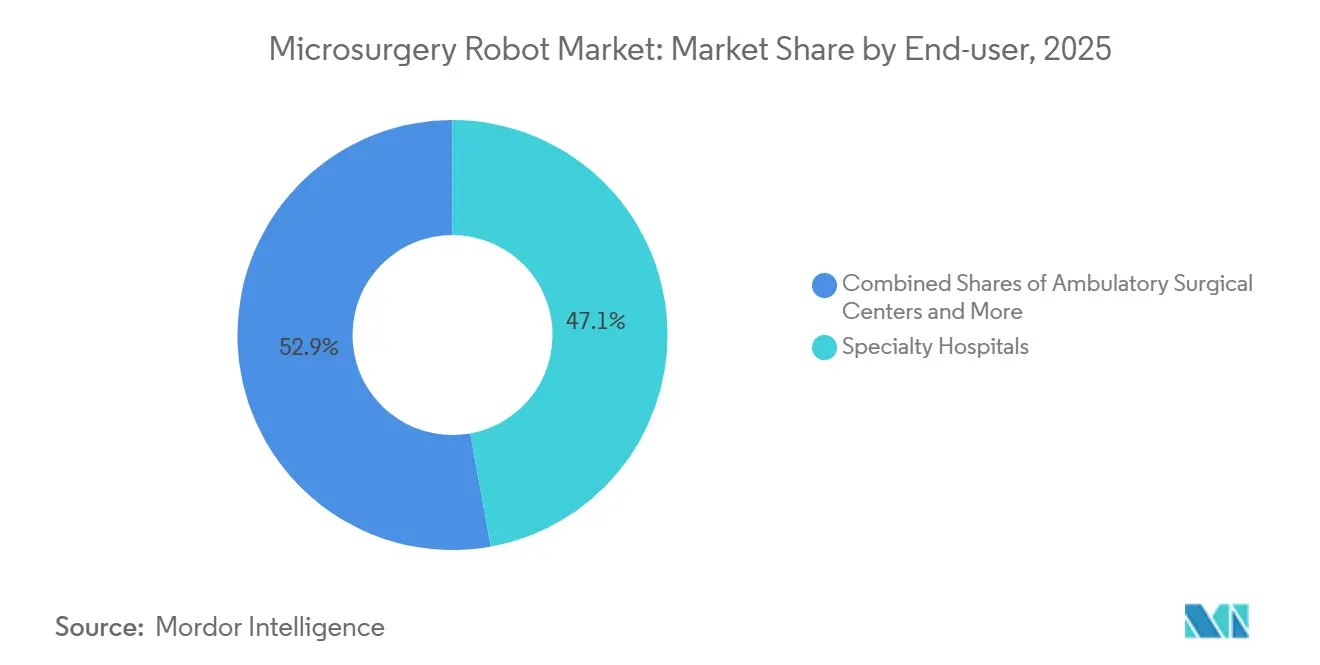

- By end user, specialty hospitals captured 47.15% of 2025 installations, yet ambulatory surgical centers are advancing at a 16.93% CAGR to 2031.

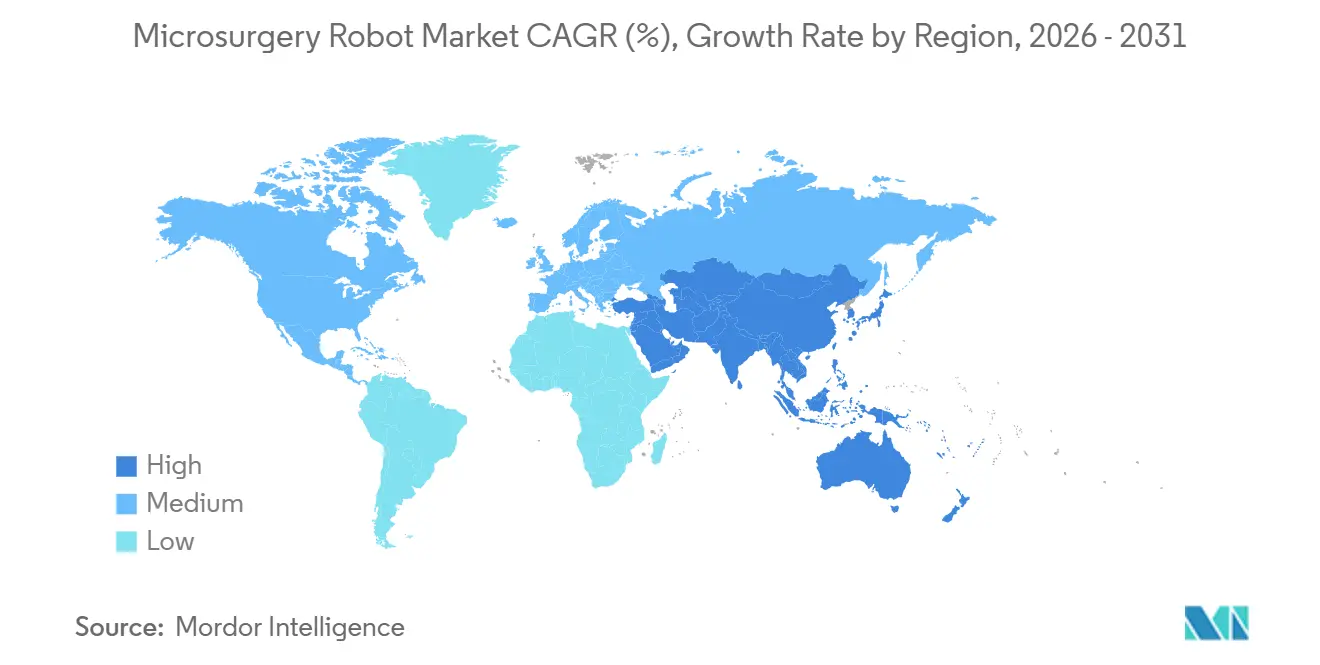

- By geography, North America commanded 45.18% of 2025 revenue, while Asia-Pacific is set to expand at a 17.77% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Microsurgery Robot Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising lymphedema burden and demand for lymphatic and microvascular reconstruction | +3.2% | Global, with peak demand in North America and Europe | Medium term (2-4 years) |

| CE-marked purpose-built microsurgery robots enabling motion scaling and tremor filtration in sub-millimeter anastomoses | +2.8% | North America, Europe, APAC core markets | Short term (≤ 2 years) |

| Clinical validation in ophthalmic and ENT microsurgery (retina, cochlear) expanding addressable procedures | +2.5% | North America, Europe, Japan | Medium term (2-4 years) |

| Digitization of open microsurgery workflows (robotic data capture, vision augmentation, AI guidance) | +2.1% | Global, early adoption in academic medical centers | Long term (≥ 4 years) |

| Surgeons' skill bottleneck in supermicrosurgery accelerating hospitals' shift to robotic platforms | +1.9% | Global, acute in regions with aging surgeon workforce | Short term (≤ 2 years) |

| Gene/cell therapy delivery use-cases (e.g., subretinal injections) requiring robotic precision | +1.4% | North America, Europe (gene therapy approval concentrated) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Lymphedema Burden and Demand for Lymphatic and Microvascular Reconstruction

Lymphedema affects 250 million people worldwide, including 10 million in the United States [2]National Lymphedema Network, “Updated Lymphedema Prevalence Statistics,” lymphnet.org. Lymphovenous anastomosis reduces limb volume by 14.26% at one year and lets nearly half of the patients taper compression garments. Robots that scale hand motion 10:1 or 20:1 permit general plastic surgeons to match fellowship-trained outcomes, and proficiency arrives in 15 robotic cases versus 40 manual cases. Demand is reinforced by the incidence of breast cancer-related lymphedema as survivorship lengthens.

CE-Marked Purpose-Built Microsurgery Robots Enabling Motion Scaling and Tremor Filtration in Sub-Millimeter Anastomoses

European centers gained a three-year head start after Symani and MUSA secured CE marks in 2021-2022, logging more than 900 clinical cases by 2025. Motion scaling converts a 10-mm hand move into a 1-mm instrument motion, and Kalman filters delete tremor frequencies above 8 Hz, cutting positional variance by up to 90% [3]IEEE Transactions on Biomedical Engineering, “Adaptive Notch Filtering for Surgical Tremor Suppression,” ieee.org. Classifying these robots as assistive rather than autonomous devices eased reimbursement talks with European payers.

Clinical Validation in Ophthalmic and ENT Microsurgery Expanding Addressable Procedures

Preceyes technology inside the KINEVO 900 platform enables sub-100-micron retinal work, improving gene-vector delivery success to 18 of 20 patients in a 2024 U.S. trial versus 12 of 20 historically. In cochlear surgery, the HEARO system lowers electrode insertion forces by 40%, preserving residual hearing. Such data encourage hospitals to extend robots beyond lymphatic cases into ophthalmology and ENT.

Digitization of Open Microsurgery Workflows

Robots record every instrument path and force applied. Academic centers are converting these datasets into AI coaching modules that warn surgeons if suture angles risk tearing fragile vessels. Integrated fluorescence or OCT overlays shorten operative time by 22% in early U.S. use because surgeons no longer glance away to external screens. Digital case logs then feed privileging committees, creating data-driven credentialing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost, setup time, and uncertain reimbursement pathways in early-stage indications | -2.3% | Global, acute in ambulatory surgical centers and community hospitals | Short term (≤ 2 years) |

| Regulatory stringency and need for large-scale, multi-center outcomes evidence | -1.6% | North America, Europe (FDA, EMA pathways) | Medium term (2-4 years) |

| Limited instrument ecosystems and cross-specialty workflow integration | -1.2% | Global, particularly affecting multi-specialty academic medical centers | Medium term (2-4 years) |

| Credentialing and training standardization gaps slow multi-site scale-up | -1.0% | North America, Europe, with spillover to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost, Setup Time, and Uncertain Reimbursement Pathways in Early-Stage Indications

Systems list from USD 500,000 to USD 2.5 million, excluding yearly service contracts that approach USD 100,000. Symani setup consumes up to one hour, cutting a daily block by one case and diluting ASC economics. CPT codes cover lymphatic work yet offer no uplift for robotic technique, so hospitals self-fund the delta while ENT and neurovascular indications lack any code.

Regulatory Stringency and Need for Large-Scale, Multi-Center Outcomes Evidence

The FDA requested long-term patency data beyond 50 patients for the MUSA-3 filing, slowing its U.S. entry. Europe’s MDR compels post-market surveillance registries that strain smaller entrants financially. Lymphovenous cohorts often carry obesity or radiation comorbidities, so trials need more sites and time to hit statistical power, stretching enrollment to 36 months on average.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Clinical Application: Oncology Anchors Revenue, Reconstructive Surgery Accelerates

Oncology procedures held 23.18% of the 2025 microsurgery robot market share, reflecting complex free-flap reconstruction that demands multiple supermicrosurgical anastomoses. Reconstructive work is forecast to expand at a 16.56% CAGR, lifting the microsurgery robot market size for this segment as lymphedema cases climb.

Hospitals view reconstructive indications as a volume engine because each breast cancer survivor represents a long-term candidate for lymphovenous bypass. Meanwhile, ophthalmology adoption is accelerating through gene-therapy delivery, the first ophthalmic use case to prove clear clinical benefit. Cardiovascular and gastrointestinal adoption remains muted because their vessel diameters do not require sub-millimeter accuracy.

By Technology or Control Mode: Teleoperation Dominates, Semi-Autonomous Systems Gain Ground

Teleoperated multi-arm systems accounted for 58.16% of 2025 revenue, benefiting from surgeon familiarity and an easier regulatory path that mirrors da Vinci precedents. Semi-autonomous micro-robots are projected to grow 17.12% each year to 2031 as retinal and gene-therapy workflows rely on imaging-based waypoints.

The microsurgery robot market size for co-manipulated devices remains smaller because they lack motion scaling, although their minimal footprint suits small operating rooms. Regulators favor human-in-the-loop architectures, yet China’s Kai system shows that piezoelectric precision may shift benchmarks if it secures FDA approval.

By End User: Specialty Hospitals Lead, Ambulatory Centers Surge

Specialty hospitals captured 47.15% of installations in 2025, leveraging high reconstructive volumes and a commercial-payer mix. Ambulatory surgical centers, however, are advancing at a 16.93% CAGR as payers route lymphovenous cases to lower-cost sites, boosting the microsurgery robot market. Community hospitals struggle to justify capital outlays because they log fewer than 20 procedures annually and lack fellowship-trained surgeons. Academic medical centers hold 28% of revenue thanks to clinical trials and training mandates, positioning them as opinion leaders that set credentialing standards.

Geography Analysis

North America held 45.18% of 2025 revenue. Early CPT coding and the April 2024 FDA clearance of Symani created commercial momentum, and private insurers now approve lymphovenous anastomosis when performed robotically on a case-by-case basis. Canada’s single-payer system moves more slowly because capital budgets are locked years ahead, while Mexico’s private hospitals lure U.S. patients at 40% lower procedure cost.

Asia-Pacific is forecast to expand at the fastest 17.77% CAGR as Chinese tertiary hospitals bought 74 units in the first half of 2025, worth more than 700 million RMB or about USD 96 million. Japan shows strong academic use, with 162 robotic pancreatoduodenectomy cases by mid-2025, but national reimbursement remains under review. South Korea and Australia provide targeted subsidies and recent regulatory clearances that open niche demand, although rural dispersion limits utilization outside major cities.

Europe contributed a significant share of the 2025 turnover after CE marks allowed earlier adoption. Germany, the United Kingdom, and France account for a notable share of regional installs, yet decentralized hospital governance and NHS budget tightening moderate growth. Post-market surveillance under MDR raises the cost of entry for smaller firms, though Germany’s reimbursement parity between robotic and manual lymphatic surgery smooths hospital economics. Adoption in the Middle East, Africa, and South America remains less percentage due to limited reimbursement frameworks.

Competitive Landscape

The microsurgery robot market remains moderately fragmented. No vendor exceeds major share, and early movers Medical Microinstruments and Microsure focus on lymphatic and reconstructive cases. Carl Zeiss Meditec dominates ophthalmic niches after acquiring Preceyes in 2020, merging robotics with its KINEVO 900 visualization suite. ForSight Robotics raised USD 100 million in June 2024 to refine retinal robots that deliver sub-50-micron accuracy, signaling competition around ophthalmology.

KouTech’s Kai platform, cleared in China during 2024, advertises 0.1-micron precision and may challenge incumbents once it pursues FDA review. Patent races now center on motion-scaling algorithms and integrated imaging; systems offering 10 degrees of freedom and fluorescence overlays fetch premiums of 20%-30% over handheld devices. Regulatory divergence forces vendors to split resources, as U.S. 510(k) pathways rely on predicates while Europe’s MDR emphasizes post-market evidence.

Microsurgery Robot Industry Leaders

Medical Microinstruments, Inc.

MicroSure B.V.

Carl Zeiss Meditec AG

ForSight Robotics Ltd.

Ophthorobotics AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Medical Microinstruments, Inc announced the commercial launch in the U.S. of its Robotic Suture. The first suture purpose-built for the Symani Surgical System represents MMI’s continued innovation in microsurgery and is suitable for cases where delicate suturing is required.

- February 2026: Affluent Medical adopted a new name, Carvolix, after buying fellow innovators Caranx Medical and Artedrone. By bringing the two companies’ micro-robotics and biomimetic implant know-how in-house, the group is now positioned as a single, integrated medtech player focused on AI-driven surgical solutions.

- December 2025: Medical Microinstruments secured FDA 510(k) clearance for Symani Dissection Instruments, widening platform use into tissue-plane separation and lymph-node dissection.

Global Microsurgery Robot Market Report Scope

As per the scope of the report, microsurgery robots are sophisticated systems designed to assist surgeons in performing highly delicate procedures on minute anatomical structures, such as nerves, blood vessels, and tiny bones, which often measure less than 1 mm in diameter. These systems primarily aim to overcome the natural limitations of the human hand, specifically by eliminating physiological tremors and providing motion scaling, which translates larger hand movements from a surgeon into much finer, sub-millimeter actions at the surgical site.

The microsurgery robots market is segmented by clinical application, technology/control mode, end-user, and geography. Based on clinical applications, the market is segmented into oncology surgery, urology surgery, obstetrics and gynecology surgery, micro anastomosis, reconstructive surgery, ENT surgery, gastrointestinal surgery, cardiovascular surgery, neurovascular surgery, ophthalmology surgery, and other applications. By technology, the market is segmented into teleoperated multi-arm microsurgical systems, co-manipulated/handheld robotic assist systems, and semi-autonomous image-guided micro-robots. By end users, the market is segmented into Academic medical centers, Specialty hospitals, Ambulatory surgical centers, and Community / General hospitals.

Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Oncology surgery |

| Urology surgery |

| Obstetrics and gynecology surgery |

| Micro anastomosis |

| Reconstructive surgery |

| ENT surgery |

| Gastrointestinal surgery |

| Cardiovascular surgery |

| Neurovascular surgery |

| Ophthalmology surgery |

| Other applications |

| Teleoperated multi-arm microsurgical systems |

| Co-manipulated/handheld robotic assist systems |

| Semi-autonomous image-guided micro-robots |

| Academic medical centers |

| Specialty hospitals |

| Ambulatory surgical centers |

| Community / General hospitals |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Clinical Application | Oncology surgery | |

| Urology surgery | ||

| Obstetrics and gynecology surgery | ||

| Micro anastomosis | ||

| Reconstructive surgery | ||

| ENT surgery | ||

| Gastrointestinal surgery | ||

| Cardiovascular surgery | ||

| Neurovascular surgery | ||

| Ophthalmology surgery | ||

| Other applications | ||

| By Technology | Teleoperated multi-arm microsurgical systems | |

| Co-manipulated/handheld robotic assist systems | ||

| Semi-autonomous image-guided micro-robots | ||

| By End-user | Academic medical centers | |

| Specialty hospitals | ||

| Ambulatory surgical centers | ||

| Community / General hospitals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the microsurgery robot market in 2026?

The microsurgery robot market size reached USD 2.1 billion in 2026 and is set to reach USD 4.1 billion by 2031, reflecting a 14.29% CAGR.

Which clinical segment grows fastest through 2031?

Reconstructive procedures linked to lymphedema are projected to post the highest 16.56% CAGR over 2026-2031.

Which technology leads current installations?

Teleoperated multi-arm platforms held 58.16% of 2025 microsurgery robot market share, topping other control modes.

What geography offers the strongest growth outlook?

Asia-Pacific is forecast to expand at 17.77% annually through 2031 due to large Chinese procurement mandates.

Page last updated on: