Surgical Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 21.42 Billion |

| Market Size (2031) | USD 31.62 Billion |

| Growth Rate (2026 - 2031) | 8.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surgical Equipment Market Analysis by Mordor Intelligence

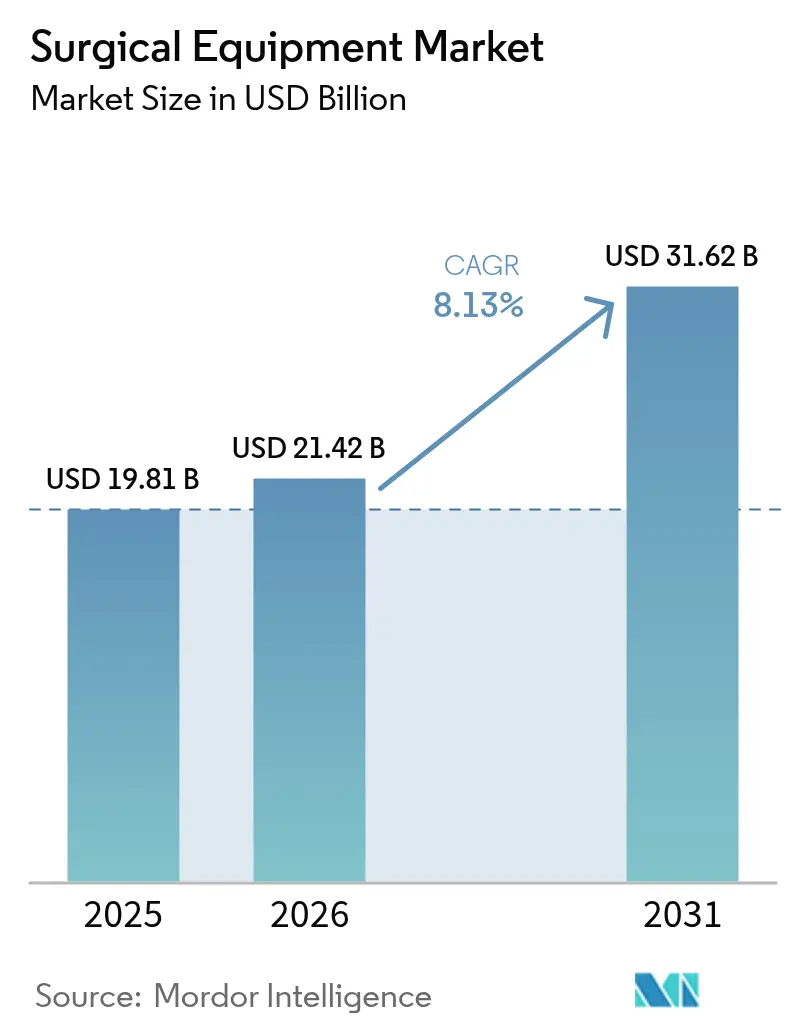

The Surgical Equipment market size is expected to grow from USD 19.81 billion in 2025 to USD 21.42 billion in 2026 and is forecast to reach USD 31.62 billion by 2031 at 8.13% CAGR over 2026-2031.

Rising procedure volumes strengthen the outlook, rapid uptake of minimally invasive techniques, and the growing presence of ambulatory surgical centers (ASCs). Powered and electrosurgical devices are set to lead product growth as clinicians seek instruments that cut, seal, and coagulate tissue in a single step. Asia-Pacific is on course to record the fastest regional expansion, reflecting capacity build-outs in China and India alongside steadily rising surgical volumes. Competitive intensity is growing as niche innovators challenge established brands with compact, workflow-specific systems designed for outpatient settings. Capital constraints in hospitals and ASCs are nudging suppliers toward flexible financing and per-procedure pricing, reshaping purchasing dynamics across the surgical equipment market.

Key Report Takeaways

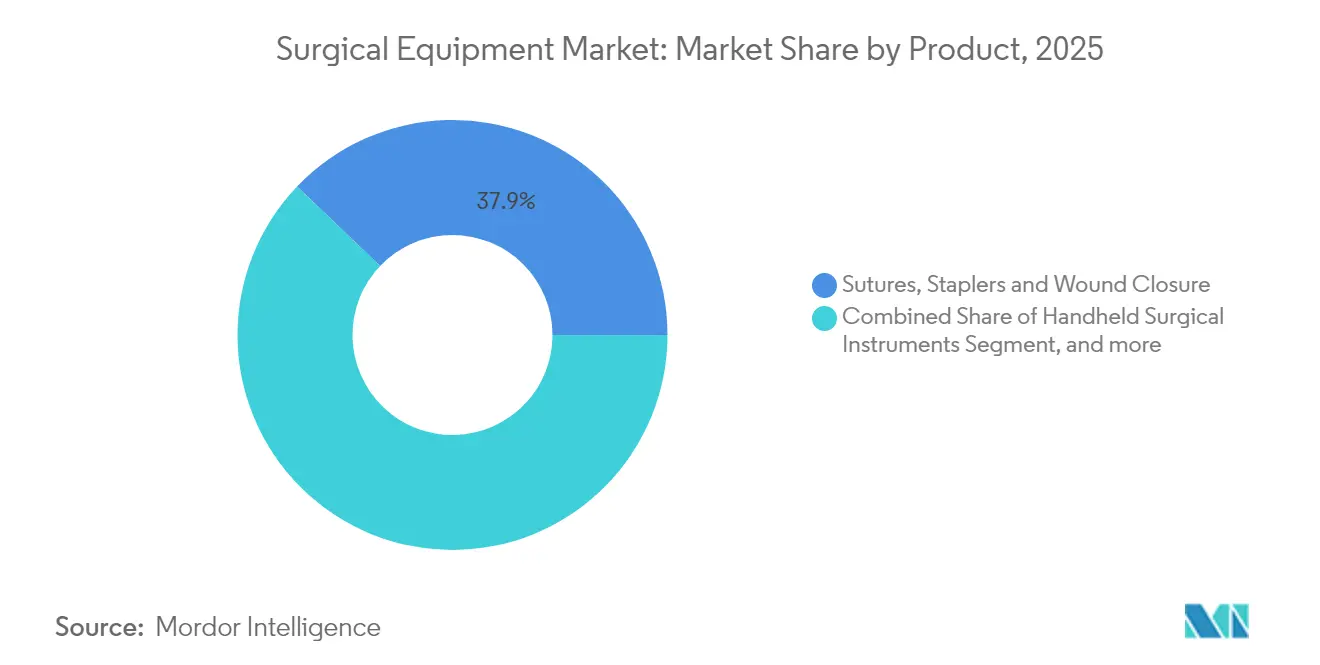

- By product type, sutures, staplers, and other wound-closure devices held 37.86% of the surgical equipment market share in 2025, while powered and electrosurgical devices are projected to grow at an 8.45% CAGR to 2031.

- By application, orthopedic and trauma surgeries commanded a 24.55% share of the surgical equipment market size in 2025, whereas plastic, cosmetic, and burn reconstruction is forecast to expand at an 8.76% CAGR through 2031.

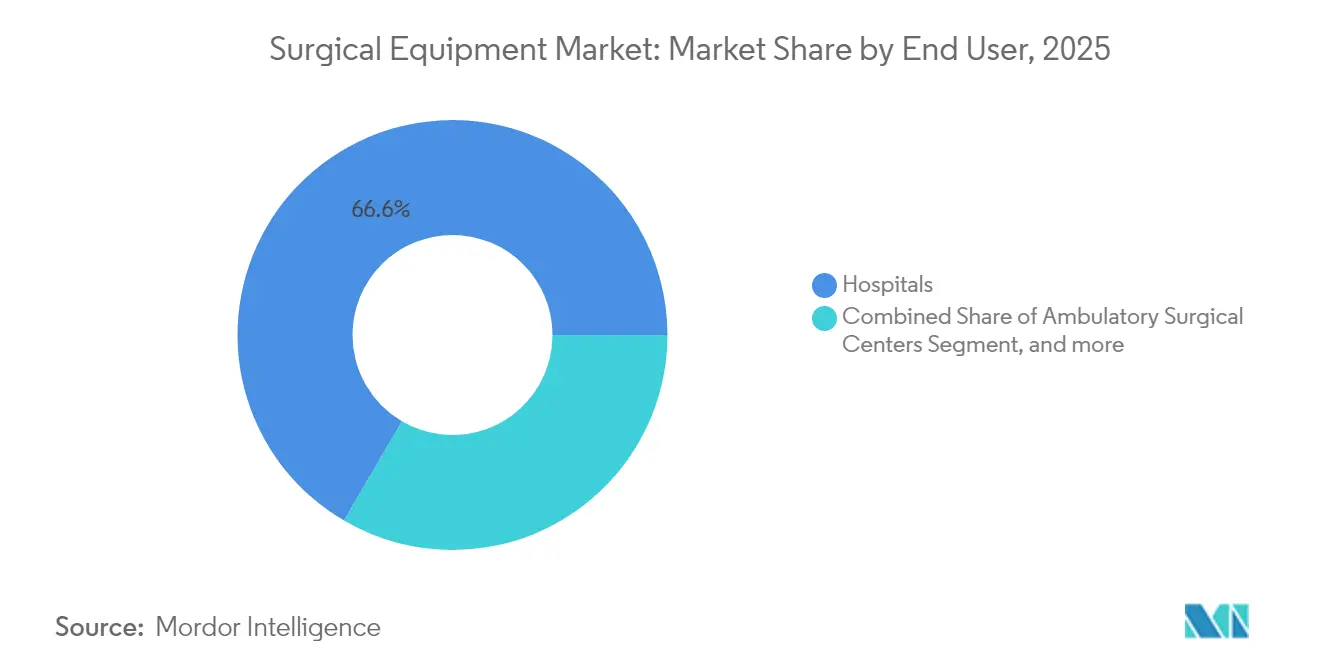

- By end user, hospitals maintained an 66.58% revenue share in 2025; ASCs are advancing at a 8.97% CAGR to 2031.

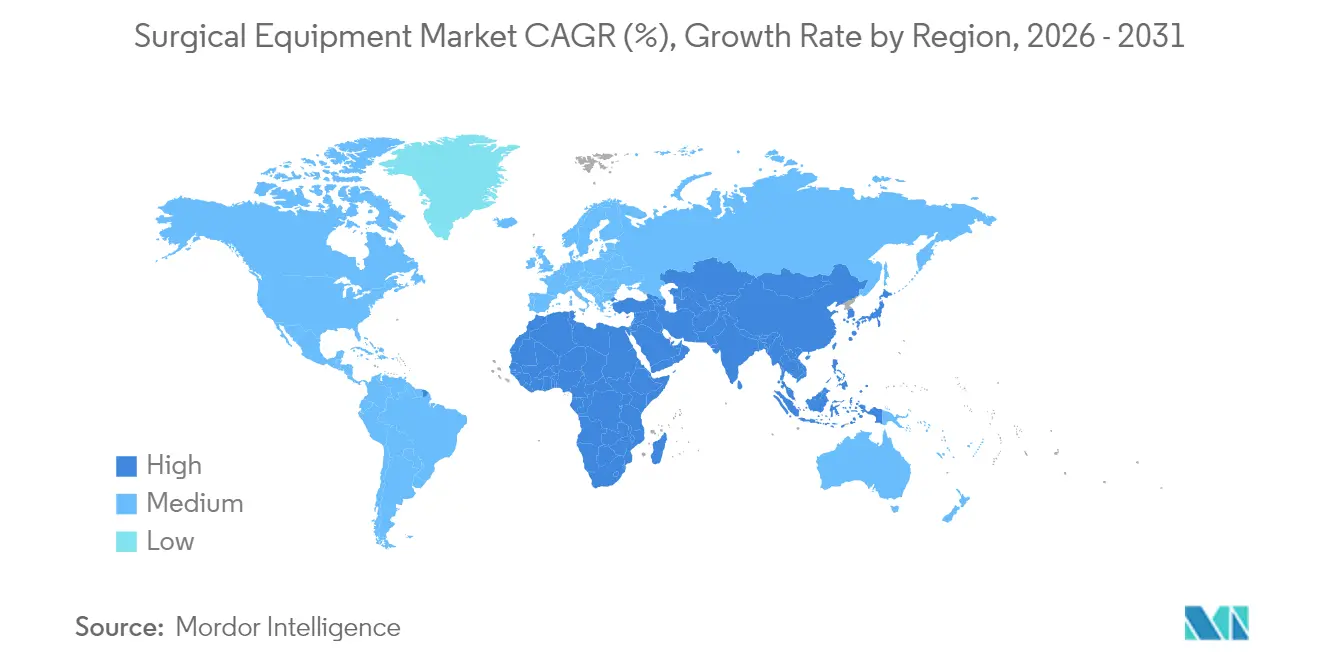

- By geography, North America led with 35.12% revenue share in 2025, while Asia-Pacific is projected to post an 8.69% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surgical Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising surgical procedure volumes | +2.1% | North America, Europe, Global | Medium term (2-4 years) |

| Increase in road-traffic and other accidents | +1.2% | Developing regions, Global | Short term (≤ 2 years) |

| Shift toward minimally invasive & robotic surgery | +2.5% | North America, Europe, Developed APAC | Medium term (2-4 years) |

| Growth of ASCs and outpatient care | +1.8% | North America, Emerging in Europe | Short term (≤ 2 years) |

| Adoption of disposable & single-use instruments | +1.0% | Developed markets, Global | Short term (≤ 2 years) |

| Expanding healthcare infrastructure in emerging economies | +1.9% | APAC, Middle East, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Procedure Volumes Driven by Aging & Chronic-Disease Prevalence

Procedure counts continue to climb, with roughly 235 million major operations performed each year. Orthopedic, cardiovascular, and oncology surgeries account for much of the incremental volume as global populations age and the burden of chronic disease rises.[1]Johnson & Johnson MedTech, “Global Procedure Growth Outlook,” jnjmedtech.com Manufacturers are responding by tailoring instruments to high-volume specialties rather than offering broad, general-purpose sets, improving throughput and reducing waste. Orthopedic procedures are growing 7.2% annually, spurring demand for powered saws, drills, and navigation aids. Cardiovascular interventions are advancing 5.8% per year, prompting investment in hybrid operating rooms that combine imaging and minimally invasive capabilities. The net effect is a sustained need for reliable, procedure-specific systems that can withstand heavy daily utilization.

Rising Number of Road and Other Accidents

Road-traffic injuries and workplace trauma continue to elevate demand for fracture fixation hardware, portable imaging, and navigation systems that enable rapid intervention in emergency settings.[2]BMJ Innovations, “Trauma device advancements,” bmj.com Beyond traditional plates and screws, trauma surgeons now seek integrated platforms capable of guiding screw placement in real time, shortening operative windows, and limiting repeat surgeries. Device makers have carved out a dedicated trauma segment within orthopedics, with growth outpacing general orthopedic equipment as hospitals expand major-injury centers and stock trauma-ready kits.

Accelerated Shift Toward Minimally Invasive & Robotic-Assisted Surgeries

Robotic and laparoscopic techniques have crossed the adoption threshold in urology, gynecology, and general surgery, bringing smaller incisions, quicker discharges, and fewer complications. Twenty new robotic systems are in development, promising competitive price points and vertical specialty expansion. Multi-visceral platforms capable of moving seamlessly from colorectal to thoracic cases are shifting the value equation toward adaptable robotic architectures. As device prices fall, mid-tier hospitals and high-volume ASCs are entering the market, widening the installed base and raising procedure counts for associated instruments and disposables.

Growth of Ambulatory Surgical Centers and Outpatient Care Models

ASCs currently perform 72% of U.S. procedures and are on track for a 25% volume jump by 2029, underpinned by 45-60% cost savings over hospital equivalents. Outpatient operators prioritize compact, easily sterilized devices that support fast room turnovers. Suppliers able to miniaturize consoles and bundle imaging and energy modalities into single units gain traction. Policy shifts that add complex orthopedic and cardiac codes to outpatient reimbursement lists are accelerating the case migration, compelling hospitals to reinvent surgical service lines and update equipment procurement strategies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and maintenance costs | -1.5% | Global, pronounced in price-sensitive markets | Medium term (2-4 years) |

| Stringent regulatory requirements | -0.8% | North America, Europe, Global | Medium term (2-4 years) |

| Shortage of skilled surgical workforce | -0.9% | Developing regions, Global | Long term (≥ 4 years) |

| Budget constraints delaying equipment upgrades | -0.7% | North America, Europe, Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Maintenance Costs of Advanced Surgical Systems

A top-tier robotic platform can cost more than USD 2 million, with annual service contracts adding 10-15%. Smaller hospitals and ASCs often defer purchases or seek pay-per-use models that link expenses to utilization.[3]American Hospital Association, “Cost of Robotic Platforms,” aha.org Leasing, profit-sharing, and risk-pooling agreements are gradually easing barriers, yet capital-intense systems remain concentrated in large academic centers.

Stringent Regulatory Approval & Compliance Requirements

Post-market surveillance mandates and unique device identifiers add complexity and cost to product launches. The United Kingdom’s evolving Medical Device Regulations and the FDA’s heightened scrutiny of AI-enabled devices lengthen approval timelines. Larger manufacturers can absorb these costs more readily, widening the competitive gulf between multinationals and start-ups.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Wound Closure Dominates While Electrosurgery Accelerates

Sutures, staplers, and other closure devices held 37.86% of the surgical equipment market share in 2025, underlining their universal role across specialties. Barbed sutures that eliminate knot-tying have shaved an average 1 minute 43 seconds off cesarean section closure times, demonstrating workflow value. Johnson & Johnson’s ECHELON ENDOPATH Staple Line Reinforcement illustrates how biomaterial advances can protect tissue and reduce leaks.

Powered and electrosurgical systems are projected to expand at an 8.45% CAGR through 2031. Instruments such as Medtronic’s LigaSure Maryland jaw blend cutting and vessel-sealing, cutting operative steps, and collateral damage. Retractors, handheld forceps, and surgical power tools remain essential staples, but the frontier lies in integrated consoles that merge energy, imaging, and smoke evacuation, streamlining the sterile field. The surgical equipment market size for powered devices is likely to gain further momentum as outpatient centers adopt multifunction towers for space efficiency.

By Application: Orthopedics Leads While Aesthetics Accelerates

Orthopedic and trauma cases accounted for 24.55% of the surgical equipment market size in 2025. Stryker’s CD NXT power system, which offers real-time drilling depth feedback, highlights the push toward safer, data-rich joint reconstruction. Robotic guidance platforms such as Mako are widening minimally invasive joint-replacement adoption, shortening hospital stays, and lowering revision rates.

Plastic, cosmetic, and burn reconstruction procedures are forecast to grow at an 8.76% CAGR through 2031, buoyed by growing patient interest in aesthetic enhancements and refinements in regenerative tissue technology. Cardiovascular and thoracic surgery maintains solid demand owing to high disease prevalence, while neurosurgery benefits from improved intra-operative visualization. The surgical equipment industry continues to diversify, with bariatric and gynecologic specialties embracing robotic single-port platforms that reduce trocar entries and postoperative pain.

By End User: Hospitals Dominate While ASCs Surge

Hospitals controlled 66.58% of global revenue in 2025, leveraging multidisciplinary teams and intensive-care backups for complex surgeries. Rising operating costs, however, have stretched capital budgets; the average age of installed equipment has climbed as purchases are deferred. This dynamic opens doors for vendors offering upgrade paths and usage-based finance.

ASCs are growing at a 8.97% CAGR and redefining procurement criteria. Devices must be compact, quick to sterilize, and interoperable across specialties to justify floor space. The surgical equipment market size tied to ASCs is amplified by CMS rule changes that reimburse more complex orthopedic and cardiac codes outside hospital walls. Specialty clinics and physician offices remain niche but present opportunities for ultra-portable, battery-powered platforms.

Geography Analysis

North America held 35.12% of 2025 revenue, driven by favorable reimbursement and early adoption of robotic and AI-enabled systems. Hospitals are under cost pressure, but ASCs are flourishing, reflecting payer incentives and patient preference for same-day procedures. Ongoing capital modernization delays have increased the average equipment life cycle, pushing providers toward service contracts and rental models. Nonetheless, U.S. and Canadian centers remain the proving ground for next-generation robotic and digital-surgery suites.

Europe presents a broad landscape anchored by robust public health systems. Germany, France, and the United Kingdom spearhead uptake of minimally invasive platforms. New Medical Device Regulations strengthen post-market oversight, raising compliance costs yet bolstering patient safety. Southern and Eastern European markets, upgrading legacy infrastructure, represent catch-up growth pockets where mid-priced, versatile instruments gain favor.

Asia-Pacific is the fastest-growing zone, advancing at an 8.69% CAGR through 2031. China is now the second-largest buyer of robotic theaters, supported by domestic manufacturers who tailor designs to local budgets. Japan leads in procedure volumes per capita, while India targets 15% annual device adoption via tax incentives and streamlined approvals. Southeast Asian nations are adding surgical suites in provincial hubs, fueling demand for turnkey, bundled equipment packages that include on-site training and service warranties.

The Middle East & Africa and South America offer long-range potential as governments allocate larger health budgets to surgical infrastructure. Private-sector hospital chains in Brazil and the Gulf Cooperation Council are early adopters of robotic systems, setting benchmarks that public facilities strive to match.

Competitive Landscape

The surgical equipment market is moderately fragmented, with Medtronic, Johnson & Johnson, Stryker, and Intuitive Surgical occupying leading positions through broad portfolios and global supply chains. Technology-centric differentiation is intensifying; Medtronic is layering AI onto surgical planning to optimize staple line selection, whereas Johnson & Johnson is integrating digital tracking into orthopedic implant workflows. Twenty emerging robotic platforms are in the pipeline, signaling heightened rivalry and potential price pressure. Vertical integration is on the rise as manufacturers extend into imaging, software, and post-acute monitoring to lock in recurring revenue and deepen customer stickiness.

Niche challengers focus on single-specialty systems, cost-efficient disposables, or ASC-tailored mini consoles. Strategic acquisitions, such as Stryker’s purchase of Inari Medical to add mechanical thrombectomy devices, demonstrate how incumbents plug capability gaps and enter high-growth adjacencies. Ecosystem playbooks that bundle hardware, software, and analytics are becoming standard as buyers seek end-to-end solutions that simplify multi-vendor coordination.

Surgical Equipment Industry Leaders

CONMED Corporation

Olympus Corporation

Stryker Corporation

B Braun Melsungen AG

Smith & Nephew plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Intuitive received FDA clearance for its SureForm 45 stapler for use with the da Vinci SP surgical system, expanding its capabilities in urologic and thoracic procedures for use with its da Vinci SP surgical system in thoracic, colorectal, and urologic procedures.

- March 2025: Johnson & Johnson MedTech showcased its VELYS Robotic-Assisted Solution with FDA clearance for unicompartmental knee arthroplasty, enhancing precision in joint replacements.

- February 2025: Stryker completed the acquisition of Inari Medical, expanding its vascular portfolio with projected sales contribution of USD 590 million for 2025. This acquisition brings Inari's peripheral vascular and venous thromboembolism (VTE) expertise to Stryker, including novel mechanical thrombectomy solutions like the FlowTriever and ClotTriever systems.

Global Surgical Equipment Market Report Scope

As per the scope of this report, surgical equipment is functionally designed for the operating room to centralize all surgical support equipment and utility services. Surgical equipment is a specially designed tool that performs actions during surgery or operation. The surgical equipment market is segmented by product (handheld devices, powered and electrosurgical devices, and sutures and staplers), application (obstetrics and gynecology, orthopedics, cardiovascular, neurology, plastic and reconstructive surgeries, and other applications), end user (hospitals, ambulatory surgical centers, and other end users) and geography (North America, Europe, Asia Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (USD million) for the above segments.

| Handheld Surgical Instruments | Forceps & Graspers |

| Scalpels & Blades | |

| Retractors & Dilators | |

| Powered & Electrosurgical Devices | High-frequency Electrosurgery Units |

| Ultrasonic & Plasma Energy Systems | |

| Surgical Power Tools | |

| Sutures, Staplers & Wound Closure | Absorbable Sutures |

| Non-absorbable Sutures | |

| Manual Staplers | |

| Sealants & Tissue Adhesives | |

| Others |

| Orthopedic & Trauma |

| Cardiovascular & Thoracic |

| Obstetrics & Gynecology |

| Neurosurgery & Spine |

| Plastic, Cosmetic & Burn Reconstruction |

| Gastrointestinal & Bariatric |

| Other Surgeries |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics & Physician Offices |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Handheld Surgical Instruments | Forceps & Graspers |

| Scalpels & Blades | ||

| Retractors & Dilators | ||

| Powered & Electrosurgical Devices | High-frequency Electrosurgery Units | |

| Ultrasonic & Plasma Energy Systems | ||

| Surgical Power Tools | ||

| Sutures, Staplers & Wound Closure | Absorbable Sutures | |

| Non-absorbable Sutures | ||

| Manual Staplers | ||

| Sealants & Tissue Adhesives | ||

| Others | ||

| By Application | Orthopedic & Trauma | |

| Cardiovascular & Thoracic | ||

| Obstetrics & Gynecology | ||

| Neurosurgery & Spine | ||

| Plastic, Cosmetic & Burn Reconstruction | ||

| Gastrointestinal & Bariatric | ||

| Other Surgeries | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics & Physician Offices | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the surgical equipment market?

The surgical equipment market size is USD 21.42 billion in 2026.

How fast is the market expected to grow?

Revenue is forecast to reach USD 31.62 billion by 2031, reflecting an 8.13% CAGR.

Which product category is expanding the fastest?

Powered and electrosurgical devices are projected to post an 8.45% CAGR through 2031.

Why are ambulatory surgical centers important for equipment suppliers?

ASCs perform 72% of U.S. surgeries and demand compact, quick-turnover instruments, driving a 8.97% CAGR in related equipment sales.

Which region offers the strongest growth outlook?

Asia-Pacific shows the highest regional CAGR at 8.69%, supported by infrastructure expansion and rising procedure volumes.

What restrains adoption of advanced robotic systems?

High capital outlays exceeding USD 2 million per unit and stringent regulatory hurdles limit uptake among smaller hospitals and ASCs.

Page last updated on: