AI-based Surgical Robots Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

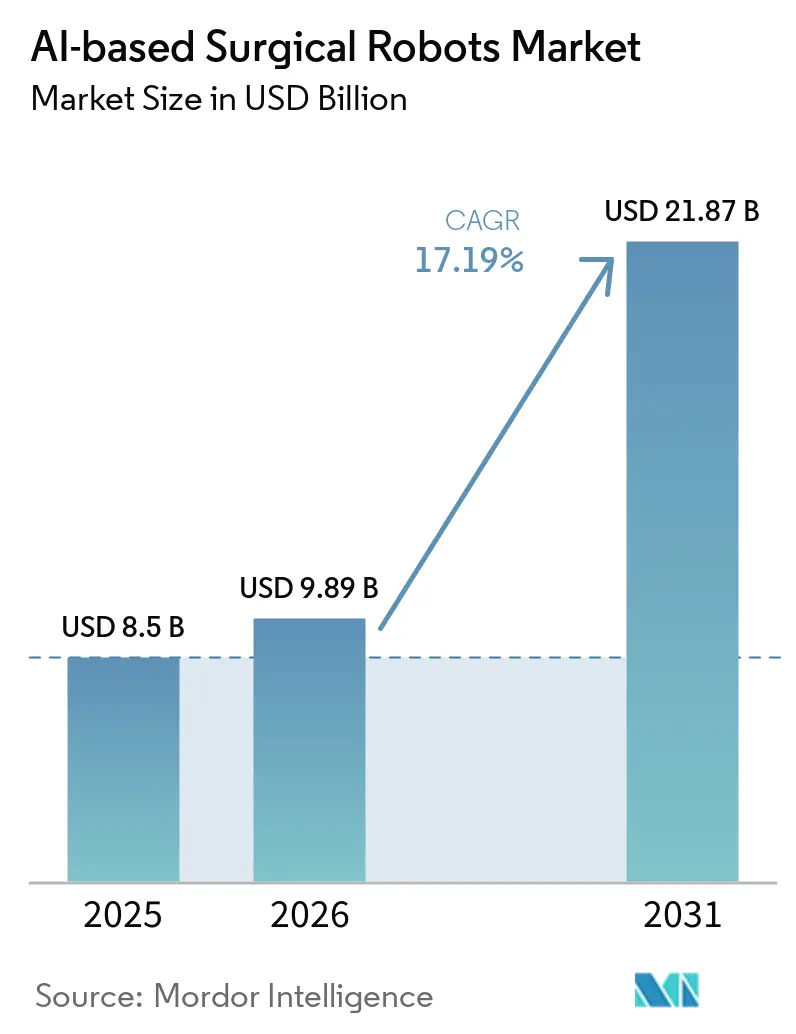

| Market Size (2026) | USD 9.89 Billion |

| Market Size (2031) | USD 21.87 Billion |

| Growth Rate (2026 - 2031) | 17.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-based Surgical Robots Market Analysis by Mordor Intelligence

The AI-based Surgical Robots Market size is expected to grow from USD 8.5 billion in 2025 to USD 9.89 billion in 2026 and is forecast to reach USD 21.87 billion by 2031 at 17.19% CAGR over 2026-2031.

Rising demand for predictable outcomes in complex soft-tissue and orthopedic procedures, tighter reimbursement alignment in outpatient settings, and the rollout of AI-enabled vision modules are reshaping purchasing decisions in favor of platforms that couple hardware with data services at [1]Centers for Medicare & Medicaid Services, “Final Rule: ASC Covered Procedures List 2024,” cms.gov. U.S. hospitals are refreshing installed fleets to gain force-feedback and collision-avoidance features, while European providers are accelerating upgrades to comply with the EU AI Act’s real-time performance-monitoring requirements. In parallel, Chinese manufacturers undercut legacy pricing significantly, compelling incumbents to defend ecosystem lock-in through multi-year instruments and software bundles.

Key Report Takeaways

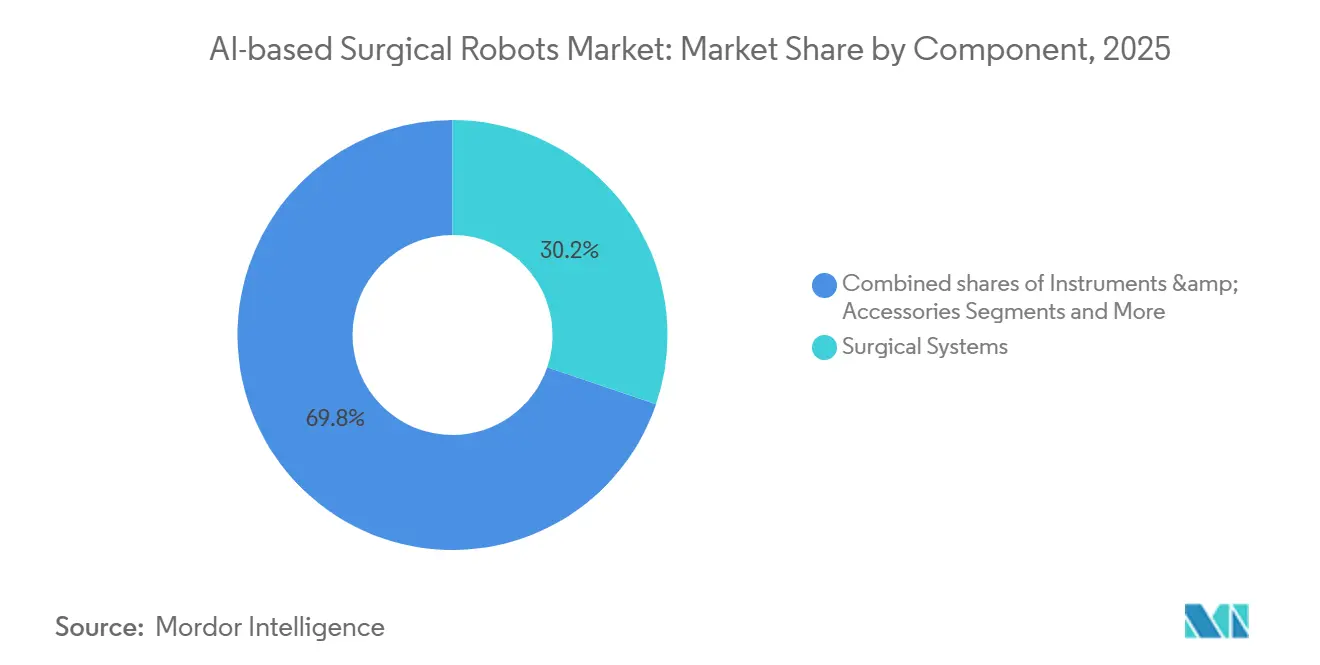

- By component, Surgical Systems captured 30.25% of the AI-based surgical robots market share in 2025, and instruments & accessories is projected to grow at a 19.90% CAGR through 2031.

- By application, General Surgery accounted for 31.09% of 2025 revenue, and Orthopedics is projected to grow at a 18.71% CAGR through 2031.

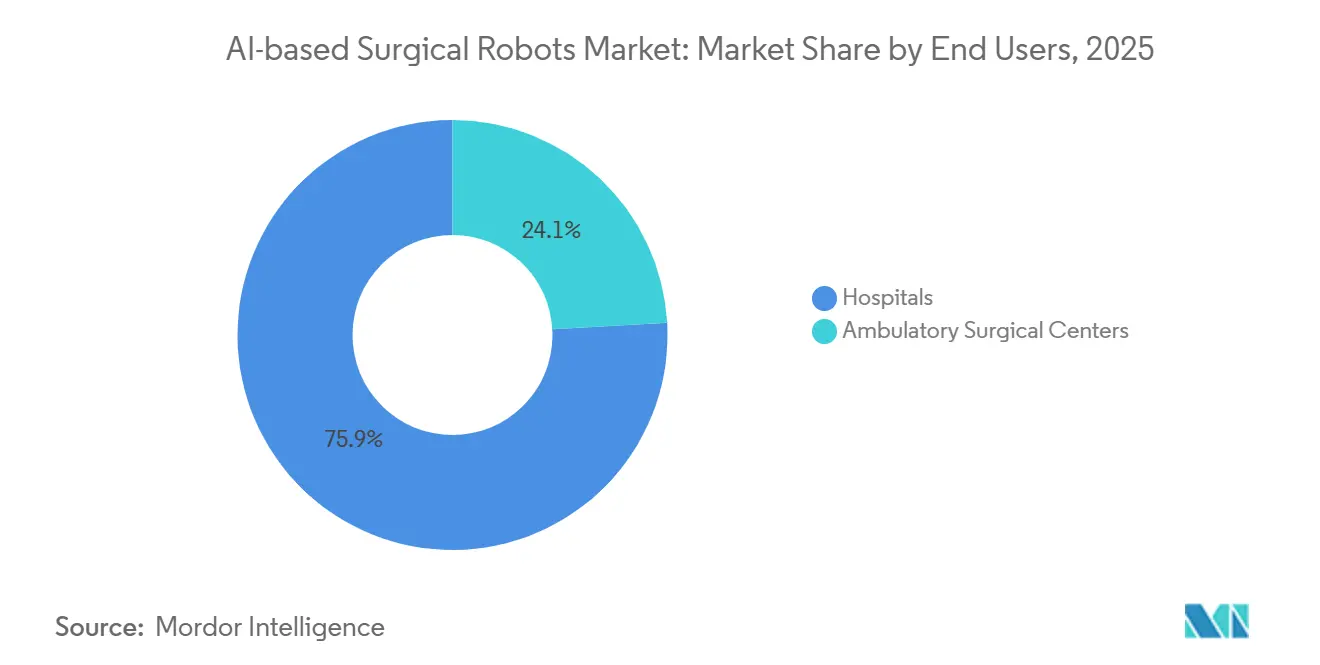

- By end user, Hospitals accounted for 75.90% of global spending in 2025; Ambulatory Surgical Centers recorded the highest CAGR of 19.25% over 2026-2031.

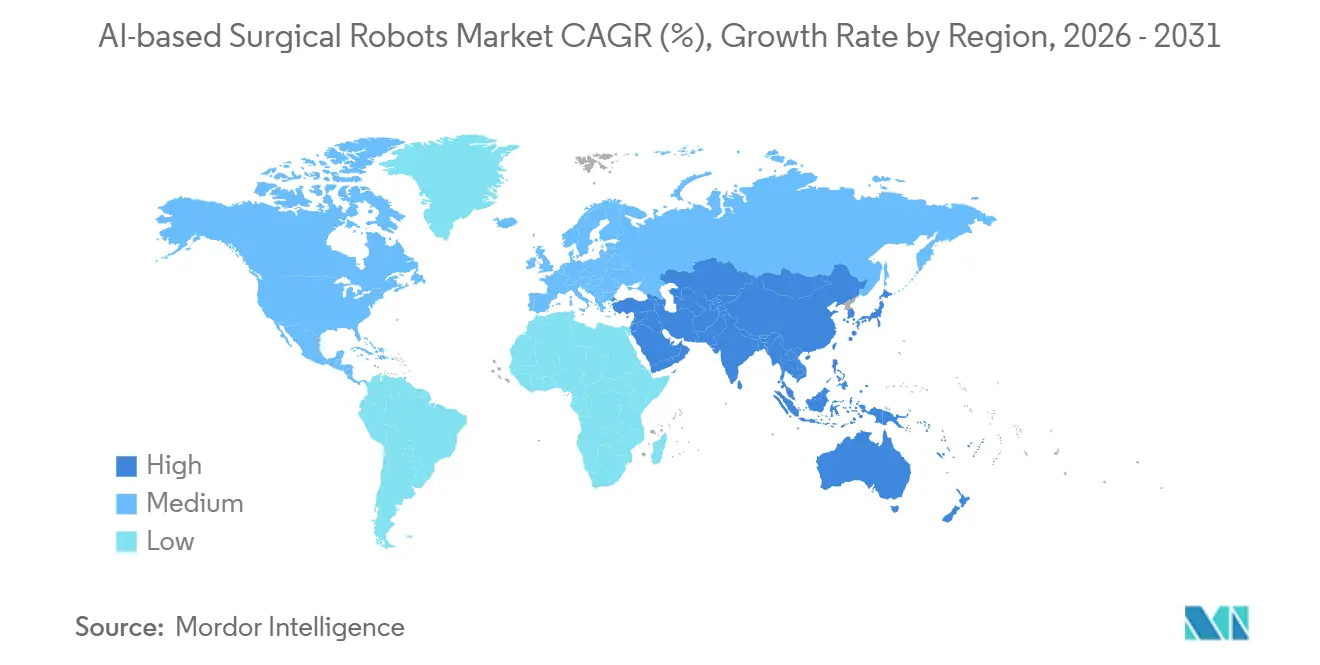

- By geography, North America led with 47.09% of 2025 revenue, and Asia-Pacific is forecast to deliver the fastest regional growth at 19.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-based Surgical Robots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MIS shift to robotic-assisted surgery | +3.2% | North America, Western Europe, Global | Medium term (2-4 years) |

| AI-enabled visualization and decision support | +4.1% | North America, Europe, Tier-1 APAC cities | Long term (≥ 4 years) |

| Expanding indications in soft tissue & ortho | +2.8% | U.S., Germany, Japan | Medium term (2-4 years) |

| Outpatient/ASC migration | +3.5% | North America, Western Europe | Short term (≤ 2 years) |

| Managed-service and per-procedure pricing | +2.9% | APAC and Latin America cost-sensitive markets | Medium term (2-4 years) |

| AI-driven training and tele-proctoring | +1.8% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

MIS Shift to Robotic-Assisted Surgery Across High-Volume Specialties

Robotic systems are displacing laparoscopy in colorectal, bariatric, and urologic cases because improved ergonomics and 3-D vision reduce conversion-to-open rates from 8% to 3% in multi-center studies. Bariatric programs report significantly shorter operative times after the first 20 robotic sleeve-gastrectomy cases [2]American Society for Metabolic and Bariatric Surgery, “Robotic Bariatric Surgery Outcomes,” asmbs.org. Urology holds a significant share of all robotic procedures worldwide in 2025, yet penetration has plateaued in radical prostatectomy, shifting incremental growth to nephrectomy and pyeloplasty. Gynecologic adoption accelerates under Medicare reimbursement parity for hysterectomy, widening hospital use cases. These volume gains shorten capital payback periods to fewer than three years for facilities performing at least 150 eligible cases annually.

AI-Enabled Visualization, Decision Support, and Data Insights Improve Predictability

Clearance of force-sensing and fluorescence-mapping modules on next-generation platforms such as da Vinci 5 enables intraoperative perfusion assessment that flags ischemic tissue before anastomosis. Medtronic’s Touch Surgery Enterprise automatically benchmarks every Hugo RAS case against best-practice pathways, feeding credentialing dashboards that lower malpractice exposure. Third-party add-ons like ActivSight decrease bile-duct injuries by 60% in cholecystectomy through real-time hyperspectral overlays [3]Journal of Surgical Research, “Hyperspectral Imaging in Cholecystectomy,” journalofsurgicalresearch.com. Each procedure uploads annotated video to cloud repositories, and the resulting network effects improve model accuracy, further locking hospitals into specific ecosystems. By 2028, software is projected to contribute a greater share of gross profit than hardware for leading manufacturers.

Expanding Indications and Procedure Volumes in Soft Tissue and Orthopedics

Stryker’s Mako system surpassed 600,000 cumulative knee and hip procedures, demonstrating alignment accuracy that correlates with 95% implant survivorship at 15 years. Zimmer Biomet’s Rosa Knee refines intraoperative alignment in 0.5-degree increments to lower revision risk. Globus Medical’s ExcelsiusGPS now places spine screws with less than 1% breach rates. Intuitive’s Ion robot biopsies sub-2 cm peripheral lung nodules with high diagnostic yield, advancing early lung-cancer detection. These successes expand the AI-based surgical robots market well beyond its original urology focus.

Outpatient/ASC Migration Enabling Compact Systems and Higher Utilization

CMS added 11 robotic procedures to the ASC-covered list, unlocking a USD 500 million opportunity for centers that achieve an eight-procedure daily throughput. CMR Surgical’s Versius has a smaller footprint than legacy multi-port rigs, cutting installation costs to under USD 50,000. Intuitive’s single-use endoscopes eliminate reprocessing delays, allowing consecutive same-day cholecystectomies. Average ASC utilization reaches 220 cases per system annually versus 180 in hospitals. Private-equity inflows exceed USD 2 billion as investors target centers posting 25% EBITDA margins on robotic volumes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of ownership | -2.7% | Cost-sensitive APAC, Latin America, and community hospitals | Medium term (2-4 years) |

| Learning curve and OR workflow disruption | -1.9% | Global, early-adopting hospitals | Short term (≤ 2 years) |

| EU AI Act high-risk compliance | -1.3% | Europe and exporting manufacturers | Long term (≥ 4 years) |

| Cybersecurity constraints on connected ORs | -1.1% | North America, Europe, and advanced APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership

A da Vinci Xi lists at USD 2.5 million and carries USD 180,000 in annual service plus USD 2,500 per-case disposable costs, bringing seven-year outlays above USD 5 million for community hospitals. Forty percent of systems in sub-100-case facilities operate at negative margins. Degradation of ten-use EndoWrist instruments after six to eight cycles effectively forces single-use economics. Chinese entrants sell complete platforms at USD 800,000 and USD 600 per procedure, fueling price pressure on incumbents. Subscription bundles offering unlimited instruments have low adoption as CFOs resist long-term lock-ins.

Learning Curve and OR Workflow Disruption

Early robotic cholecystectomies average 85 minutes of console time, nearly doubling laparoscopic benchmarks and tightening OR schedules. Anesthesia, nursing, and sterile-processing teams require retraining on platform-specific protocols. FDA guidance mandates 20 proctored cases before solo practice, yet rural hospitals often lack available mentors. Surgeon turnover exacerbates sunk training costs, leaving within two years of credentialing. Centralized simulation centers mitigate disruptions but consume capital that competes with additional system purchases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Recurring Software Revenue Gains Strategic Weight

Surgical Systems contributed a leading 30.25% to the AI-based surgical robots market in 2025, while instruments & accessories posted a 19.90% CAGR. Instruments and Services already provide the majority of Intuitive’s 2025 revenue, signaling the sector’s pivot from one-time hardware sales to annuity models.

Software & Analytics Modules attract annual subscriptions of USD 50,000-150,000 per console, and their high gross margins are reshaping strategic priorities across the AI-based surgical robots industry. ActivSight’s 120 hospital installations generated USD 18 million in recurring revenue in 2025. The AI-based surgical robots market size for these modules is projected to expand at double-digit rates as OEMs embed predictive analytics, case planning, and postoperative benchmarking into every license renewal.

By Application: Orthopedics Surges While General Surgery Remains Core

Orthopedics is the fastest-growing specialty, projected to grow 18.71% annually as robotic planning improves implant alignment and enables same-day discharge at ambulatory centers. Stryker’s Mako crossed 600,000 cumulative knee and hip cases in 2024 and then added 22% more volume in 2025 as ASC usage took off, a trend supported by clinical data showing 15-year implant survival above 95% when robots guide cuts.

General surgery maintained a 31.09% revenue share in 2025, driven by staple procedures such as cholecystectomy and colorectal resection, though growth is flattening in mature markets. Urology, once the mainstay, is now pacing behind as prostatectomy penetration tops 80%; momentum has shifted to partial nephrectomy and pyeloplasty, which benefit from ischemia times under 15 minutes. New clearances for brain biopsy, mitral valve repair, and lung-nodule sampling mean neurosurgery, cardiothoracic, and bronchoscopy are small today but scaling quickly, with Intuitive’s Ion delivering 40,000 biopsies in 2025 and 78% yields on sub-2 cm nodules.

By End User: ASCs Capture Growth as Hospitals Consolidate Volume

Ambulatory surgical centers hold the speed record, expanding at a 19.25% CAGR through 2031 as reimbursement parity and compact systems let them run roughly 220 robotic cases per console each year—about 40 more than hospital averages. CMS opened the door wider in 2024 by adding robotic inguinal hernia repair and partial colectomy to the ASC list, a USD 600 million swing in annual addressable revenue. Same-day discharge now exceeds 90% for prostatectomy and total knee arthroplasty in ASCs, cutting episode costs by up to USD 6,000.

Hospitals still own 75.90% of 2025 revenue because they handle complex multi-day stays and most resident training, yet growth slows as OR blocks tighten and budgets tilt toward IT and imaging upgrades. Community facilities deploy robots chiefly for market differentiation, not efficiency, while private-equity buyers pour more than USD 2 billion into ASC chains on the promise of 20–25% EBITDA and three-year paybacks. OEMs now design for 15-minute setup times and cloud-based case planning to win this volume, signaling that ASCs could command roughly 30% of all robotic cases by 2028.

Geography Analysis

Asia-Pacific is the growth engine, set to grow 19.78% annually through 2031, as Chinese vendors sell full platforms at roughly half the Western price and governments in India and Southeast Asia subsidize capital outlays significantly. China’s MicroPort MedBot and Tinavi held a notable local share in 2025 by pricing consoles at around USD 800,000, prompting Intuitive and Medtronic to draft economy-tier offers. India added 120 systems in 2025, largely in metro hubs catering to inbound patients from the Middle East and Africa who pay USD 8,000–12,000 per case.

North America remains the revenue leader at 47.09% of the 2025 total, yet its trajectory is moderating as urology and general-surgery penetration plateaus. The United States accounts for the majority of regional income thanks to Medicare coverage for prostatectomy, hysterectomy, and colorectal procedures, plus commercial-payer backing that now funds 30% of total-knee procedures in ASCs. Europe sits second by revenue; Germany led 2025 installs with 180 units under DRG codes that reimburse esophagectomy and pancreatic work, but the EU AI Act now tacks on an extra 12–18 months and USD 5–10 million to each new product rollout.

Adoption in the Middle East and Africa clusters in Gulf hubs where sovereign wealth funds bankroll showpiece programs; UAE and Saudi reference centers together run 8,000 robotic cases a year. South Africa’s 12-system footprint sits mostly in private chains, while public budgets focus on infectious-disease care. South America’s strength lies in Brazil, whose private groups Rede D’Or and Hapvida performed 15,000 cases in 2025; Argentina added eight consoles for prostatectomy and bariatrics under private insurance cover

Competitive Landscape

The AI-based surgical robots market exhibits moderate concentration: Intuitive Surgical holds the majority of multi-port revenue, leveraging an installed base of 9,000 consoles that generate USD 5 billion in annual consumables and service income. Medtronic counters with zero-capex Hugo Access contracts, while CMR Surgical uses portable arms to sidestep structural OR renovations.

Innovation now hinges on AI capabilities more than mechanical dexterity. Intuitive maintains over 4,200 active patents, the majority of which are tied to computer vision and predictive analytics. FDA clearance of CMR’s Versius Plus at under USD 1 million forces incumbents to shift revenue weight toward software and instruments.

Emerging disruptors such as Vicarious Surgical and Moon Surgical focus on USD 50,000 modular add-ons that retrofit existing laparoscopic towers, appealing to budget-constrained facilities. Strategic alliances—Johnson & Johnson with Auris Health, Stryker with IRCAD underscore the race to secure data pipelines that refine intraoperative AI models.

AI-based Surgical Robots Industry Leaders

Intuitive Surgical

Johnson & Johnson

Medtronic

CMR Surgical

Vicarious Surgical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Johnson & Johnson officially submitted the OTTAVA robotic system to the FDA for De Novo classification, targeting upper abdominal general surgeries.

- December 2025: CMR Surgical obtained U.S. 510(k) for Versius Plus, entering the market below USD 1 million after a 150-patient non-inferiority trial.

Global AI-based Surgical Robots Market Report Scope

As per the scope of the report, AI-based surgical robots represent a transformative leap in medicine, evolving from simple "master-slave" systems into intelligent platforms capable of real-time decision support and semi-autonomous tasks. These systems integrate Machine Learning and computer vision to analyze live video feeds, identifying critical anatomical structures, blood vessels, and tumors to guide surgeons with sub-millimeter precision.

The AI-based Surgical Robots Market is segmented by component, applications, end users, and geography. By component, the market is segmented into surgical systems, instruments & accessories, software & analytics modules, and services. By Application, the market is segmented into general surgery, urology, gynecology, orthopedics (knee, hip, shoulder), neurosurgery, cardiothoracic/thoracic, bronchoscopy/endoluminal (lung), and head & neck / ENT. By end users, the market is segmented into hospitals, and ambulatory surgical centers. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Surgical Systems |

| Instruments & Accessories |

| Software & Analytics Modules |

| Services (installation, training, maintenance) |

| General Surgery (e.g., hernia, colorectal, bariatric) |

| Urology |

| Gynecology |

| Orthopedics (knee, hip, shoulder) |

| Neurosurgery |

| Cardiothoracic/Thoracic |

| Bronchoscopy/Endoluminal (lung) |

| Head & Neck / ENT |

| Hospitals (AMCs, tertiary centers) |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Surgical Systems | |

| Instruments & Accessories | ||

| Software & Analytics Modules | ||

| Services (installation, training, maintenance) | ||

| By Application | General Surgery (e.g., hernia, colorectal, bariatric) | |

| Urology | ||

| Gynecology | ||

| Orthopedics (knee, hip, shoulder) | ||

| Neurosurgery | ||

| Cardiothoracic/Thoracic | ||

| Bronchoscopy/Endoluminal (lung) | ||

| Head & Neck / ENT | ||

| By End User | Hospitals (AMCs, tertiary centers) | |

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the AI-based surgical robots market be in 2031?

It is projected to reach USD 21.87 billion by 2031, growing at a 17.19% CAGR from 2026 to 2031.

Which surgical specialty is expanding fastest in robotic adoption?

Orthopedic joint replacement leads growth because robotic planning improves implant alignment and lowers revision rates

Why are Ambulatory Surgical Centers important to future sales?

ASCs receive reimbursement parity, run higher utilization rates, and now access compact robots offered under per-procedure contracts, driving a 19.25% forecast CAGR.

What is the main cost obstacle for smaller hospitals?

A single multi-port robot can exceed USD 5 million in seven-year total cost of ownership, making breakeven difficult below 150 annual cases.

How will the EU AI Act influence product launches?

The Act classifies surgical robots with autonomous support as high-risk devices, adding 12-18 months of conformity assessments and ongoing surveillance to commercialization timelines.

Page last updated on: