Market Overview

| Study Period | 2020 - 2031 |

|---|---|

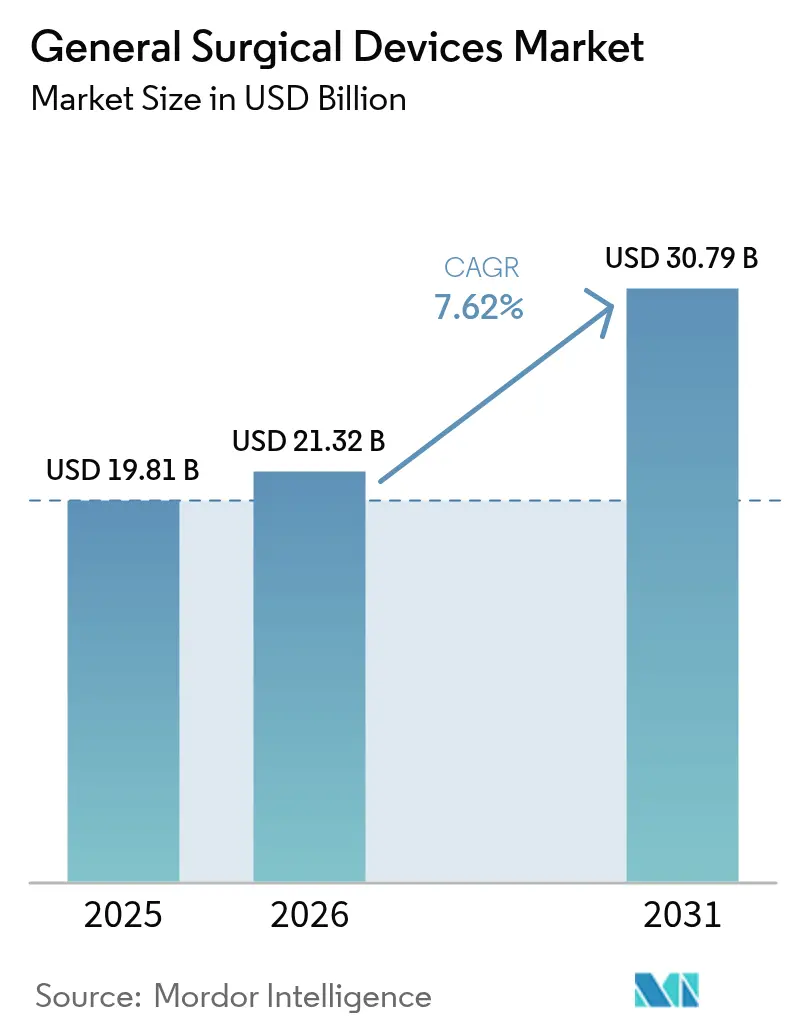

| Market Size (2026) | USD 21.32 Billion |

| Market Size (2031) | USD 30.79 Billion |

| Growth Rate (2026 - 2031) | 7.62% CAGR |

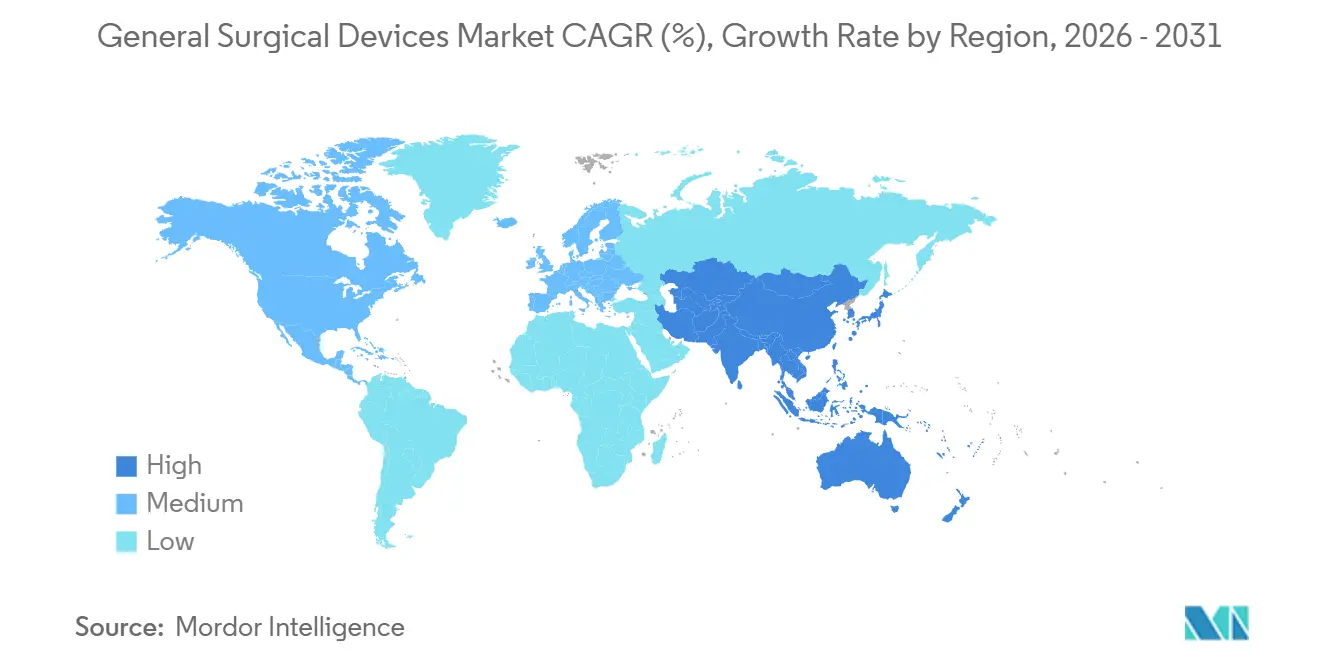

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

General Surgical Devices Market Analysis by Mordor Intelligence

The General Surgical Devices Market size is projected to expand from USD 19.81 billion in 2025 and USD 21.32 billion in 2026 to USD 30.79 billion by 2031, registering a CAGR of 7.62% between 2026 to 2031.

Increasing global procedure volumes, accelerated uptake of robotic and other minimally invasive platforms, and a hospital-wide pivot toward disposable instrumentation are propelling this expansion. Facility administrators view single-use kits as a direct route to lower sterilization overhead and tighter infection-control metrics, while surgeons value the consistency and traceability built into factory-sterile trays. Robotic systems that once sat only in academic theaters are now being financed through leasing programs and deployed in community hospitals as force-feedback upgrades reduce the learning curve. In parallel, smart generators that merge ultrasonic, bipolar, and monopolar modalities onto a single cart help operating rooms reclaim floor space and cut turnover times.

Key Report Takeaways

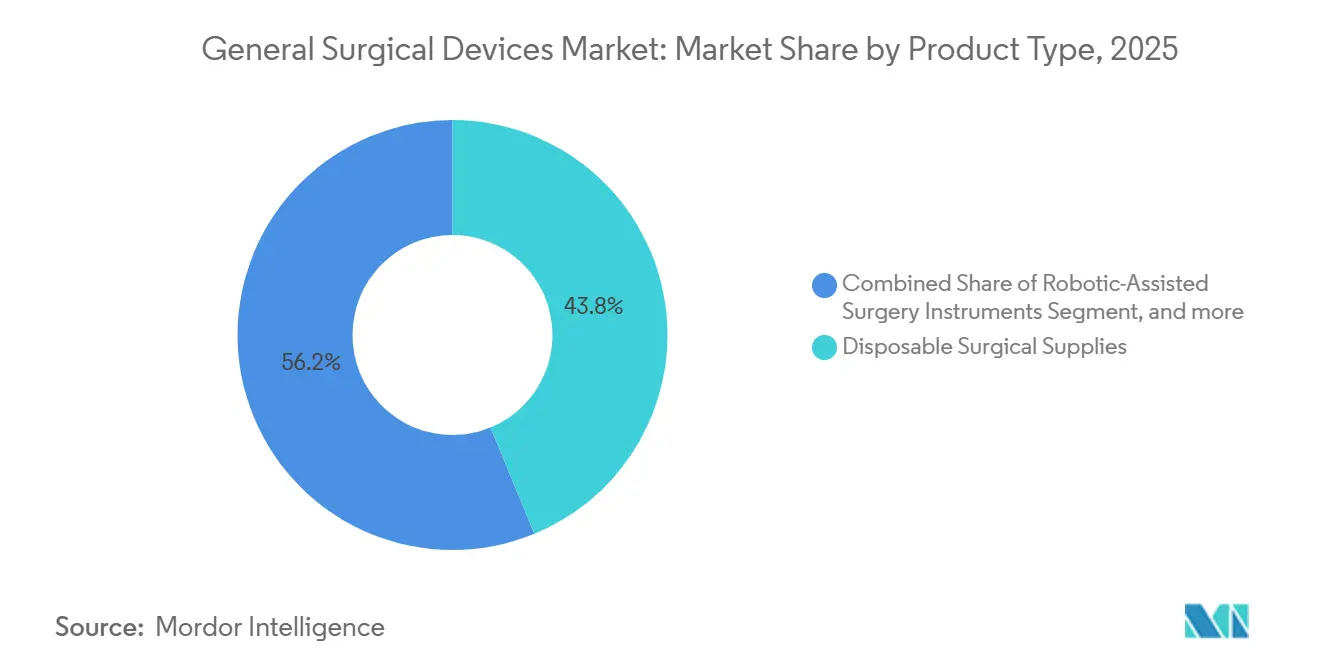

- By product type, disposables accounted for 43.78% of the general surgical devices market share in 2025, reflecting hospitals’ preference for factory-sterilized instruments that bypass reprocessing departments.

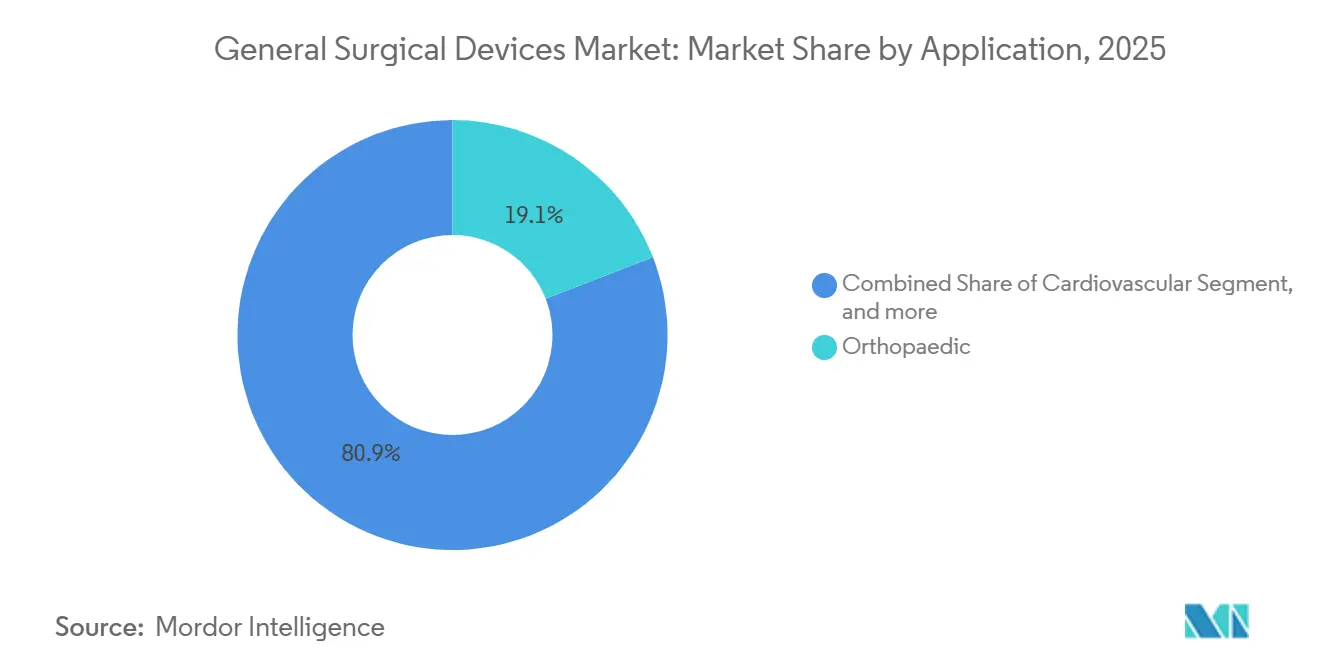

- By application, cardiovascular surgery is forecast to expand at a 9.77% CAGR through 2031, the fastest pace among all specialties, as energy-based vessel sealing and transcatheter solutions shorten recovery windows.

- By end user, hospitals retained a 58.62% revenue share in 2025, yet ambulatory surgical centers are advancing at a 10.32% CAGR as payers steer low-complexity cases toward lower-cost sites of care.

- By geography, North America accounted for 41.54% of 2025 sales, but Asia-Pacific is projected to register the most vigorous growth at an 8.54% CAGR through 2031, driven by hospital construction and rising middle-class demand.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global General Surgical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global surgical procedure volumes | +1.8% | Worldwide, rapid acceleration in Asia-Pacific | Medium term (2-4 years) |

| Shift toward minimally invasive and robotic surgeries | +2.1% | North America and Europe lead, Asia-Pacific catching up | Long term (≥ 4 years) |

| Continuous technological advancements in surgical instruments | +1.5% | R&D concentrated in North America and Europe | Long term (≥ 4 years) |

| Expansion of healthcare infrastructure in emerging markets | +1.3% | Core focus in Asia-Pacific, spillover to other regions | Medium term (2-4 years) |

| Increasing preference for disposable and single-use devices | +1.6% | North America and Europe, rising use in Asia-Pacific | Short term (≤ 2 years) |

| Growing investments in smart and connected operating rooms | +0.9% | North America and Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Surgical Procedure Volumes

An aging world population, coupled with higher chronic-disease prevalence, is driving up the need for operative care, yet only 45 countries meet the World Health Organization’s benchmark of 5,000 procedures per 100,000 people each year[1]World Bank, “Surgical Procedures (per 100,000 population),” worldbank.org. In high-income settings, Intuitive Surgical recorded 2.68 million da Vinci procedures during 2024, a 17% year-over-year jump, with general surgery accounting for the lion’s share. This momentum is forcing hospitals to broaden instrument portfolios and stretch capital budgets to maintain throughput. Manufacturers, in response, are rolling out multi-specialty trays and modular robotic arms that slot into existing infrastructure without a full operating-room overhaul. Larger case volumes, meanwhile, reinforce the economics of disposables, further anchoring the general surgical devices market in a growth posture.

Shift Toward Minimally Invasive and Robotic Surgeries

More surgeons are gravitating toward minimally invasive techniques to shorten patient recovery, reduce pain medication use, and enable same-day discharge. The arrival of force-feedback technology in the fifth-generation da Vinci platform—validated by preclinical data showing up to 43% less tissue pressure—lowers the barrier for those who previously hesitated over the loss of tactile sensation. Even so, capital intensity remains a gating factor, prompting leasing models and per-procedure billing that distribute costs across predictable caseloads. As deployment widens, the general surgical devices market sees a halo effect: ancillary ports, staplers, and energy instruments optimized for robotic articulation experience parallel growth in demand.

Continuous Technological Advancements in Surgical Instruments

Emerging generators now bundle monopolar, bipolar, ultrasonic, and advanced bipolar energy on one chassis, shrinking equipment footprints by up to 46% when compared with legacy stacks. Olympus added a distal thermal shield to its hybrid device to slow heat transfer and protect adjacent structures. Integrating multiple modalities onto a single interface not only accelerates instrument exchanges but also simplifies staff training, an often-overlooked cost driver. Forward-looking vendors are embedding sensors that stream real-time tissue data to the cloud, laying groundwork for subscription-based software that could insulate margins as hardware commoditizes, further energizing the general surgical devices market.

Increasing Preference for Disposable and Single-Use Devices

Hospitals in North America and Europe continue migrating toward single-use trocars, staplers, and vessel seals to tighten infection-control protocols. Becton Dickinson’s fully bioabsorbable Phasix ST Umbilical Hernia Patch answers surgeon requests for non-permanent implants without disrupting established techniques[2]Becton Dickinson, “Phasix ST Umbilical Patch Cleared by FDA,” bd.com. Adoption is particularly strong in ambulatory surgical centers that lack the physical space and staff for central sterile reprocessing. At the same time, traceability built into bar-coded disposables supports value-based care audits, further entrenching single-use economics inside the general surgical devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and maintenance costs of advanced systems | -1.2% | Most acute in mid-tier hospitals worldwide | Short term (≤ 2 years) |

| Stringent regulatory and compliance requirements | -0.8% | Europe, North America, China | Medium term (2-4 years) |

| Cybersecurity risks in networked surgical equipment | -0.4% | North America and Europe | Long term (≥ 4 years) |

| Shortage of skilled surgeons for next-generation technologies | -0.6% | Sub-Saharan Africa, South Asia, rural areas everywhere | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital and Maintenance Costs of Advanced Systems

Acquiring a top-tier robotic suite can require USD 2.5 million up front, while annual service contracts range between USD 100,000 and USD 200,000. Even though leasing and per-click agreements ease the initial burden, finance committees still seek proof that improved throughput offsets the expense. For many community hospitals, table-mounted or single-port robots that tuck under the operating table represent an attractive alternative by trimming floor-space penalties and capital exposure. Nevertheless, the price tag remains a hurdle that tempers near-term growth in the general surgical devices market.

Stringent Regulatory and Compliance Requirements

The European Union’s Medical Device Regulation tightened evidence requirements and extended review timelines, prompting some vendors to withdraw niche products. In the United States, a 510(k) filing now often entails post-market surveillance and cybersecurity reporting protocols[3]. Although reforms promise faster pathways for low-risk instruments, the cost of documentation and clinical validation weighs heavily on start-ups, consolidating share among deep-pocketed incumbents and slightly dampening the overall expansion rate of the general surgical devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Disposables Dominate, Robotics Accelerate

Disposable supplies accounted for 43.78% of 2025 revenue, underscoring a hospital's drive to eliminate reprocessing risk and secure sterility assurance. This dominance is reinforced each time accreditation surveys flag lapses in central sterile work-flows, pushing administrators toward single-use kits tailored for common procedures. Robotic instruments, while representing a smaller absolute slice today, are climbing at a 9.65% CAGR to 2031. Their growth depends on the expanding installed base of force-feedback-equipped systems, which makes the transition easier for mid-career surgeons. The general surgical devices market size for robotic consumables is projected to grow in tandem with each console shipped.

A second tier of growth lies in hybrid energy tools that merge ultrasonic cutting, bipolar sealing, and real-time thermal monitoring. Johnson & Johnson’s modular generator reduces cart footprints by nearly half, a design win for crowded ambulatory suites. Smart staplers have joined the fray: Medtronic’s circular model offers adaptive compression and onboard leak testing, signaling a future in which disposables become data nodes inside connected operating rooms. As premium functions move from capital equipment into single-use formats, value perception continues tilting the general surgical devices market toward advanced disposables.

By Application: Cardiovascular Surges, Orthopedics Stabilize

Orthopedic surgery generated 19.10% of 2025 sales, supported by steady demand for joint replacements and trauma hardware. Cardiovascular procedures, however, are on a faster lane, charting a 9.77% CAGR through 2031 as transcatheter valves and energy-based vessel sealing shorten hospital stays. The general surgical devices market size for cardiovascular instruments is expected to outpace orthopedics by the late forecast period, driven by devices that combine procedural exclusivity with recurring consumable pull-through.

Elsewhere, single-port robotics is redefining gynecology and urology workflows, while smart staplers target colorectal anastomosis, where leaks carry severe morbidity. Energy devices that limit thermal spread are gaining traction in neurosurgery and thoracic cases, expanding the addressable demand for general surgical devices across high-acuity specialties. Bariatric growth has moderated amid pharmacologic weight-loss alternatives, yet revisional surgeries keep the segment relevant for stapling and sealing vendors.

By End User: ASCs Outpace Hospitals in Growth

Hospitals still account for 58.62% of global revenue thanks to case-mix complexity and 24/7 support services. Yet ambulatory surgical centers are posting a 10.32% CAGR to 2031 as payers shift routine procedures to lower-cost sites. Single-use kits fit naturally into ASC economics by eliminating the need for large sterilization departments. The general surgical devices market share attributable to ASCs is projected to rise steadily, particularly for laparoscopic cholecystectomy and hernia repair packages.

Specialty clinics focusing on ophthalmology, pain, and sports medicine leverage high throughput to negotiate volume discounts, but remain fragmented buyers. Academic centers, though smaller in purchasing power, wield influence through clinical trials that validate next-generation devices before wider adoption. Collectively, these settings create a multi-channel demand pattern that rewards vendors able to tailor financing and training models across the general surgical devices market.

Geography Analysis

North America generated 41.54% of 2025 revenue, supported by nearly 10,000 installed da Vinci consoles and reimbursement models that favor minimally invasive techniques. Capital pressure on midsize hospitals persists, but leasing programs and table-mounted robots soften the blow. Ambulatory centers are flourishing as same-day discharge gains payer support, reinforcing demand for disposable kits and anchoring the general surgical devices market in the region.

Europe follows with the mature adoption of robotic and hybrid-energy platforms. Regulatory strictness under EU MDR raised compliance costs, yet recent simplification proposals aim to cut EUR 3.3 billion a year and could reignite product launches. Sustainability imperatives add a new procurement filter, rewarding manufacturers that backtake used plastics or document lifecycle carbon savings.

Asia-Pacific is the fastest-growing region, with an 8.54% CAGR. Government-funded hospital expansion and a swelling middle class widen the customer base, while localized manufacturing initiatives help vendors strike the right price point. Premium data-enabled systems populate urban referral centers, but manual-hybrid instruments still dominate secondary hospitals where budgets remain tight. Emerging markets in Latin America and the Middle East echo similar dynamics on a smaller scale, collectively nudging the general surgical devices market into new territory.

Regulatory Landscape

General surgical devices are regulated through medical device frameworks that cover quality-system requirements, clinical evidence expectations, and post-market obligations. In the United States, FDA oversight spans pathways such as 510(k) for many general surgery instruments and accessories, with manufacturing controls anchored by the Quality Management System Regulation (QMSR). The QMSR became effective on February 2, 2026 and incorporates ISO 13485:2016 by reference, which increases the value of harmonized quality documentation across global portfolios.

In Europe, the Medical Device Regulation (MDR) continues to drive higher technical file and conformity assessment workloads, with notified body capacity and consistency remaining key operational constraints. The EU also reinforced this governance layer through Commission Implementing Regulation (EU) 2026/977 dated May 4, 2026, which sets uniform quality management and procedural requirements for notified bodies under MDR and IVDR. In parallel, a December 2025 European Commission proposal targets simplification of MDR/IVDR processes to reduce administrative burden and ease certification bottlenecks. The UK continues work on its future medical device regime and has consulted on indefinite recognition of CE marked devices to maintain market access continuity.

Value Chain Analysis

The general surgical devices value chain starts with raw materials and precision components, including metals, polymers, electronics, coatings, and sterile barrier packaging, before moving through machining, molding, assembly, and sterilization. From there, products flow into labeling, regulatory release, and commercial distribution. Large OEMs typically handle design controls, regulatory files, and final product release, often using contract manufacturers and specialized component suppliers for subassemblies, while third-party logistics providers support regional warehousing and cold chain or controlled handling where required. Downstream, distribution is typically a mix of direct hospital sales and group purchasing channels, with wholesalers supplementing coverage in more fragmented markets. Post-sale activities such as in-service training, instrument maintenance, and post-market surveillance also close the loop, particularly for energy platforms and robotic instruments.

Two constraints increasingly affect both cost and service levels: (1) compliance intensity across regions, including quality systems, traceability, and shortage monitoring, and (2) operational resilience during disruptions. The FDA monitors medical device shortages and can escalate actions under mechanisms such as the Defense Production Act. In the EU, shortage reporting obligations introduced in January 2025 add additional reporting workflow for some manufacturers and distributors. Cybersecurity and IT resilience are also emerging as supply-chain considerations for case-ready disposables and robotic consumables; for example, a March 2026 cyberattack affecting Stryker systems highlighted how digital outages can disrupt order visibility, inventory allocation, and distribution continuity even when physical manufacturing capacity is unchanged.

Competitive Landscape

Five diversified multinationals—Johnson & Johnson, Medtronic, Intuitive Surgical, Stryker, and Boston Scientific—hold outsized sway, yet specialty niches remain contested by agile innovators. Johnson & Johnson’s USD 13.1 billion purchase of Shockwave Medical underscored a push toward cardiovascular tools offering strong consumable annuities. Medtronic countered with intelligent stapling and a regional R&D footprint designed for affordability in emerging markets, strengthening its position across the general surgical devices market.

Meanwhile, Karl Storz agreed to acquire Asensus Surgical, adding image-guided robotics to an endoscope-rich portfolio. Force-feedback haptics, AI-driven tissue analytics, and cloud-based fleet management are the new battlegrounds, with each player racing to craft closed ecosystems that lock in procedural spend. Heightened regulatory and cybersecurity demands raise barriers for start-ups, nudging the general surgical devices industry toward moderate consolidation without tipping into a monopoly.

General Surgical Devices Industry Leaders

Boston Scientific Corporation

B. Braun SE

Medtronic PLC

Johnson & Johnson (Ethicon, DePuy & Robotics)

Stryker Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory harmonization and clearer standards pathways create measurable whitespace for manufacturers that can industrialize compliant, traceable disposable and smart-instrument portfolios at scale. The FDA QMSR shift effective February 2, 2026 aligns US quality requirements more closely with ISO 13485:2016, supporting global quality-system convergence for suppliers serving both North America, which accounted for 41.54% of 2025 sales, and internationally distributed product lines. In the EU, updates in 2026 to the standards and evidence framework add additional anchors for portfolio planning. Implementing Decision (EU) 2026/1231 dated June 25, 2026 updated harmonized standards covering sterilization-related requirements, and Commission Delegated Regulation (EU) 2026/1451 dated March 20, 2026 expanded the list of devices exempted from mandatory clinical investigations to include common surgical instruments, such as forceps, needle holders, and cannula. This can reduce friction for some reusable tool line extensions when documentation and performance evidence are well controlled.

On the technology side, the opportunity concentrates on devices that turn minimally invasive and robotic adoption into recurring pull-through of stapling, energy, access, and single-use kits. This dynamic ties closely to ambulatory surgical center expansion, where workflows increasingly favor factory-sterile, space-saving kits. Academic work published in 2026 on miniaturized robotic instrumentation and autonomous robotic concepts, including proof-of-concept studies in colonoscopy and microsurgical tools, points to a pipeline of smaller-footprint, data-driven instruments that can translate into new accessory offerings after validation and commercialization. Within the current market structure, this favors vendors that pair modular robotic platforms and integrated energy systems with compatible disposable instrumentation, while building cybersecurity-ready connectivity and traceability to meet hospital procurement and post-market expectations.

Recent Industry Developments

- July 2026: Medtronic completed its acquisition of Scientia Vascular, adding neurovascular access and therapeutic technologies to its portfolio. The deal strengthens Medtronic's position in catheter-based procedure ecosystems that rely on recurring device utilization and complements hospital demand for integrated procedure solutions across high-acuity service lines.

- November 2025: Medtronic unveiled the Signia Circular Stapler with adaptive compression and integrated leak testing, with phased launches across the United States, Europe, and Japan. This product move pushes stapling further toward sensor-enabled performance features, reinforcing the shift of premium functionality into disposable instruments used in high-volume surgical workflows.

- November 2024: Johnson & Johnson MedTech received FDA IDE approval for the OTTAVA Robotic Surgical System. The authorization enabled pivotal clinical evaluation in soft tissue surgery, supporting the build-out of a proprietary robotic ecosystem that can drive demand for compatible instruments and consumables as the platform progresses through evidence generation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the general surgical devices market covers instruments and devices used during human surgical procedures to access tissue, cut, seal or cauterize, and close wounds, covering open surgery, minimally invasive surgery, and robot-assisted approaches.

Scope exclusions: This sizing excludes veterinary-use surgical kits and large capital imaging systems that support surgery but are not surgical devices themselves.

Segmentation Overview

- By Product Type

- Minimally Invasive Surgery Instruments

- Robotic-Assisted Surgery Instruments

- Energy-Based Surgery Instruments (RF, Ultrasonic, Laser)

- Open Surgery Instruments

- Disposable / Single-Use Surgical Supplies

- Smart / Sensor-Enabled Instruments

- Other Product Types

- By Application

- Orthopaedic

- Cardiovascular

- Gynaecology & Urology

- Neurosurgery

- Gastrointestinal / Colorectal

- Bariatric & Metabolic

- Thoracic

- Plastic & Reconstructive

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Academic & Research Institutes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the fact base and set realistic boundaries before modeling, so totals do not accidentally mix devices with adjacent equipment. We used public sources such as the World Health Organization for healthcare system indicators, the US FDA device databases for product and regulatory context, OECD health statistics for procedure and spend proxies, and the World Bank for macro and currency signals.

We also reviewed hospital and payer publications where available, trade association material on surgical volumes and practice trends, and company annual reports and investor presentations to understand portfolio exposure and demand drivers. Patent databases were checked to track innovation themes like energy-based tools and robot-assisted surgery attachments, which helped frame adoption assumptions. The sources mentioned here are illustrative only, and additional public documents and datasets were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to pressure-test key assumptions that desk sources do not explain well, especially what gets counted as a general surgical device versus adjacent capital equipment and service revenue. We spoke with manufacturers, distributors, procurement stakeholders, and clinical users across major regions, so adoption, pricing behavior, and procedure mix could be sanity-checked and then reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 15% | APAC: 45% |

| Mid tier: 50% | Functional/Unit leaders: 32% | EMEA: 36% |

| Smaller Players: 17% | Managers: 53% | Americas: 19% |

Market-Sizing & Forecasting

Sizing started with a top-down build where procedure volumes and care-setting mix were used to reconstruct demand for core surgical device categories, then translated into value using usage patterns and price bands. To keep the model grounded, we also ran selective bottom-up approximations, such as sampled ASP x volume checks for high-usage device groups and channel feedback on replacement and replenishment cycles, which were then used to adjust totals if gaps appeared.

Key inputs included surgical procedure growth by setting (hospital versus ambulatory surgical centers), minimally invasive surgery penetration, adoption of energy-based instruments, replacement frequency for reusable instruments, and expected pricing pressure from hospital procurement. Because short-term shifts can occur when procedure backlogs clear or when elective volumes change, scenario analysis was used for forecasting, and assumptions were aligned to what interviewees described as the most likely path in their regions. Where direct volume signals were missing for smaller countries, ratios tied to healthcare activity indicators were applied, and results were re-checked against regional totals before finalizing.

Data Validation & Update Cycle

Before sign-off, outputs were cross-checked against independent signals such as procedure trends, care-setting shifts, and reported category exposure in public company disclosures. When variances looked unusual, the drivers were re-opened, assumptions were re-tested, and targeted re-contacts were triggered so that outliers did not flow into the final totals.

A multi-step review is followed internally, where model logic and key inputs are checked by another analyst before the final numbers are frozen. Reports are refreshed annually, and interim updates are made when material changes affect demand or pricing. Right before delivery, a fresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's Global General Surgical Devices Market Market Size Compared With Other Published Estimates

Published market sizes for general surgical devices often differ because the counted device set is not identical, and because procedure, price, and care-setting assumptions change the totals in noticeable ways. Differences also show up when one publisher uses a different currency conversion point or a longer forecast window, which can make the current-year number look higher or lower than expected.

The table reflects a spread across publishers, and within Mordor Intelligence's scope the counted revenue centers on devices used to access, cut, seal, cauterize, or close human tissue across open, minimally invasive, and robot-assisted procedures, with veterinary-use kits and large capital imaging systems kept outside the market total. The remaining gaps usually come from base-year selection and how quickly ASP changes are applied across categories, since procurement feedback tends to show uneven price movement by device type and care setting.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 21.32 B (2026) | |

| Global Consultancy A | USD 19.88 B (2025) | Uses a different base year and may blend broader procedure-linked equipment into the device basket, and the value can shift if currency timing and inflation treatment are not aligned to the same year. |

| Industry Publisher B | USD 18.44 B (2024) | Often uses earlier-year demand conditions and a wider definition that can include complex equipment categories, which can lower the stated starting value and then amplify the long-range projection. |

Looking across the three figures, the main takeaway is that year selection and what is included as a surgical device explain most of the gap, followed by how prices and adoption are carried forward. By tying the value build to procedure activity, care-setting mix, and realistic pricing behavior, the estimate stays traceable to clear levers that can be re-checked when new data arrives.

Key Questions Answered in the Report

What is the current value of the general surgical devices market?

It reached USD 21.32 billion in 2026 and is projected to rise to USD 30.78 billion by 2031.

Which product category leads sales?

Disposable and single-use instruments dominate, holding 43.78% of 2025 revenue.

Which specialty is growing fastest?

Cardiovascular surgery is expanding at a 9.77% CAGR through 2031 on the back of transcatheter and energy-based innovations.

How quickly are ambulatory surgical centers adopting new devices?

ASC demand is growing at a 10.32% CAGR as payers favor lower-cost same-day settings.

Which region shows the highest growth potential?

Asia-Pacific is forecast to register an 8.54% CAGR, supported by hospital construction and rising disposable income.

What is the main barrier to wider robotic surgery adoption?

High capital and maintenance costs, often exceeding USD 2.5 million per console, limit uptake among mid-tier hospitals.

Page last updated on: