United States Sex Reassignment Surgery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

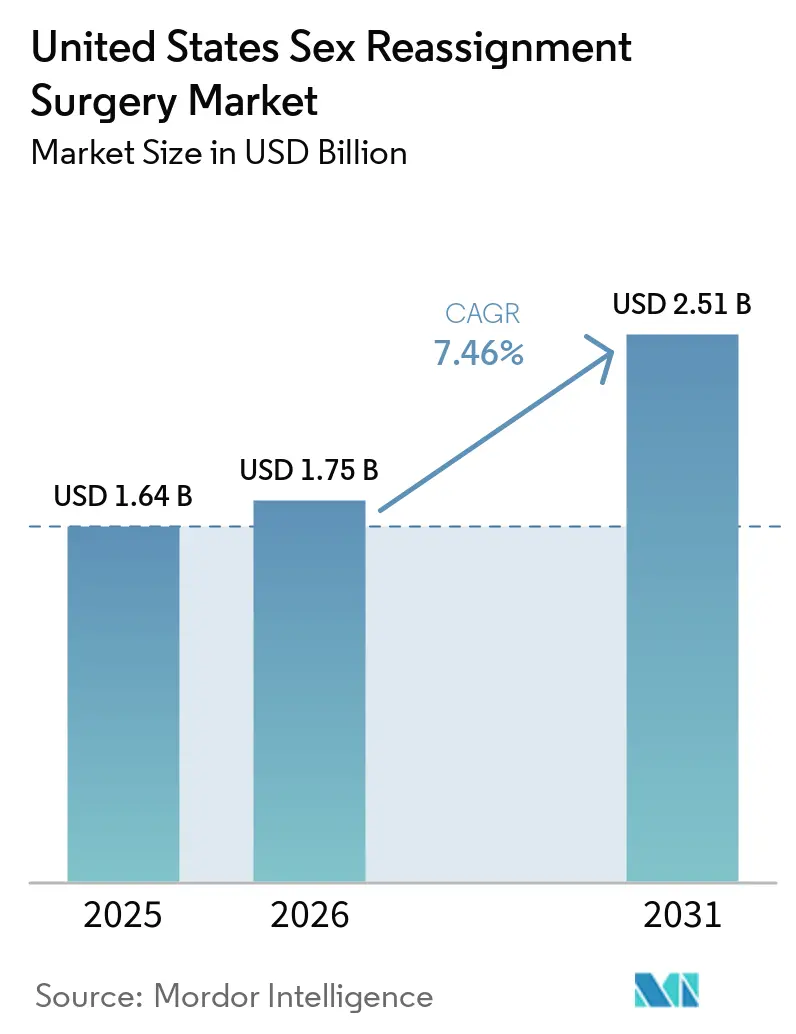

| Base Year Market Size (2025) | USD 1.64 Billion |

| Market Size (2026) | USD 1.75 Billion |

| Market Size (2031) | USD 2.51 Billion |

| Growth Rate (2026 - 2031) | 7.46% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Sex Reassignment Surgery Market Analysis by Mordor Intelligence

The United States Sex Reassignment Surgery Market size is expected to grow from USD 1.64 billion in 2025 to USD 1.75 billion in 2026 and is forecast to reach USD 2.51 billion by 2031 at 7.46% CAGR over 2026-2031.

The 2026 market reflects a specialty care segment that is still shaped by insurer authorization cycles, tight surgeon availability, and changing federal policy. The United States sex reassignment surgery market continues to expand because patient demand is rising faster than the system can add operating room capacity, fellowship-trained surgeons, and multidisciplinary support teams. That gap has concentrated procedure volume, capital, and talent in a small set of academic hospitals and specialty centers, which keeps demand strong but limits how quickly completed revenue can scale. Shield-law states in the Northeast and West are attracting patients and providers from restrictive regions, which is reinforcing regional concentration while creating growth pockets for centers with available capacity. Competitive strategy in the United States sex reassignment surgery market is therefore centered on payer navigation, geographic expansion, robotic capability, and integrated care pathways that improve conversion from consultation to surgery.

Key Report Takeaways

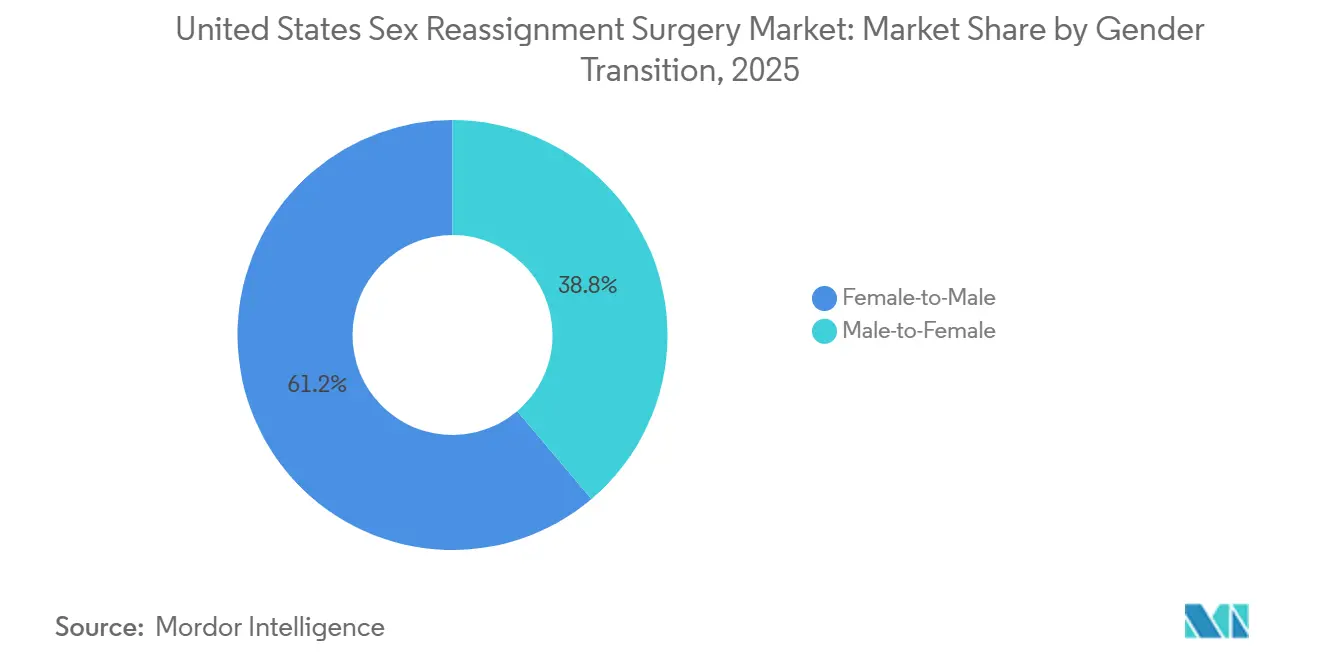

- By gender transition, female-to-male procedures held 61.23% share in 2025, while Male-to-Female procedures are projected to grow at 9.58% CAGR through 2031.

- By procedure, mastectomy accounted for 21.72% of revenue in 2025, while augmentation mammoplasty is forecast to expand at 8.85% CAGR through 2031.

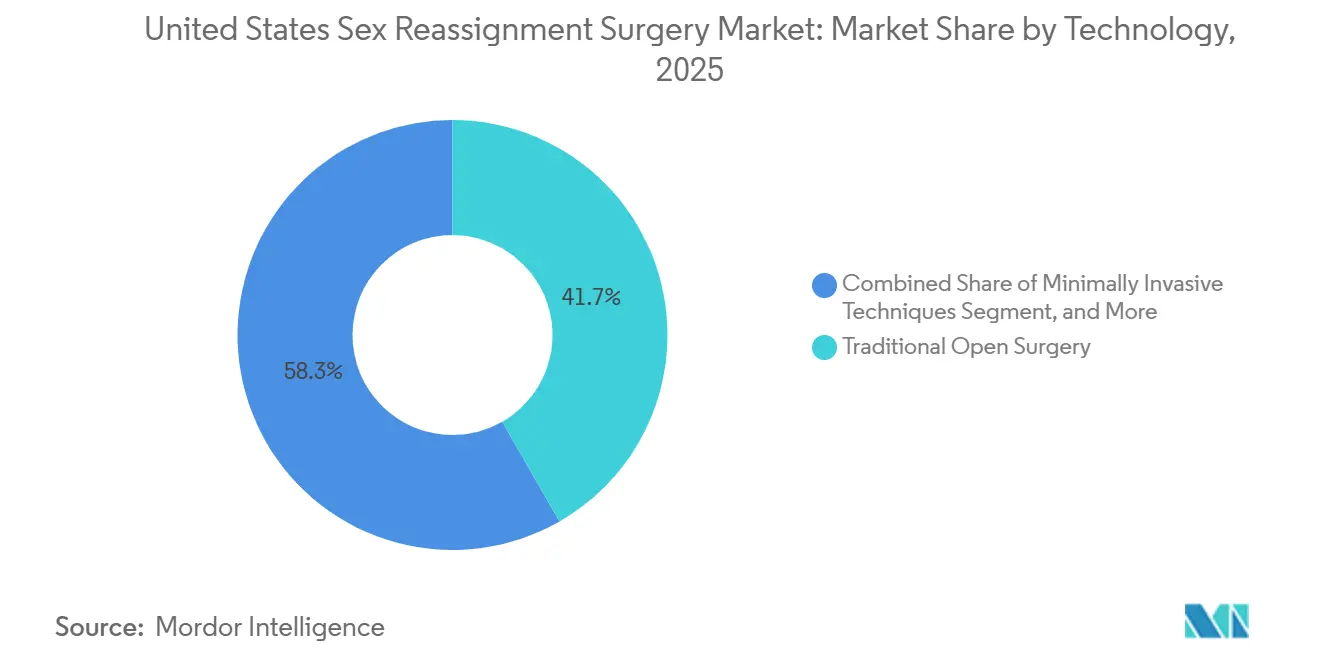

- By technology, traditional open surgery held 41.72% share in 2025, while robotic-assisted surgery is projected to grow at 10.52% CAGR through 2031.

- By end user, hospitals held 45.82% share in 2025, while specialty clinics are projected to grow at 11.06% CAGR through 2031.

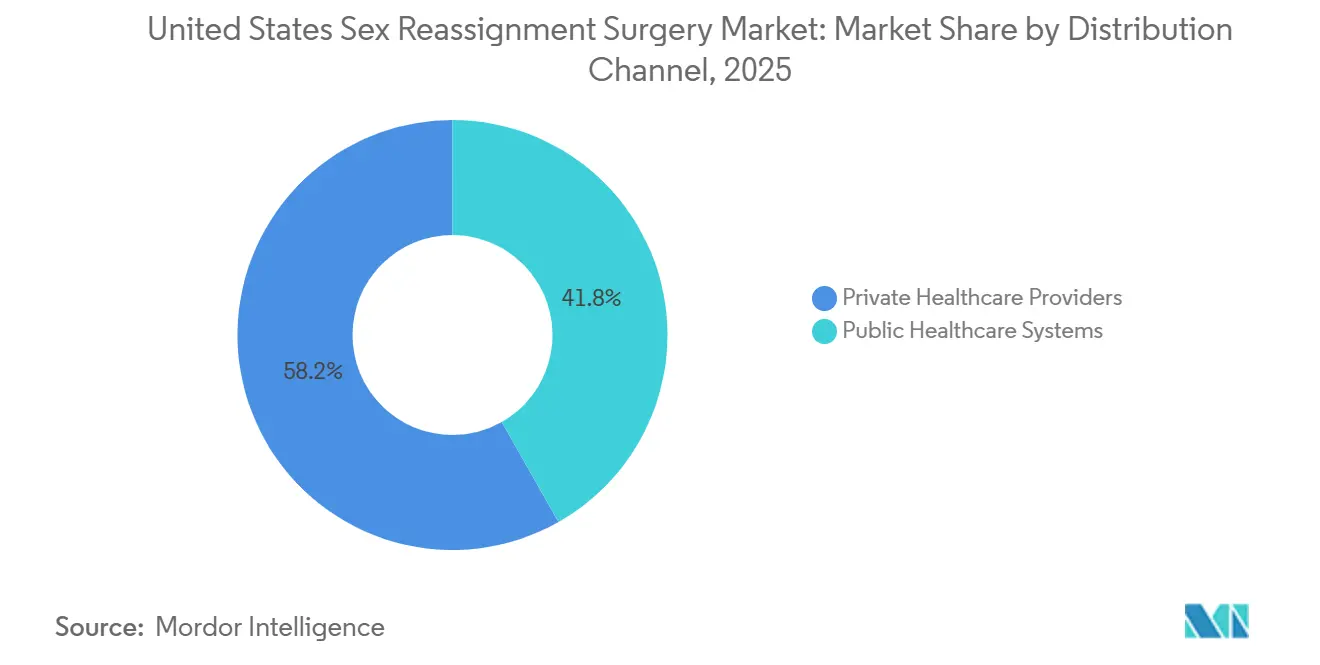

- By distribution channel, private healthcare providers held 58.23% of the United States sex reassignment surgery market share in 2025 and are projected to grow at 12.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Sex Reassignment Surgery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Insurance Coverage and Employer Health Plan Inclusion | +1.5% | Northeast and West, with spillover into the Midwest | Medium term (2-4 years) |

| Persistent Growth in Gender Dysphoria Diagnoses and Care Seeking | +2.0% | National, with concentrations in urban Northeast, West Coast, and Midwest metros | Long term (≥ 4 years) |

| Greater Patient Migration to Specialized Gender-Affirming Surgery Centers | +1.0% | California, New York, Texas, Minnesota, and Massachusetts | Short term (≤ 2 years) |

| Rapid Adoption of Robotics and 3D Imaging in Complex Reconstructive Planning | +1.2% | National, concentrated at academic centers in California, New York, Ohio, and Texas | Medium term (2-4 years) |

| U.S. State-Level Safe-Haven and Coverage Policies for Gender-Affirming Care | +0.8% | California, Massachusetts, Colorado, Oregon, Minnesota, Vermont, Delaware, and Illinois | Short term (≤ 2 years) |

| Expansion of Integrated Mental Health, Hormone, and Surgical Care Pathways | +0.7% | National, with early gains in San Francisco, Boston, New York, and Minneapolis | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Robotics and 3D Imaging in Complex Reconstructive Planning

Robotic platforms are raising the procedural ceiling in the United States sex reassignment surgery market by improving access, visualization, and precision in deep pelvic reconstruction. A 2025 review covering 500 robotic-assisted peritoneal vaginoplasty cases using the da Vinci Xi system reported a median neovaginal depth of 14.5 cm, a major complication rate of 4%, and a revision rate of 12%.[1]OAE Publishing, “Exploring the Role of Robotics in Genital Gender-Affirming Surgery: A Review of Techniques, Innovations and Outcomes,” Journal of Gender-Affirming Surgery, oaepublish.com The same review showed robotic-assisted hysterectomy in transmasculine patients produced 30 mL to 90 mL of blood loss, far below the 225 mL reported for open abdominal methods, while hospital stay remained close to laparoscopic surgery at 2.5 to 3.15 days. A 2025 paper on AI-enhanced 3D CAD/CAM guides for facial feminization reported that the digital cutting workflow was 10.2 times faster than manual planning for trained users, which points to shorter preparation time and better operating room throughput. As these methods spread through training programs, the United States sex reassignment surgery market is becoming better positioned to expand surgeon productivity without waiting for a comparable rise in highly experienced reconstructive specialists.

Persistent Growth in Gender Dysphoria Diagnoses and Care Seeking

Demand in the United States sex reassignment surgery market remains anchored in a large adult care pipeline that has continued to build even as public debate has focused heavily on minors. A 2024 cross-sectional study using 2023 insurance claims data found that gender-affirming patients generated 87% more insurance claims than non-gender-affirming patients, showing how medically active this patient group is once it enters formal care pathways.[2]Springer Nature, “Innovations in Gender Affirmation: AI-Enhanced Surgical Guides for Mandibular Facial Feminization Surgery,” Clinical Oral Investigations, link.springer.com That high utilization matters because it supports recurring contact with endocrinology, mental health, primary care, and surgical programs, which increases the likelihood of patients progressing toward operative consultation. The United States sex reassignment surgery market is also less exposed than public rhetoric suggests because adult reconstructive demand is distinct from the youth-focused restrictions that have dominated policy action. This separation of demand streams keeps the core adult opportunity intact even when provider behavior becomes more cautious in contested states.

Expanding Insurance Coverage and Employer Health Plan Inclusion

Coverage conditions in the United States sex reassignment surgery market are becoming more uneven, and that is creating both access gains and new reimbursement friction. KFF stated that beginning with plan year 2026, gender-affirming care in ACA-compliant plans is no longer treated as an essential health benefit, which means out-of-pocket costs may no longer count toward plan deductibles or maximums, and lifetime limits may apply.[3]KFF, “Do Marketplace Plans Cover Gender-Affirming Care? What Changes Have There Been to Coverage Requirements?,” KFF, kff.org At the same time, California, Colorado, New Mexico, Vermont, and Washington maintained gender-affirming care in their benchmark plan structure, and Maryland expanded Medicaid coverage beginning January 1, 2024, to include hormone therapy, top and bottom surgery, facial procedures, fertility preservation, and revision surgery. This state-level divergence is steering providers toward high-coverage-density locations where commercial reimbursement and private-pay conversion remain more durable. In practice, the United States sex reassignment surgery market will keep rewarding operators that can work effectively with employer plans, Medicaid mandates, and complex appeals rather than relying on uniform national coverage.

Expansion of Integrated Mental Health, Hormone, and Surgical Care Pathways

Integrated care models are compressing the path from diagnosis to surgery across the United States sex reassignment surgery market. The University of Michigan states that patients commonly move from initial consultation to surgery over 8 months to more than 1 year when mental health, hormone management, and surgical planning are coordinated within one program. A 2024 framework study in BMC Public Health identified connected care teams as the main structural variable associated with stronger patient-reported quality outcomes in gender-affirming care settings. The Gender Confirmation Center applied that model in Pasadena in September 2025 by combining mental health, hormonal care, and surgical consultation in one setting, which supports faster movement through pre-operative steps. A 2025 systematic review also found that hormone therapy reduced depression and improved quality of life, while surgery added further psychosocial benefit, which strengthens the medical necessity case for full-pathway programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Out-of-Pocket Cost Burden for Multi-Step Surgical Pathways | -1.5% | National, with the strongest effect in non-mandate states | Short term (≤ 2 years) |

| Surgeon and Facility Capacity Constraints in Accredited Centers | -1.0% | National, especially in rural areas and politically restrictive states | Long term (≥ 4 years) |

| Policy Volatility Across States and Payer Authorization Friction | -1.8% | South and Plains states, with secondary effects in politically contested states | Short term (≤ 2 years) |

| Revision-Surgery Risk and Post-Operative Complication Management Burden | -0.8% | National, concentrated at high-volume centers handling complex cases | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Cost Burden for Multi-Step Surgical Pathways

Financial exposure remains one of the clearest limits on volume realization in the United States sex reassignment surgery market. A 2025 PubMed-indexed study found that patients paying fully out of pocket for facial feminization surgery faced an average cost of USD 10,092 per procedure, versus USD 462 when insurance contributed even partially. The 2026 removal of essential health benefit treatment for gender-affirming care in ACA-compliant plans increases the risk that patients in non-mandate states will face higher deductibles, weaker protections, and tighter benefit design. That cost pressure is especially damaging in multi-step pathways because patients may begin treatment, complete early clinical requirements, and then postpone surgery when financing breaks down. The result is a larger pool of partially served patients, longer waiting lists, and fewer completed procedures converted into recognized revenue within the United States sex reassignment surgery market.

Policy Volatility Across States and Payer Authorization Friction

Regulatory instability is creating direct operating friction in the United States sex reassignment surgery market. NYU Langone ended its Transgender Youth Health Program in February 2026, Oregon Health & Science University confirmed in January 2026 that it had paused surgeries for patients under 19, and Kaiser Permanente paused gender-affirming surgeries for patients under 19 effective August 2025. Vanderbilt University Medical Center then exited gender-affirming surgery in April 2026, citing operational limitations and lack of surgical coverage, which deepened the access gap across the Southeast. These actions have lengthened authorization timelines, reduced provider willingness in contested states, and shifted surgical demand toward shield-law states that already face capacity pressure. Even when adult access remains legal, the United States sex reassignment surgery market still absorbs the spillover through slower approvals, staffing caution, and uneven program continuity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Gender Transition: Transmasculine Volume Dominates, but Transfeminine Revenue Accelerates

Female-to-male procedures held 61.23% of the United States sex reassignment surgery market share in 2025, which reflected the stronger uptake of chest masculinization as an early surgical step. This part of the United States sex reassignment surgery market moved faster from diagnosis to consultation because mastectomy usually carries lower procedural complexity than genital reconstruction and broader insurer acceptance. Procedure volume for transmasculine patients was concentrated in the 25 to 34 age cohort, which accounted for 41% of surgeries, and points to patients entering care after securing more stable employment and insurance. That age profile also supports steady conversion because it aligns with the period when patients are more likely to pursue irreversible surgical steps.

Male-to-female procedures are projected to grow at 9.58% CAGR through 2031, making them the fastest-expanding transition category in the United States sex reassignment surgery market. Augmentation mammoplasty supports that growth because it offers a lower-complexity, more accessible first surgery for many patients. Transfeminine care also carries a higher average revenue per case once patients move into facial feminization, voice surgery, and vaginoplasty, which helps lift value growth even when case volumes remain tighter. WPATH SOC8 has refined candidacy standards across major programs, which has preserved a measured gap between FTM and MTF procedural flow while still supporting long-term access for both groups.

By Procedure: Mastectomy Leads While Augmentation Mammoplasty Redefines Growth Vectors

Mastectomy accounted for 21.72% share of the United States sex reassignment surgery market size in 2025, making it the leading single procedure by revenue. Its role goes beyond first-year revenue because it often opens the broader FTM pathway into hysterectomy, scrotoplasty, and phalloplasty. Broad insurance acceptance has reinforced that gateway position within the United States sex reassignment surgery market. Augmentation mammoplasty is projected to expand at 8.85% CAGR through 2031 because it combines lower complexity, shorter recovery, and wider suitability for ambulatory settings.

Vaginoplasty remains the highest-revenue procedure per case, but its expansion is still limited by the small number of surgeons and centers with deep experience. Mount Sinai completed its 1,000th gender-affirming surgery in September 2025 and scheduled more than 300 procedures in 2025 alone, which illustrates both institutional scale and the intensity of demand at top centers. Phalloplasty still carries the heaviest complication burden, and a 2024 retrospective analysis reported that 30-day complications in complex staged cases could approach 76.5%, with longer operating time standing out as the strongest predictor of major events. Mount Sinai also reported abdominal phalloplasty outcomes showing 68.3% complete tactile sensitivity and 76.1% combined satisfaction in a 63-patient cohort, which suggests that newer techniques could gradually improve adoption outside a small tertiary-care circle.

By Technology: Open Surgery Holds Share While Robotics Rewrites Clinical Benchmarks

Traditional open surgery held 41.72% share in 2025, which kept it as the leading technology category across the United States sex reassignment surgery market. That position reflects the continued need for wide access and surgical familiarity in complex genital reconstruction, where anatomy and surgeon judgment still outweigh the advantages of smaller access points. Minimally invasive methods remained important in the middle of the technology mix, especially for hysterectomy and oophorectomy performed before later reconstructive stages. Robotic-assisted surgery is projected to grow at 10.52% CAGR through 2031, which makes it the fastest-rising technology segment.

A 2025 review of robotic peritoneal vaginoplasty reported a median neovaginal depth of 14.5 cm and a major complication rate of 4%, supporting outcomes that match or improve on open benchmarks in selected cases. The same review found that robotic-assisted hysterectomy in transmasculine patients could reduce blood loss to 30 mL under single-port approaches, compared with 225 mL for open abdominal surgery. It also cited a survey in which 89.7% of plastic surgeons and trainees supported adding robotics to future training, with 43.6% prioritizing microsurgery and 40.7% prioritizing flap harvest. University Hospitals Cleveland registered a clinical trial in December 2025 for the TAPCap vaginoplasty technique using robotic platforms, which shows that next-generation innovation is now closely tied to the robotic pathway.

By End User: Hospitals Anchor Volume While Specialty Clinics Capture Margin

Hospitals held 45.82% of end-user revenue in 2025, which kept them at the center of the United States sex reassignment surgery market. Academic medical centers have retained that lead because they can support the full complexity range, from lower-acuity breast procedures to multi-stage phalloplasty with microsurgical free-flap work. They also host the fellowship and training infrastructure that keeps surgeon supply concentrated in a limited number of institutions. That self-reinforcing structure has helped hospitals defend volume even as wait times have lengthened.

Specialty clinics are projected to grow at 11.06% CAGR through 2031, making them the fastest-growing end-user group in the United States sex reassignment surgery market. Their advantage comes from leaner cost structures, tighter scheduling control, and the ability to open in underserved geographies. The Gender Confirmation Center opened a comprehensive care center in Pasadena in September 2025 and expanded into San Luis Obispo County in March 2026, showing how private specialty operators are building secondary hubs outside the largest coastal metros. Ambulatory surgical centers are also gaining share in lower-complexity procedures, while other community-oriented facilities remain more vulnerable to funding pressure that can weaken referral pipelines before patients ever reach surgery.

By Distribution Channel: Private Providers Cement Position Across Both Share and Speed Metrics

Private healthcare providers held 58.23% share in 2025 and are projected to grow at 12.24% CAGR through 2031, which means they lead both scale and growth in the United States sex reassignment surgery market. This unusual combination reflects the expansion of specialty surgery networks at the same time that parts of the public system are slowing, narrowing, or exiting care lines. Public healthcare systems held the remaining 41.8%, but growth there is still more vulnerable to policy restrictions and Medicaid design differences across states. The United States sex reassignment surgery market is, therefore, becoming more dependent on private operators for both access and revenue expansion.

The split is reinforced by payer mix. A 2024 study using 2023 claims data found that commercial insurance covered 72.8% of gender-affirming patient claims, while Medicaid covered 17.2%, which shows how concentrated the patient base is in commercially insured pathways. That payer profile supports higher reimbursement density for private providers, especially in states where employer plans continue to maintain coverage. The risk is that the channel grows partly because public programs retreat, which helps near-term revenue but can create sharper political scrutiny around affordability and access over time.

Geography Analysis

The Northeast and West hold the strongest concentration of activity in the United States sex reassignment surgery market. A 2024 study using 2023 insurance claims data found that gender-affirming claims were concentrated in the West at 26.7%, the Northeast at 26.4%, and the Midwest at 24.3%, while the South accounted for 21.9%. California anchors the West through high-volume operators such as Align Surgical Associates, the Gender Confirmation Center, and UCSF, supported by a coverage environment that remains stronger than in many other states. Massachusetts strengthened provider protections in August 2025 through Chapter 16 of the Acts of 2025, which limits cooperation with out-of-state or federal investigations tied to legally protected care. These policy conditions make the Northeast and West the main receiving regions for patient and provider migration inside the United States sex reassignment surgery market.

The Midwest and mid-Atlantic show a more mixed pattern in the United States sex reassignment surgery market. Maryland expanded Medicaid coverage under the Trans Health Equity Act beginning in January 2024 and reported 1,311 in-network providers offering gender-affirming care as of November 2024. Even so, the state listed only 14 urological surgeons and 4 facial surgery providers in the network, which shows how quickly nominal coverage can run into real workforce limits. Minneapolis has also absorbed cross-border demand from nearby restrictive states, but the increase in patients has not been matched by proportional specialist expansion.

The South remains structurally underpenetrated in the United States sex reassignment surgery market. Vanderbilt University Medical Center ended its gender-affirming surgery program in April 2026, which left one of the region's most visible academic access points unavailable. That retreat forces many patients in Tennessee, Alabama, Mississippi, and Arkansas to travel across state lines for care. Travel does not fully solve the problem because receiving centers in California and Massachusetts are already managing 8 to 12-month backlogs before surgery. The capacity and geography mismatch remains the most important structural factor limiting how quickly the United States sex reassignment surgery market can translate patient demand into completed procedure revenue through 2031.

Competitive Landscape

The United States sex reassignment surgery market is moderately concentrated, with 10 to 15 institutions accounting for most complex reconstructive volume, while a much larger tail of practices handles more accessible procedures. Mount Sinai's Department of Urology completed its 1,000th gender-affirming surgery in September 2025 and scheduled more than 300 procedures in 2025, showing how scale and institutional reputation reinforce each other at the top end of the field. Align Surgical Associates strengthened its position through early adoption of robotic peritoneal pull-through vaginoplasty and by extending its geographic presence beyond California. UCSF and University Hospitals Cleveland are also using structured research and trials to support differentiation, including the STRIVE support study and the TAPCap vaginoplasty trial. This keeps competitive intensity high in the United States sex reassignment surgery market, but most of that intensity is concentrated among a relatively small number of advanced centers.

The clearest white space remains in rural areas and across much of the South, where accredited options are scarce or absent. A 2025 narrative review reported pelvic floor dysfunction in up to 94.1% of transgender men after surgery, highlighting how weak the rehabilitation layer still is after many procedures. The same review noted vaginoplasty revision rates of 27% to 60%, which creates real secondary-procedure demand that many providers still fail to capture in a systematic way. Providers that can combine index surgery, revisions, pelvic care, and structured follow-up, therefore, have a wider competitive runway inside the United States sex reassignment surgery market.

Telehealth-enabled intake and private-equity-backed specialty groups are starting to reshape how new capacity is organized in the United States sex reassignment surgery market. Even so, WPATH SOC8 continues to preserve a credentialing moat because multidisciplinary assessment, documentation, and care coordination remain hard to replicate quickly. Strong insurance authorization teams are just as important as surgical skill because appeals and coverage documentation directly affect conversion rates. Centers that pair subspecialty depth with robotic capability and payer navigation are in the strongest position to win share as the United States sex reassignment surgery market expands. The result is a field with active competition, but one where true scale still depends on specialized teams, structured workflows, and policy-resilient locations.

United States Sex Reassignment Surgery Industry Leaders

Cleveland Clinic

Mayo Clinic

Mount Sinai Health System

UCSF Health

The Johns Hopkins University

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Vanderbilt University Medical Center (VUMC) formally ended its gender-affirming surgery program, citing "operational limitations and lack of surgical coverage." The exit leaves a significant access gap in the Southeast, as VUMC had been one of the few academic centers in the region offering adult reconstructive procedures.

- February 2026: The Gender Confirmation Center expanded surgical services to San Luis Obispo County, California, becoming one of the first specialized gender-affirming surgery providers to establish a presence in the Central Coast region, following its September 2025 comprehensive care center opening in Pasadena.

- January 2026: Oregon Health & Science University (OHSU) confirmed it had paused gender-affirming surgeries for patients under 19, citing inability to maintain a surgical care team for the adolescent population amid a proposed federal rule restricting Medicare/Medicaid funding for youth gender care.

United States Sex Reassignment Surgery Market Report Scope

The United States Sex Reassignment Surgery Market refers to the commercial sector of the healthcare industry involved in providing gender-affirming surgical procedures. This includes the supply chain, hospitals, and clinics that facilitate physical transitions for transgender and non-binary individuals to align their physical appearance with their gender identity.

The United States Sex Reassignment Surgery Market is segmented by gender transition, procedure type, technology, end user, and distribution channel. By gender transition, the market includes female‑to‑male and male‑to‑female pathways. By procedure, demand spans a wide range of surgical interventions such as mastectomy, vaginoplasty, scrotoplasty, hysterectomy, phalloplasty, augmentation mammoplasty, facial feminization procedures, voice feminization surgery, reduction thyrochondroplasty, orchiectomy, metoidioplasty, and chest masculinization surgery. By technology, procedures are performed using traditional open surgery, minimally invasive techniques, and robotic‑assisted surgery. The market is further segmented by end user, including hospitals, specialty clinics, ambulatory surgical centers, and other healthcare facilities. Finally, by distribution channel, services are delivered through public healthcare systems and private healthcare providers.

| Female-to-Male |

| Male-to-Female |

| Mastectomy |

| Vaginoplasty |

| Scrotoplasty |

| Hysterectomy |

| Phalloplasty |

| Augmentation Mammoplasty |

| Facial Feminization Procedures |

| Voice Feminization Surgery |

| Reduction Thyrochondroplasty |

| Orchiectomy |

| Metoidioplasty |

| Chest Masculinization Surgery |

| Traditional Open Surgery |

| Minimally Invasive Techniques |

| Robotic-Assisted Surgery |

| Hospitals |

| Specialty Clinics |

| Ambulatory Surgical Centers |

| Other Healthcare Facilities |

| Public Healthcare Systems |

| Private Healthcare Providers |

| By Gender Transition | Female-to-Male |

| Male-to-Female | |

| By Procedure | Mastectomy |

| Vaginoplasty | |

| Scrotoplasty | |

| Hysterectomy | |

| Phalloplasty | |

| Augmentation Mammoplasty | |

| Facial Feminization Procedures | |

| Voice Feminization Surgery | |

| Reduction Thyrochondroplasty | |

| Orchiectomy | |

| Metoidioplasty | |

| Chest Masculinization Surgery | |

| By Technology | Traditional Open Surgery |

| Minimally Invasive Techniques | |

| Robotic-Assisted Surgery | |

| By End User | Hospitals |

| Specialty Clinics | |

| Ambulatory Surgical Centers | |

| Other Healthcare Facilities | |

| By Distribution Channel | Public Healthcare Systems |

| Private Healthcare Providers |

Key Questions Answered in the Report

How large is the United States sex reassignment surgery space in 2026?

It stands at USD 1.75 billion in 2026 and is projected to reach USD 2.51 billion by 2031 at a 7.46% CAGR.

Which gender transition category leads procedure demand in the United States?

Female-to-Male procedures led with 61.23% share in 2025, supported mainly by chest masculinization and faster progression to surgery.

Which procedure is growing fastest through 2031?

Augmentation mammoplasty is projected to grow at 8.85% CAGR through 2031 because it is more accessible and less complex than many genital procedures.

Why are specialty clinics expanding faster than hospitals?

Specialty clinics are projected to grow at 11.06% CAGR because they offer faster scheduling, leaner structures, and expansion into underserved areas.

What is the biggest bottleneck to future revenue growth?

Capacity remains the main bottleneck, especially the limited number of accredited surgeons and centers able to handle complex vaginoplasty and phalloplasty cases.

Page last updated on: