Spine Robotic Surgery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 533.74 Million |

| Market Size (2031) | USD 988.75 Million |

| Growth Rate (2026 - 2031) | 13.11% CAGR |

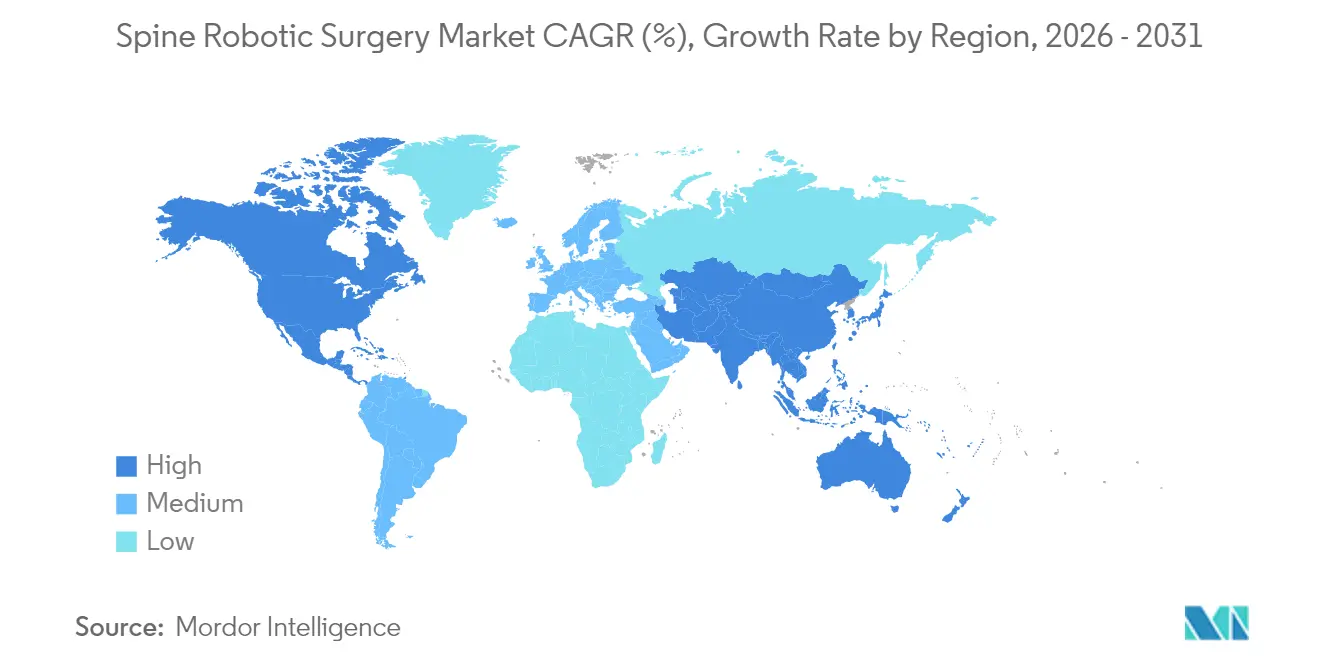

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Spine Robotic Surgery Market Analysis by Mordor Intelligence

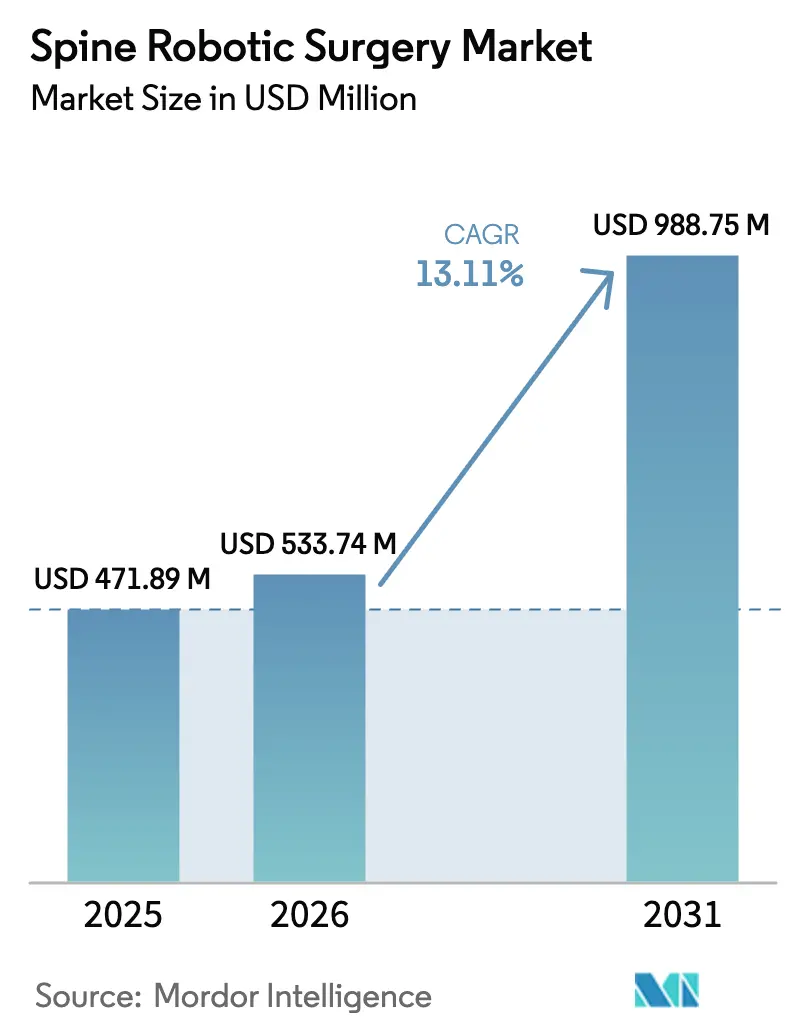

The spine robotic surgery market size in 2026 is estimated at USD 533.74 million, growing from 2025 value of USD 471.89 million with 2031 projections showing USD 988.75 million, growing at 13.11% CAGR over 2026-2031. Momentum originates from AI-assisted trajectory planning, integrated CT-navigation, and accuracy-linked reimbursement programs that reward predictable outcomes. China’s expedited “innovative device” approvals and usage-based commercial models aimed at ambulatory surgical centers are widening access to previously capital-intensive platforms. Early clinical proof points show that robot guidance regularly exceeds 95% pedicle screw accuracy, helping hospitals rationalize premium pricing through avoided revision costs. Competitive intensity remains moderate as incumbents add software services to protect installed bases while local challengers pursue value positioning in Asia-Pacific.

Key Report Takeaways

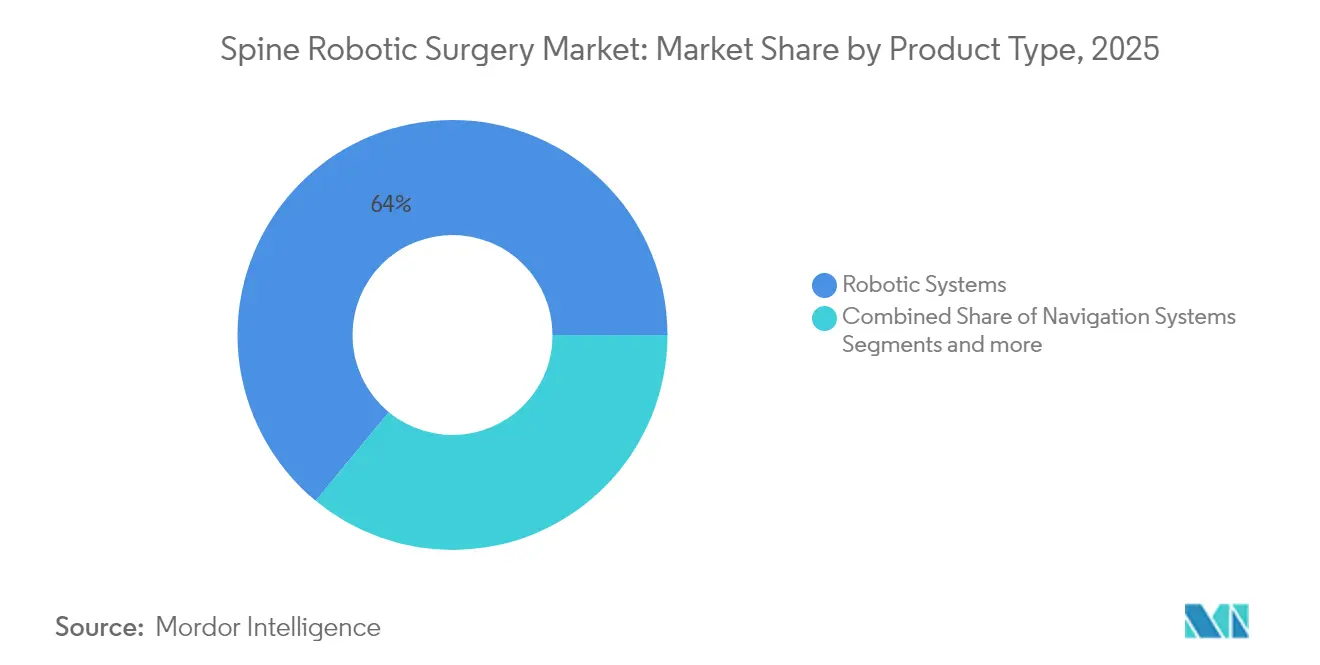

- By product type, robotic systems led with 64.02% spine robotic surgery market share in 2025, whereas navigation systems are projected to deliver the fastest 14.02% CAGR through 2031.

- By application, fusion surgery captured 76.05% of the spine robotic surgery market size in 2025 and non-fusion procedures are on track for a 14.00% CAGR to 2031.

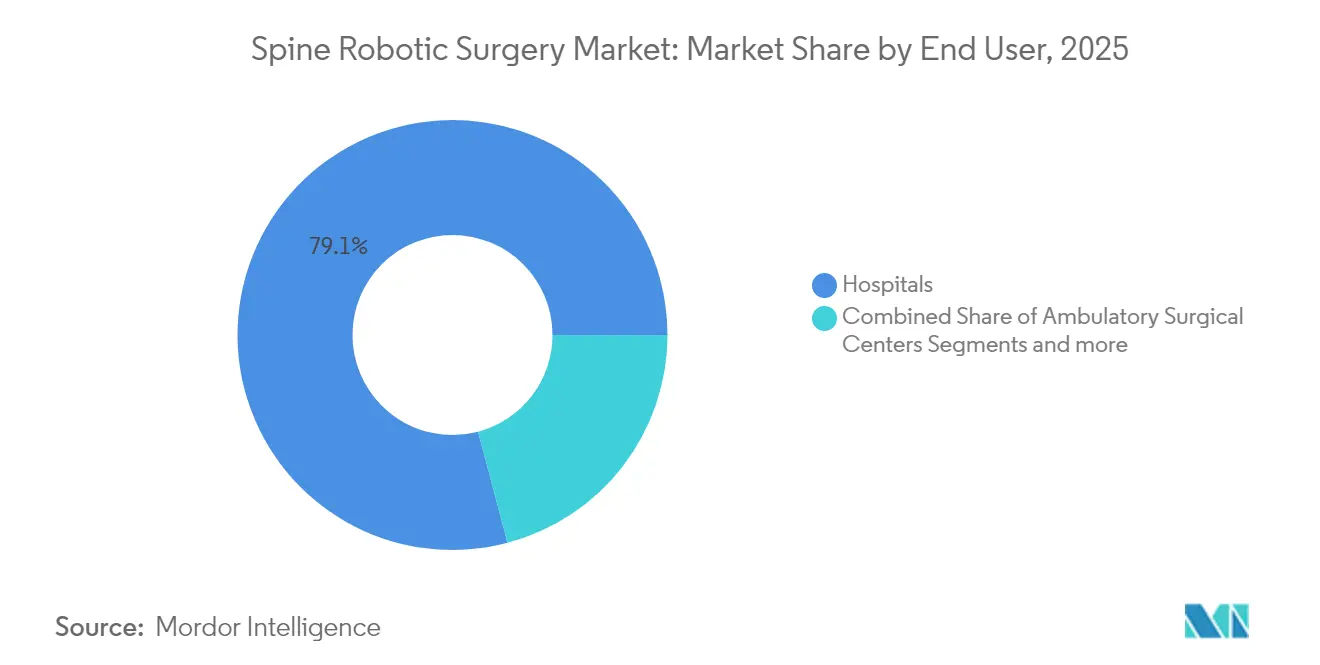

- By end user, hospitals controlled 79.12% revenue in 2025, while ambulatory surgical centers will advance at a 13.96% CAGR.

- By geography, North America contributed 42.83% sales in 2025 and Asia-Pacific is expected to post the strongest 13.88% CAGR.

- By age group, adults held 61.74% share in 2025 and the geriatric cohort is forecast to rise at a 13.93% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Spine Robotic Surgery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Minimally-invasive spine fusion robotics | +2.1% | Global with early gains in NA & EU | Medium term (2-4 years) |

| Accuracy-linked reimbursement incentives | +1.8% | North America & EU | Short term (≤ 2 years) |

| AI-powered pre-op trajectory planning tools | +1.5% | Global with spill-over to APAC | Medium term (2-4 years) |

| ASC-focused pay-per-use robot models | +1.2% | North America expanding to EU | Short term (≤ 2 years) |

| China’s fast-track device approvals | +0.9% | APAC core with influence on MEA | Long term (≥ 4 years) |

| Integrated CT-navigation robot platforms | +0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Minimally-Invasive Spine Fusion Robotics

Hospitals and surgeons are shifting complex fusion work from open to minimally invasive techniques in order to reduce tissue damage and accelerate recovery. Robot-guided pedicle screw placement has documented 98.7% accuracy in pediatric cohorts, beating fluoroscopy-guided benchmarks. Precision advantages grow in severe deformity cases where millimetric deviations can undermine fusion integrity. Typical proficiency is reached after 20-30 cases, validating system sophistication yet tempering rapid volume expansion. Providers market robotic spine programs as brand differentiators, and single-position lateral lumbar fusion has trimmed average operative time to 111.2 minutes while sustaining 95% screw accuracy.

Accuracy-Linked Reimbursement Incentives in North America & EU

The Medicare Merit-based Incentive Payment System ties payment to alignment metrics, rewarding hospitals that achieve superior radiographic outcomes. Bundled lumbar fusion payments show 36% shorter stays and 13% lower cost when optimal correction is reached. German Diagnosis Related Groups apply similar quality multipliers, reinforcing a cycle where robot accuracy secures both clinical and financial returns. As reimbursement moves from volume to value, capital committees justify robotic investment through avoided revision surgeries and labor savings.

AI-Powered Pre-Op Trajectory Planning Tools Debut

Artificial intelligence elevates preoperative planning by converting static images into dynamic screw pathways tailored to patient anatomy. Algorithms analyze CT scans, flag risky corridors, and forecast complication likelihood before incision. Early adopters report 40% shorter planning sessions and more consistent trajectories across teams. Intraoperative imaging loops let AI refine guides in real time, closing gaps between pre-op intent and live anatomy.

ASC-Focused Pay-Per-Use Robot Business Models

Usage-based pricing dismantles the USD 1-2 million barrier that historically limited adoption to tertiary hospitals. Flexible leasing links cost to actual spinal case volumes, letting ambulatory surgical centers performing 50–100 cases annually access premium technology [1] Intuitive Surgical Operations, Inc., "Flexible Financing for Acquiring Robotic Surgery Technology," intuitive.com. Outpatient programs rely on robotic precision to minimize intraoperative complications that could force hospital transfer, aligning incentives across payers, patients, and providers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and service cost | -1.4% | Global with higher impact in EMs | Long term (≥ 4 years) |

| Stringent multi-jurisdiction approvals | -0.8% | Global with delays in APAC & MEA | Medium term (2-4 years) |

| Cyber-security vulnerabilities | -0.6% | Global with focus in NA & EU | Short term (≤ 2 years) |

| Limited robotics-trained spine surgeons | -0.4% | Global with shortages in APAC & MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Service Cost of Spine Robots

Total ownership often exceeds USD 3 million once annual 10–15% service contracts are added, restricting uptake for lower-volume centers. This cost funnel concentrates units in urban hubs, raising equity concerns. Recurring maintenance and proprietary consumables compound financial burdens over system life.

Limited Pool of Robotics-Trained Spine Surgeons

Achieving competency typically requires 20–30 mentored cases plus ongoing education to retain credentials. Training capacity lags demand, especially in regions where annual spine volumes per surgeon are low. Academic fellowships are expanding but cannot yet close the skills gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Robotic Systems Drive Integration

Robotic systems delivered 64.02% of 2025 revenue, confirming their foundational role in the spine robotic surgery market. Navigation units, although smaller in base, headline growth at 14.02% CAGR by capitalizing on software-centric upgrades that bolt onto installed robots. Pedicle-screw positioning robots dominate because precision in deformity correction remains a pivotal clinical outcome. Hybrid CT-robot platforms blend real-time imaging with trajectory guidance, cutting operative cycles without sacrificing accuracy. Software and service subscriptions are expanding faster than hardware as vendors pivot toward recurring revenue models. Consumables follow installed base curves and keep margins attractive through single-use disposables that ensure sterility.

Second-generation robots ship with open-architecture software, letting hospitals integrate legacy navigation or imaging suites instead of replacing them. This interoperability reduces incremental capital outlay and encourages gradual fleet expansion. Service contracts now bundle predictive maintenance analytics, reducing downtime and reinforcing vendor-provider partnerships. As clinical data accumulate, manufacturers use machine-learning algorithms to suggest workflow improvements, creating a data moat around installed bases and elevating switching costs.

By Application: Fusion Surgery Dominance Faces Non-Fusion Challenge

Fusion surgery accounted for 76.05% of 2025 procedures, underlining a reimbursement environment that favors arthrodesis. Yet non-fusion indications are set to outpace with a 14.00% CAGR, pointing toward a structural shift within the spine robotic surgery market. Robot-assisted disc replacement and decompression now benefit from navigation upgrades that refine pathways in motion-preserving anatomy. Radiation reduction during percutaneous discectomy offers additional benefit by lowering cumulative exposure for surgical teams.

Product developers are creating end effectors optimized for endoscopic channels, enabling high-definition visualization inside narrow disc spaces. Procedural diversification insulates vendors from policy changes that could curtail fusion volumes. Healthcare systems view motion preservation plus shorter stays as aligned with value-based imperatives, setting the stage for balanced revenue between fusion and non-fusion portfolios .

By End User: ASC Growth Challenges Hospital Dominance

Hospitals retained 79.12% share in 2025 owing to capital budgets and integrated post-acute resources. Ambulatory surgical centers, however, will post the swiftest 13.96% CAGR, redefining care pathways inside the spine robotic surgery market. Outpatient single-level fusion protocols substitute overnight admissions with six-hour discharge targets, enabled by robotic accuracy that curtails operative blood loss. Pay-per-use contracts convert fixed depreciation into variable cost of goods sold, aligning with ASC cash-flow models.

Hospital managers respond by forming hub-and-spoke networks where large centers perform complex deformity work while affiliated ASCs handle routine fusions. Vendors tailor service tiers to ASC realities, emphasizing on-demand technical support and low-profile footprints that fit limited operating room space. Training content is now modularized for weekend sessions, reflecting ASC staffing patterns.

By Age Group: Geriatric Segment Drives Demographic Shift

Adults contributed 61.74% turnover in 2025, but geriatric cases will advance the fastest at 13.93% CAGR as longevity trends push degenerative spine pathology higher. Robotic precision protects frail tissues, reducing the need for extended intubation and lowering postoperative delirium risk. Software now factors age-related bone density variations into trajectory angle suggestions, supporting stable fixation in osteoporotic vertebrae.

Pediatric volume remains niche yet strategically important. Screw accuracy of 98.7% reduces re-operation rates in anatomic regions that tolerate little error. Vendors are miniaturizing instrumentation and refining safety interlocks that recognize growth plates. The combination of pediatric and geriatric growth broadens clinical utility and cushions revenue against age-specific reimbursement swings.

Geography Analysis

North America led the spine robotic surgery market with 42.83% revenue in 2025. Medicare’s quality-tied bundles reward precise alignment, making robot ownership economically rational for large health systems. FDA’s De Novo and 510(k) pathways accelerate incremental upgrades, letting manufacturers sustain rapid product cycles. Teaching hospitals publicize data that link robot use to fewer revisions, reinforcing a positive adoption loop. Venture investors back software start-ups that overlay predictive analytics on existing robotic fleets, broadening the ecosystem.

Asia-Pacific is set to record a 13.88% CAGR through 2031, the fastest globally. China’s National Medical Products Administration has compressed approval periods to under 18 months for qualifying devices, catalyzing local manufacturing scale. Domestic vendors like Tinavi Medical and MicroPort MedBot price systems 20–30% below imported units, matching budget realities while satisfying procurement quotas. Japan’s super-aging demographics and payer support for minimally invasive techniques drive steady demand. South Korea leverages robotics to retain medical tourists seeking bundled spine care packages at competitive rates.

Europe shows measured yet resilient growth. Germany anchors regional volume due to high procedure counts and DRG incentives that credit accuracy. CE-mark alignment under the Medical Device Regulation streamlines multinational launches. France and Italy co-finance robotic purchases through public-private partnerships that cap annual service expense. The UK resolved Brexit-related regulatory friction by mirroring EU technical files, re-opening a sizeable addressable market. Value-based procurement criteria favor platforms proving lower revision rates, pressuring vendors to supply longitudinal data.

Competitive Landscape

Top Companies in Spine Robotic Surgery Market

Market concentration is moderate. Medtronic, Globus Medical, and Stryker combine broad hardware lines with dedicated training ecosystems, anchoring share in Tier-1 hospitals. Medtronic’s partnership with Siemens Healthineers embeds its robot inside hybrid operating rooms where intraoperative imaging synchronizes with guidance algorithms. Globus Medical acquired NuVasive to unify implants and navigation under one commercial umbrella, unlocking cross-selling synergies. Stryker strengthens outpatient reach by ingesting Vertos Medical, which adds minimally invasive lumbar decompression to its roster.

Emerging specialists compete on price agility and software openness. Tinavi Medical’s Sino-centric supply chain curbs cost, enabling provincial hospitals to add robotics within capped budgets. eCential Robotics secured FDA clearance in March 2025, introducing a European alternative that promises fully unified navigation and robot arms inside a single drape footprint. Service differentiation intensifies as vendors roll out AI-driven troubleshooting dashboards that predict component failure before it disrupts schedules.

Cyber-security has become a decisive competitive variable. Vendors market zero-trust architectures, air-gap options, and automatic software patching that align with tightening hospital IT policies. Companies unable to demonstrate robust security certification face procurement headwinds, especially in North America where ransomware incidents have triggered high-profile elective surgery postponements.

Spine Robotic Surgery Industry Leaders

-

Stryker

-

Medtronic

-

Accuray Incorporated

-

Globus Medical, Inc.

-

Lem Surgical Ag

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: eCential Robotics received FDA clearance for its robotic guidance system, granting European technology a foothold in the United States.

- December 2024: Stryker completed the acquisition of Vertos Medical, expanding its minimally invasive spine offering for outpatient settings.

- September 2024: Medtronic broadened collaboration with Siemens Healthineers to co-develop imaging-integrated spine robotics for hybrid operating rooms.

- August 2024: Spineology raised USD 25 million to accelerate outpatient-focused robotic solutions.

Global Spine Robotic Surgery Market Report Scope

As per the scope of the report, spine surgical robots are advanced medical devices that leverage robotics, computer-assisted navigation, and cutting-edge imaging technologies to enhance the precision, accuracy, and overall outcomes of complex spinal procedures, providing healthcare providers with a competitive edge in delivering state-of-the-art surgical care. The spine robotic surgery market is segmented by product type, application, and end user. Based on product type, the market is segmented into systems, consumables and accessories, and software and services. Based on the application, the market is segmented into fusion surgery and non-fusion surgery. Based on end users, the market is segmented as hospitals and ambulatory surgical centers. The report also covers the market sizes and forecasts for the spine robotic surgery market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Robotic Systems | Pedicle-screw positioning robots |

| Navigation-integrated robots | |

| Hybrid imaging-robot platforms | |

| Navigation Systems | |

| Consumables & Accessories | |

| Software & Services |

| Fusion Surgery |

| Non-fusion Surgery |

| Hospitals |

| Ambulatory Surgical Centers |

| Others |

| Adults |

| Geriatric |

| Pediatric |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Robotic Systems | Pedicle-screw positioning robots |

| Navigation-integrated robots | ||

| Hybrid imaging-robot platforms | ||

| Navigation Systems | ||

| Consumables & Accessories | ||

| Software & Services | ||

| By Application | Fusion Surgery | |

| Non-fusion Surgery | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Others | ||

| By Age Group | Adults | |

| Geriatric | ||

| Pediatric | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the spine robotic surgery market?

The spine robotic surgery market size is USD 533.74 million in 2026.

How fast is the spine robotic surgery market expected to grow?

Between 2026 and 2031 the market is projected to expand at a 13.11% CAGR, reaching USD 988.75 million.

Which product segment holds the largest share today?

Robotic systems account for 64.02% of 2025 revenue, reflecting their critical role in precision screw placement.

Why are ambulatory surgical centers important for future growth?

ASCs will post a 13.96% CAGR because pay-per-use financing makes robotics affordable and supports outpatient fusion protocols that shorten recovery.

Which region will see the fastest growth to 2031?

Asia-Pacific is forecast to lead with a 13.88% CAGR owing to China’s expedited regulatory pathways and expanding domestic manufacturing.

Page last updated on: