Robotic Prosthetics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

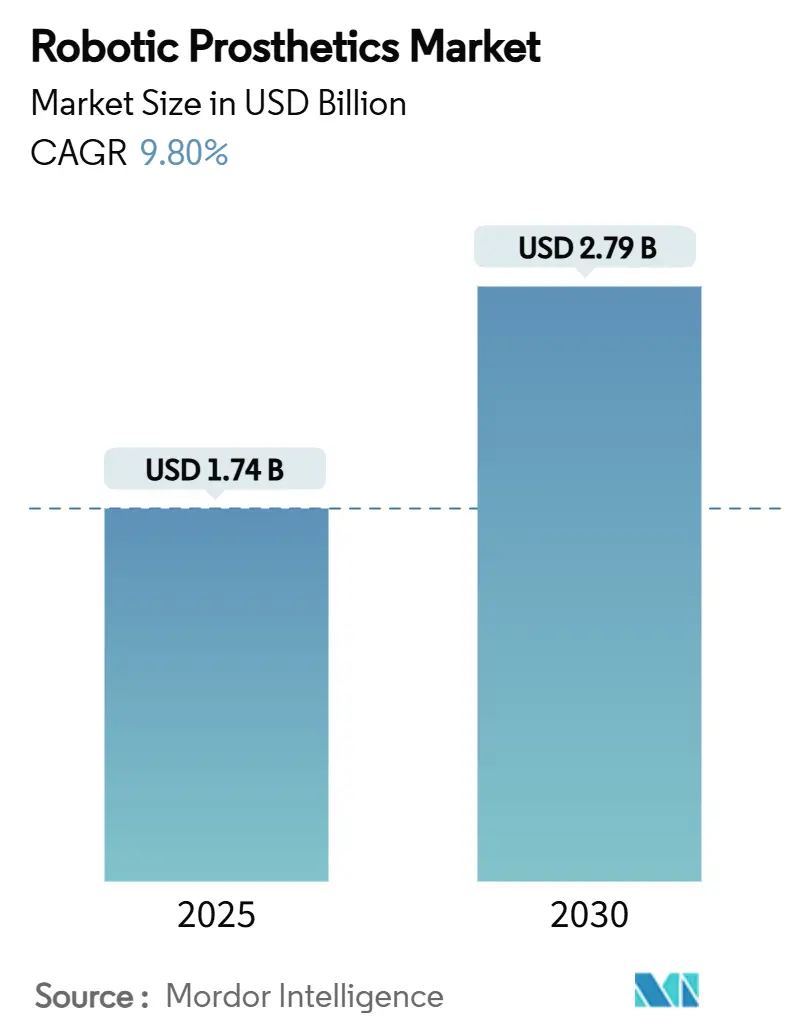

| Market Size (2025) | USD 1.74 Billion |

| Market Size (2030) | USD 2.79 Billion |

| Growth Rate (2025 - 2030) | 9.80% CAGR |

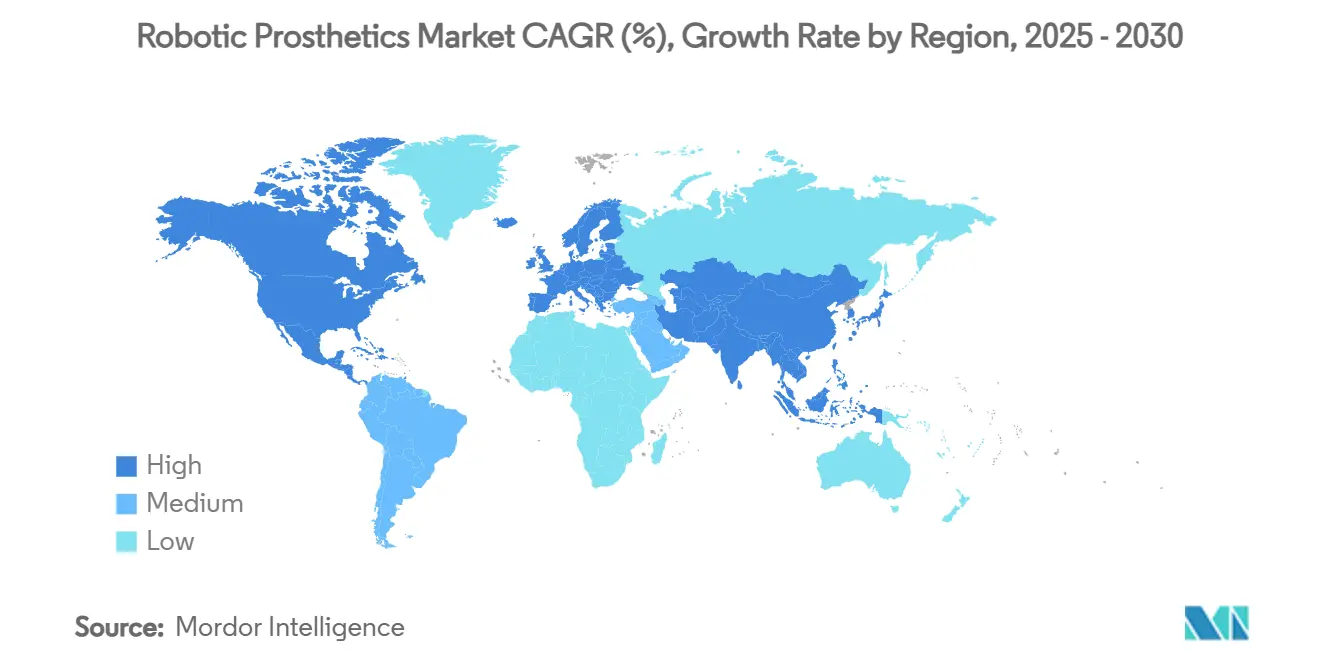

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Robotic Prosthetics Market Analysis by Mordor Intelligence

The robotic prosthetics market size reached USD 1.74 billion in 2025 and is projected to expand to USD 2.79 billion by 2030, advancing at 9.8% CAGR. Robust patent activity, improving reimbursement terms, and deeper integration of neural interfaces with additive manufacturing form the backbone of this expansion. Widespread uptake of micro-processor controlled (MPC) limbs, Medicare’s 2.4% pricing uplift for non-competitive-bid devices, and accelerating venture capital interest underscore a demand environment that rewards clinically validated performance improvements. Competitive intensity rises as traditional manufacturers face start-ups armed with minimally invasive muscle-machine interfaces and FDA breakthrough status, while national subsidy programs in China and expanded European coverage widen the global addressable pool. Supply-chain fragility around rare-earth magnets and cybersecurity obligations for connected firmware inject operational risk but also spur design shifts toward soft actuators and encrypted device architectures. Forward-looking players that marry AI-enabled intent detection with rapid-cycle 3D printing are well-placed to capture the next leg of growth across the robotic prosthetics market.

Key Report Takeaways

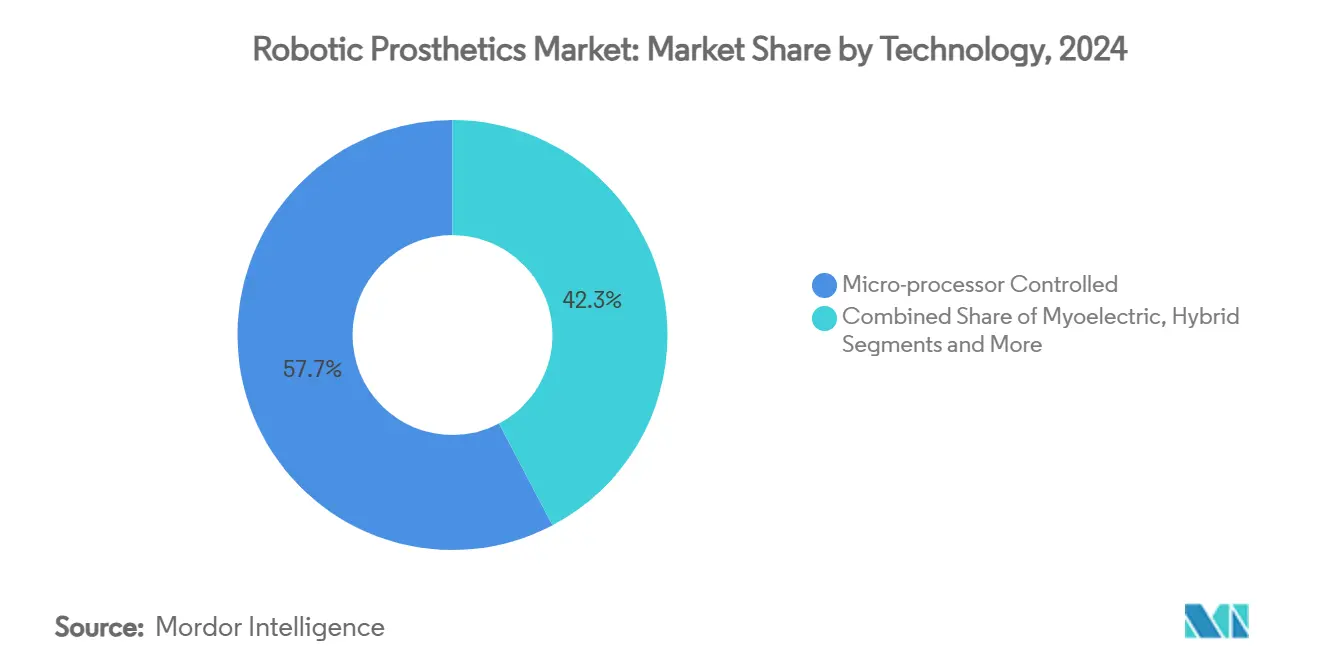

- By technology, micro-processor control led with 57.7% revenue share in 2024; hybrid neural-interface systems are forecast to expand at a 15.1% CAGR through 2030.

- By extremity, lower limb devices accounted for 56.5% of the robotic prosthetics market share in 2024, while modular multi-extremity systems are projected to grow at 13.7% CAGR to 2030.

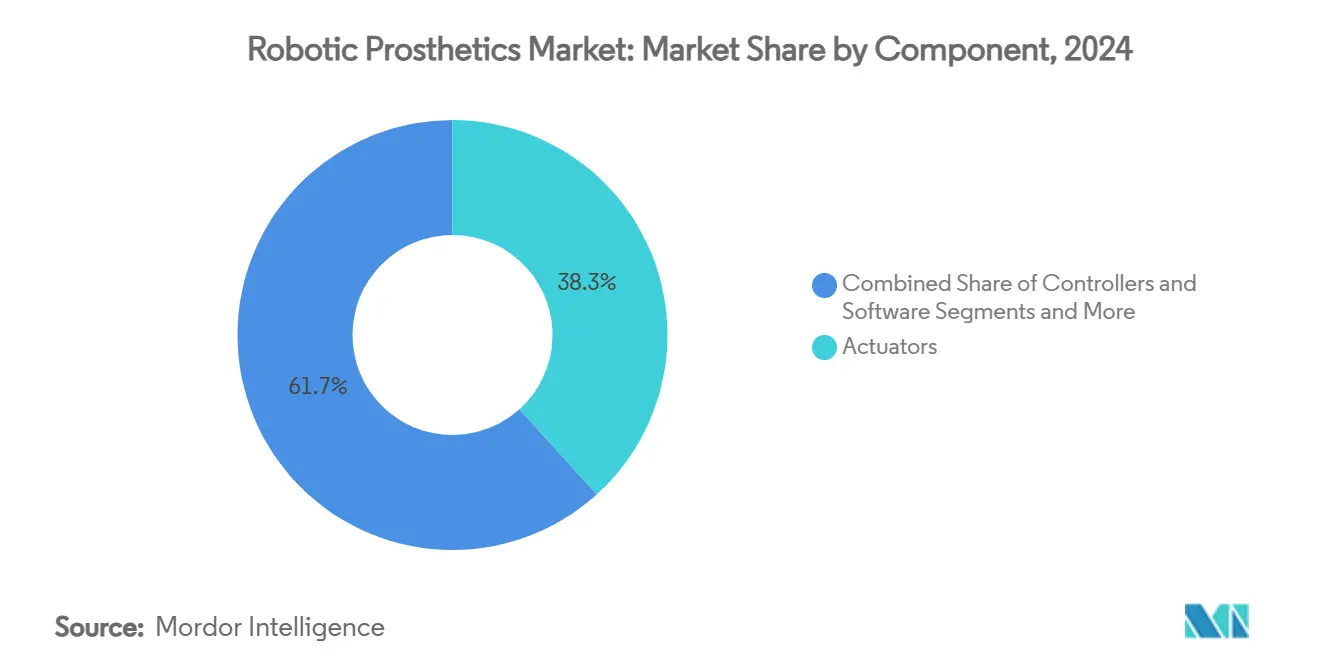

- By component, actuators commanded a 38.3% share of the robotic prosthetics market in 2024, whereas controllers and software will record the fastest 16.3% CAGR forecast.

- By end user, prosthetic and orthotic clinics held a 54.6% market share in 2024; home care is set to register a 14.5% CAGR through 2030.

- By geography, North America dominated with a 43.8% share in 2024, whereas Asia-Pacific is advancing at a 12.9% CAGR during the forecast horizon.

Global Robotic Prosthetics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of MPC knees & ankles | +2.10% | North America, EU | Medium term (2-4 years) |

| Declining cost curve of myoelectric control | +1.80% | Global; strongest in emerging markets | Long term (≥ 4 years) |

| Reimbursement expansion for bionic limbs | +1.50% | OECD & China | Medium term (2-4 years) |

| Veterans-health pilots accelerating uptake | +1.20% | North America, allies | Short term (≤ 2 years) |

| AI-enabled intent detection + additive mfg | +1.40% | Developed markets | Long term (≥ 4 years) |

| Venture funding surge into neuro-interface | +0.80% | North America, EU, Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Micro-Processor Controlled Knees & Ankles

Clinical evidence shows that MPC devices cut fall risk by up to 80%, a statistic now driving wider insurer acceptance. Ottobock’s Genium X4 knee improves stance stability, offers 5-day battery life, and maintains full waterproofing, thereby reducing day-to-day maintenance burdens for active users. Medicare’s draft rule proposing K2-level eligibility for MPC knees further broadens the reimbursable base.[1]Centers for Medicare & Medicaid Services, “Proposed LCD—Lower Limb Prostheses (DL33787),” cms.gov European payers mirror this shift, embedding MPC limbs within value-based purchasing frameworks that prioritize fall prevention and reduced inpatient episodes. Suppliers respond by bundling continuous gait-analysis apps that flag abnormal loading and trigger remote adjustments in real time.

Declining Cost Curve of Myoelectric Controllers and sEMG Sensors

Miniaturized surface electromyography arrays now achieve 97% movement-prediction accuracy when paired with force myography, improving intuitiveness without cost escalation. Open-source prosthetic designs fabricated on consumer-grade 3-D printers come in below USD 50, democratizing access in low-income settings.[2]MDPI, “Health IoT Threats: Survey of Risks,” mdpi.com Ottobock’s Myo Plus pattern-recognition platform gained a standalone CMS billing code (L6700) in 2025, cementing reimbursement pathways for machine-learning-based control. Volume production and broader code coverage together compress pricing, allowing clinics to upgrade sockets with embedded electronics rather than replace entire limbs. Manufacturers leverage cloud-based calibration tools that pare set-up times from hours to minutes, advantaging high-throughput clinics.

Favourable Reimbursement Expansion for Bionic Limbs in OECD & China

China’s nationwide subsidy now fully covers 140 assistive devices, supporting 85 million people with disabilities and 40 million seniors.[3]China Daily, “Subsidies Improve Access to Assistive Devices,” chinadaily.com.cn Western European markets report myoelectric penetration above 80% where reimbursement is universal, compared with sub-40% in restrictive systems. Policy frameworks now factor psychosocial wellbeing and long-term productivity, shifting assessments away from bare-bones mobility metrics. In the United States, the 2.4% Medicare fee-schedule uplift for 2025 affirms steady reimbursement headwinds despite budgetary pressure. This wave of coverage liberalization converts suppressed need into paying demand, bolstering the outlook for the robotic prosthetics market.

Veterans-Health Technology Pilots Accelerating Public Procurement

The Department of Veterans Affairs completed its first osseointegration surgery in 2024, creating a high-profile proof point for socket-free limb integration. Follow-on BRAVE grants of up to USD 100,000 per project fund commercialization of lab-grade prototypes, while SAHAT grants allocate USD 200,000 for solutions aimed at veterans with toxic-exposure injuries. Veterans’ Affairs purchasing patterns often set the benchmark for private insurers, shortening the time lag between military pilots and civilian uptake. Device makers tailor marketing around return-to-work metrics and reduced secondary complications to secure procurement contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prosthetic abandonment tied to comfort & weight | -1.80% | Global; higher in developing economies | Medium term (2-4 years) |

| Cyber-security & privacy risks in connected limbs | -1.20% | Highly connected markets | Long term (≥ 4 years) |

| Scarcity of qualified prosthetists outside metros | -1.50% | Rural & emerging markets | Long term (≥ 4 years) |

| Rare-earth actuator supply-chain fragility | -1.30% | North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Prosthetic Abandonment Owing to Comfort & Weight Issues

Abandonment rates range from 9% to 34% as users reject devices they perceive as heavy, hot, or insufficiently functional. Socket fit remains the most cited pain point; limb-volume fluctuations destabilize pressure distribution, triggering skin lesions and device slippage. Heat-exchanging metal liners under exploration at research labs show promise in dissipating thermal build-up without weight penalties. Meanwhile, graphene-enhanced interface materials offer antimicrobial surfaces that reduce infection risk and improve long-term skin health. Yet, until mass-market units integrate these improvements, abandonment remains a headwind to sustained usage growth across the robotic prosthetics market.

Cyber-Security & Privacy Risks in Cloud-Connected Prosthetic Firmware

Healthcare IoT ecosystems are projected to reach USD 486.34 billion by 2031, multiplying the attack surface for bad actors. Compromised firmware could disable balance control or expose biometric logs, posing life-threatening scenarios and regulatory liability for manufacturers. Current directives mandate basic encryption and regular patch cycles, yet device lifespans frequently exceed vendor support windows, creating long-tail vulnerabilities. Standard-setting bodies now weigh stricter post-market surveillance requirements, pushing OEMs to build over-the-air update pathways and zero-trust architectures. Until these frameworks reach maturity, risk-averse payers and hospital systems may limit large-scale rollouts of fully connected limbs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Micro-processor Control Dominates Innovation

Micro-processor systems held 57.7% of 2024 revenues and remain the workhorse of the robotic prosthetics market. Energy-efficient embedded chips adjust stance and swing in real time, cutting metabolic costs and extending battery life. The hybrid neural-interface segment is set to outpace all others with a 15.1% CAGR as FDA fast-track designations accelerate market entry. Myoelectric limbs retain strong clinical penetration, especially in the upper extremity, where mechanical feedback is critical to fine-motor tasks. Body-powered devices persist in austere environments, favored for durability and cost. RPNI-based interfaces promise a next-gen leap in signal fidelity; early trials show stable control over multi-year horizons.

By Extremity: Lower Limb Leadership Faces Multi-System Challenge

Lower limb solutions represented 56.5% of global 2024 sales, a reflection of higher amputation incidence and deeper reimbursement history. Socket-free osseointegrated mounts improve load transfer and proprioception, potentially eroding the comfort gap versus biological limbs. Upper limb abandonment persists at around 20% due to weight and maintenance complexity. Multi-extremity systems, posting a 13.7% CAGR, cater to polytrauma cases and congenital limb deficiencies, bundling shared batteries and control hubs for user convenience. Emerging variable-stiffness ankle-foot modules deliver smoother transitions across walking speeds, mitigating contralateral limb stress and lowering injury risk.

By Component: Actuators Drive Performance Innovation

Actuators captured 38.3% of the 2024 value, acting as the mechanical heart of powered limbs. Brushless electric motors dominate due to controllability, while hydraulics find niches in high-load tasks. Soft pneumatic muscles attract R&D funding for lightweight pediatric applications. Controllers and embedded software post a 16.3% CAGR as AI algorithms scale, leveraging cloud analytics to refine gait patterns remotely. Sensor fusion—combining sEMG, inertial, and force data—achieves 97% prediction accuracy, informing real-time joint torque modulation. Materials science advances yield titanium-graphene hybrid sockets that shed grams while boosting tensile strength, directly addressing abandonment drivers.

By End User: Clinical Settings Evolve Toward Home Care

Specialty prosthetic clinics controlled 54.6% of 2024 revenues, leveraging deep fitting expertise and insurer relationships. Yet remote-care platforms now feed device diagnostics into cloud dashboards, letting clinicians push firmware tweaks without in-person visits. Home-care grows 14.5% CAGR as insurers incentivize outpatient rehab and as elderly users prefer in-home adjustments. Hospitals remain critical during acute rehab phases; early fitting within eight weeks of amputation correlates with higher long-term utilization. Sports medicine centers cater to performance-oriented users, employing instrumented treadmills and motion capture to optimize prosthetic tuning for peak output.

Geography Analysis

North America led with a 43.8% 2024 share, thanks to robust payer systems and veteran-driven R&D pipelines. The region’s sizable amputee cohort, estimated at 2.6 million, benefits from coordinated rehabilitation networks that shorten time first to fit. EU markets maintain high penetration, aided by harmonized Medical Device Regulations that extend compliance windows for legacy devices, granting OEMs breathing room to update portfolios. Western European adoption of myoelectric limbs exceeds 80%, reflecting broad insurance coverage and centralized purchasing bodies.

Asia-Pacific, advancing at 12.9% CAGR, is propelled by China’s subsidy covering 140 assistive products and by demographic aging across Japan and South Korea. Local firms increasingly license AI-based controllers to sidestep high import duties on finished units, intensifying cost competition. India’s Make-in-India incentives reduce GST on assistive technology parts, encouraging domestic 3-D printing lines for rural distribution.

Latin America remains underpenetrated but poised for mid-single-digit growth as Brazil updates its Unified Health System procurement list to include powered knees. The Middle East and Africa see sporadic adoption driven by philanthropic programs; however, a tight supply of certified prosthetists and higher customs duties impede scale. Regional governments explore tele-rehab pilots to stretch clinician reach and increase device retention.

Competitive Landscape

Ottobock, Össur, and Blatchford together controlled significant market share in 2024, underscoring a market where scale accords sourcing leverage but does not preclude disruption. Ottobock deepened its AI stack via minority investment in Phantom Neuro, aligning with emerging neural interfaces. Össur obtained grants for ventilated liners and adjustable seals, targeting comfort-linked abandonment. Hanger’s purchase of Fillauer augmented supply-chain control and added pediatric portfolio depth.

New entrants focus on software value; Synchron and Paradromics license cloud dashboards designed for hospital IT integration, foregoing hardware margins in favor of recurring fees. Enovis added LimaCorporate for USD 864 million, stitching together implants and smart-sensor sleeves into an end-to-end orthopedics play. Patent filings shift toward battery chemistries and soft robotics, as evidenced by Johns Hopkins’ fiber battery application, which enables seamless textile integration.

Companies increasingly package remote-monitoring subscriptions alongside limbs, creating annuity streams and data feedback loops that bolster R&D. Differentiation pivots on ecosystem breadth—devices, software, clinical training—and the ability to navigate looming cybersecurity regulations without inflating cost.

Robotic Prosthetics Industry Leaders

Ottobock SE & Co. KGaA

Össur hf.

Blatchford Group

Fillauer LLC

Steeper Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: MIT unveiled an osseointegrated mechanoneural prosthesis that pairs muscle grafts with a titanium intramedullary rod to restore near-natural gait on stairs and uneven ground.

- April 2025: Phantom Neuro raised USD 19 million Series A led by Ottobock to advance Phantom X muscle-machine interface toward pivotal trials.

- March 2025: FDA granted breakthrough device status to Phantom X neural-interface prosthetic, streamlining pre-market review

- February 2025: Enovis agreed to buy LimaCorporate for EUR 800 million (USD 864 million), forging a prosthetics-orthopedics portfolio topping USD 1 billion revenue.

Global Robotic Prosthetics Market Report Scope

| Micro-processor Controlled Prosthetics |

| Myoelectric Prosthetics |

| Body-powered / Cable-operated |

| Hybrid & Others |

| Lower Limb (Knee, Ankle, Foot) |

| Upper Limb (Elbow, Wrist, Hand, Fingers) |

| Modular / Multi-Extremity Systems |

| Others (Cranio-facial, Spine) |

| Actuators (Electric, Hydraulic, Pneumatic, Soft) |

| Sensors (sEMG, IMU, Force, Pressure) |

| Controllers & Software |

| Sockets & Interface Materials |

| Prosthetic & Orthotic Clinics |

| Hospitals & Trauma Centres |

| Rehabilitation & Sports Medicine Centres |

| Home-care & Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Micro-processor Controlled Prosthetics | |

| Myoelectric Prosthetics | ||

| Body-powered / Cable-operated | ||

| Hybrid & Others | ||

| By Extremity | Lower Limb (Knee, Ankle, Foot) | |

| Upper Limb (Elbow, Wrist, Hand, Fingers) | ||

| Modular / Multi-Extremity Systems | ||

| Others (Cranio-facial, Spine) | ||

| By Component | Actuators (Electric, Hydraulic, Pneumatic, Soft) | |

| Sensors (sEMG, IMU, Force, Pressure) | ||

| Controllers & Software | ||

| Sockets & Interface Materials | ||

| By End User | Prosthetic & Orthotic Clinics | |

| Hospitals & Trauma Centres | ||

| Rehabilitation & Sports Medicine Centres | ||

| Home-care & Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Frequently Asked Question

Concise Answer

What is the current size of the robotic prosthetics market?

The robotic prosthetics market size stood at USD 1.74 billion in 2025.

How fast is the robotic prosthetics market expected to grow?

It is forecast to register a 9.9% CAGR, reaching USD 2.79 billion by 2030.

Which technology segment is growing the quickest?

Hybrid neural-interface systems are projected to rise at a 15.1% CAGR through 2030.

Which region will see the fastest growth?

Asia-Pacific leads with a 12.9% CAGR due to expanding subsidies and aging demographics.

Why do many users abandon prosthetic devices?

Discomfort, weight, and poor socket fit drive abandonment rates as high as 34% in some cohorts.

How are cybersecurity concerns being addressed?

Manufacturers are adding encryption, over-the-air update paths, and zero-trust architectures to mitigate risks in connected limbs.

Page last updated on: