United States General Surgical Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

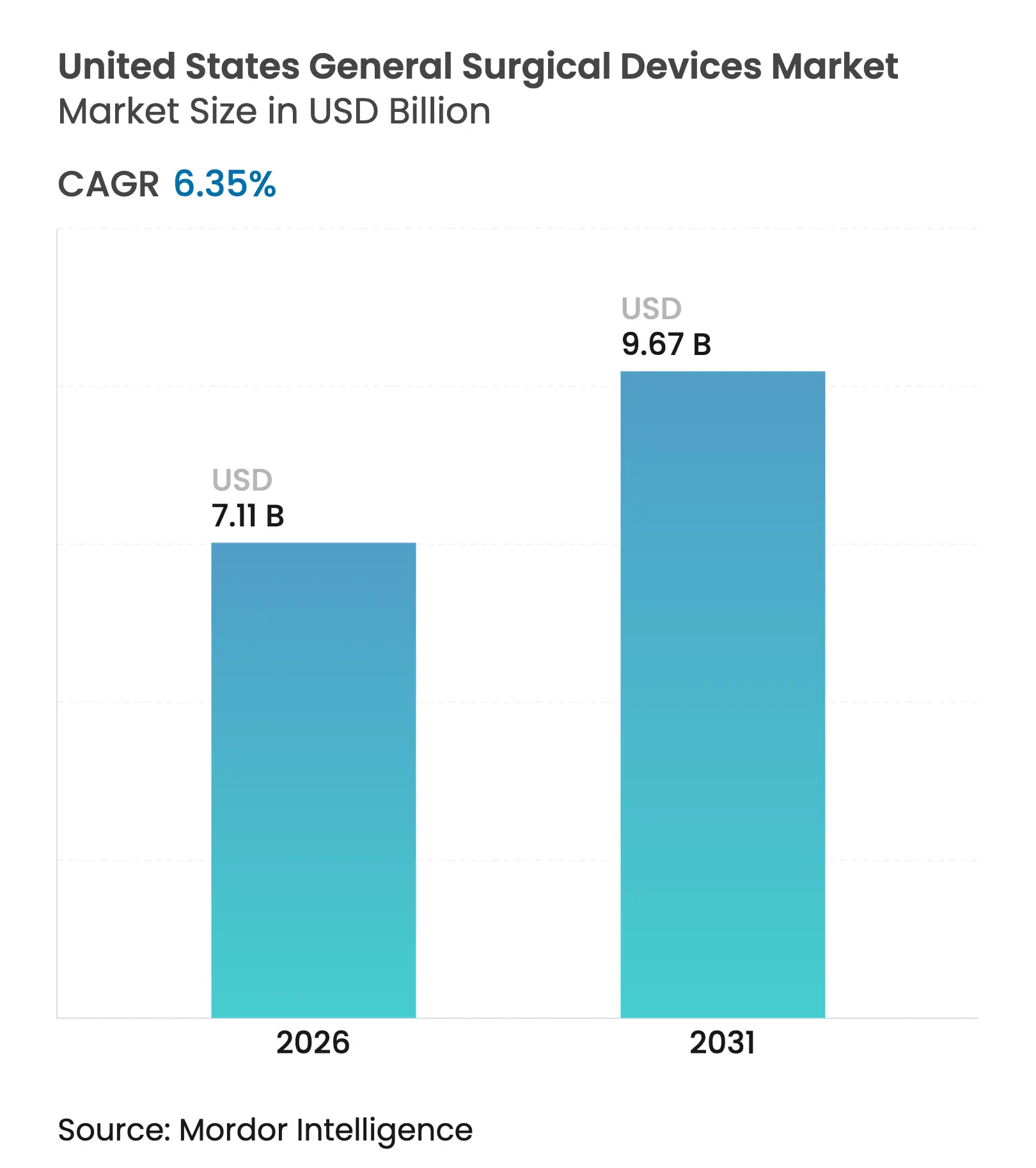

| Market Size (2026) | USD 7.11 Billion |

| Market Size (2031) | USD 9.67 Billion |

| Growth Rate (2026 - 2031) | 6.35 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

United States General Surgical Devices Market Analysis by Mordor Intelligence

The United States General Surgical Devices Market size market size in 2026 is estimated at USD 7.11 billion, growing from 2025 value of USD 6.69 billion with 2031 projections showing USD 9.67 billion, growing at 6.35% CAGR over 2026-2031. Rising procedure volumes, rapid diffusion of minimally invasive techniques, and the migration of high-acuity cases into ambulatory settings together redefine how the United States general surgical devices market allocates capital and manages inventory. Federal incentives that reward domestic production help manufacturers shorten lead times and counter tariff exposure, while AI-enabled imaging and navigation systems improve precision and labor efficiency across specialties. At the same time, payers accelerate value-based purchasing, encouraging hospitals and ASCs to favor solutions that prove lower cost per procedure. These dynamics collectively sustain robust demand even as device buyers negotiate aggressively for better pricing.

Key Report Takeaways

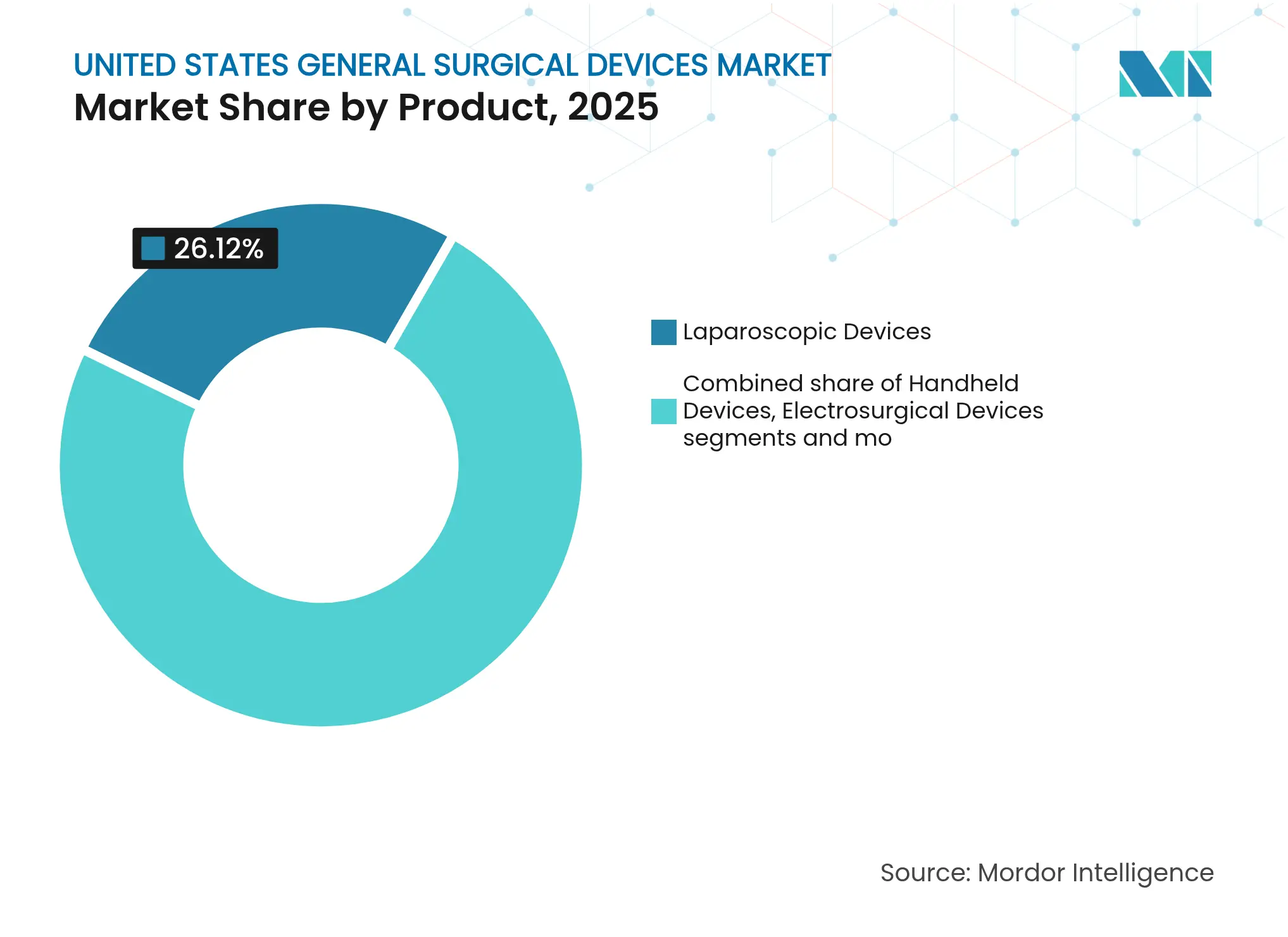

- By product, laparoscopic devices dominated the United States general surgical devices market share with 26.12% in 2025; electrosurgical devices are expected to register the fastest 8.09% CAGR through 2031.

- By procedure approach, minimally invasive surgery held 68.64% of the United States general surgical devices market share in 2025. It is further expected to grow at a CAGR of 7.03% from 2026 to 2031.

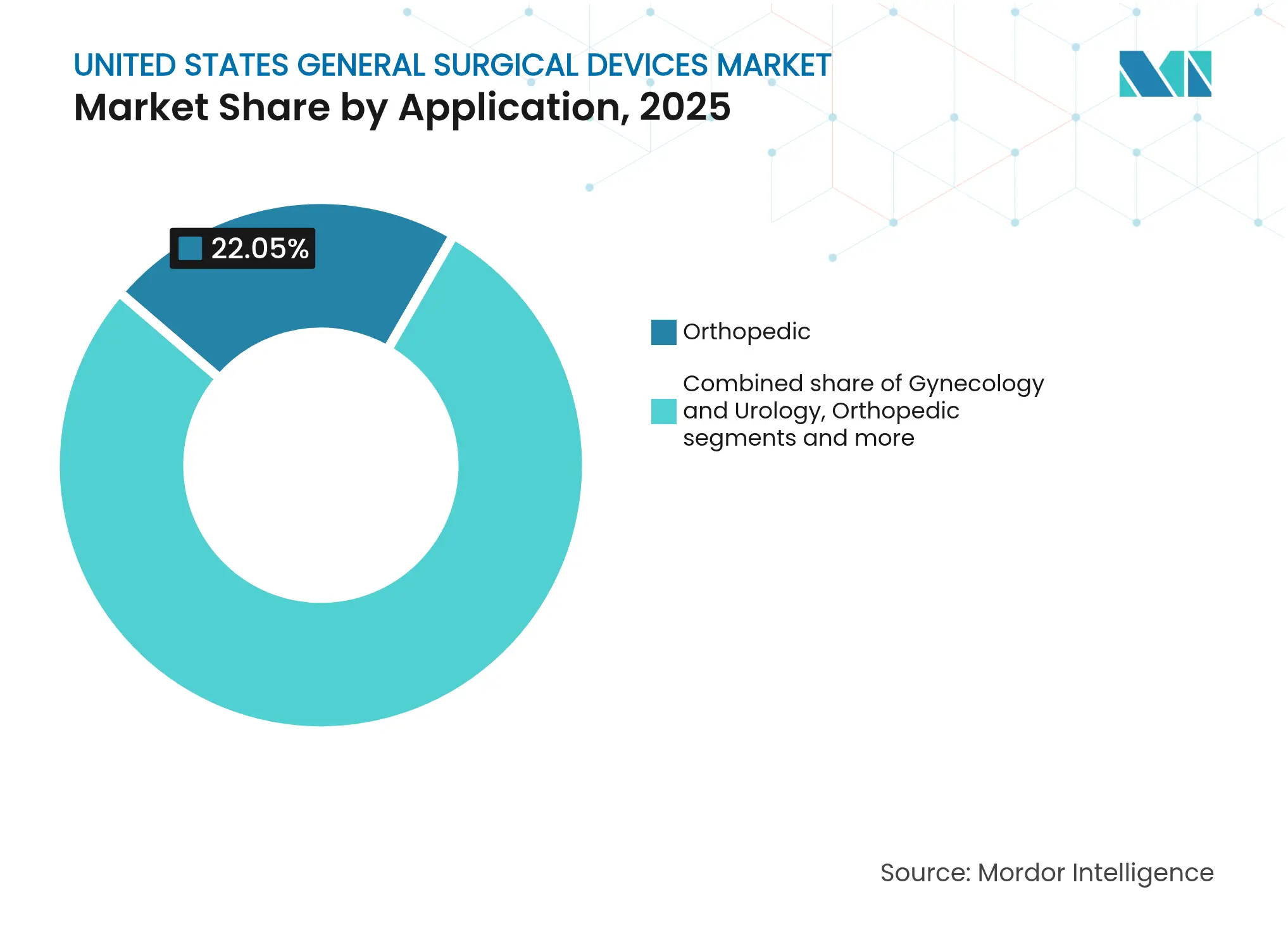

- By application, the orthopedic segment acquired a market share of 22.05% in the United States general surgical devices market in 2025, gynecology and urology lead growth with a 7.66% forecast CAGR to 2031.

- By end user, hospitals accounted for 67.98% of the United States general surgical devices market size in 2025, whereas ambulatory surgical centers are expanding at an 7.9% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States General Surgical Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Aging population & rising chronic disease burden

driving surgical demand

Aging population & rising chronic disease burden

driving surgical demand

| +1.8% | National, concentrated in Sunbelt states | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

+1.8%

|

Geographic Relevance

:

National, concentrated in Sunbelt states

|

Impact Timeline

:

Long term (≥ 4 years)

|

Increasing adoption of minimally-invasive and

robotic-assisted procedures

Increasing adoption of minimally-invasive and

robotic-assisted procedures

| +1.5% | National, led by metropolitan areas | Medium term (2-4 years) | |||

ASC expansion driving device uptake

ASC expansion driving device uptake

| +1.2% | National, accelerated in suburban markets | Medium term (2-4 years) | |||

Rapid technology advancements

Rapid technology advancements

| +0.9% | National, early adoption in academic centers | Short term (≤ 2 years) | |||

Integration of AI-guided imaging & navigation boosting

procedural efficiency

Integration of AI-guided imaging & navigation boosting

procedural efficiency

| +0.7% | National, concentrated in high-volume centers | Medium term (2-4 years) | |||

Federal incentives for domestic manufacturing reshaping

device supply chains

Federal incentives for domestic manufacturing reshaping

device supply chains

| +0.4% | National, focused on manufacturing hubs | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Aging Population & Rising Chronic Disease Burden Driving Surgical Demand

Medicare projections show spinal instrumentation costs accelerating as the 65+ cohort grows, reinforcing long-run demand for surgical care.[1]Source: Y. Huang et al., “Projections of Spinal Instrumentation Volume,” U.S. National Library of Medicine, pmc.ncbi.nlm.nih.gov Providers, therefore, invest in minimally invasive and outpatient-ready platforms that reduce length of stay and complication risk. The United States general surgical devices market consequently favors systems with smaller footprints and enhanced safety profiles. Device makers also emphasize training modules that allow staff to manage complex cases in lower-acuity settings. These shifts amplify procurement of energy devices, smart staplers, and AI-guided visualization tools tailored for higher-risk elderly patients.

Increasing Adoption of Minimally Invasive and Robotic-Assisted Procedures

Robotic hernia repairs, colon resections, and knee arthroplasties now capture rising shares of routine general surgery, with robotic TKAs already representing 13% of total knee replacements from 2018 to 2023. Hospitals leverage robotics to attract surgeons and boost OR throughput, offsetting capital costs through higher case volumes. As a result, the United States general surgical devices market sees growing orders for single-console systems, reusable end effectors, and cloud-linked analytics packages. Smaller facilities prioritize cost-efficient laparoscopic kits, creating a two-tier adoption curve that vendors address with modular pricing strategies.

ASC Expansion Driving Device Uptake

ASC procedure volumes are forecast to climb 22% by 2033, reshaping specifications toward disposable, standardized instruments. Because payers reimburse ASCs at attractive rates, administrators insist on devices that shorten turnover time and eliminate reprocessing cost. This preference encourages suppliers to develop pre-sterilized electrosurgical handpieces and self-contained wound-closure systems. The United States general surgical devices market therefore rewards manufacturers that bundle procedural kits and guarantee predictable per-case economics.

Integration of AI-Guided Imaging & Navigation Boosting Procedural Efficiency

More than 950 AI/ML devices have obtained FDA authorization to date[2]Source: AdvaMed, “The Role of Artificial Intelligence in Healthcare,” advamed.org . Tools such as Olympus’s cloud-based colonoscopy platform elevate adenoma detection while reducing operator variability. Hospitals adopt these solutions to counter staff shortages and meet value-based outcome targets. Data generated during procedures feed predictive analytics that hospitals use to refine care pathways. Consequently, AI capability has become a core differentiator in the United States general surgical devices market, influencing purchasing decisions alongside traditional performance metrics.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Escalating cost-containment & value-based reimbursement pressure on device pricing Escalating cost-containment & value-based reimbursement pressure on device pricing | -0.9% | National, acute in Medicare markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.9% | Geographic Relevance:National, acute in Medicare markets | Impact Timeline:Short term (≤ 2 years) |

Stringent FDA scrutiny and recall risk prolonging product launch timelines Stringent FDA scrutiny and recall risk prolonging product launch timelines | -0.8% | National, concentrated among Class II/III devices | Medium term (2-4 years) | |||

Supply-chain vulnerabilities & raw-material inflation elevating production costs Supply-chain vulnerabilities & raw-material inflation elevating production costs | -0.7% | National, acute for semiconductor-dependent devices | Short term (≤ 2 years) | |||

Shortage of skilled surgical workforce slowing adoption of advanced systems Shortage of skilled surgical workforce slowing adoption of advanced systems | -0.5% | Regional, concentrated in rural and underserved areas | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Escalating Cost-Containment & Value-Based Reimbursement Pressure on Device Pricing

Value analysis committees now emphasize total cost of ownership, with 32% of hospitals ranking evidence-based purchasing as their top priority. Bulk-buying intermediaries negotiate transparent contract prices that compress margins for high-end platforms. Device makers therefore bundle service agreements and offer outcome-based guarantees to defend premium positioning. Over time these pressures encourage lean product design and intensified competition inside the United States general surgical devices market.

Shortage of Skilled Surgical Workforce Slowing Adoption of Advanced Systems

Perioperative nursing vacancies reached 18% in 2024, limiting the pace at which hospitals deploy sophisticated robotics. Vendors respond by simplifying user interfaces and embedding decision support that lowers the training burden. AI-driven setup wizards, remote proctoring, and standardized procedural kits help mitigate staffing gaps. Yet persistent labor shortages particularly in rural areas temper the otherwise strong momentum of the United States general surgical devices market.

Segment Analysis

By Product: Electrosurgical Innovation Drives Energy Platform Evolution

Electrosurgical devices are projected to post an 8.09% CAGR, the fastest among product lines, reflecting sustained demand for AI-optimized tissue interaction systems. Laparoscopic instruments still account for 26.12% of the United States general surgical devices market size in 2025. Hospitals upgrade to advanced generators that reduce thermal spread, aligning with safety imperatives and cost-controlled ASC workflows. Research in Annals of Surgery shows new energy modalities lowering collateral damage without compromising hemostasis.

Handheld devices retain relevance because of standardized designs and lower price points, while zipper-based closure tools shorten closure time by 298 seconds compared with sutures. Access device quality lapses, evidenced by the 2024 recall of 165,356 units of blunt-tip trocars, underscore the value of robust manufacturing controls. Breakthrough designations, such as Absolutions’ abdominal wall closure system, further widen innovation pipelines. As a result, the United States general surgical devices market channels R&D toward versatile energy platforms and safer access solutions that cater to both inpatient and outpatient settings.

Note: Segment shares of all individual segments available upon report purchase

By Procedure Approach: Minimally Invasive Dominance Accelerates Robotic Integration

Minimally invasive techniques commanded 68.64% share of the United States general surgical devices market in 2025 and are on course for a 7.03% CAGR to 2031. Robotic platforms intensify this lead by expanding into complex abdominal and orthopedic repairs, creating an ecosystem of reusable instruments, vision towers, and cloud analytics packages. Value in Health data indicate that robotic usage is increasing across nearly all specialties.

Open surgery remains essential for multilevel reconstructions yet cedes unit volume as laparoscopic and robotic suites penetrate smaller hospitals. To stay relevant, open-approach suppliers introduce advanced headlights, high-definition visualization, and AI-assisted hemostasis technologies. In combination, these shifts reinforce patient expectations for smaller scars and quicker returns to routine life, sustaining momentum behind the United States general surgical devices market.

By Application: Gynecology and Urology Lead Growth Through Breakthrough Innovation

Orthopedics controlled 22.05% of the United States general surgical devices market size in 2025, but gynecology and urology lead growth with a 7.66% CAGR to 2031. FDA clearance for Olympus’s iTind device together with two new Category I CPT codes takes effect in 2025, providing predictable reimbursement for minimally invasive BPH therapy. Cardiology gains traction due to the 74.4% success rate achieved by Boston Scientific’s VARIPULSE system in preventing AF recurrence.

Neurology procedures also benefit from miniaturized stimulators that extend battery life while facilitating outpatient implantation. Niche applications such as bariatric robotics enter mainstream pathways, broadening adjacency opportunities within the United States general surgical devices market. Collectively, diverse specialty advances establish a balanced revenue mix that cushions cyclical swings in any single segment.

Note: Segment shares of all individual segments available upon report purchase

By End User: ASC Growth Transforms Procurement Dynamics

Hospitals represented 67.98% of the United States general surgical devices market in 2025, leveraging integrated supply chains and multi-specialty coverage. Yet ASCs expand fastest at 7.9% CAGR thanks to payer support and patient preference for same-day discharge. The Health Industry Distributors Association projects ASC volumes to rise markedly in orthopedics, spine, and GI. Specialty clinics concentrate on high-margin niches, using focused expertise to negotiate advantageous device contracts.

Manufacturers now tailor offerings by care setting: capital-intense robotic suites for tertiary hospitals, portable tower-less scopes for ASCs, and procedure-specific kits for micro-clinics. These differentiated strategies preserve margin opportunities while ensuring broad coverage across the United States general surgical devices market.

Geography Analysis

Large metropolitan regions anchor adoption curves because academic centers there pilot robotics, AI navigation, and digital workflow integration. California health systems align with local technology talent, hastening the early deployment of cloud-based surgical analytics. Further south, Sunbelt states, including Texas, Florida, and Arizona, combine inbound retiree migration with extensive ASC construction, yielding a substantial contribution to the United States general surgical devices market growth. Population aging in these areas boosts orthopedics and urology volumes, stimulating demand for single-use energy instruments.

Rural and underserved zones face equipment scarcity and workforce constraints, yet increasingly employ tele-mentoring and mobile OR programs that transport surgical capability. These initiatives open incremental channels for cost-efficient laparoscopic sets and battery-operated power tools. The Midwest maintains a balanced footprint, with integrated delivery networks standardizing procurement across both urban hubs and smaller affiliates. East Coast teaching hospitals drive high-complexity innovation, welcoming early-release robotics and AI platforms under controlled evaluation protocols. Vendor commercial teams therefore segment their go-to-market tactics: direct specialist consultative selling in coastal academic centers, distributor-led inventory programs in interior states, and service-center partnerships in ASC-dense suburbs. The resulting mosaic magnifies the competitive intensity yet also diversifies revenue, supporting resilience across the United States general surgical devices market.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

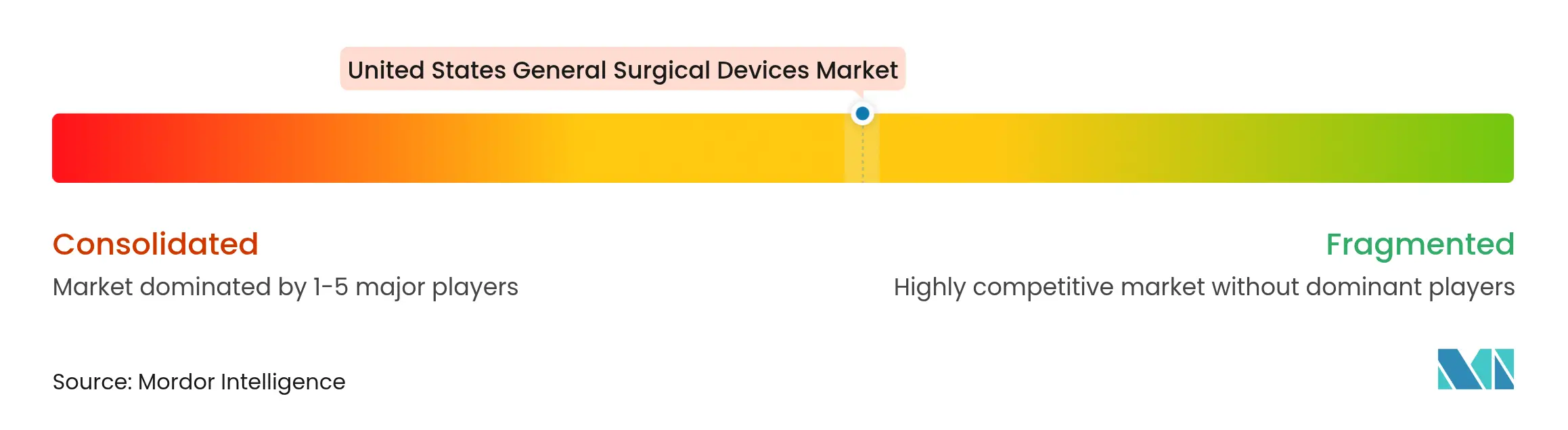

Market Concentration

The United States general surgical devices market exhibits moderate concentration, with Medtronic, Johnson & Johnson, and Stryker anchoring share positions through broad portfolios and sizable sales forces. Medtronic reported USD 2.128 billion in Medical Surgical Portfolio revenue for Q2 FY 2025, then purchased Fortimedix to augment articulating instruments. Johnson & Johnson continues an active M&A agenda to secure catheter-based technologies while broadening cardiovascular exposure, illustrating the shift toward platform ecosystems.

Smaller innovators secure FDA breakthrough designations that fast-track commercialization and make them attractive acquisition targets. Strategic alliances, such as Stryker’s distributor pacts with ASC chains, signal the importance of channel specificity. Meanwhile, Olympus focuses on AI software wrapped around capital equipment to defend pricing and open data-driven service revenue. Competitive differentiation increasingly turns on proof of outcome improvement and integration capability rather than mechanical sophistication alone, reshaping investment priorities across the United States general surgical devices market.

Barriers remain high due to stringent FDA processes and the need for surgeon education, yet digital health entrants lower entry hurdles by offering software layers that bolt onto existing hardware. This overlapping competition pushes incumbents to refresh value propositions and explore subscription models. The resulting landscape blends scale economies with nimble innovation, fostering steady but contested expansion.

United States General Surgical Devices Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: JUNE MEDICAL partnered with Aspen Surgical to distribute the Galaxy II retractor system in the United States.

- August 2024: CooperSurgical acquired obp Surgical, broadening its portfolio in lighting and single-use devices.

- May 2024: Stereotaxis purchased APT to enhance its robotic catheter offerings.

Table of Contents for United States General Surgical Devices Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Aging Population & Rising Chronic Disease Burden Driving Surgical Demand

- 4.2.2Increasing Adoption of Minimally-Invasive and Robotic-Assisted Procedures

- 4.2.3ASC (Ambulatory Surgical Center) Expansion Driving Device Uptake

- 4.2.4Rapid Technology Advancements

- 4.2.5Integration of AI-Guided Imaging & Navigation Boosting Procedural Efficiency

- 4.2.6Federal Incentives for Domestic Manufacturing Reshaping Device Supply Chains

- 4.3Market Restraints

- 4.3.1Escalating Cost-Containment & Value-Based Reimbursement Pressure on Device pricing

- 4.3.2Stringent FDA Scrutiny and Recall Risk Prolonging Product Launch Timelines

- 4.3.3Supply-Chain Vulnerabilities & Raw-Material Inflation Elevating Production Costs

- 4.3.4Shortage of Skilled Surgical Workforce Slowing Adoption of Advanced Systems

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porter’s Five Forces Analysis

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitutes

- 4.6.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product

- 5.1.1Handheld Devices

- 5.1.2Laparoscopic Devices

- 5.1.3Electrosurgical Devices

- 5.1.4Wound Closure Devices

- 5.1.5Trocars and Access Devices

- 5.1.6Other Products

- 5.2By Procedure Approach

- 5.2.1Open Surgery

- 5.2.2Minimally Invasive Surgery

- 5.3By Application

- 5.3.1Gynecology and Urology

- 5.3.2Cardiology

- 5.3.3Orthopedic

- 5.3.4Neurology

- 5.3.5Other Applications

- 5.4By End User

- 5.4.1Hospitals

- 5.4.2Ambulatory Surgical Centres

- 5.4.3Specialty Clinics

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Medtronic plc

- 6.3.2Johnson & Johnson (Ethicon & DePuy)

- 6.3.3Stryker Corporation

- 6.3.4Boston Scientific Corporation

- 6.3.5B. Braun SE

- 6.3.6Olympus Corporation

- 6.3.7Conmed Corporation

- 6.3.8Applied Medical Resources Corp.

- 6.3.9Getinge AB

- 6.3.10Zimmer Biomet Holdings Inc.

- 6.3.11Smith & Nephew plc

- 6.3.12Intuitive Surgical Inc.

- 6.3.13Teleflex Incorporated

- 6.3.14Cook Medical LLC

- 6.3.15Karl Storz SE & Co. KG

- 6.3.16CooperSurgical Inc.

- 6.3.17Arthrex Inc.

- 6.3.18Becton, Dickinson and Company

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Segmentation Overview

- By Product

- Handheld Devices

- Laparoscopic Devices

- Electrosurgical Devices

- Wound Closure Devices

- Trocars and Access Devices

- Other Products

- Handheld Devices

- By Procedure Approach

- Open Surgery

- Minimally Invasive Surgery

- Open Surgery

- By Application

- Gynecology and Urology

- Cardiology

- Orthopedic

- Neurology

- Other Applications

- Gynecology and Urology

- By End User

- Hospitals

- Ambulatory Surgical Centres

- Specialty Clinics

- Hospitals

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Mordor's US General Surgical Devices Baseline Earns Decision-Makers' Trust

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 6.69 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 6.17 B (2025) | Regional Consultancy A | Excludes laparoscopic access ancillaries; applies flat ASP from 2022 forward | ||

USD 4.32 B (2024) | Global Consultancy B | Uses hospital billings, not device shipments; conservative uptake for ambulatory settings |