Professional Visualization GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

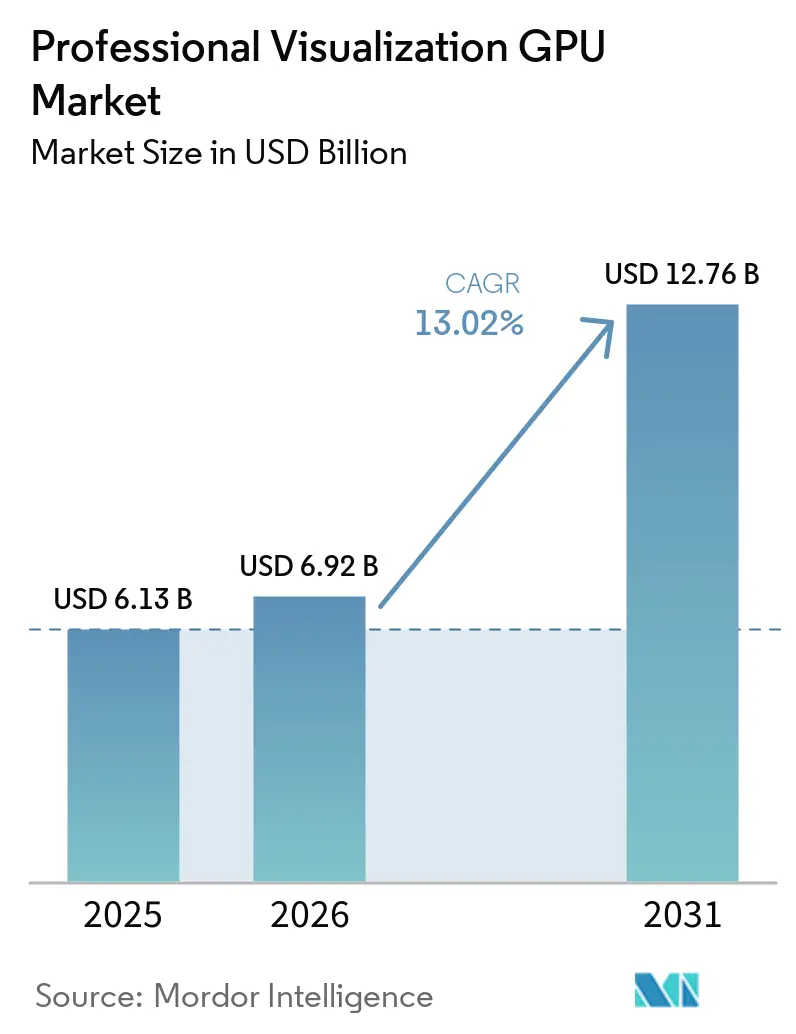

| Market Size (2026) | USD 6.92 Billion |

| Market Size (2031) | USD 12.76 Billion |

| Growth Rate (2026 - 2031) | 13.02% CAGR |

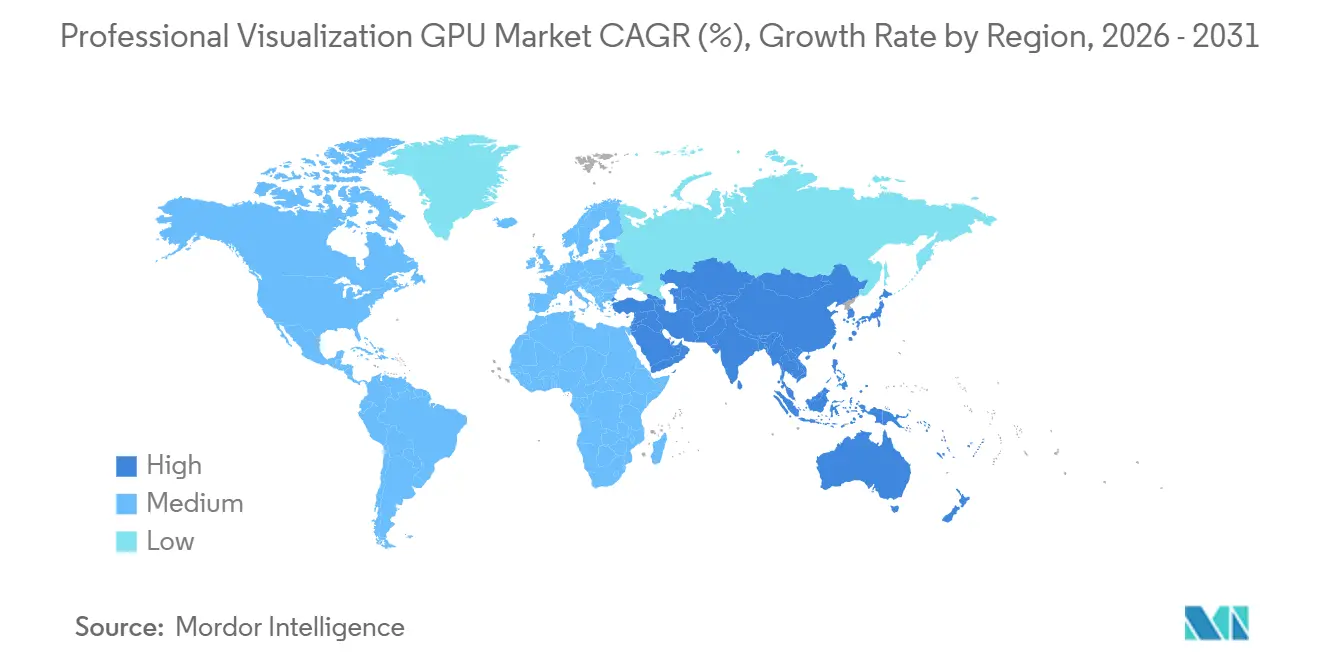

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Professional Visualization GPU Market Analysis by Mordor Intelligence

The professional visualization GPU market size was valued at USD 6.13 billion in 2025 and is forecast to reach USD 12.76 billion by 2031, advancing at a CAGR of 13.02% over the 2026-2031 period. Growth is being shaped by the shift from traditional workstation demand toward AI-ready systems that can run simulation, generative design, and real-time visualization in the same environment. As AI tools move from pilot use into daily production, buyers are placing greater weight on local inference capabilities, memory capacity, and software certification when refreshing workstation fleets. Demand is also widening beyond long-established design teams, because telecom, healthcare, media, and industrial users now rely on visual computing for digital twins, model validation, and faster content workflows. Vendors are responding through broader product ladders, closer enterprise engagement, and stronger certified software support, which helps them defend pricing and secure larger refresh programs. At the same time, supply competition with data center AI hardware and continued preference for on-premises control in regulated settings are keeping availability and deployment choice central to purchasing decisions.

Key Report Takeaways

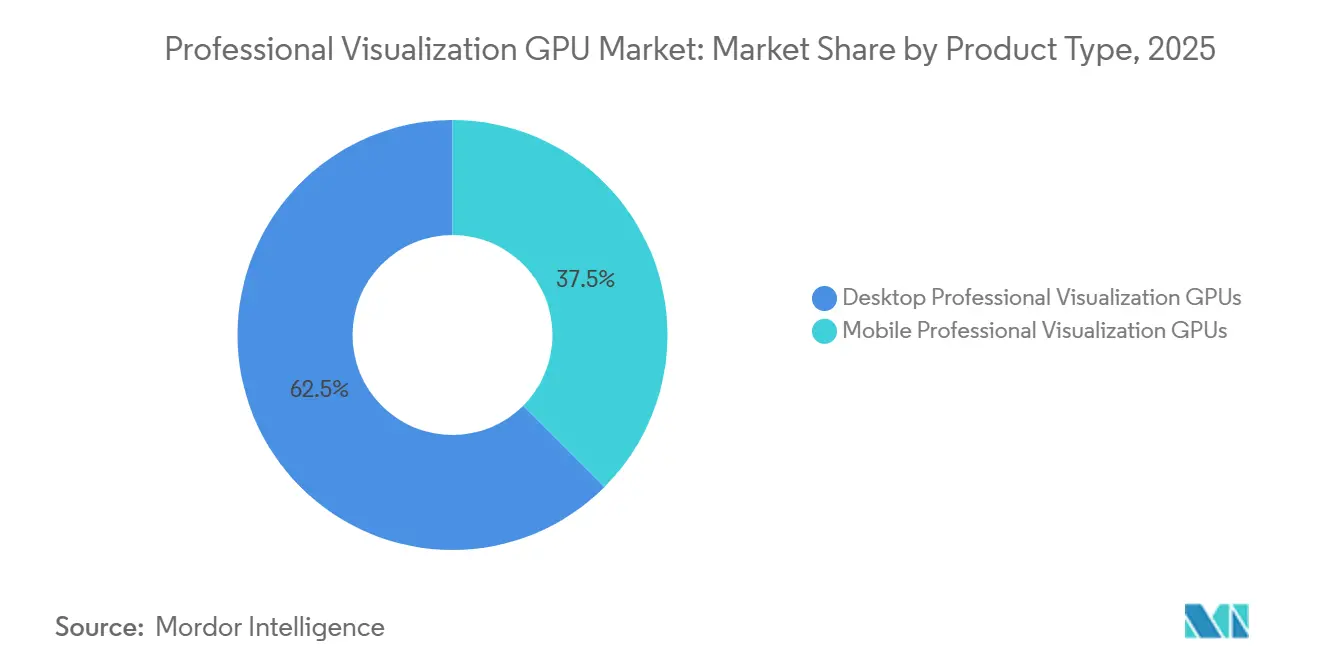

- By product type, desktop professional visualization GPUs held 62.49% of the professional visualization GPU market share in 2025, while mobile professional visualization GPUs are projected to expand at a 14.23% CAGR through 2031.

- By deployment model, on-premises virtual workstations held 53.14% share in 2025, while cloud-hosted virtual workstations are expected to grow at a 13.72% CAGR through 2031.

- By organization size, large enterprises accounted for 69.53% of the market share in 2025, while small and medium enterprises are projected to grow CAGR of 13.68% through 2031.

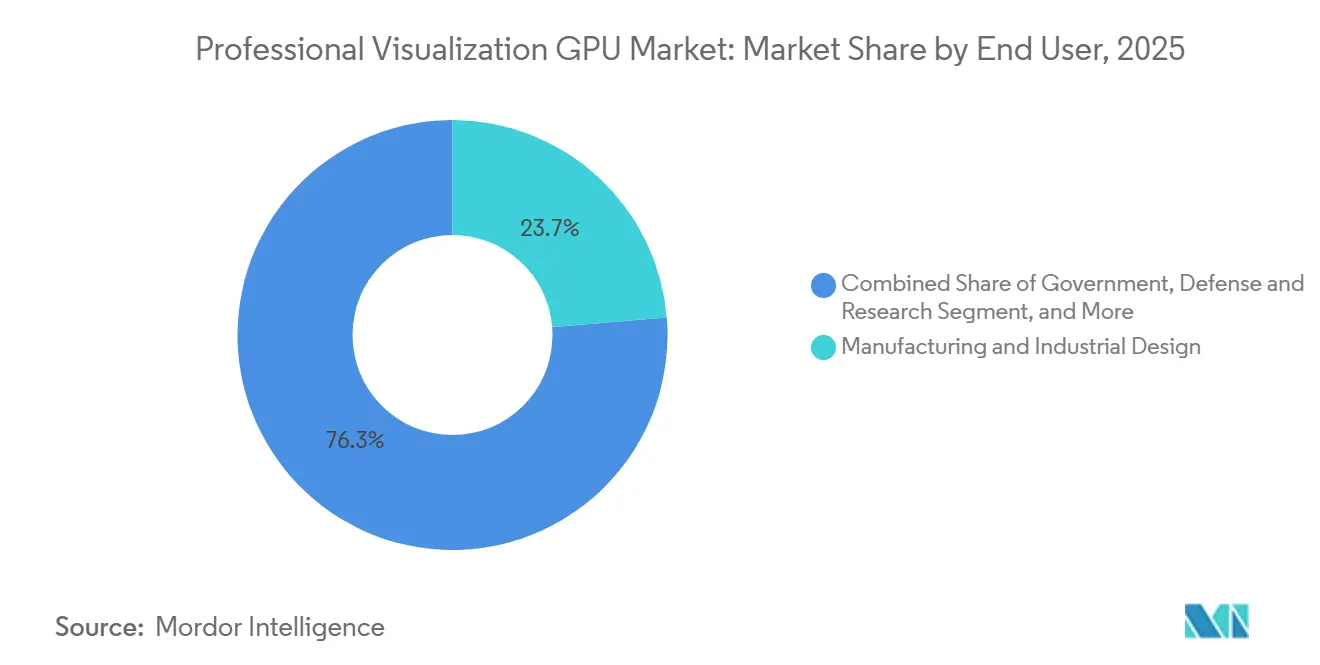

- By end user, manufacturing and industrial design captured 23.71% of the professional visualization GPU market in 2025, while IT and Telecom are forecast to advance at a 14.32% CAGR through 2031.

- By distribution channel, OEM and system integrator sales led with 36.53% share in 2025, while direct enterprise sales are projected to grow at a 13.95% CAGR through 2031.

- By geography, Asia-Pacific held 36.53% of the professional visualization GPU market in 2025, while Asia-Pacific are projected to grow a 13.37% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Professional Visualization GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of AI-Ready Workstations in Design and Simulation Workflows | +3.8% | Global, concentrated in North America and the Asia-Pacific | Short term (≤ 2 years) |

| Expansion of Remote and Hybrid Professional Visualization Workflows | +2.4% | Global, strongest in Europe and Asia-Pacific | Medium term (2-4 years) |

| Refresh Cycle From Legacy Workstations to AI-Enabled Professional PCs | +2.1% | North America and Europe primarily | Medium term (2-4 years) |

| Growing Demand for Certified Drivers and ISV-Validated Graphics Performance | +1.4% | Global | Long term (≥ 4 years) |

| Localized Data Control and On-Premise Rendering Preferences in Regulated Industries | +1.2% | Europe and APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Edge Rendering for Digital Twin, VFX, and Industrial Visualization Pipelines | +1.0% | Global, industrial hubs in Germany, Japan, and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of AI-Ready Workstations in Design and Simulation Workflows

Demand in the professional visualization GPU market is now tied closely to workstation-level AI inference across engineering, architecture, simulation, and media production teams. SimScale reported that AI-enabled engineering teams complete simulation requests in 6 hours on average, versus 17 hours with conventional workflows, and they test more than 3 times as many design variants per program. That gap is changing hardware buying behavior, because faster iteration increases the value of memory bandwidth, tensor capability, and stable software support during live project work. NVIDIA positioned its RTX PRO Blackwell series for this shift, with up to 4,000 AI TFLOPS through fifth-generation Tensor Cores and FP4 support for heavier workstation AI tasks. As design platforms place generative functions and simulation assistance directly inside core tools, rendering speed alone no longer defines workstation value. This is raising the strategic importance of professional GPUs that can support both visual computing and local AI acceleration without forcing users into separate hardware environments.

Expansion of Remote and Hybrid Professional Visualization Workflows

Remote and hybrid teams are providing a second demand channel for professional GPU visualization through virtual workstations and shared GPU environments. AWS introduced WorkSpaces G6, Gr6, and G6f bundles with NVIDIA L4 Tensor Core GPUs and 24GB VRAM, giving engineering and 3D users a higher-capacity cloud option than the earlier G4dn generation.[1]Amazon Web Services, “Amazon WorkSpaces Launches Graphics G6, Gr6, and G6f Bundles,” AWS Desktop and Application Streaming Blog, aws.amazon.com In practice, many regulated users are not replacing local workstations but are adding cloud capacity for overflow rendering, collaborative review, and remote access. NVIDIA supports that pattern with Multi-Instance GPU on the RTX PRO 6000 Blackwell, which allows up to 4 isolated GPU instances per card in mixed environments. This hybrid setup keeps high-value local hardware in place while extending professional access across distributed teams and external review cycles. It also supports average selling price growth, as enterprises still need robust anchor systems even as part of the workload shifts to virtual infrastructure.

Refresh Cycle from Legacy Workstations To AI-Enabled Professional PCs

The installed base of pre-AI workstations remains one of the clearest demand pools in the professional visualization GPU market. Autodesk’s 2026 AI Pulse findings showed that 84% of leaders said AI had already improved productivity in their organizations, increasing pressure to replace hardware that cannot support AI-enabled design tools effectively. The refresh case becomes stronger when older systems cannot support modern driver branches, stable large-assembly work, or certified graphics functions that matter in production settings. Lenovo introduced the ThinkStation P4 in May 2026 with AMD Ryzen PRO 9000 Series processors and NVIDIA RTX PRO 6000 Blackwell workstation GPUs, aimed directly at engineers, architects, and creators upgrading for AI-intensive design tasks. As performance gaps widen between older cards and current platforms, procurement cycles are moving closer to functional need rather than solely to age-based replacement. That shift is helping workstation refresh demand become more immediate, especially where AI tools are already part of approved business workflows.

Growing Demand for Certified Drivers and ISV-Validated Graphics Performance

Certified software performance remains a durable buying criterion in the professional visualization GPU market, especially where output quality and system stability affect billable work. SPEC released the SPECapc for SolidWorks 2025 benchmark in January 2026, with 60 tests that cover graphics and CPU behavior in professional engineering workloads. That benchmark reflects how enterprises increasingly want proof that a workstation configuration has been validated across the exact tools their teams use. NVIDIA still holds the broadest certification position across Autodesk, Dassault Systèmes, PTC, and Siemens environments, while AMD has used ISV validation around its Radeon AI PRO line to narrow earlier coverage gaps. Broader certification coverage lowers support risk for IT teams and makes multi-software deployments easier to standardize across sites and user groups. This keeps certified driver ecosystems central to competition, because reliability and support traceability often carry as much weight as pure hardware performance in enterprise workstation decisions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership for Professional-Grade GPUs and Workstations | -1.8% | Global, most acute for SMBs and emerging markets | Short term (≤ 2 years) |

| Supply Allocation Pressure from Consumer Gaming and Data Center Demand | -1.4% | Global | Medium term (2-4 years) |

| Fragmented Software Certification Requirements Across Applications and Geographies | -0.6% | Global | Long term (≥ 4 years) |

| Underutilization Risk in SMB Deployments with Intermittent Workloads | -0.5% | Global, SMB-focused markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership for Professional-Grade GPUs and Workstations

High ownership costs still limit how quickly the professional visualization GPU market can expand beyond large enterprise budgets. Buyers are paying for more than the card itself because certified chassis, ECC memory, software support, and validation requirements all raise total deployment cost. Flagship systems with multiple top-tier workstation GPUs also require formal capital planning, which slows decisions in smaller studios and cost-sensitive business units. Systems such as HP’s Z8 Fury G6i, which support up to 4 RTX PRO 6000 Blackwell Max-Q units, show how quickly total platform cost rises in advanced workstation deployments. This burden is strongest for smaller firms that need professional reliability but cannot spread hardware cost across large seat counts. Cloud workstation subscriptions ease upfront spending for some users, but latency still limits their fit for interactive 3D sessions that require consistent local responsiveness.

Supply Allocation Pressure from Consumer Gaming and Data Center Demand

Supply allocation remains a practical constraint for the professional visualization GPU market because workstation cards compete with data center AI accelerators and gaming products for advanced manufacturing capacity. The same supply chain that supports workstation memory and advanced GPU production is also serving stronger demand from hyperscale AI infrastructure, which tightens availability for professional systems. This creates uneven lead times and makes allocation more difficult for add-in board partners and regional distributors with less bargaining power than large OEMs. When availability becomes uncertain, some buyers delay preferred configurations or route part of the workload to cloud resources instead of refreshing local hardware immediately. That response can weaken physical workstation conversion even when the underlying need remains strong. The result is a mid-term availability risk that can affect vendor reputation in a segment where buyers expect predictable delivery on premium hardware.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mobile Professional GPUs Gain AI Certification Parity

Desktop professional visualization GPUs accounted for 62.49% of the professional visualization GPU market in 2025, keeping fixed workstations in the lead position across the product mix. Their strength comes from higher VRAM capacity, better sustained thermal performance, and early access to certification on new architectures, all of which matter in demanding production environments. They remain the preferred choice when rendering throughput, simulation stability, and long-session reliability are more valuable than portability. NVIDIA’s RTX PRO 6000 Blackwell Workstation Edition has become a reference point in 2026, with 96GB GDDR7 ECC memory and support for up to 4 Multi-Instance GPU partitions. This keeps desktop systems closely tied to large engineering teams, advanced content pipelines, and institutional workstation refresh programs.

Mobile professional visualization GPUs are forecast to grow at a 14.23% CAGR through 2031, making them the fastest-growing segment within the product type. That shift reflects the closing capability gap between mobile and desktop systems across Autodesk, SolidWorks, and Siemens NX workflows. NVIDIA’s RTX PRO Blackwell laptop range, from the PRO 500 to the PRO 5000, extends certified professional performance to field engineers and distributed creative teams who need workstation output away from fixed desks. Mobility is becoming more valuable because hybrid collaboration, site visits, and live client review cycles now sit closer to daily production than they did before. As AI-first workflows become standard, buyers are also placing more value on notebook systems that can run certified visual tools and local AI functions without defaulting to consumer gaming devices.

By Deployment Model: On-Premises Deployments Anchor Cloud Hybrid Growth

On-premises virtual workstations held 53.14% of revenue in 2025, which gave them the leading position within the deployment model sewgment of the professional visualization GPU market. Local control remains important in life sciences, defense, and industrial automation, where data-handling rules and latency requirements still favor in-house systems. These settings depend on a predictable response in interactive 3D sessions, which is harder to guarantee when critical workloads sit fully offsite. They also favor workstation environments where administrators can manage drivers, access rules, and hardware utilization directly. For that reason, the professional GPU visualization market still treats physical or locally managed GPU infrastructure as the anchor for sensitive visual computing workloads.

Cloud-hosted virtual workstations are projected to grow at a 13.72% CAGR through 2031, making them the fastest-growing deployment option. AWS has expanded enterprise access to graphics workstations with G6, Gr6, and G6f bundles powered by NVIDIA L4 GPUs and 24GB of VRAM. NVIDIA’s vGPU stack and Multi-Instance GPU support on the RTX PRO 6000 Blackwell Server Edition enable a single server card to support multiple isolated sessions in shared environments.[2]NVIDIA Corporation, “NVIDIA Blackwell RTX PRO Comes to Workstations and Servers for Designers, Developers, Data Scientists and Creatives to Build and Collaborate with Agentic AI,” NVIDIA Investor Relations, investor.nvidia.com The emerging pattern is hybrid, with organizations keeping sensitive design work local and routing bursty simulation, model tuning, and collaboration sessions to the cloud. This approach reduces the need for one-for-one workstation ownership while preserving the performance, governance, and responsiveness required in regulated or latency-sensitive workflows.

By Organization Size: SMEs Accelerate Via AI-Optimized Entry Cards and Cloud Access

Large enterprises held 69.53% of the professional visualization GPU market share in 2025, supported by centralized procurement, standard workstation policies, and synchronized refresh cycles. Their buying programs usually move through bulk OEM contracts, software support agreements, and approved hardware stacks tied to core design and engineering tools. This structure gives vendors dependable volume and helps keep higher-end professional configurations in active demand across global fleets. It also favors suppliers that can provide certified deployments, long support windows, and consistent configuration management across distributed teams. As a result, large accounts remain the base that stabilizes pricing and shipment planning across the professional visualization GPU market.

SMEs are forecast to grow at a 13.68% CAGR through 2031, making them the fastest-growing organization-size segment. This demand is being opened by lower entry points in professional hardware and by wider access to cloud-based GPU capacity for intermittent workloads. AMD has used its Radeon AI PRO portfolio to target AI-first professionals with workstation-class graphics options that address cost-sensitive buyers more directly. NVIDIA has also widened its desktop range with lower tiers in the RTX PRO Blackwell family, which gives smaller buyers certified options without the full cost of flagship memory configurations. Cloud access adds another route for firms that cannot commit to large upfront purchases, but local cards still matter where steady daily performance is operationally required.

By End User: IT And Telecom Surpasses Traditional Verticals in Growth Momentum

Manufacturing and Industrial Design accounted for 23.71% of the professional visualization GPU market in 2025, making it the largest end-user segment. Demand in this segment stays tied to automotive CAD, factory layout visualization, finite element simulation, and generative manufacturing design workflows. In many of these settings, professional GPU choices are closely tied to audited production software and the reliability of long simulation runs. That keeps the segment structurally important even as newer workload categories enter the addressable base. It also explains why workstation-grade stability still matters as much as raw rendering speed in the professional visualization GPU industry.

IT and telecom are projected to record the fastest end-user CAGR at 14.32% through 2031. Growth is driven by network infrastructure simulation, AI inference pipeline visualization, and the use of telecom digital twins in 5G planning and optimization. This widens demand beyond traditional design departments and creates new buying centers inside infrastructure, platform, and operations teams. The shift is notable because it brings the professional visualization GPU market into workflow environments that were not historic demand anchors for workstation graphics. Energy and Utilities, Government, Defense and Research, Healthcare and Life Sciences, Architecture, Engineering, and Construction, and Media and Entertainment also broaden the end-user base, which makes revenue less exposed to a slowdown in any single vertical.

By Distribution Channel: Direct Enterprise Sales Fastest Growing as Supply Dynamics Shift

OEM and system integrator sales led with 36.53% share of the professional visualization GPU market in 2025, reflecting the continued strength of bundled workstation procurement in enterprise environments. Buyers still prefer complete systems from vendors such as Dell Technologies, HP Inc., Lenovo, and BOXX Technologies because certification, service, and support are packaged together. That model simplifies fleet management for organizations that need consistent workstation configurations across many users and project sites. It is also useful when customers want a single accountable vendor for hardware integration, driver support, and after-sales service. This channel structure keeps major workstation providers in a strong position across the professional visualization GPU industry.

Direct enterprise sales are forecast to grow at a 13.95% CAGR through 2031, making them the fastest channel in the study. The shift reflects enterprise demand for allocation priority, closer configuration control, and direct vendor-managed support. HP introduced Z Boost in 2026 to share GPU resources across Catia, Siemens NX, and Blender workflows, enabling managed deployment at the workstation fleet level. As supply tightens, direct vendor relationships are becoming more valuable for buyers who want predictable delivery, support traceability, and better alignment between platform design and workload needs. This raises the strategic importance of account-level relationships, especially for organizations that treat workstation GPUs as critical infrastructure rather than discretionary hardware.

Geography Analysis

Asia-Pacific held 36.53% of the professional visualization GPU market share in 2025 and is projected to expand at 13.37% CAGR through 2031. The region combines several demand engines, including China’s semiconductor and AI infrastructure push, India’s growing engineering services and media production base, and strong workstation demand from Japanese and South Korean industrial ecosystems. China remains the largest national contributor in the region, supported by demand from content studios, architectural rendering pipelines, and CAD and simulation use cases that require localized product and channel strategies. India is becoming one of the fastest-growing national markets in the region because engineering outsourcing, domestic media production, and AI infrastructure investment are all increasing workstation demand simultaneously. Southeast Asia is also emerging as a supplementary growth center, supported by manufacturing outsourcing, digital content production in Vietnam and Indonesia, and smart infrastructure visualization programs.

North America is expected to hold the second-largest regional share, supported by dense demand from technology firms, defense contractors, engineering consultancies, and entertainment studios that rely on certified professional GPU environments. The region also benefits from being the primary launch center for NVIDIA, AMD, and Intel, which means new architectures, certified drivers, and OEM workstation designs often appear there first. That first-mover position helps the professional visualization GPU market in North America absorb premium products earlier than most other regions. Canada adds demand from energy engineering and mining design workflows, while Mexico contributes through automotive manufacturing expansion and supplier visualization needs. Europe remains important through Germany’s manufacturing base, the United Kingdom’s media and VFX activity, and France’s aerospace and automotive design clusters, while data residency and accountability rules continue to reinforce on-premises deployment choices in regulated environments.

South America and Middle East and Africa remain smaller but strategically distinct contributors to future demand. South America is centered on Brazil’s media production activity, mining visualization in Chile and Peru, and engineering services clusters in São Paulo and Belo Horizonte. The Middle East is seeing stronger uptake through smart city, digital twin, and large-scale urban simulation projects in Saudi Arabia and the UAE, while Africa is expanding from South African media, oil and gas engineering work, and emerging hubs in Kenya and Nigeria. Both regions rely more heavily on distributor and reseller channels than on direct OEM reach, which creates room for competitively priced mid-market workstation offerings.

Competitive Landscape

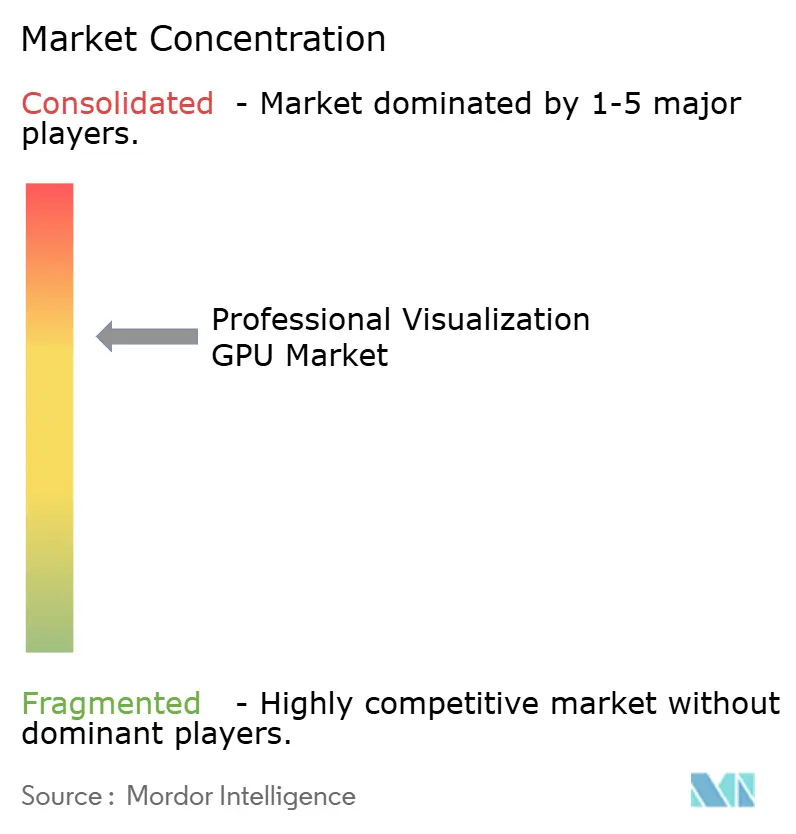

The professional visualization GPU market remains moderately concentrated at the silicon layer, where NVIDIA, AMD, and Intel control the main architecture options. More than 20 add-in board vendors compete on cooling design, local support, certification coverage, and bundle choices across different regional channels. NVIDIA still benefits from the broadest certified application position across Autodesk, Dassault Systèmes, PTC, and Siemens environments, which lowers procurement friction in mixed-software deployments. That breadth of certification gives it an advantage where enterprises value lower support risk and smoother fleet management more than the lowest upfront price. AMD and Intel continue to compete by expanding price tiers and appealing to buyers who do not need the highest AI throughput or the largest memory configurations.

NVIDIA’s March 2025 launch of the RTX PRO Blackwell series raised the technical ceiling with 96GB GDDR7 ECC memory, fifth-generation Tensor Cores, and support for Multi-Instance GPU use cases.[3]NVIDIA Corporation, “NVIDIA Blackwell RTX PRO Comes to Workstations and Servers for Designers, Developers, Data Scientists and Creatives to Build and Collaborate With Agentic AI,” NVIDIA Investor Relations, investor.nvidia.com AMD used Computex 2025 to reframe its workstation position around the Radeon AI PRO brand, shifting the message from graphics alone toward AI-first professional workloads. Lenovo followed in May 2026 with the ThinkStation P4, pairing AMD Ryzen PRO 9000 Series processors with NVIDIA RTX PRO 6000 Blackwell workstation GPUs for mainstream professional buyers. These moves show that leading companies are competing through platform design, AI readiness, and deployment flexibility rather than through graphics benchmarks alone.[4]Lenovo, “Lenovo Announces the ThinkStation P4, a Flagship Combination of Power and Value for Modern Professionals,” Lenovo Newsroom, news.lenovo.com They also show how OEM partnerships remain central to volume capture in the professional visualization GPU market.

Intel’s Arc Pro range continues to build presence where lower thermal demand and lower pricing matter more than top-end AI performance. At the same time, supplier choice at the board and system level stays broad, which prevents the market from appearing consolidated from the buyer’s point of view. Competitive positions are likely to be shaped by supply continuity, certification depth, and the ability to support hybrid workstation models across local and virtual environments. This leaves the professional visualization GPU market concentrated in core architecture control, but still competitive across system assembly, service, and regional execution.

Professional Visualization GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Huawei Technologies Co., Ltd.

Leadtek Research Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA announced the DGX Station for Windows at GTC Taipei on June 1, 2026, integrating 4 NVIDIA B200 Tensor Core GPUs with optional pairing with the RTX PRO 6000 Blackwell Workstation GPU for frontier AI compute alongside ray-traced visualization. The system, capable of running AI models up to 1 trillion parameters locally with up to 748GB of coherent memory and 20 petaflops of FP4 performance, is expected to be available from ASUS, Dell Technologies, GIGABYTE, HP, MSI, and Supermicro in Q4 2026, marking the convergence of supercomputing-class AI and professional visualization within a single deskside platform.

- May 2026: Lenovo announced the ThinkStation P4 on May 13, 2026, the first desktop workstation pairing AMD Ryzen PRO 9000 Series processors with NVIDIA RTX PRO 6000 Blackwell Workstation Edition GPUs, with 96GB GDDR7 ECC and up to 4,000 AI TOPS, with global availability from June 2026. Positioned as a mainstream-accessible AI workstation for engineers, architects, and designers tackling simulation, CAD, BIM, and rendering workflows, the platform represents the AI workstation refresh cycle pulling professional GPU demand into a broader buyer segment beyond top-tier enterprise accounts.

- March 2026: HP Inc. unveiled the Z8 Fury G6i at HP Imagine 2026 on March 24, 2026, a high-performance desktop workstation supporting up to 4 NVIDIA RTX PRO 6000 Blackwell Max-Q Workstation Edition GPUs alongside next-generation Intel processors, targeting advanced AI development, VFX, and simulation workloads. HP simultaneously introduced Z Boost GPU-sharing software extended to Catia, Siemens NX, and Blender, enabling professional GPU resources to be shared across multiple workstation users in team environments, a deployment model that improves capital efficiency for large visualization studios.

- March 2026: Moore Threads Intelligent Technology secured a CNY 660 million (USD 91 million) contract to supply its KUAE intelligent computing cluster, marking a strategic shift from standalone GPU sales to integrated AI cluster infrastructure and demonstrating the financial scale at which Chinese domestic GPU vendors are now competing for institutional orders.

Global Professional Visualization GPU Market Report Scope

The Professional Visualization GPU Market covers graphics processing units designed for professional applications that require high-performance rendering, visualization, simulation, and computation. These GPUs support use cases across industries such as media and entertainment, architecture, engineering and construction, manufacturing, healthcare, and scientific research, where advanced graphics performance, precision, and reliability are essential.

The Professional Visualization GPU Market is Segmented by Product Type (Desktop Professional Visualization GPUs, and Mobile Professional Visualization GPUs), Deployment (On-Premises Virtual Workstations, Cloud-hosted Virtual Workstations, and Hybrid Deployments), Organization Size (Large Enterprises, and Small and Medium Enterprises), End User (Manufacturing and Industrial Design, Architecture, Engineering, and Construction, Media and Entertainment, Healthcare and Life Sciences, Energy and Utilities, Government, Defense and Research, IT and Telecom, and Other End User Industries), Channel (Direct Enterprise Sales, OEM/System Integrator Sales, and Distributor/Reseller Sales), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Desktop Professional Visualization GPUs |

| Mobile Professional Visualization GPUs |

| On-Premises Virtual Workstations |

| Cloud-hosted Virtual Workstations |

| Hybrid Deployments |

| Large Enterprises |

| Small and Medium Enterprises |

| Manufacturing and Industrial Design |

| Architecture, Engineering, and Construction |

| Media and Entertainment |

| Healthcare and Life Sciences |

| Energy and Utilities |

| Government, Defense and Research |

| IT and Telecom |

| Other End Users |

| Direct Enterprise Sales |

| OEM/System Integrator Sales |

| Distributor/Reseller Sales |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Product Type | Desktop Professional Visualization GPUs | |

| Mobile Professional Visualization GPUs | ||

| By Deployment Model | On-Premises Virtual Workstations | |

| Cloud-hosted Virtual Workstations | ||

| Hybrid Deployments | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By End User | Manufacturing and Industrial Design | |

| Architecture, Engineering, and Construction | ||

| Media and Entertainment | ||

| Healthcare and Life Sciences | ||

| Energy and Utilities | ||

| Government, Defense and Research | ||

| IT and Telecom | ||

| Other End Users | ||

| By Distribution Channel | Direct Enterprise Sales | |

| OEM/System Integrator Sales | ||

| Distributor/Reseller Sales | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the professional visualization GPU market size and growth outlook?

The professional visualization GPU market was valued at USD 6.13 billion in 2025 and is forecast to reach USD 12.76 billion by 2031 at a 13.02% CAGR over 2026-2031.

Which product type drives professional GPU visualization demand?

Desktop professional visualization GPUs led with 62.49% share in 2025, while mobile professional visualization GPUs are expected to grow faster at a 14.23% CAGR through 2031.

Why are AI-ready workstations becoming central to workstation refresh decisions?

AI-enabled engineering teams completed simulation requests in 6 hours on average versus 17 hours with conventional workflows, which is increasing the need for newer GPU systems.

Which end-user group is expanding the fastest?

IT and Telecom is projected to record the highest CAGR at 14.32% through 2031, driven by network simulation, AI inference visualization, and telecom digital twin deployments.

Which region is strongest in professional visualization GPU adoption?

Asia-Pacific held 36.53% share in 2025 and is forecast to grow at 13.37% CAGR through 2031, supported by China, India, Japan, South Korea, and Southeast Asia.

What factors matter most in vendor competition?

Certification breadth, supply continuity, AI capability, and OEM partnerships are shaping competition, while NVIDIA, AMD, and Intel remain the core architecture suppliers.

Page last updated on: