GPU Programming Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.86 Billion |

| Market Size (2031) | USD 15.97 Billion |

| Growth Rate (2026 - 2031) | 22.20% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GPU Programming Platform Market Analysis by Mordor Intelligence

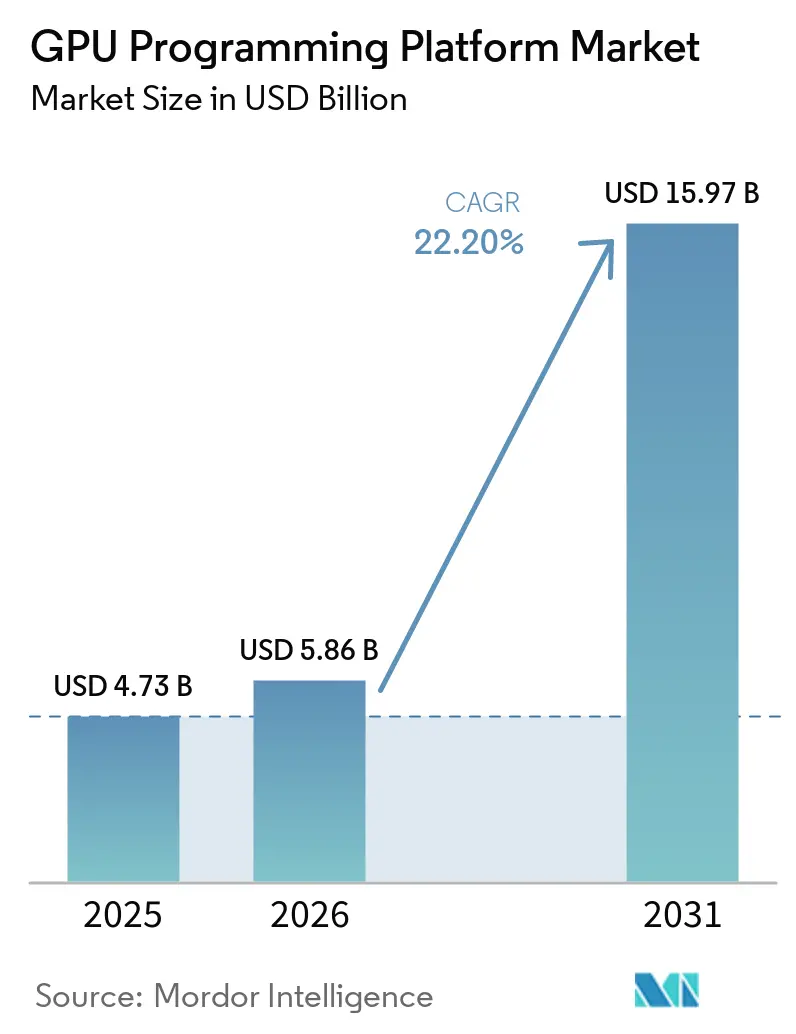

The GPU programming platform market size was USD 4.73 billion in 2025 and is projected to reach USD 15.97 billion by 2031, expanding at a CAGR of 22.20% over 2026-2031. The growth path reflects a clear shift in enterprise spending, where software layers such as programming models, compilers, middleware, and developer tools are capturing more value as GPU use broadens across AI and high-performance workloads. The GPU programming platform market is also benefiting from the spread of large language model training, rising inference deployment, and a growing need to run code across cloud, on-premises, and embedded environments without rebuilding the full stack each time. Competitive behavior is moving in the same direction, with incumbents deepening software ecosystems while newer vendors focus on portability, orchestration, and performance optimization to win adoption. This is creating a split structure in which CUDA-led environments remain deeply embedded, while open and multi-vendor approaches gain traction where cost control, supply flexibility, and data sovereignty matter more. As a result, the GPU programming platform market is likely to remain fast growing, with the strongest openings in software tooling, hybrid deployment support, and services tied to migration and optimization.

Key Report Takeaways

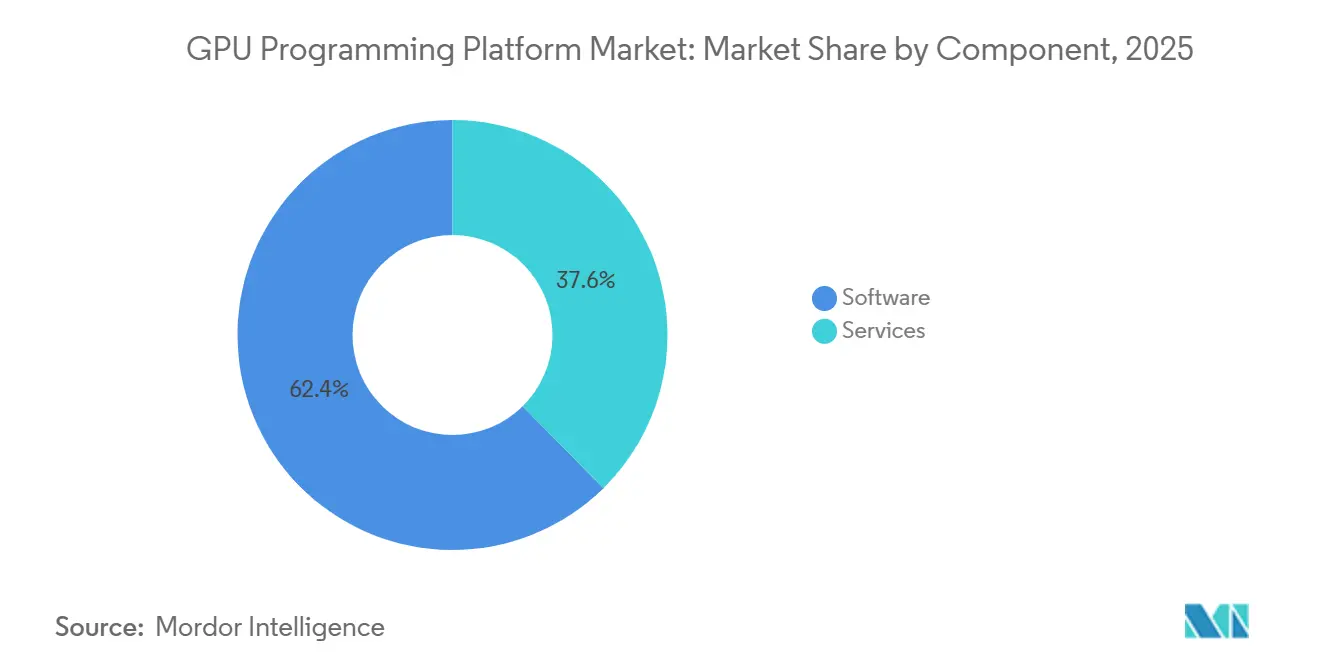

- By component, software led with 62.38% of the GPU programming platform market share in 2025 and is projected to expand at a 23.41% CAGR through 2031.

- By deployment model, public cloud held 46.51% of the GPU programming platform market share in 2025, while hybrid and multicloud are projected to expand at a 22.73% CAGR through 2031.

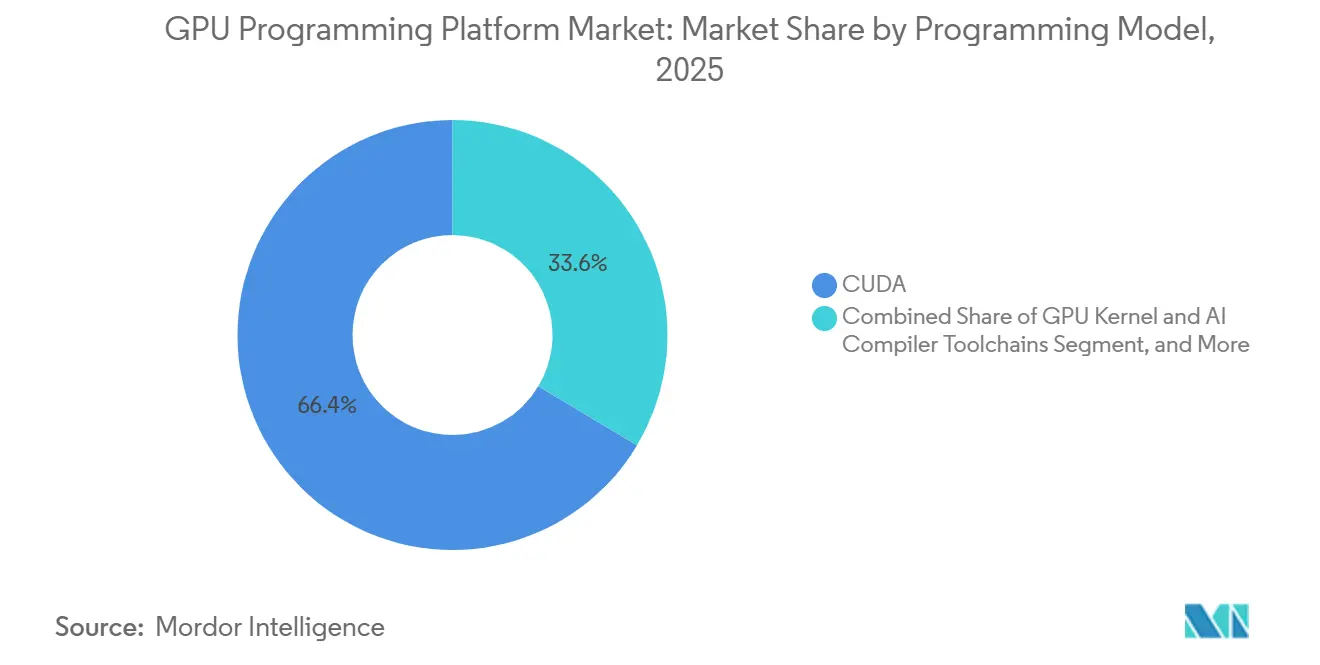

- By programming model, CUDA accounted for 66.43% share in 2025, while ROCm and HIP are projected to expand at a 23.16% CAGR through 2031.

- By end user, cloud service providers and data center operators held 34.47% share in 2025, while automotive and transportation are projected to expand at a 23.08% CAGR through 2031.

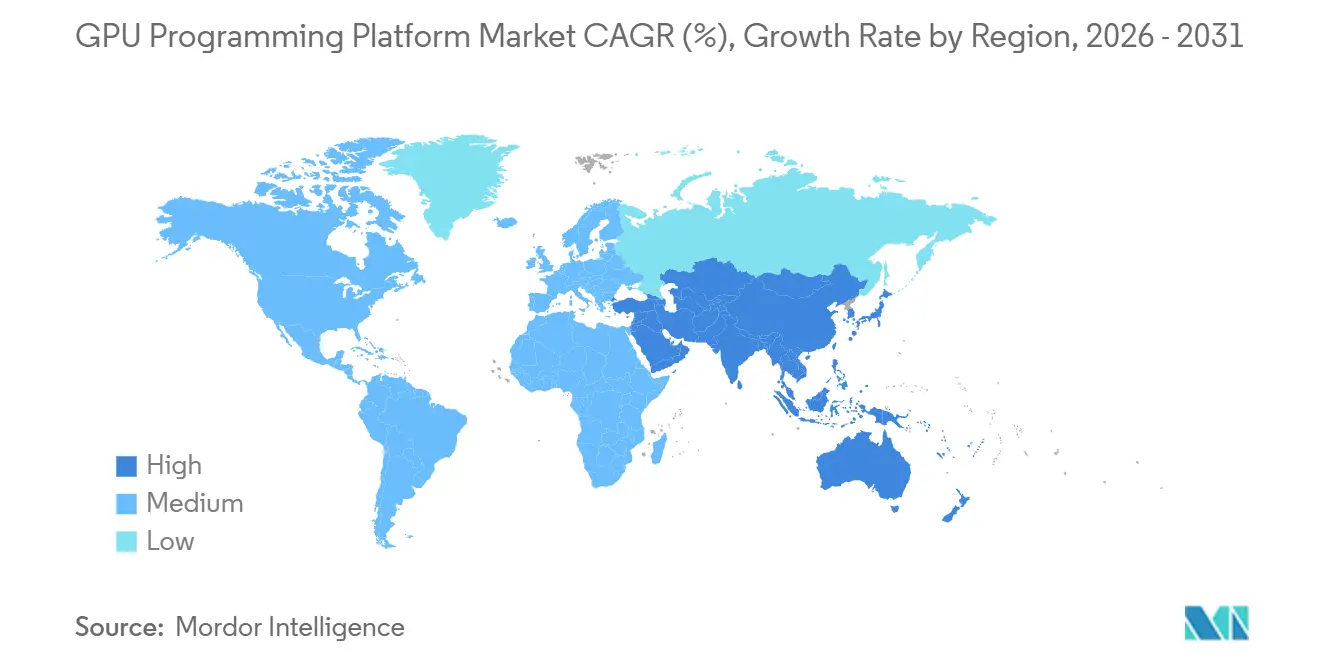

- By geography, North America held 51.82% share of the GPU programming platform market in 2025, while Asia-Pacific is projected to expand at a 22.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GPU Programming Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising AI Training and Inference Workloads Requiring Portable GPU Code | +5.0% | Global | Short term (≤ 2 years) |

| Growing Enterprise Demand for Cross-Vendor GPU Portability | +4.2% | North America and the EU | Medium term (2-4 years) |

| Expansion of Cloud-Native GPU Development Environments | +3.8% | Global | Short term (≤ 2 years) |

| Open-Source GPU Toolchains Lowering Entry Barriers for New Users | +2.8% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Increasing Use of Heterogeneous Compute in HPC And GenAI Stacks | +2.5% | North America and the EU | Medium term (2-4 years) |

| Rising Need for Performance Tuning and Developer Productivity Tools | +2.0% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising AI Training And Inference Workloads Requiring Portable GPU Code

AI model development has shifted the GPU programming platform market from a specialized niche to a mainstream software requirement for enterprise compute. NVIDIA reported that Blackwell-class systems led MLPerf Training v6.0 at scales up to 8,192 GPUs, which shows how much software performance now matters when large training clusters are deployed in production.[1]NVIDIA, “NVIDIA Blackwell Tops MLPerf Training 6.0 With Industry-Leading Scale and Performance,” NVIDIA Developer Blog, developer.nvidia.com The broader expansion is driven by inference, because production inference must run efficiently across a mix of cloud instances, local clusters, and edge systems rather than a single uniform training environment. That need is pushing the GPU programming platform market toward middleware, SDKs, and abstraction tools that can manage different memory structures, compiler behaviors, and precision settings without forcing teams to rebuild applications from scratch. The U.S. Department of Energy also noted in 2026 that AI-generated HPC code was reaching high levels of trust across key scientific domains, which supports demand for platforms that can serve both AI and scientific computing on shared GPU estates.

Growing Enterprise Demand for Cross-Vendor GPU Portability

Enterprise buyers are increasingly seeking software that reduces reliance on a single GPU vendor, especially when supply concentration and hardware pricing can influence deployment decisions. The GPU programming platform market is responding by shifting more value into portability layers that help workloads run across NVIDIA and AMD environments with fewer code changes. AMD highlighted wider ROCm adoption and broader platform support in early 2026, showing that alternative software stacks are becoming more practical for production AI and HPC use cases. Modular reinforced that direction in April 2026, when it enabled a single container to run across NVIDIA and AMD Instinct GPUs, giving enterprises a direct path to multi-vendor deployment without rewriting applications at each hardware transition. This matters because the GPU programming platform market grows faster when software decisions are no longer tied to a single hardware roadmap and when procurement teams can spread workloads across multiple suppliers.

Expansion of Cloud-Native GPU Development Environments

Cloud providers are making GPU development easier by packaging infrastructure, frameworks, and orchestration into managed environments, thereby shortening deployment cycles. Oracle integrated with NVIDIA DGX Cloud Lepton in June 2025, so developers could access GPU clusters for training, inference, digital twins, and HPC applications through a unified environment. Google Cloud also confirmed that it would deploy NVIDIA Vera Rubin NVL72 systems in the second half of 2026 within its AI Hypercomputer architecture, indicating that hyperscalers are still expanding the software stack around large GPU estates. CIQ extended Fuzzball to full multi-cloud support across CoreWeave, AWS, GCP, OCI, and Microsoft Azure in June 2026, reflecting how orchestration is becoming part of the standard cloud-native GPU toolkit. As this happens, the GPU programming platform market is moving toward an integrated cloud software model in which development, execution, placement, and optimization are managed together rather than through separate enterprise middleware layers.

Open-Source GPU Toolchains Lowering Entry Barriers for New Users

Open-source tooling is widening the addressable user base for the GPU programming platform market by reducing installation barriers and lowering the cost of experimentation. AMD said in January 2026 that ROCm downloads had increased 10x year over year and that platform support had doubled across Ryzen and Radeon products in 2025, which signals movement beyond traditional HPC and specialist data science teams. Apache TVM launched TIRx in June 2026 as an open compiler stack for ML kernels that supports both expert-written and agent-generated kernels across GPUs and AI accelerators. Canonical also packaged Intel oneAPI for Ubuntu 26.04 LTS, making SYCL development part of the standard Linux distribution path instead of a separate setup process. Together, these changes support the GPU programming platform market by making new development environments easier to access and by giving more teams a path into heterogeneous compute without starting from a proprietary stack.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Deep CUDA Ecosystem Lock-In and Migration Friction | -3.2% | Global | Long term (≥ 4 years) |

| Fragmented Standards Across HIP, SYCL, oneAPI, and OpenCL | -2.4% | North America and the EU | Medium term (2-4 years) |

| High Validation, Re-Optimization, and Testing Costs During Porting | -1.8% | Global | Medium term (2-4 years) |

| Scarcity Of GPU Compiler and Performance Engineering Talent | -1.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Deep CUDA Ecosystem Lock-In and Migration Friction

CUDA remains the strongest structural restraint on broad diversification in the GPU programming platform market because many production workloads were built, tested, and optimized first for NVIDIA environments. NVIDIA continues to deepen that position through CUDA-X libraries, compiler improvements, and developer tooling that shorten the optimization workload for teams already in the NVIDIA ecosystem. In practical terms, enterprises with large AI and HPC codebases face a long migration path because custom kernels, framework integrations, and memory management choices often require separate validation when moving to another stack. The problem is more pronounced in safety-sensitive, regulated workloads, where the validation history of an existing CUDA-based implementation can slow the adoption of alternatives. This keeps parts of the GPU programming platform market tied to incumbent environments, even when competing hardware or open stacks become more capable.

Fragmented Standards Across HIP, SYCL, oneAPI, and OpenCL

The GPU programming platform market also faces friction due to the lack of a dominant open standard across multi-vendor GPU programming. Intel’s January 2026 release notes for oneAPI DPC++ Compiler 6.3.0 showed that cross-platform interoperability was still incomplete, with Windows HIP and CUDA plugins not built in that release cycle. This leaves enterprises balancing several memory models, compiler chains, and debugging paths when they want performance across different hardware families. AMD’s continued ROCm investment and Intel’s distribution-level oneAPI packaging both move the ecosystem forward, but they do not remove the complexity that comes from parallel standards evolving at different speeds. Until toolchains become easier to align, the GPU programming platform market will continue to carry integration overhead for software vendors and enterprise engineering teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Toolchains Capture the Core Platform Premium

Software accounted for 62.38% of the GPU programming platform market in 2025 and is projected to expand at a 23.41% CAGR through 2031, indicating that value is moving toward the development and execution layers rather than remaining concentrated on hardware access alone. That position reflects the importance of programming models, compilers, middleware, profiling tools, and SDKs in making GPU workloads usable across AI training, inference, and scientific computing. NVIDIA reinforced this direction in 2026 with CUDA 13.3 and CompileIQ, which introduced AI-driven compiler autotuning and tile-based C++ kernel programming to improve optimization productivity on production workloads. As the GPU programming platform market expands, software continues to attract the strongest spending because enterprises need portability, monitoring, and faster tuning cycles more than a one-time infrastructure setup.

Services represented the remaining 37.62% share in 2025, and this part of the GPU programming platform industry is gaining weight as deployments become more complex and migration projects multiply. Consulting, integration, and code porting services are benefiting from demand to move workloads between CUDA, ROCm, and SYCL environments without disrupting production performance. Meta’s KernelAgent project, which focuses on LLM-assisted Triton kernel generation across NVIDIA and Intel XPU targets, also points to a growing need for training, implementation support, and structured developer enablement as toolchains become more automated. Managed services are likely to remain important for mid-sized enterprises that do not want to build in-house compiler and performance engineering teams, which gives the GPU programming platform market a durable services tail alongside software licensing and platform subscriptions.

By Deployment Model: Hybrid Configurations Challenge Public Cloud Orthodoxy

Public cloud held 46.51% share of the GPU programming platform market size in 2025, reflecting the scale advantage hyperscalers have in managed GPU environments, elastic capacity, and integrated development services. The leading cloud position was built on broad support from AWS, Google Cloud, Microsoft Azure, Oracle, and GPU-focused providers that package compute with orchestration and access to frameworks. VAST Data’s Polaris release in February 2026 captured that shift by offering orchestration across public cloud, neocloud, and on-premises environments through one control plane.[2]VAST Data, “VAST Data Introduces Polaris for Hybrid Multicloud AI Orchestration,” VAST Data Press Releases, vastdata.com At the same time, hybrid and multicloud are projected to expand at a 22.73% CAGR through 2031, as many enterprises seek to keep regulated data and persistent inference workloads closer to their internal infrastructure while using external capacity for peak demand.

Private cloud, dedicated hosted cloud, and on-premises estates remain important where data residency, security, or stable utilization levels justify tighter infrastructure control. Germany’s Industrial AI Cloud, launched in February 2026 with around 10,000 NVIDIA Blackwell GPUs, demonstrated that sovereign and regulated deployments can still connect to large-scale AI programs without relying solely on public cloud architectures. On-premises relevance is also visible in scientific environments such as the DOE’s NERSC Doudna system, where next-generation supercomputing still depends on a local programming environment that supports the same software libraries used in cloud AI pipelines. This mix supports the GPU programming platform market because customers are not choosing one deployment model over another, they are asking for software continuity across all of them.

By Programming Model: CUDA Leads While Open Stacks Gain Ground

CUDA captured 66.43% of the programming model segment in 2025, and that scale continues to define competition across the GPU programming platform market. NVIDIA said its CUDA ecosystem now supports more than 4 million developers, and the company continued extending the stack in 2026 with new runtime and compiler capabilities that reduce the work required to achieve high performance. This installed base matters because customers often choose programming environments based on libraries, framework maturity, and staff familiarity rather than hardware features alone. The result is that the GPU programming platform market still centers on CUDA when organizations prioritize speed to production, software depth, and an established developer pipeline.

ROCm and HIP are projected to expand at a 23.16% CAGR through 2031, which makes them the fastest-growing programming model path in the report and a meaningful challenger in the GPU programming platform market. AMD’s ROCm 7.0 release in September 2025 delivered up to 3.5x inference performance improvement over ROCm 6.0, added native Windows support, and enabled day-zero vLLM integration, all of which addressed major adoption barriers. The AMD and Modular partnership then extended the case for vendor-neutral deployment by enabling identical containers to run across AMD and NVIDIA Instinct environments without code changes. Intel’s oneAPI and SYCL also remain credible alternatives as packaging improves and Linux distribution support broadens, which means the GPU programming platform market is opening gradually even if CUDA remains the reference stack for many enterprise and AI teams.

By End User: Cloud Operators Hold the Largest Base While Automotive Moves Fastest

Cloud service providers and data center operators accounted for 34.47% of the GPU programming platform market share in 2025, which is consistent with their role as the largest direct buyers of GPU capacity and related software environments. These operators need developer tooling, performance monitoring, orchestration, and cost optimization at a scale that smaller users do not, which keeps them at the center of platform demand. CoreWeave’s March 2026 and April 2026 financings, along with its USD 6 billion agreement with Jane Street, demonstrated the significant capital flowing into GPU-specialized cloud infrastructure that relies on reliable software layers to support committed customer workloads. The GPU programming platform market benefits directly from this end-user group, as every expansion in AI cloud capacity typically drives demand for toolchains, runtime management, and developer productivity software.

Automotive and transportation is projected to expand at a 23.08% CAGR through 2031, making it the fastest-growing end-user segment in the GPU programming platform market. NVIDIA’s DRIVE software path uses CUDA and TensorRT across both cloud training and in-vehicle deployment, providing automotive programs with a single programming environment from model development through inference at the edge. The DriveOS LLM SDK goes further by supporting cross-compilation for AArch64 vehicle targets, which helps move LLM-based functions from data centers into production systems with consistent tools and APIs. Financial services, healthcare, manufacturing, and telecom also expand the customer base, but automotive stands out because software continuity, validation requirements, and real-time inference needs make the GPU programming platform market especially important in that segment.

Geography Analysis

North America held 51.82% of the GPU programming platform market share in 2025, which kept it firmly ahead of every other region. The region combines the largest concentration of GPU vendors, hyperscalers, AI software companies, and enterprise buyers, providing a strong base for both platform development and adoption. CoreWeave’s funding activity in 2026 and its USD 6 billion agreement with Jane Street showed that commercial demand for GPU infrastructure was still scaling rapidly in the region. NVIDIA’s September 2025 collaboration with Intel also reflected the depth of the North American supply chain and platform coordination around AI infrastructure.[3]Intel, “Intel and NVIDIA to Jointly Develop AI Infrastructure and Personal Computing Products,” Intel Newsroom, newsroom.intel.com In addition, the U.S. Department of Energy continued to support code portability and abstraction work for advanced computing, which helps sustain long-term software demand around heterogeneous GPU environments.

Europe remains a structurally important region for the GPU programming platform market because data sovereignty, industrial policy, and regulated AI deployment are shaping demand. The EU planned a portfolio of up to 5 AI Gigafactories, with the first facilities expected to become operational from 2026, which supports a new wave of sovereign GPU software environments tied to public and industrial investment ZDF. Germany’s Industrial AI Cloud, developed with Deutsche Telekom, NVIDIA, and Polarise, added one of the clearest examples of this model in February 2026 through a large Blackwell-based deployment. This environment favors software stacks that can combine compliance, performance tracking, and deployment flexibility across private and connected cloud resources.

Asia-Pacific is projected to expand at a 22.68% CAGR through 2031, which makes it the fastest-growing regional block in the GPU programming platform market. The growth is tied to sovereign compute buildouts and domestic ecosystem development, especially in China and India, where GPU infrastructure strategy is becoming part of broader AI capacity planning. The region also benefits from growing acceptance of open and multi-vendor toolchains as enterprises prepare for mixed GPU fleets instead of one uniform hardware base. South America and the Middle East and Africa remain earlier-stage markets, but the infrastructure conditions for adoption are improving as hyperscalers and regional GPU cloud providers widen access to advanced compute. As that access improves, the GPU programming platform market should broaden across finance, manufacturing, and telecom workloads in these regions as well.

Competitive Landscape

The GPU programming platform market is moderately concentrated, with the strongest concentration at the programming model layer and much broader fragmentation across services, orchestration, and portability tooling. NVIDIA holds the most defensible position because CUDA combines scale, long library history, and developer familiarity in a way that few rivals currently match. The company reinforced that advantage in 2026 through CUDA 13.3 and CompileIQ, which added AI-driven compiler tuning and easier high-performance kernel development inside its existing software stack. NVIDIA also broadened enterprise distribution through a larger collaboration with Red Hat around Rubin-era systems, which links its GPU software stack more closely to common enterprise operating and orchestration environments. These moves keep the GPU programming platform market anchored to NVIDIA across much of AI training and enterprise deployment.

AMD is mounting the clearest competitive challenge by pairing hardware scale-up with steady ROCm improvements and a more open software posture. ROCm 7.0 improved inference performance, added native Windows support, and tightened framework compatibility, which addressed several practical barriers that had slowed broader production use. The April 2026 AMD and Modular partnership then gave enterprises a way to run one container across AMD and NVIDIA Instinct GPUs, which directly targeted demand for less vendor-specific deployment. This combination positions AMD as the main beneficiary when customers want the GPU programming platform market to become more portable and less tied to a single stack.

Competitive white space remains largest in portability middleware, AI-assisted kernel generation, and orchestration for hybrid and edge environments. Anyscale showed the commercial value of this layer in March 2026 when it integrated NVIDIA cuDF into Ray Data and reported 80% lower multimodal data processing cost than CPU-only pipelines in that workflow.[4]Anyscale, “Anyscale Cuts Multimodal AI Data Processing Costs by 80% With NVIDIA RTX PRO 4500 Blackwell,” Anyscale, anyscale.com Intel is also taking a longer-term route by embedding oneAPI packaging into Ubuntu 26.04 LTS, which can influence developer behavior at the distribution level rather than only through direct hardware sales. GPU cloud specialists such as CoreWeave are becoming important channel partners because they bundle infrastructure scale with software access and can accelerate adoption for platform vendors. In automotive, NVIDIA’s Halos OS and ISO 26262 ASIL D positioning create a strong qualification advantage that can lock programming environments into vehicle programs for multiple years.

GPU Programming Platform Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Amazon Web Services, Inc.

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA announced the Vera Rubin platform at ISC High Performance 2026, delivering over 7 exaflops of AI compute and 5 petaflops of native FP64 precision per system, with CUDA-X libraries across the full stack. Leibniz Supercomputing Centre, NERSC, and Los Alamos National Laboratory selected Vera Rubin for their next flagship supercomputer programs. Global system manufacturers including Dell Technologies, HPE, and Supermicro will bring NVL4-based systems to market in Q4 2026.

- June 2026: Modular released Platform 25.6, delivering unified GPU support across NVIDIA, AMD, including MI355X, and Apple Silicon in a single container. Early benchmarks showed MAX on AMD MI355X outperforming vLLM on Blackwell in certain configurations, and Mojo’s unified programming model was extended to consumer-grade AMD and NVIDIA GPUs for the first time.

- June 2026: CIQ expanded its Fuzzball AI and HPC orchestration platform to full multi-cloud support across CoreWeave, AWS, GCP, OCI, and Microsoft Azure, enabling enterprise teams to define GPU workloads once and route execution automatically across cloud environments based on cost, performance, and data locality.

- June 2026: Apache TVM launched TIRx, an open-source hardware-native DSL and compiler for ML kernels targeting GPUs and AI accelerators, supporting expert-written, agent-generated, and megakernel workflows in a unified compilation framework.

Global GPU Programming Platform Market Report Scope

The GPU programming platform market encompasses software, frameworks, development tools, libraries, and related solutions that enable developers and enterprises to program, optimize, and deploy applications using graphics processing units (GPUs). The report analyzes the market across key components, deployment models, applications, end-user industries, and geographies, covering adoption trends, growth drivers, restraints, competitive landscape, and market opportunities during the forecast period.

The GPU Programming Platform Market Report is Segmented by Component (Software [Programming Tools and Compilers, Middleware, SDKs, and Portability Tools, Libraries and Runtime Systems, Performance Monitoring and Profiling Tools, and Developer, Testing, and Debugging Tools], and Services [Consulting, Integration, and Code Migration Services, Managed Services, and Training, Support, and Maintenance Services]), Deployment Model (On-Premises, Public Cloud, Private Cloud/Dedicated Hosted Cloud, and Hybrid and Multicloud), Programming Model (CUDA, ROCm and HIP, oneAPI and SYCL, OpenCL, Directive-Based Models, GPU Kernel and AI Compiler Toolchains, and Other Programming Models), End User (Cloud Service Providers and Data Center Operators, IT, Software, Internet and SaaS Providers, Telecommunications, Banking, Financial Services and Insurance, Healthcare and Life Sciences, Manufacturing, Automotive and Transportation, and Other End Users), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | Programming Tools and Compilers |

| Middleware, SDKs, and Portability Tools | |

| Libraries and Runtime Systems | |

| Performance Monitoring and Profiling Tools | |

| Developer, Testing, and Debugging Tools | |

| Services | Consulting, Integration, and Code Migration Services |

| Managed Services | |

| Training, Support, and Maintenance Services |

| On-Premises |

| Public Cloud |

| Private Cloud / Dedicated Hosted Cloud |

| Hybrid and Multicloud |

| CUDA |

| ROCm and HIP |

| oneAPI and SYCL |

| OpenCL |

| Directive-Based Models |

| GPU Kernel and AI Compiler Toolchains |

| Other Programming Models |

| Cloud Service Providers and Data Center Operators |

| IT, Software, Internet, and SaaS Providers |

| Telecommunications |

| Banking, Financial Services, and Insurance |

| Healthcare and Life Sciences |

| Manufacturing |

| Automotive and Transportation |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Component | Software | Programming Tools and Compilers |

| Middleware, SDKs, and Portability Tools | ||

| Libraries and Runtime Systems | ||

| Performance Monitoring and Profiling Tools | ||

| Developer, Testing, and Debugging Tools | ||

| Services | Consulting, Integration, and Code Migration Services | |

| Managed Services | ||

| Training, Support, and Maintenance Services | ||

| By Deployment Model | On-Premises | |

| Public Cloud | ||

| Private Cloud / Dedicated Hosted Cloud | ||

| Hybrid and Multicloud | ||

| By Programming Model | CUDA | |

| ROCm and HIP | ||

| oneAPI and SYCL | ||

| OpenCL | ||

| Directive-Based Models | ||

| GPU Kernel and AI Compiler Toolchains | ||

| Other Programming Models | ||

| By End User | Cloud Service Providers and Data Center Operators | |

| IT, Software, Internet, and SaaS Providers | ||

| Telecommunications | ||

| Banking, Financial Services, and Insurance | ||

| Healthcare and Life Sciences | ||

| Manufacturing | ||

| Automotive and Transportation | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and future outlook of the GPU programming platform space?

The GPU programming platform market stood at USD 4.73 billion in 2025 and is projected to reach USD 15.97 billion by 2031, growing at 22.20% CAGR over 2026-2031.

Which component leads revenue generation?

Software led with 62.38% share in 2025 and is also projected to post the fastest growth at a 23.41% CAGR, showing that toolchains and middleware are capturing the largest value pool.

Why is hybrid and multicloud adoption rising for GPU programming platforms?

Enterprises want to split workloads across on-premises and cloud environments for compliance, cost control, and GPU availability, which is why hybrid and multicloud is projected to grow at a 22.73% CAGR through 2031.

Why does CUDA still dominate programming model adoption?

CUDA held 66.43% share in 2025 because of its large developer base, mature libraries, and deep framework integration, which still give it the strongest production position.

Which end-user group is creating the largest demand base?

Cloud service providers and data center operators held 34.47% share in 2025 because they buy and manage GPU capacity at scale and rely heavily on orchestration, optimization, and developer tooling.

Which region is growing the fastest?

Asia-Pacific is projected to expand at a 22.68% CAGR through 2031, supported by sovereign compute buildouts and broader interest in multi-vendor GPU software environments.

Page last updated on: