Workstation GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.21 Billion |

| Market Size (2031) | USD 12.15 Billion |

| Growth Rate (2026 - 2031) | 18.45% CAGR |

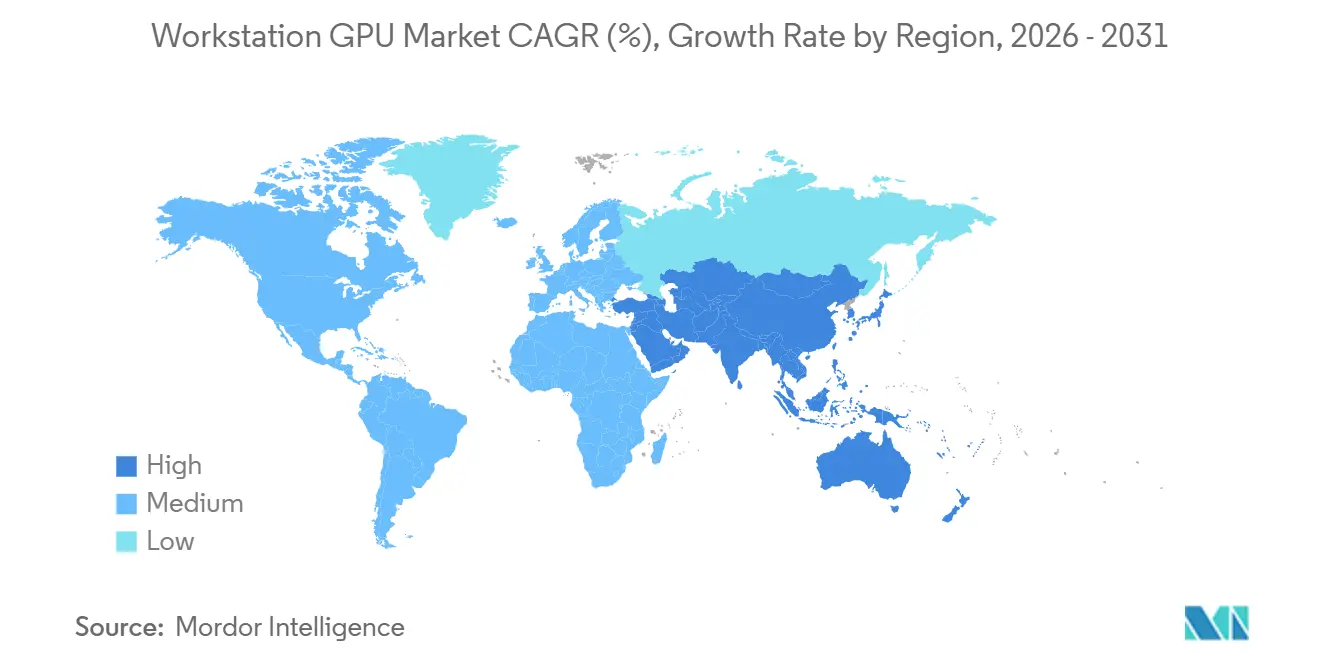

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Workstation GPU Market Analysis by Mordor Intelligence

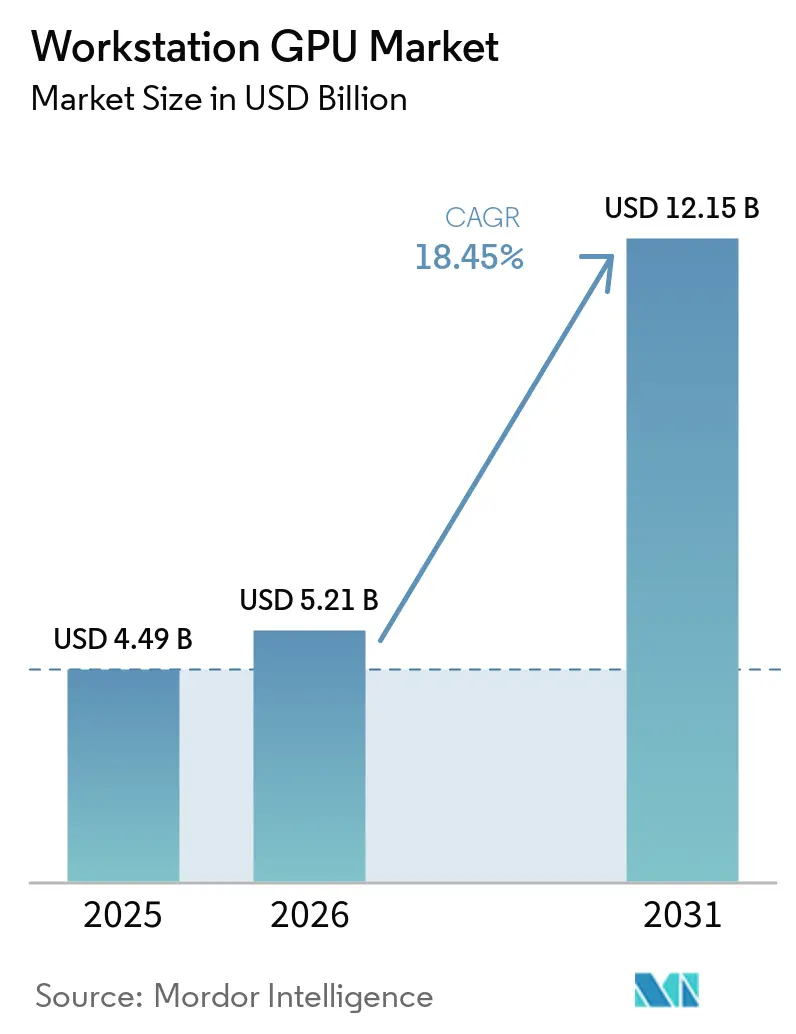

The workstation GPU market size was valued at USD 4.49 billion in 2025 and is projected to reach USD 12.15 billion by 2031, growing at a CAGR of 18.45% from 2026 to 2031. The workstation GPU market is being reshaped by a clear shift toward local AI inference, as enterprises want high-density compute that can stay close to proprietary data and regulated workflows. Demand is also rising because professional users now expect one platform to handle simulation, design, rendering, and model inference without moving workloads between separate systems. The workstation GPU market is also benefiting from a synchronized product refresh cycle across major silicon vendors and workstation OEMs, which is bringing more performance, more memory, and wider platform choice into current buying cycles. At the same time, supply tightness in advanced memory and packaging is limiting how much of this demand can be converted into shipments in the near term. Competition in the workstation GPU market is therefore widening through software ecosystems, certification depth, pricing strategy, and system-level design, while the strongest opportunities remain tied to secure on-premise AI development, digital twin workflows, and premium visualization systems.

Key Report Takeaways

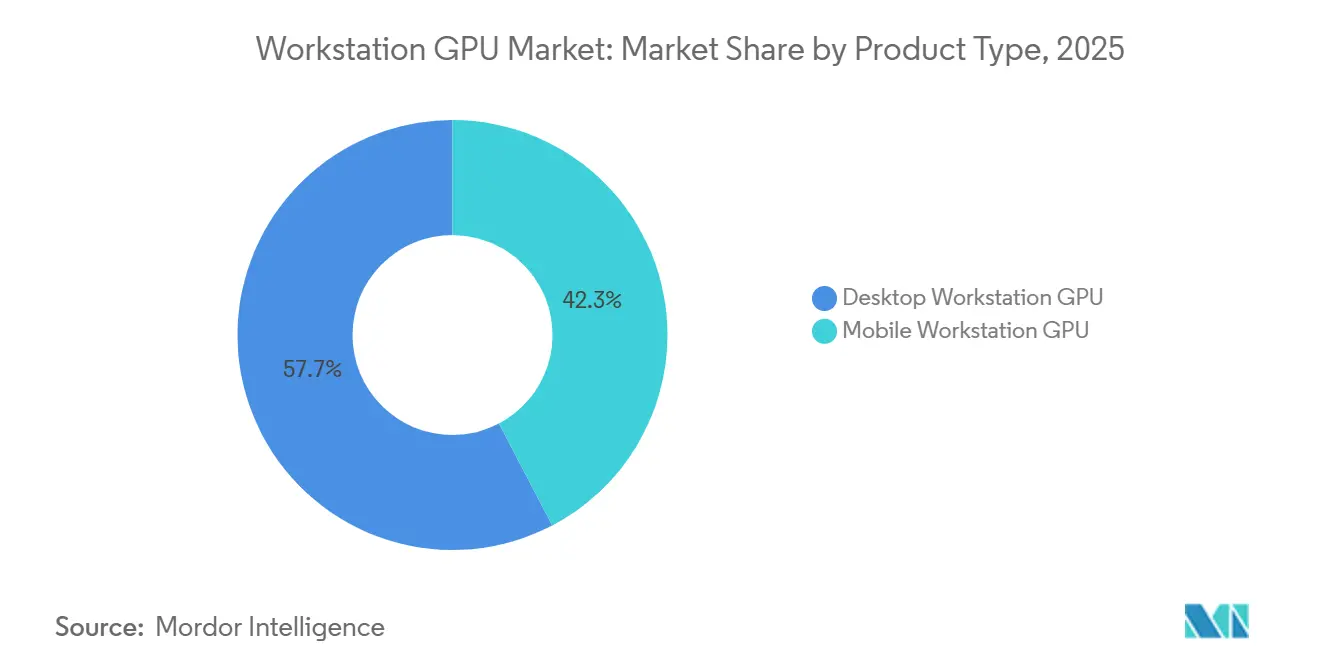

- By product type, desktop workstation GPU held 57.68% of the workstation GPU market share in 2025, while mobile workstation GPU are projected to expand at a 19.63% CAGR through 2031.

- By application, CAD, CAM and CAE accounted for 28.14% of revenue in 2025, while AI Development and Data Science are projected to grow at a CAGR at 19.51% through 2031.

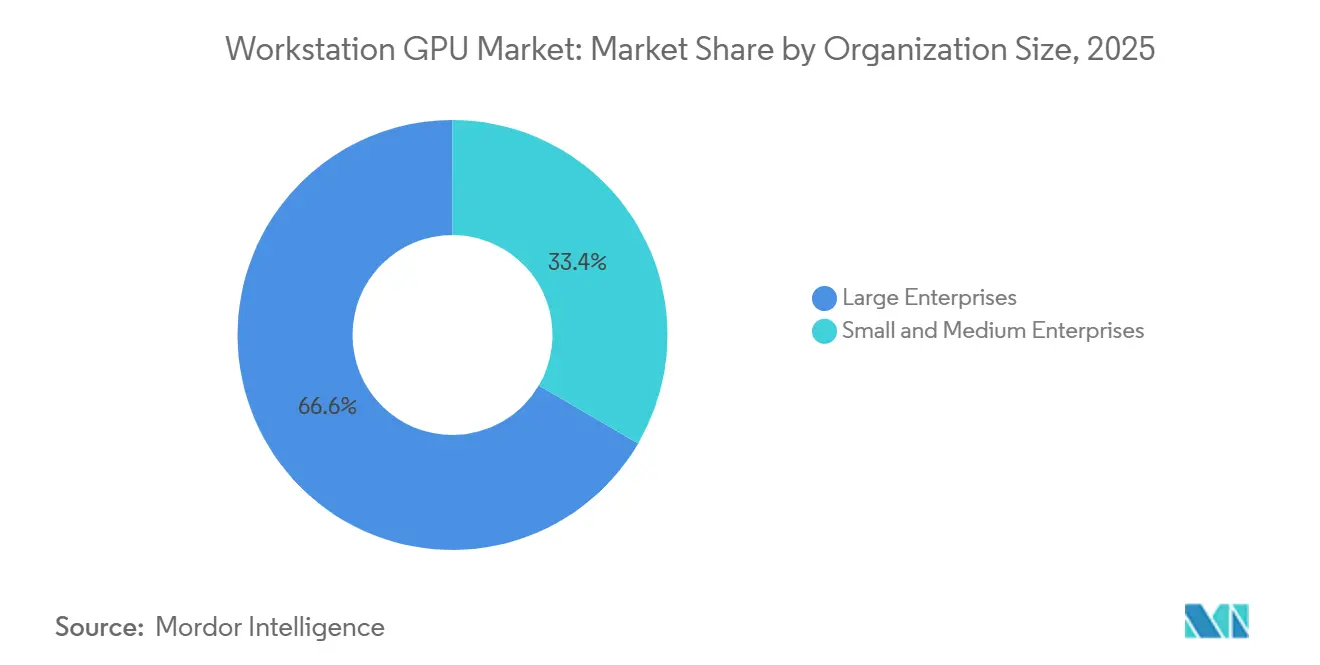

- By organization size, large enterprises held 66.59% of revenue in 2025, while small and medium enterprises are expected to expand at a 19.84% CAGR through 2031.

- By industry vertical, Architecture, Engineering and Construction retained 25.46% share in 2025, while Automotive and Transportation is projected to grow at a 20.18% CAGR through 2031.

- By geography, North America held 36.53% of the workstation GPU market in 2025, while Asia-Pacific is projected to advance at a 20.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Workstation GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising AI Inference and Local Model Workflows on Workstations | +5.2% | Global, concentrated near-term demand in North America and Western Europe | Short term (≤ 2 years) |

| Rising CAD, Simulation, and Digital Twin Workloads in Engineering Teams | +3.8% | Global, strongest in North America, Germany, and APAC advanced-manufacturing hubs | Medium term (2-4 years) |

| Enterprise Demand for Secure On-Premise AI Development Environments | +3.1% | North America and Europe, with spillover to APAC financial hubs | Medium term (2-4 years) |

| Refresh Cycle for Professional Visualization and Content Creation PCs | +2.5% | North America and Europe, with early uptake in South Korea and Japan | Short term (≤ 2 years) |

| Chiplet and Advanced Packaging Road Maps Improving Pro GPU Performance Density | +2.0% | Global, with technology leadership centered in APAC semiconductor fabs | Long term (≥ 4 years) |

| Export Controls and Supply Chain Localization Supporting Regional GPU Substitution | +1.5% | China, India, South Korea, with spillover to Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising AI Inference and Local Model Workflows on Workstations

The workstation GPU market is gaining momentum from enterprise demand for local AI inference in settings where cloud processing is difficult to approve or justify. NVIDIA introduced the RTX PRO Blackwell family in March 2025, and the flagship workstation edition delivered up to 4,000 AI TOPS and 96 GB of GDDR7 ECC memory, elevating local model execution to a much higher performance class.[1]NVIDIA Corporation, “NVIDIA Blackwell RTX PRO Comes to Workstations and Servers for Designers, Developers, Data Scientists and Creatives to Build and Collaborate with Agentic AI,” GlobeNewswire, globenewswire.com The same launch broadened the workstation GPU market by integrating AI development, model inference, visualization, and content workflows into a single professional platform. AMD also entered this part of the workstation GPU market in July 2025 with the Radeon AI PRO R9700, a 32 GB professional card built for workstation systems and ROCm 6.3 compatibility. This pattern matters because enterprises are no longer buying only rendering speed; they are buying enough local memory and certified performance to keep proprietary AI work close to the user. As that requirement spreads, the workstation GPU market is moving beyond its older dependence on CAD and rendering alone.

Rising CAD, Simulation, and Digital Twin Workloads in Engineering Teams

The workstation GPU market is also being pushed by engineering teams that now expect much faster simulation and digital twin execution on professional hardware. NVIDIA said leading CAE vendors, including Ansys, Altair, Cadence, Siemens, and Synopsys, achieved up to 50x acceleration with Blackwell in selected workloads, thereby changing the economics of workstation-side simulation. The same release noted that BMW and Volvo Cars were using Blackwell-accelerated digital twins, which shows how the workstation GPU market is now tied to product development speed and design validation, not only to visual output. Springer Nature also documented broader digital twin adoption across design, simulation, validation, and optimization in smart manufacturing environments, which supports the longer-term demand base for these systems. That shift raises the minimum specification that engineering teams expect from a professional GPU, because they now need stable performance across simulation, visualization, and collaboration within the same workflow. As a result, the workstation GPU market is pulling more value from engineering software stacks and less from stand-alone graphics acceleration.

Enterprise Demand for Secure On-Premise AI Development Environments

The workstation GPU market is benefiting from enterprise efforts to keep AI development inside controlled infrastructure. VMware stated in October 2025 that VMware Private AI Foundation with NVIDIA added government-ready capabilities, with FIPS 140 cryptography enabled by default across key VCF components, supporting high-assurance deployments. HPE also announced secure AI Factory innovations with NVIDIA for government and enterprise adoption, underscoring that the workstation GPU market is tied to broader sovereign and regulated AI buildouts. Lenovo Press added a direct cost angle by showing that on-premises generative AI can reach cloud cost parity in 12 to 18 months for high-utilization teams, making local deployment easier to defend in budget reviews. This means the workstation GPU market is supported by both compliance logic and usage economics. When these two factors reinforce each other, buying decisions become less sensitive to short-term hardware price swings. That makes the premium end of the workstation GPU market more durable than standard enterprise PC demand.

Refresh Cycle for Professional Visualization and Content Creation PCs

The workstation GPU market is also getting support from a rare multi-vendor refresh window. NVIDIA refreshed its professional lineup in 2025 with RTX PRO Blackwell desktop and mobile products that introduced fifth-generation Tensor Cores, PCIe Gen 5, and broader memory options across the stack. Intel entered the same buying cycle with the Arc Pro B70 in March 2026, priced at USD 949 with 32 GB of ECC GDDR6, giving budget-sensitive buyers a new certified option. Lenovo then announced the ThinkStation P4 in May 2026 with AMD Ryzen PRO 9000 processors and NVIDIA RTX PRO 6000 Blackwell GPUs, which showed OEM confidence in the current workstation replacement cycle. These launches matter because they compress delayed purchases into a shorter period and give enterprises a reason to standardize on current-generation platforms. That effect is especially visible in the workstation GPU market where certification, memory capacity, and workflow compatibility all matter more than raw component pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership for Professional GPU Workstations | -2.8% | Global, more pronounced in SME segments and emerging markets | Medium term (2-4 years) |

| Supply Tightness in Advanced Memory and Substrate Components | -2.5% | Global, with allocation advantages concentrated in North America and Western Europe | Short term (≤ 2 years) |

| Power, Thermal, and Form Factor Constraints in Desktop and Mobile Systems | -1.6% | Global, more acute in space-constrained APAC deployments | Long term (≥ 4 years) |

| Driver Certification and Application Compatibility Complexity | -1.2% | Global, most acute for AMD and Intel platforms entering CAE and medical imaging verticals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership for Professional GPU Workstations

The workstation GPU market still faces a meaningful adoption barrier because full professional systems remain expensive to acquire and maintain. The NVIDIA RTX PRO 6000 Blackwell Workstation Edition had a retail price near USD 8,500 in 2025, and the input indicated that a fully configured high-end workstation for AI or simulation often exceeded USD 20,000 per seat. Lenovo Press also showed that the financial case for on-premises generative AI depends heavily on utilization, meaning smaller firms with uneven workloads have a longer payback window. This cost issue extends beyond the GPU itself, as enterprises also need supporting CPU power, memory, storage, cooling, energy, security tools, and management time. That combination slows adoption in the lower end of the workstation GPU market, even when the technical need is clear. It also explains why large enterprises still dominate revenue while smaller firms are adopting more selectively.

Supply Tightness in Advanced Memory and Substrate Components

The workstation GPU market is also constrained by component availability, especially where high-end memory and advanced packaging are required. The input tied this issue to tight HBM3E and GDDR7 supply and to limited CoWoS packaging capacity, which restricts how quickly vendors can convert demand into shippable units. This matters because professional buyers often wait for specific memory capacity, certification, and thermal profiles, so substitution is not always easy when flagship cards are unavailable. The effect is visible across premium products and mid-range professional cards, since both categories depend on stable component flows to support enterprise rollouts. In practical terms, this means the workstation GPU market can show strong demand signals and still deliver slower revenue conversion when supply allocations remain tight. It also keeps lead times and procurement planning at the center of enterprise purchase decisions in 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mobile Workstations Gain Ground in Distributed Engineering Teams

Desktop workstation GPUs accounted for 57.68% of the workstation GPU market size in 2025, while mobile workstation GPUs are projected to grow at a 19.63% CAGR through 2031. The desktop side of the workstation GPU market remained larger because tower systems still offer more thermal headroom, more expansion capacity, and better support for high-bandwidth PCIe Gen 5 data paths. That matters for simulation, digital twin, and advanced visualization users who depend on multi-GPU scaling or very high memory footprints. The installed base also remains tied to long-running engineering environments where desktop certification and fleet standardization matter as much as peak graphics speed.

Mobile workstation GPUs are growing faster as engineering and AI teams are increasingly distributed, yet they still need professional-grade hardware that supports certified applications and local inference. NVIDIA said its RTX PRO Blackwell laptop GPU range scaled up to 24 GB of GDDR7 and added Blackwell Max-Q efficiency features, which reduced the practical gap between mobile and desktop use in many professional workflows. The input also noted that mobile performance is moving toward 80% to 90% of desktop equivalents for several inference and visualization tasks, which is changing how enterprises define acceptable field performance. Lenovo’s 2026 workstation push further supports that shift because OEMs are treating mobility and workstation-class output as part of the same product planning cycle. As a result, the workstation GPU market is likely to see a narrower share gap between desktop and mobile systems over the forecast period.

By Application: AI Development Defines the Next Growth Vector in Professional GPU Demand

CAD, CAM and CAE held 28.14% of the workstation GPU market size in 2025, while AI Development and Data Science are projected to expand at a 19.51% CAGR through 2031. CAD, CAM and CAE remained the anchor application in the workstation GPU market because design, structural analysis, and engineering validation are already embedded in enterprise workflows. The input tied this leadership to solver acceleration, mesh refinement, and real-time physics simulation features inside major commercial software platforms. NVIDIA also said that Ansys, Siemens, and Synopsys were among the software providers bringing CUDA-X-accelerated releases to workstation-class hardware, which reinforces why this application continues to drive current demand.

AI Development and data science are growing faster because enterprises want dedicated systems for model fine-tuning, inference optimization, and retrieval-augmented workflows without relying fully on shared cloud clusters. That change is broadening the workstation GPU market into private AI development, where memory capacity, secure local storage, and software compatibility all matter at the workstation level. Other applications still carry meaningful demand, especially 3D Rendering and Visualization and Media Production and Content Creation, where ray tracing and real-time output remain essential for client work. Scientific Computing and Simulation also stays stable through demand from research labs, pharmaceutical firms, and public research environments, while Medical Imaging and Healthcare Visualization adds a more specialized layer of demand around on-premise imaging and planning tools. The broader result is that the workstation GPU market now supports many buyers who want one platform for AI and visualization in the same work session, rather than separate systems for each task.

By Organization Size: Enterprise Procurement Anchors the Market as SMEs Accelerate

Large enterprises held 66.59% of the workstation GPU market share in 2025, while small and medium enterprises are expected to grow at a 19.84% CAGR through 2031. Large companies led the workstation GPU market because they can absorb high per-seat cost and usually need certified fleets, vendor-backed support, and longer hardware refresh planning. They also operate at a scale where secure local AI development, digital engineering, and content production justify premium hardware standards across many users. That keeps enterprise procurement at the center of current revenue even as other buyer groups are becoming more active.

Small and medium enterprises are growing faster because lower-cost professional products are widening access to the workstation GPU market. Intel launched the Arc Pro B70 in March 2026 at USD 949, while AMD continued to position workstation-ready AI GPUs as more accessible entry points for professional users. Lenovo Press also showed that the economics of local AI improve quickly when utilization is steady, which helps explain why mid-market teams are revisiting workstation ownership instead of defaulting to rented cloud capacity. AMD and Nutanix added another layer in February 2026 through a strategic partnership and a USD 150 million investment tied to enterprise AI platforms, which points to a stronger channel push into these buyers.[2]Advanced Micro Devices, Inc. and Nutanix, “AMD and Nutanix Announce Strategic Partnership to Advance an Open and Scalable Platform for Enterprise AI,” GlobeNewswire, globenewswire.com This means the workstation GPU market is likely to keep its enterprise revenue base while adding more incremental volume from smaller organizations.

By Industry Vertical: Automotive Digital Twin Pipelines Set the Premium Demand Standard

Architecture, Engineering and Construction retained 25.46% share in 2025, while Automotive and Transportation is projected to grow at a 20.18% CAGR through 2031. Architecture, Engineering and Construction led the workstation GPU market because BIM expansion, visual rendering, structural analysis, and city-scale digital twin work all keep professional GPU demand high across firms of different sizes. These workflows depend on predictable performance and stable software certification, which favors professional workstation deployment over generic graphics hardware. The segment also benefits from recurring demand rather than one-time experimentation, which helps explain its large revenue position in 2025.

Automotive and transportation are growing faster because vehicle makers are using GPU-accelerated virtual design, crash simulation, aerodynamic modeling, and immersive review systems across more stages of development. NVIDIA’s technical blog reported that Rivian used RTX PRO 6000 Blackwell Workstation Edition GPUs for immersive vehicle design reviews with photorealistic 4K rendering, reflecting the premium standard being set in this vertical. Hyundai Motor Group expanded its use of Blackwell AI infrastructure and Omniverse Enterprise for factory digital twins in late 2025, furthering the wider shift from physical testing to connected virtual environments. Manufacturing and Industrial Design remains another strong vertical through CNC simulation, additive manufacturing design, and factory modeling, while Media and Entertainment continues to support consistent demand for rendering and compositing. Together, these patterns show that the workstation GPU market is increasingly defined by sectors where simulation, visualization, and AI are starting to merge into the same production workflow.

Geography Analysis

North America held 36.53% of the workstation GPU market share in 2025, while Asia-Pacific is forecast to grow at a 20.35% CAGR through 2031. North America led the workstation GPU market because it combines large technology budgets with dense demand from defense contractors, life sciences organizations, and media production studios. Buyers in the region also place high value on certified platforms, secure local compute, and stable enterprise support. HPE and NVIDIA reinforced that environment in 2025 with an AI Factory for Government design aimed at secure AI deployment in the public sector and regulated settings.[3]Hewlett Packard Enterprise, “HPE Advances Government and Enterprise AI Adoption Through Secure AI Factory Innovations with NVIDIA,” BusinessWire, businesswire.com Canada and Mexico also contribute through automotive engineering centers and supply chain design teams that align closely with U.S. workstation standards.

Europe remained the second-largest regional market for workstations and GPUs, with Germany, the United Kingdom, and France as the main demand centers. Germany remained central because automotive, aerospace, and industrial machinery companies continue to depend on simulation, digital twins, and precision design workflows that require professional GPU capabilities. NVIDIA’s work with Siemens and other CAE partners supports that setup by bringing faster engineering computation into production environments. The United Kingdom and France add steady demand through visual effects, media work, scientific research, and computational modeling. Italy and the rest of the region contribute through product design, architecture, and light industrial manufacturing, which keeps Europe broad-based rather than concentrated in one end market.

Asia-Pacific is the fastest-growing part of the workstation GPU market because China, India, Japan, and South Korea are all adding demand from different starting points. The input linked China’s momentum to domestic GPU substitution under export control pressure, while the OECD noted wider government efforts to build more resilient semiconductor value chains. India is adding another layer through its expanding AI development services base and infrastructure push around GPU deployment, which supports adjacent demand for local professional compute. Japan and South Korea continue to rely on workstation-class systems for semiconductor EDA, robotics design, and automotive engineering. Southeast Asia is emerging through electronics manufacturing services and design capability growth, while South America and the Middle East and Africa remain smaller but developing markets supported by digital twin work in energy and expanding technology services.

Competitive Landscape

The workstation GPU market operates through two connected competitive layers, the silicon layer and the system integration layer. At the silicon level, NVIDIA holds the strongest position in the workstation GPU market because it combines a broad RTX PRO Blackwell lineup with CUDA depth, AI capability, and extensive ISV certification coverage. AMD competes by emphasizing price-performance for AI inference and large memory capacity in professional systems, especially with the Radeon AI PRO R9700 positioning. Intel widened the silicon contest in March 2026 when it launched the Arc Pro B70 and B65, which gave the workstation GPU market a lower-cost certified path in the mid-range segment. Intel also tied that move to WHQL-certified driver support from launch, directly addressing a long-standing concern about professional stability in regulated workflows.

At the system level, the workstation GPU market is much more fragmented because OEMs and specialist builders compete on platform design, cooling, certifications, and support rather than on chip ownership. Lenovo, Dell, HP, and BOXX Technologies all operate in this layer, and their differentiation depends on workstation architecture, product mix, and enterprise readiness. BOXX launched the APEXX T3 workstation in June 2026 with AMD Ryzen Threadripper 9000 processors and NVIDIA RTX PRO 2000 Blackwell GPUs, which showed how specialist vendors are targeting demanding 3D and motion media users with tightly defined systems.[4]BOXX Technologies, “BOXX Launches APEXX T3 Workstation With NVIDIA RTX PRO 2000 Blackwell Graphics,” BOXX Technologies, boxx.com Lenovo also announced the ThinkStation P4 in May 2026 with AMD Ryzen PRO 9000 processors and NVIDIA RTX PRO 6000 Blackwell GPUs, which was a clear strategic move toward premium AI and visualization workloads in a flagship workstation. These moves show that the workstation GPU market is being shaped as much by platform packaging and workflow targeting as by raw silicon competition.

A second strategic pattern is ecosystem control around enterprise AI. AMD and Nutanix announced a multi-year partnership in February 2026, backed by a USD 150 million AMD investment, to advance open enterprise AI platforms on AMD accelerated compute infrastructure. NVIDIA and Microsoft also announced a unified software stack for agentic AI deployment across Windows devices, cloud systems, and local workstations in May 2026, which connected workstation adoption more directly to enterprise developer workflows. That means the workstation GPU market is no longer being contested only through hardware benchmarks, because software paths, certification depth, and deployment convenience now shape the buying decision. Open space still exists in mobile workstation platforms for hybrid engineering teams, mid-range inference systems for smaller companies, and specialized professional systems for medical imaging and life sciences. Even so, the overall workstation GPU market remains constrained by supply and certification realities, which prevents any single competitive tactic from deciding the full landscape on its own.

Workstation GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Micro-Star International Co., Ltd.

ASUSTeK Computer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: BOXX Technologies launched the APEXX T3 workstation, featuring AMD Ryzen Threadripper 9000 processors, up to 64 cores, paired with NVIDIA RTX PRO 2000 Blackwell GPUs. The system targets demanding motion media and 3D content creation professionals, representing the first commercial workstation to incorporate NVIDIA's RTX PRO 2000 Blackwell GPU with 16 GB of GDDR7 memory and 17 TFLOPS of single-precision performance.

- May 2026: Lenovo announced the ThinkStation P4, the first workstation to combine AMD Ryzen PRO 9000 Series processors with NVIDIA RTX PRO 6000 Blackwell Workstation Edition GPUs, 96 GB GDDR7 ECC, achieving up to 4,000 AI TOPS. The system also introduced the first deployment of AMD 3D V-Cache technology in the professional desktop workstation segment, with availability in select markets from June 2026.

- May 2026: AMD expanded its Ryzen PRO 9000 Series processor lineup for workstations, introducing new high-performance SKUs designed to power next-generation professional desktop computing and announced availability in OEM systems starting in the second half of 2026.

- May 2026: NVIDIA and Microsoft announced a unified software stack for agentic AI deployment across Windows devices, cloud, and local workstations. The collaboration introduced NVIDIA RTX Spark and DGX Station for Windows, enabling enterprise developers to run frontier models of up to 1 trillion parameters on-premises using NVIDIA Blackwell-powered workstations.

Global Workstation GPU Market Report Scope

The Workstation GPU Market analyzes graphics processing units (GPUs) specifically designed for professional workstations. These GPUs are optimized for tasks such as 3D rendering, CAD (Computer-Aided Design), video editing, and other computationally intensive applications. The scope of the report includes market trends, growth drivers, challenges, competitive landscape, and forecasts for the study period.

The Workstation GPU Market Report is Segmented by Product Type (Desktop Workstation GPU, and Mobile Workstation GPU), Application (CAD, CAM and CAE, 3D Rendering and Visualization, Media Production and Content Creation, Scientific Computing and Simulation, Medical Imaging and Healthcare Visualization, AI Development and Data Science, and Other Applications), Organization Size (Small and Medium Enterprises, and Large Enterprises), Industry Vertical (Architecture, Engineering and Construction, Manufacturing and Industrial Design, Media and Entertainment, Automotive and Transportation, and Other Industry Verticals), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Desktop Workstation GPU |

| Mobile Workstation GPU |

| CAD, CAM and CAE |

| 3D Rendering and Visualization |

| Media Production and Content Creation |

| Scientific Computing and Simulation |

| Medical Imaging and Healthcare Visualization |

| AI Development and Data Science |

| Other Applications |

| Small and Medium Enterprises |

| Large Enterprises |

| Architecture, Engineering and Construction |

| Manufacturing and Industrial Design |

| Media and Entertainment |

| Automotive and Transportation |

| Other Industry Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Product Type | Desktop Workstation GPU | |

| Mobile Workstation GPU | ||

| By Application | CAD, CAM and CAE | |

| 3D Rendering and Visualization | ||

| Media Production and Content Creation | ||

| Scientific Computing and Simulation | ||

| Medical Imaging and Healthcare Visualization | ||

| AI Development and Data Science | ||

| Other Applications | ||

| By Organization Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Industry Vertical | Architecture, Engineering and Construction | |

| Manufacturing and Industrial Design | ||

| Media and Entertainment | ||

| Automotive and Transportation | ||

| Other Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the workstation GPU space?

The workstation GPU market size was USD 4.49 billion in 2025 and is projected to reach USD 12.15 billion by 2031, with an 18.45% CAGR from 2026 to 2031.

Which product category is leading demand for professional GPU systems?

Desktop workstation GPUs led revenue in 2025 with a 57.68% share because they still offer the best thermal headroom, expansion capacity, and support for heavy engineering workloads.

Which application is growing fastest in professional GPU adoption?

AI Development and Data Science is projected to expand at a 19.51% CAGR through 2031 as enterprises move more model fine-tuning and inference work to dedicated local systems.

Which buyer group contributes the most revenue today?

Large enterprises held 66.59% of revenue in 2025 because they can fund certified fleets, long support contracts, and secure on-premise AI and engineering workflows.

Which end-use sector is expanding fastest for workstation-class GPUs?

Automotive and Transportation is forecast to grow at a 20.18% CAGR through 2031 as vehicle makers expand digital twins, immersive design reviews, and virtual validation tools.

Which region offers the strongest growth outlook through 2031?

Asia-Pacific is expected to record the fastest regional growth at a 20.35% CAGR, supported by China’s substitution push, India’s AI services expansion, and demand from Japan and South Korea.

Page last updated on: