Industrial GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.18 Billion |

| Market Size (2031) | USD 12.09 Billion |

| Growth Rate (2026 - 2031) | 18.47% CAGR |

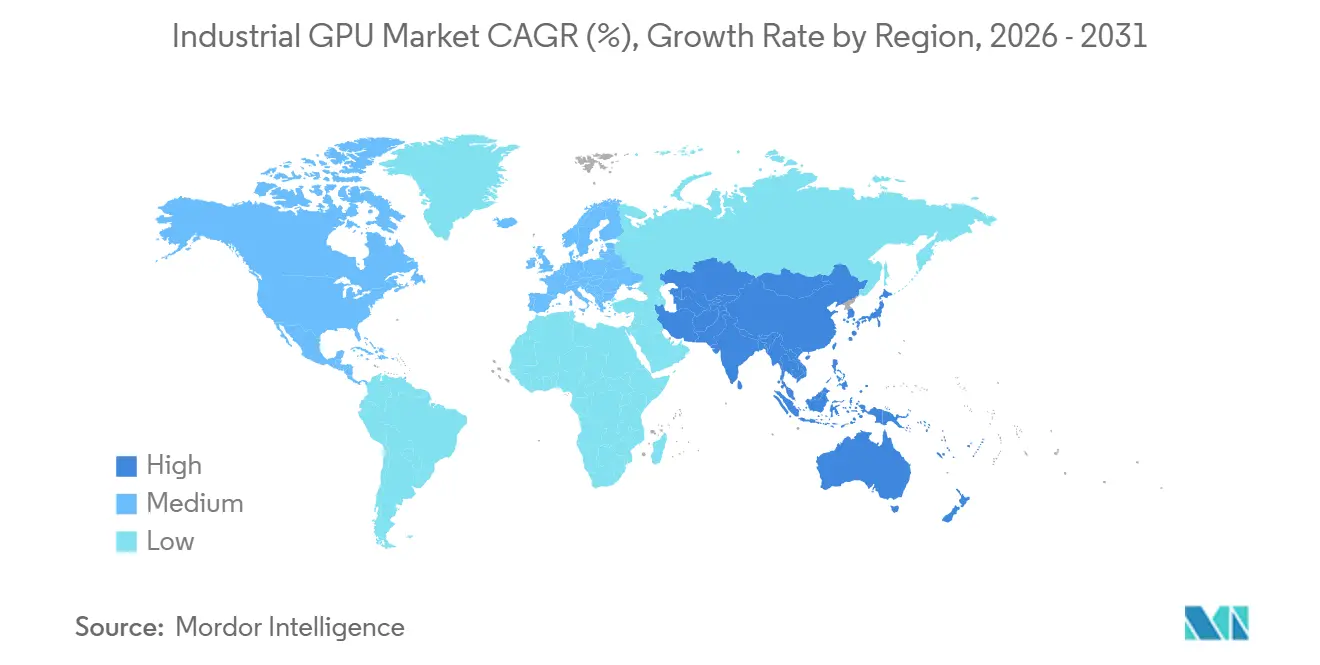

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

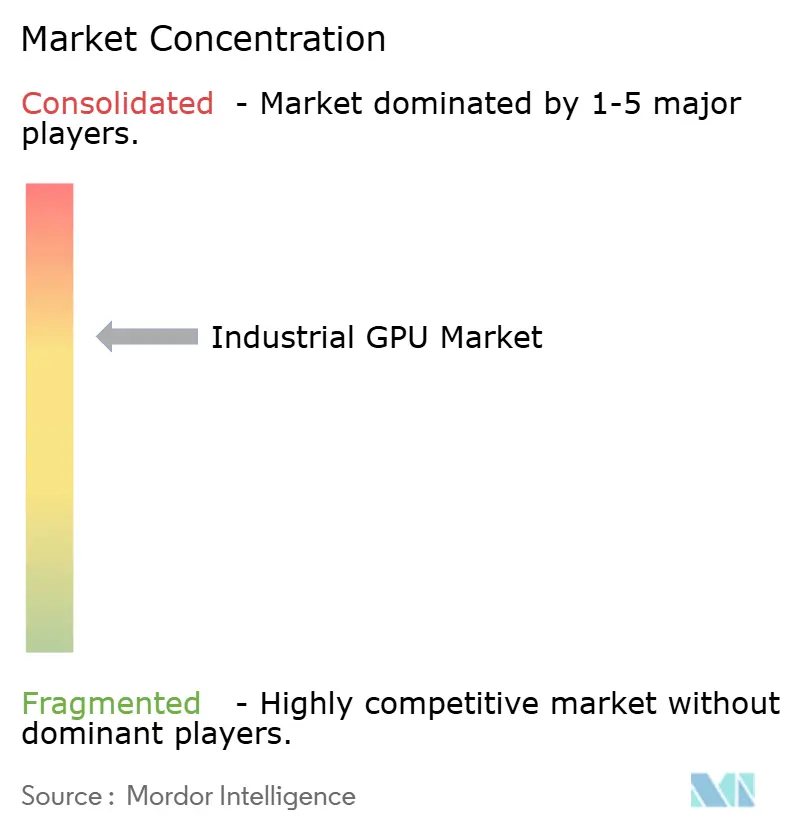

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial GPU Market Analysis by Mordor Intelligence

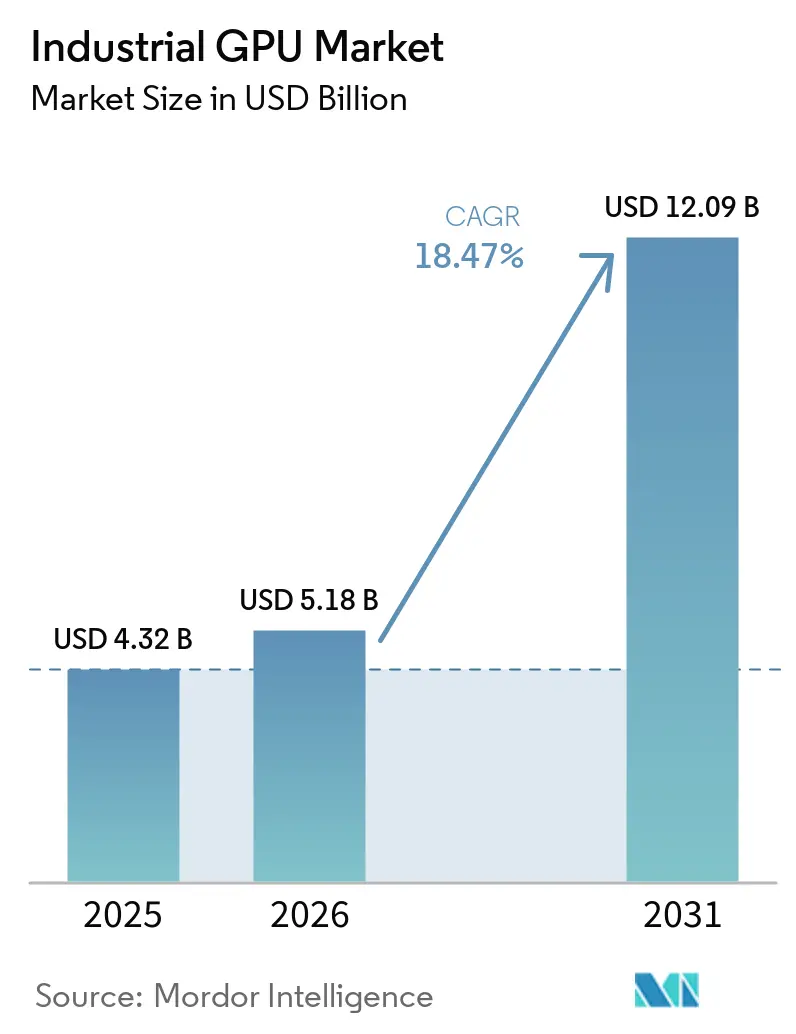

The industrial GPU market size is expected to increase from USD 4.32 billion in 2025 to USD 5.18 billion in 2026 and reach USD 12.09 billion by 2031, growing at a CAGR of 18.47% over 2026-2031. Growth is tied to the broader adoption of edge AI inference, real-time machine vision, and robotics orchestration in industrial settings where CPU-only systems do not meet response-time requirements. Procurement is also moving toward platforms that combine compute performance with safety readiness, thermal fit, and long lifecycle support, which is changing how automation OEMs qualify suppliers. Smart factory programs across Asia-Pacific are expanding the deployment base, while policy-led technology localization is creating separate procurement paths in China and Western-aligned markets. At the same time, advanced packaging bottlenecks and long certification cycles are slowing some high-performance deployments, which favors vendors that can offer integrated hardware, software, and compliance support. The competitive environment remains centered on a small group of silicon providers with strong software ecosystems, while opportunities continue to expand for embedded module makers, robotics platform vendors, and industrial system integrators.

Key Report Takeaways

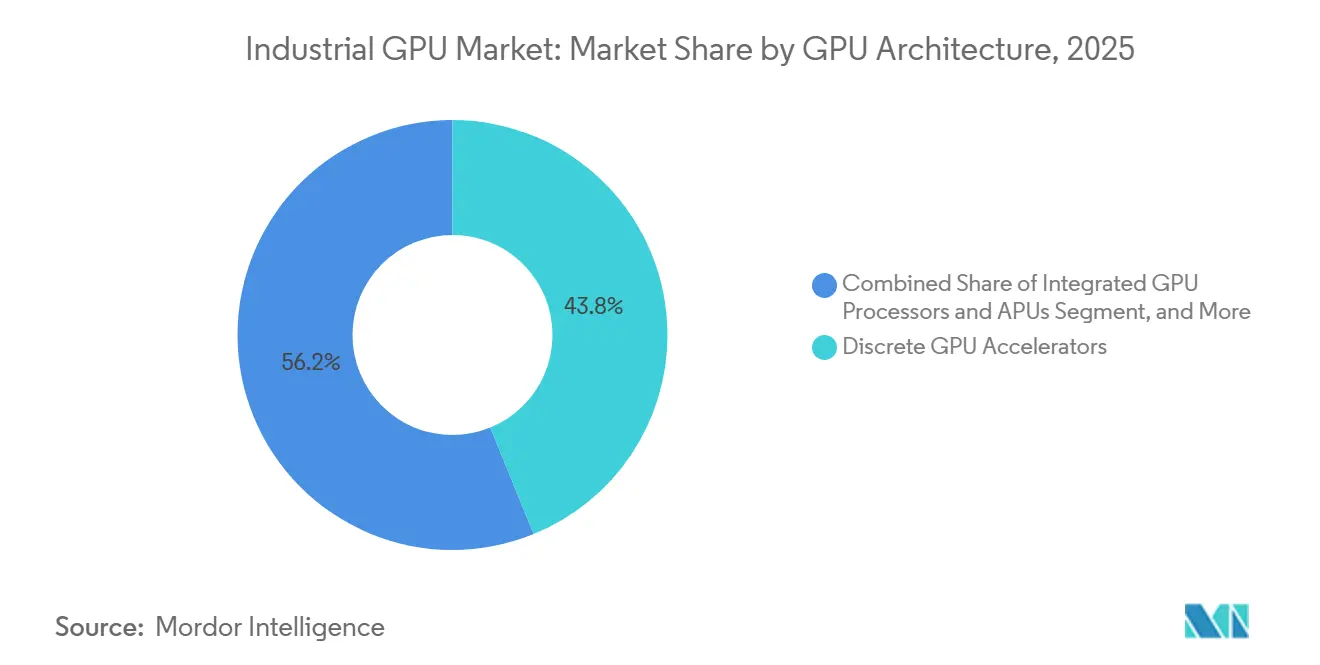

- By GPU architecture, discrete GPU accelerators held 43.84% share in 2025 for the industrial GPU market, while GPU-enabled heterogeneous edge SoCs are projected to expand at a 19.42% CAGR through 2031.

- By hardware form factor, PCIe add-in cards held 36.42% share in 2025, while SoMs and CoMs are projected to expand at a 19.64% CAGR through 2031.

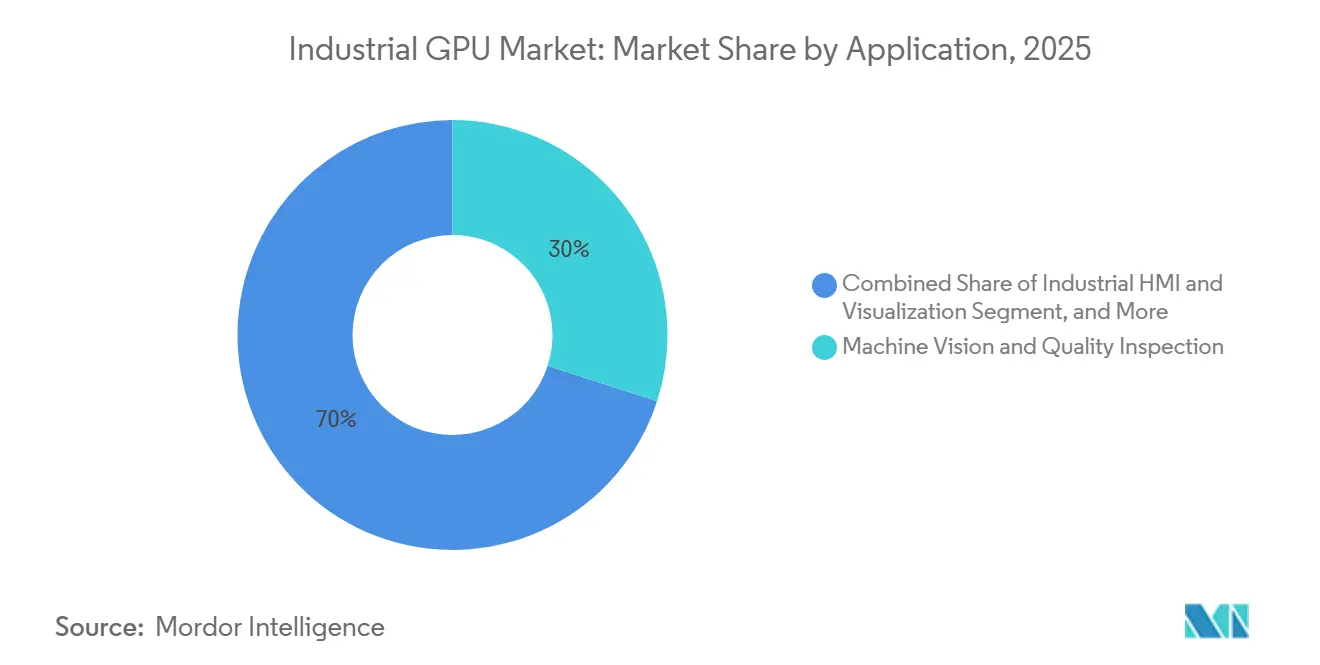

- By application, machine vision and quality inspection accounted for 29.98% of the industrial GPU market size in 2025, while robotics and autonomous material handling are projected to advance at a 19.59% CAGR through 2031.

- By end-user industry, manufacturing accounted for 44.12% of the industrial graphics processing unit (GPU) market in 2025, while logistics and warehousing are projected to expand at a 19.61% CAGR through 2031.

- By geography, Asia-Pacific held 46.63% of the industrial GPU market share in 2025 and is also projected to record the highest regional CAGR at 19.38% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial GPU Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Edge AI Inference Demand in Industrial Automation | +4.2% | Global, with concentrated gains in Asia-Pacific and North America | Short term (≤ 2 years) |

| Increasing Adoption of Discrete GPUs in High-Throughput Industrial Workloads | +3.3% | North America and Europe for brownfield retrofits, Asia-Pacific for greenfield projects | Short term (≤ 2 years) |

| Growing Deployment of Digital Twins and Simulation in Smart Factories | +2.8% | Asia-Pacific core, with spillover to Europe and North America | Medium term (2-4 years) |

| Expanding Use of Functional-Safety-Ready GPU Platforms in Robotics | +2.1% | Europe, North America, and Asia-Pacific | Medium term (2-4 years) |

| Rising Visualization Intensity in Machine Vision and Quality Inspection | +1.6% | Global, with early gains in automotive and electronics hubs | Short term (≤ 2 years) |

| Increasing Software-Defined Industrial Compute Architectures | +1.2% | North America and Europe as early movers, followed by Asia-Pacific | Long term (≥ |

| Source: Mordor Intelligence | |||

Rising Edge AI Inference Demand in Industrial Automation

The industrial GPU market is being reshaped by the movement of AI inference from centralized computing environments to production lines, inspection stations, and autonomous mobile systems. Physical AI workloads now combine visual reasoning, sensor fusion, and machine coordination, which places parallel processing at the center of industrial compute design.[1]NVIDIA, “NVIDIA Factory Operations Blueprint Gives Factories a New AI Brain,” NVIDIA Blog, blogs.nvidia.com NVIDIA positioned IGX Thor for industrial and medical edge deployments with real-time physical AI capabilities, showing how the industrial GPU market is shifting toward purpose-built edge platforms rather than adapted data center hardware. Cognex reinforced this direction in April 2026, when it launched the In-Sight 6900 Vision Controller powered by NVIDIA Jetson technology for edge AI inspection workloads. As deployments move closer to the line, buyers are treating GPU-based edge systems as core industrial infrastructure, not as temporary pilot tools, which supports longer, deeper procurement cycles across the industrial GPU market.

Increasing Adoption of Discrete GPUs in High-Throughput Industrial Workloads

Discrete accelerators remain central to the industrial GPU market because they let operators add compute capacity without replacing qualified server and industrial PC platforms. This modular path matters in retrofits, where every system change can trigger cost, downtime, and compliance work that plant teams try to avoid. Advantech supported this model in January 2026 with MIC-78 Series expansion modules for the MIC-780 modular industrial computer, including a PCIe Gen 5 GPU module for edge AI inference and machine vision up to 250W. The company extended that push in March 2026 with mass production of the SKY-MXM series based on NVIDIA RTX PRO Blackwell Embedded GPUs for compact, real-time, AI-intensive industrial systems. These launches show that the industrial GPU market is still rewarding form factors that combine upgrade flexibility, installed-base compatibility, and support for high-throughput inspection and simulation tasks.

Growing Deployment of Digital Twins and Simulation in Smart Factories

Digital twins are becoming a more important growth layer in the industrial GPU market as they move from design-stage visualization to live operational planning. NVIDIA stated in June 2025 that its industrial AI cloud initiative for European manufacturing would connect Omniverse-based digital twin tools across large factory networks, which reflects broader adoption of GPU-backed simulation workflows. That shift deepened in June 2026 when Micron and MetAI completed SimReady semiconductor fab twins on NVIDIA Omniverse OpenUSD libraries, enabling cleanroom-scale simulation with far greater model fidelity. As twin fidelity rises, industrial buyers must size GPU deployments for simulation memory and rendering loads, not just for inference at the edge. This is expanding the role of the industrial GPU market in planning, commissioning, and production-optimization programs that run in parallel with factory automation upgrades.

Expanding Use of Functional-Safety-Ready GPU Platforms in Robotics

Functional safety is becoming a stronger purchase criterion in the industrial GPU market as robots, autonomous vehicles, and intelligent machines assume more decision-making tasks near people and equipment. NVIDIA introduced IGX Thor with a Safety Island designed for IEC 61508 SIL 3 capability, demonstrating that performance is now packaged with safety architecture at the silicon and platform levels. NVIDIA expanded that push in June 2026 through Halos for Robotics, a full-stack functional safety system that joined hardware, operating software, and inspection workflows for physical AI deployments. Connect Tech followed in March 2026 with Tempo IGX, a robotics platform built on NVIDIA IGX and placed on a functional safety certification path for autonomous off-highway vehicles and industrial mobile robotics. This shift gives vendors with pre-assessed safety elements a stronger position in the industrial GPU market, as OEMs seek to shorten certification work and reduce redesign risk across long operating cycles.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Thermal and Power Constraints in Rugged Industrial Environments | -2.0% | Global, most acute in sealed outdoor and process-industry deployments | Short term (≤ 2 years) |

| Long Validation Cycles for Safety-Critical Industrial Deployments | -1.5% | Europe and North America, where certification regimes are stricter | Long term (≥ 4 years) |

| Fragmented Software Portability Across GPU Ecosystems | -1.1% | Global, with the greatest effect in multi-vendor deployments | Medium term (2-4 years) |

| Supply Chain Volatility in Advanced Semiconductor Packaging | -0.8% | Global, with concentration around advanced packaging capacity | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Thermal and Power Constraints in Rugged Industrial Environments

Thermal and power limits continue to hold back part of the industrial GPU market because many industrial environments were not built for data center-class accelerator profiles. Premio noted that industrial systems often operate over wide temperature ranges, in sealed enclosures, and under dust and vibration, all of which reduce usable headroom for high-performance GPU hardware.[2]Premio, “GPU Thermal Management for Industrial AI,” Premio, premioinc.com The same source also pointed to dust-related cooling losses that can degrade thermal performance over time, increasing the risk of throttling and shorter component lifespans in harsh deployments. This creates a design gap between the power draw of advanced AI accelerators and the lower thermal envelope that many rugged platforms can sustain. The industrial GPU market, therefore, continues to depend on specialized embedded systems, fanless designs, and careful workload balancing when deployments move beyond climate-controlled facilities.

Long Validation Cycles For Safety-Critical Industrial Deployments

Validation cycles remain a meaningful drag on the industrial GPU market because certified industrial systems cannot be refreshed at the same pace as mainstream compute hardware. NVIDIA stated in June 2026 that its AI Systems Inspection Lab and Halos framework were created to support inspection, assessment, and the reuse of safety workflows across physical AI systems. That progress helps, but it does not eliminate the lengthy review process for safety-critical robots, autonomous platforms, and machine control functions. Connect Tech's March 2026 move to place its Tempo IGX robotics platform on a functional safety certification path also shows that suppliers now compete not only on performance, but on how quickly they can guide integrators through compliance work. As a result, the industrial GPU market still favors larger vendors and better-funded OEMs that can absorb extended qualification timelines across product generations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By GPU Architecture: Discrete Accelerators Lead, But SoC Integration Is Advancing

Discrete GPU accelerators held a 43.84% share of the industrial GPU market in 2025, making them the leading architecture for line-side AI servers and rack-mounted edge systems. Their position reflects the practical advantage of modular upgrades, broad PCIe compatibility, and the ability to fit into existing industrial compute environments without a full redesign. In many brownfield plants, that flexibility reduces disruption and makes it easier to expand visual inspection, simulation, and AI control capacity in stages. The industrial GPU market still rewards that approach because many operators prefer incremental performance additions over full platform replacement. Even so, the segment is no longer defined solely by raw accelerator cards, as buyers increasingly evaluate power envelope, lifecycle support, and software integration simultaneously.

GPU-enabled heterogeneous edge SoCs are projected to expand at a 19.42% CAGR through 2031, indicating a faster shift toward compact integration at the edge. These devices combine a GPU, an NPU, image processing, and safety support into a single package that fits more easily into low-power industrial enclosures than larger discrete systems. AMD moved into this direction in January 2026 with the Ryzen AI Embedded P100 Series, which combined Zen 5 CPU cores, a 50-TOPS XDNA 2 NPU, and integrated Radeon graphics for machine vision IPCs, autonomous mobile robots, and 3D medical imaging. Integrated GPU processors and APUs remain important for supervisory visualization, HMI, and lighter inference tasks where capital budgets and thermal limits are tighter. Across the industrial GPU market, this mix shows that discrete systems still anchor performance-heavy use cases, while compact SoC designs are accelerating wherever deployment density, power control, and simplified qualification matter more.

By Hardware Form Factor: PCIe Cards Hold The Base While Modular Embedded Designs Scale Faster

PCIe add-in cards accounted for 36.42% of the market share in 2025, making them the largest hardware form factor in the industrial GPU market. Their strength lies in compatibility with existing industrial servers and the straightforward upgrade path they offer for rack-level machine vision, AI analytics, and simulation tasks. This is especially valuable in sites that want to raise compute density without changing the surrounding system architecture. Advantech's January 2026 MIC-78 GPU expansion module and its March 2026 SKY-MXM launch both showed continued investment in modular accelerator paths for industrial computing. That pattern suggests the industrial GPU market still depends heavily on standards-based cards where serviceability and installed-base fit remain high priorities.

SoMs and CoMs are projected to grow at a 19.64% CAGR through 2031, which makes them the fastest-growing form factor in the industrial GPU market. OEMs are moving toward standardized modules because they shorten development cycles and allow hardware refresh with less redesign effort than fully custom boards. Advantech's March 2026 rollout of GPU-rich embedded modules for compact industrial systems reflected that move toward higher density within tighter space envelopes. MXM and mezzanine graphics modules continue to serve rugged and transit-oriented applications where soldered-down interconnect stability matters, while single-board computers and carrier-board solutions stay relevant for cameras, gateways, and low-power edge nodes. Soldered-down GPU and SoC designs also have a place in high-volume products where bill-of-materials control and compact packaging matter more than field replaceability, broadening the form-factor spread across the industrial GPU market.

By Application: Machine Vision Anchors Revenue While Robotics Carries The Fastest Expansion

Machine vision and quality inspection accounted for 29.98% of the industrial GPU market in 2025, maintaining its position as the leading application. The installed base is broad because visual defect detection is often the first AI use case manufacturers adopt at scale. Cognex strengthened this segment in April 2026 with the In-Sight 6900 Vision Controller powered by NVIDIA Jetson technology for edge AI inspection. Cognex also stated in May 2026 that more than 100 manufacturing customers had progressed from single-line use to multi-site rollout through its OneVision environment, showing continued expansion of AI vision in production settings. That keeps machine vision as the main revenue driver in the industrial GPU market, even as other workloads improve performance.

Robotics and autonomous material handling are projected to grow at a 19.59% CAGR through 2031, which gives this application the fastest growth profile in the industrial GPU market. The segment is benefiting from physical AI frameworks that integrate perception, planning, and machine coordination on a single accelerated edge stack. NVIDIA's June 2026 Halos launch highlighted industrial robotics as a key target, with Agility Robotics deploying the system in Digit for industrial customers including Amazon, GXO, and Toyota Motor Manufacturing Canada. Digital twin and industrial simulation are also scaling, especially in semiconductors and automotive, while industrial HMI, edge AI analytics, predictive maintenance, and medical imaging continue to widen the application base for the industrial GPU market. This spread across visual inspection, autonomous movement, simulation, and control is broadening demand beyond a single-use deployment model in the industrial GPU market.

By End-User Industry: Manufacturing Leads While Logistics and Warehousing Expand Faster

Manufacturing accounted for 44.12% of the industrial GPU market in 2025, making it the largest end-user segment. Electronics assembly, automotive production, and complex process lines continue to be the deepest users of GPU-backed vision, simulation, and real-time control. This leadership is supported by the way GPUs move from stand-alone inspection tasks into broader factory operating layers. NVIDIA's industrial AI cloud initiative, launched in June 2025 with Schaeffler, BMW Group, and Siemens, demonstrated how digital twin and AI workflows are being linked across factory networks rather than confined to isolated cells. As a result, the industrial GPU market is becoming increasingly embedded in production planning, asset modeling, inspection, and machine coordination within manufacturing operations.

Logistics and warehousing are projected to expand at a 19.61% CAGR through 2031, which makes them the fastest-growing end-user segment. Growth is tied to the need for autonomous movement, high-speed sorting, and warehouse orchestration in environments where labor pressure and SKU complexity are persistent. NVIDIA's robotics safety rollout in June 2026 and its broader factory operations blueprint both point to heavier use of accelerated compute in material handling and facility coordination. Healthcare and life sciences, energy and utilities, and aerospace and defense remain established outlets for medical imaging, fault detection, radar processing, and other specialized compute tasks. Together, these verticals keep the industrial graphics processing unit (GPU) market diversified even though manufacturing and logistics remain the clearest growth centers.

Geography Analysis

Asia-Pacific held 46.63% share of the industrial GPU market size in 2025 and is projected to expand at a 19.38% CAGR through 2031. The region remains the largest deployment base because it combines dense electronics manufacturing, automotive production, semiconductor capacity, and aggressive factory modernization programs. Japan added to that momentum in February 2026, when SmartVision introduced the EAC-7000 Series, powered by NVIDIA Jetson Thor, for next-generation edge AI robotics. Hitachi also stated in April 2026 that its edge AI semiconductor work had moved into implementation for manufacturing, inspection, robotics, and logistics hardware, with energy efficiency gains of more than 10 times compared with general-purpose GPU processing.[3]Hitachi, “Hitachi Develops Edge AI Semiconductor as Physical AI Foundation Technology Supporting HMAX Industry,” Hitachi, hitachi.com These moves show why the industrial GPU market remains strongest in Asia-Pacific, where new factory programs and embedded hardware development continue to reinforce each other.

North America and Europe are the next two major regional clusters in the industrial GPU market, but their demand profiles differ from those in Asia-Pacific. North America benefits from a deep ecosystem around accelerated computing, robotics software, and simulation platforms that can be qualified across multiple industrial use cases. Europe places greater emphasis on safety-led procurement, especially in collaborative robotics, machine control, and regulated industrial environments, where stronger compliance pathways are required. NVIDIA's June 2025 industrial AI cloud initiative for European manufacturing highlighted how digital twin tools are being deployed across large manufacturing networks in the region. The industrial GPU market in both regions is therefore shaped less by sheer unit volume and more by certified deployment models, deep software integration, and long lifecycle platform support.

South America, the Middle East, and Africa remain smaller parts of the industrial graphics processing unit (GPU) market, but they matter because their use cases differ from the leading regions. In South America, mining, process industries, and distributed manufacturing sites create demand for predictive maintenance, machine vision, and edge systems that support remote support. In the Middle East and Africa, smart infrastructure, construction, logistics, and energy projects are creating early openings for GPU-enabled industrial automation. These markets are still developing, but they expand the industrial GPU market beyond climate-controlled factory settings and increase the need for rugged, power-aware, and deployment-specific hardware designs.

Competitive Landscape

The industrial GPU market is moderately consolidated at the silicon platform layer, but it remains fragmented across board integration, packaging, and embedded system assembly. NVIDIA continues to hold a strong position because it pairs hardware with a broad software stack that spans visual AI, robotics, sensor processing, and digital twins. That combination matters in the industrial GPU market because OEMs often prefer fewer validation points when they are building long-life systems. NVIDIA reinforced this position in October 2025 with IGX Thor, which combined high AI compute with a safety-oriented architecture and a 10-year lifecycle commitment for industrial and medical edge deployments.[4]NVIDIA, “NVIDIA IGX Thor Robotics Processor Brings Real-Time Physical AI to the Industrial and Medical Edge,” NVIDIA Blog, blogs.nvidia.com It widened that lead in June 2026 through Halos for Robotics, which turned safety from a chip feature into a broader platform and workflow offering for industrial customers.

Competition in the industrial GPU market also depends on which vendors can translate silicon roadmaps into deployable industrial form factors. Advantech showed an aggressive execution pace in 2026 through multiple launches across MIC-AI systems, SKY-MXM modules, IGX Thor platforms, and GPU expansion hardware for industrial edge computing. Cognex strengthened the machine vision layer with OneVision and the In-Sight 6900, which linked cloud-to-edge vision development with GPU-backed inspection hardware. Hitachi took a different route by advancing edge AI semiconductors focused on energy efficiency for industrial equipment, underscoring that competition in the industrial GPU market also comes from architectures designed to reduce power draw in embedded deployments. This leaves the market split between a few software-heavy platform leaders and a wide field of integrators that compete on packaging, thermal design, and application fit.

Another competitive feature of the industrial graphics processing unit (GPU) market is the rising importance of certification readiness as a barrier to entry. Vendors that can support IEC 61508, ISO 13849, and related inspection workflows have a clearer path into robotics, autonomous handling, and safety-sensitive machine intelligence. Connect Tech's March 2026 certification-path strategy for Tempo IGX reflected how system providers are trying to position themselves earlier in the compliance cycle. The result is an industrial GPU market in which switching costs rise after qualification, supporting platform concentration at the top while leaving room for many specialized embedded suppliers below.

Industrial GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Imagination Technologies Limited

Qualcomm Incorporated

Matrox Electronic Systems Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA launched Halos for Robotics, an industry-first full-stack functional safety system for physical AI integrating IGX Thor hardware with Halos OS, targeting IEC 61508 SIL 3 and ISO 13849 compliance. Agility Robotics became the first adopter, deploying Halos in its Digit humanoid for industrial customers including Amazon, GXO, and Toyota Motor Manufacturing Canada.

- June 2026: Micron and MetAI completed development of SimReady semiconductor fab twins on NVIDIA Omniverse OpenUSD libraries, enabling GPU-accelerated simulation of full cleanroom production environments at semiconductor scale.

- June 2026: NVIDIA announced the Factory Operations Blueprint (FOX) at GTC Taipei/Computex, a reference design for AI-driven factory manager agents that orchestrates vision inspection, material transport, and machine-to-machine coordination. Pegatron adopted the blueprint and reported an estimated 15% reduction in asset redundancy costs.

- May 2026: Cognex announced general availability of OneVision, its collaborative AI vision development environment, reporting over 100 manufacturing customers worldwide progressing from single-line applications to multi-site deployments since the June 2025 beta launch.

Global Industrial GPU Market Report Scope

The Industrial GPU Market comprises graphics processing units (GPUs), GPU-enabled computing platforms, and associated technologies deployed across industrial environments to accelerate artificial intelligence (AI), machine vision, automation, simulation, visualization, and edge computing workloads. Industrial GPUs provide high-performance parallel processing capabilities that enable real-time data analysis, advanced image processing, predictive analytics, autonomous operations, and digital transformation initiatives across manufacturing facilities, logistics networks, healthcare systems, energy infrastructure, and other industrial settings.

The Industrial GPU Market Report is Segmented by GPU Architecture (Discrete GPU Accelerators, Integrated GPU Processors and APUs, and GPU-Enabled Heterogeneous Edge SoCs), Hardware Form Factor (PCIe Add-In Cards, MXM and Mezzanine Graphics Modules, System-on-Modules and Computer-on-Modules, Single-Board Computers and Embedded GPU Carrier Boards, and Soldered-Down GPU/SoC Solutions), Application (Machine Vision and Quality Vision, Robotics and Autonomous Material Handling, Digital Twin and Industrial Simulation, Industrial HMI and Visualization, and Edge AI Analytics and Predictive Maintenance, and Medical and Critical Imaging), End-User Industry (Manufacturing, Logistics and Warehousing, Healthcare and Life Sciences, Energy and Utilities, Aerospace and Defense, Other End-User Industries), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Discrete GPU Accelerators |

| Integrated GPU Processors and APUs |

| GPU-Enabled Heterogeneous Edge SoCs |

| PCIe Add-In Cards |

| MXM and Mezzanine Graphics Modules |

| System-on-Modules and Computer-on-Modules |

| Single-Board Computers and Embedded GPU Carrier Boards |

| Soldered-Down GPU/SoC Solutions |

| Machine Vision and Quality Inspection |

| Robotics and Autonomous Material Handling |

| Digital Twin and Industrial Simulation |

| Industrial HMI and Visualization |

| Edge AI Analytics and Predictive Maintenance |

| Medical and Critical Imaging |

| Manufacturing |

| Logistics and Warehousing |

| Healthcare and Life Sciences |

| Energy and Utilities |

| Aerospace and Defense |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By GPU Architecture | Discrete GPU Accelerators | |

| Integrated GPU Processors and APUs | ||

| GPU-Enabled Heterogeneous Edge SoCs | ||

| By Hardware Form Factor | PCIe Add-In Cards | |

| MXM and Mezzanine Graphics Modules | ||

| System-on-Modules and Computer-on-Modules | ||

| Single-Board Computers and Embedded GPU Carrier Boards | ||

| Soldered-Down GPU/SoC Solutions | ||

| By Application | Machine Vision and Quality Inspection | |

| Robotics and Autonomous Material Handling | ||

| Digital Twin and Industrial Simulation | ||

| Industrial HMI and Visualization | ||

| Edge AI Analytics and Predictive Maintenance | ||

| Medical and Critical Imaging | ||

| By End-User Industry | Manufacturing | |

| Logistics and Warehousing | ||

| Healthcare and Life Sciences | ||

| Energy and Utilities | ||

| Aerospace and Defense | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast size of the industrial GPU market?

The industrial GPU market was valued at USD 4.32 billion in 2025, is expected to reach USD 5.18 billion in 2026, and is forecast to reach USD 12.09 billion by 2031 at a CAGR of 18.47%.

Which application generates the most revenue in industrial GPU deployments?

Machine vision and quality inspection led in 2025 with 29.98% share, reflecting the wide use of GPU-backed visual defect detection in manufacturing environments.

Which industrial GPU application is growing the fastest through 2031?

Robotics and autonomous material handling is projected to record the fastest growth at a 19.59% CAGR, supported by rising use of physical AI, autonomous systems, and safety-ready edge platforms.

Which end-user group leads demand for industrial GPU solutions?

Manufacturing remained the largest end-user in 2025 with 44.12% share, driven by electronics assembly, automotive production, and digital twin use across factory operations.

Which region is leading adoption of industrial GPU platforms?

Asia-Pacific led the industrial GPU market in 2025 with 46.63% share and is also expected to post the highest regional CAGR at 19.38% through 2031.

What is shaping competition among industrial GPU vendors in 2026?

Competition is being shaped by full-stack software ecosystems, safety certification readiness, thermal design capability, and the ability to convert silicon advances into deployable industrial form factors.

Page last updated on: