Hyperscale Data Center Graphics Processing Unit (GPU) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

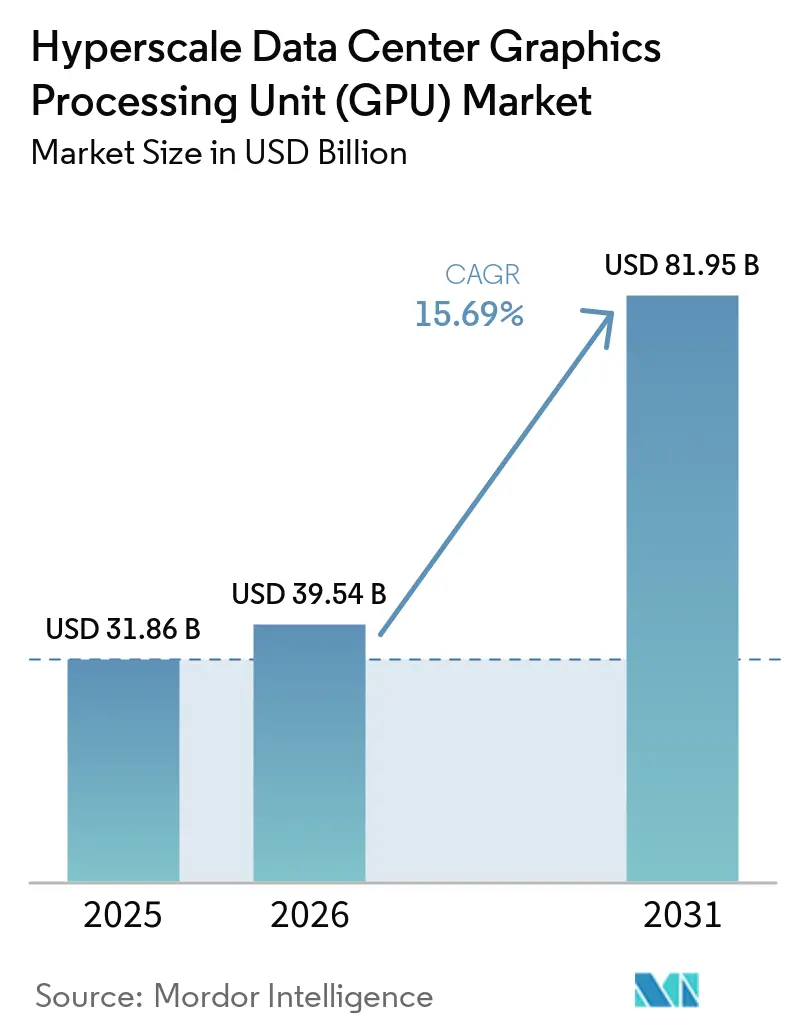

| Market Size (2026) | USD 39.54 Billion |

| Market Size (2031) | USD 81.95 Billion |

| Growth Rate (2026 - 2031) | 15.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hyperscale Data Center Graphics Processing Unit (GPU) Market Analysis by Mordor Intelligence

The Hyperscale data center GPU market size is projected to expand from USD 31.86 billion in 2025 and USD 39.54 billion in 2026 to USD 81.95 billion by 2031, registering a 15.69% CAGR between 2026 and 2031. Explosive spending on generative AI training clusters, the mainstreaming of cloud inference services, and accelerating edge deployments together anchor this outsized trajectory. Cloud data centers absorbed most 2025 demand, yet incremental capacity is now shifting toward micro-edge nodes as hyperscalers chase single-digit-millisecond latency targets for autonomous systems and cloud gaming. Advances in high-bandwidth interconnects, liquid cooling, and chiplet-based packaging are dismantling memory and thermal bottlenecks that once limited cluster scale. Meanwhile, custom accelerators from Microsoft, AWS, and Google are broadening the supply base without eroding the software gravity that still pins enterprises to NVIDIA’s CUDA ecosystem.

Key Report Takeaways

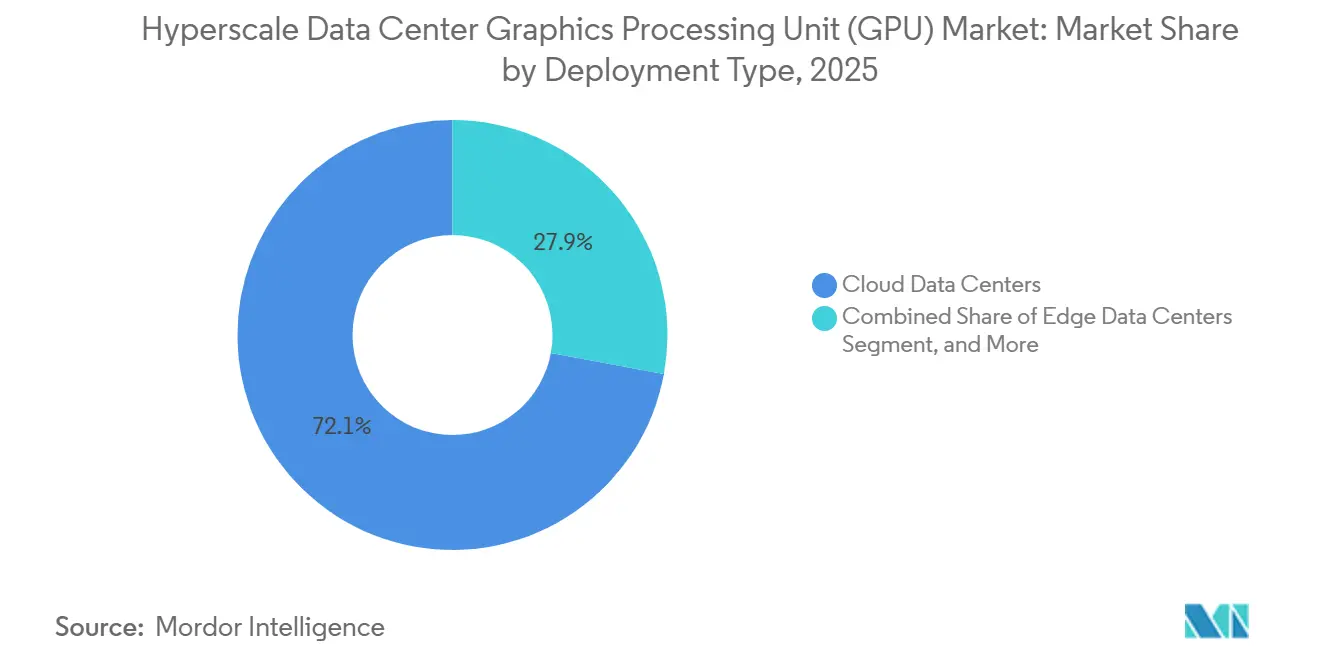

- By deployment type, cloud data centers led with a 72.1% share of the Hyperscale data center GPU market in 2025; edge data centers are forecast to grow at a 19.3% CAGR through 2031.

- By GPU type, training devices accounted for 56.7% of the Hyperscale data center GPU market in 2025, while inference GPUs are advancing at a 18.5% CAGR through 2031.

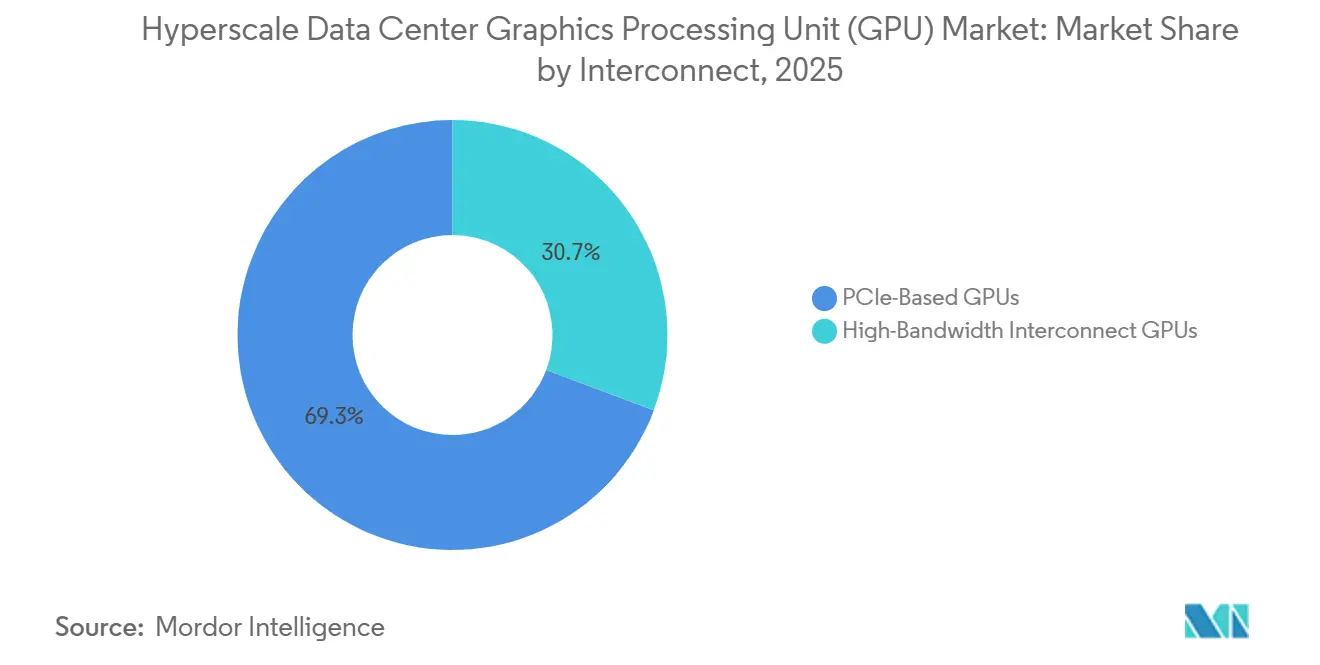

- By interconnect, PCIe-based GPU solutions held 69.3% of the Hyperscale data center GPU market share in 2025, but high0bandwidth interconnect GPUs are expanding at an 18.1% CAGR during 2026-2031.

- By workload type, artificial intelligence and machine learning dominated the Hyperscale data center GPU market in 2025, accounting for 44.2%, whereas graphics and visualization workloads are set to post a 19.2% CAGR through 2031.

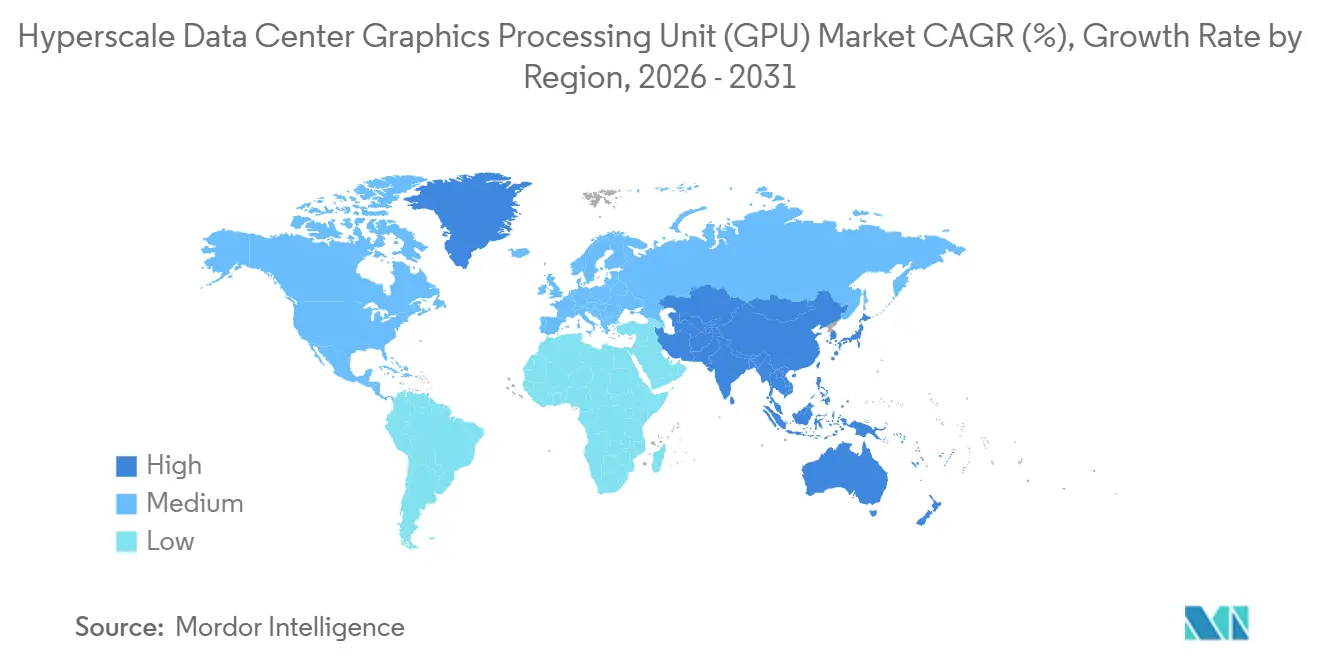

- By Geography, North America commanded 42.8% of the 2025 revenue share in the Hyperscale data center GPU market; Asia-Pacific is expected to register a 17.8% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hyperscale Data Center Graphics Processing Unit (GPU) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of AI and ML Workloads in Cloud Data Centers | +4.2% | Global, concentrated in North America and Asia-Pacific | Long term (≥ 4 years) |

| Rapid Scaling of Generative AI Model Training Clusters | +3.8% | North America and Europe, expanding into Asia-Pacific | Medium term (2-4 years) |

| Transition Toward Heterogeneous Computing Architectures | +2.1% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Growing Demand for Cloud Gaming and 3-D Graphics Workloads | +1.6% | Urban centers in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Emergence of Chiplet-Based Disaggregated GPU Designs | +1.4% | Global, led by U.S. and Asian semiconductor hubs | Long term (≥ 4 years) |

| Adoption of Liquid Cooling for High-Density GPU Racks | +0.9% | Global, acute in regions with energy regulations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation Of AI And ML Workloads In Cloud Data Centers

Cloud platforms have converted GPUs from specialist accelerators into baseline infrastructure. New AI-optimized virtual machines on Microsoft Azure and Trainium2 instances on AWS lowered entry barriers for enterprise customers migrating legacy machine-learning pipelines. Capital allocations reflect permanence rather than experimentation; Meta reserved USD 65 billion for AI compute in 2026, chiefly for multimodal training clusters. Power density has surged 10-20-fold versus traditional servers, forcing data-center redesigns that integrate rack-level liquid cooling and revised power distribution. Workload diversity now spans vision, recommendation, and autonomy, each demanding a mix of inference-optimized cards and training-grade units, ensuring the Hyperscale data center GPU market remains on a structurally rising curve.[1]AWS Staff, “Trainium2 Extends Choice in AWS AI Instances,” Amazon Web Services Blog, aws.amazon.com

Rapid Scaling of Generative AI Model Training Clusters

Parameter growth from billions to trillions is compelling operators to assemble petaflop-scale clusters. xAI’s Memphis complex is scaling toward 1 million GPUs by 2027, and Mistral AI’s Paris facility replicates this model in Europe. Centralization maximizes equipment utilization and amortizes capex across successive model iterations, but only hyperscalers can fund the USD-billion class builds. Technically, liquid cooling and fabrics such as NVLink 5.0 cut inter-GPU latency below one microsecond, allowing 70-plus-GPU trays to appear as a single logical device. The result is a multiplier effect on the Hyperscale data center GPU market, with every uplift in model size translating to a disproportionate lift in cluster capacity.[2]Nicolas Chapuy, “Mistral AI Unveils Paris GPU Megacenter,” Mistral AI Blog, mistral.ai

Transition Toward Heterogeneous Computing Architectures

Data centers are abandoning uniform server fleets in favor of blended nodes that match compute engines to workload phases. AMD’s MI300X combines CPU and GPU chiplets, while Intel’s Gaudi 3 targets transformer training with an open-software stack. Custom silicon from hyperscalers, Google’s TPU v5p and AWS Graviton plus Inferentia, adds further heterogeneity. Operators can therefore allocate premium training GPUs where bandwidth is critical, and cheaper accelerators for preprocessing or edge inference, trimming the total cost of ownership. This architectural evolution secures a multi-device future for the Hyperscale data center GPU market while diluting single-vendor dependency.[3]Mark Papermaster, “AMD MI300X Launch Highlights Heterogeneous Integration,” AMD Corporate Blog, amd.com

Growing Demand for Cloud Gaming And 3-D Graphics Workloads

Cloud gaming exited its experimental phase once membership on GeForce NOW crossed the 100 million mark. Real-time rendering demands different silicon blocks, ray-tracing cores and variable-rate shading, than matrix-centric AI chips. Xbox Cloud Gaming and Sony’s PlayStation Plus are rolling out edge facilities within 20 milliseconds of users, prompting hyperscalers to drop graphics-optimized GPUs in metro micro-pods. Latency economics, therefore, diversify deployment patterns even as centralized AI train clusters swell, and they place a fresh ceiling on legacy PCIe interconnects. The outcome is sustained, diversified volume for the Hyperscale data center GPU market across both training and visualization domains.[4]Janet Haas, “GeForce NOW Surpasses 100 M Members,” NVIDIA Blog, nvidia.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure for Hyperscale GPU Clusters | -1.8% | Global, peak in North America and Europe | Medium term (2-4 years) |

| Supply Chain Bottlenecks in Advanced Packaging and HBM | -1.5% | Asia-Pacific manufacturing hubs, global impact | Short term (≤ 2 years) |

| Rising Regulatory Pressure on Data-Center Energy Use | -0.8% | Europe, North America, Singapore | Long term (≥ 4 years) |

| Geopolitical Export Controls Limiting GPU Availability | -0.7% | China, Russia, restricted markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for Hyperscale GPU Clusters

A single rack of Blackwell GB200 NVL72 lists between USD 3 million and USD 4 million before facility costs. Oracle’s USD 6.5 billion rollout underlines the minimum price of admission, while recurring power bills can hit USD 10 million per year for a 10 MW cluster. Utilization averaging 60%-70% obliges providers to overbuild capacity, extending payback periods, and squeezing mid-tier clouds. Consequently, only the largest operators with access to low-cost renewable energy can compete at the training frontier, tempering near-term growth for the Hyperscale data center GPU market.

Supply Chain Bottlenecks in Advanced Packaging and HBM

HBM3 and HBM4 remain scarce despite foundry expansions. TSMC’s CoWoS lines are fully booked through 2026, stretching GPU lead times past nine months. Secondary markets for previous-generation H100 cards retain high resale values because supply trails demand by up to 40%. While Samsung’s GDDR7 provides a stopgap for inference, its bandwidth ceiling disqualifies it from large-model training. Short-run shortages, therefore, act as a brake on otherwise explosive demand in the Hyperscale data center GPU market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Edge Acceleration Outpaces Cloud Consolidation

Edge facilities captured a 19.3% CAGR outlook versus mid-teens growth for centralized hyperscale hubs, reflecting the widening role of real-time inference in vehicles, smart-city sensors, and industrial robotics. The Hyperscale data center GPU market size linked to cloud sites remains dominant, yet its share inches lower as operators like AWS Outposts deliver cloud management on-premises. In practice, a dual-architecture equilibrium is emerging where 100-MW mega-facilities train trillion-parameter models while 1-MW micro-pods push decisions to within 10 ms of users.

Capital allocation favors both ends of the spectrum. Amazon’s USD 200 billion through 2030 addresses mega-sites, whereas NVIDIA’s IGX Orin shipments illustrate strong OEM appetite for edge appliances. Financial services and healthcare firms keep modest private clusters to satisfy data-sovereignty rules, a niche that still feeds the wider Hyperscale data center GPU market. As utilization analytics improve, some inference loads are expected to bounce between edge and core depending on regional demand curves.

By GPU Type: Training Dominance Meets Inference Efficiency

Training-grade boards accounted for 56.7% of revenue in 2025, anchoring the cash flow engine for vendors. Yet inference-centric devices with lower precision and power budgets are growing rapidly, aided by hyperscaler in-house silicon. Inference GPUs should grow 18.5% annually, mirroring the doubling cadence of model sizes that force disaggregation across thousands of cards.

The Hyperscale data center GPU market size for inference hardware remains smaller but could exceed 40% of the total value by 2031 if conversational AI, retrieval-augmented generation, and real-time co-pilots permeate mainstream software. NVIDIA’s L4, AWS Inferentia2, and Google TPU v5e exemplify the economics: fewer flops per watt but superior cost per request. Training clusters, then, reprioritize cutting-edge memory bandwidth, securing a two-tier product mix in which last-year silicon enjoys a lucrative afterlife as an inference workhorse.

By Interconnect: Legacy PCIe Yields To Fabric Architectures

PCIe sockets still populated 69.3% of boards in 2025 because they slot easily into standard servers, a comfort factor for enterprise IT teams. However, High-bandwidth interconnect multi-petabyte-per-second fabrics such as NVLink and InfiniBand are indispensable once cluster scale rises above 8 GPUs. These fabrics, bundled with Blackwell and Hopper systems, sustain an 18.1% CAGR, pulling total Hyperscale data center GPU market revenue along.

Hyperscalers layer proprietary networks, Google’s optical links, AWS Elastic Fabric Adapter, over merchant fabric to shave microseconds and protect intellectual property. Edge servers remain PCIe for cost and simplicity, but their share erodes as even regional pods experiment with compact NVLink bridges that elevate small-form clusters into multi-node trainers.

By Workload Type: AI Dominance Coexists With Graphics Resurgence

AI and ML streams booked 44.2% of 2025 spending, yet graphics and visualization spooled a headline 19.2% CAGR that keeps demand diversified. Real-time ray tracing for 4K-120 fps gaming couples GPU cores with different tensor units, and platform operators are unwilling to compromise either set of capabilities.

High-performance computing is blurring into AI-accelerated simulation, while GPU-accelerated analytics lowers query times on petabyte datasets. Consequently, SKU portfolios now bundle tensor, RT, and CUDA cores in configurable ratios. This functional fusion broadens application reach, pulling incremental users and their budgets into the Hyperscale data center GPU market.

Geography Analysis

North America retained a 42.8% revenue share in 2025 and continues to wield unparalleled purchase power as Amazon, Microsoft, Google, and Meta funnel USD-hundreds-of-billions into AI capacity. Export controls that restrict top-tier GPU shipments to China inadvertently redirect a larger slice of the limited supply toward domestic sites, bolstering the region’s command of the Hyperscale data center GPU market. Canadian clusters in Toronto and Montreal enjoy low-cost hydroelectricity and university-sourced talent, while Mexico’s budding near-shoring economy is catalyzing edge nodes tailored to logistics robotics.

Asia-Pacific is the fastest riser at a forecast 17.8% CAGR. China’s home-grown Ascend 910C fills the void left by U.S. sanctions, allowing Alibaba, Tencent, and Baidu to keep pace in large language model rollouts. Japan’s JPY 2 trillion subsidy pool (USD 13.4 billion) underwrites domestic clusters, and South Korea leverages HBM leadership for vertical integration spanning memory through accelerator. India’s metro triad, Bangalore, Hyderabad, Mumbai, anchors sovereign AI ambitions, while Southeast Asian capitals harvest fresh edge deployments after Singapore partially lifted its data-center freeze.

Europe’s prospects hinge on stringent energy directives that cap PUE at 1.3 for new builds. Germany and the Nordics retrofit facilities with immersion and rear-door cooling to host high-density racks. The United Kingdom’s AI Safety Institute buys 5,000 GPUs to audit frontier models, while France’s Mistral AI plants a Blackwell campus inside Paris’s city limits. Renewable abundance lures operators to southern Spain and Italy, although deployment timelines remain tied to grid-upgrade schedules. Other regions, South America and the Middle East and Africa, collectively account for less than one-tenth of current value, yet Saudi Arabia’s USD 20 billion NEOM blueprint and South Africa’s Johannesburg edge pods foreshadow pockets of high-growth demand that will enrich the global Hyperscale data center GPU market footprint.

Competitive Landscape

NVIDIA commands a significant share of training revenue through an unmatched combination of silicon roadmaps, CUDA lock-in, and Mellanox networking bundling. Blackwell GB200 quadruples Hopper throughput, and the 2027 Rubin architecture promises a further 2.5× leap, sustaining a treadmill effect that nudges customers into annual refreshes. Custom chips, Microsoft Maia, AWS Trainium2, Google TPU v5p, handle about 15%-20% of internal hyperscaler workloads but rarely reach the open cloud, so they chip away at wallet share rather than mind share in the Hyperscale data center GPU market.

AMD is the leading merchant challenger, combining CPU and GPU chiplets to support heterogeneous workloads that integrate vector math with scalar preprocessing. Intel’s Gaudi 3 offers competitive transformer speeds within an open-software context, attracting early adopters willing to rewrite kernels. Start-ups such as Cerebras and Groq carve niches in wafer-scale training and streaming inference, respectively. OEMs Super Micro and Dell differentiate via turnkey, liquid-cooled rack solutions that ship within 45 days, compressing deployment timetables that historically stretched to quarters.

Regulation is now a strategic variable: U.S. export rules split the market into unrestricted and compliance-reduced SKUs, prompting NVIDIA’s H20 line for China and accelerating Huawei’s push into Ascend accelerators. Intellectual-property moves mirror hardware battles; NVIDIA’s December 2024 patent on chiplet-based disaggregation signals an intent to modularize future parts, a tactic that also aids yield. Net-net, elevated concentration persists, but the expanding Hyperscale data center GPU market value pool allows multiple silicon designs to coexist without catastrophic pricing compression.

Hyperscale Data Center Graphics Processing Unit (GPU) Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Amazon Web Services, Inc.

Google LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: OpenAI and NVIDIA revealed a USD 500 billion pact to build the 10 gigawatt Stargate data center, slated to host over 1 million GPUs for next-gen model development.

- January 2026: Mistral AI announced a Parisian facility fitted with Blackwell GB200 NVL72 systems, targeting late-2026 completion.

- December 2025: xAI doubled its Memphis Colossus supercomputer to 200,000 GPUs, on course for 1 million units by 2027.

- November 2025: Meta earmarked USD 65 billion for 2026 AI compute, a 40% uptick on 2024 outlays.

Global Hyperscale Data Center Graphics Processing Unit (GPU) Market Report Scope

The Hyperscale Data Center GPU Market Report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, Edge Data Centers), GPU Type (Training GPUs, Inference GPUs), Interconnect (PCIe-Based GPUs, High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, Data Analytics, Graphics and Visualization), and Geography (North America, Europe, Asia-Pacific, South America, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

| Cloud Data Centers |

| Enterprise / Private Data Centers |

| Edge Data Centers |

| Training GPUs |

| Inference GPUs |

| PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs |

| Artificial Intelligence (AI) and Machine Learning (ML) |

| High-Performance Computing (HPC) |

| Data Analytics |

| Graphics and Visualization |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Deployment Type | Cloud Data Centers | |

| Enterprise / Private Data Centers | ||

| Edge Data Centers | ||

| By GPU Type | Training GPUs | |

| Inference GPUs | ||

| By Interconnect | PCIe-Based GPUs | |

| High-Bandwidth Interconnect GPUs | ||

| By Workload Type | Artificial Intelligence (AI) and Machine Learning (ML) | |

| High-Performance Computing (HPC) | ||

| Data Analytics | ||

| Graphics and Visualization | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Hyperscale data center GPU market by 2031?

It is forecast to reach USD 81.95 billion by 2031, expanding at a 15.69% CAGR.

Which deployment environment will grow fastest over the next five years?

Edge data centers are expected to post a 19.3% CAGR through 2031 as latency-sensitive applications proliferate.

Who dominates training GPUs today?

NVIDIA holds an estimated 80%-85% share of training revenue, maintained by its CUDA software ecosystem.

How severe are supply chain bottlenecks for HBM?

Demand outstripped supply by up to 40% in 2025, pushing GPU lead times to nine months and supporting a buoyant resale market.

Which region is likely to record the highest CAGR?

Asia-Pacific is projected to expand at a 17.8% CAGR, propelled by sovereign AI initiatives in China, Japan, South Korea, and India.

Are custom accelerators replacing NVIDIA in the cloud?

Microsoft Maia, AWS Trainium2, and Google TPU v5p now handle 15%-20% of internal hyperscaler workloads but have not disrupted NVIDIA's merchant market dominance.

Page last updated on: