GPU Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

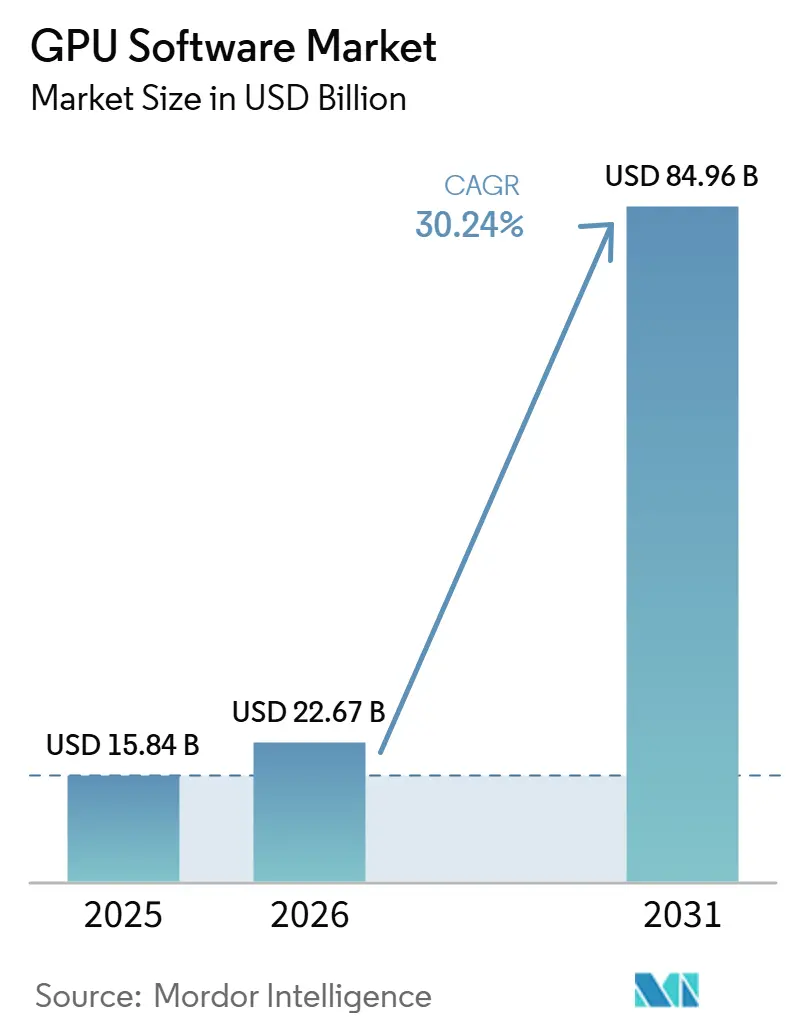

| Market Size (2026) | USD 22.67 Billion |

| Market Size (2031) | USD 84.96 Billion |

| Growth Rate (2026 - 2031) | 30.24% CAGR |

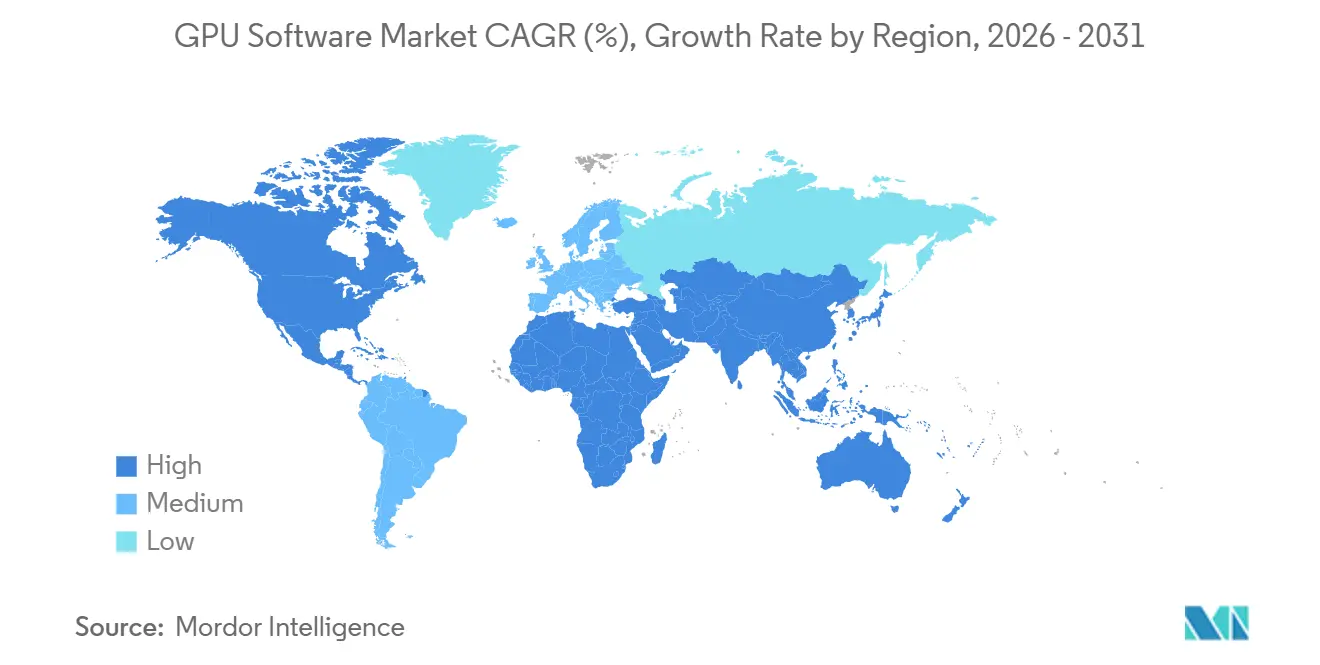

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

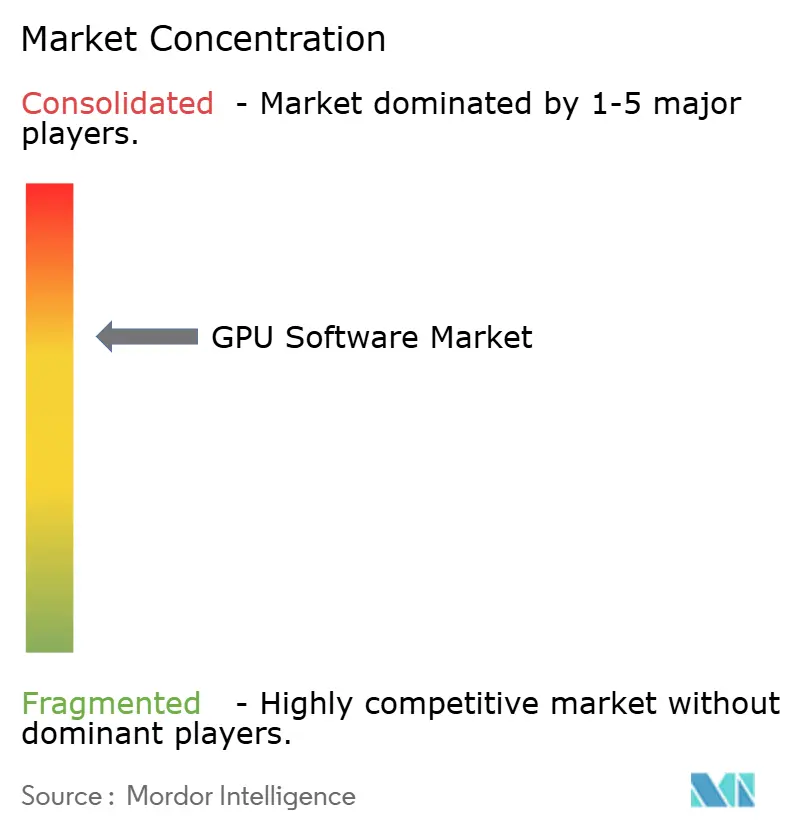

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GPU Software Market Analysis by Mordor Intelligence

The GPU software market size is expected to increase from USD 15.84 billion in 2025 to USD 22.67 billion in 2026 and reach USD 84.96 billion by 2031, growing at a CAGR of 30.24% over 2026-2031. Growth in the GPU software market is increasingly tied to recurring software licensing, managed orchestration services, and inference optimization frameworks rather than one-time hardware purchases. Enterprise AI spending remains the main demand base, and that spending is making software control layers more important because they shape utilization, cost, and deployment speed across large GPU estates. Competition is also shifting toward the software layer, where developer ecosystems, libraries, and workflow familiarity create stronger switching costs than hardware benchmarks alone. Export controls on advanced GPUs to China remain a near-term constraint, while they also encourage the development of alternate software stacks that may gradually split parts of the global ecosystem. At the same time, agentic AI workloads are creating demand for new middleware that can manage persistent GPU memory use and low-latency runtime behavior at production scale.

Key Report Takeaways

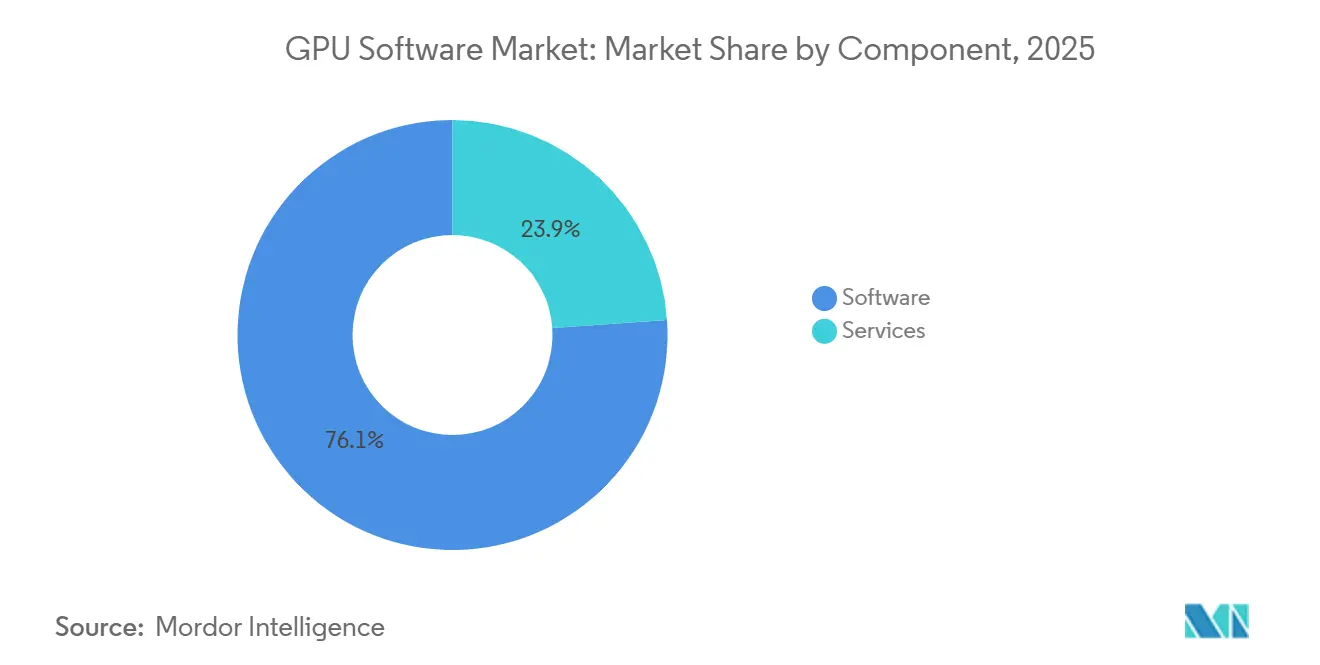

- By component, software held 76.11% share of the GPU software market in 2025, and software is also projected to expand at 31.21% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 45.33% of revenue in 2025, while hybrid cloud and private cloud is projected to record the fastest growth at 31.62% CAGR through 2031.

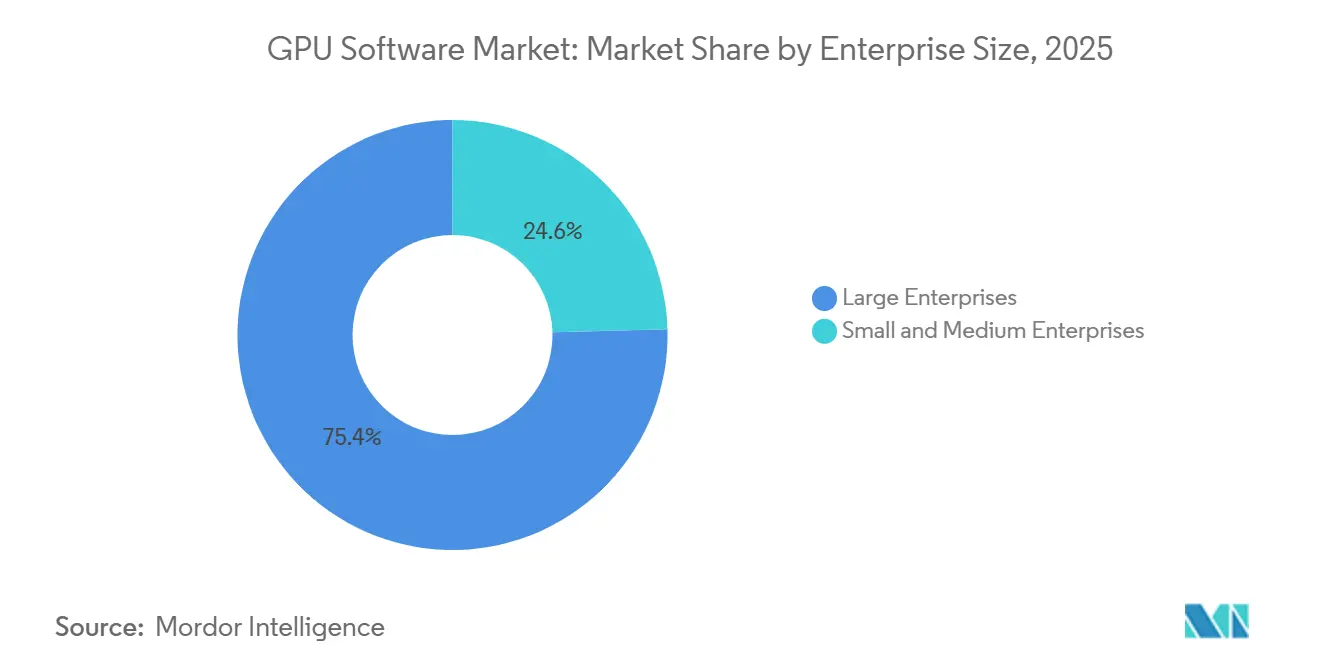

- By enterprise size, large enterprises represented 75.42% of revenue in 2025, while small and medium enterprises are projected to grow at 31.53% CAGR through 2031.

- By application, artificial intelligence and machine learning captured 52.12% share of GPU software market in 2025, while the same segment is projected to expand at 31.32% CAGR through 2031.

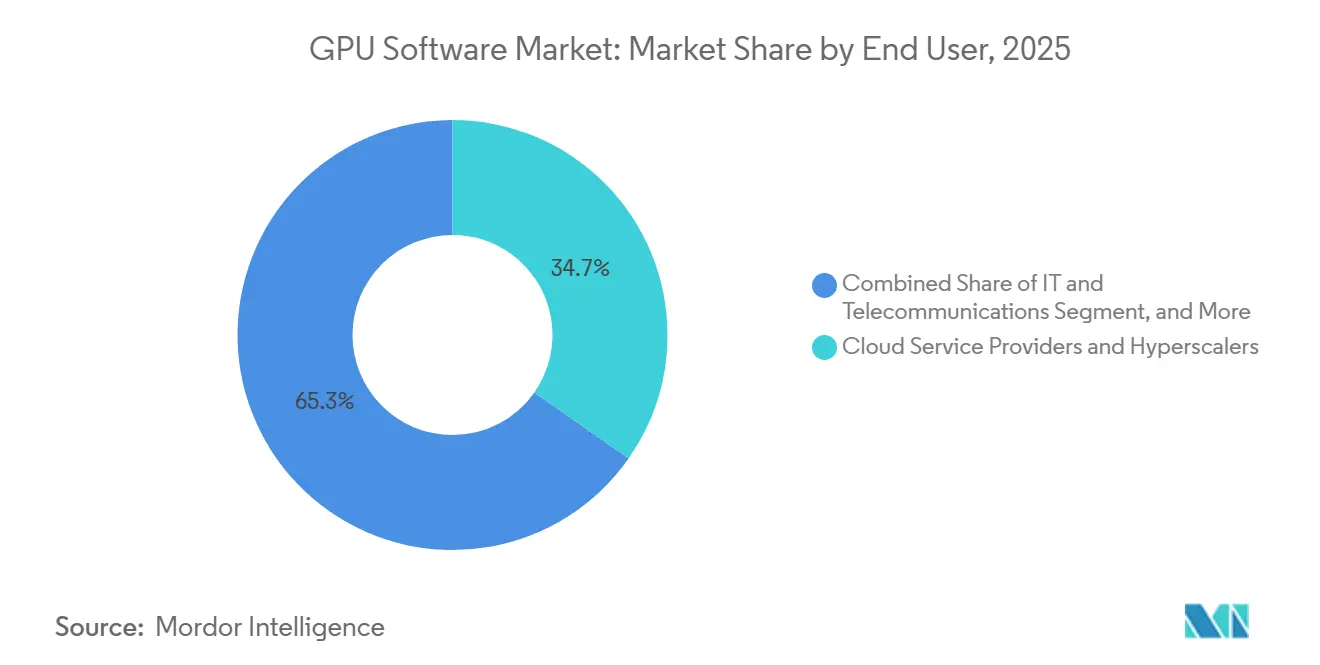

- By end user, cloud service providers and hyperscalers held 34.73% of revenue in 2025, while cloud service providers and hyperscalers are also projected to advance at the fastest pace, at 31.44% CAGR through 2031.

- By geography, North America held 48.44% of revenue in 2025, while Asia-Pacific is also projected to advance at the fastest pace, at 31.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GPU Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption of Generative AI and Large Language Model Workloads | +9.5% | Global | Short term (≤ 2 years) |

| Rising Demand for GPU Orchestration in Hybrid and Multi-Cloud Environments | +5.8% | North America and Europe | Short term (≤ 2 years) |

| Growing Use of GPU Software for High-Performance Computing Workloads | +4.3% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Expansion of Cloud Gaming and Real-Time Rendering Use Cases | +2.9% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Shift Toward Fractional GPU Provisioning and Pay-Per-Use Access Models | +2.1% | Global | Short term (≤ 2 years) |

| Rising Enterprise Focus on GPU Utilization, Monitoring, and Cost Optimization | +1.8% | Global, with early adoption in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Generative AI and Large Language Model Workloads

Generative AI spending remains the strongest growth driver for the GPU software market because large model training and inference place sustained pressure on scheduling, memory use, and runtime efficiency. Inference serving has become especially important because software overhead per request directly affects the operating cost of enterprise AI deployments. NVIDIA stated in its fiscal 2026 results that Blackwell Ultra delivers up to 50x better performance and 35x lower cost for agentic AI than Hopper on the SemiAnalysis InferenceX benchmark, which supports faster platform migration and shorter refresh cycles.[1]NVIDIA Corporation, “NVIDIA Announces Financial Results for Fourth Quarter and Fiscal 2026,” NVIDIA Newsroom, nvidianews.nvidia.com NVIDIA also said that the CUDA-X ecosystem now spans nearly 6,000 accelerated applications, which shows how deeply the GPU software market is tied to an established software base rather than hardware alone. The same product cycle also introduced Cosmos and Isaac GR00T open models for physical AI and robotics, which extends the GPU software market into factory automation and autonomous system simulation.

Rising Demand for GPU Orchestration in Hybrid and Multi-Cloud Environments

The GPU software market is also benefiting from rising demand for orchestration across public cloud, private cloud, and sovereign environments. Enterprises are increasingly using permanent hybrid setups where sensitive model training stays on owned or controlled infrastructure and overflow inference runs move to external cloud capacity. Mirantis launched integration between its k0rdent AI platform and NVIDIA Run:ai in April 2026, and the company said this allows neoclouds and enterprises to deploy production-ready AI environments in minutes rather than weeks.[2]Mirantis, “Mirantis Automates AI Factory Deployments With k0rdent AI and NVIDIA Run:ai,” Mirantis Press Center, mirantis.com Mirantis and Supermicro also announced a validated sovereign AI and hybrid cloud stack in March 2026, which shows that suppliers are turning hybrid orchestration into a more standardized commercial offer. This pattern supports faster expansion in hybrid cloud and private cloud because the software layer manages workload placement, data locality, and utilization across different infrastructure environments.

Growing Use of GPU Software for High-Performance Computing Workloads

High-performance computing is widening the demand base for the GPU software market beyond enterprise AI and graphics workloads. NVIDIA stated in June 2026 that its technologies power more than 400 of the world's 500 fastest supercomputers, which equals 81% of the TOP500 list released at ISC High Performance 2026. That installed base matters because supercomputing deployments rely on software libraries, optimization tools, and workflow management layers that often stay in place for long operating cycles. NVIDIA also introduced the Vera Rubin NVL rack at ISC 2026 with up to 144 GPUs per rack, 5 petaFLOPS of FP64 performance, and 2.8x memory bandwidth improvement over Blackwell, which expands software use cases in molecular dynamics, fusion modeling, and drug discovery. The same announcement noted that 35 new AI supercomputers are deploying across 23 European countries, which indicates that the GPU software market is gaining support from publicly backed research infrastructure as well as private enterprise demand.

Expansion of Cloud Gaming and Real-Time Rendering Use Cases

Cloud gaming and real-time rendering continue to add a separate demand stream to the GPU software market because these workloads require persistent GPU sessions, low latency, and stable frame delivery. Those operating conditions are different from batch AI workloads, so they favor software that can balance memory use, session concurrency, and rendering performance in real time. NVIDIA said in its fiscal 2026 results that DLSS 4.5 delivers up to 3x performance improvement in AI-generated visuals for gaming contexts, which highlights the role of software optimization in extracting more output from installed GPU hardware. The same rendering technologies are increasingly relevant in industrial visualization and digital twin environments, where real-time scene generation and remote interaction matter as much as image quality. This overlap keeps the GPU software market connected to both entertainment and enterprise visualization budgets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity Across Heterogeneous GPU and Cloud Stacks | -3.2% | Global | Short term (≤ 2 years) |

| Security, Privacy, and Data Sovereignty Concerns in Shared GPU Environments | -2.5% | Europe, Asia-Pacific | Medium term (2-4 years) |

| Limited Availability of Advanced GPU Infrastructure and Related Talent | -1.8% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| High Ongoing Cost of Enterprise-Grade GPU Software and Managed Services | -1.4% | Global, concentrated in SME segment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity Across Heterogeneous GPU and Cloud Stacks

Integration complexity remains a real brake on the GPU software market because production environments often combine different chips, drivers, server types, and deployment models. Each hardware generation brings new interconnect behavior, memory hierarchies, and software dependencies, which raises testing and optimization work for enterprise teams. AMD said its ROCm 7.0 software for the Instinct MI350 series added broader FP4 and FP6 support and new data center scalability features, which shows that alternative software stacks are advancing but still add another layer of compatibility work for users.[3]AMD, “AMD ROCm 7.0 Software: Supercharging AI and HPC Infrastructure With AMD Instinct Series GPUs and Open Innovation,” AMD, amd.com NVIDIA's fiscal 2026 results also underline how deeply its ecosystem is embedded through CUDA-X and thousands of accelerated applications, which makes migration away from an established stack slower and more expensive. As a result, multi-vendor deployments often face longer validation cycles and slower returns on infrastructure spending in the GPU software market.

Security, Privacy, and Data Sovereignty Concerns in Shared GPU Environments

Security, privacy, and data residency concerns are restraining the GPU software market most clearly in regulated sectors and regions with tighter digital governance rules. A 2025 European Parliament study found systemic dependence on non-EU providers across Europe's software and digital stack, including AI platforms and cloud infrastructure, which increases concern over legal exposure and control of sensitive data. That concern is pushing more enterprise and public sector workloads toward sovereign or locally controlled GPU environments instead of fully shared public cloud setups. Deutsche Telekom and NVIDIA brought Germany's first Industrial AI Cloud online in Munich in February 2026, with around 10,000 NVIDIA Blackwell GPUs and 0.5 ExaFLOPS of compute capacity for industrial customers, which shows how suppliers are responding with local infrastructure options. This makes security and sovereignty both a restraint and a factor shaping the regional structure of the GPU software market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Layer Anchors Dominant Revenue Share

Software held 76.11% of the GPU software market in 2025, which shows that customers place more value on orchestration, observability, and inference optimization than on access to compute alone. NVIDIA said the CUDA-X ecosystem supports nearly 6,000 accelerated applications, and that scale continues to support a deep installed base for the software layer across AI, science, and visualization workloads. This position also helps explain why software is the fastest-growing component at 31.21% CAGR through 2031, because enterprises are moving from isolated clusters to more persistent workload management frameworks. The services segment accounted for the remaining share of the GPU software market in 2025, and much of that revenue came from managed GPU cloud and deployment support.

The commercial line between software and services is becoming less clear in the GPU software industry because suppliers increasingly bundle orchestration, monitoring, and optimization into managed infrastructure offers. Mirantis positioned its k0rdent AI integration with NVIDIA Run:ai as a way to automate AI platform deployment and lifecycle management, which shows how software functionality is being wrapped into broader service delivery. CoreWeave also reported strong fiscal 2025 growth and a larger enterprise focus, which indicates that GPU-native providers are monetizing software control layers alongside cloud capacity rather than treating them as separate products. This bundling supports higher recurring revenue and makes stand-alone component comparisons less straightforward across the GPU software market.

By Deployment Mode: Hybrid Cloud Drives the Fastest Expansion

Cloud-based deployment accounted for 45.33% of the GPU software market in 2025, while hybrid cloud and private cloud is projected to grow at 31.62% CAGR through 2031. The largest installed base still sits in cloud environments because they give enterprises faster access to GPU capacity and let them scale training and inference without owning all hardware. At the same time, the fastest growth is shifting toward hybrid designs because those setups give users more control over data placement and security while preserving burst capacity. Mirantis and Supermicro announced a validated sovereign AI and hybrid cloud deployment stack in March 2026, which reflects rising commercial demand for ready-built hybrid GPU environments.

On-premises deployment remains relevant in regulated sectors and research settings where data residency and system control cannot be compromised. Edge and embedded deployment is still a smaller base in the GPU software market, but it is becoming more relevant in automotive validation, industrial digital twins, and other asset-level inference workloads. SoftBank launched Infrinia AI Cloud OS in January 2026 to let AI data center operators provide multi-tenant Kubernetes-as-a-Service and inference-as-a-Service on GPU infrastructure, and that release points to stronger software support for distributed deployment models. The deployment mix is therefore widening, but the software layer remains the main tool for tying these environments together.

By Enterprise Size: SME Adoption Accelerates Through Managed Services

Large enterprises represented 75.42% of the GPU software market in 2025, which reflects the capital, engineering depth, and operating discipline required for production-scale GPU use. These organizations usually manage larger model pipelines, more complex compliance needs, and multi-region infrastructure, so they remain the main buyers of advanced orchestration and optimization software. Small and medium enterprises are still becoming the fastest-growing customer group, with 31.53% CAGR through 2031, because managed services and fractional provisioning are lowering the cost and skill threshold for adoption. NVIDIA said its NIM microservices are available through cloud channels such as AWS Marketplace and Oracle Cloud Infrastructure, which supports easier deployment of optimized inference endpoints for smaller users.

The competitive shift in this segment matters because much of the new SME demand is going to born-digital GPU cloud providers rather than traditional enterprise software vendors. CoreWeave said in its fiscal 2025 results that it was broadening its customer mix beyond a single hyperscaler concentration, which suggests that the GPU software market is opening to a wider pool of enterprise and AI-native clients. That broadening creates room for simpler procurement, shorter deployment cycles, and more packaged software experiences for smaller businesses. It also means the GPU software market is no longer tied only to the spending patterns of the largest enterprises.

By Application: AI and ML Consolidates Market Leadership

Artificial intelligence and machine learning accounted for 52.12% of the GPU software market size in 2025, and this segment is also projected to grow at 31.32% CAGR through 2031. That combination of scale and speed shows that AI and ML remain the central demand engine for the GPU software market. NVIDIA's fiscal 2026 disclosures highlighted the breadth of the CUDA-X software ecosystem and the Blackwell transition, both of which support continued lock-in for model training, inference optimization, and workflow acceleration. As a result, migration costs in AI pipelines remain high even as alternative hardware and software options continue to improve.

High-performance computing is the second-largest application base, and it reinforces the GPU software market through long-lived scientific and engineering workflows. NVIDIA said its technologies power 81% of the TOP500 list, which shows how deeply GPU software is embedded in research computing environments. Rendering, analytics, simulation, digital twins, video processing, and gaming continue to broaden the tail of specialized demand in the GPU software market. NVIDIA's product cycle also connected AI, robotics, weather modeling, and visualization more closely, which supports new commercial sub-markets without changing the leading role of AI and ML.

By End User: Hyperscalers Anchor Demand While Verticals Broaden

Cloud service providers and hyperscalers represented 34.73% of the GPU software market size in 2025, and they are also projected to grow at 31.44% CAGR through 2031. Their lead position reflects the fact that most enterprises still access large-scale GPU capacity through hosted platforms rather than through wholly owned infrastructure. CoreWeave reported USD 5.1 billion in fiscal 2025 revenue and a revenue backlog of USD 66.8 billion by year-end 2025, which illustrates the scale of demand flowing through specialized GPU cloud providers. That concentration also means that capacity planning and software efficiency decisions made by a small number of infrastructure operators can influence the wider GPU software market.

IT and telecommunications remains the second-largest end-user base because operators use GPU software for network analytics, video processing, and edge inference. Healthcare and life sciences continues to expand as GPU software is used in drug discovery, molecular simulation, and AI model development for research workflows. Automotive also stands out because simulation-heavy ADAS validation and synthetic data generation require sustained GPU throughput and specialized software frameworks. BFSI demand remains meaningful, but the GPU software market faces a tighter deployment path in this vertical because security, privacy, and control requirements shape where and how workloads can run.

Geography Analysis

North America accounted for 48.44% of the GPU software market share in 2025, which made it the largest regional contributor. The region leads because it combines hyperscaler capital spending, deep enterprise AI adoption, and a strong installed base of software developers working within established GPU ecosystems. CoreWeave said its revenue backlog rose to USD 99.4 billion as of March 31, 2026, up from USD 66.8 billion at year-end 2025, which points to a large committed demand base centered heavily in North American cloud and enterprise activity. NVIDIA's fiscal 2026 results also showed the continued expansion of the CUDA-X ecosystem and Blackwell platform transition, which supports ongoing upgrade cycles across North American customers. This keeps North America in a strong position through the forecast period even as regional growth rates elsewhere move higher.

Asia-Pacific is projected to expand at 31.42% CAGR through 2031, making it the fastest-growing region in the GPU software market. SoftBank launched Infrinia AI Cloud OS in January 2026 for AI data center operators that want to offer multi-tenant Kubernetes-as-a-Service and inference-as-a-Service on GPU infrastructure. NTT DATA also launched GPU as a Service for large-scale machine learning workloads in Japan, targeting use cases such as LLM development, autonomous driving, and drug discovery. These moves show that the GPU software market in Asia-Pacific is being supported by local platform development as well as demand from cloud-first enterprise adoption and sovereign AI investment programs.

Europe and the rest of the world contribute a different growth profile to the GPU software market, one shaped more directly by data control and sovereign infrastructure needs. The European Parliament's 2025 study on software and cyber dependencies highlighted the extent of Europe's reliance on non-EU providers, which adds urgency to regional control over AI and cloud infrastructure. Deutsche Telekom and NVIDIA brought Germany's first Industrial AI Cloud online in Munich in February 2026 with around 10,000 NVIDIA Blackwell GPUs and 0.5 ExaFLOPS of capacity, which shows how that policy pressure is translating into real infrastructure. Bitkom also said AI and HPC workloads accounted for 15% of German data center capacity in 2025 and are projected to reach 40% by 2030, which supports the case for continued regional build-out.

Competitive Landscape

The GPU software market is moderately concentrated at the platform level and more fragmented at the tooling and specialty cloud level. NVIDIA remains the central platform vendor because its software ecosystem includes a developer community of more than 6 million and nearly 6,000 accelerated applications, which creates durable switching costs for enterprises and research users. Google Cloud expanded its AI Hypercomputer platform in 2026 and said it can support up to 960,000 NVIDIA GPUs across multiple sites through the Virgo Network, which shows how hyperscalers are competing through integrated infrastructure and software scale. Oracle also said OCI achieved NVIDIA Exemplar Cloud status for the GB200 NVL72 platform, which signals a strategy focused on pairing advanced GPU infrastructure with differentiated cloud software environments. The result is a GPU software market where a few large vendors shape the base platform, while adjacent software layers remain open to specialized challengers.

CoreWeave has emerged as one of the clearest challengers in the GPU software market by combining GPU-native cloud infrastructure with tightly integrated software operations. The company reported fiscal 2025 revenue of USD 5.1 billion and later reported first quarter 2026 revenue of USD 2.1 billion, which shows that demand for specialized GPU cloud platforms is expanding quickly. Mirantis has also moved to strengthen its position through the k0rdent AI integration with NVIDIA Run:ai and its validated hybrid stack with Supermicro, both of which reduce deployment complexity for enterprise buyers. These strategic moves show that challengers are not trying to displace the leading ecosystem outright, but are instead building value in orchestration, sovereign deployment, and workload portability.

The next competitive opening in the GPU software market is likely to stay in cross-vendor orchestration and edge-oriented software rather than in direct platform replacement. AMD continues to push ROCm as an open software stack for AI and HPC, and the ROCm 7.0 release shows ongoing work to improve usability and scale in data center environments. Regional providers are also gaining room where sovereign control matters more than pure scale, as shown by Deutsche Telekom's industrial AI cloud in Germany and SoftBank's AI cloud operating stack in Japan. This keeps the overall competitive picture balanced between entrenched ecosystem power and narrower opportunities for differentiated software execution.

GPU Software Industry Leaders

NVIDIA Corporation

Amazon Web Services, Inc.

Microsoft Corporation

Google LLC

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA disclosed at ISC High Performance 2026 in Hamburg that its Vera Rubin architecture supports 35 new AI supercomputers actively deploying across 23 European countries, including national supercomputing centers and EuroHPC AI factories, extending NVIDIA's scientific computing software footprint into publicly funded HPC markets.

- April 2026: Mirantis launched integration between its k0rdent AI platform and NVIDIA Run:ai, enabling neoclouds and enterprises to deploy production-ready AI factories within minutes via automated GPU orchestration software lifecycle management.

- March 2026: Mirantis and Supermicro announced validation of a pre-integrated sovereign AI and hybrid GPU cloud deployment stack based on Mirantis k0rdent AI and Supermicro modular server architecture, targeting European and regulated-market operators with a Metal-to-Model deployment path.

- February 2026: Deutsche Telekom and NVIDIA brought Germany's first Industrial AI Cloud online in Munich, deploying approximately 10,000 NVIDIA Blackwell GPUs with 0.5 ExaFLOPS compute capacity, with Siemens, Agile Robots, and Perplexity among the first customers.

Global GPU Software Market Report Scope

The GPU Software Market refers to the industry segment dedicated to the development and deployment of software solutions that harness the computational power of Graphics Processing Units (GPUs) for diverse applications such as artificial intelligence (AI), machine learning (ML), deep learning, data analytics, scientific simulations, gaming, and visualization.

The GPU Software Market Report is Segmented by Component (Software and Services), Deployment Mode (Cloud-Based, On-Premises, Hybrid Cloud / Private Cloud, and Edge / Embedded), Enterprise Size (Large Enterprises and Small and Medium Enterprises), Application (Artificial Intelligence and Machine Learning, High-Performance Computing, Data Analytics, Graphics Rendering and Visualization, Simulation and Digital Twins, Video Processing and Streaming, Gaming and Cloud Gaming Infrastructure, and Other Applications), End User (Cloud Service Providers and Hyperscalers, IT and Telecommunications, Healthcare and Life Sciences, BFSI, Media and Entertainment, Automotive, Manufacturing, and Other End Users (Government and Defense, Retail and E-Commerce)), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid Cloud / Private Cloud |

| Edge / Embedded |

| Large Enterprises |

| Small and Medium Enterprises |

| Artificial Intelligence and Machine Learning |

| High-Performance Computing |

| Data Analytics |

| Graphics Rendering and Visualization |

| Simulation and Digital Twins |

| Video Processing and Streaming |

| Gaming and Cloud Gaming Infrastructure |

| Other Applications |

| Cloud Service Providers and Hyperscalers |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| BFSI |

| Media and Entertainment |

| Automotive |

| Manufacturing |

| Other End Users (Government and Defense, Retail and E-Commerce) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Component | Software | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid Cloud / Private Cloud | ||

| Edge / Embedded | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Application | Artificial Intelligence and Machine Learning | |

| High-Performance Computing | ||

| Data Analytics | ||

| Graphics Rendering and Visualization | ||

| Simulation and Digital Twins | ||

| Video Processing and Streaming | ||

| Gaming and Cloud Gaming Infrastructure | ||

| Other Applications | ||

| By End User | Cloud Service Providers and Hyperscalers | |

| IT and Telecommunications | ||

| Healthcare and Life Sciences | ||

| BFSI | ||

| Media and Entertainment | ||

| Automotive | ||

| Manufacturing | ||

| Other End Users (Government and Defense, Retail and E-Commerce) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the GPU software market?

The GPU software market was valued at USD 15.84 billion in 2025, is expected to reach USD 22.67 billion in 2026, and is forecast to reach USD 84.96 billion by 2031 at a 30.24% CAGR.

Which application generates the most revenue in GPU software?

Artificial intelligence and machine learning led with 52.12% of revenue in 2025, and it is also projected to be the fastest-growing application through 2031.

Why are hybrid and private deployments growing faster in GPU software?

Hybrid cloud and private cloud deployments are projected to grow at 31.62% CAGR because enterprises want public cloud elasticity while keeping sensitive workloads under tighter control.

Which customer group is creating the fastest new demand?

Small and medium enterprises are projected to grow at 31.53% CAGR as managed services and fractional GPU access lower the cost and skill barrier for adoption.

Which region leads the GPU software market today?

North America led with 48.44% share in 2025 because of strong hyperscaler investment, broad enterprise AI adoption, and a deep software developer base.

What is changing competition in GPU software the most?

Competition is shifting toward orchestration, optimization, and deployment software because customers now care as much about utilization, portability, and control as they do about raw GPU capacity.

Page last updated on: