GPU Cloud Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.62 Billion |

| Market Size (2031) | USD 37.69 Billion |

| Growth Rate (2026 - 2031) | 19.26% CAGR |

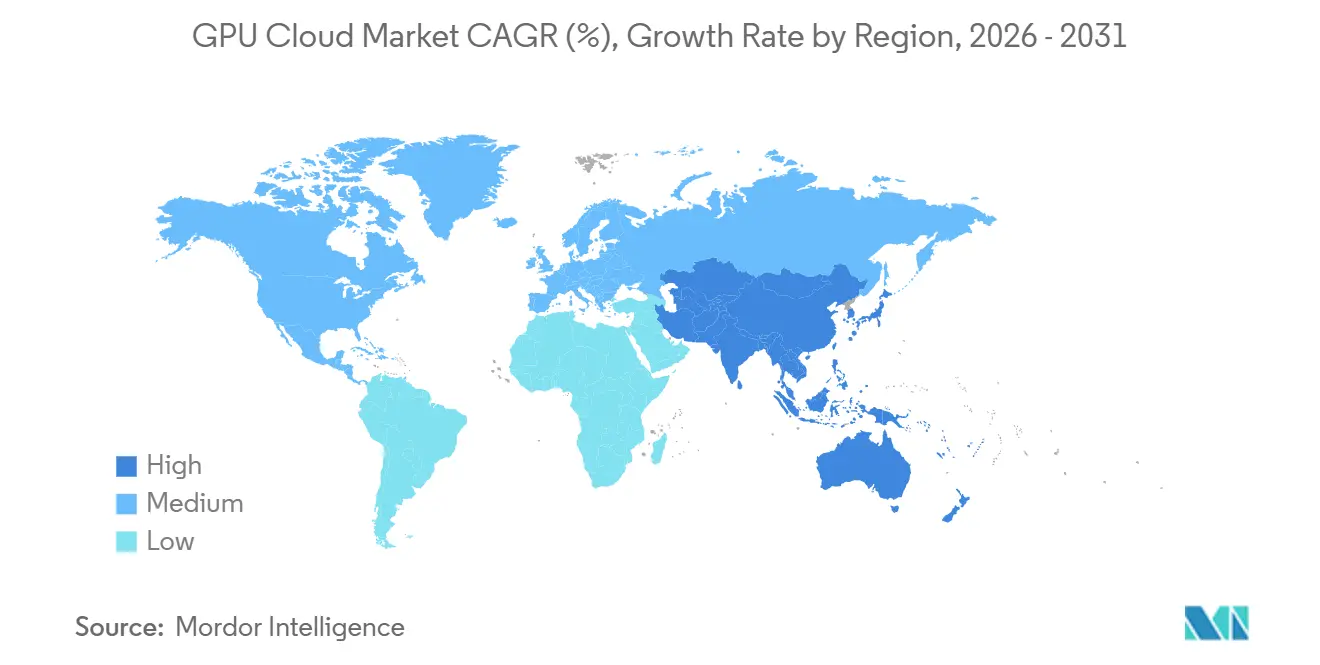

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

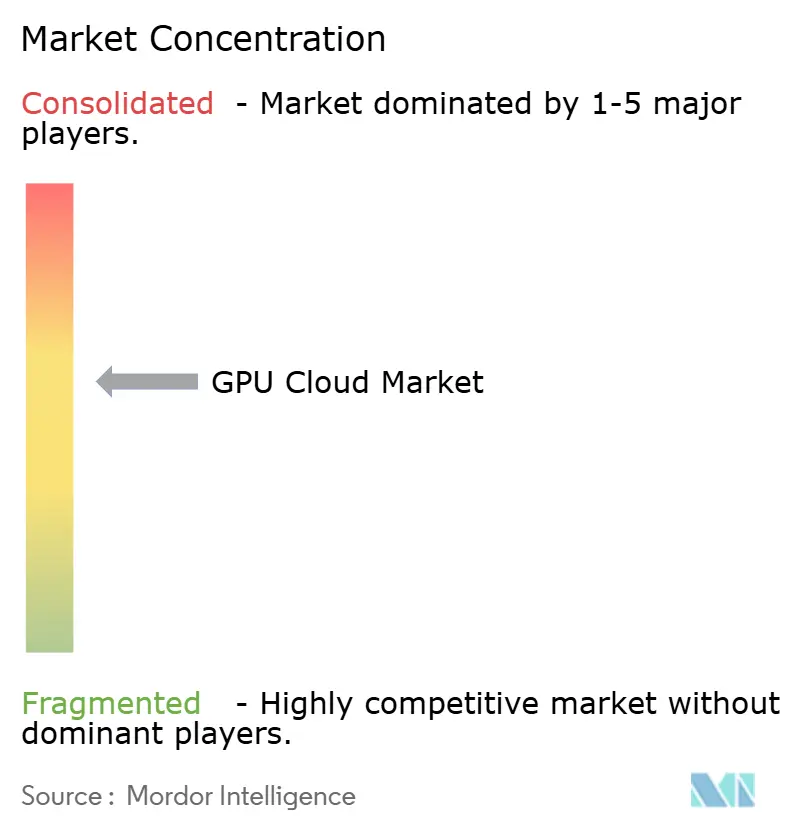

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GPU Cloud Market Analysis by Mordor Intelligence

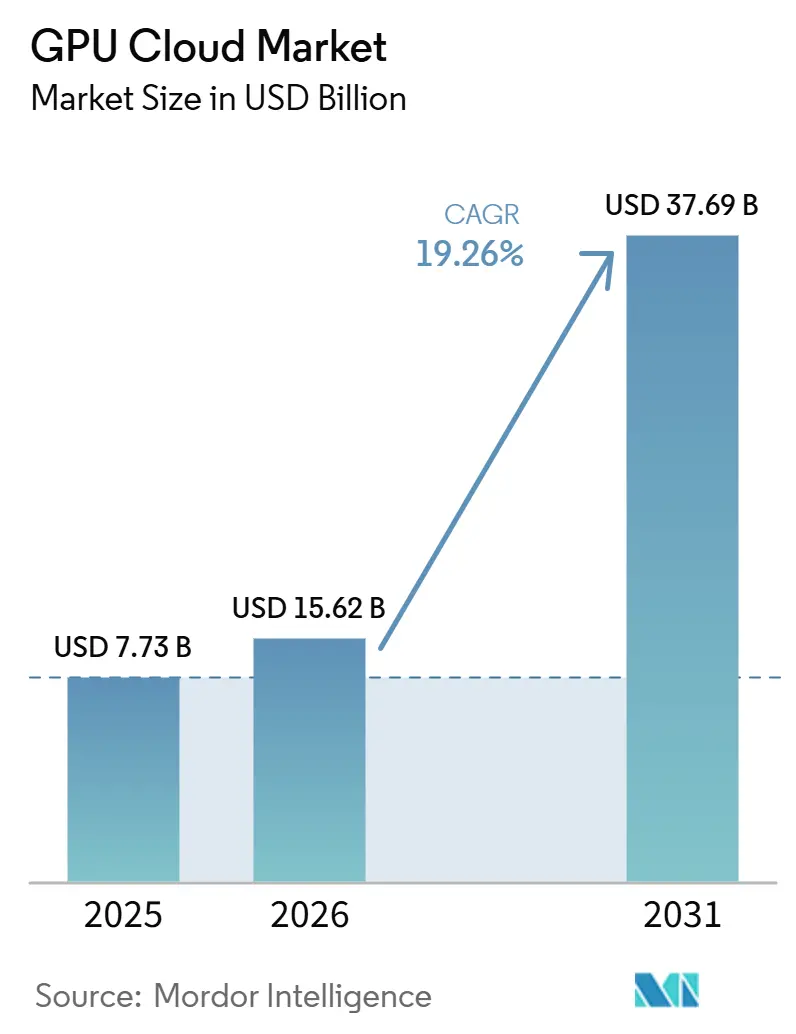

The GPU cloud market size is expected to increase from USD 7.73 billion in 2025 to USD 15.62 billion in 2026 and reach USD 37.69 billion by 2031, growing at a CAGR of 19.26% over 2026-2031. The GPU cloud market is expanding because enterprises now treat AI workloads as ongoing operating needs instead of limited pilot programs. Spending patterns in the GPU cloud market are also shifting from one-time training bursts toward steady inference demand, which keeps GPU capacity in use for longer periods. The GPU cloud market is further supported by demand for raw compute access, managed AI environments, and dedicated deployments that can meet stricter performance expectations. Competitive behavior in the GPU cloud market reflects this transition, with hyperscalers defending scale advantages while specialist providers target training-intensive and dedicated inference workloads. The strongest opportunities in the GPU cloud market are tied to managed AI tooling, regulated hosting environments, and regional capacity buildouts that can serve production AI more reliably.

Key Report Takeaways

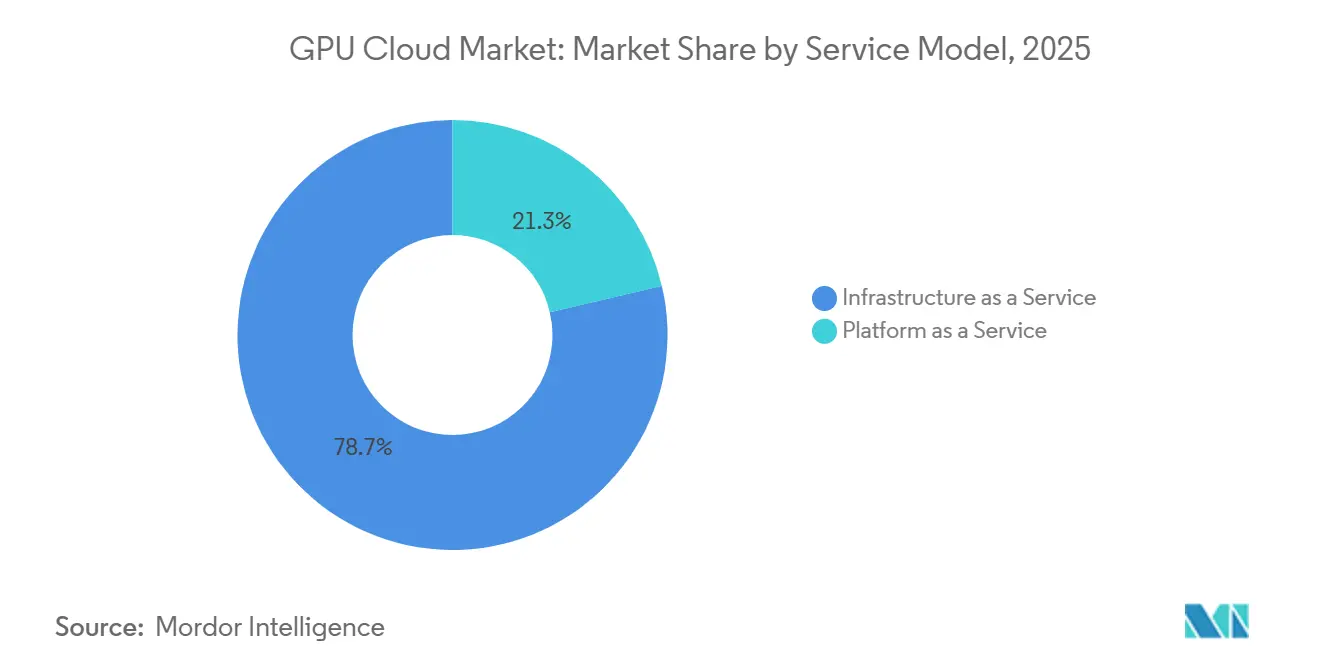

- By service model, Infrastructure as a Service led with a 78.66% share of the GPU cloud market in 2025, while Platform as a Service is projected to expand at a 19.32% CAGR through 2031.

- By GPU workload class, AI Training and Large-Scale HPC GPU Instances held a 62.34% share of the GPU cloud market in 2025, while AI Inference and General Accelerated Compute GPU Instances are projected to grow at a 19.41% CAGR through 2031.

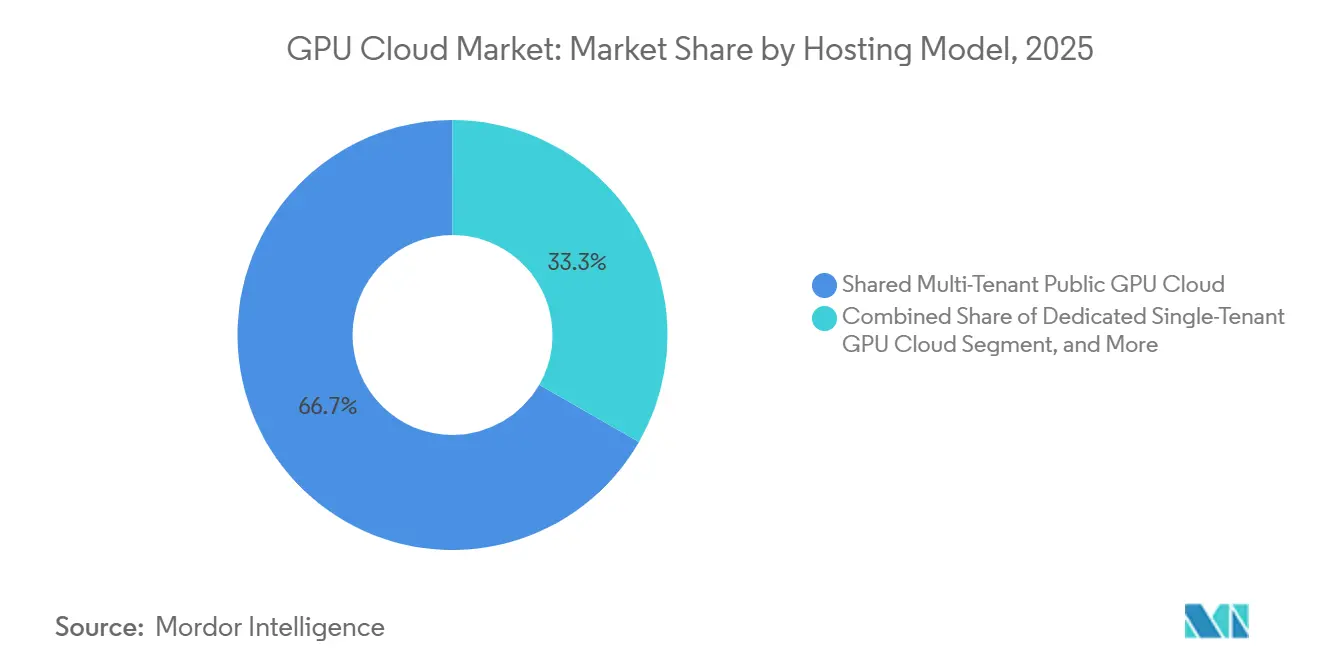

- By hosting model, Shared Multi-Tenant Public GPU Cloud accounted for a 66.71% share in 2025, while Dedicated Single-Tenant GPU Cloud is projected to advance at a 19.33% CAGR through 2031.

- By organization size, Large Enterprises held 77.12% of the GPU cloud market share in 2025, while SMEs and AI-native startups are projected to expand at a 19.43% CAGR through 2031.

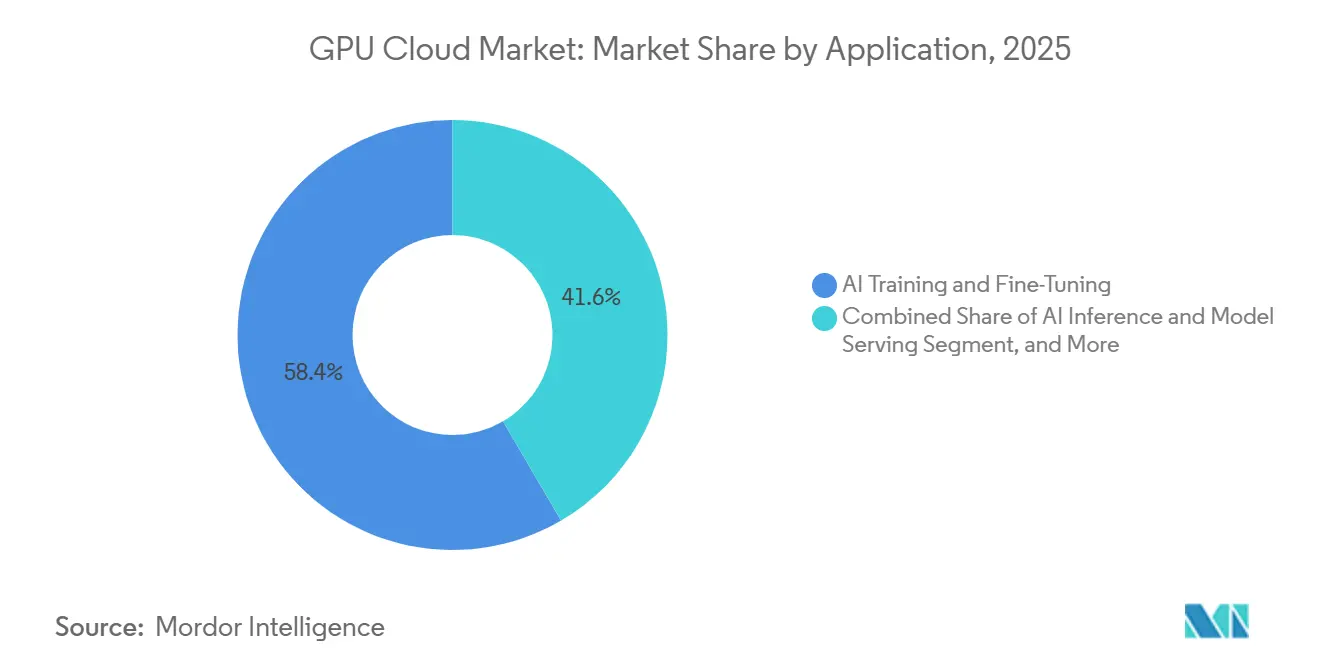

- By application, AI Training and Fine-Tuning captured a 58.42% share in 2025, while AI Inference and Model Serving is projected to grow at a 19.57% CAGR through 2031.

- By end-user industry, IT, Telecom, Software, and Internet Platforms accounted for a 66.43% share in 2025, while Healthcare, Life Sciences, and Pharmaceuticals is projected to expand at a 19.66% CAGR through 2031.

- By geography, North America held 72.76% of the GPU cloud market in 2025, while Asia-Pacific is projected to grow at a 19.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GPU Cloud Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Generative AI and LLM Training Demand | +4.5% | Global | Short term (≤ 2 years) |

| Growth in Agentic AI Inference Workloads | +4.0% | Global, US-led with APAC spill-over | Short term (≤ 2 years) |

| Enterprise Shift Toward Elastic Pay-Per-Use GPU Capacity | +3.0% | North America and EU, with APAC secondary | Medium term (2-4 years) |

| Sovereign AI and Data Residency Requirements | +2.5% | EU, Asia-Pacific, Middle East and Africa | Medium term (2-4 years) |

| Expansion of GPU-Heavy Cloud Gaming and Real-Time Rendering | +1.5% | North America, Asia-Pacific | Long term (≥ 4 years) |

| Fractional GPU Scheduling and Composable GPU Fabrics | +1.0% | Global, early adoption in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Generative AI And LLM Training Demand

Generative AI and large language model development remain the central demand engine for the GPU cloud market. Each new model generation requires larger training clusters, denser networking, and more memory per deployment, which pushes providers to secure capacity earlier and on longer terms. This has increased the advantage of operators that already control large GPU estates and can deliver tightly integrated training environments. The GPU cloud market is also becoming more concentrated at the top of the training stack because very large model builds need specialized infrastructure that only a limited number of providers can assemble at scale. CoreWeave’s public filings and operating disclosures showed how access to large GPU fleets and large data center commitments became a defining competitive asset for training-focused providers in this market.[1]CoreWeave, Inc. Form S-1, U.S. Securities and Exchange Commission, sec.gov CoreWeave’s March 2025 IPO announcement further showed that investors viewed large-scale AI compute capacity as a durable growth category rather than a short-lived build cycle.[2]CoreWeave, Inc. Form S-1, U.S. Securities and Exchange Commission, sec.gov

Growth In Agentic AI Inference Workloads

The GPU cloud market is also being pushed forward by a rapid increase in agentic AI inference workloads. Production agents do more than answer prompts because they plan actions, retrieve context, invoke tools, and evaluate outputs across multiple cycles for a single task. That pattern keeps inference clusters active for longer periods and raises the value of low-latency serving capacity inside the GPU cloud market. NVIDIA leadership stated in 2025 that agentic inference can require far more compute than early generative AI systems, which supports the expectation of heavier serving demand over time. CoreWeave’s May 2026 launch of a unified agentic AI platform showed how providers are linking reinforcement learning, production inference, observability, and continuous improvement into one managed workflow. As this operating model spreads, the GPU cloud market is shifting toward more persistent inference demand and away from a purely training-led utilization curve.

Enterprise Shift Toward Elastic Pay-Per-Use GPU Capacity

Elastic pricing remains a major adoption lever for the GPU cloud market because many enterprises still cannot justify owning large GPU fleets for uneven workloads. Pay-per-use access lowers the entry barrier for teams that need production AI capacity without locking capital into underused hardware. This is especially relevant in the GPU cloud market when workloads move from experimentation to deployment, and buyers need to match cost more closely to usage. Managed environments strengthen this demand because they reduce the time and effort required to stand up training, inference, and orchestration layers. CoreWeave’s product expansion in 2026 showed how providers are moving beyond raw infrastructure into integrated environments that help enterprises shorten deployment cycles. The same shift helps smaller companies enter the GPU cloud market with service layers that reduce the need for large in-house infrastructure teams.

Sovereign AI And Data Residency Requirements

Sovereign AI requirements are creating a clear growth lane in the GPU cloud market for dedicated, regulated, and jurisdiction-bound deployments. Buyers in regulated sectors increasingly need stronger control over where data resides, how models are served, and which entities can access infrastructure. This makes the GPU cloud market more favorable to local and regional providers that can combine compliance positioning with meaningful GPU capacity. Deutsche Telekom’s AI factory plan in Munich, built with up to 10,000 NVIDIA Blackwell GPUs, showed how telecom incumbents are repositioning as sovereign infrastructure providers for industrial AI use cases. Microsoft’s April 2026 commitment to expand AI infrastructure in Japan showed that global providers are also responding by deepening local capacity in priority jurisdictions.[3]CoreWeave, Inc., “CoreWeave Advances AI-Native Cloud Platform with NVIDIA HGX B300,” CoreWeave News, coreweave.com As a result, the GPU cloud market is no longer defined only by scale, because regional trust and residency control are shaping provider selection more directly.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HBM and Advanced Packaging Supply Constraints | -2.5% | Global, APAC fabs as primary chokepoint | Short term (≤ 2 years), Medium term (2-4 years) |

| GPU Spot Price Volatility and Capacity Hoarding | -2.0% | Global | Short term (≤ 2 years) |

| Energy and Cooling Intensity of Dense GPU Racks | -1.0% | North America, EU, capacity-constrained power markets | Medium term (2-4 years), Long term (≥ 4 years) |

| Customer Lock-In Around Specialized AI Toolchains | -0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

HBM And Advanced Packaging Supply Constraints

High-bandwidth memory remains the clearest physical bottleneck for the GPU cloud market because modern AI accelerators depend on it for performance at scale. When memory supply tightens, cloud providers cannot expand deployable capacity at the same pace as demand, even if data center space and buyer interest remain strong. This pressure is amplified by advanced packaging constraints, which slow the conversion of chip demand into usable systems. Reporting tied to AMD leadership in 2026 noted that HBM demand growth was outpacing supply growth, while major suppliers had already sold through their 2026 HBM3E output. The GPU cloud market, therefore, rewards providers with long-term allocation relationships because supply access is functioning as a competitive moat rather than a normal procurement input. This constraint also limits how quickly new entrants can challenge established operators in the highest-value parts of the GPU cloud market.

GPU Spot Price Volatility And Capacity Hoarding

Price volatility remains a practical restraint for the GPU cloud market because spot capacity does not always provide predictable access when demand spikes. Large buyers increasingly reserve blocks of capacity to protect their own road maps, which reduces elasticity for smaller customers and distorts short-term pricing. That behavior weakens one of the original benefits of the GPU cloud market, which was the ability to scale quickly without long contract cycles. It also nudges buyers toward reserved or dedicated agreements that trade flexibility for certainty. As reserved structures become more common, the GPU cloud market can lose some of the open capacity that helped newer users access advanced compute on demand. This does not reduce long-term demand, but it does make access less even across customer groups and adds friction for mid-tier users who rely on burst availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Model: PaaS Closes the Gap as Managed AI Toolchains Mature

Infrastructure as a Service accounted for 78.66% of the GPU cloud market in 2025, which made it the dominant service layer for buyers that wanted direct control over compute, networking, and memory policies. That position reflected the early maturity of the GPU cloud market, where many large customers still preferred to assemble and tune environments themselves. Raw GPU access remained attractive for training-heavy users who needed flexibility across frameworks, cluster designs, and scaling rules. The service mix also showed that most spending still sat closest to the infrastructure layer, even as buyer expectations were beginning to change.

Platform as a Service is projected to grow at a 19.32% CAGR through 2031, which points to a steady narrowing between raw capacity and managed AI environments. The GPU cloud market is moving in this direction because enterprises increasingly need orchestration, observability, reinforcement learning workflows, and model serving within one operating layer. CoreWeave’s May 2026 rollout of unified agentic AI capabilities illustrated how providers are folding training and inference operations into a closed improvement loop rather than offering compute alone. This means the GPU cloud market is not replacing IaaS, but it is adding more value above it as customers push for faster deployment and lower engineering overhead. Over time, providers that combine strong infrastructure with usable platform tooling should hold a more durable position than providers that compete on GPU access alone.

By GPU Workload Class: Inference Becomes The Main Expansion Engine

AI Training and Large-Scale HPC GPU Instances held a 62.34% share of the GPU cloud market by workload class in 2025. That lead reflected the heavy concentration of spending around frontier model development, large enterprise fine-tuning programs, and research computing projects that still required large training clusters. In the earlier phase of the GPU cloud market, training demand shaped how providers built data center footprints, interconnect designs, and capacity planning models. Those workloads remain central because they still consume dense, high-value compute over defined project windows. Training also continues to anchor provider reputation because customers often judge platform strength by how well it supports demanding model development tasks.

AI Inference and General Accelerated Compute GPU Instances are projected to grow at a 19.41% CAGR through 2031, which marks a clear change in where the GPU cloud market will spend more time and capacity. Once models move into production, they create continuous serving demand with tighter latency requirements and longer utilization cycles. That changes the economics of the GPU cloud market because inference can accumulate more total compute-hours over a model’s operating life than a single training run. Research presented at ECRTS in 2025 on hardware compute partitioning for NVIDIA GPUs pointed to more efficient scheduling approaches that can improve utilization across varied workload profiles. As production AI expands, providers in the GPU cloud market will need to balance training credibility with strong inference architecture and scheduling discipline.

By Hosting Model: Single-Tenant Demand Accelerates as Compliance and Performance Converge

Shared Multi-Tenant Public GPU Cloud accounted for 66.71% of the hosting model segment in 2025, which confirmed its role as the default entry point for startups, researchers, and enterprise pilots. Multi-tenant environments won early demand because they offered faster provisioning and lower initial commitment. In the GPU cloud market, that structure matched the needs of teams testing models, running short cycles, or building initial products without strict isolation needs. It also lets providers pool capacity more efficiently across diverse customers. This made shared public environments the practical foundation of the GPU cloud market during its earlier scaling phase.

Dedicated Single-Tenant GPU Cloud is projected to expand at a 19.33% CAGR through 2031 as performance predictability and compliance requirements carry more weight in buying decisions. The GPU cloud market is seeing dedicated demand rise not only for security reasons but also because production inference pipelines cannot absorb noisy-neighbor effects when latency matters. Regulated sectors, large model operators, and high-value customer-facing systems all place a premium on stable throughput. Hosted private and sovereign configurations extend this pattern by giving enterprises dedicated hardware with operational support and clearer jurisdictional control. LIQID’s composable GPU architecture showed how dedicated environments can gain more flexibility through real-time reallocation across workloads without physical intervention. That kind of design can help the GPU cloud market narrow the efficiency gap between dedicated and shared deployment models.

By Organization Size: Enterprise Dominance Persists but Startup Disruption Is Structural

Large Enterprises held 77.12% of the GPU cloud market by organization size in 2025, which showed how much current demand still depends on buyers with deep budgets and long procurement cycles. Frontier model development, multi-year contracts, and enterprise-scale AI programs continued to absorb a large share of available capacity. In the GPU cloud market, this concentration also reflected who could secure access fastest when the premium GPU supply stayed tight. Research institutions and public-sector organizations remained important because they often validated new service models and sustained demand for advanced computing environments. Their role in the GPU cloud market has been strategic even when they have not matched enterprise spending levels.

SMEs and AI-native startups are projected to grow at a 19.43% CAGR through 2031 as managed services and per-GPU-hour pricing lower the threshold for serious AI deployment. The GPU cloud market is becoming more accessible to smaller users because developers no longer need to own the entire stack to ship production systems. RunPod’s June 2026 milestone of 1 million registered developers showed that developer-first GPU platforms had already reached meaningful commercial scale. This shift matters because smaller buyers often bring faster experimentation cycles and create demand for simplified orchestration, serverless access, and narrower workflow tools. If this trend continues, the GPU cloud market will remain enterprise-led in revenue while becoming much broader in its active user base. That combination can widen the market without fully changing who accounts for the largest current spending blocks.

By Application: AI Inference and Model Serving Redefines Workload Economics

AI Training and Fine-Tuning held 58.42% of the application segment in 2025, which showed that model development still represented the largest immediate use case for the GPU cloud market. Training remained the densest and most expensive workload category because it demanded large clusters and high memory performance over concentrated time periods. That spending pattern gave providers a strong incentive to prioritize training-friendly architectures and premium accelerator access. It also kept the GPU cloud market closely tied to the strategies of AI labs, software platforms, and research-heavy enterprises. Even so, the application mix has already begun to broaden in ways that affect provider design choices.

AI Inference and Model Serving is projected to grow at a 19.57% CAGR through 2031, which signals that the GPU cloud market is becoming more operational and service-oriented. Inference workloads usually need more stable throughput and lower tail latency than buyers can tolerate in loosely managed environments. This creates a different performance profile inside the GPU cloud market, one that values consistency and serving efficiency as much as raw peak power. NVIDIA and Eli Lilly announced in January 2026 a co-innovation AI lab for drug discovery that linked AI infrastructure, biomedical data, and next-generation compute over a multi-year period. That example showed how inference, simulation, and model improvement can sit inside a long-lived enterprise workflow rather than a one-off training event. As more deployments follow that pattern, the GPU cloud market will need to optimize for continuous business processes instead of isolated compute spikes.

By End-User Industry: Healthcare Acceleration Reframes GPU Cloud as a Life Sciences Infrastructure

IT, Telecom, Software, and Internet Platforms accounted for 66.43% of the GPU cloud market by end-user industry in 2025. This lead made sense because these organizations build AI features directly into digital products, run large inference estates, and often have the technical teams needed to adopt new compute models quickly. Their workloads span model fine-tuning, search, recommendations, customer service, and infrastructure optimization. In the GPU cloud market, this group remains the main demand anchor because it creates both training and inference consumption at scale. Its dominance also reinforces the importance of platform usability, networking performance, and broad framework support.

Healthcare, Life Sciences, and Pharmaceuticals are projected to expand at a 19.66% CAGR through 2031, which makes it the fastest-growing end-user vertical in the GPU cloud market. This shift reflects a deeper move toward GPU-backed research and production environments in drug discovery, diagnostics, and computational biology. Roche’s March 2026 deployment of more than 3,500 NVIDIA Blackwell GPUs across hybrid cloud and on-premises environments showed that large life sciences companies are treating advanced compute as a core operating asset. Compliance demands also strengthen the case for dedicated and sovereign hosting in this vertical, especially when sensitive health data and regulated workflows are involved. BFSI, automotive, manufacturing, and media continue to build demand through fraud modeling, simulation, digital twins, and rendering workloads, but healthcare is changing the profile of the GPU cloud market more structurally. It broadens the market beyond digital-native users and ties future growth to research-intensive sectors with persistent compute needs.

Geography Analysis

North America held 72.76% of the GPU cloud market in 2025, which made it the clear center of current global demand. The region benefits from the concentration of frontier AI labs, major hyperscalers, deep private capital pools, and a large base of enterprise AI adopters. In the GPU cloud market, this creates a reinforcing cycle where providers, buyers, and technical talent remain close to one another and shorten the path from infrastructure buildout to commercial use. Canada and Mexico also support the regional position through data center expansion, cross-border provisioning, and adjacency to the United States demand patterns.

Europe held the second-largest share of the GPU cloud market, and its growth path is being shaped less by raw scale and more by sovereignty requirements. Demand in the region is being pulled by compliance expectations tied to data residency, regulated AI use, and the need for stronger local control over infrastructure. This favors providers that can combine meaningful capacity with regional trust and certification positioning. Deutsche Telekom’s Munich AI factory plan showed how European incumbents are building large domestic GPU estates to support industrial and regulated use cases. Nebius also announced in June 2026 that it would invest approximately GBP 1.7 billion, approximately USD 2.16 billion, in new NVIDIA-powered infrastructure deployments in the United Kingdom. These moves show that the GPU cloud market in Europe is being built around local capacity relevance rather than volume alone.

Asia-Pacific is projected to grow at a 19.68% CAGR through 2031, which makes it the fastest-growing regional segment in the GPU cloud market. Growth is being supported by expanding domestic AI programs, rising enterprise adoption, and the need for local infrastructure that can support national and regional data requirements. Microsoft’s USD 10 billion commitment in Japan in April 2026 underscored the scale of regional investment now flowing into AI infrastructure, cybersecurity, and talent capacity. South America and the Middle East and Africa remain earlier-stage parts of the GPU cloud market, but they are developing as selective growth zones where local hosting demand and sovereign compute ambitions are starting to attract more infrastructure attention.

Competitive Landscape

The GPU cloud market has a tiered structure that separates hyperscalers, specialist neoclouds, and developer-focused platforms by scale, customer type, and service depth. AWS, Microsoft Azure, and Google Cloud set the broad reference point because they combine GPU access with mature cloud ecosystems, enterprise relationships, and integrated services. At the same time, the GPU cloud market has left room for specialist operators that focus on performance-sensitive training, dedicated inference, and faster provisioning of advanced accelerators. This has kept competition active rather than settled, even though the largest providers still hold the strongest scale advantages.

Specialist providers are gaining ground by building more focused operating models around GPU-heavy AI workloads. CoreWeave’s SEC filing and public market debut highlighted how purpose-built infrastructure, large GPU fleets, and deep data center commitments can support a differentiated position in the GPU cloud market. CoreWeave later announced the broad availability of NVIDIA HGX B300 and outlined plans to deploy NVIDIA Vera Rubin NVL72, which showed how product timing itself has become a competitive lever. Nebius added another example when it signed a long-term AI infrastructure agreement with Meta valued at USD 12 billion over five years, alongside an additional USD 15 billion purchase commitment for available compute capacity across upcoming clusters. These moves show that the GPU cloud market is being shaped by both hardware access and long-duration demand contracts.

Competitive differentiation in the GPU cloud market is also moving beyond hardware availability into orchestration, observability, scheduling, and customer workflow integration. Providers now have stronger incentives to create toolchain attachment because it can improve retention and raise the value captured above raw compute. Academic work continues to support this direction, including ACM research published in June 2026 on hybrid scheduling for fine-grained GPU sharing. That research matters because better scheduling can reduce waste and improve the economics of shared environments within the GPU cloud market. Even so, the current market still favors operators with secure accelerator supply, meaningful capital access, and the ability to scale dedicated capacity quickly.

GPU Cloud Industry Leaders

Lambda, Inc.

RunPod, Inc.

Vast.ai, Inc.

Nebius Group N.V.

CoreWeave, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: CoreWeave set a new record in the MLPerf Training v6.0 benchmark by training the DeepSeek-V3 671B model in 2.02 minutes on 8,192 NVIDIA GB300 NVL72 GPUs, the largest GB300 cluster submitted in this benchmark round. The result establishes CoreWeave Cloud as the fastest publicly validated GPU training environment for large-scale language model training.

- June 2026: Nebius announced an investment of approximately GBP 1.7 billion (approximately USD 2.16 billion) to build out 3 new NVIDIA infrastructure deployments in the United Kingdom, targeting 65 MW of combined capacity when fully ramped in 2027. This positions Nebius as one of the largest sovereign-adjacent GPU cloud investors in Europe.

- June 2026: DigitalOcean added AMD Instinct MI350X GPUs to its Agentic Inference Cloud, with plans to deploy AMD Instinct MI355X GPUs in the subsequent quarter, expanding its GPU Droplet portfolio with liquid-cooled racks optimized for large-scale inference.

- June 2026: RunPod launched Flash as a generally available production SDK, enabling Python-native serverless GPU deployment without Docker containers. The tool eliminates a major developer friction point in serverless GPU development workflows and positions RunPod as an orchestration layer above raw compute provisioning.

Global GPU Cloud Market Report Scope

The GPU Cloud Market refers to the market for cloud-based services that provide on-demand access to GPU compute resources over the internet. These platforms let users rent high-performance GPUs for AI training, inference, rendering, simulation, and other compute-intensive workloads without buying hardware.

The GPU Cloud Market Report is Segmented by Service Model (IaaS, PaaS), GPU Workload Class (AI Training and Large-Scale HPC GPU Instances, AI Inference and General Accelerated Compute GPU Instances, Graphics, Visualization, Rendering, and VDI GPU Instances, and Cost-Optimized and Legacy GPU Instances), Hosting Model (Shared Multi-Tenant Public GPU Cloud, Dedicated Single-Tenant GPU Cloud, Hosted Private GPU Cloud, and Sovereign and Regulated GPU Cloud), Organization Size (Large, SMEs, and Research Institutions, Academia, and Public-Sector Organizations), Application (AI Training and Fine-Tuning, AI Inference and Model Serving, High-Performance Computing and Scientific Simulation, Rendering, Animation, VFX, and Virtual Production, and Cloud Gaming), End-User (IT, Telecom, Software, and Internet Platforms, Media, Entertainment, Gaming, and Advertising, BFSI, Automotive, Mobility, and Autonomous Systems, Healthcare, Life Sciences, and Pharmaceuticals, and Manufacturing, Semiconductor, and Industrial), and Geography (North America, Europe, Asia-Pacific, South America, MEA). The Market Forecasts are Provided in Terms of Value (USD).

| Infrastructure as a Service |

| Platform as a Service |

| AI Training and Large-Scale HPC GPU Instances |

| AI Inference and General Accelerated Compute GPU Instances |

| Graphics, Visualization, Rendering, and VDI GPU Instances |

| Cost-Optimized and Legacy GPU Instances |

| Shared Multi-Tenant Public GPU Cloud |

| Dedicated Single-Tenant GPU Cloud |

| Hosted Private GPU Cloud |

| Sovereign and Regulated GPU Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| Research Institutions, Academia, and Public-Sector Organizations |

| AI Training and Fine-Tuning |

| AI Inference and Model Serving |

| High-Performance Computing and Scientific Simulation |

| Rendering, Animation, VFX, and Virtual Production |

| Cloud Gaming |

| Others (Visualization, Virtual Workstations, and Digital Twins) |

| IT, Telecom, Software, and Internet Platforms |

| Media, Entertainment, Gaming, and Advertising |

| BFSI |

| Automotive, Mobility, and Autonomous Systems |

| Healthcare, Life Sciences, and Pharmaceuticals |

| Manufacturing, Semiconductor, and Industrial |

| Other End-User Industries (Retail and E-Commerce, Energy and Utilities) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Service Model | Infrastructure as a Service | |

| Platform as a Service | ||

| By GPU Workload Class | AI Training and Large-Scale HPC GPU Instances | |

| AI Inference and General Accelerated Compute GPU Instances | ||

| Graphics, Visualization, Rendering, and VDI GPU Instances | ||

| Cost-Optimized and Legacy GPU Instances | ||

| By Hosting Model | Shared Multi-Tenant Public GPU Cloud | |

| Dedicated Single-Tenant GPU Cloud | ||

| Hosted Private GPU Cloud | ||

| Sovereign and Regulated GPU Cloud | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| Research Institutions, Academia, and Public-Sector Organizations | ||

| By Application | AI Training and Fine-Tuning | |

| AI Inference and Model Serving | ||

| High-Performance Computing and Scientific Simulation | ||

| Rendering, Animation, VFX, and Virtual Production | ||

| Cloud Gaming | ||

| Others (Visualization, Virtual Workstations, and Digital Twins) | ||

| By End-User Industry | IT, Telecom, Software, and Internet Platforms | |

| Media, Entertainment, Gaming, and Advertising | ||

| BFSI | ||

| Automotive, Mobility, and Autonomous Systems | ||

| Healthcare, Life Sciences, and Pharmaceuticals | ||

| Manufacturing, Semiconductor, and Industrial | ||

| Other End-User Industries (Retail and E-Commerce, Energy and Utilities) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and future size of the GPU cloud market?

The GPU cloud market stood at USD 7.73 billion in 2025, reaches USD 15.62 billion in 2026, and is forecast to reach USD 37.69 billion by 2031 at a 19.26% CAGR.

Which service model leads GPU cloud spending today?

Infrastructure as a Service leads the service mix with a 78.66% share in 2025 because many customers still want direct control over GPU resources and cluster settings.

What is growing fastest in GPU cloud workloads?

AI Inference and General Accelerated Compute GPU Instances are expanding fastest at a 19.41% CAGR through 2031 as production AI systems create steady serving demand.

Why are dedicated deployments gaining traction?

Dedicated Single-Tenant GPU Cloud is projected to grow at a 19.33% CAGR because enterprises increasingly need predictable performance, stronger isolation, and better support for regulated workloads.

Which end-user group creates the most demand right now?

IT, Telecom, Software, and Internet Platforms hold the largest share at 66.43% in 2025 because they run both large training programs and continuous inference at scale.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is projected to grow at a 19.68% CAGR as regional AI infrastructure investment and local hosting needs continue to expand.

Page last updated on: