Predictive Carbon Forecasting and Scenario Modeling Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.59 Billion |

| Market Size (2031) | USD 3.66 Billion |

| Growth Rate (2026 - 2031) | 18.09% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Predictive Carbon Forecasting and Scenario Modeling Software Market Analysis by Mordor Intelligence

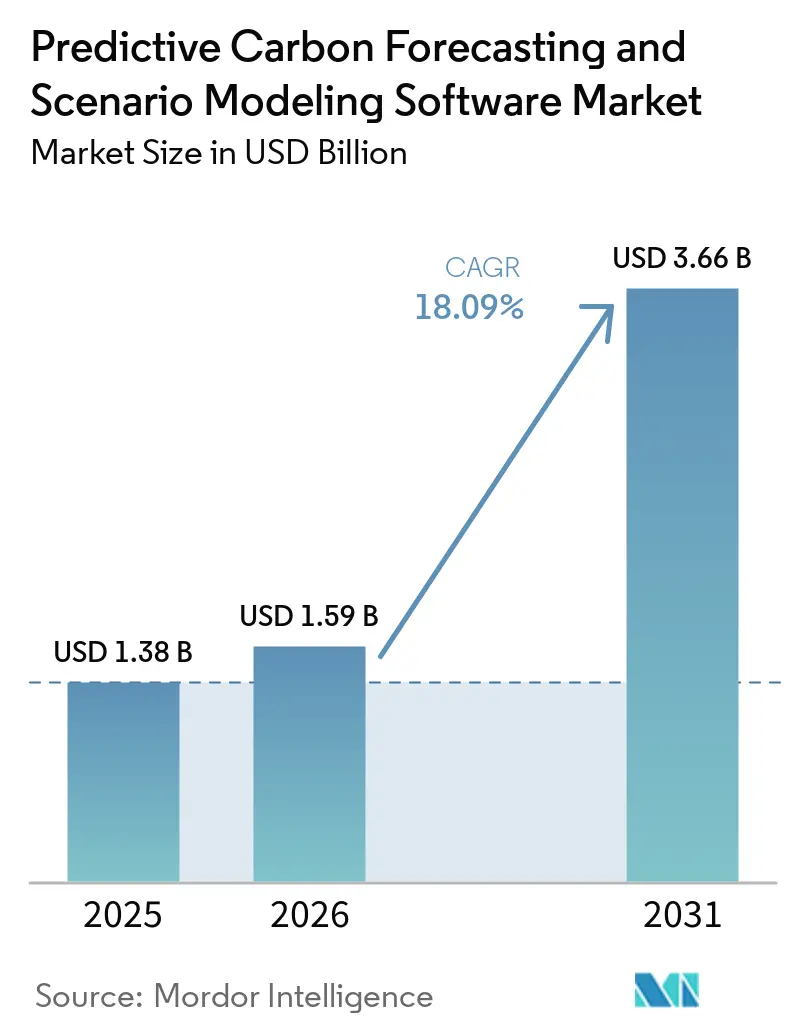

The predictive carbon forecasting and scenario modeling software market size is projected to expand from USD 1.38 billion in 2025 and USD 1.59 billion in 2026 to USD 3.66 billion by 2031, registering a CAGR of 18.09% between 2026 and 2031. The market moved beyond periodic emissions reporting and became more closely tied to planning cycles, board reviews, and capital allocation decisions, which lifted demand for software that can test carbon outcomes under different business and policy conditions. Climate exposure is now more often treated as a financial planning issue, so buyers are looking for tools that connect emissions pathways with operating choices, supply chain risks, and portfolio decisions. Competitive activity is also shifting, as large enterprise software vendors embed baseline carbon functions into broader cloud and ERP environments, while specialized vendors focus on deeper modeling, stronger audit trails, and faster scenario testing. AI-led workflow improvements are reducing simulation time and data preparation effort, which is changing buyer expectations around usability and speed. The result is a predictive carbon forecasting and scenario modeling software market that remains high-growth but is becoming more selective, with long-term opportunity moving toward vendors that can combine modeling depth, decision support, and credible regulatory coverage.

Key Report Takeaways

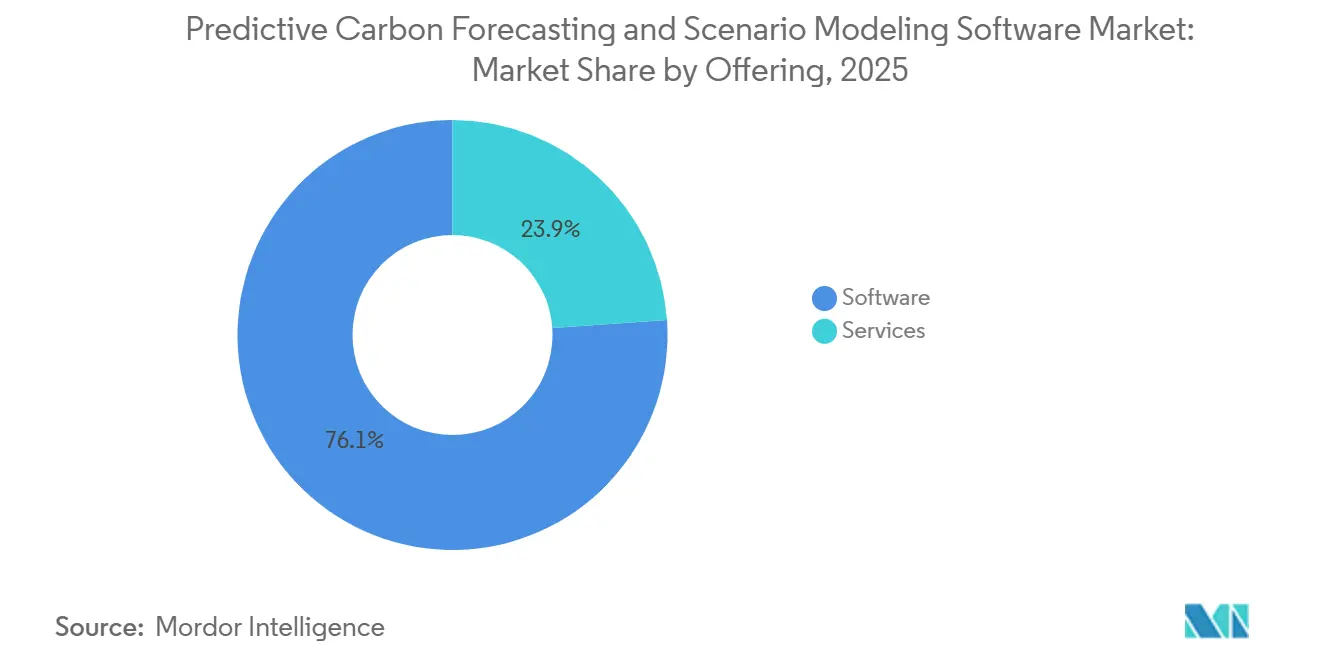

- By offering, software accounted for 76.12% of the predictive carbon forecasting and scenario modeling market share in 2025 revenue, while services are projected to expand at a 21.54% CAGR through 2031.

- By deployment mode, cloud-based deployments accounted for 65.13% of revenue in 2025 and are projected to expand at a 20.92% CAGR through 2031.

- By application, climate scenario and pathway modeling accounted for 33.12% share of the predictive carbon forecasting and scenario modeling software market size in 2025, while climate and transition risk assessment is projected to expand at a 22.37% CAGR through 2031.

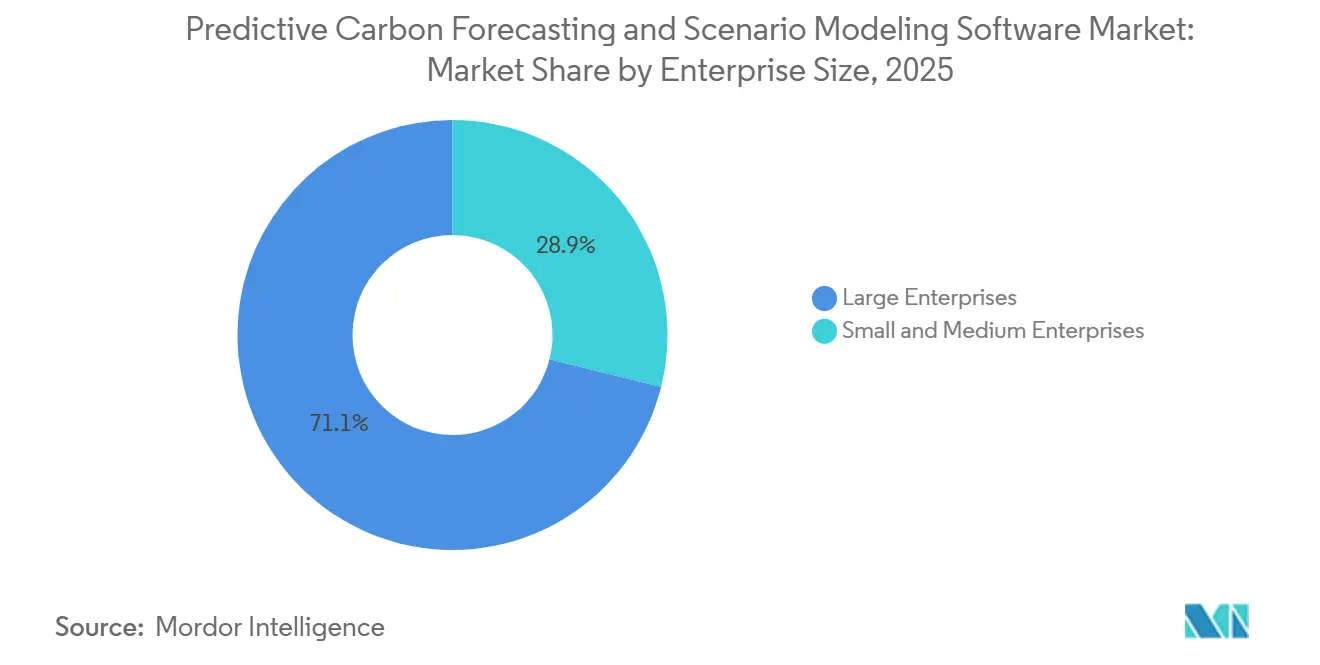

- By enterprise size, large enterprises held 71.12% of the predictive carbon forecasting and scenario modeling software market share in 2025, while small and medium enterprises are projected to expand at a 22.71% CAGR through 2031.

- By end-user industry, energy and utilities accounted for 22.24% of revenue in 2025, while BFSI is projected to expand at a 24.12% CAGR through 2031.

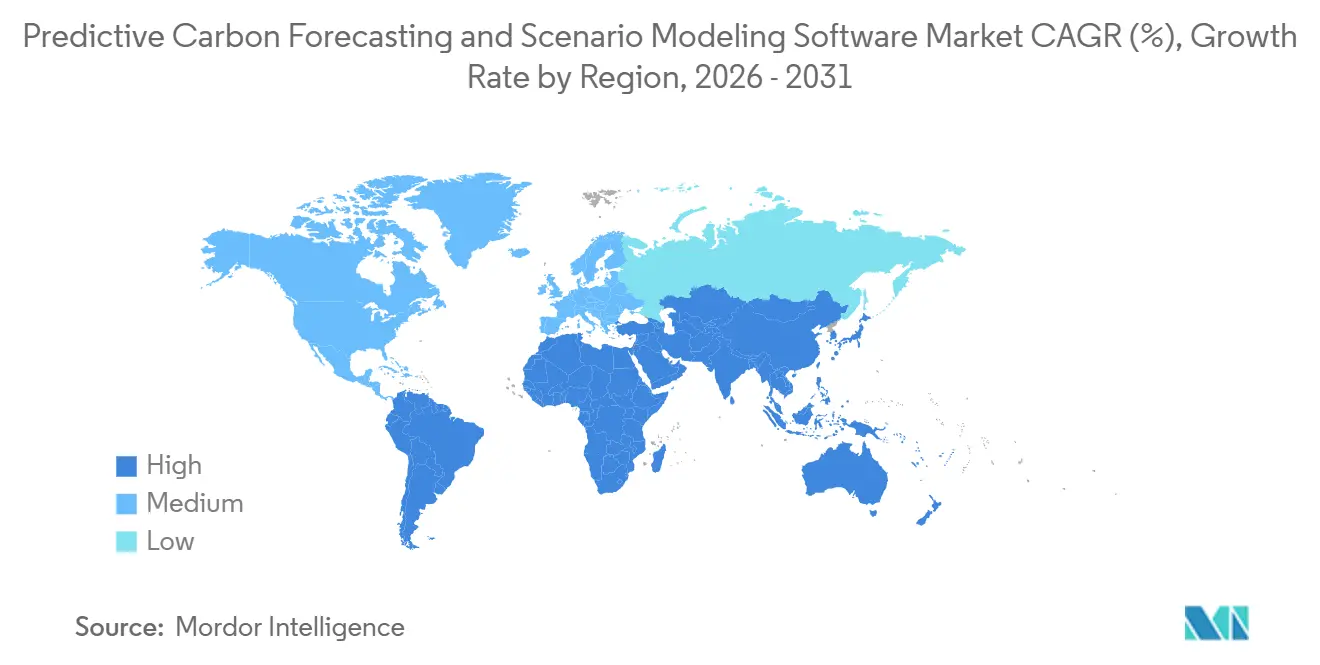

- By geography, North America held 35.12% revenue share in 2025, while Asia-Pacific is projected to expand at a 22.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Predictive Carbon Forecasting and Scenario Modeling Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Pressure on Climate Disclosures and Net-Zero Planning | +3.5% | Global, with concentrated compliance demand in Europe, the United Kingdom, Singapore, Australia, and California | Short term (≤ 2 years) |

| Integration of AI for Emissions Forecasting and Abatement Pathway Optimization | +3.2% | Global, with early adoption concentrated in North America and Western Europe | Medium term (2-4 years) |

| Rising Enterprise Demand for Forward-Looking Carbon Scenario Planning | +2.6% | North America and Europe core, with spillover to Asia-Pacific and the Middle East | Short term (≤ 2 years) |

| Expansion of ESG-Linked Capital Allocation and Board-Level Climate Governance | +2.2% | Global, with early gains in institutional investor-heavy markets across North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Growing Adoption of Cloud-Based Sustainability Platforms in Large Enterprises | +1.9% | North America and Europe primary, with accelerating uptake in Asia-Pacific | Medium term (2-4 years) |

| Need to Quantify Transition Risk Across Supplier, Asset, and Portfolio Decisions | +1.6% | Asia-Pacific core, with spillover to the Middle East and Africa and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Pressure on Climate Disclosures and Net-Zero Planning

Regulatory pressure remains the most immediate driver of software demand, as disclosure rules now require companies to organize carbon data to support planning, verification, and scenario testing rather than simple year-end reporting. The IFRS Foundation updated greenhouse gas disclosure requirements under IFRS S2 in December 2025 to reduce implementation complexity while preserving decision-useful reporting, helping sustain enterprise demand as reporting expectations evolved across market.[1]IFRS Foundation, “IFRS S2 Climate-Related Disclosures,” IFRS Foundation, ifrs.org The United States introduced uncertainty when the SEC proposed rescinding its climate disclosure rules in May 2026, but that did not remove the broader demand for decision-ready tools, as many companies still operate across multiple reporting regimes and face investor expectations. This matters for the predictive carbon forecasting and scenario modeling software market because scenario analysis is increasingly treated as part of financial governance, not only as a sustainability compliance task. Vendors that frame their tools as planning infrastructure are therefore better positioned than vendors that depend mainly on compliance checklists. The effect is that the predictive carbon forecasting and scenario modeling software market continues to benefit from regulation even when individual rules are revised, delayed, or challenged.

Integration of AI for Emissions Forecasting and Abatement Pathway Optimization

AI is reshaping how carbon software is used because buyers now expect faster data cleaning, quicker simulations, and more interactive interpretation of results within a single workflow. SAP stated in May 2026 that its Footprint Optimization Agent reduced scenario simulation time from around 1 day to 20 minutes, demonstrating how software competition is moving toward faster response times and greater operational usability.[2]SAP SE, “Autonomous Enterprise, New Sustainability AI Agents,” SAP News Center, news.sap.com A peer-reviewed study published in April 2026 also found that coordinated deep-learning architectures outperformed traditional baseline methods for predicting carbon emissions in energy-intensive industries, supporting the broader move toward AI-driven forecasting models. That shift expands the role of these tools from static emissions reporting into active pathway selection, transaction-level analysis, and faster decision support. It also raises the bar for product design in the predictive carbon forecasting and scenario modeling software market, because buyers will compare not only model breadth but also the time needed to reach a usable answer. As more platforms embed AI natively, the predictive carbon forecasting and scenario modeling software market is likely to further separate between vendors with strong technical depth and those that only automate surface-level reporting tasks.

Rising Enterprise Demand for Forward-Looking Carbon Scenario Planning

Enterprise demand is rising because companies increasingly need to test how carbon exposure could affect budgets, asset use, supplier choices, and longer-term capital decisions under different transition pathways. That need is especially visible as carbon planning moves closer to finance teams, risk teams, and executive committees that want forward-looking outputs rather than historical emissions snapshots. In April 2025, one survey reported that 79% of companies had already disclosed emissions across all three scopes, while 47% of non-reporting firms planned to begin Scope 3 disclosure within 2 years, suggesting a growing pipeline of buyers for more advanced modeling tools.[3]Sphera Solutions, “Sphera’s 2025 Scope 3 Report Reveals Sustainability Progress Despite Persistent Data Challenges,” Sphera, sphera.com The practical result is that the predictive carbon forecasting and scenario modeling software market is not growing only because new buyers are entering, but also because existing users are moving from measurement toward pathway optimization and transition risk analysis. Demand is not uniform: mature organizations are seeking deeper scenario layers, while many mid-sized buyers are still building data foundations. Vendors that can support both stages without weakening premium functionality are in a stronger position within the predictive carbon forecasting and scenario modeling software market.

Expansion of ESG-Linked Capital Allocation and Board-Level Climate Governance

Investor and board scrutiny is reinforcing adoption, as companies are increasingly expected to demonstrate that their decarbonization plans are credible, measurable, and tied to capital decisions. In 2025, Norges Bank Investment Management published its 2030 Climate Action Plan and made clear that board-level climate engagement remains part of its stewardship approach, signaling that large investors prefer structured planning over narrative commitments alone. Allianz Global Investors also tightened its 2026 voting policy expectations regarding the quality and material alignment of ESG metrics, increasing pressure on companies to support climate-linked performance claims with stronger analytical evidence. This makes the predictive carbon forecasting and scenario modeling software market more relevant to governance functions because outputs from these tools increasingly inform discussions around incentives, strategic priorities, and resilience under changing transition conditions. The driver is structurally important because investor oversight tends to persist even when policy cycles become less predictable. As a result, the predictive carbon forecasting and scenario modeling software market is gaining support from governance channels that are less tied to a single reporting season or jurisdiction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Quality and Availability of Scope 3 and Supplier Activity Data | -2.4% | Global, most acute in markets with deep and fragmented supply chains such as Southeast Asia, South Asia, and Central Europe | Medium term (2-4 years) |

| High Integration Complexity With ERP, EHS, and Data-Lake Environments | -2.1% | Global, with particular severity in multi-ERP environments common in Asia-Pacific and South America | Short term (≤ 2 years) |

| Budget Scrutiny and Slow ROI Realization for Mid-Market Buyers | -1.8% | North America and Europe, particularly affecting buyers in the USD 50 million to USD 500 million revenue band | Short term (≤ 2 years) |

| Model Credibility Concerns From Assumption Sensitivity and Audit Scrutiny | -1.4% | Global, intensified in jurisdictions requiring limited or reasonable assurance under major climate reporting frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Quality and Availability of Scope 3 and Supplier Activity Data

Supplier data quality remains the largest operating constraint, because the most material emissions categories are often the least standardized and the hardest to verify across complex value chains. In April 2025, one survey found that 79% of organizations identified supplier data availability as their top challenge, while 62% pointed to internal data quality as a major barrier, which shows that reporting maturity has not solved the input problem. Another study noted that Scope 3 emissions often account for more than 75% of a company’s total emissions and that supplier data gaps remain the main obstacle to accurate quantification.[4]MIT Sloan Management Review, “Supply Chain Sustainability, Top Ways Firms Track Scope 3 Emissions,” MIT Sloan Management Review, mitsloan.mit.edu That weakness directly affects the predictive carbon forecasting and scenario modeling software market because models can only be as credible as the data used to train, map, and test them. Companies can still use spend-based proxies and estimation logic, but those methods weaken confidence when investors, auditors, or procurement teams need greater precision. Until supplier participation improves at scale, the predictive carbon forecasting and scenario modeling software market will continue to face a practical ceiling on how far model outputs can be trusted in high-stakes decisions.

High Integration Complexity With ERP, EHS, and Data-Lake Environments

Integration complexity slows adoption because carbon planning tools need to pull information from finance systems, procurement records, logistics data, utility inputs, and operational platforms that were not designed around shared emissions logic. Research published in January 2025 found that carbon footprint management within ERP environments faces high integration costs, structural data mismatches, and technical compatibility issues, especially for Scope 3 and product-level use cases. The problem becomes harder in multi-ERP companies, post-acquisition environments, and firms that still rely on inconsistent master data across regions and business units. That slows time-to-value in the predictive carbon forecasting and scenario modeling software market because implementation often becomes a broad data architecture project rather than a direct application rollout. Cloud-native vendors are responding with connectors and managed ingestion layers, but those measures reduce effort rather than eliminate it. Integration, therefore, remains a meaningful adoption barrier in the predictive carbon forecasting and scenario modeling software market, especially for buyers with limited internal data engineering capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Platforms Anchored Revenue While Services Scaled

Software accounted for 76.12% of revenue in 2025, indicating that licensed platforms remained the center of enterprise spending in the predictive carbon forecasting and scenario modeling market. Buyers increasingly favored tools they could use repeatedly across reporting, planning, and risk review cycles rather than relying solely on project-led advisory work. This pattern also indicates that many organizations had already moved past early scoping exercises and started embedding carbon analysis into routine operating processes. In that setting, platform ownership matters because recurring access enables faster updates, broader internal use, and more consistent governance of assumptions and audit trails. It also gives vendors a stronger basis for product improvement because subscription revenue can be reinvested in modeling depth, AI functionality, and workflow design.

Services are still expanding faster, with a projected CAGR of 21.54% through 2031, because software alone does not remove the need for implementation support, scenario design, and interpretation of results. Many organizations can collect basic emissions data, but they still need external help to build credible abatement pathways, stress-test commitments, and prepare outputs for investor or auditor review. This means service growth is not a sign of weak software adoption, but rather that the predictive carbon forecasting and scenario modeling software market is moving into more complex use cases. As modeling becomes more material to strategy, buyers are more willing to pay for expert support around model setup and governance. Over time, this creates a linked revenue pattern in which software remains the anchor and services grow as an attached layer around deeper adoption. The predictive carbon forecasting and scenario modeling software market, therefore, shows a mature software core with a growing advisory edge, rather than a choice between the 2 models.

By Deployment Mode: Cloud Architecture Captured Adoption Scale

Cloud-based deployment accounted for 65.13% of revenue in 2025, reflecting enterprise demand for flexible platforms that can handle large data volumes, support regular updates, and enable scenario testing across different business units. In the predictive carbon forecasting and scenario modeling software market, cloud deployment reduces infrastructure friction and enables centralization of emissions data, scenario libraries, and user access across global operations. It also supports faster product updates when rules, pathways, and disclosure requirements change. That is important in a category where models must be refreshed as assumptions evolve and as companies widen their Scope 3 coverage. Cloud architecture further helps vendors deliver analytics features that require greater computing capacity and shared model environments.

Cloud-based deployment is projected to expand at a 20.92% CAGR through 2031, indicating that the largest model remains the fastest-growing in the predictive carbon forecasting and scenario modeling software market. In May 2026, one vendor introduced a cloud-native platform designed to deliver an audit-ready baseline within weeks while reducing data-collection effort, underscoring why buyers associate cloud models with faster setup and lower operating drag. On-premise environments still matter for institutions with strict control needs, and hybrid models remain useful where data residency or contractual sensitivity is a concern. Even so, new deployments continue to favor the cloud because the value of faster onboarding, shared access, and easier scaling is hard to match through local infrastructure. This dynamic gives cloud vendors more room to widen their reach inside the predictive carbon forecasting and scenario modeling software market. It also encourages product design that assumes continuous data ingestion and frequent scenario iteration rather than infrequent batch analysis.

By Application: Scenario Modeling Led While Transition Risk Assessment Grew Fastest

Climate scenario and pathway modeling accounted for 33.12% of revenue in 2025, confirming that this function remained the core use case in the predictive carbon forecasting and scenario modeling software market. Companies need these models to test how different transition pathways could affect assets, operations, and long-range planning assumptions. The segment also benefited from the fact that scenario analysis has moved closer to mainstream governance and disclosure processes. As a result, it became the most established entry point for buyers who wanted more than backward-looking carbon measurement. In many organizations, scenario modeling also serves as a basis for later add-ons, such as supplier analysis, risk layering, and capital planning.

Climate and transition risk assessment is projected to grow at a 22.37% CAGR through 2031, indicating where the next wave of demand is building in the predictive carbon forecasting and scenario modeling software market. This faster growth suggests that companies are extending climate analysis beyond board disclosures into underwriting, procurement screening, asset reviews, and portfolio management. The application is gaining traction because users increasingly want to connect emissions pathways with cost exposure, financing conditions, and operational resilience. That broadens the commercial scope of the predictive carbon forecasting and scenario modeling software market, since transition risk tools can be used across finance, supply chain, and strategy teams rather than just by sustainability functions. It also raises the need for clearer scenario assumptions, stronger evidence trails, and better links to internal planning systems. Over the forecast period, the predictive carbon forecasting and scenario modeling software market is likely to see more spending shift toward tools that help users move from pathway viewing to decision-ready risk evaluation.

By Enterprise Size: Large Enterprises Led While SMEs Expanded Faster

Large enterprises accounted for 71.12% of revenue in 2025, reflecting that the predictive carbon forecasting and scenario modeling software market has so far been driven by organizations with the budget, data depth, and governance pressure needed for enterprise-wide deployment. Large companies often operate across regions, suppliers, and asset classes, so they have a stronger need for platforms that can coordinate multiple reporting boundaries and scenario assumptions. They are also more exposed to investor scrutiny and board oversight, which makes climate planning more visible at the executive level. In practice, this gave large enterprises an early adoption advantage because they could absorb longer implementation cycles and support dedicated carbon management teams. Their scale also made the payback case easier, where financing, procurement, or portfolio decisions were directly affected by transition risk.

Small and medium enterprises are projected to expand at a 22.71% CAGR through 2031, which signals a widening buyer base for the predictive carbon forecasting and scenario modeling software market. Growth in this segment is being pushed less by internal governance and more by commercial pressure from larger customers, lenders, and supply chain partners that increasingly expect verified carbon data. Cloud pricing, faster onboarding, and lighter implementation models are also improving access for firms without large sustainability teams. This does not mean SMEs are buying the same tools in the same way as large corporations. Instead, many are entering the predictive carbon forecasting and scenario modeling software market through narrower workflows that focus on disclosure readiness, customer reporting, and basic scenario planning. As these firms mature, some will move into more advanced abatement and transition analysis. That progression gives vendors room to build tiered product strategies that capture smaller buyers without losing enterprise depth.

By End-User Industry: Energy and Utilities Anchored Revenue While BFSI Accelerated

Energy and utilities accounted for 22.24% of revenue in 2025, making the segment the largest end-user segment in the predictive carbon forecasting and scenario modeling software market. This leadership aligns with the sector’s exposure to both physical and transition risks, as long-life assets, fuel shifts, and grid investment decisions all require scenario-based planning. These companies also face large emissions baselines and significant capital commitments, which makes the quality of forecasting and abatement modeling more consequential. In many cases, software is used not only to estimate future emissions but also to compare retirement, retrofit, and renewable integration pathways. That creates a strong need for tools that link operational assumptions to financial and regulatory outcomes.

BFSI is projected to expand at a 24.12% CAGR through 2031, which makes it the fastest-growing end-user segment in the predictive carbon forecasting and scenario modeling software market. Banks, insurers, and asset managers increasingly need tools that can quantify financed emissions, portfolio alignment, and transition exposure across clients, sectors, and investment books. Their use case is distinct because value depends less on owned operational emissions and more on the quality of scenario logic applied to lending, underwriting, and asset allocation. This creates space for vendors that can support portfolio-level modeling, institution-wide controls, and stronger evidence chains for governance review. It also means the predictive carbon forecasting and scenario modeling software market is broadening from an operational emissions category into a financial risk and allocation category. As this shift continues, BFSI demand is likely to shape product roadmaps around portfolio analytics, cross-entity comparisons, and clearer scenario explainability.

Geography Analysis

North America accounted for 35.12% of revenue in 2025, making it the largest regional contributor to the predictive carbon forecasting and scenario modeling software market. The region benefits from a dense base of listed companies, mature software procurement practices, and a strong concentration of enterprise platform vendors. It also has a deep investor ecosystem that tends to push climate reporting and planning issues into board and finance discussions sooner than in less mature enterprise software markets. The United States remained the main demand center because many large companies already had disclosure processes and internal controls that could be extended into carbon planning workflows. This gave the predictive carbon forecasting and scenario modeling software market a strong commercial base in North America, even as the federal policy environment became less consistent.

Asia-Pacific is projected to expand at a 22.91% CAGR through 2031, which makes it the fastest-growing regional segment in the predictive carbon forecasting and scenario modeling software market. A broader shift toward formal climate disclosure requirements, rising decarbonization investment, and the growing need for supplier-level carbon visibility across export-oriented production networks support growth in the region. China added an important technology signal in April 2026 when the Chinese Academy of Sciences released the Panshi Yuheng carbon accounting large model v1.0, showing active development of domestic carbon modeling infrastructure NEA.GOV.CN. That matters because regional adoption is not driven solely by imported compliance frameworks, but also by local capability-building and industrial policy goals. The predictive carbon forecasting and scenario modeling software market, therefore, has room to grow in Asia-Pacific through both multinational demand and local platform development.

Europe continues to provide a strong base for the predictive carbon forecasting and scenario modeling software market because climate governance is already embedded in many corporate reporting and risk management processes. Even where reporting simplification has reduced some compliance burden, scenario analysis remains closely tied to how enterprises frame material climate exposure and long-term planning. South America is still smaller, but export-oriented sectors and financial institutions are creating selective demand for more structured carbon planning tools. The Middle East and Africa remain early-stage markets, yet interest is rising as state energy companies, sovereign investors, and listed firms are building more formal climate transition roadmaps. Across these regions, the predictive carbon forecasting and scenario modeling software market is most likely to grow where buyers can connect compliance needs with practical planning value rather than treat software as a reporting-only purchase.

Competitive Landscape

The predictive carbon forecasting and scenario modeling software market is still moderately fragmented, with enterprise incumbents and climate-focused specialists competing from different angles. Large platforms like SAP, Microsoft, Salesforce, IBM, and Oracle leverage scale, existing customer bases, and integration with finance and operational systems. Meanwhile, specialists such as Persefoni, Watershed, Sweep, Normative, and CarbonChain differentiate through deeper climate workflows, stronger audit trails, and carbon-specific product design. This creates a competitive landscape shaped less by uniform dominance and more by whether vendors succeed through distribution breadth or modeling depth.

Strategic activity in 2026 underscored how quickly vendors are sharpening product value by focusing on speed, integration, and data credibility. SAP introduced its Footprint Optimization Agent, cutting simulation time from about a day to 20 minutes, highlighting the race toward faster execution and interactive analysis. EcoVadis and Workiva announced a partnership linking supplier carbon data with Workiva Carbon, signaling stronger end-to-end value chain coordination. IFS launched IFS Zero for asset-intensive industries, reinforcing the importance of vertical relevance and rapid onboarding. These moves show that the market rewards solutions that address both upstream data challenges and downstream decision needs within a unified platform.

White space remains in SME-accessible tiers, sector-specific scenario libraries, and tighter links between carbon outputs and broader planning systems. Heavy industry, BFSI, and supplier-intensive sectors still need more tailored workflows than generic carbon tools can provide. As basic accounting features become standard in enterprise suites, higher-value growth will concentrate in platforms that defend their position through credible scenario modeling, decision support, and seamless integration with core business processes. The market is therefore evolving toward a sharper divide between broad feature coverage and truly decision-grade modeling capability.

Predictive Carbon Forecasting and Scenario Modeling Software Industry Leaders

SAP SE

Salesforce, Inc.

Microsoft Corporation

Persefoni AI, Inc.

Watershed Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: EcoVadis and Workiva Inc. announced a strategic partnership connecting EcoVadis' Carbon Data Network (CDN) with Workiva Carbon, enabling mutual customers to collect, calculate, and coordinate GHG emissions data across entire value chains with investor-grade accuracy. The integration directly addresses the Scope 3 supplier data quality constraint that affects 79% of enterprise reporters, positioning both platforms competitively in the audit-ready disclosure segment.

- May 2026: SAP SE unveiled new sustainability AI agents at SAP Sapphire, including the Footprint Optimization Agent, which reduces scenario simulation time from approximately one day to 20 minutes. The agents, expected to be generally available by end of 2026, also gather Scope 1, 2, and 3 data and identify emission hotspots, addressing a data accuracy gap where industry-average ESG figures deviate 30-40% or more from actuals.

- May 2026: IFS launched IFS Zero, an agentic Emissions Operating System for asset-intensive industries, providing a unified platform for measuring, disclosing, and optimizing Scope 1, 2, and 3 emissions. The solution, launched alongside IFS Cloud 26R1 on May 28, 2026, targets a 30% reduction in data collection effort and an audit-ready baseline within weeks, with Generation Investment Management research estimating IFS technology could help abate over 2% of global CO₂ with full adoption across its 3 largest industrial sectors.

- April 2026: China's Institute of Advanced Studies, Chinese Academy of Sciences, released the "Panshi Yuheng" carbon accounting large model v1.0 on April 8, 2026, the world's first panoramic carbon accounting system covering production-side, consumption-side, and natural-source emissions in a unified framework. The model supports China's national carbon market construction and provides a domestic alternative to international scenario modeling architectures.

Global Predictive Carbon Forecasting and Scenario Modeling Software Market Report Scope

The Predictive Carbon Forecasting and Scenario Modeling Software market refers to platforms and services that enable organizations to anticipate future carbon emissions, assess climate-related risks, and plan decarbonization strategies through advanced analytics and scenario modeling. These solutions provide functionalities such as emissions forecasting, climate scenario and pathway modeling, transition risk assessment, abatement optimization, and sustainability reporting. By embedding predictive intelligence into enterprise operations, these platforms help organizations align with global climate targets, comply with ESG frameworks, and make data-driven decisions for long-term resilience.

The Predictive Carbon Forecasting and Scenario Modeling Software market report is segmented by Offering (Software, and Services), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Application (Emissions Forecasting, Climate Scenario and Pathway Modeling, Climate and Transition Risk Assessment, and Decarbonization Planning and Abatement Optimization), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (BFSI, Energy and Utilities, Oil and Gas, Manufacturing and Industrial, Transportation and Logistics, Technology and Telecommunications, Retail and Consumer Goods, and Other Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Emissions Forecasting |

| Climate Scenario and Pathway Modeling |

| Climate and Transition Risk Assessment |

| Decarbonization Planning and Abatement Optimization |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Energy and Utilities |

| Oil and Gas |

| Manufacturing and Industrial |

| Transportation and Logistics |

| Technology and Telecommunications |

| Retail and Consumer Goods |

| Other Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By offering | Software | ||

| Services | |||

| By Deployment Mode | Cloud-Based | ||

| On-Premise | |||

| Hybrid | |||

| By Application | Emissions Forecasting | ||

| Climate Scenario and Pathway Modeling | |||

| Climate and Transition Risk Assessment | |||

| Decarbonization Planning and Abatement Optimization | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End User Industry | BFSI | ||

| Energy and Utilities | |||

| Oil and Gas | |||

| Manufacturing and Industrial | |||

| Transportation and Logistics | |||

| Technology and Telecommunications | |||

| Retail and Consumer Goods | |||

| Other Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size outlook for the predictive carbon forecasting and scenario modeling software market?

The predictive carbon forecasting and scenario modeling software market was valued at USD 1.38 billion in 2025, stood at USD 1.59 billion in 2026, and is projected to reach USD 3.66 billion by 2031 at an 18.09% CAGR.

What is driving adoption of carbon scenario modeling platforms?

The main demand drivers are tighter climate disclosure expectations, stronger investor and board scrutiny, rising need for forward-looking planning, and faster AI-enabled modeling workflows.

Which application area is growing the fastest through 2031?

Climate and transition risk assessment is the fastest-growing application, with a projected 22.37% CAGR, as buyers connect carbon pathways with financial and operational decisions.

Why do large enterprises still lead spending in this space?

Large enterprises held 71.12% of revenue in 2025 because they face heavier governance pressure, larger data integration needs, and broader cross-border reporting and planning requirements.

Which region shows the strongest growth potential?

Asia-Pacific is projected to grow the fastest at a 22.91% CAGR through 2031, supported by stronger disclosure expectations, industrial decarbonization activity, and expanding local modeling capability.

Which end-user group is expanding the quickest?

BFSI is projected to grow at a 24.12% CAGR through 2031, driven by financed emissions analysis, portfolio alignment work, and climate risk assessment across lending and investment activities.

Page last updated on: