Carbon Disclosure Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.38 Billion |

| Market Size (2031) | USD 5.62 Billion |

| Growth Rate (2026 - 2031) | 18.75% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Carbon Disclosure Software Market Analysis by Mordor Intelligence

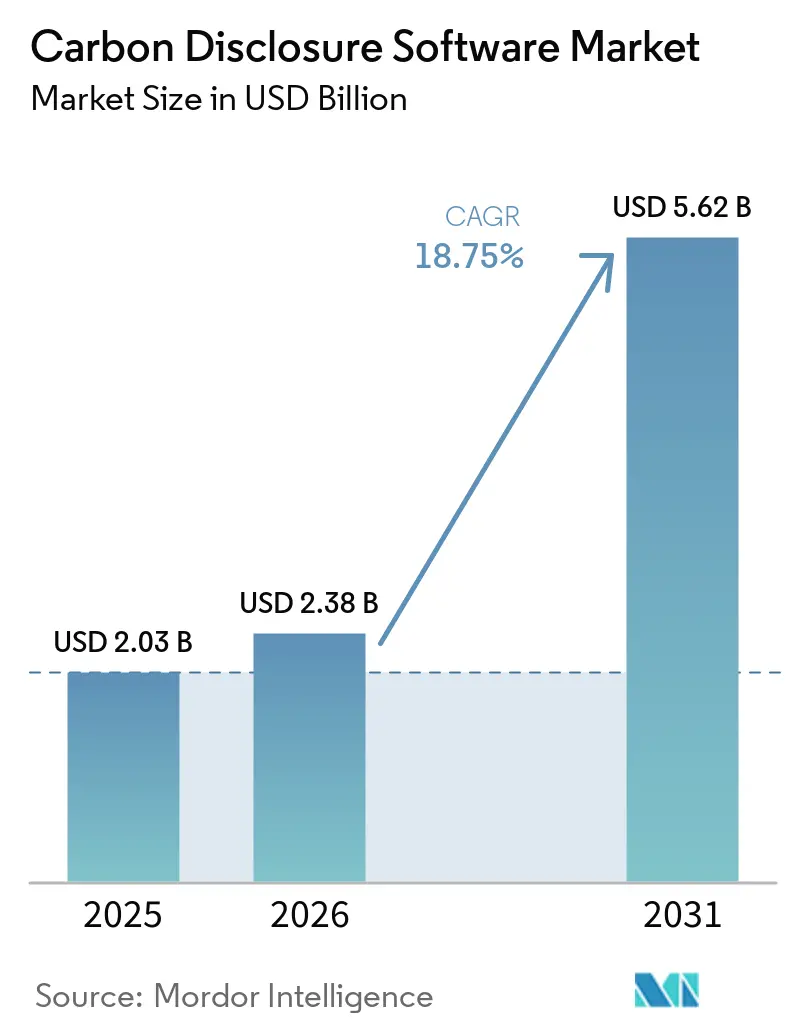

The carbon disclosure software market size is projected to be USD 2.03 billion in 2025, USD 2.38 billion in 2026, and reach USD 5.62 billion by 2031, growing at a CAGR of 18.75% from 2026 to 2031. Growth is sustained by a combination of mandatory disclosure rules, lender and investor scrutiny, and better enterprise data systems that support recurring reporting cycles rather than one-time filing exercises. Regulatory changes across Europe, North America, and Asia-Pacific have widened the number of companies that need formal carbon records, even though the timing and scope differ by jurisdiction. Capital markets are reinforcing this shift because sustainability-linked debt and labeled bond activity now depend more heavily on verified greenhouse gas information, which gives enterprises a financial reason to keep audit-ready systems in place. Vendors are also moving beyond basic reporting tools and competing more directly on data lineage, supplier network reach, and AI-assisted workflow automation. Even with risks tied to policy timing, privacy concerns, and ERP interoperability, the structural need for reliable carbon data keeps the carbon disclosure software market on a durable growth path.

Key Report Takeaways

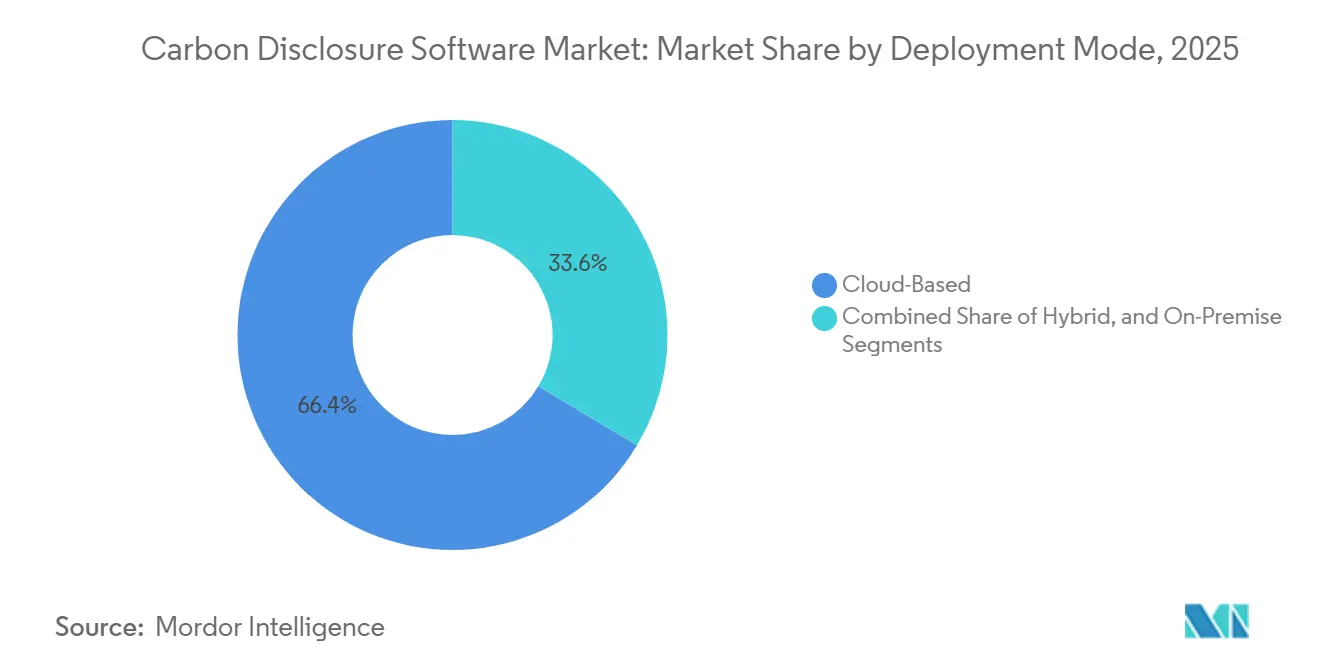

- By deployment mode, cloud-based solutions accounted for 66.42% of revenue in 2025, while hybrid deployment is projected to expand at the fastest CAGR of 19.87% from 2026 to 2031.

- By enterprise size, large enterprises held 64.15% share in 2025, while small and medium enterprises are expected to record the fastest CAGR of 21.34% through 2031.

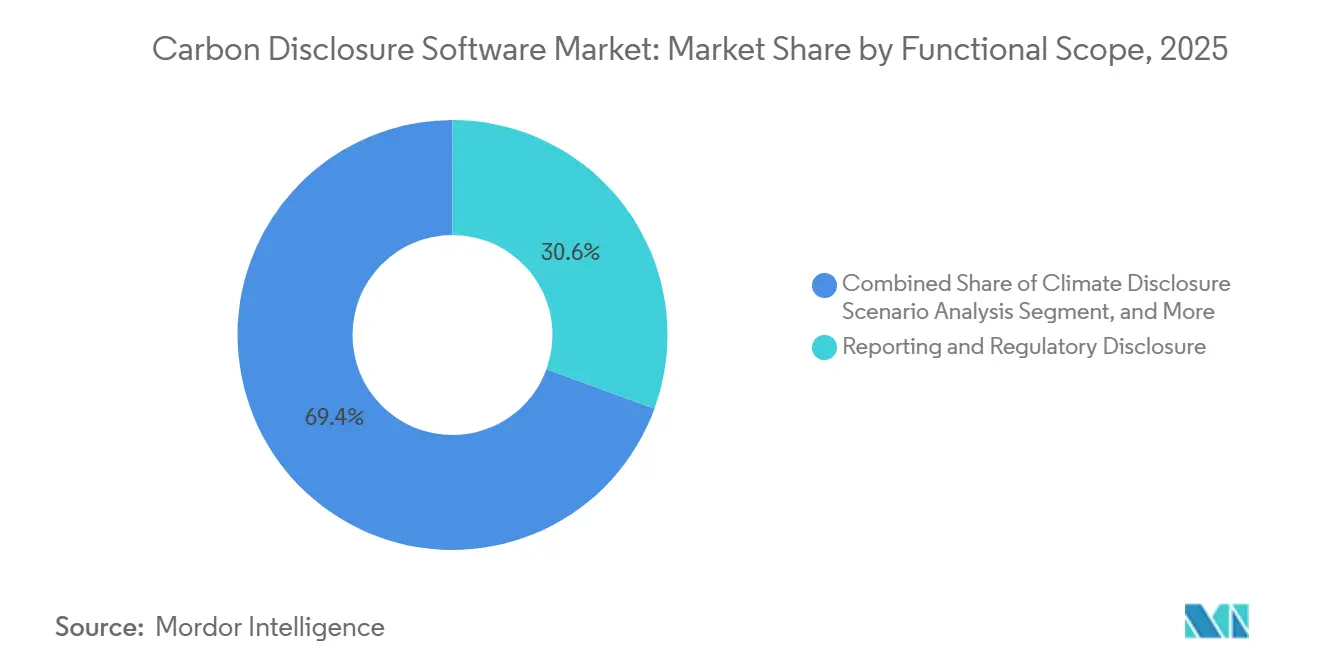

- By functional scope, Reporting and Regulatory Disclosure captured 30.56% of revenue in 2025, while Climate Disclosure Scenario Analysis is projected to grow at the fastest CAGR of 22.45% from 2026 to 2031.

- By end-user industry, industrial manufacturing accounted for 27.84% of revenue in 2025, while energy and utilities are projected to expand at the fastest CAGR of 20.91% through 2031.

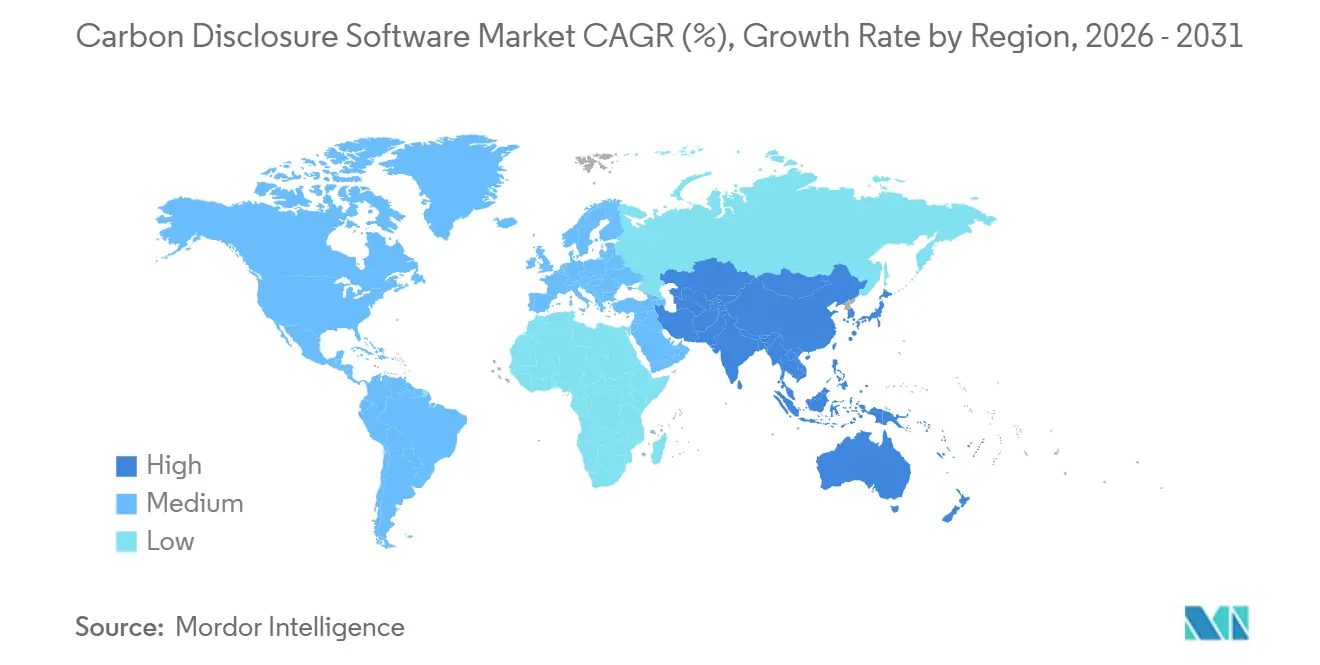

- By geography, Europe held 35.12% share in 2025, while Asia-Pacific is expected to expand at the fastest CAGR of 24.63% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Carbon Disclosure Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Global Climate Disclosure Mandates | +4.2% | Global, with EU, North America, and APAC as core jurisdictions | Short term (≤ 2 years) |

| Rising Scope 3 Supplier Data Digitization | +3.8% | Global, EU and North America as primary demand anchors | Medium term (2-4 years) |

| Enterprise Shift to Cloud-Native Sustainability Stacks | +3.1% | Global | Medium term (2-4 years) |

| Audit-Ready Carbon Data for Sustainability-Linked Finance | +2.4% | Global, primarily EU and North America | Medium term (2-4 years) |

| EU Digital Product Passport and Product-Level Traceability | +1.8% | EU core, spill-over to global supply chains | Medium term (2-4 years) |

| Generative AI For Automated Data Collection and Reconciliation | +2.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Global Climate Disclosure Mandates

The carbon disclosure software market is being driven by the expanding set of rules that now require formal climate reporting across several jurisdictions simultaneously. In Europe, the CSRD framework and the March 2026 Omnibus revision maintained disclosure obligations for larger entities above the revised employee and turnover thresholds, thereby preserving a large compliance base for software adoption.[1]European Commission, “Corporate Sustainability Reporting,” European Commission, finance.ec.europa.eu That matters because companies now need systems that can store calculation methods, source documentation, and assurance trails in a structured way, rather than keeping fragmented spreadsheets. North America and Asia-Pacific add another layer of demand through state rules, phased reporting programs, and newer national climate disclosure standards, reducing the risk that a single regulatory delay can fully halt spending. China’s Ministry of Finance also issued Corporate Sustainable Disclosure Standard No. 1, Climate (Trial) in December 2025, which adds another formal policy anchor for the carbon disclosure software market in Asia-Pacific.

Rising Scope 3 Supplier Data Digitization

Scope 3 reporting remains one of the strongest growth supports for the carbon disclosure software market because supplier information is both essential and difficult to collect at scale. Sphera’s 2026 survey of more than 1,000 sustainability leaders found that 73% of organizations voluntarily disclose Scope 3 data, 89% plan further expansion, and only 45% have limited confidence in the accuracy of their current data, indicating a wide gap between reporting ambition and readiness.[2]Sphera, “The 2026 Sphera Scope 3 Report,” Sphera, sphera.com That gap creates steady demand for platforms that can gather primary supplier data, separate estimates from verified inputs, and preserve a usable audit trail across categories. The carbon disclosure software market also benefits when large buyers repeatedly request the same data from smaller suppliers, turning disclosure from a periodic task into an ongoing workflow across procurement, sustainability, and finance teams. As supplier requests become more machine-readable and more frequent, software that standardizes submissions and reconciles inconsistent source records is becoming part of the core reporting stack.

Enterprise Shift To Cloud-Native Sustainability Stacks

A clear move toward cloud-native deployment is also shaping the carbon disclosure software market as companies replace fragmented tools with platforms that can support audit-ready reporting. European disclosure rules increasingly require detailed methodology notes, visible source tracking, and consistent data lineage, which are easier to manage when updates, controls, and user access are centralized. This is one reason older installations built for limited reporting use cases are losing ground to platforms designed around shared data models and continuous updates. Watershed’s work on automated utility bill ingestion and SAP’s plan to make new sustainability AI agents broadly available by the end of 2026 both show how platform design is moving toward always-on collection, validation, and workflow support.[3]Watershed Technology, “AI-Powered ESG Reporting, Any Metric, Any Report,” Watershed, watershed.com As a result, buyers in the carbon disclosure software market are comparing vendors less on template coverage alone and more on whether one platform can support subsidiaries, joint ventures, suppliers, and legacy systems without heavy manual reconciliation.

Generative AI For Automated Data Collection And Reconciliation

Generative AI is changing the operating model of the carbon disclosure software market by reducing the labor tied to collection, cleaning, and reconciliation. Watershed said in April 2026 that its AI agents reduced time to disclosure-ready data by 80%, and one implementation completed a 5-hour manual project in 20 minutes, which shows how quickly automation is moving into everyday reporting work. These productivity gains matter because data preparation still absorbs a large share of sustainability team time, especially when records arrive through invoices, utility bills, supplier spreadsheets, or non-standard documents. As that work becomes more automated, teams can spend more time on planning, supplier engagement, and decision support, which helps explain why advanced modules are gaining traction across the carbon disclosure software market. Vendors that combine AI speed with clear audit trails and review controls are likely to hold a stronger position as enterprise buyers look for both efficiency and defensibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Data Quality And Methodology Complexity | -1.8% | Global | Short term (≤ 2 years) |

| SME Budget And Change-Management Constraints | -1.2% | Global, heightened pressure in EU and APAC mid-market | Medium term (2-4 years) |

| Supplier Data Privacy And Commercial Sensitivity Concerns | -0.9% | Global, particularly EU, APAC, and supply-chain-dense industries | Medium term (2-4 years) |

| Fragmented Global Reporting Standards And Overlapping Frameworks | -1.1% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Data Quality And Methodology Complexity

The carbon disclosure software market still faces a major barrier in the gap between collected emissions data and audit-ready disclosure inputs. Research published in 2025 showed that many SMEs lack automated reporting systems and methodological expertise, and that first-year CSRD implementation costs ranged from EUR 5,000 (USD 5,400) to EUR 18,000 (USD 19,440), making early adoption difficult for smaller firms. This challenge goes beyond simple data availability because assurance reviewers increasingly expect source transparency, visibility into primary-versus-secondary data, and repeatable controls across categories. Companies that bought earlier carbon tools without strong provenance features are now facing migration work as reporting deadlines tighten. The result is longer implementation cycles and slower near-term conversion for parts of the carbon disclosure software market.[4]Springer Nature, “Recommended Features for Digital Reporting Systems to Support Emissions Disclosures for Small and Medium-Sized Enterprises,” Springer Nature, link.springer.com

SME Budget And Change-Management Constraints

Budget and change-management limits create a separate drag on the carbon disclosure software market, especially in supplier-heavy value chains. Smaller firms are often drawn into carbon reporting through customer requests rather than direct legal obligations, making internal spending approval harder to secure. The same 2025 research on SME disclosure systems showed that even entry-level compliance work can take a meaningful share of operating budgets when outside support is required. This pressure is one reason why self-serve products, modular subscriptions, and lighter onboarding models are becoming more important across the carbon disclosure software market. Until buying, training, and data ownership become easier for smaller firms, adoption is likely to rise in uneven steps rather than in a straight line.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Hybrid Architecture Extends Cloud Efficiency To Regulated Data Environments

Cloud-based solutions accounted for 66.42% of the carbon disclosure software market share in 2025, underscoring buyers' preference for scalable platforms with lower infrastructure requirements. The carbon disclosure software market leaned toward cloud delivery because regulatory content changes, collaboration needs, and ERP integrations are easier to manage in a centralized software environment. Purpose-built vendors such as Watershed, Persefoni, and Sweep helped normalize this model by building their products from the start around faster updates, distributed user access, and shared data workflows. On-premises deployment remained relevant for government users, utilities, and financial institutions where data residency rules or internal security standards limit the free movement of operating data.

Hybrid deployment is the fastest-growing segment of the carbon disclosure software market, with a projected CAGR of 19.87% from 2026 to 2031. Demand is strongest in industrial and energy settings where enterprises want cloud analytics and reporting but still keep sensitive plant or operational data under tighter internal control. This pattern becomes more visible when carbon records are tied to production yields, facility throughput, or product-level calculations that buyers do not want to move entirely into external environments. Vendors are responding with secure data gateways and local validation layers, so the carbon disclosure software market can support both cloud reporting speed and stronger control over source data

By Enterprise Size: SME Demand Accelerates As Supply Chain Mandates Cascade

Large enterprises held 64.15% of the carbon disclosure software market in 2025, reflecting earlier compliance exposure and the budget capacity needed for multi-framework software rollouts. The carbon disclosure software market first expanded most rapidly in larger organizations because these buyers had to align subsidiaries, lenders, auditors, and multiple reporting frameworks simultaneously. This group also had a stronger need for formal controls, recurring assurance support, and centralized records that could withstand investor and board scrutiny. Sustainability-linked debt reinforced that pattern because issuers need annual independent verification of greenhouse gas performance under widely used market principles, which supports recurring platform use rather than one-time filing activity.

Small and medium enterprises are projected to grow at the fastest CAGR of 21.34% from 2026 to 2031 in the carbon disclosure software market. Much of this demand is coming through supply chains, as large buyers now ask smaller suppliers for primary emissions data even when mandatory rules do not directly cover those suppliers. Research published in 2025 showed that first-year CSRD implementation costs for SMEs ranged from EUR 5,000 (USD 5,400) to EUR 18,000 (USD 19,440), which explains why lower-cost, guided tools are gaining traction. The carbon disclosure software market is therefore evolving into a two-tier structure, with enterprise-grade systems serving complex organizations and lighter self-serve tools competing for adoption within supplier networks.

By Functional Scope: Scenario Analysis Emerges As The Strategic Value Anchor

Reporting and Regulatory Disclosure held 30.56% of revenue in 2025, making it the largest functional category in the carbon disclosure software market. The earliest software purchase still starts with the need to produce compliant and externally defensible outputs rather than with advanced planning tools. That has kept framework mapping, XBRL support, and disclosure workflow control close to the center of product design as the carbon disclosure software market continues to mature. Assurance and audit readiness are also gaining weight because disclosure rules increasingly require a documented chain of evidence for how records were collected, reviewed, and approved.

Climate Disclosure Scenario Analysis is the fastest-growing segment of the carbon disclosure software market, with a projected CAGR of 22.45% from 2026 to 2031. This shift shows that buyers are moving beyond backward-looking reporting and investing more in tools that connect emissions pathways to business planning. Companies now need to explain how strategy performs across different climate pathways, which raises demand for modules that link operational data, transition assumptions, and financial outcomes in a single place. As a result, the carbon disclosure software market is giving more strategic value to vendors that combine reporting depth with planning capability instead of offering disclosure templates alone.

By End-User Industry: Industrial Manufacturing Anchors Demand While Energy And Utilities Accelerate

Industrial manufacturing accounted for 27.84% of revenue in 2025 in the carbon disclosure software market, making it the largest end-user segment. Demand stayed strong because manufacturers faced both company-level disclosure rules and product-level carbon documentation requirements. The first carbon-footprint declaration requirement for EV batteries took effect on February 18, 2026, reinforcing software spending on traceability, product data management, and supplier documentation. Sphera’s Supplier PCF Calculator and its later work with Rolls-Royce Power Systems showed how the carbon disclosure software market is moving deeper into product workflows, rather than remaining limited to corporate disclosure activity.

Energy and utilities are projected to expand at the fastest CAGR of 20.91% from 2026 to 2031 in the carbon disclosure software market. Utilities need credible emissions records for transition planning, disclosure compliance, and capital raising tied to environmental performance. The same demand for verifiable data keeps BFSI active because financed emissions reporting depends on reliable portfolio-level carbon records and consistent methodology. Retail, IT and telecom, healthcare, government, and transportation add breadth to the carbon disclosure software market as digital product data, procurement requirements, and operating disclosures become more formal across sectors.

Geography Analysis

Europe accounted for 35.12% of revenue in 2025 and held the largest regional position in the carbon disclosure software market. The region remains ahead because climate reporting has already moved from policy design into live filing, assurance review, and vendor selection across large enterprises. The March 2026 revision, which focused mandatory coverage on companies with more than 1,000 employees and net turnover above EUR 450 million (USD 486 million), narrowed the scope but increased the importance of robust reporting systems for the largest in-scope entities. Product-level traceability rules, including the battery carbon-footprint declaration requirement, add another layer of platform demand across European manufacturing.

North America remained the second-largest regional cluster in the carbon disclosure software market, supported by voluntary reporting, investor pressure, and state-level disclosure rules. California’s SB 253 kept large enterprises focused on Scope 3 readiness, even while the federal climate disclosure agenda remained less predictable. The region also benefits from a deep base of enterprise software buyers, lenders, and multinational companies that need auditable emissions data across their operations and supply chains. South America is smaller today, but listed company ESG requirements in Brazil and the development of a framework aligned with ISSB guidance are widening future demand for the carbon disclosure software market.

Asia-Pacific is the fastest-growing region in the carbon disclosure software market, with a projected CAGR of 24.63% from 2026 to 2031. Japan’s ISSB-aligned filing path, Australia’s phased Scope 3 rollout, and China’s climate disclosure framework are pushing the region toward more formal compliance. China’s Ministry of Finance issued Corporate Sustainable Disclosure Standard No. 1, Climate (Trial) in December 2025, and the Ministry of Ecology and Environment had already published voluntary greenhouse gas disclosure guidance in March 2025, which strengthened the policy base for enterprise reporting. The region’s role as the main production base for global manufacturing also matters because suppliers are receiving more carbon data requests from customers in Europe and North America. The Middle East and Africa remain smaller in absolute terms, but sovereign finance programs, exchange requirements, and public-sector reporting are steadily expanding the addressable market for carbon disclosure software.

Competitive Landscape

The carbon disclosure software market remains moderately fragmented, with purpose-built specialists and ERP-linked vendors competing on regulatory depth, data architecture, and supplier-network reach rather than on brand scale alone. Vendors such as Persefoni, Watershed, Sweep, Normative, and Sphera compete with larger enterprise software providers that are embedding sustainability tools into broader cloud suites. This structure keeps the carbon disclosure software market open enough for specialist innovation while still requiring vendors to demonstrate they can support audit-grade workflows across multiple frameworks. As buyer expectations rise, the gap is widening between platforms built for continuous reporting operations and tools that still depend on lighter template-based processes.

Agentic AI has become one of the clearest differentiators in the carbon disclosure software market. Watershed reported in April 2026 that its AI agents reduced the time to disclosure-ready data by 80%, demonstrating how quickly automation is moving into routine collection, cleaning, and analysis tasks. SAP’s plan to make new sustainability AI agents broadly available by the end of 2026 also shows that carbon disclosure is being drawn into core enterprise process design instead of sitting at the edge of software budgets. In practical terms, the carbon disclosure software market is rewarding vendors that can combine automation speed with control, reviewability, and a usable evidence trail.

Strategic partnerships and product-level carbon tools are shaping the next phase of competition in the carbon disclosure software market. Sphera’s January 2026 work with Rolls-Royce Power Systems on Environmental Product Declarations showed how vendors can move from company disclosure into engineering and product certification workflows. Sweep and Arcadis also formed a global partnership in 2025 to combine software with implementation support, thereby widening Sweep’s reach among large enterprise buyers. Vendors that can cover product carbon footprints, supplier data exchange, and formal disclosure within a single environment are likely to capture a larger share of the consolidation opportunity ahead. The carbon disclosure software market still leaves room for specialists, but the entry bar keeps rising as buyers now expect AI capabilities, assurance-ready controls, and cross-framework coverage in a single system.

Carbon Disclosure Software Industry Leaders

Persefoni AI, Inc.

Watershed Technology, Inc.

SAP SE

Microsoft Corporation

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Persefoni AI launched the Persefoni Analytics Agent, an agentic AI tool enabling enterprise sustainability teams to interact with emissions data via natural language queries and generate in-depth visualizations; the platform has supported more than 500 enterprise customers and 9,000+ organizations globally, reinforcing its audit-grade carbon disclosure positioning.

- April 2026: Watershed launched a suite of AI data agents at San Francisco Climate Week, including agents for data cleaning and analysis; test customers reduced time to disclosure-ready data by 80%, with one implementation completing a 5-hour manual project in 20 minutes, demonstrating transformative efficiency gains for Scope 3 dataset management.

- March 2026: Watershed expanded its AI reporting platform to cover all ESG metrics with an AI-assisted report builder and conversational advisor, enabling companies to manage non-standard data, produce reports aligned with any framework, and receive AI-generated gap analysis and audit-perspective reviews.

- February 2026: The European Parliament and Council published the CSRD Content Directive (EU 2026/470) in the Official Journal on February 27, 2026, revising mandatory CSRD reporting thresholds to companies with more than 1,000 employees and net turnover exceeding EUR 450 million (approximately USD 486 million), materially narrowing the mandatory scope while concentrating compliance investment among the largest remaining in-scope entities.

Global Carbon Disclosure Software Market Report Scope

The Carbon Disclosure Software market comprises digital solutions that help organizations manage, report, and verify climate-related data in compliance with global disclosure frameworks such as CDP, TCFD, and ISSB. These platforms provide functionality including disclosure data management, regulatory reporting, assurance and audit readiness, analytics and performance insights, and climate risk scenario analysis.

The Carbon Disclosure Software market report is segmented by Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Functional Scope (Disclosure Data Management, Reporting and Regulatory Disclosure, Assurance, Verification and Audit Readiness, Disclosure Analytics and Performance Insights, Climate Disclosure Scenario Analysis), End-user Industry (Industrial Manufacturing, Energy and Utilities, BFSI, Retail and Consumer Goods, IT and Telecom, Healthcare and Life Sciences, Government and Public Sector, Transportation and Logistics, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Disclosure Data Management |

| Reporting and Regulatory Disclosure |

| Assurance, Verification and Audit Readiness |

| Disclosure Analytics and Performance Insights |

| Climate Disclosure Scenario Analysis |

| Industrial Manufacturing |

| Energy and Utilities |

| BFSI |

| Retail and Consumer Goods |

| IT and Telecom |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Transportation and Logistics |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Functional Scope | Disclosure Data Management | |

| Reporting and Regulatory Disclosure | ||

| Assurance, Verification and Audit Readiness | ||

| Disclosure Analytics and Performance Insights | ||

| Climate Disclosure Scenario Analysis | ||

| By End-user Industry | Industrial Manufacturing | |

| Energy and Utilities | ||

| BFSI | ||

| Retail and Consumer Goods | ||

| IT and Telecom | ||

| Healthcare and Life Sciences | ||

| Government and Public Sector | ||

| Transportation and Logistics | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the size of the carbon disclosure software market?

The carbon disclosure software market stood at USD 2.38 billion in 2026, up from USD 2.03 billion in 2025, and is projected to reach USD 5.62 billion by 2031 at a CAGR of 18.75%.

Which region leads carbon disclosure software adoption?

Europe led with 35.12% share in 2025 because CSRD filing, assurance review, and taxonomy-linked reporting have already moved into active implementation.

Which region is growing the fastest through 2031?

Asia-Pacific is projected to expand at a 24.63% CAGR from 2026 to 2031, supported by Japans ISSB-aligned pathway, Australias phased Scope 3 rollout, and Chinas evolving climate disclosure framework.

Which deployment model is most widely used today?

Cloud-based deployment led with 66.42% share in 2025 because buyers favored scalable systems with easier updates, collaboration, and ERP connectivity.

Why are SMEs becoming more important for software vendors?

SMEs are projected to grow at a 21.34% CAGR through 2031 as large enterprise customers push supplier networks to provide primary emissions data for Scope 3 reporting.

Which end-user group is creating the strongest demand?

Industrial manufacturing led with 27.84% share in 2025, while energy and utilities is projected to grow fastest at 20.91% CAGR because both sectors need auditable carbon data for compliance and capital access.

Page last updated on: