Labor Optimization And Demand Forecasting Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.63 Billion |

| Market Size (2031) | USD 2.23 Billion |

| Growth Rate (2026 - 2031) | 6.48% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Labor Optimization And Demand Forecasting Software Market Analysis by Mordor Intelligence

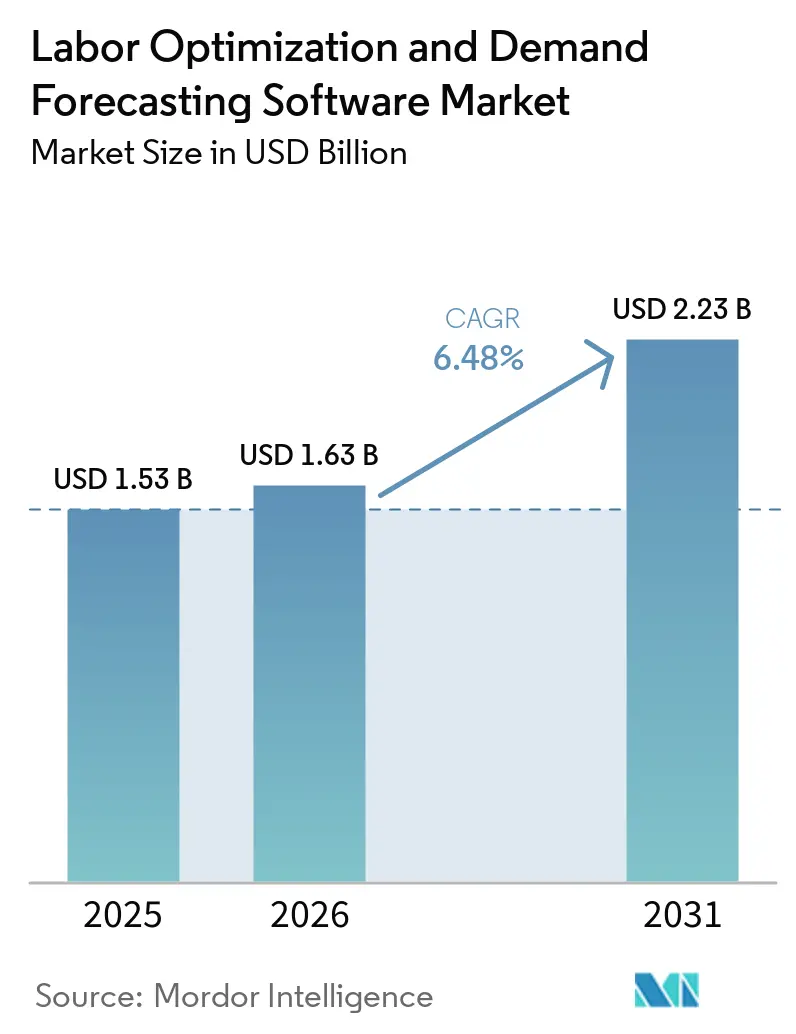

The labor optimization and demand forecasting software market size is expected to increase from USD 1.53 billion in 2025 to USD 1.63 billion in 2026 and reach USD 2.23 billion by 2031, growing at a CAGR of 6.48% over 2026-2031. The market is moving beyond basic scheduling because employers now need a single system that connects staffing plans, operating budgets, frontline execution, and regulatory compliance. AI-led planning tools are making these platforms more valuable because they can respond to demand shifts faster than older workforce systems. Buyers are also placing greater weight on measurable labor outcomes, which is pushing vendors to integrate forecasting, scheduling, analytics, and task execution into a tighter workflow. Demand is broadening across large enterprises and mid-sized employers as compliance pressure, wage inflation, and labor volatility make manual planning harder to sustain. Competitive activity is also increasing as workforce management specialists, supply chain software providers, and vertical-focused firms all expand their product depth and geographic reach.

Key Report Takeaways

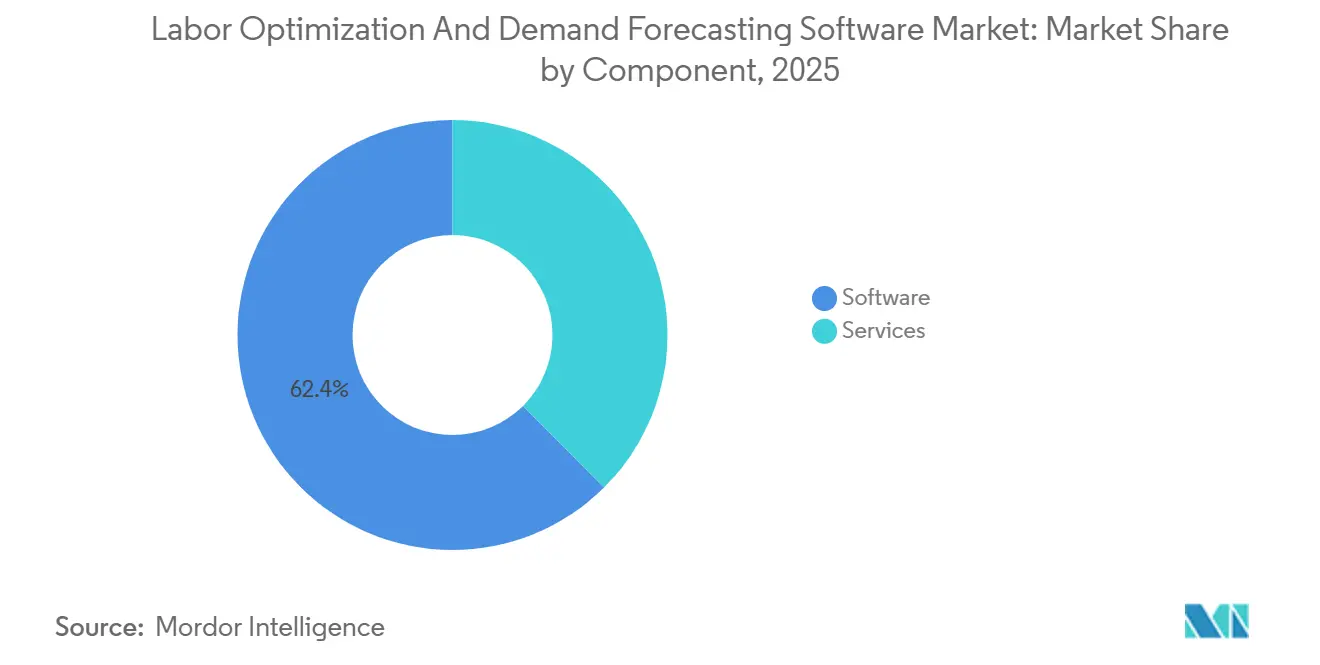

- By component, software held 62.44% of the labor optimization and demand forecasting software marketrevenue in 2025, while services recorded the highest projected CAGR at 9.12% through 2031.

- By functionality, demand forecasting accounted for 35.45% of revenue in 2025, while workforce analytics and performance optimization is projected to expand at an 8.36% CAGR through 2031.

- By deployment model, on-premise held 67.34% of the labor optimization and demand forecasting software market revenue in 2025, while cloud-based deployment is forecast to grow at a 9.91% CAGR through 2031.

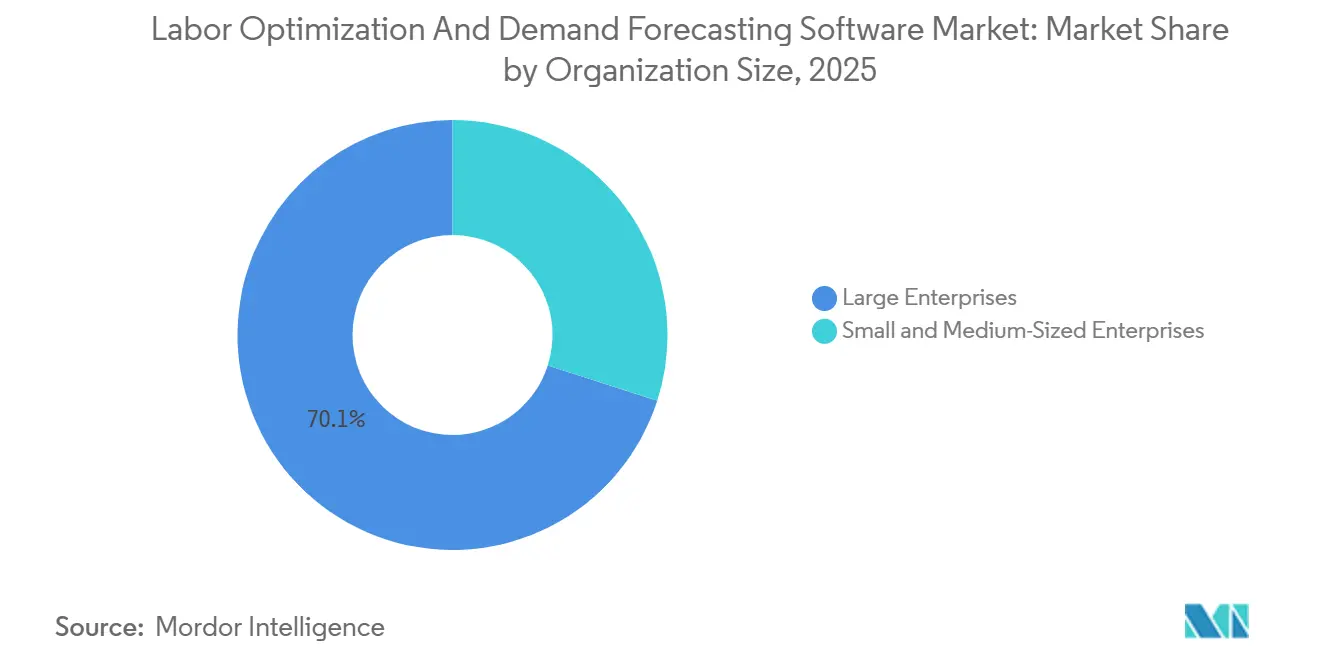

- By organization size, large enterprises held 70.05% of revenue in 2025, while SMEs are projected to expand at a 9.56% CAGR through 2031.

- By end-use industry, retail and e-commerce accounted for 34.65% of the labor optimization and demand forecasting software market revenue in 2025, while healthcare and life sciences is forecast to grow at a 7.89% CAGR through 2031.

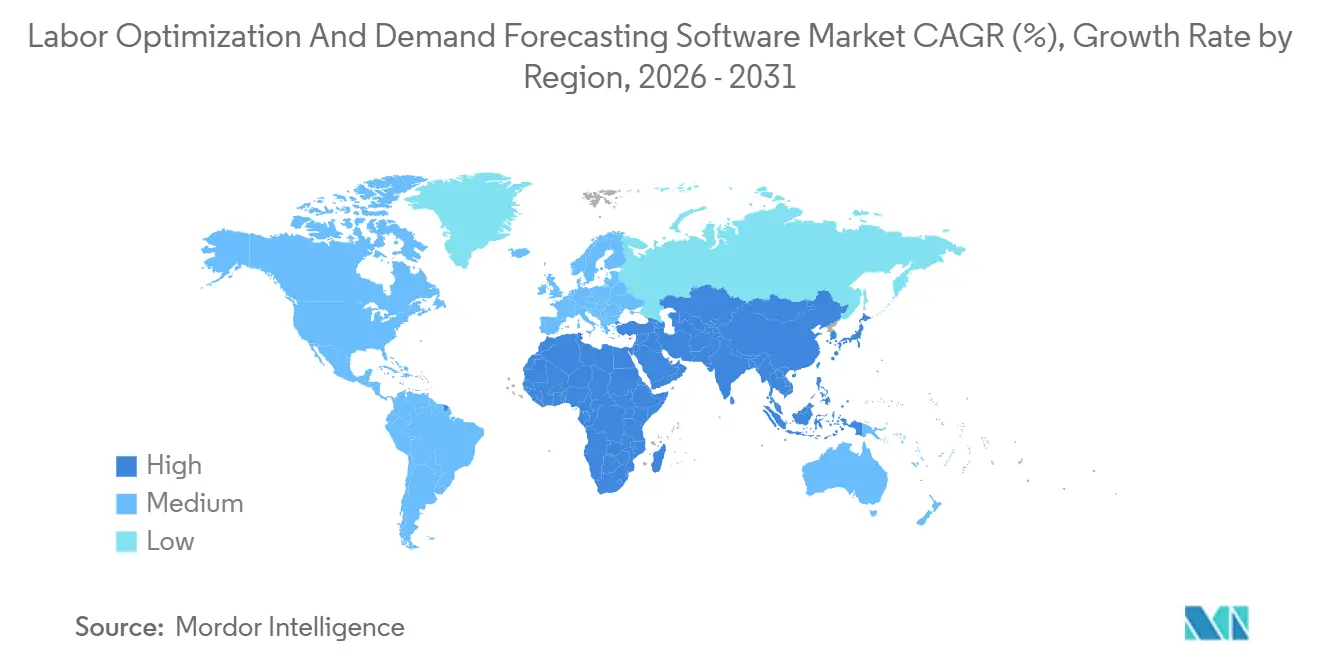

- By geography, North America held 36.81% of revenue in 2025, while Asia-Pacific is projected to expand at an 8.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Labor Optimization And Demand Forecasting Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Driven Workforce Analytics and Automated Scheduling | +2.2% | Global, with concentrated initial gains in North America and Western Europe | Short term (≤ 2 years) |

| Rising Wage Inflation and Fair Workweek Compliance Pressure | +1.5% | North America and EU, spill-over to APAC | Short term (≤ 2 years) |

| Omnichannel and Shorter Fulfillment Windows Increasing Labor Volatility | +1.0% | Global, led by North America, Western Europe, and East Asia | Medium term (2-4 years) |

| Cloud Adoption by Multi-Site Midmarket Employers | +0.7% | Global, with accelerated adoption in APAC and MEA | Medium term (2-4 years) |

| Convergence of Store-Level Demand Forecasting, Labor Planning, and Fresh and Perishable Operations | +0.5% | North America, Europe, emerging APAC grocery | Medium term (2-4 years) |

| Schedule Fairness, Earned Wage Access, and Frontline Retention as a Shared Buying Criterion | +0.4% | North America, Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Driven Workforce Analytics and Automated Scheduling

The labor optimization and demand forecasting software market is gaining momentum as agentic AI shifts workforce management from post-facto reporting to in-the-moment action. Legion Technologies launched more than 90 AI features in January 2026 across forecasting, scheduling, time and attendance, and labor optimization, and said customers using its full engagement suite saw an average 33% improvement in retention.[1]Legion Technologies, “Legion Elevates Hourly Workforce Management With 90+ New Product Features That Maximize Employee Value,” Legion Technologies, legion.co The same release said Legion recorded 216% revenue growth in 2025, showing how strongly buyers are responding to platforms that can automate labor decisions rather than just visualize them. UKG also expanded the market’s AI layer in November 2025 with Workforce Intelligence Hub, built on a large operating data set that includes 10 billion punches and 12 billion schedules processed each year. That scale matters because better data improves forecast quality, overtime detection, and workforce well-being analysis in the same operating view. As the labor optimization and demand forecasting software market matures, vendors with deeper proprietary data pools are likely to hold a stronger accuracy advantage than newer challengers.

Rising Wage Inflation and Fair Workweek Compliance Pressure

The labor optimization and demand forecasting software market is also being supported by the rising cost of labor errors when scheduling rules tighten. GovDocs reported that 8 U.S. cities had enacted predictive scheduling ordinances in 2026, and Los Angeles County’s ordinance took effect on July 1, 2025, for retail employers nationwide with 300 or more employees. Chicago’s Fair Workweek Ordinance widened coverage in July 2025 by raising the wage threshold to USD 62,561.9 per year, expanding the pool of protected workers, and increasing compliance exposure for employers with many locations. When employers must give 14-day advance notice and pay penalties for late schedule changes, weak forecasting creates direct payroll leakage rather than merely operational inconvenience. This is why the labor optimization and demand forecasting software market is increasingly tied to demand sensing as much as to scheduling itself. Similar 14-day notice rules across Oregon, Chicago, Seattle, and Philadelphia also point to a more standardized compliance burden for national operators, which supports broader software adoption.

Omnichannel and Shorter Fulfillment Windows Increasing Labor Volatility

The labor optimization and demand forecasting software market is benefiting from the way omnichannel retail has changed, where and when labor is needed. ShipBob’s 2026 fulfillment report said 85.8% of surveyed brands now sell across 2 or more channels, up from 78% a year earlier, and 77.4% handle some level of brick-and-mortar store orders. DC Velocity reported that logistics and fulfillment costs for retailers rose by more than 20% between 2023 and 2026, reflecting the operational strain created by faster fulfillment promises and more complex order routing. This shift means labor forecasts now need to reconcile store traffic, warehouse order flow, and click-and-collect arrivals in near real time. Platforms that cannot translate those demand streams into short staffing intervals leave operators exposed to margin loss from overstaffing and service failures from understaffing. As a result, the labor optimization and demand forecasting software market is moving closer to fulfillment orchestration than to stand-alone workforce administration.

Cloud Adoption by Multi-Site Midmarket Employers

The labor optimization and demand forecasting software market is also widening because cloud delivery has lowered the entry barrier for employers that were once too small for traditional enterprise suites. ATOSS said it served around 21,100 customers in 50 countries, and its cloud and subscription revenue rose 28% in fiscal 2025 to EUR 92.7 million (USD 97.5 million). That pattern suggests that midmarket adoption is being driven by recurring services, phased deployment, and faster time-to-value rather than by one-time license decisions. HRTime reported that Germany’s mandatory electronic time-recording legislation is expected to take effect in 2026 for large companies and within 12 months thereafter for SMEs, which strengthens the case for digital, audit-ready systems. This compliance burden is especially important for employers with 200 to 2,000 workers that do not have the internal IT depth to maintain a custom workforce infrastructure. In that setting, the labor optimization and demand forecasting software market is being pulled by risk reduction and operational simplicity as much as by software modernization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy HRIS, Payroll, ERP, and POS Integration Complexity | -1.8% | Global, most acute in large enterprise and mid-market North America and Europe | Short term (≤ 2 years) |

| Data Privacy and Algorithmic Compliance Risk | -1.2% | EU and increasingly North America, emerging in APAC | Short term (≤ 2 years) |

| Sparse Intraday Demand Signals at Long-Tail Sites Reducing Forecast Quality | -0.5% | Global, concentrated in emerging markets and rural geographies | Medium term (2-4 years) |

| Works Council and Union Scrutiny of Black-Box Scheduling Decisions | -0.4% | Germany, France, Benelux, Nordics, spill-over to UK and Spain | Medium to long term (2-5 years) |

| Source: Mordor Intelligence | |||

Legacy HRIS, Payroll, ERP, and POS Integration Complexity

The labor optimization and demand forecasting software market still faces its largest deployment barrier when buyers try to connect new planning tools with old payroll, HRIS, ERP, and POS systems. Paycor said a June 2024 Gartner survey found fewer than 25% of HR functions were maximizing business value from their HR technology, and integration failures were a primary reason. Finch noted that the top 10 payroll providers account for only 62% of the U.S. market, leaving a long tail of smaller providers with different data structures that often require custom mapping work. TimeCheck Software said disconnected systems can force multi-location employers to spend 2 to 3 days consolidating payroll inputs through manual extraction and spreadsheet reconciliation. These delays matter because poor integration not only slows deployment but also weakens the quality of the demand data feeding the forecast engine. That makes the labor optimization and demand forecasting software market harder to scale in the mid-implementation phase, especially for employers with many legacy systems and inconsistent labor data.

Data Privacy and Algorithmic Compliance Risk

The labor optimization and demand forecasting software market also faces a rising compliance burden as regulators focus more closely on AI in workplace decisions. Bitkom’s 2025 guidance on the EU AI Act said that most AI-driven workforce scheduling and performance-monitoring tools fall into the high-risk category, triggering rules on risk management, technical documentation, human oversight, and bias controls. The same regulatory framework carries penalties of up to 7% of global annual turnover for prohibited practices, which raises the cost of weak vendor readiness. The European Parliamentary Research Service said workers’ exposure to algorithmic management tools is expected to rise from 42.3% to 55.5% in the medium term, while workplace regulation remains uneven across the region. This uncertainty slows procurement because buyers now need evidence that automation can be audited, explained, and challenged by people before contracts move forward. For the labor optimization and demand forecasting software market, that means product quality alone is no longer enough in Europe and is becoming less enough in North America as well.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Expand as Ongoing Support Becomes Essential

Software accounted for 62.44% of revenue in 2025, indicating that the software layer remained the largest share of the labor optimization and demand forecasting market in current deployments. The core software stack kept that position because it houses the scheduling engines, demand models, compliance rules, and analytics layers that create switching costs for enterprise customers. In the labor optimization and demand forecasting software market, these functions are the foundation of the products buyers rely on every day for labor planning, execution, and reporting. Software also benefited from the installed base of recurring subscriptions built over the past several years as vendors shifted customers toward cloud-linked commercial models. That installed base gives leading providers a reliable revenue stream and more room to attach adjacent capabilities over time.

Services is the faster-growing component, with the labor optimization and demand forecasting software market size for services projected to expand at a 9.12% CAGR through 2031. This growth reflects a clear shift in buyer behavior, as employers increasingly need implementation support, managed analytics, and change management to turn software output into measurable labor results. ATOSS reported that cloud and subscription revenue rose 27% year over year to EUR 27 million (USD 28.9 million) in Q1 2026, accounting for 53% of total quarterly sales. AI-led workforce tools also require retraining, integration upkeep, and compliance checks under frameworks such as ISO 27001, SOC 2, and the EU AI Act, which increases the service's load after deployment. That is why the labor optimization and demand forecasting software industry is not only selling licenses anymore, it is also selling ongoing operating support tied to labor performance and compliance readiness.

By Functionality: Demand Forecasting Remains the Base Layer While Analytics Gains Pace

Demand forecasting accounted for 35.45% of revenue in 2025, which made it the largest functional block in the labor optimization and demand forecasting software market. That position reflects its role as the base input for labor budgeting, scheduling, and reforecasting, because poor demand signals degrade the quality of every downstream planning action. In practical terms, employers need the system to merge transaction history, seasonality, local events, and real-time demand changes before any schedule can be optimized. This is why demand forecasting continues to anchor platform design, even as vendors add broader analytics and task-execution tools. The category remains especially important in multi-site environments where labor decisions must be updated quickly and consistently across many locations.

Workforce analytics and performance optimization is the fastest-growing functional segment, and the labor optimization and demand forecasting software market size for this area is projected to rise at an 8.36% CAGR through 2031. Growth is being supported by the fact that analytics modules are often sold into existing customers as upgrades, which gives vendors a faster path to incremental recurring revenue than a full new deployment. Logile’s 2025 labor planning study, cited by GFOS, found that 77% of retail employees said poor labor planning hurts revenue, and 80% reported additional stress or overload due to understaffing.[2]GFOS, “Workforce Scheduling for Retail, Built for Multi-Location Operations,” GFOS, gfos.com Blue Yonder also said its warehouse AI can improve labor forecasting from weeks ahead to minutes ahead of a shift by applying AI and machine learning to inbound throughput signals. As a result, the labor optimization and demand forecasting software market is placing greater emphasis on tools that quantify labor productivity in financial terms rather than solely measuring schedule adherence. In the labor optimization and demand forecasting software industry, this makes analytics a strong expansion path once the forecasting core is already in place.

By Deployment Model: On-Premise Holds the Installed Base While Cloud Leads Renewals

On-premises captured 67.34% of revenue in 2025, giving it the largest market share in the labor optimization and demand forecasting software market by deployment. That share reflected a large installed base of enterprise customers rather than a universal preference for on-premise architecture in new buying cycles. Healthcare systems, energy operators, and regulated manufacturers often remained in on-premises environments due to data residency concerns, sovereign data rules, and deep ties to legacy ERP systems. This kept legacy deployments relevant in sectors where workforce systems are embedded in critical operating workflows. It also shows that architecture choices in this market are still shaped by regulation and installed system complexity as much as by software performance.

Cloud-based deployment is the fastest-growing mode, and the labor optimization and demand forecasting software market size for cloud is projected to grow at a 9.91% CAGR through 2031. The strongest drivers are SMEs, multi-site midmarket employers, and enterprise customers who are moving modules one at a time rather than replacing the entire system in a single event. Yahoo Finance’s summary of ATOSS management commentary said the company planned to retain on-premises support for large enterprises while pushing SMB migration to the cloud by 2030, with AI services and subscription economics as incentives. Germany’s expected electronic time-recording rules are also pushing employers toward tamper-proof, audit-ready digital systems, which improves the case for modern cloud delivery. In the labor optimization and demand forecasting software market, cloud is becoming the growth engine, even as on-premises solutions remain important in the current revenue mix.

By Organization Size: Large Enterprises Drive Current Revenue While SMEs Scale Faster

Large enterprises accounted for 70.05% of revenue in 2025, making them the largest buyer group in the labor optimization and demand forecasting software market. This concentration reflects a simple operating reality because payroll exposure, compliance obligations, and integration complexity all grow quickly with workforce size. Large organizations also offer vendors better cross-sell economics, as a single platform can span multiple sites, job roles, and compliance jurisdictions simultaneously. These buyers often have the scale to justify specialized modules for forecasting, dynamic labor management, task execution, and workforce analytics. That makes enterprise accounts the revenue anchor even as the market broadens into smaller customer tiers.

SMEs are growing faster, with a projected 9.56% CAGR through 2031, as lower deployment barriers expand access to labor-optimization and demand-forecasting software. UKG serves more than 80,000 organizations globally and processes more than USD 1 trillion in payroll annually, which gives it a large base for AI upselling across different employer sizes. Legion and Netchex reported that embedded earned wage access tools reached 60-70% employee adoption, compared with 24-30% for stand-alone apps, while hourly worker replacement costs averaged USD 2,000 to USD 5,000 per employee. That matters for smaller employers because frontline retention pain can be proportionally higher when labor costs take up a larger share of the business. In the labor optimization and demand forecasting software market, SME demand is therefore becoming increasingly compelling because the value case rests on compliance, retention, and labor efficiency.

By End-Use Industry: Retail Leads Revenue While Healthcare Moves Ahead in Growth

Retail and e-commerce held 34.65% of revenue in 2025, which kept this vertical in the leading position across the labor optimization and demand forecasting software market. Retail’s lead is rooted in years of investment in labor standards, staffing models, and sales-to-labor planning disciplines, which made it the earliest and deepest commercial base for workforce technology vendors. Omnichannel activity has reinforced that lead because store labor, fulfillment labor, and pickup-related staffing now move together instead of separately. ShipBob said 85.8% of surveyed brands sell across 2 or more channels, which keeps intraday labor demand volatile and difficult to manage manually. This makes retail a strong fit for forecasting tools that can translate multiple demand signals into short staffing windows.

Healthcare and life sciences is the fastest-growing vertical, with a projected 7.89% CAGR through 2031 in the labor optimization and demand forecasting software market. The strongest demand driver is structural labor shortage, because the World Health Organization estimates a shortfall of 10 million healthcare workers by 2030. Under those conditions, hospitals and other care settings need better demand forecasting and dynamic scheduling to deploy certified staff efficiently and reduce reliance on expensive temporary labor. The sector also carries stricter operating requirements around staffing quality, patient coverage, and sensitive data handling, which raises the value of purpose-built workforce platforms. That is why the labor optimization and demand forecasting software market is finding more room in healthcare even though retail remains the largest revenue contributor today.

Geography Analysis

North America accounted for 36.81% of revenue in 2025, giving the region the largest share in the labor optimization and demand forecasting software market by geography. The region’s lead rests on a dense compliance framework, a large base of enterprise buyers, and a strong concentration of workforce management vendors with mature AI road maps. In the United States, predictive scheduling laws across major cities and counties have made manual compliance more difficult for retailers and other multi-site employers. That pressure raises the value of systems that combine demand sensing, scheduling, and audit-ready recordkeeping in a single workflow. In the labor optimization and demand forecasting software market, North America remains the commercial hub because regulatory complexity and enterprise scale reinforce one another.

Europe held the second-largest regional position in the labor optimization and demand forecasting software market, supported by Germany, the United Kingdom, and France. Demand in the region is shaped less by fair workweek laws alone and more by co-determination rules, mandatory time recording, and the EU AI Act’s treatment of employment AI as a high-risk use case. Germany’s expected shift toward mandatory electronic time recording from 2026 adds a direct compliance trigger for digital workforce systems. The European Parliament’s late 2025 call for tighter oversight of algorithmic management also adds short-term friction to buying while encouraging a longer-term move toward explainable, auditable software.

Asia-Pacific is the fastest-growing region, and the labor optimization and demand forecasting software market is projected to expand at an 8.77% CAGR through 2031. Growth is being led by China, India, Australia, South Korea, and Japan, as retailers, restaurant chains, and manufacturers digitize labor operations at scale for the first time. GaiaWorks said its deployments across APAC retail and food-and-beverage clients achieved 99% accuracy in labor cost allocations, supporting the region’s shift away from manual scheduling.[3]GaiaWorks, “WFM for Retail, FandB and Convenience Stores,” GaiaCloud, gaiacloud.com Middle East adoption is rising with workforce modernization programs and the expansion of organized retail, logistics, and hospitality, while Africa and South America remain earlier-stage opportunities tied to formalization in labor-intensive sectors.

Competitive Landscape

The labor optimization and demand forecasting software market has a split structure, with a more concentrated enterprise tier and a much more fragmented layer of SME-focused and vertical-specific suppliers. UKG, Blue Yonder, ATOSS, and WorkForce Software remain prominent at the top end because they can support large deployments, broad compliance needs, and deeper product portfolios. At the same time, newer AI-first vendors are gaining attention by moving faster in automation, user experience, and vertical tailoring. This mix keeps pricing pressure active in some customer groups while pushing feature competition higher in enterprise deals. The labor optimization and demand forecasting software market, therefore, remains open enough for challengers to grow, even though the leading vendors still hold clear scale advantages.

Strategic activity in 2025 and 2026 shows that vendors are trying to deepen AI capabilities and strengthen industry coverage simultaneously. UKG completed its acquisition of Shiftboard in May 2025 to expand its scheduling depth in energy and manufacturing, and later launched Dynamic Labor Management and Workforce Intelligence Hub in November 2025 to strengthen real-time labor decision support.[4]UKG Inc., “UKG Acquires Shiftboard, a Leading Energy and Manufacturing Employee Scheduling Solutions Provider,” UKG, ukg.com Legion also expanded its position in January 2026 with 90-plus AI innovations and a live footprint across 35 countries, which shows that specialist vendors can still win share with a focused product story. Blue Yonder further expanded the competitive field by bringing agentic AI into warehouse, transportation, manufacturing, and retail workflows in March 2026, linking labor orchestration more closely to broader supply chain execution.

Healthcare is becoming one of the clearest targets for consolidation and specialization in the labor optimization and demand forecasting software market. Symplr acquired Smart Square from AMN Healthcare in July 2025, and Viventium acquired Apploi in February 2026 to build a scaled healthcare-focused human capital management platform. Quickbase’s April 2026 acquisition of Solvice also shows that broader operations software providers are beginning to embed automated scheduling as a product capability rather than treating it as a separate category. Compliance readiness under the EU AI Act is also becoming a competitive filter, as buyers increasingly demand explainable AI, human oversight, and audit trails before signing workforce software contracts.

Labor Optimization And Demand Forecasting Software Industry Leaders

WorkForce Software, LLC

Deputechnologies Pty Ltd

Legion Technologies, Inc.

ATOSS Software SE

Quinyx AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Logile, Inc. won the Gold Stevie Award for Best Use of AI in Business Transformation and the Silver Stevie Award for Best AI-Powered Product or Service, following a Nucleus Research case study confirming that Vallarta Supermarkets achieved a 1,070% ROI and USD 10 million in attributable profit over 3 years using Logile's Fresh Inventory Management. The company also reported over 45% annual recurring revenue growth.

- April 2026: ATOSS Software SE signed a new contract with Charité - Universitätsmedizin Berlin to deploy its workforce management platform for service scheduling and time recording across clinical operations, replacing legacy systems and enabling data-driven demand planning for care personnel.

- March 2026: Logile launched its Fresh Operations Management Suite, a unified platform for grocery retailers synchronizing customer demand, labor capacity, and cost visibility for fresh departments, addressing the convergence of perishable inventory management and labor planning in a single workflow.

- March 2026: Blue Yonder expanded its agentic AI and mobile capabilities across manufacturing planning, transportation management, warehouse management, and retail, including a new Warehouse Management AI for live operational briefs and a Fulfillment and Sourcing Agent in beta.

Global Labor Optimization And Demand Forecasting Software Market Report Scope

The labor optimization and demand forecasting software predicts workforce needs and fine-tunes staffing levels. By analyzing operational inputs like sales and customer traffic, these AI-driven platforms ensure labor aligns with real-time business demands. Industries such as retail, healthcare, and logistics, which often face fluctuating operational needs, widely adopt these solutions. The primary goals are to boost workforce efficiency, cut labor costs, and elevate service delivery.

The Labor Optimization and Demand Forecasting Software Market Report is Segmented by Component (Software, and Services [Implementation and Integration Services, Consulting Services, Support and Maintenance Services, and Training and Managed Services]), Functionality (Demand Forecasting, Labor Budgeting and Optimization, Workforce Scheduling, Intraday Management and Reforecasting, Task and Execution Planning, and Workforce Analytics and Performance Optimization), Deployment Model (Cloud-Based, and On-Premise), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-Use Industry (Retail and E-commerce, Foodservice and Hospitality, Manufacturing, Transportation and Logistics, Healthcare and Life Sciences, Consumer Services and Leisure, and Other End-Use Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | |

| Services | Implementation and Integration Services |

| Consulting Services | |

| Support and Maintenance Services | |

| Training and Managed Services |

| Demand Forecasting |

| Labor Budgeting and Optimization |

| Workforce Scheduling |

| Intraday Management and Reforecasting |

| Task and Execution Planning |

| Workforce Analytics and Performance Optimization |

| Cloud-Based |

| On-Premise |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Retail and E-commerce |

| Foodservice and Hospitality |

| Manufacturing |

| Transportation and Logistics |

| Healthcare and Life Sciences |

| Consumer Services and Leisure |

| Other End-Use Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | |

| Services | Implementation and Integration Services | |

| Consulting Services | ||

| Support and Maintenance Services | ||

| Training and Managed Services | ||

| By Functionality | Demand Forecasting | |

| Labor Budgeting and Optimization | ||

| Workforce Scheduling | ||

| Intraday Management and Reforecasting | ||

| Task and Execution Planning | ||

| Workforce Analytics and Performance Optimization | ||

| By Deployment Model | Cloud-Based | |

| On-Premise | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End-Use Industry | Retail and E-commerce | |

| Foodservice and Hospitality | ||

| Manufacturing | ||

| Transportation and Logistics | ||

| Healthcare and Life Sciences | ||

| Consumer Services and Leisure | ||

| Other End-Use Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 size of the labor optimization and demand forecasting software market?

The labor optimization and demand forecasting software market stands at USD 1.63 billion in 2026 and is projected to reach USD 2.23 billion by 2031 at a 6.48% CAGR.

What is driving growth in labor optimization and demand forecasting software?

Growth is being supported by AI-led workforce analytics, fair workweek compliance pressure, omnichannel labor volatility, and wider cloud adoption among multi-site employers.

Which region leads labor optimization and demand forecasting software adoption?

North America led with 36.81% of 2025 revenue, helped by strong enterprise demand and a dense predictive scheduling compliance environment.

Which region is growing fastest in labor optimization and demand forecasting software?

Asia-Pacific is the fastest-growing region, with an 8.77% CAGR through 2031, as retail, foodservice, and manufacturing employers digitize labor operations at scale.

Which deployment model is expanding fastest?

Cloud-based deployment is growing fastest at a 9.91% CAGR through 2031, even though on-premise still held the largest share in 2025 because of legacy enterprise installations.

Which end-use industry offers the strongest growth opportunity?

Healthcare and life sciences is the fastest-growing end-use vertical at a 7.89% CAGR through 2031, supported by global staffing shortages and stricter workforce planning needs.

Page last updated on: