Application Carbon Footprint Monitoring Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.6 Billion |

| Market Size (2031) | USD 2.12 Billion |

| Growth Rate (2026 - 2031) | 28.72% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Application Carbon Footprint Monitoring Software Market Analysis by Mordor Intelligence

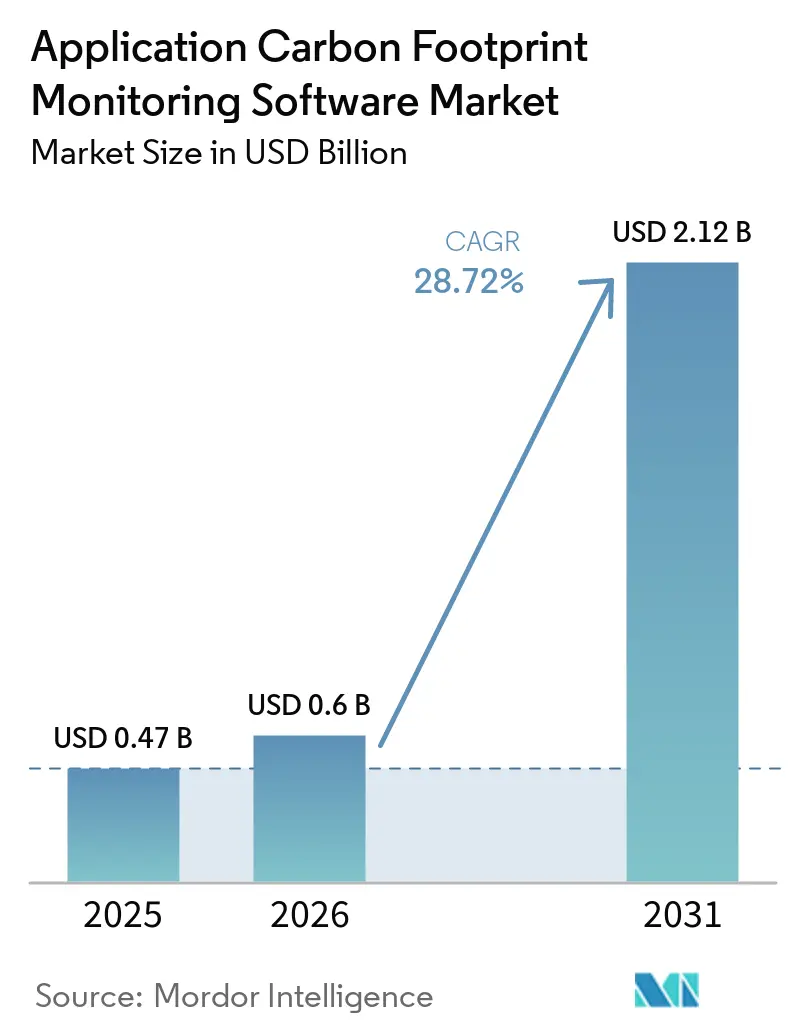

The application carbon footprint monitoring software market size is expected to grow from USD 0.47 billion in 2025 to USD 0.60 billion in 2026 and is forecast to reach USD 2.12 billion by 2031 at 28.72% CAGR over 2026-2031. The application carbon footprint monitoring software market is expanding as carbon accounting moves beyond a narrow reporting function into a core disclosure process that now requires stronger audit trails, better data lineage, and tighter internal controls across large organizations. Near-term buying activity is being pushed by mandatory reporting timelines, especially where companies must prepare 2026 emissions data for filing in 2027, which is shortening procurement cycles and forcing earlier platform selection. The convergence of Scope 3 data requirements, multi-country disclosure rules, and AI-enabled data harmonization is also reducing tolerance for manual spreadsheets and fragmented advisory-led workflows. Competition is becoming more intense as vendors try to position carbon accounting within broader ESG and finance software stacks, while buyers increasingly prefer platforms that can support supplier-specific data and enterprise-wide reporting from the same system. Integration cost, factor-library inconsistency, and reporting-method differences still slow some deployments, but the long-term direction of the application carbon footprint monitoring software market remains tied to mandatory disclosure rules that are becoming harder for large companies to avoid.

Key Report Takeaways

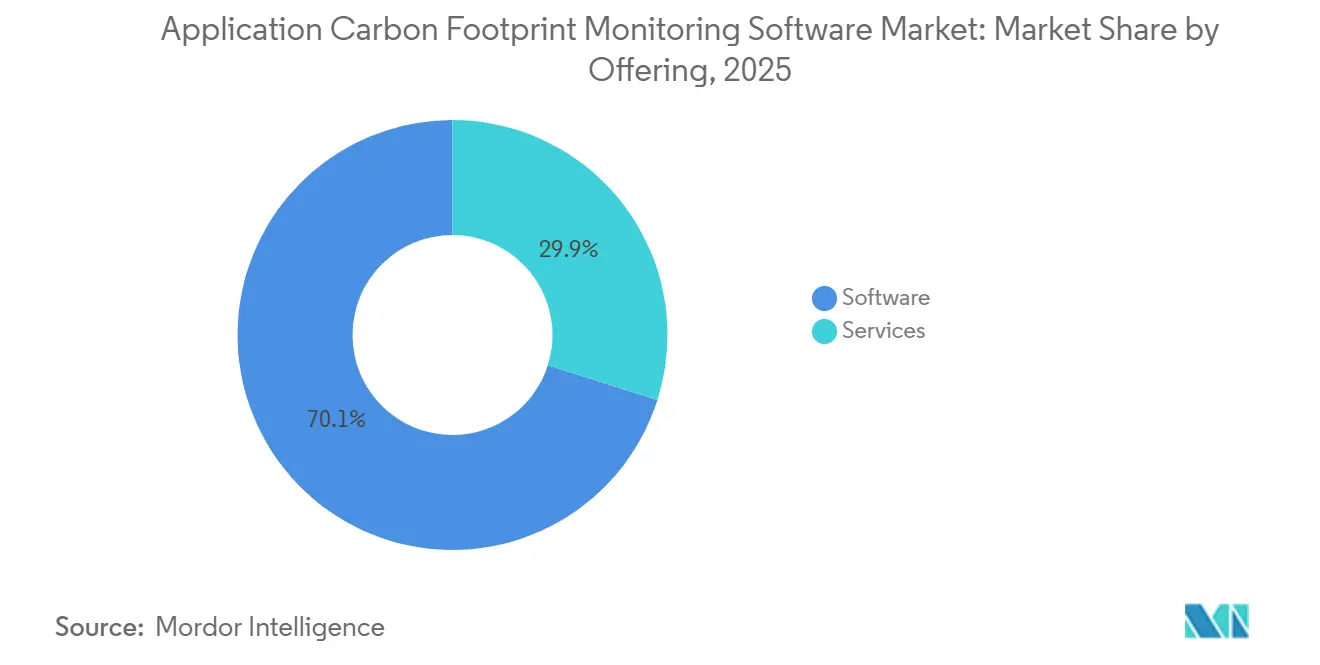

- By offering, software held 70.12% of the application carbon footprint monitoring software market in 2025, while services are projected to expand at a 29.34% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 67.41% of the market in 2025, while hybrid deployment is projected to grow at a 29.12% CAGR through 2031.

- By enterprise size, large enterprises held 65.23% share in 2025, while small and medium enterprises are expected to expand at a 29.87% CAGR through 2031.

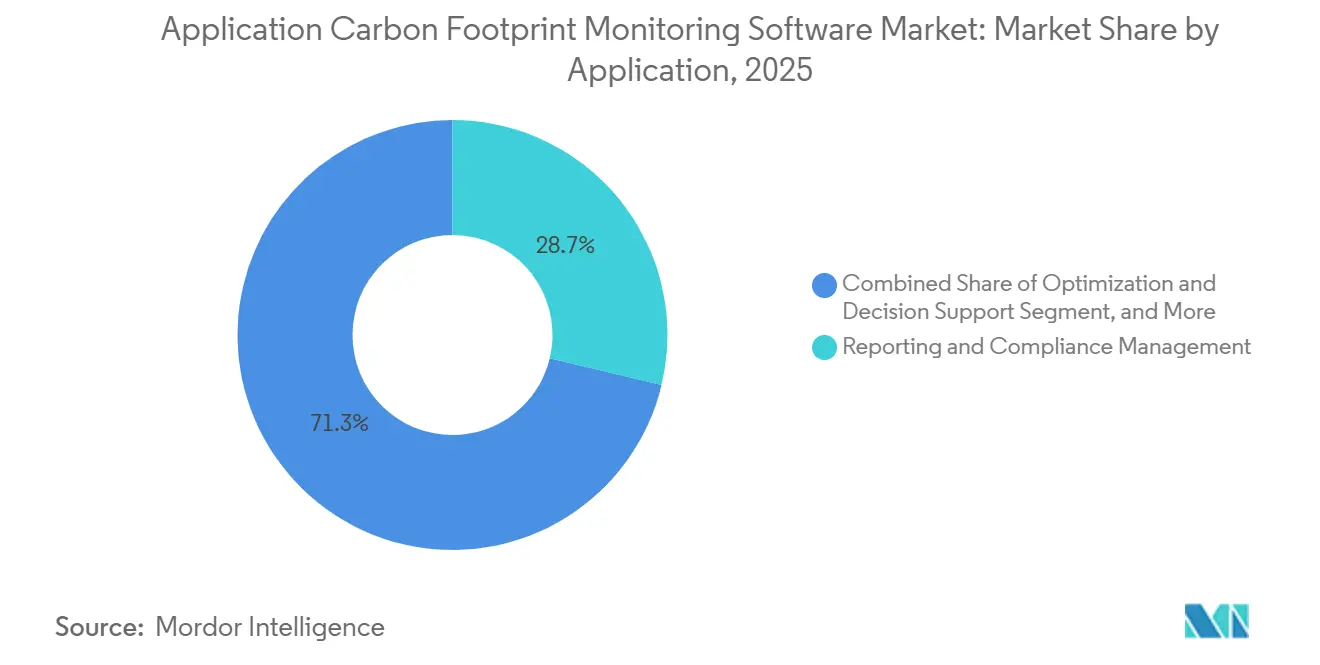

- By application, reporting and compliance management accounted for 28.74% of the market share in 2025, while optimization and decision support are projected to advance at a 30.15% CAGR through 2031.

- By end-use industry, IT and telecom held 26.45% share in 2025, while retail and e-commerce are projected to expand at a 29.05% CAGR through 2031.

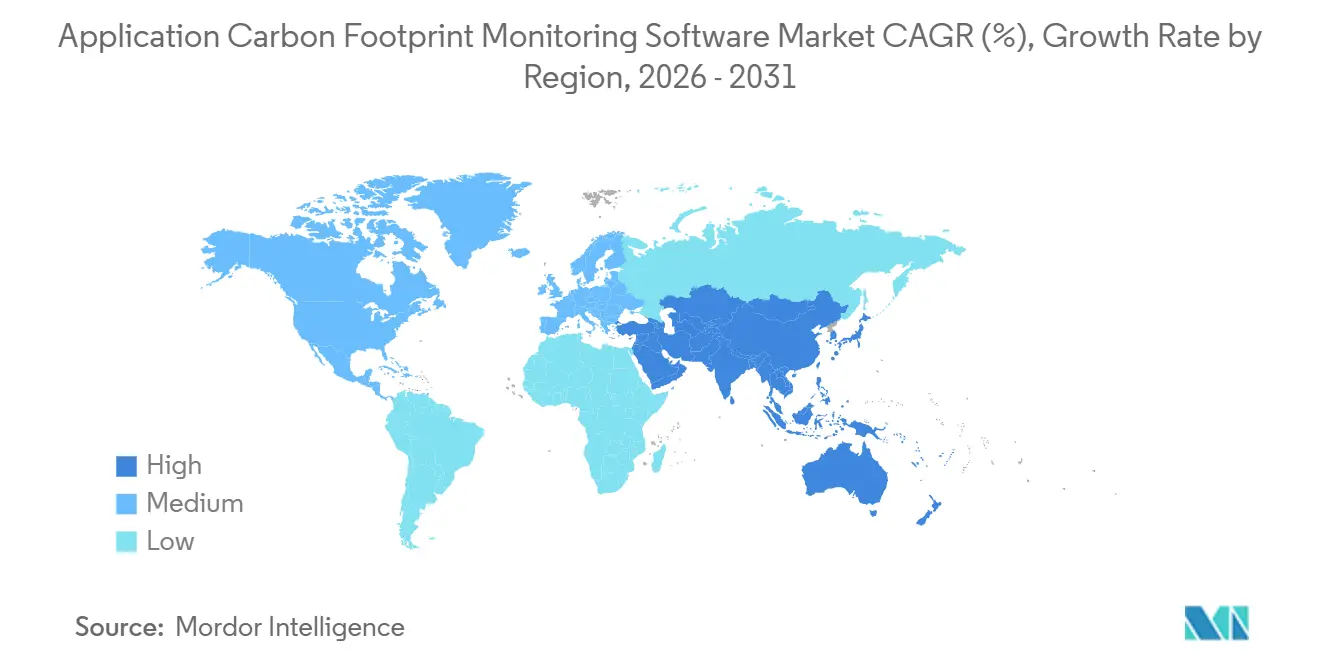

- By geography, Europe held 34.63% share of the application carbon footprint monitoring software market size in 2025, while Asia-Pacific is projected to record the fastest regional CAGR of 30.12% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Application Carbon Footprint Monitoring Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Carbon Disclosure Regulations and Compliance Mandates | +8.5% | Global, near-term gains concentrated in EU and California | Short term (≤ 2 years) |

| Corporate Net-Zero Commitments and ESG Procurement Pressure | +6.8% | Global | Medium term (2-4 years) |

| AI-Powered Scope 3 Data Harmonization Across Complex Supply Chains | +5.2% | Global, with APAC and EU as core markets | Medium term (2-4 years) |

| Digital Product Passport Readiness and Product-Level Emissions Traceability | +3.1% | EU, with spill-over to export-focused APAC and North America | Medium term (2-4 years) |

| Embedded Carbon Accounting in Enterprise Finance and ERP Workflows | +2.0% | Global, led by SAP and Oracle ERP ecosystems | Long term (≥ 4 years) |

| Carbon-Linked Supplier Selection and Customer Audit Requirements | +1.4% | Global, with early traction in EU and US Tier-1 procurement | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Carbon Disclosure Regulations and Compliance Mandates Drive Platform Procurement

Hardening disclosure timelines remains the clearest near-term growth driver for the application carbon footprint monitoring software market. The European Commission states that companies under the Corporate Sustainability Reporting Directive must report against the European Sustainability Reporting Standards, which provide a formal compliance framework for climate data collection and reporting across a large corporate base.[1]European Commission, “Corporate Sustainability Reporting,” Finance, finance.ec.europa.eu In practice, that means many Wave 1 organizations are now building systems to capture 2026 emissions data in a way that supports filing in 2027, and that timing is pushing software purchases forward rather than allowing long phased rollouts. The proposed rescission of the U.S. climate-related disclosure rules does not remove pressure on multinational companies that still need globally compatible reporting processes, especially when their European operations or revenue exposure keep them subject to cross-border requirements. This is why the application carbon footprint monitoring software market is seeing demand shift toward platforms that can produce audit-ready inventories, preserve method consistency, and shorten the time between data collection and final assurance. Companies that delay system upgrades risk entering the first mandatory cycles with incomplete data models, weaker controls, and less time to correct supplier-level gaps.

Corporate Net-Zero Commitments and ESG Procurement Pressure Sustain Structural Demand

Corporate climate commitments keep the application carbon footprint monitoring software market active even before every reporting rule reaches full enforcement. Large buyers are pushing carbon data requests into procurement workflows, which means suppliers are being asked for more primary emissions information at the point of sourcing rather than after annual reporting closes. EcoVadis said in May 2026 that its integration with Workiva Carbon was designed to help shared customers move from industry-average estimates to more granular supplier carbon data, which shows how buyer requirements are shaping software architecture.[2]EcoVadis, “EcoVadis Continues Expansion of Carbon Data Network With Workiva,” EcoVadis, resources.ecovadis.com That pattern matters because supplier pressure reaches many firms that are not yet directly regulated but still need to remain qualified with major customers in retail, manufacturing, and global service chains. The application carbon footprint monitoring software market, therefore, benefits from a pull-through effect that is commercial as much as regulatory, and that tends to start earlier than a legal filing deadline. Vendors that can automate supplier questionnaires, data validation, and evidence trails inside procurement-linked workflows are better placed to capture this part of the demand.

AI-Powered Scope 3 Data Harmonization across Complex Supply Chains Resets Accuracy Expectations

AI-enabled data handling is becoming one of the clearest differentiators in the application carbon footprint monitoring software market. SINAI Technologies said in its Q1 2026 product updates that it enhanced AI Emissions Match for automated multi-scope data ingestion, reflecting how vendors are using automation to normalize fragmented operational and supplier inputs at scale.[3]SINAI Technologies, “SINAI Carbon Management Platform Updates, Q1 2026,” SINAI Technologies, sinai.com EcoVadis also expanded its Carbon Data Network in 2026 by adding Carbmee and its SKU-level emissions capabilities, signaling a broader market shift toward more machine-readable, supplier-connected carbon data flows. As a result, buyers now expect carbon platforms to do more than store data; they expect them to reconcile formats, match factors, flag gaps, and produce outputs that can be reviewed by finance and assurance teams. This higher expectation is pushing the application carbon footprint monitoring software market toward tools that show how calculations are built, rather than relying on opaque processing logic. Over time, vendors that combine AI assistance with visible method controls are likely to gain an advantage as enterprise buyers become less tolerant of black-box estimates.

Digital Product Passport Readiness and Product-Level Emissions Traceability Expand Software Scope

Product-level traceability is widening the role of the application carbon footprint monitoring software market beyond corporate totals and annual disclosure packs. Vendor roadmaps increasingly show that customers want a single data foundation that can support both enterprise inventories and product-level carbon outputs across large catalogs and supplier networks. EcoVadis said in April 2026 that CarbonMee joined its Carbon Data Network, bringing SKU-level emissions data capabilities, demonstrating how product-level visibility is moving closer to mainstream enterprise workflows. Persefoni said in March 2025 that its new funding would support the launch of dedicated Product Carbon Footprint and life-cycle assessment capabilities, indicating that vendors see product-level accounting as a durable growth area rather than a side feature. This matters because the application carbon footprint monitoring software market is no longer shaped solely by corporate disclosure teams; it is also shaped by product, sourcing, and operations teams that need item-level carbon information. As those use cases spread, integrated platforms that connect corporate reporting with product-level calculations are likely to hold a stronger cost and workflow advantage over disconnected point tools.

Restraints Impact Analysis*

| estraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Cost Across ERP, Procurement, and Supplier Data Ecosystems | -3.5% | Global, most acute in large enterprise multi-ERP estates | Medium term (2-4 years) |

| Inconsistent Emissions Factors and Methodology Reconciliation Issues | -2.4% | Global | Long term (≥ 4 years) |

| Vendor Lock-In Risk from Proprietary Reporting Logic and Data Models | -1.8% | Global | Medium term (2-4 years) |

| Cybersecurity and Audit-Trail Integrity Concerns for Sensitive Sustainability Data | -1.1% | Global, heightened in regulated industries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Integration Cost Across ERP, Procurement, and Supplier Data Ecosystems Constrains Deployment

Integration cost remains one of the clearest brakes on faster adoption in the application carbon footprint monitoring software market. SAP said in its Q4 2025 Sustainability Footprint Management updates that it introduced a BTP booster to reduce tenant setup complexity, which is a practical sign that deployment burdens in multi-system environments are real, even for large software-led programs.[4]SAP, “SAP Sustainability Footprint Management, Q4-25 Updates and Highlights,” SAP Community, community.sap.com Many enterprises still operate a mix of SAP, Oracle, cloud applications, and legacy on-premises tools, which creates repeated mapping work across procurement, logistics, energy, and financial records before carbon outputs can be trusted. Mid-sized firms often feel this problem more sharply because they lack the internal IT and sustainability systems staff needed to manage a long configuration cycle without outside support. The application carbon footprint monitoring software market, therefore, faces a two-speed deployment pattern, where larger buyers move forward despite the cost, while smaller buyers delay adoption or continue using weaker proxy methods. Vendors with strong prebuilt connectors, cleaner onboarding workflows, and lower dependence on custom integration work are likely to reduce friction in the next stage of market expansion.

Inconsistent Emissions Factors And Methodology Reconciliation Issues Undermine Reporting Credibility

Methodological inconsistencies still pose a significant restraint on the application of carbon footprint monitoring software in the market. The GHG Protocol stated in its March 2026 Phase 1 Progress Update that its Scope 3 Standard revision work is addressing topics such as boundary setting, data quality hierarchies, facilitated value chain activities, and financed emissions, confirming that key calculation issues remain under active review. When standards and factor approaches continue to evolve, companies face the risk that current inventories will need to be restated, re-explained, or rebuilt in later reporting periods. This affects buyer confidence because finance teams and auditors want year-to-year comparability, while sustainability teams want enough flexibility to incorporate better data over time. The application carbon footprint monitoring software market is therefore placing greater emphasis on transparent factor selection, clear assumptions, and version control across methodologies. Vendors that cannot make changes traceable are more exposed when customers need to defend why two reporting cycles were calculated differently.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Platforms Lead While Services Expand Around Complexity

Software held 70.12% of the application carbon footprint monitoring software market share in 2025, showing that buyers preferred scalable SaaS platforms over manual approaches and one-off advisory-led workflows. That leadership reflects the need to manage multi-entity disclosures, track evolving requirements, and support internal controls across several reporting frameworks from a single operating layer. Workiva said in June 2024 that it launched Workiva Carbon after acquiring Sustain. Life, which shows how established reporting software vendors are extending their core platforms into carbon accounting rather than treating it as a separate niche. The application carbon footprint monitoring software market has therefore seen software gain traction not only as a tool for sustainability teams, but also as a layer that finance and governance functions can use with less process fragmentation. Services are projected to grow at a 29.34% CAGR through 2031 because many organizations still need help with setup, method selection, supplier outreach, and assurance preparation during first-time disclosure cycles.

The services opportunity does not weaken the software case; it strengthens it by building recurring implementation and advisory work around the platform layer. In the application carbon footprint monitoring software industry, this is creating a bundled model where clients buy software for continuity and services for execution support during the first several reporting cycles. That model is especially attractive for companies that lack internal life cycle assessment capability or do not yet have stable carbon data governance in place. It also raises switching costs, because once inventories, factor choices, and evidence libraries are embedded in a vendor-led workflow, the effort required to rebuild them elsewhere becomes material. The application carbon footprint monitoring software market is therefore moving toward a structure in which software anchors long-term retention, and services deepen account value during onboarding, expansion, and methodology refresh work.

By Deployment Mode: Cloud Leads On Speed While Hybrid Gains On Control

Cloud-based deployment commanded 67.41% share in 2025, reflecting buyer preference for centralized SaaS environments that can process supplier data at scale and roll out framework updates without heavy local IT effort. This model fits the application carbon footprint monitoring software market because reporting rules and factor libraries change quickly, and cloud delivery lets vendors update templates and logic more efficiently. On-premises systems still matter in sectors where data sovereignty, internal hosting, or strict audit controls take priority over deployment speed. Hybrid deployment, however, is emerging as the fastest-growing option, and the application carbon footprint monitoring software market size for hybrid deployment is projected to expand at 29.12% CAGR through 2031. That growth shows that many multinational buyers want cloud-scale analytics while still retaining tighter control over sensitive supplier, financial, or operational records in selected jurisdictions.

Cybersecurity and governance concerns are reinforcing that shift rather than replacing it. Sustainability data can reveal supplier structures, sourcing patterns, production intensity, and cost-linked operating details, leading security teams to increasingly view it as commercially sensitive rather than administrative. The application carbon footprint monitoring software market is also being shaped by buyers who do not want carbon systems to sit too far away from ERP and finance data environments. SAP announced in December 2024 that SAP Green Ledger became generally available, reflecting a broader movement toward finance-linked carbon data structures that often require tighter alignment with enterprise architecture. As a result, hybrid deployment is gaining popularity because it supports both scalability and control, while the cloud segment remains dominant because it remains the easiest model for faster rollouts and continuous regulatory updates. The application carbon footprint monitoring software market is likely to keep both models active, with buyer choice increasingly determined by governance requirements rather than pure infrastructure preference.

By Enterprise Size: Large Enterprises Dominate While SMEs Catch Up Fast

Large enterprises held a 65.23% share in 2025, reflecting how reporting pressure first concentrated among organizations with broader legal exposure, more complex supply chains, and more formal net-zero governance. These buyers usually manage multiple legal entities, geographic units, and supplier tiers, so the cost of weak carbon data is higher for them than it is for smaller firms. The application carbon footprint monitoring software market has also benefited from the fact that board-level oversight and investor scrutiny were already stronger in this group before the newest rules came into force. Small and medium enterprises are projected to grow at a 29.87% CAGR through 2031, showing that adoption is now moving beyond the first wave of very large organizations. Persefoni said in March 2025 that its Pro offering had reached more than 6,000 sign-ups and had expanded to include free multi-framework sustainability reporting, indicating active efforts to lower the entry barrier for smaller users.

The next growth phase will depend on whether smaller companies can adopt without carrying the enterprise-grade implementation cost. In the application carbon footprint monitoring software industry, vendors are responding with self-service workflows, automated categorization, and simpler supplier-request tools that reduce the need for consulting-intensive rollouts. Tanso said in 2025 that its TÜV-certified platform can reduce compliance time by up to 80%, demonstrating how SME-focused providers are competing on usability and deployment speed rather than breadth alone. The application carbon footprint monitoring software market is likely to see strong demand from SMEs, as large customers increasingly require verified product or supplier emissions data, even if the smaller supplier is not yet directly regulated. That pull-through effect matters because it turns carbon software from a voluntary purchase into a business continuity requirement for many smaller firms. Over time, the gap between large and small enterprise adoption should narrow if low-touch onboarding and AI-supported data preparation continue to improve.

By Application: Reporting Leads Today While Decision Support Gains Strategic Weight

Reporting and compliance management captured 28.74% of the market share in 2025, making it the largest application area because it offers the most immediate response to mandatory disclosure pressure. For many buyers, the first step has been to centralize emissions data, map it to accepted frameworks, and generate outputs that can move through assurance and board review with less manual effort. The application carbon footprint monitoring software market, therefore, still leans toward compliance-led deployments, especially among organizations that are entering their first formal reporting cycles. Carbon measurement and attribution, runtime carbon monitoring, and sustainability analytics are also gaining relevance as buyers increasingly seek more detailed operational visibility rather than year-end totals alone. Optimization and decision support is projected to grow at a 30.15% CAGR through 2031, and the application carbon footprint monitoring software market size for this segment is projected to expand faster than any other application as companies connect carbon-reduction choices with capital planning.

That shift becomes clearer when decarbonization planning moves from sustainability teams into finance and operations committees. SINAI Technologies said in 2025 that it launched an AI-powered transition planning tool built around a Corporate Marginal Abatement Cost Curve, which shows how software vendors are translating emissions data into project prioritization and investment decisions. Once companies can model abatement pathways within planning workflows, the application of carbon footprint monitoring software begins to serve not only disclosure needs but also budgeting and portfolio management. This is especially relevant for large industrial users that need to compare several emissions-reduction projects across long capital cycles. The application carbon footprint monitoring software market is therefore moving from measurement and reporting toward action planning, while compliance remains the entry point for most new customers. That progression is important because it raises retention potential, as platforms become harder to remove once they support both reporting and investment decisions.

By End-Use Industry: IT And Telecom Leads While Retail And E-Commerce Accelerates

IT and telecom accounted for 26.45% in 2025, reflecting the sector’s early readiness for data-intensive reporting and its direct exposure to digital emissions measurement. Companies in this group often have stronger digital operating models, which makes it easier to instrument workloads, organize data streams, and integrate carbon reporting into existing systems. The application carbon footprint monitoring software market has therefore found an early base in IT and telecom, where internal capability and reporting urgency are often better aligned than in slower-moving sectors. BFSI remained a major user group because financing, portfolio disclosure, and governance demands require a stronger data structure, even when direct operational emissions are limited. Retail and e-commerce are projected to grow at a 29.05% CAGR through 2031, indicating how quickly supply-chain reporting pressure is driving adoption into customer-facing sectors with large supplier networks and heavy purchased goods exposure.

That demand has practical consequences for platform design. Retailers need systems that can handle large volumes of supplier outreach, product-level inputs, and evidence management without turning annual reporting into a manual exercise. The application carbon footprint monitoring software industry is also seeing stronger demand from manufacturing, energy and utilities, oil and gas, transportation and logistics, construction, and government users that need better visibility at the activity and supplier levels. These sectors often begin with compliance reporting, but many move quickly into product footprinting, scenario modeling, and procurement-linked measurement once the base inventory is established. The application carbon footprint monitoring software market is therefore broadening across verticals, even though adoption patterns still vary by reporting maturity, digital capability, and supply-chain complexity. Over the forecast period, retail and e-commerce should remain among the clearest growth stories, as supplier-level data collection is becoming increasingly difficult to avoid in consumer goods value chains.

Geography Analysis

Europe accounted for 34.63% of the application carbon footprint monitoring software market share in 2025, making it the largest regional market. The region benefits from the highest concentration of companies working through mandatory sustainability reporting frameworks, which creates a more immediate software buying cycle than in most other regions. The application carbon footprint monitoring software market in Europe also benefits from stronger corporate reporting infrastructure, deeper ESG program maturity, and earlier alignment between sustainability, finance, and compliance teams. This regional lead is reinforced by the fact that climate disclosure is now more closely tied to enterprise reporting obligations than to voluntary reputation programs alone. North America remained the second-largest region, and many U.S.-based multinationals still need globally compatible tools even after the proposed rescission of domestic climate disclosure rules, because cross-border obligations do not disappear with a local rule change.\

Asia-Pacific is projected to record the fastest regional CAGR of 30.12% through 2031, making it the fastest-growing geography in the application carbon footprint monitoring software market. Growth is being supported by a mix of export-driven pressure, formalized domestic disclosure, and rising enterprise attention to product-level and supply-chain carbon data. Japan, South Korea, India, and China are all contributing to this momentum, although the demand patterns differ by regulatory maturity and industry mix. The strongest traction is likely to come from large enterprises and export-focused manufacturers that need enterprise-grade systems to support both domestic reporting and cross-border customer requirements.

South America, the Middle East, and Africa still represent smaller revenue pools, but they are becoming more relevant as carbon disclosure expectations spread through global value chains. In the Middle East, SINAI Technologies said in Q1 2026 that it deployed what it described as the region’s first AI-enabled enterprise decarbonization platform in Saudi Arabia, signaling growing demand for formal carbon management tools. South America is gaining attention as large corporates in energy, mining, and agribusiness strengthen disclosure readiness and supplier engagement ahead of tighter investor and trade expectations. Africa remains at an earlier stage, but listed-company reporting needs and capital-access requirements are pushing more organizations toward recurring software subscriptions rather than pilot-only deployments.

Competitive Landscape

The application carbon footprint monitoring software market remains highly fragmented, with more than 30 active vendors competing across enterprise, mid-market, and vertical-focused positions. This fragmentation reflects the wide range of buyer needs, from basic compliance reporting to supplier data exchange, product footprinting, runtime monitoring, and capital-planning support. The competitive field broadly splits between integrated platform vendors such as Workiva and Sphera, and focused specialists such as Carbmee, Persefoni, Normative, and SINAI Technologies, which compete on depth in specific workflows. Sphera said in 2026 that it was named a leader in the Green Quadrant for Enterprise Carbon Management Software, highlighting how scientific depth, lifecycle assessment content, and enterprise execution remain important differentiators in large-account competition. The application carbon footprint monitoring software market is therefore not consolidating around one product model, but around a narrower set of capabilities that buyers now view as essential, especially Scope 3 depth, traceable methods, and stronger ERP connectivity.

Partnership-led ecosystem building is becoming one of the clearest ways to gain ground in the application carbon footprint monitoring software market. EcoVadis said in May 2026 that its partnership with Workiva connected supplier carbon data from the Carbon Data Network with Workiva Carbon, which gives both companies a stronger position in audit-ready Scope 3 workflows. EcoVadis also said in April 2026 that it added Carbmee to the same network, showing how vendors are using connected data ecosystems to strengthen product-level and supplier-specific carbon exchange. SAP’s continued rollout of finance-linked sustainability tools is also important because installed-base ERP vendors can make basic carbon accounting easier to access, which pushes specialist vendors to compete higher up the value chain on Scope 3 complexity, product data, and decision support.

Recent strategic moves also show that consolidation is coming through platform extension as much as through direct acquisition. Workiva used an acquisition to move carbon accounting closer to enterprise reporting workflows, while Diligent chose a partnership and client transition with Persefoni to maintain continuity in carbon accounting without building the capability internally. The application carbon footprint monitoring software market still has room for specialists, especially in SME tooling, asset-intensive sectors, and runtime application emissions tracking. Even so, the strongest vendors are increasingly those that can combine multi-framework coverage, audit-grade data lineage, supplier network access, and finance system alignment within a single operating environment. As the application carbon footprint monitoring software market matures, buyers are likely to reduce the number of tools they use and favor vendors that can support reporting, analysis, and action planning without forcing repeated data rebuilds.

Application Carbon Footprint Monitoring Software Industry Leaders

Persefoni AI, Inc.

Watershed Technology, Inc.

SAP SE

Sphera Solutions, Inc.

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: EcoVadis announced a strategic partnership with Workiva Inc. to connect EcoVadis' Carbon Data Network primary supplier carbon data with Workiva Carbon, enabling mutual enterprise customers to transition from industry average emissions estimates to granular, audit-ready Scope 3 calculations. The partnership positions EcoVadis as the supplier data engine and Workiva as the calculation and disclosure layer, creating a joint offering that targets the most critical data-quality gap in CSRD ESRS E1 Wave 1 reporting.

- May 2026: Sweep and Arcadis launched a global partnership combining Sweep's sustainability intelligence platform with Arcadis' advisory, delivery, and transformation expertise. The partnership is designed to help enterprises convert fragmented sustainability data into operational business intelligence and carbon reduction strategies, with growing commercial momentum in the US market.

- April 2026: Sweep and CFGI announced a strategic partnership combining Sweep's sustainability data management platform with CFGI's finance, accounting, and ESG expertise. The collaboration targets enterprises preparing for CSRD and IFRS S2 reporting obligations, delivering audit-ready sustainability disclosures backed by technical accounting controls.

- April 2026: ClimeCo and Greenly announced a strategic collaboration combining Greenly's AI-first GHG accounting platform with ClimeCo's environmental market advisory capabilities. The partnership streamlines compliance-grade emissions accounting for over 3,500 Greenly clients across 20 industries, enabling companies to align with global disclosure regulations and invest in verifiable decarbonization projects.

Global Application Carbon Footprint Monitoring Software Market Report Scope

The Application Carbon Footprint Monitoring Software market comprises digital platforms and services that enable organizations to measure, monitor, and optimize greenhouse gas emissions from applications and IT workloads. These solutions provide functionalities such as carbon measurement and attribution, runtime carbon monitoring, reporting and compliance management, sustainability analytics and benchmarking, and optimization and decision support. By embedding carbon intelligence into application performance monitoring, these systems help enterprises reduce energy consumption, improve resource efficiency, and align IT operations with ESG and decarbonization goals.

The Application Carbon Footprint Monitoring Software market report is segmented by Offering (Software and Services), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Application (Carbon Measurement and Attribution, Runtime Carbon Monitoring, Reporting and Compliance Management, Sustainability Analytics and Benchmarking, Optimization and Decision Support), End-Use Industry (IT and Telecom, BFSI, Industrial Manufacturing, Energy and Utilities, Oil and Gas, Retail and E-Commerce, Food and Beverage Manufacturing, Transportation and Logistics, Construction and Infrastructure, Government and Public Sector, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Carbon Measurement and Attribution |

| Runtime Carbon Monitoring |

| Reporting and Compliance Management |

| Sustainability Analytics and Benchmarking |

| Optimization and Decision Support |

| IT and Telecom |

| BFSI |

| Industrial Manufacturing |

| Energy and Utilities |

| Oil and Gas |

| Retail and E-Commerce |

| Food and Beverage Manufacturing |

| Transportation and Logistics |

| Construction and Infrastructure |

| Government and Public Sector |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Offering | Software | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Application | Carbon Measurement and Attribution | |

| Runtime Carbon Monitoring | ||

| Reporting and Compliance Management | ||

| Sustainability Analytics and Benchmarking | ||

| Optimization and Decision Support | ||

| By End-User Industry | IT and Telecom | |

| BFSI | ||

| Industrial Manufacturing | ||

| Energy and Utilities | ||

| Oil and Gas | ||

| Retail and E-Commerce | ||

| Food and Beverage Manufacturing | ||

| Transportation and Logistics | ||

| Construction and Infrastructure | ||

| Government and Public Sector | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the size of the application carbon footprint monitoring software market?

The application carbon footprint monitoring software market was valued at USD 0.47 billion in 2025, stands at USD 0.60 billion in 2026, and is forecast to reach USD 2.12 billion by 2031 at a CAGR of 28.72%.

Which region leads demand for application carbon footprint monitoring software?

Europe led in 2025 with 34.63% of global revenue, supported by dense reporting obligations and stronger corporate sustainability reporting infrastructure.

Which deployment model is growing fastest in this space?

Hybrid deployment is the fastest-growing model with a projected 29.12% CAGR through 2031, as companies try to balance cloud scale with tighter data governance.

Why are large enterprises still the main buyers of carbon monitoring platforms?

Large enterprises held 65.23% share in 2025 because they face more complex multi-entity reporting, larger Scope 3 inventories, and stronger board and investor scrutiny.

What is the main application area for these platforms today?

Reporting and compliance management led with 28.74% share in 2025, because many buyers still start with audit-ready disclosure and regulatory reporting before expanding into planning tools.

Which end-use segment is expected to grow the fastest through 2031?

Retail and e-commerce is expected to grow the fastest at 29.05% CAGR, driven by supplier-data requirements and product-level carbon reporting across large purchased-goods networks.

Page last updated on: