Organic Chips Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 16.74 Billion |

| Market Size (2031) | USD 30.37 Billion |

| Growth Rate (2026 - 2031) | 6.32% CAGR |

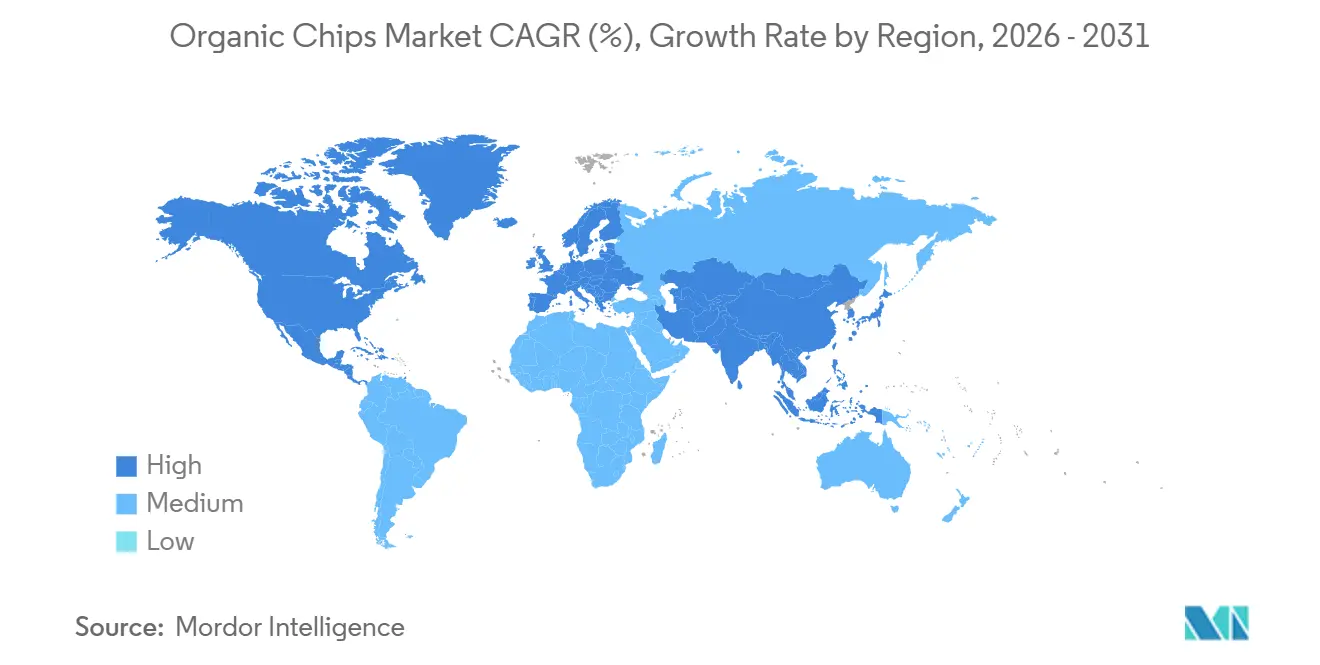

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Organic Chips Market Analysis by Mordor Intelligence

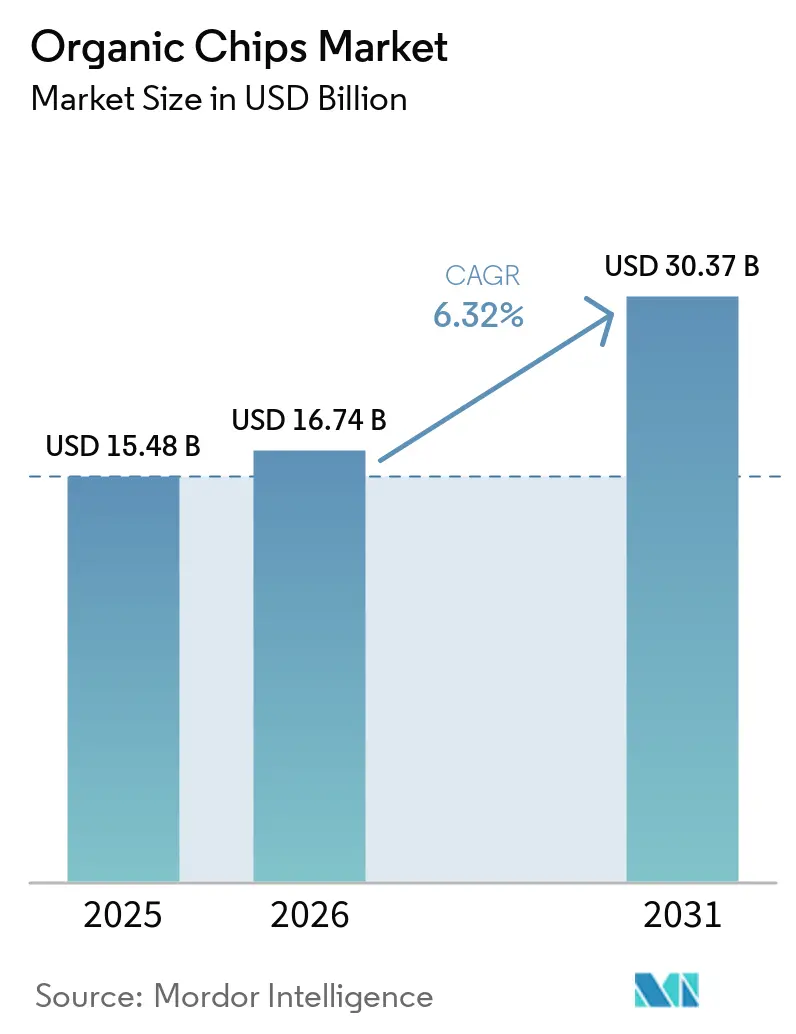

The organic chips market size is projected to expand from USD 15.48 billion in 2025 to USD 16.74 billion in 2026 and to USD 20.37 billion by 2031, registering a CAGR of 6.32% between 2026 and 2031. The category is benefiting from a broader rise in organic food spending, as the U.S. organic sector reached USD 76.6 billion in 2025 and grew 6.8%, faster than conventional food categories that year, according to the Organic Trade Association[1]Source: Organic Trade Association, “Organic Food and Products Hit USD 76.6 Billion in 2025, Doubling Conventional Market Growth,” New Hope Network, newhope.com. That demand pattern supports the organic chips market because shoppers are moving toward certified, clean-label snack options rather than treating organic purchases as occasional trade-ups. Competition is also being shaped by tighter certification rules, since brands with stronger traceability systems are better placed to defend shelf space and retailer trust. Product development in flavors, formats, and sustainable packaging is broadening appeal without straying from the category’s minimal-ingredient identity. The organic chips market is also gaining from stronger online discovery and broader premium retail placement, which helps brands explain sourcing, certification, and ingredient quality more clearly to younger buyers.

Key Report Takeaways

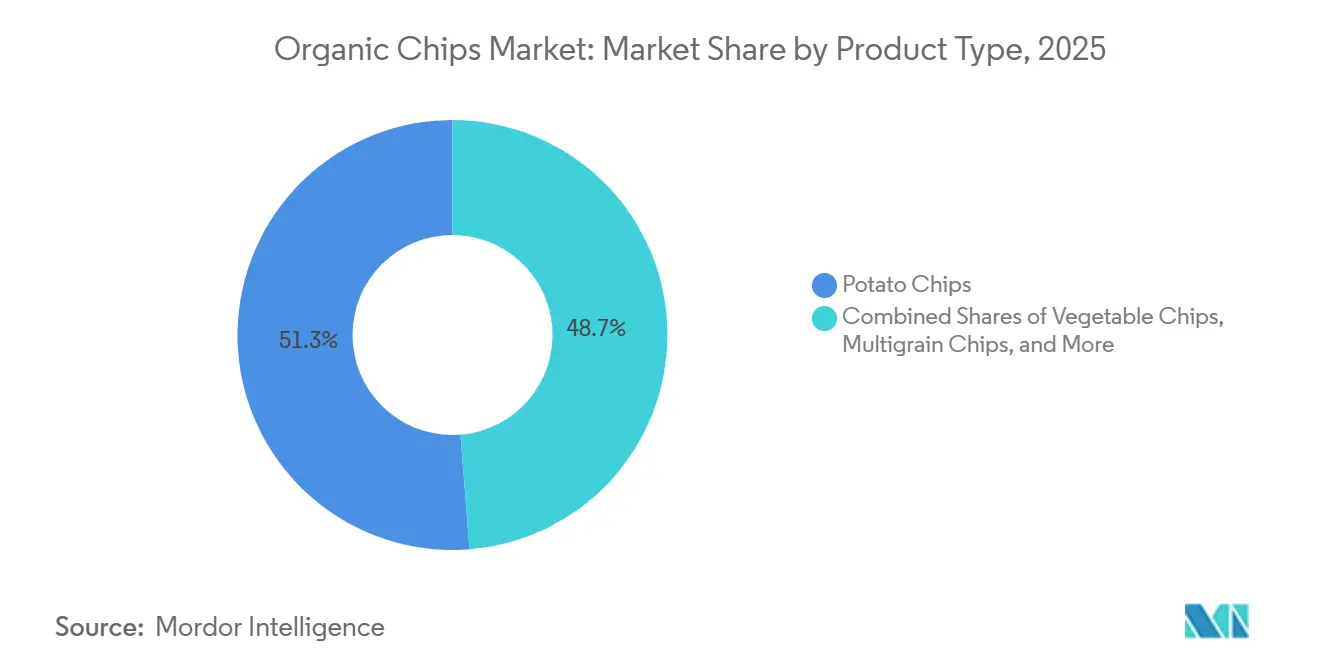

- By product type, Potato Chips led with 5126% of the organic chips market share in 2025, while Multigrain Chips recorded the highest projected CAGR at 7.54% through 2031.

- By flavor, Salted accounted for 65.78% of the organic chips market size in 2025, while Flavored is forecast to grow at a 7.62% CAGR through 2031.

- By packaging type, Bags held 45.38% of the organic chips market size in 2025, while Resealable Pouches are set to expand at a 7.23% CAGR through 2031.

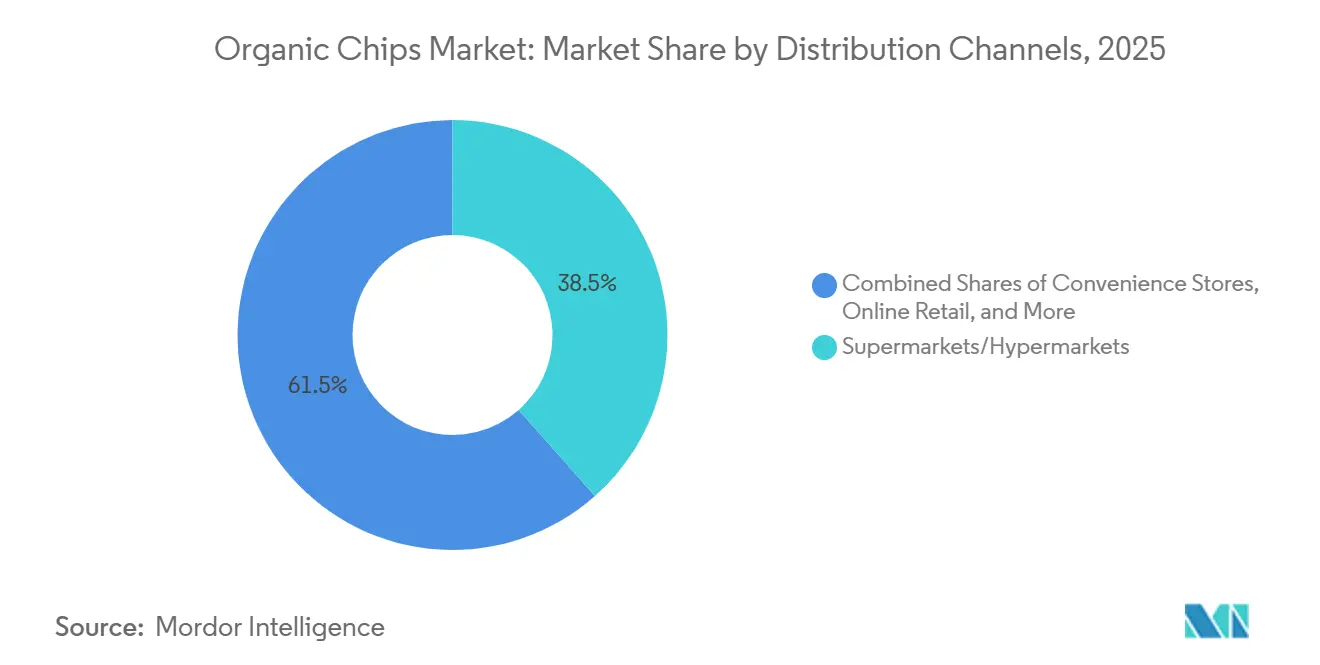

- By distribution channel, Supermarkets and Hypermarkets captured 38.47% of the organic chips market size in 2025, while Online Retail is projected to grow at a 7.78% CAGR through 2031.

- By geography, North America held 42.31% of the organic chips market share in 2025, while Asia-Pacific is forecast to record the fastest regional CAGR at 8.02% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Organic Chips Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for clean-label products | +1.4% | Global, led by North America and Western Europe, expanding to APAC urban centers | Medium term (2-4 years) |

| Growth of vegan and gluten-free dietary trends | +1.2% | Global, strongest in North America and Europe, with rapid uptake in urban APAC | Short term (≤ 2 years) |

| Product innovation and flavor diversification | +1.0% | Global, particularly North America, APAC, and Latin America | Short term (≤ 2 years) |

| Increasing awareness of organic and non-GMO foods | +0.8% | Global, led by North America and EU, with spillover to MEA urban markets | Medium term (2-4 years) |

| Growing popularity of plant-based diets | +0.7% | North America and Europe core, expanding to APAC premium segments | Medium term (2-4 years) |

| Sustainability and ethical consumption trends | +0.6% | Global, strongest in Northern and Western Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Clean-Label Products

Clean-label expectations now shape how the organic chips market competes in premium snacking. The USDA Strengthening Organic Enforcement rule became fully effective in March 2024, and it widened certification expectations across the supply chain, including brokers and importers. From July 2025, only NOP-certified entities appeared on import certificates, which raised the bar for claim verification in cross-border organic trade. That shift favors brands that already maintain chain-of-custody records and certification files across ingredients, processing, and import activity. It also makes retailer conversations less about broad brand messaging and more about proof that ingredient claims can withstand formal review. In the organic chips market, this creates a stronger position for established certified brands and a slower path for conventional snack suppliers trying to reformulate into organic lines.

Growth of Vegan and Gluten-Free Dietary Trends

The organic chips market is well placed to benefit from vegan and gluten-free demand because many chip formats fit those needs without major product redesign. Brands can therefore serve multiple diet preferences through the same core platform, especially when recipes are based on potatoes, corn, grains, or vegetables with simple seasoning systems. Nature’s Path expanded its gluten-free organic snack offering in January 2026 with a certified organic Love Crunch Gluten Free Strawberry Cheesecake granola launch, showing how established organic snack companies are actively leaning into this overlap. The same company followed with protein-led launches in 2025 and 2026, which points to a broader move toward snacks that combine organic certification with diet-specific functionality. This supports repeat purchases because shoppers do not need to trade away taste or convenience when choosing products that align with gluten-free or plant-based eating. For the organic chips market, the result is a wider buyer base that includes health-focused consumers, allergen-conscious households, and premium snack shoppers looking for cleaner labels.

Product Innovation and Flavor Diversification

Product innovation is a direct growth lever for the organic chips market because the basic salted format is already mature in many developed retail channels. Nature’s Path launched Que Pasa Organic Rolled Chips in August 2025, introducing the category’s first organic rolled tortilla chip with Chile & Lime and Spicy Queso variants made from heirloom corn. That move shows how companies are adding novelty through shape, texture, ingredient story, and flavor rather than moving away from the certified organic positioning that anchors trust. Flavor expansion also helps brands justify premium pricing because it gives consumers a clearer reason to trade up from conventional chips beyond the organic seal alone. In the organic chips market, flavored launches can create stronger trial rates in new regions while also refreshing mature shelves where plain salted options already dominate display space. The pace of SKU turnover is therefore becoming an important competitive tool, especially for companies that can scale new flavor concepts without weakening sourcing discipline.

Sustainability and Ethical Consumption Trends

Sustainability is becoming harder to separate from product quality in the organic chips market. Amcor and Burts launched a crisp pack in August 2025 using 55% post-consumer recycled content, and the companies tied the format to rising consumer interest in recycled packaging materials. TIPA also introduced a home-compostable metallized high-barrier snack film in February 2025, which addressed a practical challenge that has limited wider adoption of compostable formats in snack categories. Clearspring then removed single-use plastic trays from its Organic Seaveg Crispies range in April 2025, linking packaging redesign to both waste reduction and operating efficiency. These developments suggest that packaging choice is becoming part of brand credibility rather than a secondary issue handled after product formulation. In the organic chips market, this raises the value of suppliers and brands that can meet freshness, shelf-life, and sustainability needs in the same package structure.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of organic raw materials | -0.9% | Global, strongest in import-dependent markets including APAC, MEA, and South America | Medium term (2-4 years) |

| Certification and regulatory compliance costs | -0.6% | Global, with concentrated burden on small-to-mid-size operators in North America and Europe | Short term (≤ 2 years) |

| Intense competition from conventional chips at lower price points | -0.5% | Global, most pronounced in price-sensitive markets including MEA, South America, and tier-3 and tier-4 cities in APAC | Short term (≤ 2 years) |

| Volatility in organic raw material procurement and pricing | -0.3% | Global, particularly affecting sunflower oil and potato-dependent supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Organic Raw Materials

The organic chips market still faces a basic affordability problem because certified organic inputs remain more expensive than standard alternatives. That cost gap becomes more visible in frying oils, potatoes, corn ingredients, and seasoning blends, where even small changes in procurement costs can alter margin structure for premium snack products. The pressure increased in the 2025 to 2026 season as Ukraine’s sunflower seed crop fell by 8%, which kept FOB Black Sea refined sunflower oil prices in the USD 1,100 to USD 1,250 per tonne range through Q2 2026. For brands that use sunflower oil in frying or flavor delivery, it added another layer of cost strain on top of the existing organic premium. This matters more in the organic chips market because retail price premiums are already high enough to narrow the addressable base in price-sensitive channels. Companies with broader sourcing options, longer contracts, or stronger manufacturing scale are therefore better positioned to protect margins without weakening product quality.

Certification and Regulatory Compliance Costs

Certification spending remains a meaningful restraint for the organic chips market because it does not end once a product receives approval. USDA organic certification fees range from USD 700 to USD 2,500 or more annually, while the Organic Certification Cost Share Program reimburses up to 75% of eligible fees with a cap of USD 750 per certification scope. The support is helpful, but it does not remove the wider administrative work tied to audit preparation, supplier verification, recordkeeping, and import documentation[2]Source: CCOF, “Organic Certification Cost Share Program Update,” CCOF, ccof.org. The USDA Strengthening Organic Enforcement rule also expanded the number of domestic businesses that need certification, adding new compliance work across the chain rather than limiting it to growers and processors. In the organic chips market, multi-ingredient products can face a heavier burden because each organic component must remain traceable across separate suppliers and handling steps. That makes regulatory readiness a direct operating cost, and it tends to weigh more heavily on smaller brands than on diversified snack companies with dedicated compliance teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Potato Chips Hold Scale While Multigrain Chips Build Faster Momentum

Potato Chips held 51.26% of the organic chips market share in 2025, which kept them as the largest product type by a wide margin. Their lead reflects strong shopper familiarity, broad retail acceptance, and a manufacturing base that already understands how to scale potato-based snacks across premium and mainstream channels. In the organic chips market, potato products also benefit from simple ingredient communication because the base format fits clean-label expectations without extensive explanation. That advantage matters in impulse purchases, where buyers often make quick decisions based on taste, familiarity, and trust in a short ingredient list. The segment therefore remains central to category volume, even as newer subcategories attract more attention in premium launches.

Multigrain Chips are projected to grow at a 7.54% CAGR through 2031, which makes them the fastest-growing product type in the organic chips market. Their appeal rests on how well they connect organic certification with broader nutrition cues such as whole grains, ancient grains, seed mixes, and more varied textures. That combination gives brands more room to present products as a step up from standard potato chips without moving too far away from the familiar chip format. Vegetable Chips, Corn Chips, and other emerging bases still matter because they give the organic chips industry more flexibility in addressing regional tastes and shelf differentiation. Over time, the product mix is likely to become more layered, with potato chips anchoring scale while multigrain and alternative-base products capture the category’s premium growth.

By Flavor: Salted Products Stay Core While Flavored Lines Expand Premium Demand

Salted chips accounted for 65.78% of the organic chips market size in 2025, which shows that the category still relies on a simple, minimal-ingredient proposition. That position is not only a taste preference. It also reflects the trust consumers place in products that present organic credentials in the most direct form. In the organic chips market, salted formats are often the first point of trial because they ask buyers to pay for cleaner sourcing rather than for added seasoning complexity. This keeps the segment especially important in retailers where the category is still building awareness. It also gives brands a stable base from which they can extend into more premium variants.

Flavored chips are forecast to grow at a 7.62% CAGR through 2031, which makes them the faster-moving side of the flavor split. Nature’s Path’s 2025 Que Pasa launch showed how brands are broadening the organic chips market through more distinctive flavor stories such as Chile & Lime and Spicy Queso while still emphasizing heirloom corn and cleaner formulations. Flavored products usually carry stronger premium positioning because they offer novelty, more visible brand identity, and a clearer reason for shoppers to try another SKU. They also demand better control over certified seasoning supply and formulation consistency, which favors companies with established sourcing networks. As a result, flavor innovation is likely to remain one of the clearest ways the organic chips industry raises value even when unit volumes grow at a steadier pace.

By Packaging Type: Bags Retain the Lead While Resealable Formats Improve Usage Value

Bags held 45.38% of the organic chips market size in 2025, making them the most common packaging format across the category. Their lead comes from low material intensity, wide machine compatibility, and easy integration into standard shelf layouts. In the organic chips market, bags also work well for brands that need a familiar pack shape while keeping the front panel focused on organic claims, ingredients, and certification marks. That makes them especially effective in supermarkets, where shoppers compare multiple snack brands in a short time. The format is therefore likely to remain the default for mainstream distribution and larger-volume SKUs.

Resealable Pouches are projected to grow at a 7.23% CAGR through 2031, which points to a different kind of value in the organic chips market. These packs fit portion control, freshness retention, and premium presentation, which align closely with the habits of health-conscious snack buyers. They can also support higher price points because they offer a more useful pack experience after the initial purchase. TIPA’s high-barrier compostable snack film and Amcor’s recycled-content crisp packaging both show that suppliers are trying to solve performance and sustainability needs at the same time. Bulk Containers and other pack types will continue to serve club, foodservice, and single-serve occasions, but the faster movement is clearly in formats that combine convenience with a stronger premium cue. That shift suggests packaging is becoming a more active part of brand choice rather than only a logistics decision.

By Distribution Channel: Supermarkets Lead Volume While Online Retail Gains Strategic Importance

Supermarkets and Hypermarkets held 38.47% of the organic chips market size in 2025, which kept them as the largest distribution channel. Their lead is tied to scale, visibility, and the role they play in product discovery for shoppers who still want to compare organic snacks in person. In the organic chips market, this channel is also where natural food sections and broader premium snacking sets help newer brands appear beside more established names. Physical shelves remain important because the category still depends on front-of-pack trust signals such as certification logos, ingredient simplicity, and premium packaging cues. That gives supermarkets a continued role in first purchase and repeat pickup alike.

Online Retail is projected to grow at a 7.78% CAGR through 2031, making it the fastest-growing channel for the organic chips market. Digital channels help brands explain sourcing, flavor intent, and packaging choices in more detail than a shelf tag can provide. They also support direct feedback loops on trial packs, variety bundles, and subscription offers, which is useful in a category where product story matters almost as much as taste. The Organic Trade Association’s 2026 report identified Millennials and Gen Z as the fastest-growing organic buyer groups, which supports the fit between the organic chips market and online shopping behavior. Health and Beauty Stores and other channels still matter because they attract a more intentional premium shopper, but the strongest structural shift is toward digital channels that help niche brands build awareness with less dependence on traditional shelf access.

Geography Analysis

North America held 42.31% of the organic chips market share in 2025, which kept it as the largest regional contributor. The region benefits from mature organic food retail networks, stronger consumer understanding of organic labels, and a larger base of brands already operating in natural and premium snack categories. According to the International Food Information Council data from 2024, more than half of Americans (56%) replace traditional meals with snacking in the United States[3]Source: International Food Information Council, "American Consumer Perceptions of Snacking", ific.org. organic sector reached USD 76.6 billion in 2025 and grew 6.8%, which provided a favorable backdrop for premium snack categories such as the organic chips market. Younger buyer groups are also expanding their role in organic purchasing, which supports the trial of new snack formats and faster digital discovery. Canada adds depth through established organic brands, while Mexico remains relevant as a supply and product development base for corn-based and tortilla-style snack formats.

Europe remained the second-largest regional market for the organic chips market, supported by advanced organic consumption patterns in Germany, the United Kingdom, France, and the Nordic countries. The region’s importance is not only demand-driven. It is also shaped by stricter expectations around packaging sustainability, product documentation, and retailer compliance. That creates a setting where certified organic positioning can be strengthened further by credible packaging choices and cleaner supply chain records. The organic chips market is therefore likely to reward suppliers that can combine ingredient transparency with lower-impact packaging rather than treating those issues separately. European competition is likely to remain premium-led, with greater emphasis on documentation quality and retailer acceptance than on low-price volume play alone.

Asia-Pacific is forecast to grow at an 8.02% CAGR through 2031, making it the fastest-growing region in the organic chips market. Rising disposable incomes, urban health awareness, and stronger organized retail are widening the consumer base for premium packaged snacks across the region. The demand pattern also fits well with products that can connect organic sourcing to plant-based eating and cleaner everyday snacking. South America offers a smaller but developing opportunity, while the Middle East and Africa remain earlier-stage markets where premium demand exists but scale is more limited. Across both regions, the organic chips market still faces stronger price pressure from conventional products, which can slow adoption even when consumer interest in wellness and cleaner labels is improving.

Competitive Landscape

The organic chips market remains fragmented, and no single company holds a decisive leadership position. That said, the space is seeing stronger activity from large food companies that want faster entry into premium organic snacking. Hershey completed its acquisition of LesserEvil in November 2025 for approximately USD 750 million, after first announcing the deal in April 2025 and highlighting LesserEvil’s USD 165 million revenue in 2024. That move shows that established snack groups are willing to buy growth, brand authenticity, and cleaner-label credibility rather than build them slowly from within. It also raises the pressure on independent brands because larger owners can bring broader distribution, media spending, and supply chain support after an acquisition closes.

Campbell’s is taking a different route in the organic chips market by focusing on network efficiency and scale. In January 2026, the company announced a USD 230 million supply chain investment through fiscal 2026, including the closure of its Hyannis, Massachusetts potato chip plant and added capacity in Hanover, Pennsylvania, and Charlotte, North Carolina. That kind of restructuring matters because premium snack categories still face input cost pressure, so manufacturing flexibility can be as important as brand equity. Utz also reported nearly 5% Branded Salty Organic Net Sales growth in 2025, supported by Boulder Canyon and paired with a 35% year-over-year rise in marketing spending to widen geographic reach. These examples show that the competitive battle in the organic chips market is taking place across acquisitions, plant networks, and brand support rather than through one dominant player taking share from the entire field. The result is a category where concentration remains low, but scale advantages are becoming more visible.

There is still open space in the organic chips market where larger incumbents are not covering every premium niche. Protein-enriched formats, more region-specific flavor profiles, and digitally native brands with strong traceability systems all have room to grow within the category. Compliance capability is also becoming a competitive filter, because brands that can document organic handling more clearly are in a better position with both retailers and cross-border supply partners. The organic chips market therefore remains open enough for innovation, but not simple enough for small brands to scale without strong sourcing, packaging, and compliance discipline.

Organic Chips Industry Leaders

-

The Hain Celestial Group, Inc.

-

General Mills, Inc.

-

Kettle Foods

-

Terra Chips

-

Cape Cod Potato Chips

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Healthy snacking brand To Be Honest (TBH), a subsidiary of Ghodawat Consumer Limited (GCL), launched Mix Veggie Chips, strengthening its presence in India's rapidly growing clean-label and better-for-you snacks segment. The new product combines vacuum-cooked golden sweet potato, purple sweet potato, jackfruit, beetroot, and okra, offering over 90% nutrient retention, 40% less fat, and no palm oil.

- September 2025: Natural Grocers expanded its private-label product portfolio with the launch of Organic Restaurant-Style Tortilla Chips, available in Blue Corn, White Corn, and Yellow Corn varieties. Made with authentic stone-ground organic corn and sea salt, the chips are certified organic, non-GMO, vegan-friendly, and kosher.

- June 2025: Calbee America launched Weston’s Family Farms Organic Potato Chips, a new line of USDA-certified organic, non-GMO, and gluten-free potato chips developed in partnership with Gold Dust & Walker Farms. The product range is made from single-source potatoes sourced through a 20-year farming partnership and is available in Sea Salt, Sea Salt & Vinegar, and White Truffle flavors.

Global Organic Chips Market Report Scope

| Potato Chips |

| Vegetable Chips |

| Corn Chips |

| Multigrain Chips |

| Others |

| Salted |

| Flavored |

| Bags |

| Resealable Pouches |

| Bulk Containers |

| Others |

| Supermarkets/Hypermarkets |

| Health & Beauty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Potato Chips | |

| Vegetable Chips | ||

| Corn Chips | ||

| Multigrain Chips | ||

| Others | ||

| Flavor Type | Salted | |

| Flavored | ||

| Packaging Type | Bags | |

| Resealable Pouches | ||

| Bulk Containers | ||

| Others | ||

| By Distribution Channels | Supermarkets/Hypermarkets | |

| Health & Beauty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the organic chips space?

The organic chips market size stands at USD 16.74 billion in 2026 and is forecast to reach USD 20.37 billion by 2031 at a 6.32% CAGR.

Which region leads demand for organic chips?

North America led with 42.31% share in 2025, supported by mature organic retail channels and stronger consumer familiarity with certified products.

Which region is growing the fastest through 2031?

Asia-Pacific is projected to expand at an 8.02% CAGR through 2031, ahead of other regions, due to urban health awareness and rising premium snack demand.

Which product type dominates sales today?

Potato Chips held 51.26% share in 2025, making them the largest product type because of broad familiarity and strong retail acceptance.

Page last updated on: