Organic Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

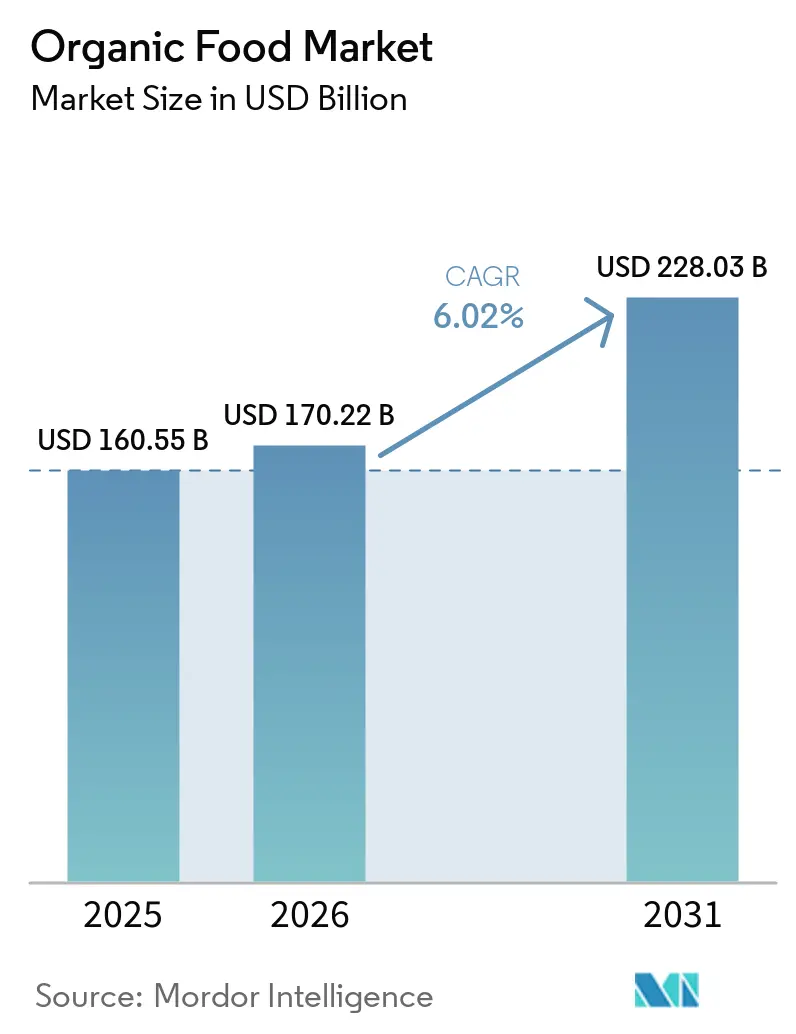

| Market Size (2026) | USD 170.22 Billion |

| Market Size (2031) | USD 228.03 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organic Food Market Analysis by Mordor Intelligence

The organic food market size is expected to grow from USD 160.55 billion in 2025 to USD 170.22 billion in 2026 and is forecast to reach USD 228.03 billion by 2031 at 6.02% CAGR over 2026-2031. Consumers are increasingly adding certified organic products to their mainstream grocery baskets, shifting away from their previous niche status. This change is driven by a stronger focus on health-conscious eating habits, careful attention to ingredient sourcing, and growing concerns about the use of synthetic inputs in food production. Retailers are expanding their distribution networks, governments are supporting organic farming systems, and digital platforms are making organic products more accessible, which collectively reduce the market's reliance on specialized outlets. Although challenges such as limited raw material supply and premium pricing remain, companies are meeting these obstacles with growing consumer demand, diversified distribution channels, and significant investments in brand development, ensuring the market maintains a steady growth trajectory.

Key Report Takeaways

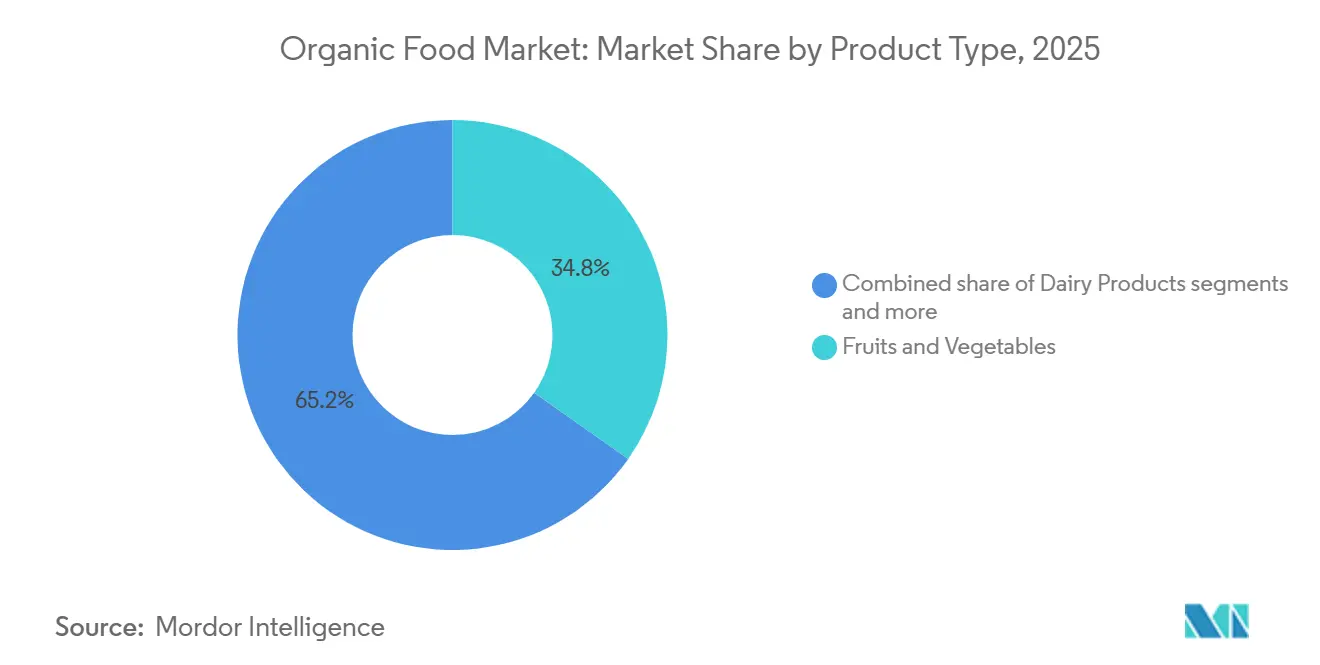

- By product type, fruits and vegetables held 34.78% share in 2025, while meat, fish, and poultry is projected to grow at a 7.21% CAGR through 2031.

- By form, fresh or chilled held 65.31% share in 2025, while frozen is projected to grow at a 7.51% CAGR through 2031.

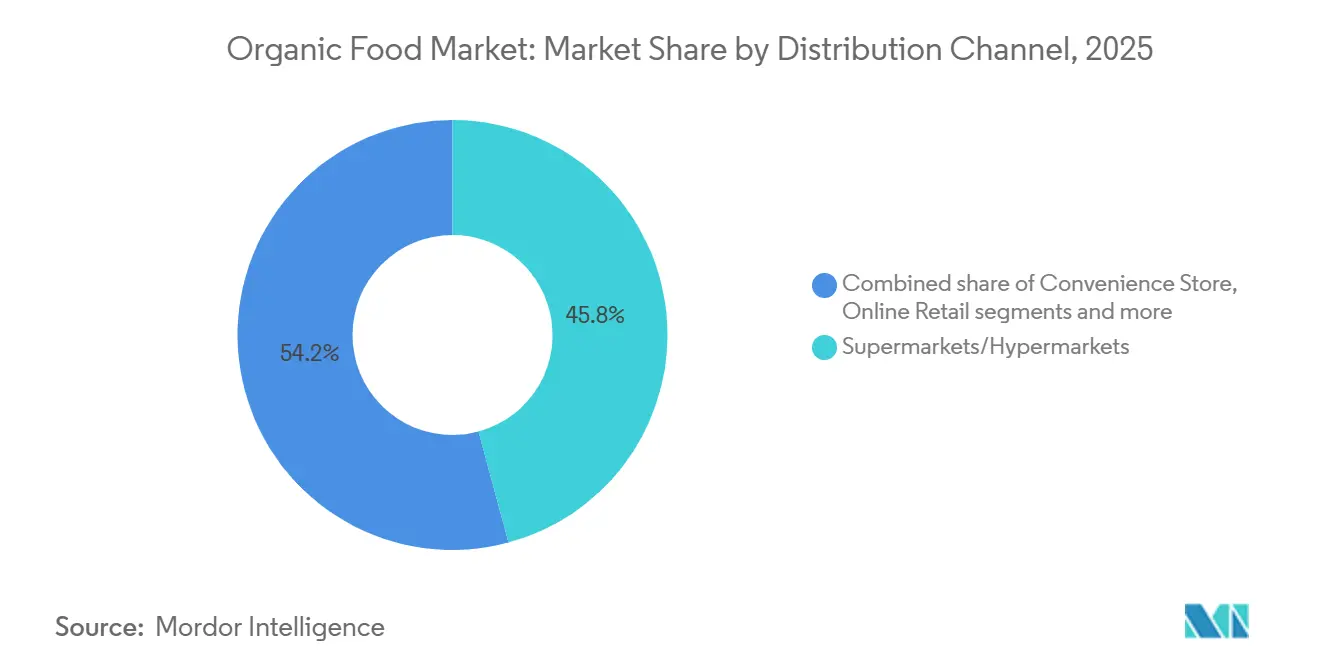

- By distribution channel, supermarkets and hypermarkets held 45.81% share in 2025, while online retail stores are projected to grow at an 8.15% CAGR through 2031.

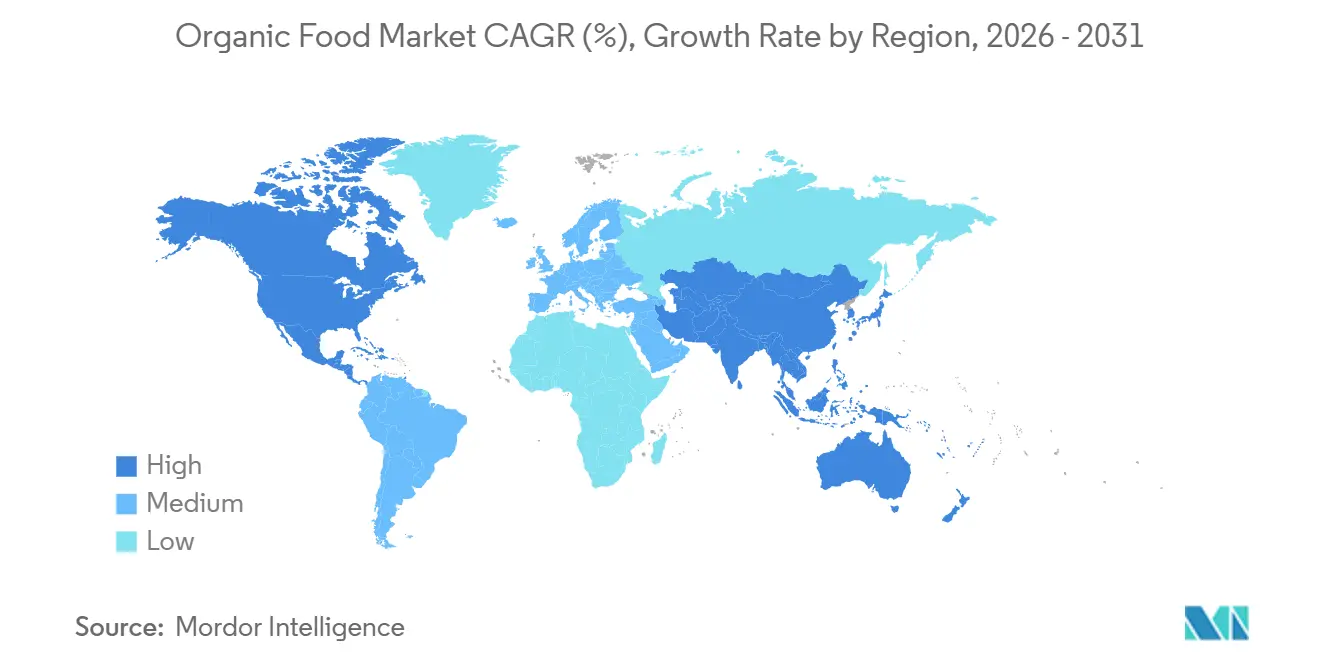

- By geography, North America held 38.45% share in 2025, while Asia-Pacific is projected to grow at a 7.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Organic Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Chemical-Free and Pesticide-Free Food Products | +1.4% | Global, led by North America and Europe | Medium term (2-4 years) |

| Increasing Preference for Natural, Clean-Label Products | +1.1% | Global, highest in North America and Northern Europe | Short term (≤ 2 years) |

| Rising Prevalence of Lifestyle-Related Diseases | +0.9% | Global, intensifying in Asia-Pacific and South America | Long term (≥ 4 years) |

| Supportive Government Initiatives Promoting Organic Farming and Products | +0.7% | Europe, India, North America, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Strong Marketing, Social Media Influence, and Brand Positioning Around Organic and Natural | +0.6% | Global, highest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Increasing Environmental and Sustainability Concerns | +0.5% | Global, led by Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for chemical-free and pesticide-free food products

The rising preference for food products produced without synthetic chemicals and pesticide residues is significantly contributing to the growth of the organic food market. Consumers are becoming increasingly aware of the links between dietary choices, health outcomes, and food safety, prompting a shift toward organically grown fruits, vegetables, dairy products, and packaged foods. Concerns over exposure to artificial fertilizers, pesticides, and genetically modified ingredients have further strengthened demand for certified organic alternatives. This trend is particularly evident among health-conscious consumers seeking clean-label and naturally sourced food options. At the same time, greater access to organic products through supermarkets, specialty stores, and online platforms is supporting wider adoption. According to the Organic Trade Association, U.S. organic product sales reached an all-time high of USD 76.6 billion in 2025, reflecting a 6.8% increase compared to the previous year[1]Source: Organic Trade Association, “U.S. Organic marketplace achieved significant growth in 2025”, ota.com. The strong sales growth underscores the expanding consumer willingness to invest in food products perceived as safer, more natural, and environmentally responsible.

Increasing preference for natural, clean-label products

Consumers are increasingly scrutinizing ingredient lists and seeking food products that are free from artificial additives, preservatives, synthetic colors, and genetically modified ingredients. This shift is being fueled by rising health awareness, demand for transparency, and a desire for minimally processed foods that align with healthier lifestyles. Organic food products naturally fit within the clean-label movement due to their strict production standards and limited use of synthetic inputs. Food manufacturers and retailers are responding by expanding their organic and clean-label product portfolios to meet evolving consumer expectations. According to research by the CBI Ministry of Foreign Affairs, clean-label products are expected to account for more than 70% of product portfolios in 2025 and 2026, up significantly from 52% in 2021[2]Source: CBI Ministry of Foreign Affairs, “Which trends offers opportunities”, cbi.eu. This substantial increase highlights the growing influence of clean-label trends on purchasing behavior, creating favorable conditions for continued growth in the organic food market.

Rising prevalence of lifestyle-related diseases

The increasing prevalence of lifestyle-related diseases is driving consumer demand for healthier dietary choices, thereby supporting the growth of the organic food market. Rising incidences of diabetes, obesity, cardiovascular disorders, and hypertension have heightened awareness of the role nutrition plays in disease prevention and long-term health management. As a result, consumers are increasingly opting for organic foods, which are perceived as being free from synthetic pesticides, artificial additives, and other potentially harmful substances. This trend is particularly strong among individuals seeking natural and nutrient-rich food options to support healthier lifestyles. Healthcare professionals and public health campaigns are also encouraging greater consumption of wholesome and minimally processed foods. According to the International Diabetes Federation (IDF), approximately 589 million adults aged 20–79 years were living with diabetes in 2024, and this figure is expected to reach 853 million by 2050[3]Source: International Diabetes Federation, “Diabetes around the world in 2024”, idf.org. The growing burden of chronic diseases is therefore reinforcing the demand for organic food products, contributing to sustained market expansion.

Supportive government initiatives promoting organic farming and products

Government support for organic agriculture is playing a significant role in driving the growth of the organic food market. Many countries are implementing policies, subsidies, certification programs, and financial incentives to encourage farmers to adopt organic farming practices and reduce reliance on synthetic fertilizers and pesticides. Governments are also investing in research, training, and awareness campaigns to improve organic farming productivity and strengthen supply chains. In addition, the establishment of organic certification standards and labeling regulations has enhanced consumer confidence in organic products. Export promotion programs and public procurement initiatives are further expanding market opportunities for organic producers. These measures are helping increase the availability and accessibility of organic food products across retail channels. As governments continue to prioritize sustainable agriculture, environmental conservation, and food safety, supportive policy frameworks are expected to remain a key factor driving the expansion of the organic food market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Production and Raw Material Costs Leading to Premium Shelf Prices | -0.7% | Global | Short term (≤ 2 years) |

| Stringent Organic Certification, Labeling Rules, and Compliance Overheads | -0.5% | Global, especially Europe, North America, India | Medium term (2-4 years) |

| Limited Consumer Awareness in Developing Regions | -0.4% | Asia-Pacific excluding China and Japan, Middle East and Africa, parts of South America | Long term (≥ 4 years) |

| Supply Chain and Distribution Challenges for Organic Products | -0.5% | Global, most acute in Middle East and Africa and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher production and raw material costs leading to premium shelf prices

Higher production and raw material costs pose a notable challenge to the growth of the organic food market. Organic farming practices often require greater labor input, natural pest management techniques, and adherence to stringent certification requirements, resulting in higher operational expenses than conventional farming. In addition, lower agricultural yields, limited supplies of certified organic ingredients, and higher processing and distribution costs contribute to increased overall production expenditures. These added costs are typically reflected in the final retail price of organic products, making them significantly more expensive than conventional alternatives. The premium pricing can limit accessibility for budget-conscious consumers and reduce purchase frequency, especially in price-sensitive markets. Economic pressures such as inflation and declining disposable incomes can further influence consumers to opt for lower-cost conventional products.

Stringent organic certification, labeling rules, and compliance overheads

Stringent organic certification and labeling requirements present a significant challenge for participants in the organic food market. Producers and manufacturers must comply with detailed regulations governing farming practices, processing methods, ingredient sourcing, and product traceability to obtain and maintain organic certification. The certification process often involves extensive documentation, regular inspections, audits, and renewal procedures, which can increase administrative and operational costs. For small-scale farmers and emerging businesses, these compliance requirements may create financial and resource burdens that limit market participation. Additionally, varying organic standards across different countries can complicate international trade and increase export-related compliance costs. Delays in certification approvals and the need for continuous monitoring further add to operational complexities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Produce Commands the Base While Protein Categories Accelerate

Fruits and Vegetables accounted for the largest share of the organic food market, representing 34.78% of total revenue in 2025. The segment's dominance is primarily driven by strong consumer preference for fresh organic produce, which is often perceived as healthier and safer than conventionally grown alternatives. Rising awareness regarding pesticide residues and chemical fertilizers has encouraged consumers to increase their purchases of organic fruits and vegetables. In addition, expanding retail availability through supermarkets, specialty stores, and online channels has improved product accessibility across both developed and emerging markets. Government initiatives supporting organic farming and sustainable agricultural practices have further strengthened supply within this category.

Meat, Fish, and Poultry is projected to be the fastest-growing product type segment, registering a CAGR of 7.21% during 2026–2031. Growth is being fueled by increasing consumer demand for ethically sourced and chemical-free animal protein products. Consumers are becoming more conscious about animal welfare standards, antibiotic usage, and feed quality, which is driving interest in certified organic meat and seafood offerings. Rising disposable incomes in emerging economies are also supporting premium food purchases, including organic protein products. Furthermore, retailers and foodservice operators are expanding their organic meat, fish, and poultry portfolios to meet evolving consumer preferences.

By Form: Fresh/Chilled Formats Lead but Frozen Formats Break Ahead

Fresh/Chilled products dominated the organic food market, accounting for 65.31% of total revenue in 2025. The segment's leadership is largely attributed to strong consumer preference for minimally processed foods that retain their natural taste, texture, and nutritional value. Fresh organic fruits, vegetables, dairy products, and meat continue to attract health-conscious consumers seeking clean-label and preservative-free food options. Growing awareness regarding food quality and sustainability has further strengthened demand for fresh organic products across both developed and emerging economies. In addition, the expansion of supermarket chains, specialty organic stores, and improved cold-chain infrastructure has enhanced product availability and accessibility.

Frozen products are projected to be the fastest-growing form segment, registering a CAGR of 7.51% during 2026–2031. Rising consumer demand for convenience foods that offer longer shelf life without compromising organic certification is a major factor driving growth. Frozen organic products provide year-round availability and help reduce food waste, making them increasingly attractive to busy households. Advancements in freezing technologies have also improved product quality, taste retention, and nutritional preservation, encouraging wider adoption. Retailers are continuously expanding their frozen organic product portfolios, including vegetables, fruits, ready meals, and snacks, to cater to evolving consumer preferences.

By Distribution Channel: Supermarkets Anchor Volume but Digital Channels Redefine Access

Supermarkets and Hypermarkets accounted for the largest share of the organic food market, representing 45.81% of total revenue in 2025. The segment's dominance is driven by its extensive product assortment, competitive pricing, and ability to offer consumers a convenient one-stop shopping experience. These retail formats have significantly expanded their organic food portfolios in response to rising consumer demand for healthier and sustainably sourced products. Strong supplier networks and well-established distribution systems enable supermarkets and hypermarkets to maintain consistent product availability across various organic categories. In addition, promotional campaigns, private-label organic offerings, and dedicated organic sections have helped attract a broader customer base.

Online Retail Stores are projected to be the fastest-growing distribution channel, registering a CAGR of 8.15% during 2026–2031. Growth is being fueled by increasing internet penetration, widespread smartphone usage, and the growing preference for convenient shopping experiences. Consumers are increasingly purchasing organic food products online due to the availability of a wider product selection, detailed product information, and doorstep delivery services. The expansion of e-commerce platforms and direct-to-consumer organic brands has further strengthened the channel's growth prospects. Subscription-based purchasing models, personalized recommendations, and digital promotions are also encouraging repeat purchases among consumers.

Geography Analysis

North America dominated the global organic food market, accounting for 38.45% of total revenue in 2025. The region's leadership is supported by high consumer awareness regarding health, nutrition, and sustainable food consumption. Strong demand for organic fruits, vegetables, dairy products, and packaged foods continues to drive market expansion across the United States and Canada. Well-established certification systems, extensive retail networks, and widespread availability of organic products have further strengthened market penetration. In addition, rising consumer preference for clean-label and non-GMO products has encouraged manufacturers to expand their organic product portfolios.

Asia-Pacific is projected to be the fastest-growing regional market, registering a CAGR of 7.64% during 2026–2031. Growth is being driven by rapid urbanization, rising disposable incomes, and increasing awareness of the health benefits associated with organic food consumption. Consumers across countries such as China, India, Japan, South Korea, and Australia are increasingly seeking food products that are free from synthetic chemicals and pesticides. Expanding middle-class populations and changing dietary preferences are creating significant opportunities for organic food manufacturers and retailers. Governments across the region are also promoting organic farming practices through policy support, certification programs, and agricultural development initiatives.

Europe, South America, and the Middle East & Africa continue to play important roles in the development of the global organic food market. Europe remains one of the most mature markets, supported by strong environmental awareness, stringent organic certification standards, and high consumer demand for sustainably sourced food products. Countries such as Germany, France, Italy, and the United Kingdom maintain substantial consumption of organic products across multiple categories. In South America, increasing organic agricultural production and rising export opportunities are supporting market growth, particularly in countries such as Brazil and Argentina. Meanwhile, the Middle East & Africa region is witnessing gradual expansion due to improving consumer awareness, rising health consciousness, and increasing availability of organic products through modern retail channels.

Competitive Landscape

The organic food market exhibits a moderately concentrated competitive landscape, characterized by the presence of several multinational food companies alongside specialized organic food producers. Leading participants such as Danone S.A., General Mills, Inc., and The Hain Celestial Group, Inc. maintain strong market positions through extensive product portfolios, established distribution networks, and well-recognized brands. These companies leverage their global reach and operational scale to strengthen their presence across key organic food categories. Market participants continue to focus on expanding their certified organic offerings in response to growing consumer demand for clean-label and sustainably produced foods. Strategic investments in product innovation, supply chain optimization, and brand development remain central to maintaining competitive advantages.

Competition within the market is driven by continuous product innovation, portfolio diversification, and efforts to address emerging consumer trends. Manufacturers are introducing new organic snacks, beverages, dairy alternatives, frozen foods, and plant-based products to capture a broader customer base. Companies are also investing in organic ingredient sourcing and sustainable farming partnerships to ensure a stable supply of certified raw materials. Acquisitions and strategic collaborations have become common approaches for expanding market presence and entering new geographic regions. In addition, firms are utilizing digital marketing strategies and e-commerce platforms to enhance consumer engagement and strengthen brand visibility.

The market also benefits from the growing participation of regional and niche organic food producers that cater to specific consumer preferences and local demand patterns. While global players dominate through scale and distribution capabilities, smaller companies often compete through product specialization, premium positioning, and locally sourced ingredients. Retailers are increasingly expanding private-label organic product offerings, further intensifying competition across various categories. The rise of online retail channels has lowered barriers to market entry and provided emerging brands with greater access to consumers. Sustainability commitments, ethical sourcing practices, and environmentally responsible packaging have become important factors influencing competitive positioning.

Organic Food Industry Leaders

Danone S.A.

General Mills, Inc.

The Hain Celestial Group, Inc.

United Natural Foods, Inc.

Nature's Path Foods Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Straus Family Creamery expanded the distribution of its organic super-premium ice cream nationwide through Whole Foods Market, marking the brand’s first entry into Whole Foods stores across the East Coast. The expansion includes organic ice cream pints and quarts in multiple flavors and significantly broadens the company’s retail footprint across the United States.

- January 2026: LT Foods Ltd. launched the “DAAWAT I’m Organic” range, introducing Organic Basmati Rice and Organic Sona Masoori Rice with QR-based traceability technology. The new product line enables consumers to access detailed information on cultivation, certification, processing, storage, and packaging through a front-pack QR code, enhancing transparency across the organic food value chain.

- May 2025: Hewitt Foods USA introduced The Organic Meat Co., a new organic meat brand featuring a USDA-certified organic, grass-fed, and grass-finished beef product line. The launch was designed to capitalize on rising consumer demand for organic and grass-fed meat products, supported by strong growth in organic meat sales across the United States. The initial portfolio includes organic ground beef and premium beef cuts produced without antibiotics, added hormones, or feedlot confinement.

Global Organic Food Market Report Scope

Organic food refers to agricultural and processed food products that are produced, handled, and certified according to established organic farming standards. The organic food is segmented by product type, form, distribution channel, and geography. By product type, the market is segmented into fruits and vegetables, meat, fish and poultry, dairy products, frozen and processed foods, and others. By form, the market is segmented into fresh/chilled, canned, and frozen. Based on distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD million).

| Fruits and Vegetables |

| Meat, Fish and Poultry |

| Dairy Products |

| Frozen and Processed Foods |

| Other Foods |

| Fresh/Chilled |

| Canned |

| Frozen |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| Noth America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Fruits and Vegetables | |

| Meat, Fish and Poultry | ||

| Dairy Products | ||

| Frozen and Processed Foods | ||

| Other Foods | ||

| By Form | Fresh/Chilled | |

| Canned | ||

| Frozen | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Region | Noth America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected value of the organic food sector by 2031?

The organic food market is forecast to reach USD 228.03 billion by 2031, rising at a 6.02% CAGR from 2026 to 2031.

Which product group leads global sales in organic food?

Fruits and vegetables led in 2025 with 34.78% share, supported by frequent purchases and strong concern around pesticide residues.

Which channel is growing fastest for organic food sales?

Online retail stores are projected to grow the fastest at an 8.15% CAGR through 2031, helped by wider digital shelf space and e-grocery adoption.

Which region currently leads organic food demand?

North America held 38.45% of global revenue in 2025.

What is the fastest-growing geographic region for organic food?

Asia-Pacific is projected to grow at a 7.64% CAGR through 2031, driven by urban middle-class demand and stronger food safety awareness.

Page last updated on: