Organic Packaged Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.75 Trillion |

| Market Size (2031) | USD 2.39 Trillion |

| Growth Rate (2026 - 2031) | 6.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

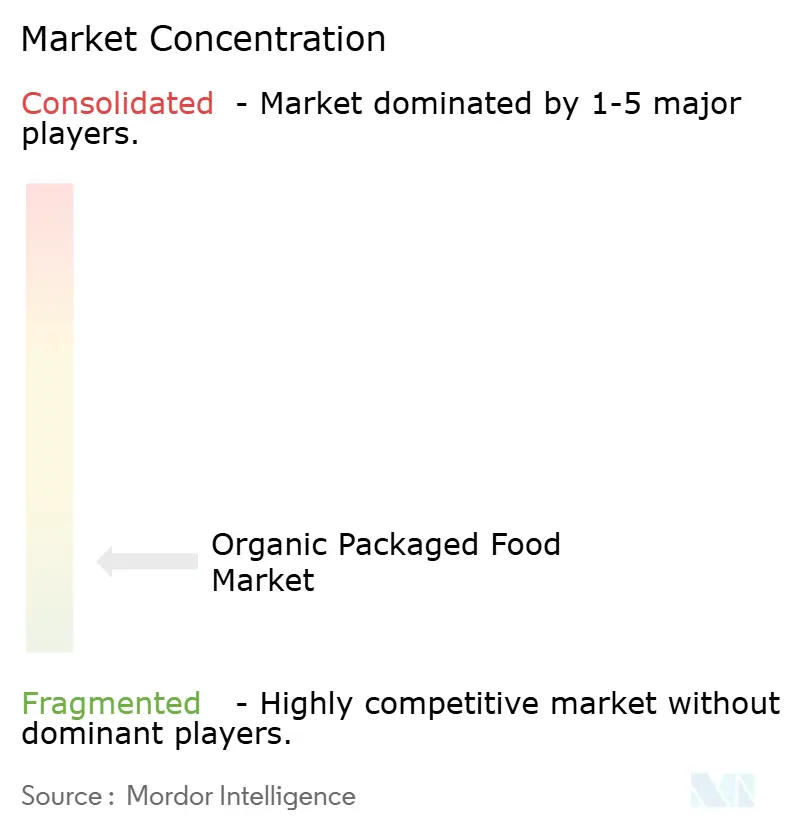

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Organic Packaged Food Market Analysis by Mordor Intelligence

The organic packaged food market size is projected to expand from USD 1.65 trillion in 2025 and USD 1.75 trillion in 2026 to USD 2.39 trillion by 2031, registering a CAGR of 6.39% between 2026 and 2031. The organic packaged food market is growing faster than the conventional packaged food market because a larger share of consumers now treats organic purchases as a routine food choice rather than an occasional premium purchase. The shift is supported by stronger interest in simpler ingredient lists, greater trust in certification systems, and retail formats that make organic products easier to access during everyday grocery trips and through digital orders. Policy support in the United States and Europe is also helping the organic packaged food market by improving investment conditions in the supply chain and providing farmers and processors with clearer signals for long-term capacity planning. At the same time, the organic packaged food market remains fragmented, meaning growth is shared among large multinational food groups, focused organic specialists, and smaller brands that use additional claims, such as Non-UPF verification and regenerative sourcing, to stand out. The main risk is still price pressure, as organic premiums remain visible across many categories, and a limited supply of certified ingredients can slow scale-up when demand rises quickly, especially in markets where consumer spending remains more sensitive.

Key Report Takeaways

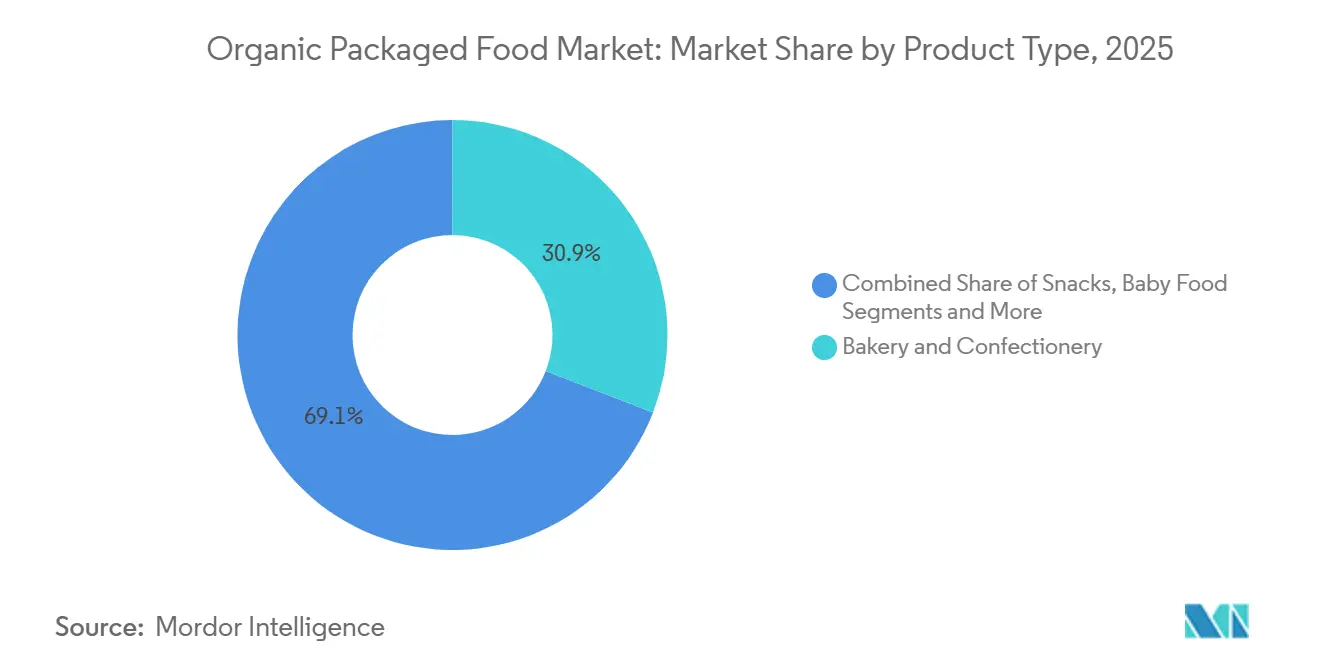

- By product type, Bakery and Confectionery held 30.87% of the organic packaged food market share in 2025, while Ready Meals are projected to expand at a CAGR 7.08% through 2031.

- By packaging type, PET and Glass Bottles accounted for 43.33% of the organic packaged food market size in 2025, while Pouches are expected to post the fastest projected CAGR at 6.94% through 2031.

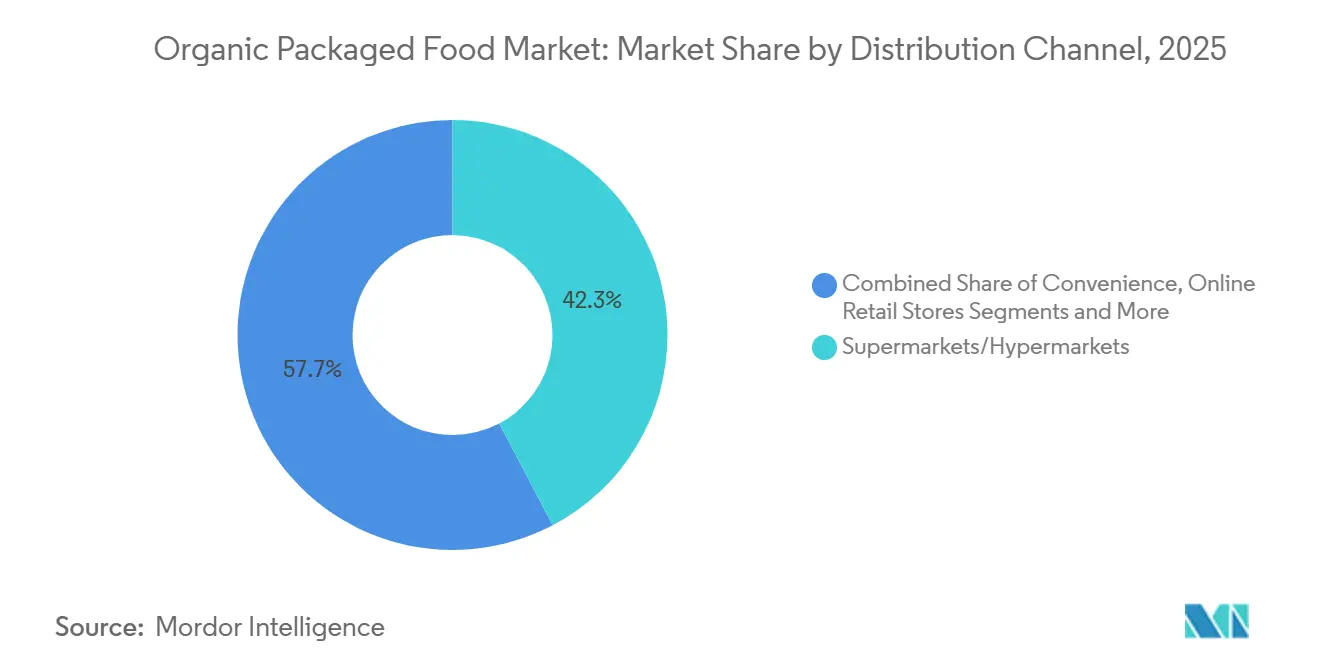

- By distribution channel, Supermarkets and Hypermarkets captured 42.27% share in 2025, while Online Retail Stores are anticipated to grow at the fastest CAGR of 7.84% through 2031.

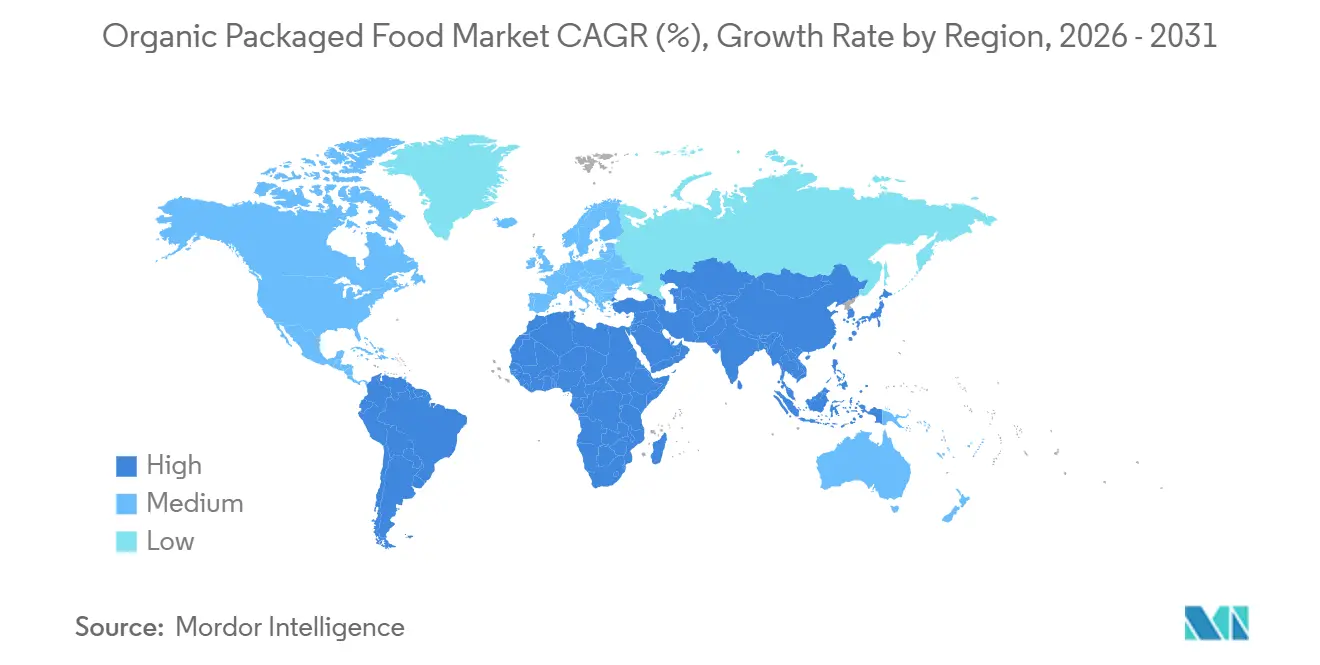

- By geography, North America led the organic packaged food market with 35.18% share in 2025, while Asia-Pacific is projected to expand at the fastest CAGR of 7.46% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Organic Packaged Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing preference for minimally processed and chemical-free packaged food products | +2.0% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Rising demand for clean-label snacks, cereals, bakery products, and beverages | +1.5% | North America and Europe core, spill-over to APAC urban centers | Short term (≤ 2 years) |

| Growing demand for organic baby food and children-focused nutrition products | +0.8% | Global, led by North America, rapid uptake in APAC and South America | Long term (≥ 4 years) |

| Product innovation in organic ready-to-eat meals, breakfast foods, and functional beverages | +0.7% | North America, Western Europe, expanding to urban APAC | Medium term (2-4 years) |

| Growing influence of wellness, preventive health, and immunity-focused food consumption | +1.0% | Global, particularly APAC, North America, and MEA urban centers | Medium term (2-4 years) |

| Government incentives for organic food producers | +0.5% | Europe and North America, emerging in South and East Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing preference for minimally processed and chemical-free packaged food products

Consumer aversion to synthetic pesticides, artificial additives, and ultra-processed food formulations is re-ranking purchase criteria across mature and developing markets alike. The "Make America Healthy Again" cultural movement in the United States and the EU's Farm to Fork strategy, targeting 25% of EU agricultural land under organic farming by 2030, have both conferred policy-level credibility on organic certification that market-level advertising cannot replicate, according to the European Commission, EU Organic Action Plan[1]Source: European Commission, “Finalists Announced for the 2025 EU Organic Awards,” European Commission Agriculture and Rural Development, agriculture.ec.europa.eu. Amy's Kitchen earned Non-UPF Verified™ certification for 37 of its products in March 2026, becoming one of the first nationally distributed packaged food brands to achieve this independent process verification, demonstrating that demand is strong enough for manufacturers to invest in third-party credentialing well beyond USDA Organic alone. The fastest growth in clean-label organics is occurring in shelf-stable categories, where the absence of synthetic preservatives becomes a differentiated proof point rather than a manufacturing limitation.

Rising demand for clean-label snacks, cereals, bakery products, and beverages

Snacks and cereals are the category battleground where organic positioning intersects with convenience and impulse purchase dynamics. The Organic Trade Association's 2026 Organic Market Report confirmed that Millennials and Gen Z together represent the fastest-growing organic buyer segment, with their path-to-purchase dominated by on-the-go snacking occasions and driven by demand for ingredient transparency. Nature's Path Organic Foods, North America's largest independent organic breakfast and snack brand, launched the first certified organic granola inspired by the viral Dubai chocolate trend in May 2026, pairing USDA-certified whole grains with Fair Trade dark chocolate and real whole pistachios. The bakery and confectionery segment, which commanded the largest product-type share at 30.87% in 2025, benefits from dual demand vectors: the premiumization of everyday breakfast and the social media amplification of artisan-baked goods. General Mills accelerated its commitment to regenerative organic ingredients in November 2025, quadrupling the use of Kernza, a perennial grain, across four Cascadian Farm cereals, a move that ties organic certification to soil-health metrics and positions the brand ahead of anticipated EU supply-chain sustainability due diligence standards. Beverages compound this growth vector: Evolution Fresh launched USDA Certified Organic RTD teas in 2025 that blend cold-pressed juice with real brewed tea, targeting the functional beverage occasion at a 50-calorie, 10g-sugar formulation that resets category benchmarks.

Growing demand for organic baby food and children-focused nutrition products

Parental risk aversion around infant nutrition makes the baby food segment among the most structurally protected within the organic packaged food market. The Organic Trade Association's 2026 Organic Market Report recorded that organic baby food and formula grew 8.8% in 2025, now accounting for 11.0% of organic grocery sales, a rate triple that of total organic grocery growth, confirming structural rather than cyclical demand. Earth's Best, operating under Hain Celestial, debuted its Big Kids Snacks line in April 2026, certified USDA Organic, non-GMO, and formulated without artificial flavors or preservatives, extending its organic safety positioning from infancy into early childhood (ages 4 to 8) and broadening the addressable market window per household. The underlying second-order dynamic is that parents who begin purchasing organic for infant nutrition exhibit high retention as children age, creating a lifetime-value pathway that conventional CPG brands struggle to replicate from the other direction. Subscription-based organic baby food models are gaining material distribution ground, building recurring revenue and reducing dependence on shelf-space negotiations in brick-and-mortar retail. The FDA's infant formula oversight framework and USDA NOP certification requirements create structural barriers that shield certified-organic brands from low-cost substitutes and maintain quality floors that reinforce consumer trust.

Product innovation in organic ready-to-eat meals, breakfast foods, and functional beverages

Ready meals are the fastest-growing product type in the organic packaged food market, with a 7.08% CAGR through 2026–2031. This reflects a structural behavioral shift: consumers who normalized convenience eating during the pandemic era are now migrating those habits into organic and clean-label alternatives, seeking to reconcile time poverty with health intent. Amy's Kitchen ranked No.1 by dollar share across multiple organic frozen and shelf-stable ready-meal categories in 2025, including frozen entrees and burritos, and expanded into more than 150 Costco warehouses in May 2026, normalizing the organic ready-meal price point at high-volume club-channel scale. Functional beverages are a parallel accelerator: Danone launched profee-inspired ambient protein shakes in May 2026 with 30g of complete protein and 5g of prebiotic fiber per serving, blending organic nutrition credentials with the GLP-1 dietary support format that is demonstrably reshaping the snacking landscape. Manufacturers investing in high-pressure processing and UHT organic formulations are expanding shelf-life envelopes without synthetic preservatives, directly addressing one of the market's core restraint dynamics. The intersection of organic certification with protein-forward, GLP-1-aligned ready-meal formats represents an emerging sub-category that is still substantially underserved by established organic brands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher retail prices compared to conventional packaged food products | -1.5% | Global, most acute in price-sensitive APAC and South America | Short term (≤ 2 years) |

| Limited shelf life of organic packaged foods due to lower use of synthetic preservatives | -0.8% | Global, heightened in South America, MEA, and developing APAC | Medium term (2-4 years) |

| High certification, testing, traceability, and audit costs for manufacturers | -0.6% | Global, most acute for SMEs and emerging-market suppliers | Long term (≥ 4 years) |

| Challenges in scaling organic farming and supply chain logistics | -0.7% | Global, most severe in APAC, South America, and MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher retail prices compared to conventional packaged food products

The structural cost premium of organic packaged food over conventional alternatives remains the most persistent barrier to mass-market adoption globally. Organic production economics embed a baseline price markup rooted in lower yields per hectare, higher labor inputs, and the full cost stack of certification, all of which are passed through to retail shelf prices. The Soil Association's 2025 UK Organic Market Report identified "consumers buying less due to the cost of living" as one of the top three challenges for the sector, directly confirming that price sensitivity suppresses trial and repeat purchases among lower- to middle-income households, even when aspirational demand exists. A counterintuitive dynamic is emerging: private-label organic products in European hypermarkets are capturing share from branded organic lines, providing cost-accessible entry points that ultimately broaden category penetration rather than cannibalizing established premium brands. USDA economic analysis found organic retail price premiums narrowed in several categories in 2024 as supply-side investment increased, but this convergence has not yet translated into sufficient price parity to unlock mass-market volume in most APAC and Latin American markets. Manufacturers that invest in scale efficiencies, consolidated organic ingredient procurement, co-manufacturing agreements, or vertically integrated organic supply chains, are best positioned to compress the price gap without sacrificing margin.

High certification, testing, traceability, and audit costs for manufacturers

USDA organic certification costs vary widely from a few hundred dollars per year for simple operations to tens of thousands for large-scale processors, creating a structurally uneven competitive landscape that disadvantages smaller entrants and emerging-market suppliers. The USDA's Organic Certification Cost Share Program (OCCSP), which historically reimbursed up to 75% of certification costs (capped at USD 750 per category per year), was defunded by Congress for 2025 after exclusion from the Farm Bill extension, removing a critical support mechanism for transitioning operators precisely when certification applications were surging. New organic certifications surged nearly 200% in 2024, straining certifying agencies and extending processing timelines, which, in turn, delay market entry for producers and disrupt supply timelines for manufacturers, according to the Organic Integrity Cooperative (2025)[2]Source: Organic Integrity Cooperative, "New Organic Certifications Surge Nearly 200% in 2024" organicintegrity.coop. The EU's January 2025 update to Regulation 2018/848, requiring imported organic products to meet the same standards as EU-produced goods, increased administrative and financial burdens for non-EU suppliers, with some cooperative supply chains in third countries at risk of abandoning certification altogether. Taken together, these compliance factors create a real risk of supplier attrition in critical organic ingredient categories, which could tighten supply and inflate input costs for packaged food manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bakery and Confectionery Anchors Share, Ready Meals Lead Future Growth

The Bakery and Confectionery segment holds 30.87% of product-type share in 2025, supported by widespread consumer familiarity with organic certification in bread, granola, and cereal categories and the high purchase frequency of baked goods across breakfast and snacking occasions. General Mills' Cascadian Farm and Nature's Path collectively illustrate how organic cereals and granolas have embedded themselves as default premium breakfast options across North American grocery stores, both brands deploying trend-responsive innovation (Kernza grains in November 2025 and Dubai chocolate in May 2026, respectively) to sustain relevance in a category where flavor novelty drives repeat trial. Snacks benefit from dual demand dynamics: the pouch format is accelerating per-unit velocity in direct-to-consumer and online channels, while single-serve organic snack bars and protein-enriched formats are capturing incremental on-the-go occasions.

Ready Meals are the fastest-growing product type, projected to grow at a 7.08% CAGR through 2026-2031, underpinned by a behavioral shift from ingredient-level organic purchasing to whole-meal organic convenience, with Amy's Kitchen bringing organic frozen and shelf-stable meals to 45 million new US households in 2025 alone. Baby Food is one of the highest unit-level willingness-to-pay segments in the entire organic packaged food market, according to the OTA, 2026 Organic Market Report. Dairy and Dairy Alternatives, Breakfast Cereals, and Condiments and Sauces each serve distinct consumer cohorts and purchasing occasions, collectively anchoring stable mid-tier volume. Meat, Poultry and Seafood is emerging as a high-value growth pocket. The OTA reported organic meat, poultry, and seafood surged at a sigificant rate in the US in 2025, signaling genuine demand acceleration in a category where organic certification commands the most significant price premium

By Packaging Type: PET/Glass Bottles Hold Lead, Pouches Capture the Growth Curve

PET and Glass Bottles command 43.33% of packaging type share in 2025, reflecting their structural dominance across organic beverages, dairy, and liquid condiment categories. Glass in particular functions as a quality and purity signal for organic brands: the association between glass packaging and chemical-free product integrity aligns directly with the organic certification ethos, allowing premium pricing that is harder to justify in flexible or rigid plastic formats. The beverage category, growing at 7.2% in the US in 2025, with dairy alternative beverages (including organic oat milk), reinforces the role of PET and glass bottle formats as volume carriers in the fastest-expanding organic liquid categories, according to the OTA, 2026 Organic Market Report.

Pouches are the fastest-growing packaging format, projected at a 6.94% CAGR through 2026-2031, driven by the intersection of three structural forces: e-commerce compatibility (lightweight, transit-resilient), sustainability positioning (lower material weight versus glass or rigid plastic), and versatility across organic snack and baby food applications where resealability and single-serve convenience are decisive purchase factors. Cans serve a specialized role in organic ready meals, soups, and preserved goods, where their high-barrier properties partially offset the shelf-life constraints imposed by restricted synthetic preservative use, making them particularly relevant for the growing organic ready-meal segment.

By Distribution Channel: Supermarkets Dominate, Online Retail Emerges as the Structural Accelerator

Supermarkets and Hypermarkets command 42.27% of the organic packaged food distribution share in 2025, sustained by their footfall advantage, refrigerated category infrastructure, and the promotional machinery that scales organic shelf penetration across mainstream households. Italian organic market data from the Sana Observatory 2026 illustrates the channel's structural resilience: hypermarkets and supermarkets grew organic sales 4.3% in Italy in 2025, while modern retail accounted for 64% of total Italian organic consumption, even as e-commerce registered an independent 5.9% uplift. The channel's private-label organic momentum is also strategically significant: European discounters, including Lidl, registered a 0.5% organic share-of-trade uplift in the UK in 2024, confirming that organic is entering value-retail formats and no longer requires access to specialty channels, according to the Soil Association's UK Organic Market Report 2025.

Online Retail Stores are the fastest-growing channel, forecast at a 7.84% CAGR through 2026-2031. USDA ERS data confirms the internet's share of US organic food sales reached 6.7% in 2024, reflecting more than a decade of compound behavioral adoption rather than a short-term spike. Subscription models and direct-to-consumer relationships represent the channel's structural amplifier: they generate recurring revenue, enable premium organic assortment curation, and allow brands to build consumer education assets, product origin storytelling, regenerative farming content, that physical retail shelf space cannot accommodate. UK Soil Association data reinforces the digital signal: organic is twice as likely to be purchased online as non-organic, and 23% of supermarket organic purchases are completed via online grocery ordering, as per the Soil Association, UK Organic Market Report 2025[3]Source: Soil Association Certification, “Organic Market Report 2025,” Soil Association, soilassociation.org. Convenience and Grocery Stores play a complementary trial-and-top-up role, where single-serve organic formats and smaller-pack SKUs are creating first-exposure moments for consumers not yet committed to primary-destination organic shopping.

Geography Analysis

North America held 35.18% of the organic packaged food market share in 2025, making it the largest regional contributor. In the United States, USDA Economic Research Service data showed that organic food retail sales grew by 5.2%, well ahead of conventional food sales. The Organic Trade Association also reported that U.S. organic food was the largest market in 2025, which supports the view that organic demand is becoming more deeply embedded in everyday grocery spending. General Mills stated in its 2026 responsibility report that it remains the largest producer of natural and organic packaged food in the United States, and that 1 in 10 North American products is certified organic or made with organic ingredients. Canada and Mexico add to the region through supply ties, cross-border sourcing, and growing urban demand, while strong certification and labeling systems continue to support premium pricing and consumer confidence.

Europe remains the second major center of demand in the organic packaged food market, supported by policy alignment, mature retail infrastructure, and broad familiarity with certified organic claims. The European Commission continues to support the 25% organic farmland target by 2030, providing the region with a long-term signal for supply chain development and category expansion. The EU Council’s May 2026 negotiating position on simpler organic production and labeling rules should help lower administrative friction for producers while strengthening rule clarity across the regional organic packaged food market. South America is led by Brazil and Argentina, while the Middle East and Africa remain earlier-stage markets led by the UAE, Saudi Arabia, South Africa, and selected urban centers where premium retail and expatriate demand are strongest, even though logistics and price sensitivity still limit broader adoption.

Asia-Pacific is the fastest-growing region in the organic packaged food market, with a projected CAGR of 7.46% through 2031, and this reflects the region’s mix of rising middle-class demand, food-safety concerns, and stronger digital grocery access. China is benefiting from growing consumer attention to food integrity and from continued work on certification and sustainable agriculture systems that support domestic organic supply. India is strengthening its role through organic farming programs and through online grocery platforms that expose urban consumers to wider organic assortments than traditional trade can usually provide. Japan and Australia bring different strengths to the regional picture, with Japan focused on health-oriented premium food demand and Australia combining strong production standards with export credibility across Asian retail markets.

Competitive Landscape

The organic packaged food market remains fragmented, and competition is spread across multinational food companies, focused organic specialists, and smaller brands with strong category depth. Danone and Nestlé compete through broad portfolios and distribution reach, but neither dominates the full organic packaged food market across all product types and regions simultaneously. General Mills continues to hold an important leadership position in the United States, and its 2026 responsibility report highlighted both scale in organic production and the use of regenerative agriculture across more than 800,000 acres. Amy’s Kitchen is taking a different route by building trust through product-level credibility, including Non-UPF Verified certification for 37 products and wider Costco distribution for frozen meals. That contrast shows that the organic packaged food market rewards both scale and specialization, provided the brand can back its claims with sourcing discipline and recognizable quality signals.

Portfolio reshaping has become a visible part of competition in the organic packaged food market. Hain Celestial completed the USD 115 million sale of its North American snacks business in March 2026, which sharpened its focus on categories such as tea, yogurt, and organic baby food instead of maintaining a broader natural snacks spread. SunOpta’s completion of its arrangement with Refresco in April 2026 pointed to a second theme, where supply chain and manufacturing scale matter as much as brand ownership in organic beverages and plant-based products. Nature’s Path also showed that independent brands can still move quickly when it launched a certified organic granola range linked to a fast-moving consumer flavor trend in May 2026. Together, these moves show that competition in the organic packaged food market is shifting toward sharper category focus, faster innovation, and better control over upstream supply.

Compliance is becoming a stronger competitive filter in the organic packaged food market because traceability and labeling standards are tightening in both the United States and Europe. Companies that invest early in audit trails, certified sourcing, and cross-market documentation are likely to defend margins better than operators that rely heavily on loosely controlled third-party networks. At the same time, smaller and mid-sized brands still have room to win in areas such as regenerative organic products, cleaner processing claims, ready meals, and children’s nutrition, where consumer trust can be built through product quality rather than sheer advertising scale. The structure of the organic packaged food market therefore remains open enough for focused challengers, even as larger players strengthen their sourcing and compliance moats.

Organic Packaged Food Industry Leaders

-

Danone S.A.

-

Nestlé S.A.

-

General Mills, Inc.

-

The Hain Celestial Group

-

Kellanova

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Amy's Kitchen announced expansion into more than 150 Costco warehouses across key US regions, bringing its Cheese Enchiladas and Bean & Cheese Burritos to club-channel scale at accessible price points. In 2025, the brand held the No. 1 dollar share in organic frozen pizza at 89.09% and in burritos at 73.8%.

- May 2026: Nature's Path Organic Foods launched Love Crunch Dubai Style Chocolate Granola and Love Crunch Dark Chocolate & Blueberry Cream, the first certified organic granola products inspired by the viral Dubai chocolate trend, at Target, Kroger, and its DTC channel.

- April 2026: SunOpta completed its acquisition by Refresco, consolidating organic beverage supply-chain capabilities and creating a larger platform for organic plant-based drinks, broths, and snacks across retail and foodservice channels in North America.

- March 2026: Hain Celestial completed the USD 115 million sale of its North American snacks business, including Garden Veggie Snacks, Terra chips, and Garden of Eatin', to Snackruptors, sharpening its portfolio around Celestial Seasonings teas, Earth's Best Organic baby foods, and The Greek Gods yogurt.

Global Organic Packaged Food Market Report Scope

Organic packaged food refers to food products that are processed, packaged, and certified as organic, produced without the use of synthetic pesticides, fertilizers, genetically modified organisms (GMOs), or artificial additives. The organic packaged food market is segmented by product type, packaging type, distribution channel, and geography. By product type, the market includes dairy and dairy alternatives, bakery and confectionery, snacks, meat, poultry and seafood, baby food, breakfast cereals, ready meals, condiments and sauces, and other product types. Based on packaging type, the market is categorized into PET/glass bottles, pouches, cans, and other packaging formats. By distribution channel, the market covers supermarkets/hypermarkets, convenience/grocery stores, online retail stores, and other distribution channels. By geography, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market size and forecasts provided for each region. For each segment, market sizing and forecasts have been conducted on a value basis (USD).

| Dairy and Dairy Alternatives |

| Bakery and Confectionery |

| Snacks |

| Meat, Poultry and Seafood |

| Baby Food |

| Breakfast Cereals |

| Ready Meals |

| Condiments and Sauces |

| Other Products Types |

| PET/Glass Bottles |

| Pouches |

| Cans |

| Others |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Dairy and Dairy Alternatives | |

| Bakery and Confectionery | ||

| Snacks | ||

| Meat, Poultry and Seafood | ||

| Baby Food | ||

| Breakfast Cereals | ||

| Ready Meals | ||

| Condiments and Sauces | ||

| Other Products Types | ||

| By Packaging Type | PET/Glass Bottles | |

| Pouches | ||

| Cans | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in organic packaged food through 2031?

Growth is being supported by health-focused food choices, stronger demand for clean-label convenience products, wider online access, and public support for organic supply chains. The category is projected to grow at a 6.39% CAGR through 2031.

Which product category leads global demand for organic packaged food?

Bakery and Confectionery led in 2025 with 30.87% share, supported by high purchase frequency across breakfast and snacking occasions.

Which product category is growing the fastest?

Ready Meals are projected to grow the fastest at a 7.08% CAGR through 2031, reflecting stronger demand for organic convenience and full-meal solutions.

Which sales channel is most important for organic packaged food brands?

Supermarkets and Hypermarkets remain the largest channel with 42.27% share in 2025, but Online Retail Stores are expanding faster at a 7.84% CAGR.

Which region offers the strongest growth outlook?

Asia-Pacific has the fastest growth outlook, with a projected 7.46% CAGR through 2031, supported by rising middle-class demand, food safety concerns, and digital grocery expansion.

Page last updated on: