Fried Potato Chips Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

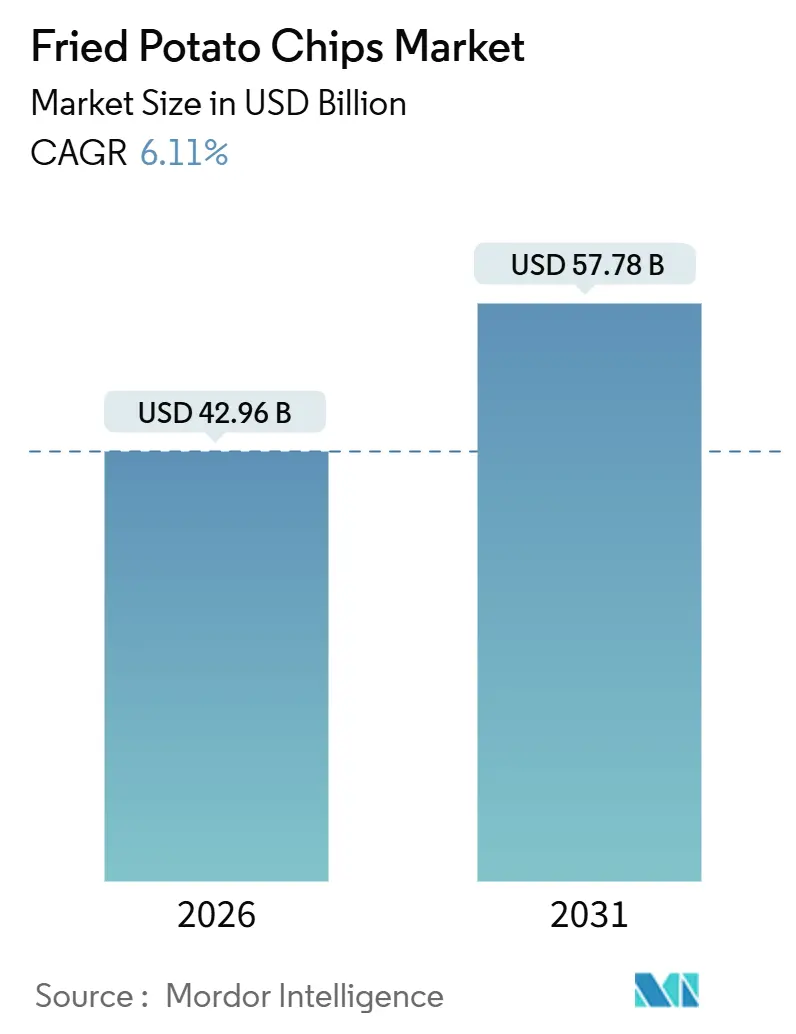

| Market Size (2026) | USD 42.96 Billion |

| Market Size (2031) | USD 57.78 Billion |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

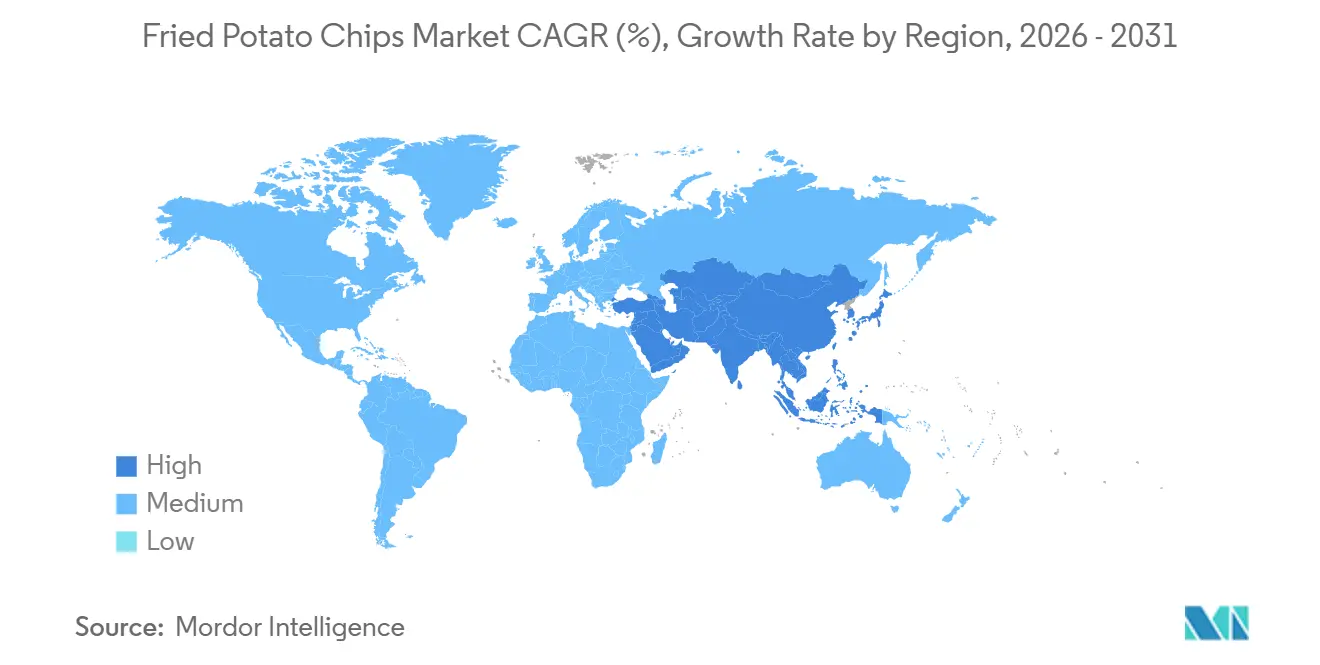

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fried Potato Chips Market Analysis by Mordor Intelligence

The global fried potato chips market reached USD 42.96 billion in 2026 and is expected to grow to USD 57.78 billion by 2031, at a CAGR of 6.11%. This growth trajectory highlights a market balancing two opposing forces: the age-old allure of convenient and indulgent snacking and the rising scrutiny from both regulators and consumers on sodium content, saturated fats, and deep-frying methods. The market's resilience can be attributed to manufacturers adeptly navigating between health-conscious reformulations and premium indulgences. This dual strategy effectively appeals to both wellness-oriented millennials and traditionalists. Mars' USD 35.9 billion acquisition of Kellanova in 2024 serves as a testament to the industry's dynamics, emphasizing that in a market where shelf presence and promotional efforts are paramount, scale and distribution prowess are key.

North America commanded 32.78% of global revenue in 2025, yet Asia-Pacific is poised to grow at 6.89% through 2031, driven by urbanization, rising disposable incomes, and localized flavor innovation that mirrors regional palates.

However, the market faces challenges, particularly from health regulations and the encroachment of alternative snacks. The European Union's Regulation 1169/2011 emphasizes front-of-pack nutrition labeling, and Regulation 1333/2008 limits food additives. These regulations necessitate reformulation cycles, which can risk altering taste profiles and alienating loyal consumers. Concurrently, alternative snacks like veggie chips, popcorn, and protein-based options are gaining traction, especially among Generation Z consumers who lean towards functional benefits and sustainability over traditional brand loyalty.

Key Report Takeaways

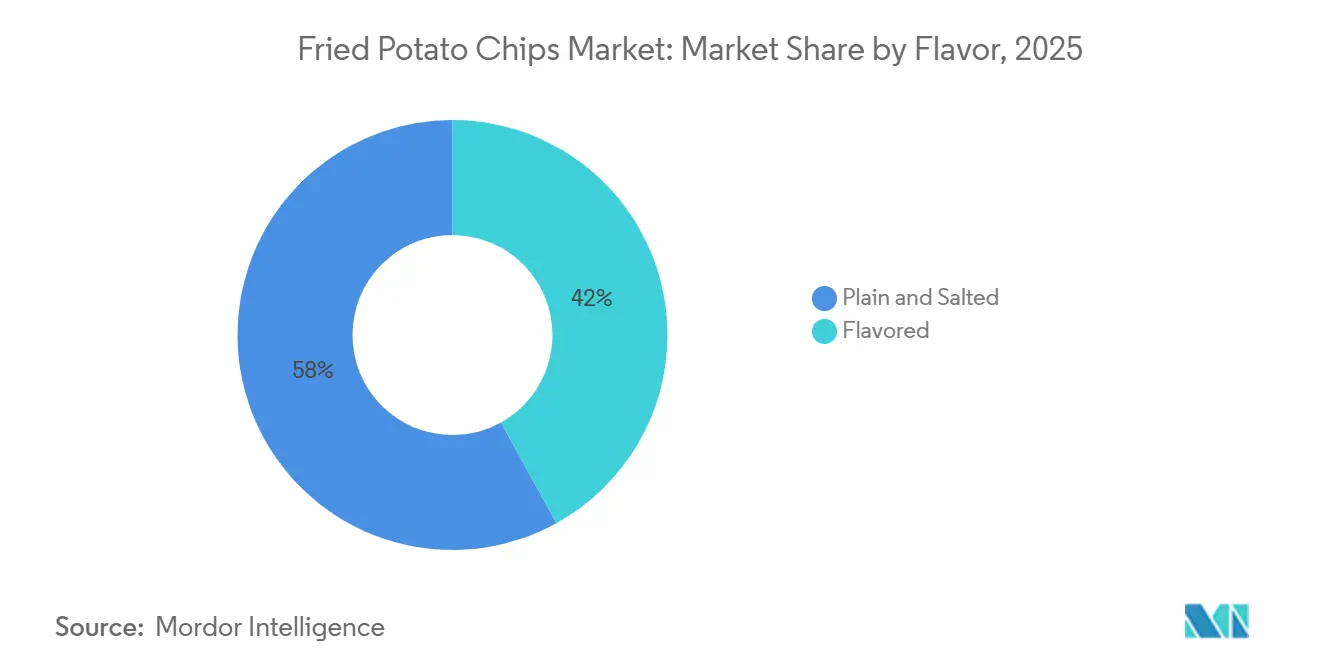

- By flavor, plain and salted chips captured 58.04% of the fried potato chips market size in 2025, while flavored variants are forecast to expand at a 6.48% CAGR through 2031.

- By packaging type, pouches and bags led with 77.81% of the fried potato chips market share in 2025, whereas rigid containers are projected to grow at a 7.32% CAGR to 2031.

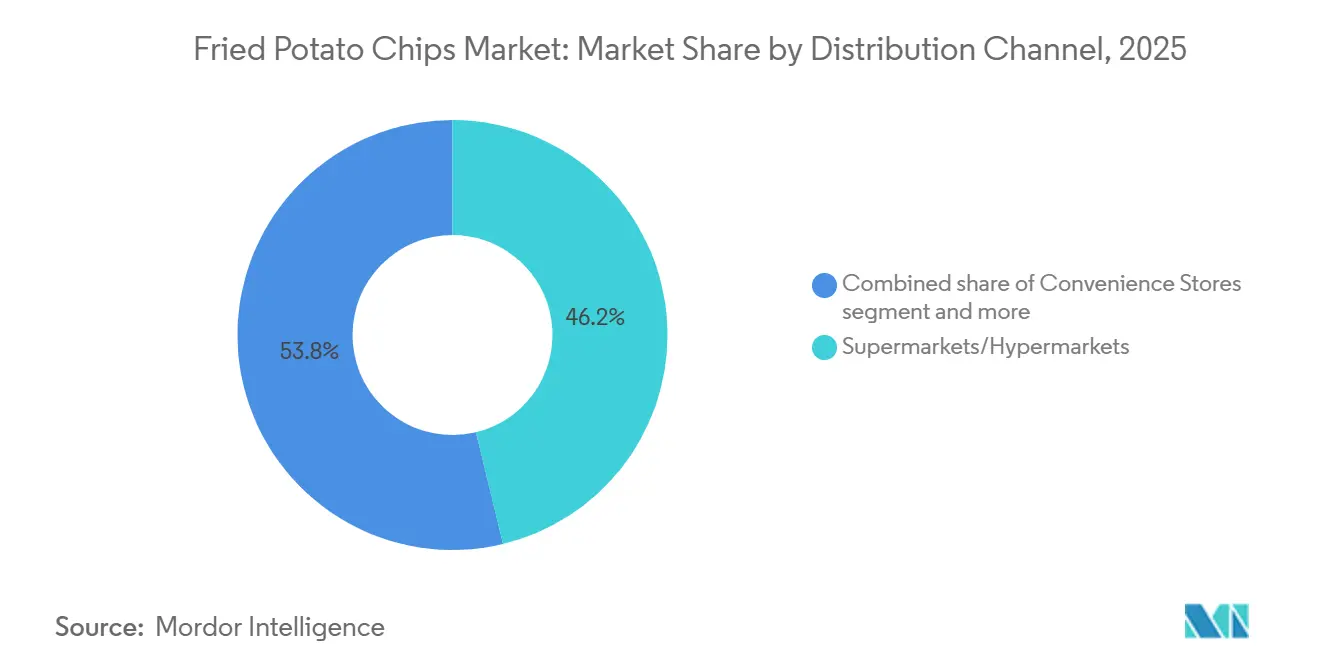

- By distribution channel, supermarkets and hypermarkets held 46.23% share of the fried potato chips market size in 2025; online retail is set to grow at a 7.14% CAGR through 2031.

- By geography, North America accounted for 32.78% of the fried potato chips market revenue in 2025, while Asia-Pacific is advancing at a 6.89% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fried Potato Chips Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising preference for convenient, ready-to-eat snacks | +1.2% | Global, with peak intensity in North America and Asia-Pacific urban centers | Medium term (2-4 years) |

| Strong snacking culture among younger consumers | +1.0% | Global, led by North America, Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Continuous flavor innovation tailored to local taste profiles | +0.9% | Asia-Pacific core, spillover to Middle East and Africa, Latin America | Medium term (2-4 years) |

| Strong brand building and aggressive marketing by global and regional players | +0.8% | Global, with concentrated spend in North America and Europe | Short term (≤ 2 years) |

| Growth of clean-label positioning, with simpler ingredient lists, non-GMO claims | +0.7% | North America and Europe, emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Expansion of healthier formulations such as reduced-fat, low-salt, baked or better-for-you fried chips | +0.6% | North America and Europe, selective adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising preference for convenient, ready-to-eat snacks

As urbanization accelerates and time becomes increasingly scarce, traditional meal structures are undergoing significant changes. Consumers are shifting toward portable and shelf-stable snacks that require no preparation, addressing the growing need for convenience. Potato chips have emerged as a preferred choice, with their individually wrapped portions fitting seamlessly into daily routines such as commutes, office desk drawers, and other on-the-go consumption occasions that traditional meals often fail to accommodate. India's organized snack market has been experiencing substantial growth, driven by the increasing prevalence of nuclear families and extended work hours, which have normalized snacking as a practical alternative to full meals. This transformation in snacking behavior is rooted more in necessity than in impulse, providing the category with greater resilience during economic downturns compared to discretionary indulgences. In response to these evolving consumer preferences, manufacturers are introducing resealable packaging formats and multi-serve packs that effectively combine convenience with portion control. Rigid canisters, in particular, are proving to be more efficient in meeting this dual requirement compared to traditional flexible pouches.

Strong snacking culture among younger consumers

Millennials and Generation Z snack more frequently than earlier generations, influenced by social media platforms, endorsements from influencers, and a shift away from traditional meal schedules. These younger demographics place a high value on diverse flavors, visually appealing products, and snacks that can be easily shared online. Potato chips effectively meet these preferences through limited-edition product launches, striking packaging designs, and aesthetics that resonate well on social media platforms like Instagram. At the same time, there is a growing demand for transparency among these consumers. Many shoppers have expressed concerns about food safety, while others are increasingly worried about the rising costs of food. This creates a challenging balance between offering premium products and catering to value-conscious buyers. Companies that address this challenge by providing a range of product options, such as affordable salted chips alongside high-quality, kettle-cooked alternatives, are successfully attracting consumers across different income levels. The changing perception of snacking, which is now viewed as a legitimate eating occasion rather than a guilty indulgence, is driving consistent growth in consumption volumes and contributing to the long-term expansion of the market.

Growth of clean-label positioning, with simpler ingredient lists, non-GMO claims

Driven by skepticism from millennials and Generation Z toward artificial additives and unclear supply chains, clean-label positioning has transitioned from a niche focus to mainstream acceptance. Brands are now reformulating their products, moving away from ingredients like monosodium glutamate, artificial colors, and hydrogenated oils. Instead, they are opting for natural seasonings, sea salt, and healthier oils such as high-oleic sunflower or avocado oil. This trend is especially evident in North America and Europe. In these regions, regulatory frameworks, such as the European Union's Regulation 1333/2008, not only restrict certain additives but also require clear labeling of allergens and preservatives[1]Source: European Union "REGULATION (EC) No 1333/2008 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL," europa.eu. Furthermore, verifications like the non-GMO Project and organic certifications have become essential for premium products. Brands such as Kettle Foods and Burts Chips are even centering their identities around ingredient transparency. However, a significant challenge remains: preserving taste and shelf life without synthetic preservatives. This technical challenge tends to benefit vertically integrated players with their own research and development capabilities. While clean-label products have successfully attracted health-conscious consumers, reflected in their growing market impact, the premium pricing needed to cover reformulation costs has hindered broader market penetration.

Expansion of healthier formulations such as reduced-fat, low-salt, baked or better-for-you fried chips

Healthier formulations are addressing the long-standing perception of potato chips as indulgent snacks lacking nutritional value. Baked chips, which avoid the deep-frying process, significantly reduce fat content. However, this often compromises the signature crunch and mouthfeel that consumers associate with the category. Reduced-sodium options align with voluntary targets established by the United States Food and Drug Administration. In 2024, the agency issued guidance encouraging manufacturers to reduce sodium levels by a notable percentage over the next decade. At the same time, air-frying and vacuum-frying technologies provide a balanced solution, preserving the desired texture while lowering fat absorption. Despite these advancements, the substantial capital investment required to upgrade production lines remains a significant hurdle for mid-sized manufacturers. However, cost-conscious consumers often resist paying a premium. As a result, success in this segment depends on gradual, incremental improvements rather than groundbreaking innovations, which limits the potential for immediate market share growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating health concerns around obesity, cardiovascular disease and high sodium intake | -0.8% | Global, with acute pressure in North America and Europe | Long term (≥ 4 years) |

| Regulatory pressure to cut salt, saturated fats, and artificial additives in savory snacks | -0.6% | Europe and North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| Intensifying competition from alternative snacks | -0.5% | Global, led by North America and urban Asia-Pacific | Short term (≤ 2 years) |

| Negative perception of deep-fried snacks | -0.4% | North America and Europe, selective impact in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating health concerns around obesity, cardiovascular disease and high sodium intake

In developed markets, where a significant portion of adults face obesity challenges, public health campaigns are increasingly associating fried snacks with chronic diseases, leading to shifts in consumption patterns. A standard serving of potato chips contains a considerable amount of sodium. When combined with other processed foods, this intake often pushes consumers closer to or beyond the daily sodium limit recommended by the World Health Organization[3]Source: World Health Organization "Guideline: sodium intake for adults and children,"who.int. Cardiovascular disease continues to be the leading cause of death worldwide, with dietary sodium recognized as a risk factor that can be modified. Policymakers and health advocates are addressing this issue through strategies such as taxation, warning labels, and enhanced public awareness initiatives. Manufacturers are actively working to counter this trend. They are introducing smaller, portion-controlled packaging, focusing on clear and transparent nutrition labeling, and partnering with dietitians. These efforts aim to reposition chips as occasional indulgences rather than everyday food items. While it is acknowledged that changing consumer behavior is a gradual process, the ongoing emphasis on health messaging is expected to steadily reduce per-capita consumption, particularly among aging populations.

Regulatory pressure to cut salt, saturated fats, and artificial additives in savory snacks

As regulatory frameworks become increasingly stringent across global markets, companies are facing significant challenges in reformulating their products. These reformulation efforts place considerable pressure on research and development budgets and risk alienating consumers who are sensitive to changes in taste. The European Union's Regulation 1169/2011 requires front-of-pack nutrition labeling, with some member states implementing traffic-light color coding to clearly identify products high in sodium and fat. This labeling approach can stigmatize such products at the point of purchase. Additionally, the European Food Safety Authority has issued opinions supporting sodium reduction targets, while the United States Food and Drug Administration's guidance for the year 2024 introduces voluntary benchmarks[2]Source: United States Food and Drug Administration "FDA Starts Next Phase of Sodium Reduction Efforts," fda.gov. If widely adopted, these benchmarks have the potential to reshape industry standards. The costs of compliance are not evenly distributed. Multinational corporations are better positioned to absorb reformulation expenses by spreading them across their global portfolios. In contrast, regional players often face significant financial strain, which can lead to reduced profit margins or even force them to exit the market. The impact of these challenges reflects the dual burden of reformulation costs and the potential loss of sales volume if changes in taste profiles fail to meet consumer expectations. However, the medium-term timeline provides manufacturers with an opportunity to adapt their strategies before regulatory enforcement becomes more rigorous.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flavor: Premiumization Drives Flavored Chip Acceleration

Flavored chips are anticipated to grow at a compound annual growth rate (CAGR) of 6.48% through 2031, surpassing the overall market growth. Manufacturers are addressing the challenge of commoditization by introducing diverse flavor profiles such as barbecue, sour cream and onion, cheese-based, spicy, and sweet-savory options. In 2025, plain and salted chips accounted for 58.04% of the market share, driven by their versatility as popular accompaniments to sandwiches and dips. However, this dominance is gradually declining as younger consumers increasingly prioritize unique flavors and visually appealing, Instagram-worthy packaging over traditional functionality. In North America, barbecue remains the most popular flavored sub-segment. In contrast, spicy variants dominate in India and Mexico, where cultural preferences for capsaicin-rich foods are deeply ingrained. Europe leads in cheese-based flavors, leveraging its strong dairy traditions, while Japan and South Korea are witnessing growing demand for sweet-savory blends like honey-butter and caramel-sea salt, reflecting the popularity of dessert-snack hybrids in these regions. Sour cream and onion occupy a middle ground, appealing to consumers seeking tangy flavors without heat, though its growth has plateaued as brands focus on introducing bolder and more distinctive profiles.

PepsiCo's global flavor development process, which involves testing thousands of concepts annually, underscores the significant research and development efforts required to sustain this segmentation strategy. The increasing preference for flavored chips aligns with a broader trend of premiumization, where consumers are willing to pay higher prices for enhanced sensory experiences that plain salted chips cannot provide. This dynamic is expected to persist as disposable incomes rise in emerging markets, enabling more consumers to trade up for premium products. The shift highlights the evolving consumer demand for innovation and differentiation in the snack food industry, emphasizing the importance of continuous flavor development to maintain market relevance and growth.

By Packaging Type: Rigid Containers Capture Premiumization and Freshness Demand

Rigid containers and canisters are experiencing remarkable growth, advancing at a CAGR of 7.32%, which is the fastest among all packaging formats. This growth is primarily driven by evolving consumer preferences, as individuals increasingly value features such as resealability, portion control, and extended freshness over the lower unit costs provided by flexible pouches. In 2025, pouches and bags dominated the market with a 77.81% share, largely due to their cost advantages, lighter weight for logistics, and compatibility with high-speed filling lines. However, these formats face limitations in multi-serve scenarios, as they often fail to maintain product crispness after opening, leading to dissatisfaction among consumers. Rigid containers, such as Pringles' iconic tube and Doritos' STAX format, effectively address this issue by incorporating airtight seals and stackable chip geometries that reduce breakage during transport. These containers are particularly appealing to urban, higher-income households, who perceive the benefits of reduced food waste and enhanced convenience as worth the additional cost. Multipack formats, which bundle single-serve pouches for use in lunchboxes and vending machines, provide a middle ground between bulk bags and rigid containers. These formats offer the advantage of portion control without the premium pricing associated with rigid containers.

Sustainability concerns are increasingly influencing packaging decisions across the industry. The 7.32% CAGR for rigid containers highlights a structural shift in the packaging industry, where packaging is no longer viewed as a mere commodity input but as a value-added feature. This shift favors brands with the scale to absorb higher material costs and the innovation pipelines to differentiate themselves through unique and functional packaging formats. As sustainability and consumer preferences continue to evolve, companies that can align their packaging strategies with these trends are likely to gain a competitive edge in the market.

By Distribution Channel: Online Retail Reshapes Convenience and Discovery

Online retail is expected to grow at a CAGR of 7.14% through 2031, fueled by the rise of quick-commerce platforms, subscription snack boxes, and the increasing adoption of e-groceries. Despite this growth, supermarkets and hypermarkets are projected to retain a significant 46.23% market share in 2025. This dominance is largely due to their ability to drive impulse purchases through strategies like end-cap displays and promotional pricing. India's quick commerce sector accounted for over two-thirds of all e-grocery orders. These platforms are transforming last-mile logistics and enabling brands to bypass traditional retail intermediaries. Convenience stores, which cater to on-the-go consumers and late-night shoppers, maintain a stable position in the market but face challenges from rising real estate costs and competition from vending machines and micro-markets.

Other distribution channels, including vending machines, gas stations, and direct-to-consumer models, address fragmented demand but lack the scale to significantly alter market dynamics. The divide between physical and digital shopping channels is less about replacing one another and more about meeting specific shopping occasions. For instance, consumers often purchase bulk packs at supermarkets for home use, single-serve pouches at convenience stores for immediate consumption, and variety packs online for exploration and gifting. Brands that effectively optimize their product assortments and pricing strategies across these channels are gaining a disproportionate share of the market. Examples include offering exclusive flavors online, promotional multipacks in hypermarkets, and premium single items in convenience stores. The projected 7.14% CAGR for online retail highlights the role of e-commerce as both a discovery platform and a subscription service. However, its overall market share is expected to remain limited due to the low unit value of the category and consumers' preference for tactile evaluation before making a purchase.

Geography Analysis

In 2025, North America emerged as the leading segment and held 32.78% of global revenue. This dominance was driven by the United States' potato chip market, with rising per-capita consumption. The market expansion is being propelled by premiumization. Products such as kettle-cooked, organic, and exotic-flavor variants command significant price premiums over mass-market offerings. Canada and Mexico also contribute to the region's growth, with Mexico's preference for spicy flavors creating opportunities for brands to localize heat profiles. However, the region faces challenges from health advocacy groups advocating for soda taxes to be extended to salty snacks, a regulatory risk that could pressure margins if implemented. In Europe, the market is shaped by stringent regulations under European Union (EU) Regulation 1169/2011, which governs sodium, additives, and labeling. This has led to continuous reformulation cycles.

Asia-Pacific is the fastest-growing segment, expanding at a CAGR of 6.89% through 2031. This growth is fueled by China's urbanization, India's increasing penetration of organized retail, Japan's trend toward premiumization, and Australia's adoption of multicultural flavors. In China, the market is divided between multinational brands dominating tier-one cities and local players thriving in tier-two and tier-three cities, where price sensitivity and regional flavor preferences give them an edge. Australia's multicultural population drives demand for globally inspired flavors, such as Thai sweet chili and Indian tandoori, positioning the country as a hub for innovation that can be scaled to other markets. The region's growth trajectory depends on continued urbanization, the development of cold-chain infrastructure, and regulatory stability.

Other regions, including South America and the Middle East and Africa, represent emerging frontiers. In South America, Brazil and Argentina lead consumption. Brazil's snack market benefits from urbanization and a growing middle class, although economic volatility and currency depreciation create challenges for importers. In the Middle East and Africa, Saudi Arabia, the United Arab Emirates (UAE), and South Africa anchor demand. Expatriate populations in the UAE and Saudi Arabia drive demand for globally recognized brands and Halal-certified products, creating opportunities for multinational companies willing to navigate complex regulatory environments.

Competitive Landscape

In the fried potato chips industry, while the top two players command significant shelf space, there is still considerable opportunity for regional competitors to thrive. PepsiCo, through its Frito-Lay division, and Kellanova, known for its Pringles brand, dominate the market by leveraging their extensive distribution networks, significant investments in research and development, and strong marketing capabilities.

The competitive landscape has intensified with Mars’ acquisition of Kellanova, which strategically aligns confectionery and salty snack portfolios under a single umbrella. At the same time, regional players such as ITC with its Bingo brand, Calbee, Intersnack, and Utz are successfully defending their market positions by offering culturally relevant flavors, sourcing potatoes locally, and maintaining agile innovation cycles to meet consumer demands. PepsiCo expanded its portfolio by acquiring Siete Foods, a grain-free snack specialist, for USD 1.2 billion in 2024, signaling a strategic move into the growing "better-for-you" snack segment.

Emerging disruptors and various direct-to-consumer startups are challenging established players by introducing plant-based snack options and utilizing social media platforms for product launches. Technology adoption is becoming a critical differentiator in the industry, with leaders employing artificial intelligence (AI) for flavor modeling and blockchain technology for traceability. These advancements not only accelerate time-to-market but also strengthen clean-label claims, which are increasingly important to consumers. Overall, the competition in the fried potato chips market strikes a balance between the economies of scale achieved by major players and the flexibility of regional specialists, ensuring a dynamic yet not overly fragmented industry landscape.

Fried Potato Chips Industry Leaders

-

Intersnack Group GmbH & Co. KG

-

PepsiCo, Inc.

-

Kellanova

-

Calbee Group

-

Utz Brands, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Utz, a prominent United States salty snack brand, teamed up with Alex’s Lemonade Stand Foundation, the nation's leading independent charity for childhood cancer, to unveil its newest creation: lemonade-flavored potato chips. The Utz Lemonade Potato Chips meld the zesty sweetness of lemonade with Utz's signature salty crunch, offering a bold and distinctive flavor.

- April 2025: Kettle Studio, renowned for its gourmet kettle-cooked artisanal chips, debuted its new Air-Fried Chips line. Responding to the rising demand for healthier snacks, Kettle Studio's Air-Fried Chips boast 50% less oil than traditional potato chips, yet maintain the brand's signature bold crunch and flavor.

- July 2024: Samyang Foods introduced three new potato chip flavors, namely Original Buldak, Four Cheese, and Habanero and Lime, targeting the Japanese snack market. These chips, under the globally acclaimed Buldak brand, seek to embody the savory and spicy essence of Buldak Bokkeummyeon.

Global Fried Potato Chips Market Report Scope

Fried potato chips are thin slices of potato that are deep‑fried in oil until crisp, seasoned (commonly with salt or flavorings), and packaged or served as a ready‑to‑eat snack. The fried potato chips market is segmented by flavor, distribution channel, and geography. By flavor, the market is segmented into plain and salted, and flavored. By packaging type, the market is segmented into Pouches/Bags, Rigid Containers/Canisters, and Others (Multipack). By distribution channel, the market is segmented into hypermarkets/supermarkets, convenience stores, online channels, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Plain and Salted | |

| Flavored | Barbecue |

| Sour Cream and Onion | |

| Cheese-based flavors | |

| Spicy | |

| Sweet and Savory blends | |

| Others |

| Pouches/Bags |

| Rigid Containers/Canisters |

| Others (Multipack) |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Flavor | Plain and Salted | |

| Flavored | Barbecue | |

| Sour Cream and Onion | ||

| Cheese-based flavors | ||

| Spicy | ||

| Sweet and Savory blends | ||

| Others | ||

| By Packaging Type | Pouches/Bags | |

| Rigid Containers/Canisters | ||

| Others (Multipack) | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and CAGR forecast for the fried potato chips market?

The fried potato chips market size stands at USD 42.96 billion in 2026 and is set to grow at a 6.11% compound annual growth rate to reach USD 57.78 billion by 2031.

Which flavor segment is expanding fastest?

Flavored chips are projected to grow at 6.48% annually through 2031, outpacing plain and salted variants.

Which region offers the highest growth potential?

Asia-Pacific leads with a 6.89% CAGR driven by urbanization, rising incomes, and localized flavor innovation.

How is online retail shaping sales channels?

Online retail, including quick-commerce platforms, is growing at 7.14% and supports flavor discovery and subscription models, though supermarkets retain the largest share.

What restrains market growth most sharply?

Escalating health concerns around obesity and sodium intake impose the biggest drag at -0.8% on the CAGR forecast.

Page last updated on: