Organic Bakery Products Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

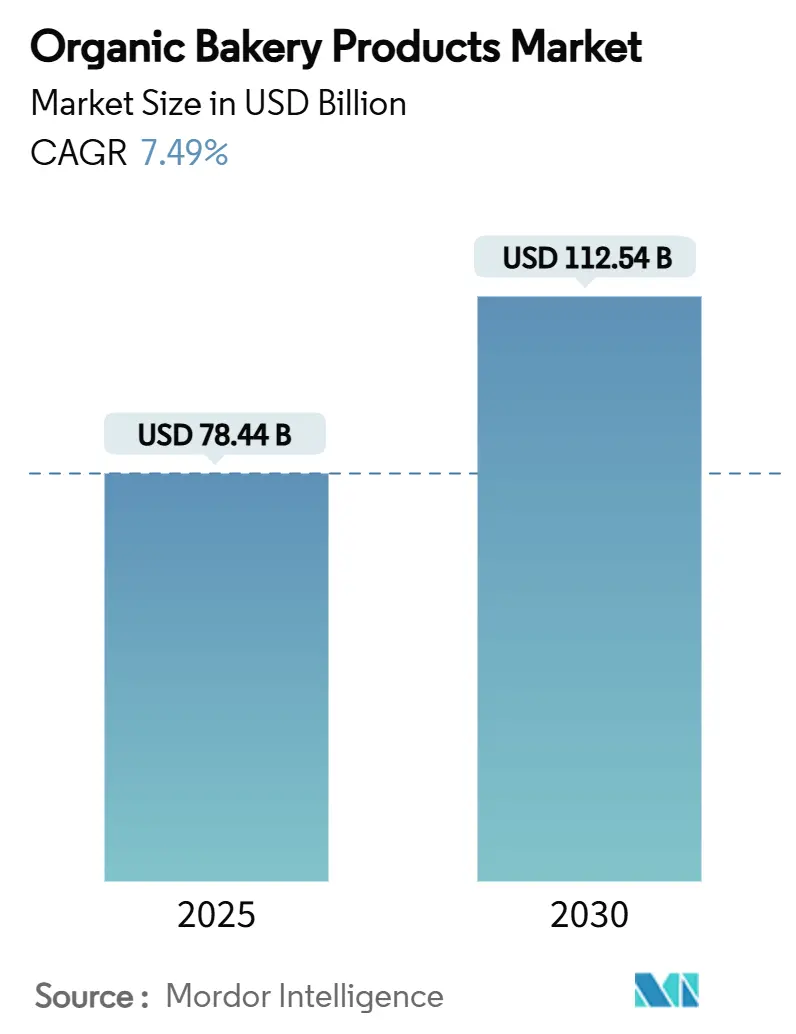

| Market Size (2025) | USD 78.44 Billion |

| Market Size (2030) | USD 112.54 Billion |

| Growth Rate (2025 - 2030) | 7.49% CAGR |

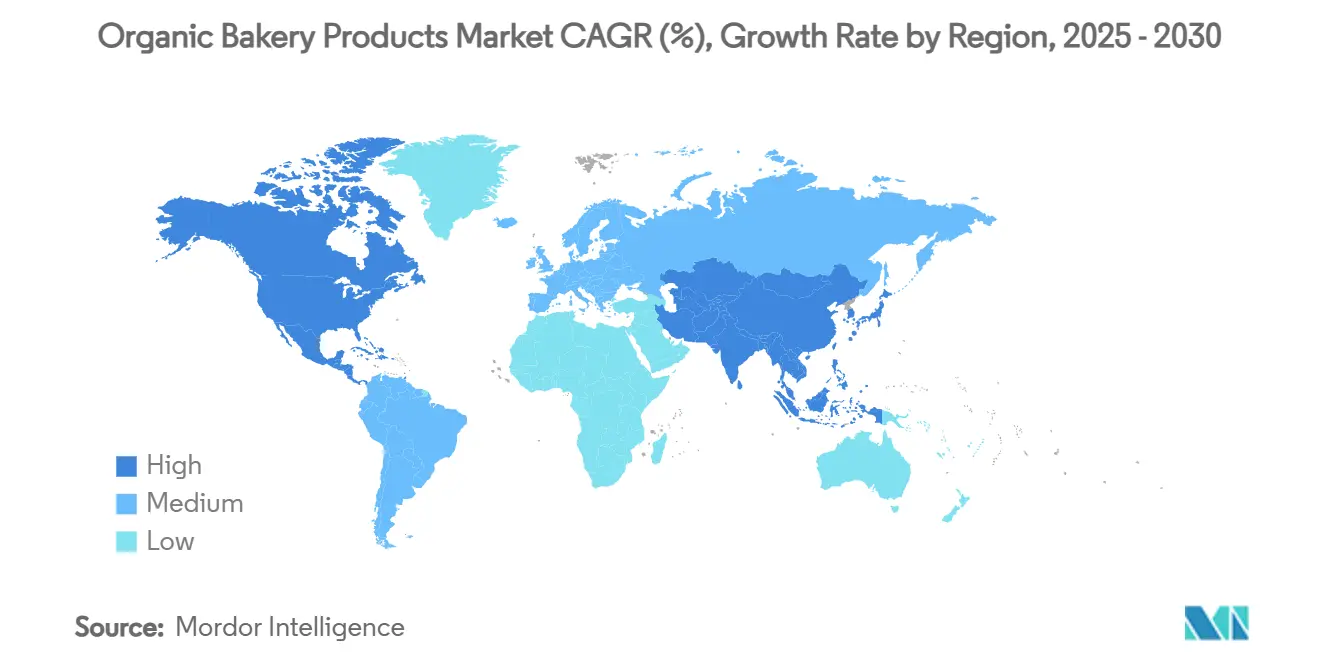

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

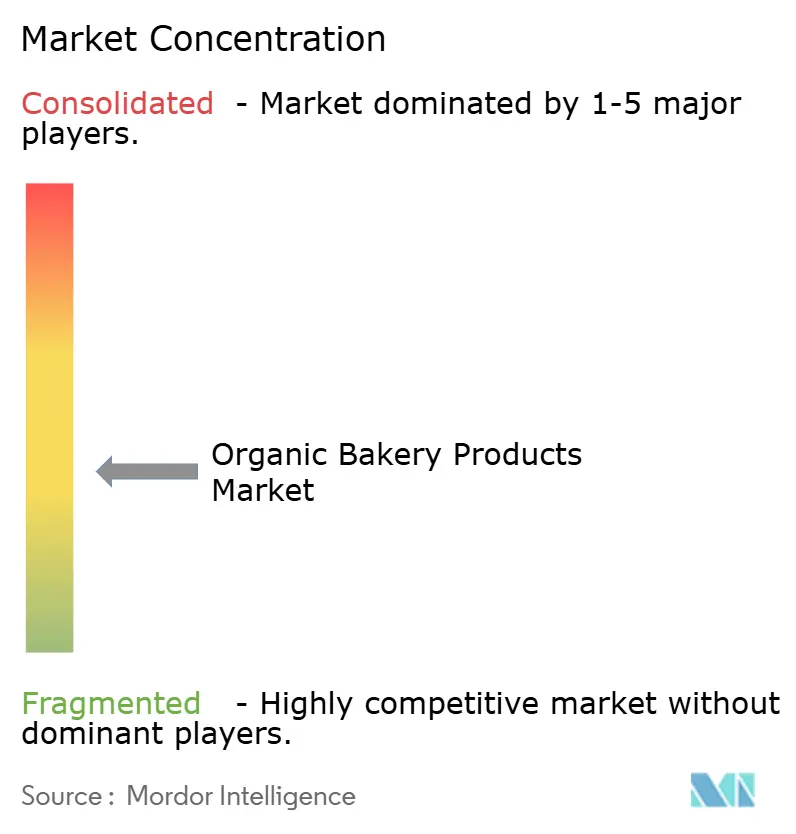

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Organic Bakery Products Market Analysis by Mordor Intelligence

The organic bakery products market demonstrates robust expansion potential, valued at a market size of USD 78.44 billion in 2025 and projected to reach USD 112.54 billion by 2030, representing a compound annual growth rate of 7.49% CAGR. This growth trajectory reflects fundamental shifts in consumer behavior toward health-conscious consumption patterns, supported by strengthened regulatory frameworks including the USDA's Strengthening Organic Enforcement Act of 2023 mandates enhanced certification requirements for all organic product handlers[1]Source: Federal Register, "Strengthening Organic Enforcement", federalregister.gov. The market's expansion is further amplified by the increase of online organic food sales, with continued acceleration during the pandemic period. Consumers are seeking bakery goods that are free from artificial additives, pesticides, and genetically modified ingredients, leading manufacturers to incorporate organic elements such as organic baking powder, gluten-free options, and natural preservatives. In addition, organic bakery products are seeing greater exposure in cafes, restaurants, and packaged food aisles, which amplifies consumer adoption. A notable restraint for the organic bakery market is the volatile and often higher raw material prices, especially for certified organic ingredients. Overall, the organic bakery products market is expected to grow by increasing consumer inclination toward healthful ingredients and clean label products.

Key Report Takeaways

- By product category, bread and rolls led with 34.54% of organic bakery products market share in 2024, whereas biscuits and cookies are projected to grow at an 8.18% CAGR through 2030.

- By form, fresh/shelf stable led with 91.34% of organic bakery products market share in 2024, whereas frozen are projected to grow at an 7.87% CAGR through 2030.

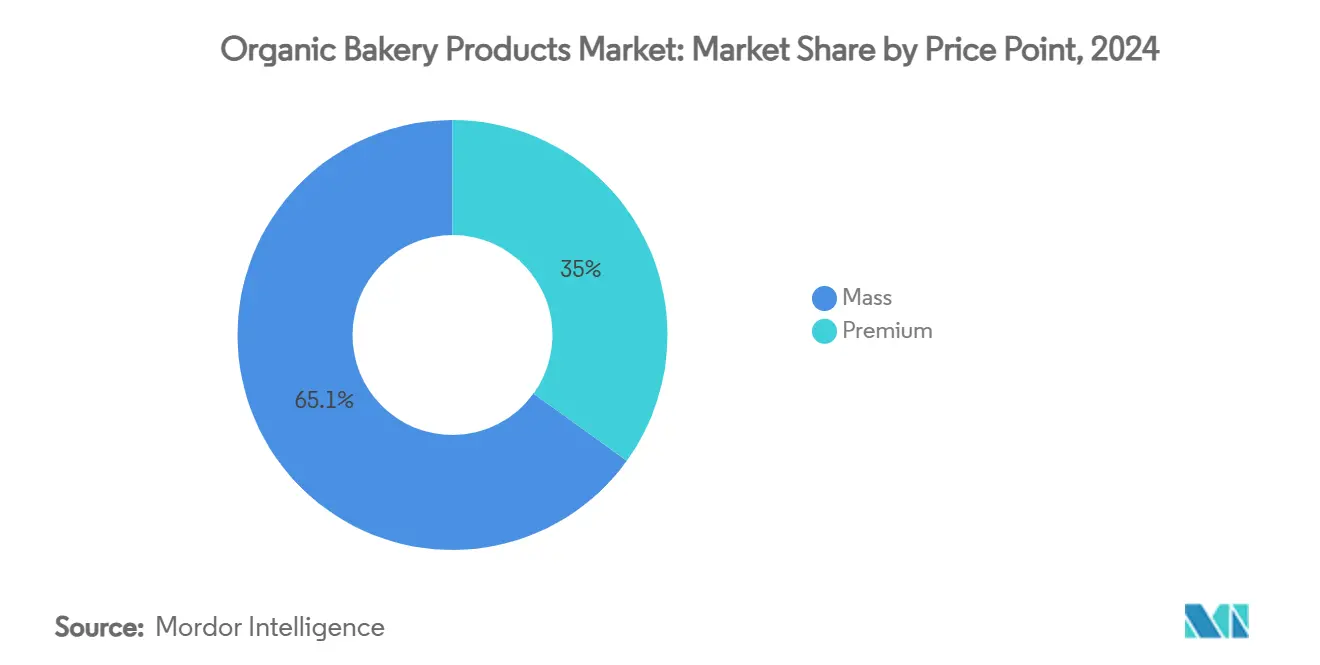

- By price point, mass led with 65.05% of organic bakery products market share in 2024, whereas premium are projected to grow at an 7.57% CAGR through 2030.

- By distribution channel, retail accounted for a 78.88% share of the organic bakery products market size in 2024, and Horeca/foodservice is forecast to expand at a 9.04% CAGR to 2030.

- By region, Asia-Pacific held 31.20% of the organic bakery products market share in 2024, and North America is expected to record the highest regional CAGR of 7.89% between 2025 and 2030.

Global Organic Bakery Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-conscious consumer trends | +1.8% | Global, with strongest impact in North America and Europe | Long term (≥ 4 years) |

| Demand for gluten-free, vegan, and allergen-friendly organic baked goods | +1.2% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rise of e-commerce | +0.9% | Global, with early gains in developed markets | Short term (≤ 2 years) |

| Government support and certification programs | +0.7% | Global, with regulatory leadership in United States and European Union | Long term (≥ 4 years) |

| Wider use of organic bakery items in cafes and restaurants | +1.1% | North America and Europe, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Innovation in organic ingredients | +0.8% | Global, with R&D concentration in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health-Conscious Consumer Trends

Consumer health consciousness has evolved beyond basic organic certification to encompass functional benefits, with high protein claims appearing in 14% of United States bread launches in 2024. The premiumization effect extends to pricing tolerance, with consumers demonstrating willingness to pay higher prices for products combining organic certification with functional attributes like sprouted grains and ancient grain formulations. Organic bakery goods, made with natural, non-GMO ingredients, are widely viewed as healthier options and are especially appealing to those concerned about issues like obesity, diabetes, and food allergies, as well as to consumers following specific diets such as gluten-free or vegan. According to the International Diabetes Federation, adult diabetes prevalence in 2024 exceeded 15% in Turkey, Mexico, and the United States, exceeded 13% in Portugal, China, and Spain, and exceeded 12% in Japan and South Korea [2]Source: International Diabetes Federation, "Prevalence of diabetes among adults in selected countries as of 2024", diabetesatlas.org. The demand for “clean label” and additive-free foods has brought leading product categories such as organic bread, cookies, and snack bars to the forefront, while also encouraging brands to introduce whole grains, reduced sugar, and high-fiber options, all aligned with modern health and wellness goals. Millennials and Gen Z consumers, in particular, are shaping this shift, driving innovation and growth in the sector

Rise of E-Commerce

The rise of e-commerce has become a major driver of demand in the organic bakery products market by making these goods significantly more accessible to consumers worldwide. Online grocery platforms and digital marketplaces allow shoppers to conveniently browse and purchase a wide variety of organic bakery items—from breads and pastries to gluten-free snacks—from the comfort of their homes. This ease of access is especially important for consumers in areas lacking specialty organic stores, effectively expanding the reach of organic bakeries beyond their local markets and enabling them to serve a much broader audience. E-commerce also empowers organic bakery brands to scale rapidly, tap into new customer segments, and leverage advanced logistics and subscription models to reach repeat buyers and build brand loyalty. Large platforms such as Amazon and Alibaba provide exposure to millions of customers, while industry leaders like Whole Foods and Thrive Market have seen strong growth in online sales of organic baked goods. Furthermore, the convenience and time-saving benefits of e-commerce resonate with busy, health-conscious consumers who increasingly seek transparent ingredient sourcing, clean-label claims, and allergen-friendly options without the need to visit multiple stores.

Government Support and Certification Programs

The USDA's Strengthening Organic Enforcement Act of 2023 introduces mandatory certification requirements for all organic product handlers, including brokers and importers, creating enhanced traceability and consumer confidence. This regulatory evolution addresses historical challenges in organic supply chain integrity, with new requirements for NOP Import Certificates and increased frequency of unannounced inspections. The certification framework's expansion creates barriers to entry that benefit established players while eliminating marginal operators who cannot meet enhanced compliance standards. Government support extends beyond regulation to market development, with the USDA announcing USD 24.8 million in funding for organic market development initiatives in 2024[3]Source: U.S. Department of Agriculture, "USDA Easing Producers’ Transition to Organic Production with New Programs and Partnerships", usda.gov. International harmonization efforts, particularly between United States and European Union organic standards, facilitate cross-border trade and expand market opportunities for compliant producers, creating scale advantages for companies with global distribution capabilities.

Wider Use of Organic Bakery Items in Cafes and Restaurants

As more foodservice establishments incorporate organic breads, pastries, cookies, and cakes into their menus, these products gain increased exposure to a diverse and trend-sensitive customer base. Diners who frequent cafes and restaurants often seek unique, healthier, and premium experiences—organic offerings meet this expectation by aligning with preferences for natural ingredients, clean labels, and foods free from artificial additives and preservatives. This direct visibility and sampling opportunity can lead consumers to develop a preference for organic bakery goods, which then translates into higher off-premise demand in retail and e-commerce channels as well. As restaurants and cafes respond by offering organic options, not only do they differentiate themselves within a crowded marketplace, but they also foster awareness of the health, environmental, and flavor advantages of organic products. This, in turn, contributes to greater overall market demand, as consumer expectations shift and organic bakery products become more mainstream. Thus, the integration of organic bakery items into foodservice establishments is acting as a powerful catalyst for market growth, making organic products more accessible, desirable, and normalized in everyday consumer choices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited shelf life | -1.4% | Global, with acute impact in e-commerce channels | Short term (≤ 2 years) |

| Inconsistent product quality | -0.8% | Global, with regulatory focus in North America and Europe | Medium term (2-4 years) |

| Risk of counterfeit or mislabelled products | -0.6% | Global, with enforcement concentration in developed markets | Long term (≥ 4 years) |

| Supply chain challenges | -1.1% | Global, with acute impact in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Shelf Life

Organic bakery products face inherent shelf life limitations due to the absence of synthetic preservatives, with industry studies indicating up to 30% of bakery products may be lost due to supply chain inefficiencies. Without these chemical stabilizers, organic breads, pastries, and sweets are more vulnerable to physical, chemical, and especially microbiological spoilage—such as mold, bacteria, and yeast—which can occur rapidly, particularly in products with higher moisture content. As a result, organic bakery items tend to have a shorter window for safe consumption and acceptable quality, leading to higher rates of product waste and more frequent restocking needs. Packaging innovations, including nitrogen-filled environments and natural preservative alternatives like vegetable glycerin and natamycin, offer partial solutions but require significant investment in specialized equipment and formulation expertise. The shelf life challenge creates competitive disadvantages for smaller organic producers who lack the scale to invest in advanced packaging technologies, contributing to market consolidation trends. Consequently, the short shelf life of organic options creates meaningful barriers for manufacturers and sellers, limiting broader adoption and slowing the expansion of the organic bakery market despite strong demand.

Supply Chain Challenges

Supply chain challenges significantly amplify cost pressures in the organic bakery products market, restricting its growth on multiple fronts. One of the central issues is the higher cost and limited availability of organic ingredients. Organic production typically yields less than conventional farming and requires strict adherence to certifications, making raw materials like organic wheat, flour, and sugars both scarce and expensive. This scarcity pushes up procurement costs for bakers, who already face premium pricing structures and intensified competition for quality inputs. When supply disruptions occur—due to factors like poor harvests, transport constraints, or global commodity price volatility—ingredient costs can surge unpredictably, further squeezing profit margins. These elevated ingredient costs are compounded by the complexity and fragility of the organic supply chain. Many millers, distributors, and bakers struggle with inconsistent supply, variable product quality, and a lack of reliable long-term supplier relationships. Any breakdown—whether from delayed deliveries, poor communication, or sudden recipe tweaks—impacts bakeries’ ability to produce, stock, and price finished goods efficiently. Such instability often forces bakeries to pass increased costs onto consumers, risking reduced demand as price-sensitive buyers shift to cheaper conventional alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bread and Rolls Dominance Faces Snacking Disruption

Bread and rolls command 34.54% market share in 2024, reflecting their foundational role in organic bakery consumption patterns, while biscuits and cookies emerge as the fastest-growing segment at 8.18% CAGR (2025-2030). This growth differential highlights the premiumization trend in snacking categories, where consumers demonstrate higher willingness to pay for organic certification in discretionary products compared to staple items. Cakes and pastries maintain steady performance in the premium occasion segment, benefiting from artisanal positioning and clean-label trends that align with organic values. Morning goods capture growing breakfast-on-the-go consumption, particularly in urban markets where convenience intersects with health consciousness.

The segment dynamics reflect broader consumer behavior shifts toward snacking over traditional meal structures, with biscuits and cookies positioned to capitalize on portion control and indulgence trends. Innovation in ancient grains and alternative flours creates differentiation opportunities across all product types, with companies like Trader Joe's launching Organic Super Bread featuring organic pumpkin, flax, and sunflower seeds to appeal to health-conscious consumers in January 2025. Other product types, including specialty items and seasonal offerings, provide niche opportunities for premium positioning and limited-edition strategies that command higher margins while building brand loyalty.

By Form: Fresh Products Maintain Dominance Despite Frozen Innovation

Fresh and shelf-stable products dominate with 91.34% market share in 2024, reflecting consumer preferences for immediate consumption and perceived quality advantages, while frozen organic bakery products demonstrate accelerated growth at 7.87% CAGR (2025-2030). This growth trajectory indicates evolving consumer acceptance of frozen organic products, particularly as packaging and preservation technologies improve product quality and extend shelf life without compromising organic integrity. The frozen segment benefits from convenience trends and e-commerce expansion, where temperature-controlled distribution enables broader geographic reach for organic bakery brands.

Frozen product innovation focuses on maintaining texture and flavor integrity, with companies like Lancaster Colony developing patent-pending formulations for gluten-free frozen bread that enhance consumer experience in August 2024. The segment evolution reflects supply chain optimization strategies, where frozen formats enable production efficiency and inventory management while reducing food waste throughout the distribution network. Fresh products continue to benefit from artisanal positioning and premium pricing, particularly in specialty retail channels where consumers associate freshness with quality and authenticity.

By Price Point: Premium Segment Accelerates Despite Mass Market Scale

Mass market products command 65.05% market share in 2024, demonstrating organic bakery products' mainstream adoption beyond traditional premium positioning, while premium products achieve faster growth at 7.57% CAGR (2025-2030). This premium acceleration reflects consumer willingness to pay higher prices for enhanced organic attributes, including ancient grains, sprouted formulations, and artisanal production methods. The premium segment benefits from brand differentiation strategies that emphasize unique ingredients, sustainable sourcing, and functional benefits beyond basic organic certification.

Premium positioning creates sustainable competitive advantages through brand loyalty and reduced price sensitivity. Mass market expansion reflects organic certification's democratization, where scale economies enable broader accessibility while maintaining certification integrity. The price point dynamics indicate market maturation, where organic attributes become table stakes rather than premium differentiators, creating opportunities for value-engineered products that maintain organic certification while achieving competitive pricing.

By Distribution Channel: Retail Dominance Challenged by Foodservice Growth

Retail channels maintain 78.88% market share in 2024, encompassing supermarkets, specialty stores, and online platforms, while foodservice demonstrates superior growth velocity at 9.04% CAGR (2025-2030). This foodservice acceleration reflects institutional adoption in fast-casual restaurants, university campuses, and healthcare facilities where younger demographics' sustainability preferences drive menu innovation. Within retail, supermarkets and hypermarkets dominate, while specialty stores command premium pricing for curated organic selections.

Online retail experiences rapid expansion, benefiting from pandemic-driven behavioral shifts and younger consumers' digital purchasing preferences. Convenience and grocery stores provide accessibility for impulse purchases and routine replenishment, while specialty stores maintain importance for discovery and education about organic benefits. The distribution evolution favors omnichannel strategies that integrate online and offline touchpoints, creating competitive advantages for companies with robust digital capabilities and flexible fulfillment networks.

Geography Analysis

Asia-Pacific's market leadership at 31.20% share in 2024 reflects the region's demographic advantages and economic development trajectory, with China's organic market reaching new heights, supported by major food companies, promoting organic products to enhance consumer awareness. The region benefits from expanding middle-class populations with increasing disposable incomes and health consciousness, creating sustainable demand for premium organic bakery products. India and Southeast Asia emerge as key growth drivers, with the OECD-FAO Agricultural Outlook highlighting their expected influence in global food consumption patterns. Japan's mature organic market provides premium positioning opportunities, while emerging markets like Indonesia and Thailand offer volume growth potential as organic awareness develops. The region's growth trajectory benefits from government support for organic agriculture and increasing retail infrastructure that facilitates organic product distribution.

North America demonstrates the fastest regional growth at 7.89% CAGR (2025-2030), driven by institutional adoption in foodservice settings, e-commerce expansion, and regulatory support through USDA organic market development initiatives. The region's organic food market, with in-store bakery and rising fresh bread sales, reflects sustained consumer demand despite inflationary pressures. United States leads regional growth through premiumization trends and brand innovation, with companies like Flowers Foods expanding organic portfolios through strategic acquisitions including the USD 795 million Simple Mills purchase in February 2025. Canada and Mexico contribute through cross-border trade facilitation and expanding retail presence, while the region benefits from established organic certification infrastructure and consumer education programs that support market development.

Europe maintains significant market presence through established organic infrastructure and regulatory frameworks, with Germany's organic market, experiencing 5.7% growth in 2024 despite economic challenges. The region's market dynamics reflect mature consumer awareness and sophisticated distribution networks, and indicates democratization trends that expand organic accessibility. United Kingdom, France, Italy, and Spain contribute through diverse consumption patterns and premium positioning strategies, while Nordic countries like Sweden demonstrate high per-capita organic consumption rates. European bakers increasingly expand into United States markets, recognizing growth opportunities and market potential. The region benefits from harmonized organic standards that facilitate cross-border trade and create scale advantages for multinational organic bakery companies operating across European markets.

Competitive Landscape

The organic bakery products market exhibits moderate fragmentation, creating strategic consolidation opportunities as evidenced by recent high-value acquisitions. Major players including Grupo Bimbo SAB de CV, Flowers Foods, General Mills Inc., The Hain Celestial Group Inc., and Alvarado Street Bakery compete through portfolio diversification strategies. The competitive intensity reflects product quality differentiation, brand loyalty cultivation, and promotional effectiveness, with companies like Bimbo Bakeries experiencing operational pressures from consumer shifts toward private label and value channels, resulting in 46% operating income decline in Q2 2024.

Strategic patterns emphasize health-focused product development, geographic expansion, and technology adoption to achieve competitive advantages, with companies investing in ancient grain formulations, gluten-free innovations, and sustainable packaging solutions to differentiate their organic offerings. The FDA's enforcement actions against major players like Bimbo Bakeries for allergen mislabeling violations highlight regulatory compliance as a competitive differentiator, creating advantages for companies with robust quality management systems.

Opportunities exist in foodservice channel penetration, where institutional buyers demonstrate willingness to pay premium pricing for organic certification, and in emerging markets where organic awareness continues developing. Technology adoption focuses on supply chain optimization, quality control enhancement, and e-commerce capabilities, with companies leveraging digital platforms to reach younger demographics while maintaining product integrity through advanced packaging and preservation technologies.

Organic Bakery Products Industry Leaders

-

Grupo Bimbo SAB de CV

-

General Mills Inc.

-

The Hain Celestial Group Inc.

-

Alvarado Street Bakery

-

Flowers Foods Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Dave's Killer Bread expanded its product lineup with the national launch of organic Sandwich Rolls in two fan-favorite varieties: 21 Whole Grains and Seeds and Sandwich Rolls Done Right. Dave's was on a mission to redefine this classic by providing organic, high-quality ingredients that elevated every bite and inspired the best part of sandwich-making: endless customization and versatility.

- September 2024: Organic food supplier Biona expanded its bakery offering with the launch of Organic Super Seed Bread. The sliced loaf was high in protein and contained oat kernels, sunflower seeds, flax seeds, and pumpkin seeds. It was made without artificial additives, preservatives, wheat, yeast, sugar, or chemical pesticides.

- July 2024: Essential, a Certified USDA Organic, bake-at-home, artisan bread that restored the ancient way of bread making with a 140-year-old sourdough starter, became available nationwide. Made with wholesome, minimal ingredients, Essential artisan loaves had a crisp, chewy, golden crust and a light, full-bodied, fragrant crumb.

Global Organic Bakery Products Market Report Scope

| Bread and Rolls |

| Biscuits and Cookies |

| Cakes and Pastries |

| Morning Goods |

| Other Product Types |

| Fresh/Shelf Stable |

| Frozen |

| Mass |

| Premium |

| Horeca/Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Specialty Stores | |

| Online Retail | |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

| By Product Type | Bread and Rolls | |

| Biscuits and Cookies | ||

| Cakes and Pastries | ||

| Morning Goods | ||

| Other Product Types | ||

| By Form | Fresh/Shelf Stable | |

| Frozen | ||

| By Price Point | Mass | |

| Premium | ||

| By Distribution Channel | Horeca/Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Specialty Stores | ||

| Online Retail | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the organic bakery products market?

The organic bakery products market size is USD 78.44 billion in 2025.

How fast is the organic bakery products market growing?

The market is projected to grow at a 7.49% CAGR, reaching USD 112.54 billion by 2030.

Which region leads the organic bakery products market?

Asia-Pacific holds the largest regional share at 31.20% in 2024.

Which product segment is expanding the quickest?

Biscuits and cookies are forecast to post the fastest growth at an 8.18% CAGR through 2030.

Page last updated on: