U.S. Potato Chips Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

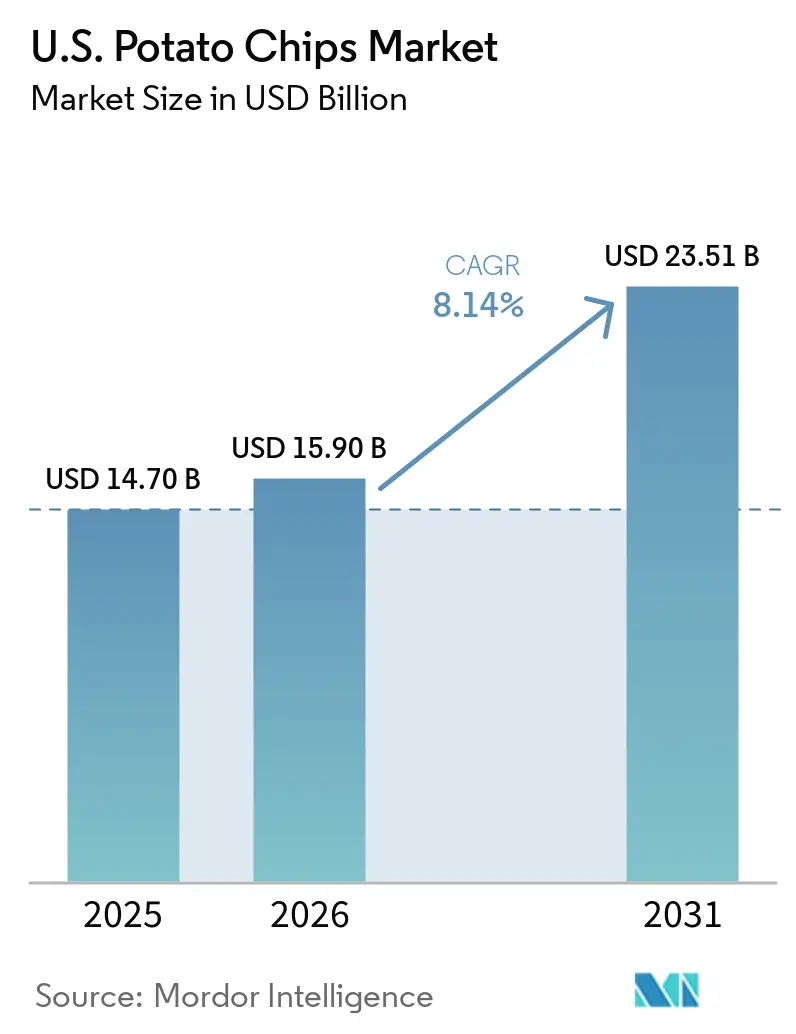

| Base Year Market Size (2025) | USD 14.70 Billion |

| Market Size (2026) | USD 15.90 Billion |

| Market Size (2031) | USD 23.51 Billion |

| Growth Rate (2026 - 2031) | 8.14% CAGR |

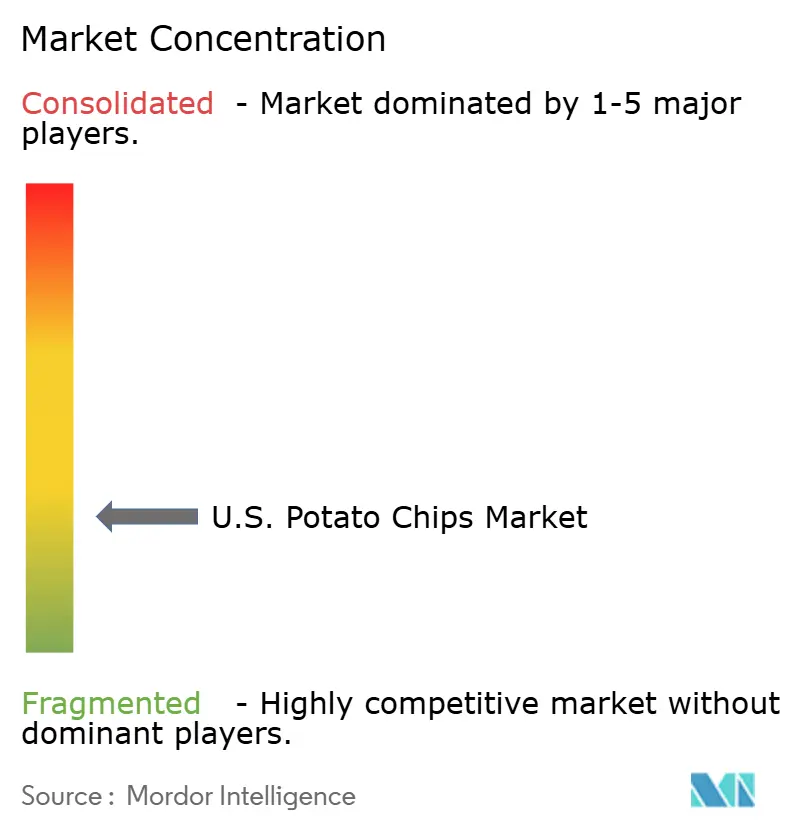

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Potato Chips Market Analysis by Mordor Intelligence

In 2025, the US potato chips market was valued at USD 14.70 billion. It is projected to grow to USD 15.90 billion in 2026 and reach USD 23.51 billion by 2031, with a CAGR of 8.1% during the forecast period (2026-2031). The category remains a key player in the nation's snack market, driven by consistent household demand as both an impulse buy and a grocery staple. Manufacturers are focusing on cleaner labels, diverse flavors, and competitive pricing, while premium and health-focused brands are entering national retail channels previously hard to access. According to the data from the USDA, in 2024, potato chips accounted for 18% of the US's domestic potato availability on a fresh-weight basis, highlighting their strong connection to US agriculture. Fluctuations in chip demand significantly impact growers and processors. Companies without strong contracts, scale, or pricing power face higher risks due to consumer price sensitivity and limited raw potato supplies.

Key Report Takeaways

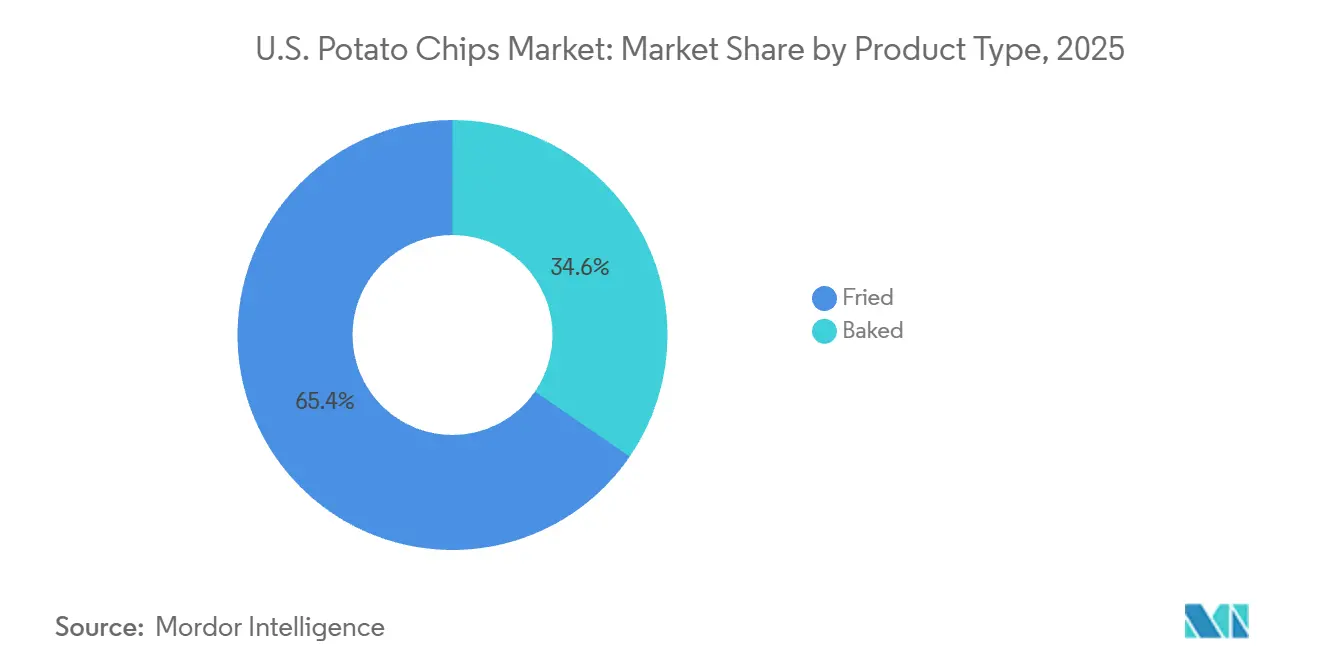

- By product type, fried potato chips held 65.43% share in 2025, while baked potato chips are forecast to grow at an 8.95% CAGR through 2031.

- By flavor, plain or salted chips accounted for 56.87% share in 2025, while flavored chips are projected to expand at a 9.03% CAGR through 2031.

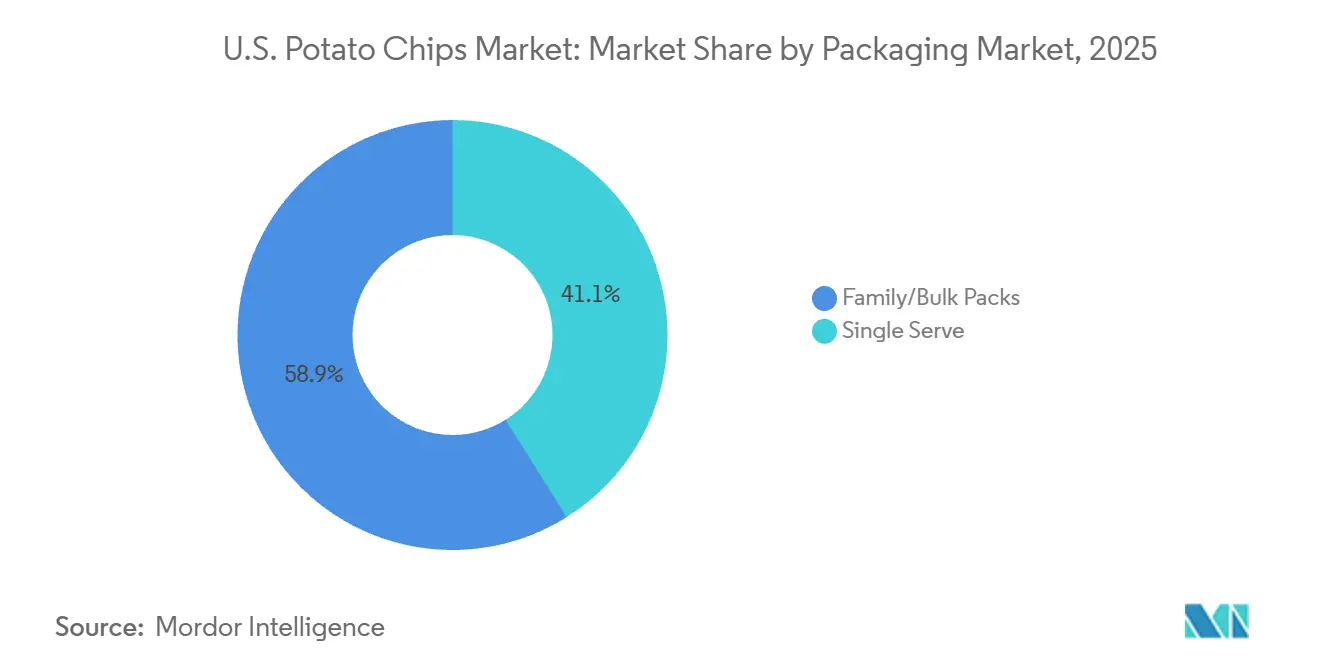

- By packaging type, family or bulk packs led with 58.92% share in 2025, while single-serve packs are expected to grow at a 9.65% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets held 60.32% share in 2025, while online retail stores recorded the highest projected CAGR at 10.25% through 2031.

- By geography, the South captured 33.29% share in 2025, while the Northeast is forecast to advance at a 10.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Potato Chips Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-conscious product innovation | +1.2% | National, early adoption in West and Northeast | Medium term (2-4 years) |

| Snacking convenience and lifestyle trends | +1.8% | National, highest intensity in Northeast and West urban corridors | Short term (≤ 2 years) |

| Plant-based and clean-label demand | +0.9% | West Coast and Northeast, expanding into Midwest and South | Medium term (2-4 years) |

| Aggressive marketing and branding by key players | +0.7% | National | Short term (≤ 2 years) |

| Flavor and texture experiential snacking | +1.1% | National, strongest commercial pull in South and Northeast | Short term (≤ 2 years) |

| Retail packaging and distribution innovations | +0.8% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health-Conscious Product Innovation

In the US potato chips market, mainstream brands are elevating their standards for oils, additives, and label claims. PepsiCo announced its commitment to eliminate artificial flavors and colors from its core Lay’s products in the US by the close of 2025. Additionally, the company is enhancing Lay’s Baked with olive oil and updating Lay’s Kettle Cooked Reduced Fat to feature avocado oil. According to Potatoes USA, from July 2024 to March 2025, the retail sales volume of chips saw a 2.6% uptick, even as retail prices dipped by 0.96% per pound. This trend indicates a robust demand that isn't reliant on inflated pricing. Such behavior suggests that consumers are increasingly gravitating towards cleaner, premium products in their chip purchases, viewing them as standard rather than niche. As a result, the US potato chips market has established a higher cost baseline. The shift towards premium oils and cleaner ingredient lists demands heftier budgets for R&D, procurement, and compliance, a challenge for smaller producers to match.

Snacking Convenience and Lifestyle Trends

The US potato chips market is thriving as snacking outside formal meals gains popularity. Conagra Brands projects a 39% rise in away-from-home snacking occasions per person by 2027 compared to pre-pandemic levels, with chips remaining a top portable snack choice. In 2025, NACS reported the 23rd consecutive year of growth in US convenience store in-store sales, with salty snacks among the top-performing categories for sales and profits. Additionally, 95.2% of convenience store customers consumed their salty snacks on the same day, highlighting the rapid shelf-to-use transition. This rapid consumption supports the market, as repeat purchases rely more on daily routines, portability, and availability in convenient pack sizes.

Plant-Based and Clean-Label Demand

Major retail channels in the US potato chips market are increasingly welcoming clean-label brands. Jackson’s, an avocado oil chip brand, made significant strides in 2026, securing placements at prominent retailers like Costco, Walmart, Target, Whole Foods, Sprouts, Kroger, CVS, 7-Eleven, and even Amazon. This shift underscores the brand's leap from specialty retail to mainstream and convenience outlets. In Q1 2025, Utz highlighted in its earnings that Boulder Canyon led as the top potato chip brand in the US's natural channel for the year-to-date. Such developments indicate that a focus on cleaner ingredients and premium oils is translating into tangible sales volumes, moving beyond mere shelf distinction. While the US potato chips market is becoming more accommodating to challenger brands, achieving national scale still leans in favor of those with robust supply chains and retail strategies.

Flavor and Texture Experiential Snacking

In the US potato chips market, companies are using limited editions and new flavors as strategic tools to drive sales rather than as short-term marketing tactics. Utz, in its Q2 2025 filing, reported that Circana identified dill pickle as the fastest-growing flavor in the US potato chip category. To tap into this trend, Utz introduced a 15-ounce Fried Dill Pickle product exclusively for club members. NACS recorded 435 new candy and salty snack items launched in the convenience channel in 2025, showcasing the rapid innovation that keeps the category competitive. Kellanova leveraged AI and clean room technology to identify three high-value audience segments for Pringles, boosting first-party data capture by 30%. This mix of flavor innovation and advanced audience targeting strengthens the US potato chips market by enabling more precise and effective product launches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health awareness and shift toward low-fat alternatives | -0.8% | National, strongest in West and Northeast | Long term (≥ 4 years) |

| Regulatory scrutiny on nutrition labeling and acrylamide | -0.6% | National, compliance influence across all manufacturers | Medium term (2-4 years) |

| Labor shortages in potato farming and processing | -0.4% | Red River Valley, Idaho, Pacific Northwest | Short term (≤ 2 years) |

| Volatility in raw material prices | -0.5% | National, upstream concentration in Idaho and Pacific Northwest | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health Awareness and the Shift Toward Low-Fat Alternatives

Consumers in the U.S. potato chips market are increasingly leaning towards lower-fat and lighter snack options. According to the USDA, shipments of chipping potatoes from January to mid-July 2025 were down 15% from the previous year and 11% from the same period in 2023. This decline indicates that the growth in retail value is more a result of product mix and pricing strategies rather than a significant uptick in the volume of traditional fried chips[1]Source: U.S. Department of Agriculture Economic Research Service, “Vegetables and Pulses Outlook, July 2025,” esmis.nal.usda.gov . To maintain their volume in standard fried formats, producers may need to consider either reducing prices or offering more credible, health-oriented products. While there's still potential for growth in the U.S. potato chips market, the trend is clearly moving towards healthier-looking and more justifiable repeat-purchase formats.

Regulatory Scrutiny on Nutrition Labeling and Acrylamide

Compliance with regulations on acrylamide, labeling, and ingredient reviews is increasingly burdensome for the U.S. potato chips market. The FDA has issued guidance on acrylamide, urging producers to monitor reducing sugars, control frying temperatures, and employ blanching when necessary to mitigate risks. Meanwhile, the European Union has established a reference level of 750 µg/kg for potato chips and snacks. This benchmark is particularly significant for U.S. manufacturers with export ambitions and is closely monitored by domestic operators[2]Source: European Commission, “Regulation (EU) 2017/2158 Establishing Mitigation Measures and Benchmark Levels for the Reduction of Acrylamide in Food,” EUR-Lex, eur-lex.europa.eu. Additionally, the FDA's 2025 actions concerning color additives and food labeling accelerated reformulation efforts across various packaged food lines, including chips. These regulatory costs disproportionately impact regional and mid-tier firms, making it increasingly challenging for them to navigate the U.S. potato chips market without specialized regulatory, technical, and procurement expertise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fried Commands Volume Baseline; Baked Accelerates on Health Tailwinds

In 2025, fried potato chips accounted for 65.43% of the U.S. potato chips market, maintaining their position as the category leader by volume. USDA NASS reported that in 2024, potatoes used for chips and shoestrings totaled 55.8 million cwt, a 3% decrease from 57.8 million cwt in 2023. Despite this decline, fried chips remain a key processing use for potatoes in the U.S. NACS data showed that potato chips made up 32.9% of the salty snack segment in convenience stores, outperforming other salty snacks and tortilla or corn chips. This dominance is supported by large-scale frying infrastructure, consistent production capacity, and established supply agreements, which continue to favor fried chips in the U.S. potato chips market.

The U.S. market for baked potato chips is projected to grow at a robust 8.95% CAGR from 2026 to 2031, making baked chips the fastest-growing segment. USDA and HHS dietary guidelines recommend limiting saturated fat intake to less than 10% of daily calories, driving demand for lower-fat chip options in schools, workplaces, and health-focused retail channels. Baked chips also reduce acrylamide risks by avoiding the high-temperature frying process used in traditional chips. The market is shifting toward products with reduced fat, cleaner oils, and simpler ingredient lists, which explains the growing popularity of baked chips in health-conscious assortments.

By Flavor: Plain/Salted Anchors Household Penetration; Flavored Leads the Innovation Pipeline

In 2025, plain or salted potato chips held a 56.87% market share, highlighting their popularity and regular household consumption. The BLS Consumer Expenditure Survey reported an average annual household spending of USD 178.53 on potato chips and snacks, with plain or salted chips being the most common choice. Their versatility allows them to pair well with dips, sandwiches, and beverages, or be enjoyed on their own. This flexibility makes the segment resilient, especially when consumers reduce spending on premium or novelty products in the US potato chips market.

The flavored potato chips segment in the US is projected to grow at a 9.03% CAGR from 2026 to 2031, the fastest among flavor categories. PepsiCo’s Lay’s brand introduced 40 limited-edition globally inspired flavors across North America for the FIFA World Cup 2026, including three US-exclusive variants, showcasing how major brands use global events to attract consumers. Additionally, NACS reported 435 new candy and salty snack items in the convenience channel in 2025, with flavor playing a key role in driving impulse purchases. These flavored launches consistently boost the US potato chips market, as each limited-edition release provides a unique reason for consumers to buy beyond routine pantry restocking.

By Packaging Type: Family Packs Drive Stock-Up Economics; Single Serve Captures On-the-Go Demand

In 2025, family or bulk pack formats commanded a dominant 58.92% share of the market, buoyed by stock-up tendencies in club stores and mass retail outlets. As of February 2026, FMI highlighted that the average US household spent USD 169 weekly on groceries. Additionally, with 45,575 supermarkets dotting the national landscape in 2024, it's evident that routine grocery shopping bolsters the demand for larger pack formats. These larger bags not only provide a better cost per ounce but also lessen the frequency of repurchases, aligning perfectly with the value-driven shopping habits of numerous households. Consequently, family packs have cemented their position in the US potato chips market, as consumers increasingly view them as staple pantry items rather than mere indulgences.

Forecasts indicate that single-serve packaging is set to experience the swiftest CAGR of 9.65% from 2026 to 2031, underscoring a shift towards quick trips and out-of-home consumption. In early 2026, Shearer’s Foods inaugurated its potato chip production at the Moraine, Ohio, facility, unveiling a high-speed automated line tailored for premium single-serve and multipack offerings. With an annual production capacity of 36 million pounds, the plant's design underscores a robust confidence in the sustained demand for portable formats. The rising market size of single-serve packs in the US potato chips arena can be attributed to the growing emphasis on convenience, portion control, and the appeal of variety packs in both grocery and club channels.

By Distribution Channel: Supermarkets Anchor Category Visibility; Online Reshapes Market Access

In 2025, supermarkets and hypermarkets dominated distribution channels, accounting for 60.32% of the market share and serving as the primary visibility driver for the category. FMI data on store counts and household spending highlights that grocery trips remain a key routine for households, with potato chips consistently included in purchases. Utz reported a 2.5% growth in branded salty snacks retail sales in Q4 2025, outperforming the category's overall 1.1% growth. This growth was driven by better distribution and strong market share retention in core regions. Shelf placements in these channels continue to favor large brands with higher trade spending, helping them maintain dominance in the US potato chips market.

Online retail is expected to grow at a 10.25% CAGR from 2026 to 2031, making it the fastest-growing distribution channel in the US potato chips market. FMI projects a recovery in total US online grocery sales by 2031. In 2025, online food sales rose nearly 19%, contributing to about 75% of grocery dollar growth. FMI also noted that 7.1% of grocery item sales were online in 2024, and by 2025, 94% of grocery shoppers used both online and in-store channels. This shift benefits premium and clean-label brands, as digital platforms reduce placement barriers that remain prevalent in physical stores.

Geography Analysis

In 2025, the South led the US potato chips market with a 33.29% share. BLS reported 53,222 thousand consumer units in the region, the largest in the country, while FRED data showed an average food-at-home spending of USD 5,502 per consumer unit in 2024. The region's widespread convenience and dollar stores ensure easy access to single-serve and pantry formats, driving sales across price ranges. Popular local flavors like Cajun, BBQ, and spicy variants sustain strong demand, making it difficult for generic flavors to compete.

From 2026 to 2031, the Northeast is expected to grow at the fastest rate in the US potato chips market, with a projected CAGR of 10.81%. BLS recorded 23,430 thousand consumer units in the region, with an average pre-tax income of USD 116,310, well above the national average of USD 103,012. Higher incomes reduce resistance to premium-priced options like baked, clean-label, and artisanal kettle-cooked chips. Additionally, dense urban grocery networks in cities such as New York, Boston, and Philadelphia provide specialty products with greater shelf visibility and repeat purchase opportunities.

Competitive Landscape

The U.S. potato chips market is moderately consolidated nationally but remains highly competitive due to strong regional and niche brands. PepsiCo leads the market with its Frito-Lay portfolio, including Lay's and Ruffles, supported by extensive distribution networks, significant marketing, and strong retailer ties. Other key players like Kellanova, The Campbell's Company, Utz Brands, and Herr Foods Inc. compete with established brands, diverse flavors, and expanding retail presence.

Competition is driven by product innovation, premiumization, and changing consumer preferences. Companies are introducing kettle-cooked, organic, reduced-fat, and clean-label chips while offering bold, globally-inspired flavors to attract younger consumers. Recent launches from Kettle Brand and Utz highlight the focus on flavor innovation and limited-edition products as key strategies.

Regional players like Better Made, Old Dutch, Zapp's, and Martin's maintain loyal customer bases. As consumers prioritize value, leading brands balance premium products with affordability, invest in healthier formulations, packaging redesigns, and improve supply chain efficiency. Moving forward, brand strength, distribution reach, innovation, and responsiveness to health trends will shape the U.S. potato chips market.

U.S. Potato Chips Industry Leaders

PepsiCo, Inc.

Kellanova

The Campbell's Company

Herr Foods Inc

Utz Brands, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: PepsiCo's Lay's brand launched 40 limited-edition globally inspired potato chip flavors across North America in partnership with the FIFA World Cup 2026, including 3 exclusive US variants. The campaign represents the largest single-event flavor activation in Lay's history, designed to drive household trial among flavor segments that standard year-round SKUs do not reach.

- February 2026: Shearer's Foods began potato chip production at its new Moraine, Ohio facility, a 390,000-square-foot plant converted from a former General Motors site at a total investment of USD 106 million. According to the company, the facility targets an annual output of 36 million pounds of chips and is expected to employ more than 300 workers at full operation.

- January 2026: Jackson's announced its nationwide retail expansion into club, grocery, natural, convenience, and e-commerce channels simultaneously, securing placement at Costco, Walmart, Target, Whole Foods, Sprouts, Kroger, CVS, 7-Eleven, and Amazon, marking the brand's transition from health specialty to mainstream national distribution.

U.S. Potato Chips Market Report Scope

| Baked |

| Fried |

| Plain/Salted |

| Flavored |

| Single Serve |

| Family/Bulk Packs |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| South |

| Midwest |

| West |

| Northeast |

| By Product Type | Baked |

| Fried | |

| By Flavor | Plain/Salted |

| Flavored | |

| By Packaging Type | Single Serve |

| Family/Bulk Packs | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Region | South |

| Midwest | |

| West | |

| Northeast |

Key Questions Answered in the Report

What is the expected value of the US potato chips sector by 2031?

The US potato chips market is forecast to reach USD 23.51 billion by 2031, rising from USD 15.90 billion in 2026 at an 8.1% CAGR.

Which product type leads sales in US potato chips?

Fried potato chips led with 65.43% share in 2025, supported by entrenched processing capacity and strong convenience-store demand.

Which flavor segment is growing the fastest in potato chips in the United States?

Flavored potato chips are projected to grow at a 9.03% CAGR through 2031, supported by limited editions and culturally themed launches.

Why is online grocery becoming more important for chip brands?

Online retail stores are projected to grow at a 10.25% CAGR, and digital grocery growth gives premium and clean-label brands more access beyond traditional shelf constraints.

Page last updated on: