Organic Wine Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

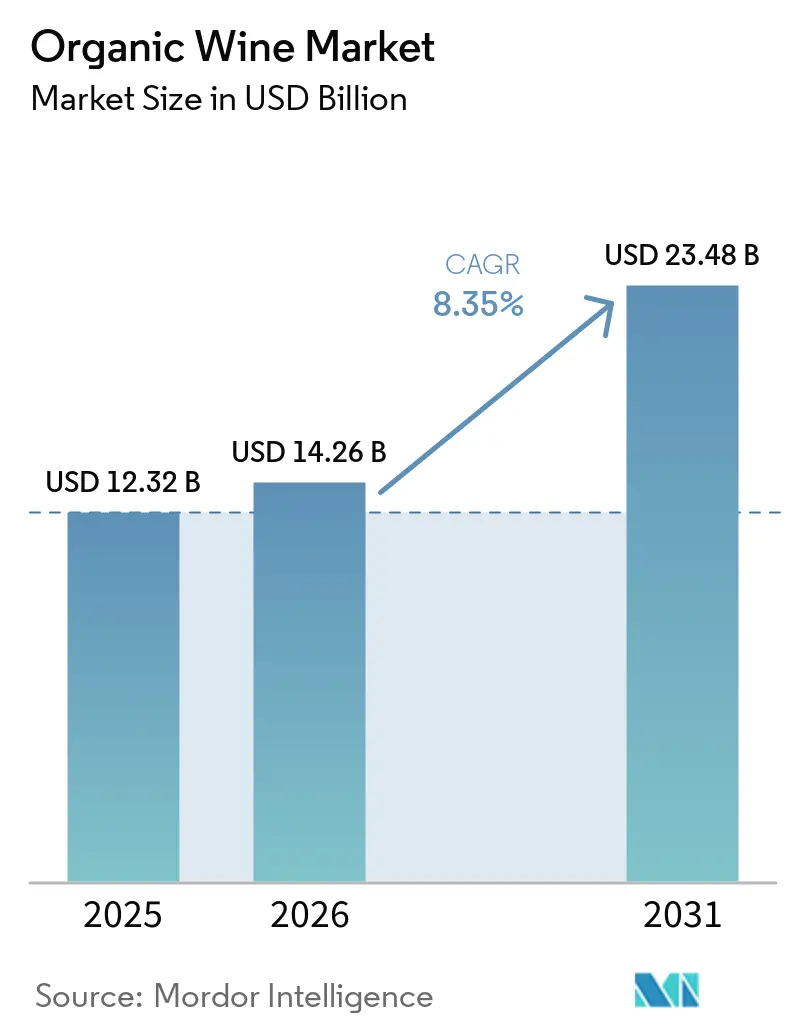

| Market Size (2026) | USD 14.26 Billion |

| Market Size (2031) | USD 23.48 Billion |

| Growth Rate (2026 - 2031) | 8.35% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organic Wine Market Analysis by Mordor Intelligence

The organic wine market size is projected to expand from USD 12.32 billion in 2025 to USD 14.26 billion in 2026 and to USD 23.48 billion by 2031, registering a CAGR of 8.4% between 2026 and 2031. The organic wine market is gaining from stronger demand for clean-label alcoholic beverages, especially among younger adults who pay closer attention to farming methods, ingredient transparency, and sustainability claims. The category is also benefiting from tighter European rules on organic oenological practices, which support product integrity and raise confidence in certified offerings across export markets. Premium buying behavior is supporting growth as consumers buy fewer bottles in some markets but show greater willingness to spend on quality, provenance, and certification. Europe remains the structural center of the organic wine market because it combines vineyard scale, mature wine culture, and established organic standards, while Asia-Pacific is set to post the fastest regional expansion through 2031. The main pressure point in the organic wine market sits on supply, as weaker vineyard conversion activity and higher compliance costs are tightening certified grape availability even when end-market demand stays firm.

Key Report Takeaways

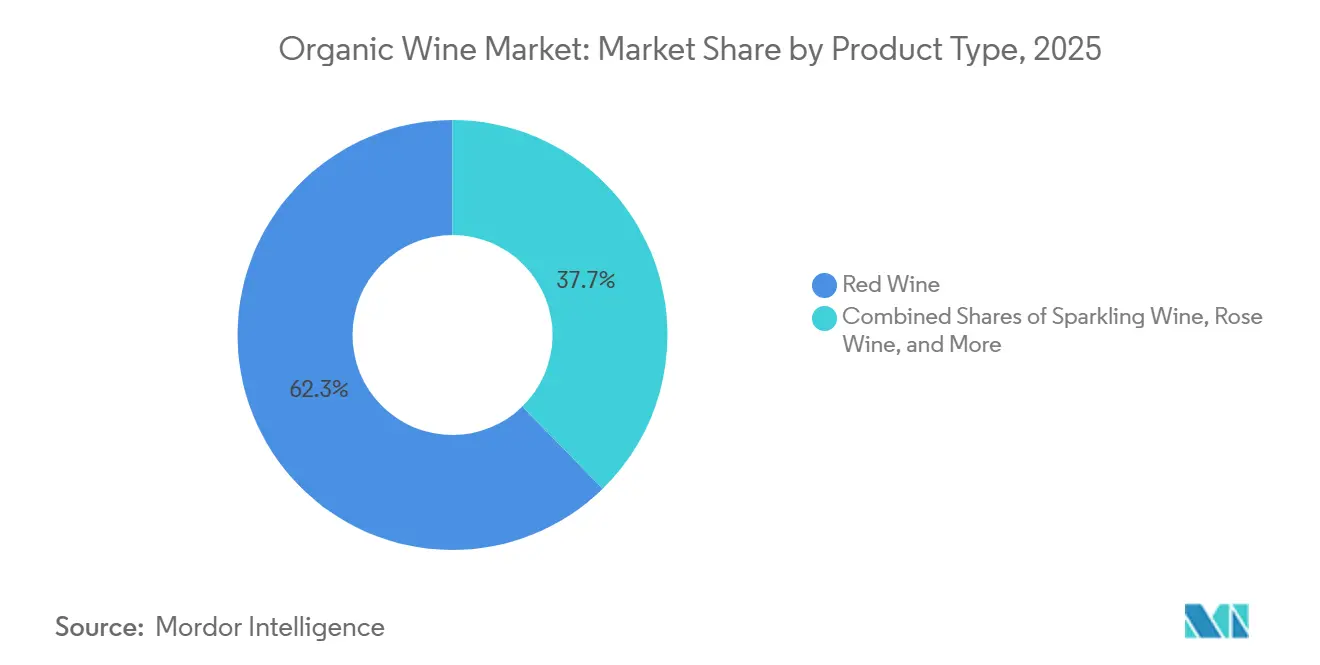

- By product type, Red Wine held 62.31% of revenue share in 2025, while Sparkling Organic Wine is forecast to expand at a 10.56% CAGR through 2031.

- By packaging, Bottles accounted for a 96.25% share in 2025, while Cans recorded the highest projected CAGR at 10.15% through 2031.

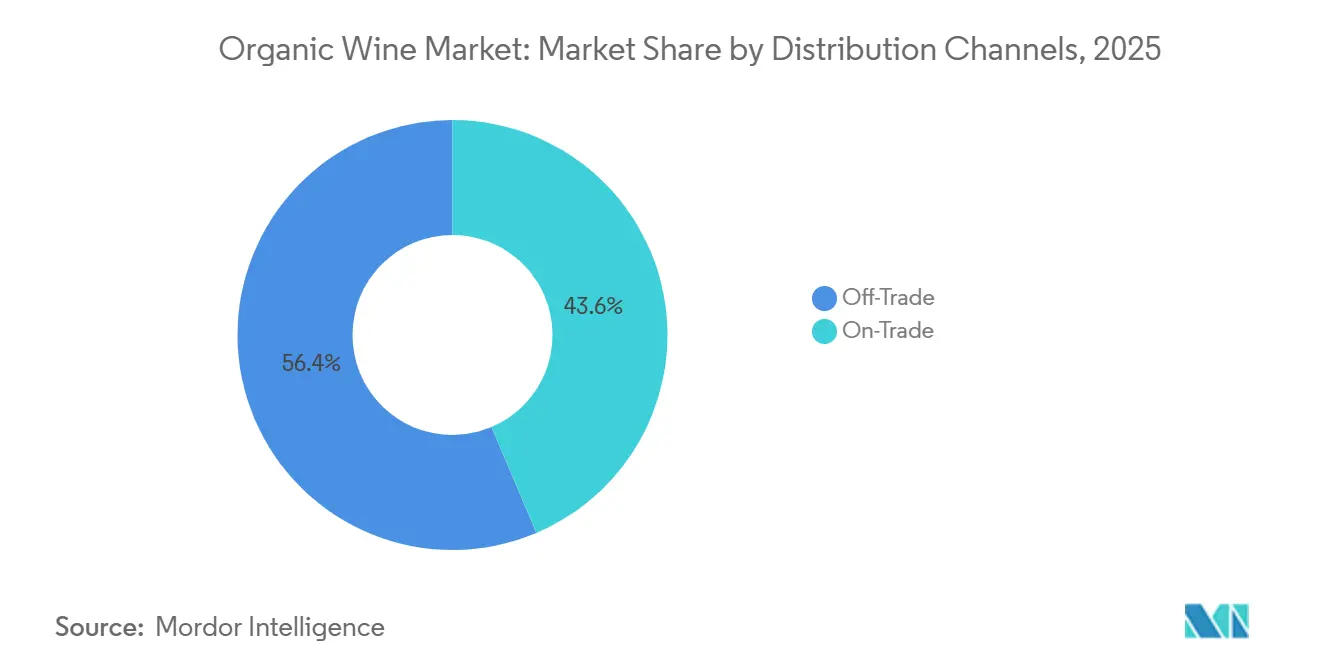

- By distribution channel, Off-Trade held a 56.38% share in 2025, while On-Trade is advancing at a 9.97% CAGR through 2031.

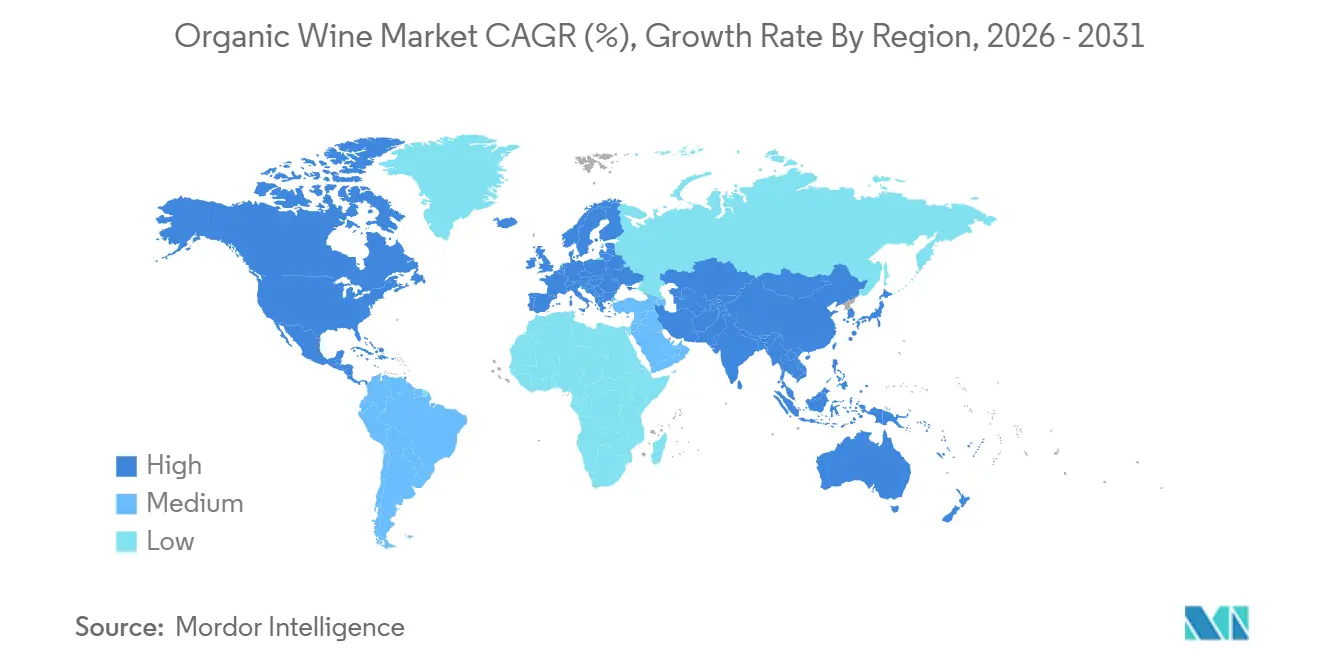

- By geography, Europe captured a 75.62% share in 2025, while Asia-Pacific is forecast to grow at a 10.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Organic Wine Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Preference for Natural and Clean-Label Products | +2.3% | Global, strongest in North America and Western Europe | Short term (≤ 2 years) |

| Growing Awareness of Environmental Sustainability | +1.2% | Europe, especially France, Germany, and Scandinavia, and North America | Medium term (2-4 years) |

| Growth of Eco-Conscious Millennial and Gen Z Consumers | +1.8% | Global, led by North America, Western Europe, and Australia | Short term (≤ 2 years) |

| Increasing Health Consciousness Among Consumers | +1.0% | Global | Medium term (2-4 years) |

| Premiumization Trend in the Wine Industry | +1.4% | Europe and North America, with spillover into core Asia-Pacific markets | Medium term (2-4 years) |

| Rising Adoption by Restaurants and Hospitality Sector | +0.9% | Europe, core Asia-Pacific markets, and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Preference for Natural and Clean-Label Products

The organic wine market is moving beyond a simple sustainability claim and is becoming more closely tied to trust in how wine is grown and processed. A 2025 Wine Market Council study found that consumers were willing to pay a premium for sustainably produced wine and an even stronger premium for certified organic variants, with this willingness remaining firm in higher-income households[1]Source: Wine Market Council, “Why Consumers Really Buy Eco-Friendly Wines, New WMC Study Uncovers Surprising Insights,” Wine Industry Advisor, wineindustryadvisor.com. This matters because the organic wine market depends on credibility, and buyers increasingly respond to specific production cues rather than broad environmental language. Retailers are responding by giving more visible shelf space to organic and biodynamic labels in mainstream grocery settings, which makes trial easier and repeat buying more likely. Producers that explain farming practices, sulfite management, and certification details are building a stronger premium position than those relying on generic branding alone. The result is that the organic wine market is seeing demand shaped less by novelty and more by documented process transparency.

Growth of Eco-Conscious Millennial and Gen Z Consumers

The organic wine market is also being reshaped by younger drinkers who connect wine choice with health, environmental impact, and traceable production. At Millésime Bio 2026, under-35 buyers stood out for preferring certified and clearly explained wines even as their total alcohol intake declined, which shows a shift in how value is judged in the category. This consumer group is less loyal to legacy labels and more willing to switch when another brand offers stronger sourcing proof or deeper certification. That behavior gives smaller estate-led brands a fairer route into the organic wine market than in conventional wine, where scale and distribution often dominate buying decisions. It also explains why newer formats are gaining attention, because younger consumers are discovering organic wine in more casual and mobile drinking occasions. The organic wine market is therefore expanding through a mix of values-led purchasing and changes in where and how younger consumers enter the category.

Premiumization Trend in the Wine Industry

The organic wine market is benefiting from premiumization because certification is increasingly acting as a signal of care, authenticity, and product distinction. Concha y Toro reported that premium-and-above wines represented 57.4% of total wine sales in 2025, and its acquisition of Maison Mirabeau added a premium Provence brand with regenerative organic credentials to its portfolio. That deal shows how larger groups are using organic and regenerative assets to upgrade brand mix and improve pricing power rather than treating certification as a side label. This creates a more competitive setting for small producers, but it also expands the accepted price band for estate-grown certified wine. In the organic wine market, premiumization is not only raising average selling prices, but it is also changing the kind of assets buyers value in acquisitions. Vineyard quality, appellation strength, and certification depth are now being combined more directly in portfolio strategy.

Rising Adoption by Restaurants and Hospitality Sector

The organic wine market is gaining a useful growth channel through restaurants, bars, and premium hospitality venues where trial happens naturally at the point of service. Italy’s organic food market reached EUR 6.9 billion (USD 7.5 billion) in 2025, and out-of-home consumption accounted for 20% of total organic spending. The same source reported that 85% of Italian restaurant operators offered organic wines, which means the on-trade channel is already a real route to consumer exposure rather than a future possibility. Premium venues in Great Britain also matter because they account for 42% of on-trade wine volume and 49% of on-trade wine value, which supports better price realization for quality-focused offerings. For the organic wine market, restaurant listings do more than add sales volume, they also shape brand credibility and consumer education. This makes hospitality a value-building channel even when off-trade remains larger in absolute volume.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Production Costs | -1.1% | Global, most acute in France and Germany | Short term (≤ 2 years) |

| Complex and Costly Certification Requirements | -0.6% | North America and Europe | Medium term (2-4 years) |

| Availability of Alternate Organic Beverages | -0.5% | North America and Western Europe | Medium term (2-4 years) |

| Limited Availability of Organic Vineyards and Raw Materials | -0.9% | France, Bordeaux, Burgundy, and Germany | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Production Costs

The organic wine market faces a real cost challenge because organic viticulture is more labor-intensive and more exposed to yield pressure during difficult seasons. A 2025 long-term field trial published in Agronomy for Sustainable Development found that organic viticulture yields averaged 18% below conventional systems over the observation period, with the gap widening in adverse weather years. A 2026 Sonoma study also showed that regenerative-organic systems only improved value over the long term when yields held steady, while a 20% yield loss pushed economics into deficit. Those economics explain why some growers hesitate to convert or expand certified acreage, even as final-bottle demand improves. In the organic wine market, producers with strong brand equity can pass through some of these costs, but smaller operators often cannot. That creates uneven resilience across the supply base and keeps the category more exposed to margin pressure than demand trends alone suggest.

Limited Availability of Organic Vineyards and Raw Materials

The organic wine market also depends on a narrow pool of certified vineyards in the regions that carry the strongest quality and export credentials. France entered 2024 with organic production already important across the wine landscape, yet the pace of new conversion weakened and then turned more restrictive as climate pressure and production costs rose. In Europe, existing certified estates therefore gain pricing support when demand keeps rising, but new supply does not keep pace. Limited raw material availability also matters for branded producers that want secure volumes across several vintages, because they need dependable access to certified fruit, not just one favorable harvest. The 3-year transition period for organic certification further slows the entry of new growers because expenses rise before the bottle can capture an organic premium. For the organic wine market, this creates a structural bottleneck at the vineyard level that is harder to solve quickly than a normal retail distribution gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Red Wine Holds the Base While Sparkling Builds the Strongest Forward Momentum

Red Wine held 62.31% of the organic wine market share in 2025, which reflects its deep link with food occasions, established consumer familiarity, and strong positioning in Europe and North America. The organic wine market still leans on red wine as the segment that anchors volume, price stability, and brand recognition across mature retail channels. White Organic Wine remained the next largest category in the draft, and its improving retail performance in France points to a wider shift toward lighter drinking styles and more flexible food pairing occasions. Rosé Organic Wine is also strengthening its position as premium Provence and regenerative credentials attract consumers who want a more contemporary premium proposition.

Sparkling Organic Wine market size for the sparkling segment is projected to expand at a 10.56% CAGR between 2026 and 2031, making it the fastest-growing product type in the organic wine market. This growth is tied to occasion-led consumption, where consumers may drink less frequently but choose better bottles when they do purchase. The category also benefits from a younger consumer profile, since under-35 drinkers are more open to celebratory and lower-volume premium occasions than older buyers. The February 2025 EU rule change that allows de-alcoholization of organically certified wine gives sparkling producers a clearer route into low-ABV innovation and broadens the addressable audience[2]Source: European Commission, “Commission Delegated Regulation (EU) 2025/405 of 13 December 2024 Amending Regulation (EU) 2018/848 as Regards Oenological Practices,” EUR-Lex, eur-lex.europa.eu. In practical terms, the organic wine market is likely to keep red wine as its revenue base while sparkling becomes a more important source of new premium demand.

By Packaging: Bottles Stay Dominant While Cans Improve Relevance Through Convenience and Sustainability

Bottles accounted for 96.25% of the organic wine market size in 2025, showing how firmly glass still defines quality cues in wine retail, gifting, storage, and restaurant service. The organic wine market continues to rely on bottles because the premium image of organic wine is still closely tied to conventional bottle presentation in both mature and emerging channels. Glass also fits the expectations of collectors, hospitality buyers, and consumers who associate heavier formats with seriousness and quality. This gives bottle-led packaging a strong hold on higher-value price tiers even as sustainability claims become more central in category messaging.

Cans are forecast to grow at a 10.15% CAGR through 2031, which makes them the fastest-expanding packaging format in the organic wine market. Their appeal is strongest among younger consumers who want portability, casual consumption, and lower-packaging waste in a product that still signals quality and provenance. Vinca Wines supported that trend in March 2025 when it launched the United Kingdom’s first full-sized 100% post-consumer recycled aluminum wine bottle for its organic Sicilian range, with initial distribution across more than 300 Tesco stores. The same company extended the format into another SKU in October 2025, showing that alternative packaging is moving from one-off novelty into a repeatable portfolio choice. The organic wine market is therefore keeping bottle-led premium conventions at the top end while steadily expanding room for sustainable convenience formats.

By Distribution Channel: Off-Trade Delivers Scale While On-Trade Shapes Perception and Premium Value

Off-Trade held a 56.38% share in 2025, which made it the larger route to market for the organic wine market across grocery, specialty retail, and e-commerce channels. This channel benefits from wider product visibility, better repeat access for household buyers, and the steady build-out of organic sections in mainstream stores. In Italy, organic product sales through e-commerce grew 5.9% in 2025, which shows how digital ordering is supporting wider access to certified labels beyond the physical shelf. Spain’s rising number of organic wine exporters also supports the off-trade channel because it broadens assortment for retail-led export markets.

On-Trade is projected to grow at a 9.97% CAGR through 2031, which makes it the fastest-moving channel in the organic wine market. Premium hospitality venues matter because they influence both trial and price expectations, especially when sommeliers and restaurant operators actively explain sourcing and farming credentials. In Great Britain, premium on-trade venues account for 42% of wine volume and 49% of wine value, which shows how strongly quality-led settings shape spending patterns. Italy’s out-of-home organic consumption also continued to rise in 2025, which supports the idea that restaurants are becoming a meaningful education and sampling platform for the category. The organic wine market therefore uses off-trade for scale, but it increasingly depends on on-trade to lift brand value and reinforce premium positioning.

Geography Analysis

Europe held 75.62% of organic wine market share in 2025, which confirms that the region remains the center of production, regulation, and consumption for the organic wine market. This lead rests on a strong overlap between wine culture, consumer familiarity with organic products, and the policy structure that supports organic farming. France, Italy, and Spain collectively controlled most of the European Union’s organic vineyard base, and France alone reported more than 164,000 hectares of organic vineyards in the broader regional landscape. Germany also remains important as a demand center, with its organic market reaching EUR 18.23 billion, equal to USD 19.9 billion, in 2025[3]Source: Agence Bio, “Carnet Bio UE 2026,” Agence Bio, agencebio.org. The organic wine market in Europe is also helped by the regulatory framework under Regulation 2018/848 and the 2025 delegated update on oenological practices, which keeps standards visible and consistent across the region.

North America forms a high-value but more selective part of the organic wine market, with demand centered on consumers who buy with clear intent rather than through habitual volume drinking. The United States remains the key market in the region because premium buyers increasingly connect wine quality with farming practice and product transparency. At the same time, compliance requirements have become more demanding for importers under strengthened organic enforcement rules, which raises operating costs and favors larger distributors with better administrative capacity. Canada adds a stable premium base to the regional picture, while Mexico remains smaller and more urban-led in its development path. The organic wine market in North America is therefore attractive in price terms, but it is less straightforward from a compliance and route-to-market perspective.

Asia-Pacific is forecast to grow at a 10.25% CAGR through 2031, which makes it the fastest-growing regional segment in the organic wine market. Australia is an important driver because health and wellness preferences already align well with organic wine positioning in the country. China and India are still earlier in the adoption curve, but affluent consumers in both countries are increasingly connecting organic certification with premium status and perceived product quality. Japan and South Korea offer more structured premium retail environments, which can help imported certified labels build visibility with consumers who value provenance and product assurance. South America remains important on the supply side of the organic wine market because Chile and Argentina host well-known estate producers serving export demand into Europe and North America. Middle East and Africa present narrower but credible opportunities, mainly through premium hospitality and travel retail in markets such as the United Arab Emirates and South Africa.

Competitive Landscape

The organic wine market is moderately concentrated, with a small group of large wine companies operating alongside many estate-led and certification-focused producers. That structure means scale matters in distribution and brand reach, but it does not fully decide success because consumers in the organic wine market also respond strongly to authenticity, vineyard story, and third-party verification. Concha y Toro, Treasury Wine Estates, and other multinational groups bring portfolio breadth, while specialist organic producers compete more effectively on farming identity and category credibility. This mix keeps the organic wine market more open than many conventional beverage categories, even though large groups still shape premium shelf access and international placement.

Certification depth is becoming one of the clearest points of separation in the organic wine market. Concha y Toro’s February 2026 acquisition of Maison Mirabeau is a strong example because it added a premium Provence rosé brand and regenerative organic credentials in one move. Bonterra’s 2026 pilot with autonomous UV-C light robots in California shows another direction, where technology is being used to support low-input viticulture and strengthen operational efficiency alongside sustainability messaging. Neal Family Vineyards also raised the bar in January 2026 with a Napa Valley single-vineyard release carrying Demeter Biodynamic, CCOF Organic, and Regenerative Organic Certified status, which signals the growing importance of stacked credentials in the upper end of the category. These moves show that competition in the organic wine market is increasingly taking place through farming proof and production architecture, not only brand marketing.

Packaging and portfolio strategy are also shaping competitive behavior in the organic wine market. Vinca Wines built a visible point of difference by expanding full-sized recycled aluminum packaging across its organic Sicilian range, which helped the brand link organic sourcing with modern convenience and lower-footprint presentation. Treasury Wine Estates announced its Ascent portfolio transformation in June 2026, narrowing brand focus toward a smaller set of priority labels, which could leave more room for specialist organic players in some retail spaces. A 2024 study in Environmental Research Communications also found that many organically produced wines are not always sold with an organic label, which shows that the commercial value of certification can differ by farm characteristics and positioning strategy. That finding fits the current shape of the organic wine market, where some brands advertise certification very directly and others use it more selectively within a broader quality message. The competitive picture is therefore neither fully consolidated nor fully fragmented, because market power in the organic wine market is divided between scale, terroir, certification, and channel access.

Organic Wine Industry Leaders

Bronco Wine Company

Kendall-Jackson Winery

Emiliana Organic Vineyards

King Estate Winery

The Wine Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Mack & Schühle Italia expanded its Grapur organic wine range by launching a new sparkling brut (spumante), marking the brand’s third product offering. The new sparkling wine contains 9.5% alcohol, aligning with the growing consumer preference for lower-alcohol and mindful drinking options.

- April 2026: Robert Hall Winery, part of O’Neill Vintners & Distillers, introduced two Regenerative Organic Certified (ROC) wines, 2024 Cabernet Sauvignon and 2025 Sauvignon Blanc, exclusively at Whole Foods Market across the United States.

- September 2025: Tapi Wines, a boutique winery from Marlborough, New Zealand, launched the 2025 Tapi Marlborough Sauvignon Blanc in Shenzhen, becoming the first New Zealand wine to receive both New Zealand organic certification (BioGro) and official Chinese organic certification (COFCC). The launch was facilitated through a partnership with Shenzhen-based importer MoWine and leverages the China–New Zealand Organic Product Mutual Recognition Arrangement, which enables eligible New Zealand organic products to carry China’s official organic seal.

Global Organic Wine Market Report Scope

| Red Organic Wine |

| White Organic Wine |

| Rosé Organic Wine |

| Sparkling Organic Wine |

| Bottles |

| Cans |

| Off-Trade |

| On-Trade |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Red Organic Wine | |

| White Organic Wine | ||

| Rosé Organic Wine | ||

| Sparkling Organic Wine | ||

| By Packaging | Bottles | |

| Cans | ||

| By Distribution Channel | Off-Trade | |

| On-Trade | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the organic wine market by 2031?

The organic wine market is forecast to reach USD 23.48 billion by 2031, rising from USD 14.26 billion in 2026 at an 8.4% CAGR over 2026 to 2031.

Which product type leads sales in organic wine?

Red Wine led the organic wine market in 2025 with 62.31% share, supported by established food-pairing habits and strong presence in mature wine markets.

Which segment is growing fastest in organic wine products?

Sparkling Organic Wine is the fastest-growing product segment, with a forecast CAGR of 10.56% through 2031, helped by premium occasion-led consumption and new low-ABV opportunities.

Why is Europe so important in this category?

Europe held 75.62% share in 2025 because it combines large organic vineyard area, mature wine culture, strong consumer trust in certification, and a well-developed regulatory framework.

Page last updated on: