Tortilla Chips Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

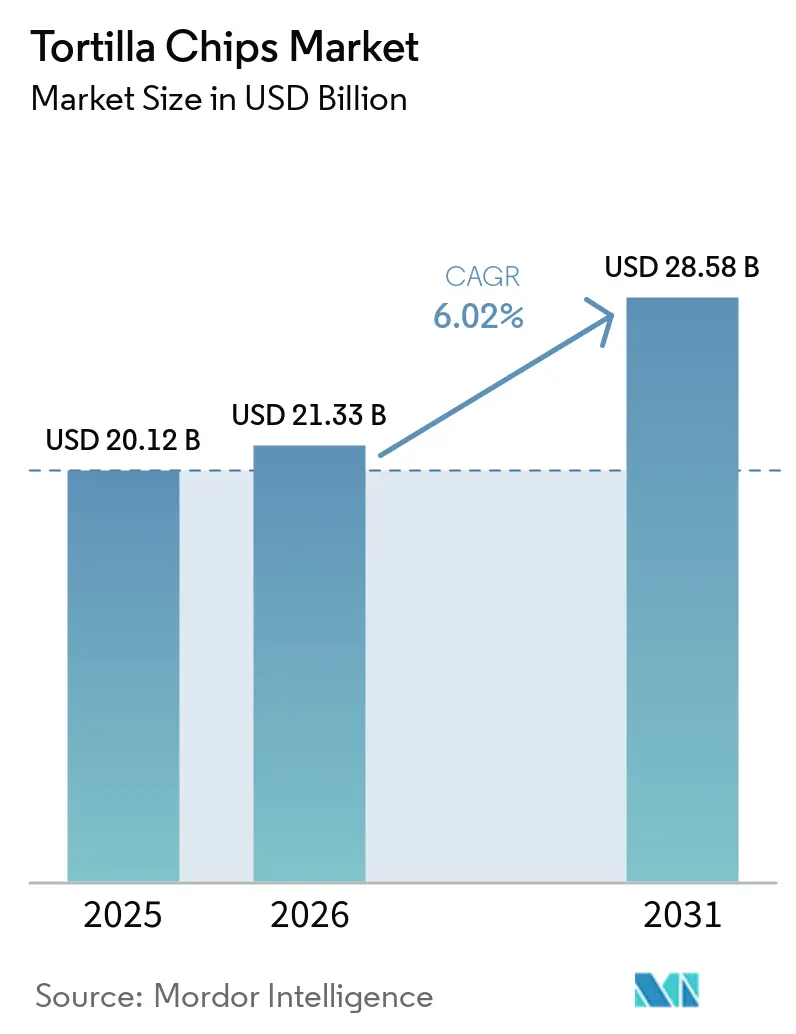

| Market Size (2026) | USD 21.33 Billion |

| Market Size (2031) | USD 28.58 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tortilla Chips Market Analysis by Mordor Intelligence

Global tortilla chips market size in 2026 is estimated at USD 21.33 billion, growing from 2025 value of USD 20.12 billion with 2031 projections showing USD 28.58 billion, growing at 6.02% CAGR over 2026-2031. This growth trajectory reflects the sector's resilience amid evolving consumer preferences toward healthier snacking alternatives and premium flavor experiences. The market's expansion is underpinned by strategic consolidation moves, with PepsiCo's USD 1.2 billion acquisition of Siete Foods in January 2025 signaling intensified competition for the health-conscious consumer segment.

Key Report Takeaways

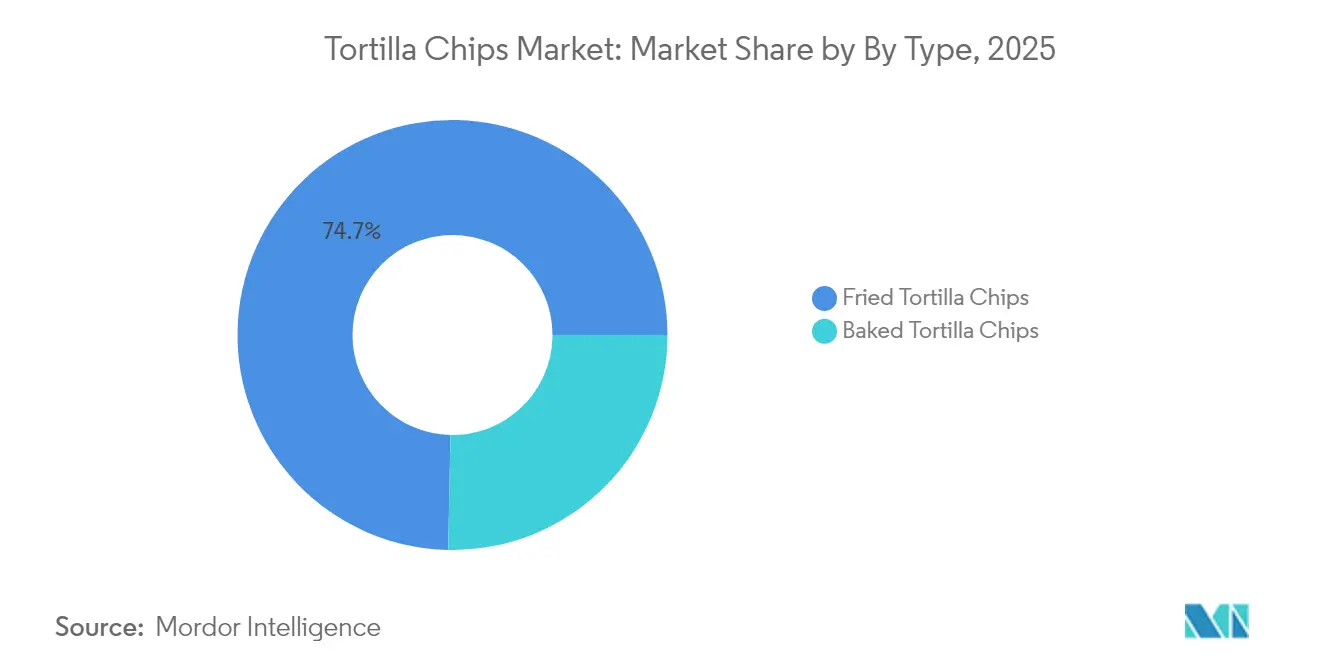

- By type, fried chips held a 74.68% tortilla chips market share in 2025, whereas baked chips record the fastest 6.89% CAGR for 2026-2031.

- By flavor, flavored varieties captured 67.98% of the tortilla chips market size in 2025 and are projected to expand at 6.32% CAGR through 2031.

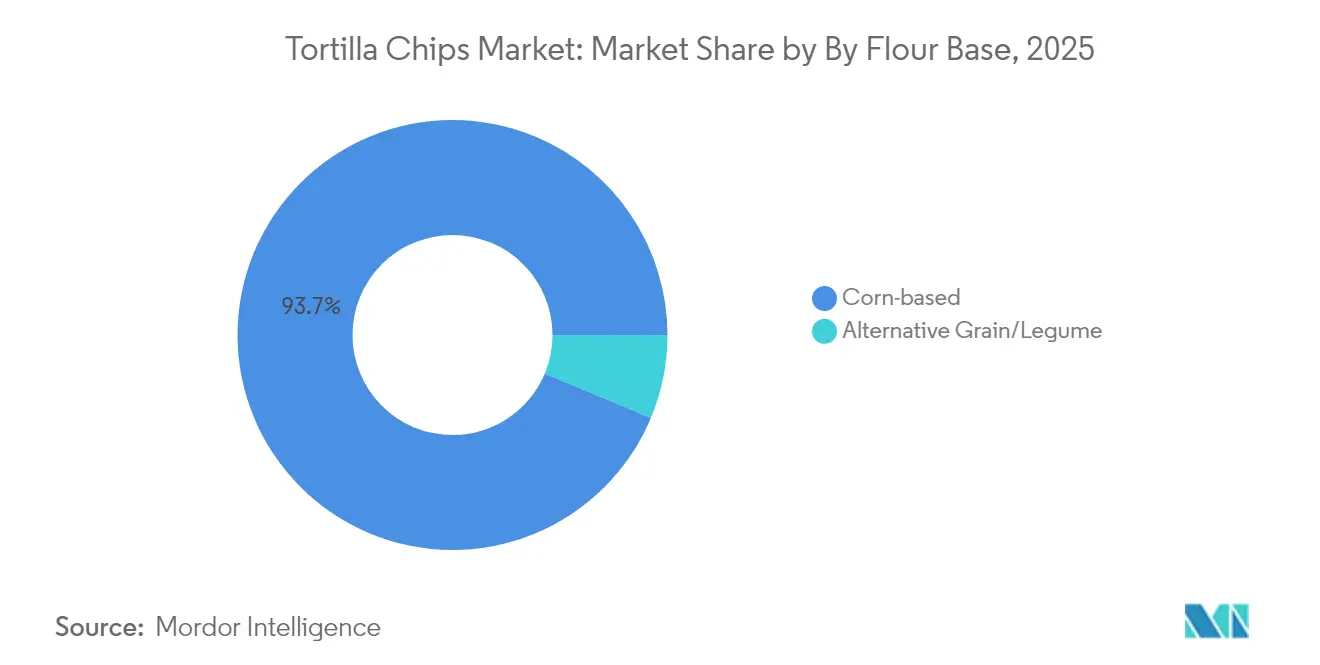

- By flour base, corn formulations retained 93.72% share in 2025, yet alternative grains lead segment growth at 6.98% CAGR to 2031.

- By distribution channel, supermarkets/hypermarkets accounted for 47.25% of 2025 sales, while online retail accelerates at 7.55% CAGR over the forecast horizon.

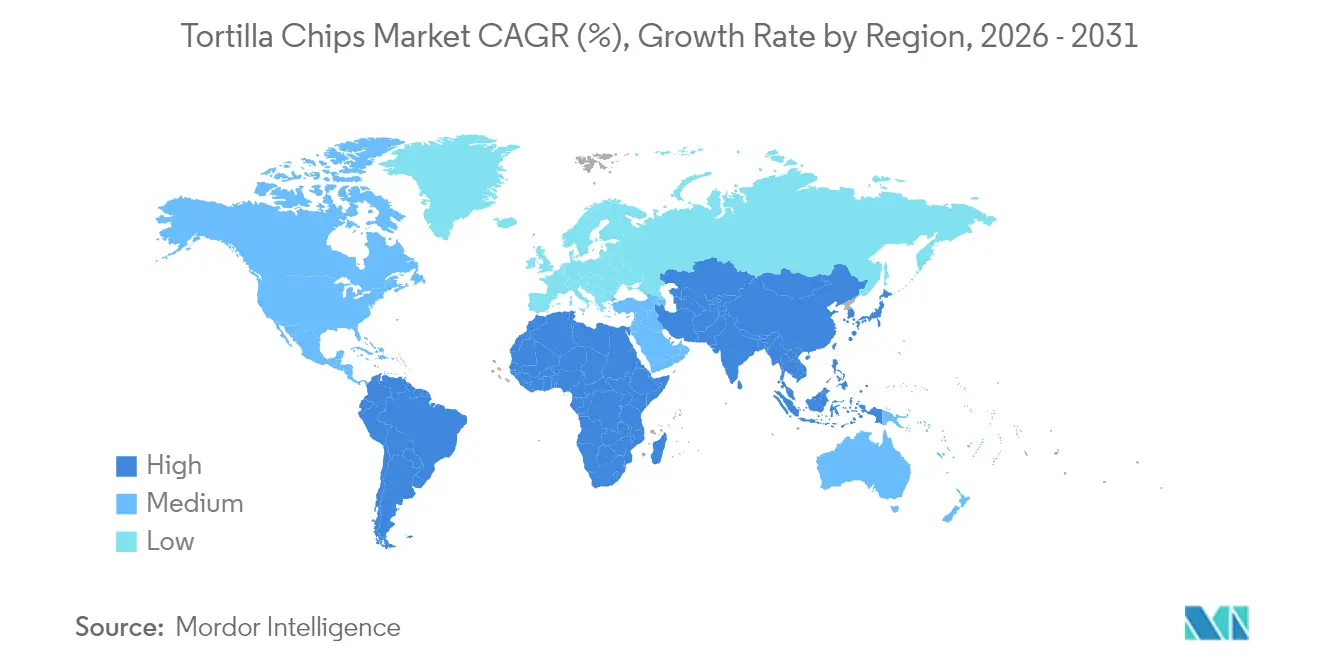

- By geography, North America led with 37.90% revenue share in 2025; Asia-Pacific posts the highest 7.31% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tortilla Chips Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continuous product innovation, including new flavors and healthier formulations | +1.2% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Rising health consciousness leading to demand for gluten-free, organic, baked, and multigrain options | +0.8% | North America and Europe core, expanding to Asia-Pacific urban centers | Long term (≥ 4 years) |

| Increasing consumer demand for convenient and ready-to-eat snacks | +0.7% | Global, accelerated in Asia-Pacific emerging markets | Short term (≤ 2 years) |

| Increasing consumer interest in ethnic, bold, and exotic flavor varieties | +0.6% | North America and Asia-Pacific, spill-over to Latin America | Medium term (2-4 years) |

| Innovation in packaging with single-serve, resealable, and sustainable designs | +0.5% | Global, regulatory-driven in EU and North America | Medium term (2-4 years) |

| Growing trend towards functional snacking with added protein, fiber, or other beneficial nutrients | +0.4% | North America and Europe, early adoption in urban Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Continuous Product Innovation Drives Market Expansion

Product innovation cycles accelerate across the global tortilla chips landscape, with manufacturers launching more new SKUs. The introduction of Chamoy-flavored chips and Takis' Chile Limon variant in February 2025 demonstrates how companies leverage ethnic flavor profiles to capture diverse consumer segments. The innovation imperative extends beyond flavors to include texture modifications, with companies investing in air-frying technologies that reduce oil content by 30% while maintaining crispness. This technological advancement addresses health concerns without compromising taste experience, enabling premium positioning strategies that command 15-20% price premiums over traditional offerings.

Health-Conscious Formulations Reshape Product Portfolios

Consumer health awareness drives fundamental reformulation strategies, with baked tortilla chips segment growth at 7.12% CAGR significantly outpacing the overall market. Alternative grain formulations incorporating quinoa, lentils, and chickpeas grow at 7.27% CAGR, reflecting protein-seeking behaviors among millennial and Gen-Z consumers. Siete Foods' success prior to PepsiCo's acquisition demonstrates market appetite for grain-free alternatives. FDA's updated "healthy" claim criteria, effective January 2025, create regulatory tailwinds for reformulated products meeting sodium reduction and whole grain requirements.

Convenience Culture Accelerates Ready-to-Eat Demand

The convenience snacking trend is gaining momentum across global markets, with single-serve packaging formats increasingly outpacing bulk options in popularity and growth. Workplace snacking habits, permanently altered by hybrid work arrangements, drive demand for portable, mess-free formats that align with mobile consumption patterns. Companies are introducing portion-controlled packages, such as 1-ounce portion-controlled packages address portion awareness while maintaining convenience appeal. This trend particularly resonates in Asia-Pacific markets, where urbanization and longer commuting times create sustained demand for grab-and-go snacking solutions.

Sustainable Packaging Innovation Addresses Environmental Concerns

Packaging sustainability initiatives gain momentum, with Frito-Lay's compostable bag technology and PHA-based materials representing breakthrough innovations that address environmental concerns without compromising product freshness. These developments respond to consumer surveys indicating 59% willingness to pay premium prices for sustainable products[1]Source: European Environment Agency, “Public Views on the Circular Economy,” eea.europa.eu. Resealable formats grow 28% year-over-year, addressing food waste concerns while extending product freshness. Single-serve packaging innovations balance convenience with portion control, particularly appealing to health-conscious consumers managing caloric intake.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns related to high sodium, fat, and calorie content in traditional fried tortilla chips | -0.9% | Global, strongest impact in health-conscious North American and European markets | Long term (≥ 4 years) |

| Intense competition from other snack categories | -0.6% | Global, particularly acute in mature North American market | Medium term (2-4 years) |

| Fluctuating prices and supply instability of raw materials | -0.4% | Global, with highest impact in cost-sensitive emerging markets | Short term (≤ 2 years) |

| Regulatory and labeling complexities across different countries | -0.3% | Global, most pronounced in EU and North America with strict regulations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health Concerns Challenge Traditional Formulations

Traditional fried tortilla chips face mounting scrutiny over sodium content averaging 170mg per serving and saturated fat levels that contribute to dietary health concerns. FDA's front-of-package labeling requirements mandate prominent display of high-sodium warnings that influence consumer purchasing decisions[2]Source: U.S. Food and Drug Administration, “Front-of-Package Nutrition Labeling,” fda.gov. Medical research linking excessive sodium intake to hypertension creates regulatory pressure for reformulation, with some manufacturers reducing sodium content by 25% while investing in flavor enhancement technologies to maintain taste appeal. This reformulation process increases production costs by 8-12% while potentially alienating consumers accustomed to traditional flavor profiles.

Competitive Pressure from Alternative Snack Categories

Tortilla chips confront intensified competition from rapidly growing snack categories, including protein bars, vegetable chips, and popped snacks that capture health-conscious consumer segments. The broader snack market's fragmentation creates shelf space competition, with retailers allocating premium positioning to higher-margin alternatives. Mondelez's strategic focus on premium crackers and Hershey's expansion into better-for-you snacking demonstrate how established players pivot resources away from traditional chip categories. Private label penetration in the snack category is further creating additional margin pressure on branded tortilla chip manufacturers while limiting pricing flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Baked Variants Challenge Fried Dominance

Fried tortilla chips maintain commanding market leadership with 74.68% share in 2025, yet baked alternatives accelerate at 6.89% CAGR through 2031, outpacing the overall tortilla market growth. This performance divergence reflects fundamental shifts in consumer health priorities, where traditional taste preferences increasingly compete with nutritional considerations. Baked varieties typically contain 50% less fat than fried counterparts while maintaining satisfactory crunch characteristics through advanced air-frying technologies. The segment's growth trajectory benefits from the FDA's updated nutritional guidelines that favor reduced-fat formulations, creating regulatory tailwinds for continued expansion.

Manufacturing innovations in baked chip production, including multi-stage heating processes and texture enhancement additives, address historical consumer complaints about inferior mouthfeel compared to fried alternatives. Companies invest heavily in R&D to bridge this sensory gap, with some manufacturers achieving taste parity through proprietary seasoning application techniques. The premium pricing opportunity for baked varieties, typically 15-20% higher than fried options, provides attractive margin enhancement potential for manufacturers willing to invest in production capability upgrades.

By Flavor: Premium Flavored Varieties Drive Market Value

Flavored tortilla chips dominate with 67.98% market share in 2025 while simultaneously leading growth at 6.32% CAGR, demonstrating sustained consumer appetite for taste innovation and premium positioning. Plain/salted varieties, despite representing 32.02% of the market, experience slower growth as consumers increasingly seek bold, differentiated flavor experiences. The flavored segment's dual leadership in both size and growth rate indicates successful premiumization strategies that command higher retail prices while driving volume expansion.

Ethnic flavor innovations particularly drive segment performance, with Mexican-inspired varieties like chile-lime and jalapeño maintaining strong appeal while Asian-fusion options gain traction among younger demographics. Chamoy flavor launch and Takis' continued heat-profile expansion demonstrate how manufacturers leverage cultural authenticity to build brand differentiation. Flavor complexity increases through multi-layered seasoning applications, with some premium varieties incorporating up to 7 distinct spice components to create unique taste profiles that justify premium pricing strategies.

By Flour Base: Alternative Grains Disrupt Corn Hegemony

Corn-based tortilla chips dominate with 93.72% market share in 2025, reflecting traditional manufacturing expertise and established supply chain efficiencies. However, alternative grain and legume formulations emerge as the fastest-growing segment at 6.98% CAGR, driven by gluten-free dietary requirements and protein-seeking consumer behaviors. This growth differential suggests potential long-term market share erosion for corn-based varieties as alternative formulations achieve scale economies and taste parity.

Quinoa, lentil, and chickpea-based formulations lead alternative grain innovation, offering protein content 40-60% higher than traditional corn varieties while addressing gluten-free dietary restrictions. Manufacturing challenges for alternative grains, including higher ingredient costs and specialized processing requirements, currently limit widespread adoption but create opportunities for premium positioning strategies that justify elevated retail prices.

By Distribution Channel: Digital Commerce Transforms Retail Landscape

Supermarkets/hypermarkets maintain distribution leadership with 47.25% market share in 2025, leveraging extensive shelf space allocation and promotional capabilities that drive volume sales. However, online retail channels accelerate at 7.55% CAGR, significantly outpacing traditional retail growth and reflecting permanent consumer behavior shifts toward digital commerce. Convenience stores capture impulse purchasing opportunities while other distribution channels collectively address niche market segments.

E-commerce growth particularly benefits premium and specialty tortilla chip brands that struggle for shelf space in traditional retail environments. Direct-to-consumer strategies enable manufacturers to capture higher margins while building direct customer relationships that inform product development decisions. Amazon's grocery expansion and Walmart's e-commerce investments create additional distribution opportunities for tortilla chip manufacturers, while subscription box services introduce products to health-conscious consumers seeking curated snacking experiences

Geography Analysis

North America's market leadership with 37.90% share in 2025 reflects decades of consumer habit formation and extensive distribution infrastructure that supports both mainstream and premium positioning strategies. The region's mature market characteristics include sophisticated flavor preferences, with consumers demonstrating willingness to pay premium prices for artisanal and health-conscious formulations. Canada's snack market shows particular strength in organic and non-GMO varieties, with regulatory frameworks supporting clean-label positioning strategies that command retail price premiums.

Asia-Pacific's emergence as the fastest-growing region at 7.31% CAGR reflects fundamental economic and cultural shifts that create sustained demand expansion opportunities. China's urbanization drives Western snacking adoption, while India's concentrated market structure demonstrates successful localization strategies that blend international formats with regional taste preferences. Japan's sophisticated consumer preferences create opportunities for texture innovation and premium positioning. Southeast Asian markets benefit from rising disposable incomes and increasing exposure to Western food culture through digital media and travel experiences.

Europe demonstrates steady growth supported by stringent food safety regulations and consumer preferences for sustainable packaging solutions that align with environmental consciousness trends. The region's regulatory environment, including EU packaging waste directives, creates compliance requirements that favor manufacturers with advanced sustainable packaging capabilities. Middle East and Africa represent long-term growth opportunities as urbanization and Western food adoption accelerate, though current infrastructure limitations and import dependency create near-term market development challenges.

Competitive Landscape

The global tortilla chips market exhibits moderate consolidation, indicating oligopolistic characteristics where major players maintain significant market influence through brand portfolio breadth and distribution network control. Strategic consolidation accelerates through high-value acquisitions, partnerships, and new product launches. Technology deployment focuses on manufacturing efficiency improvements and sustainable packaging innovations, with companies investing in flavor development and automated quality control systems that reduce production costs while enhancing product consistency.

White-space opportunities emerge in functional snacking categories where protein fortification and alternative grain formulations address unmet consumer needs for nutritious convenience foods. Emerging disruptors leverage direct-to-consumer strategies and social media marketing to build brand awareness without traditional retail distribution investments, creating competitive pressure on established players' market share.

Patent filings in packaging technology, particularly compostable materials and freshness preservation systems, indicate intensified innovation competition as companies seek sustainable differentiation advantages. Regulatory compliance factors include FDA front-of-package labeling requirements that create competitive advantages for companies with cleaner nutritional profiles and transparent ingredient sourcing practices.

Tortilla Chips Industry Leaders

Amplify Snack Brands

GRUMA S.A.B. de C.V.

Utz Brands Inc.

Grupo Bimbo SAB de CV

PepsiCo Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Natural Grocers, a family-operated natural and organic grocery retailer, has introduced Organic Restaurant-Style Tortilla Chips to its private-label product line. The chips are available in three flavors and are made with stone-ground organic corn and sea salt. The products are certified non-GMO, organic, vegan-friendly, and kosher. They contain no synthetic colors, flavors, artificial sweeteners, or preservatives.

- February 2025: Takis introduced two new flavors to its snack product line: Nacho Xplosion and Chile Limon. The Nacho Xplosion flavor combines cheese and spice elements, while Chile Limon represents the company's first global flavor release, offering a milder heat profile with citrus notes.

- January 2025: PepsiCo, Inc. completed the acquisition of Garza Food Ventures LLC, operating as Siete Foods, for USD 1.2 billion. Siete Foods' portfolio includes grain-free tortillas, tortilla chips, potato chips, salsas, and other products that focus on better-for-you ingredients.

Global Tortilla Chips Market Report Scope

A tortilla chips is a snack item prepared from corn tortillas that have been sliced into triangles and fried or baked. Global Tortilla Chips Market is segmented by type into baked tortilla chips and fried tortilla chips. By distribution channels into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. By geography into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| Baked Tortilla Chips |

| Fried Tortilla Chips |

| Plain/Salted |

| Flavored |

| Corn-based |

| Alternative Grain/Legume |

| Supermarkets / Hypermarkets |

| Convenience Stores |

| Online Retail Channels |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Baked Tortilla Chips | |

| Fried Tortilla Chips | ||

| By Flavor | Plain/Salted | |

| Flavored | ||

| By Flour Base | Corn-based | |

| Alternative Grain/Legume | ||

| By Distribution Channel | Supermarkets / Hypermarkets | |

| Convenience Stores | ||

| Online Retail Channels | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is global demand for tortilla chips in 2026?

The tortilla chips market size is valued at USD 21.33 billion in 2026.

What growth rate is forecast through 2031?

Global value is projected to climb to USD 28.58 billion, reflecting a 6.02% CAGR.

Which type is growing fastest?

Baked tortilla chips lead with a 6.89% CAGR between 2026 and 2031, outpacing fried options.

Which region shows the strongest expansion?

Asia-Pacific posts the highest 7.31% CAGR on rising urbanization and Western snack adoption.

Page last updated on: