Organic Snacks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

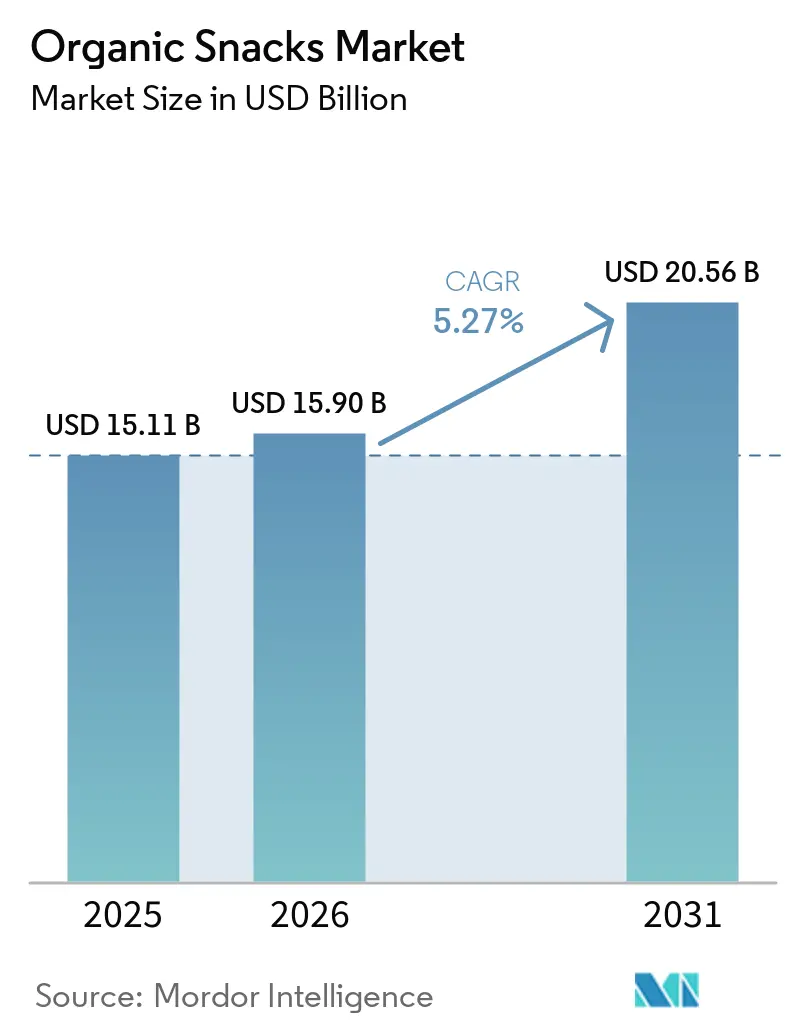

| Market Size (2026) | USD 15.90 Billion |

| Market Size (2031) | USD 20.56 Billion |

| Growth Rate (2026 - 2031) | 5.27% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Organic Snacks Market Analysis by Mordor Intelligence

The organic snacks market size is projected to expand from USD 15.1 billion in 2025 and USD 15.9 billion in 2026 to USD 20.6 billion by 2031, registering a CAGR of 5.3% between 2026 to 2031. This growth is fueled by a significant shift in consumer behavior, with organic certification transitioning from a niche preference to a mainstream choice in many households. In 2025, the U.S. organic sector hit a record of USD 76.6 billion, with 6.8% growth. In contrast, the broader conventional food market saw a 3.4% increase, highlighting the robust demand for organic products, as noted by the Organic Trade Association[1]Source: Organic Trade Association, "Organic Market Overview", ota.com. While North America was the dominant player in 2025, the Asia-Pacific region is poised for the fastest expansion. This dynamic positions the organic snacks market with a solid footing in developed markets and a promising trajectory in emerging ones. The product and channel landscape is evolving, with bakery snacks and online retailing outpacing the average growth, bolstering premium pricing, wider accessibility, and enhanced consumer loyalty. Despite challenges like price disparities, ingredient supply constraints, and new traceability regulations, the organic snacks market is showing resilience. Recent investments, acquisitions, and strategic sourcing moves indicate an adaptive rather than a slowing trend in the category.

Key Report Takeaways

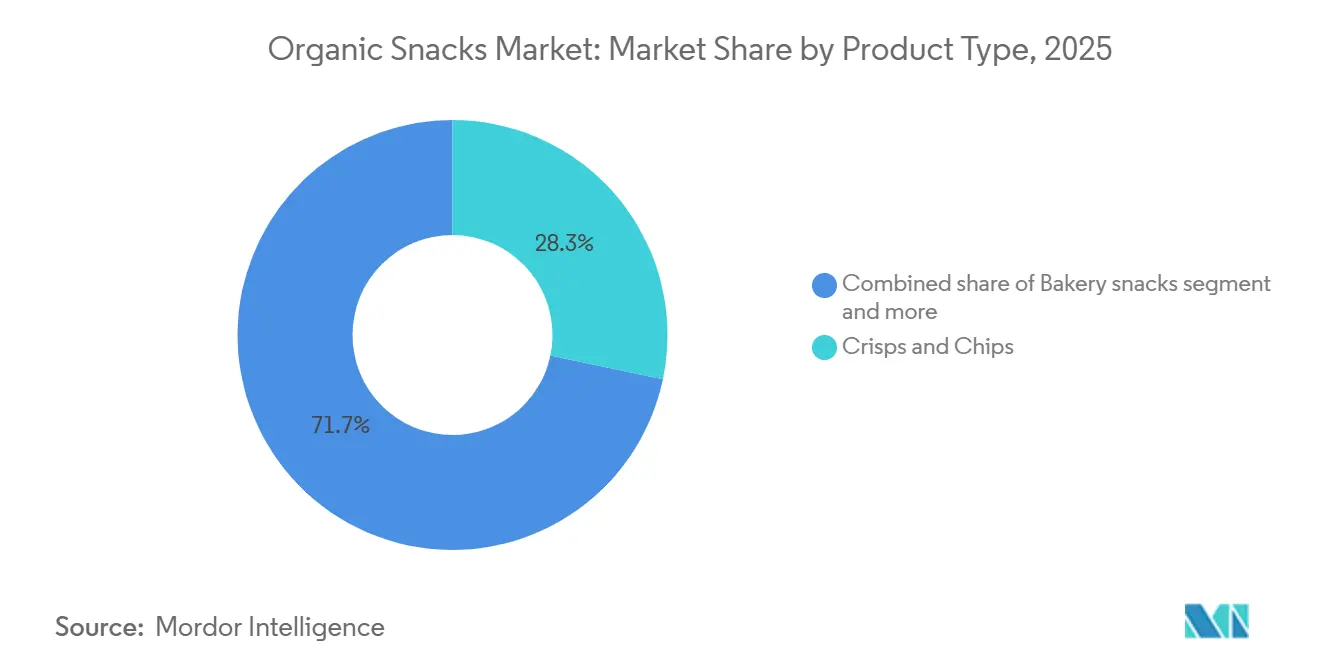

- By product type, Chips and Crisps held 28.3% of 2025 revenue, while Bakery Snacks is forecast to grow at 9% CAGR during 2026-2031.

- By packaging type, Bags and Pouches accounted for 55.3% of 2025 revenue, while Cans is projected to expand at 8.1% CAGR during 2026-2031.

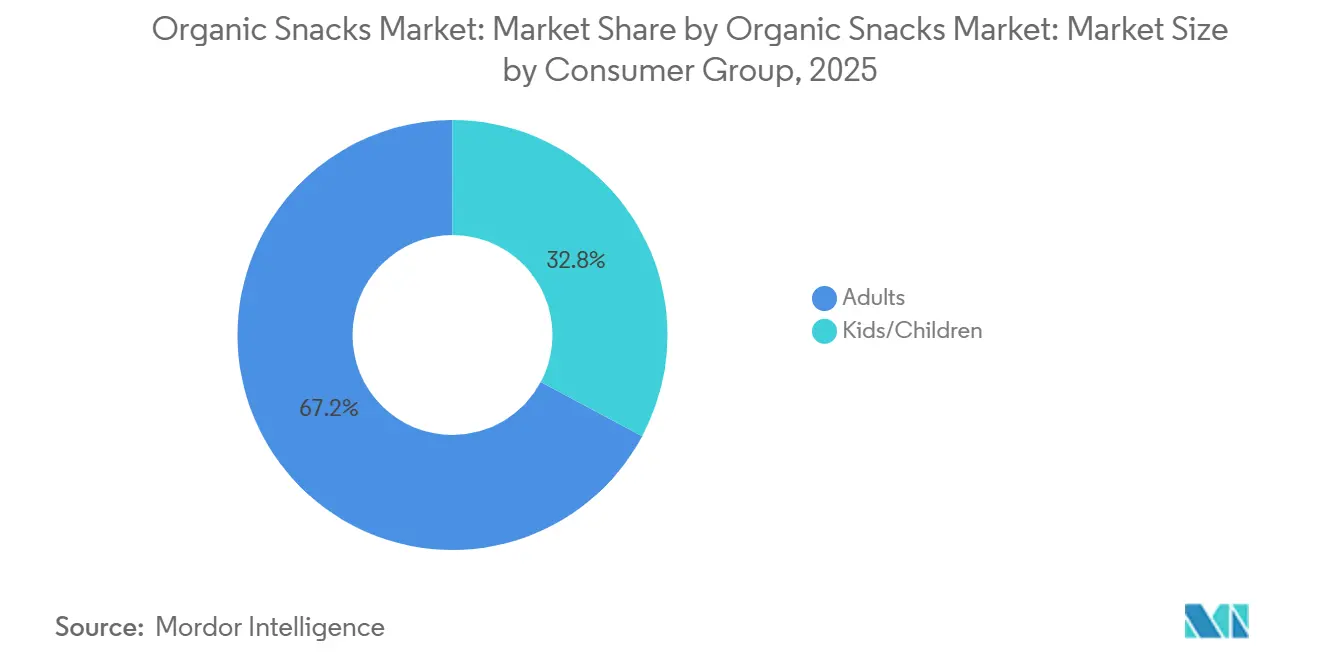

- By consumer group, Adults represented 67.2% of 2025 revenue, while Kids and Children is expected to record the highest CAGR at 9.6% through 2031.

- By distribution channel, Supermarkets and Hypermarkets captured 35.5% of 2025 revenue, while Online Retail Stores is set to grow at 9.8% CAGR during 2026-2031.

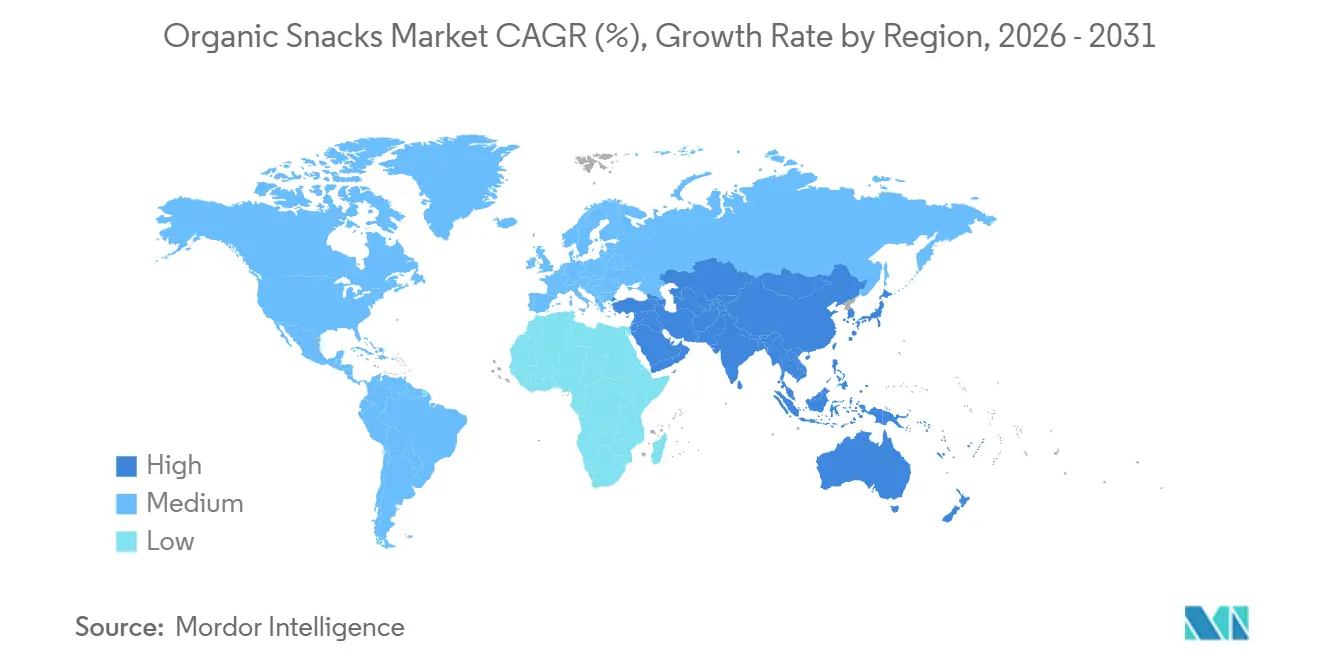

- By geography, North America held 38.1% of the 2025 revenue base, while Asia-Pacific is projected to register the fastest regional CAGR at 11.2% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Organic Snacks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-Led Trading Up Into Organic And Clean-Label Snacks | +1.3% | Global, led by North America and Europe, expanding to APAC urban centers | Medium term (2-4 years) |

| E-Commerce And Omnichannel Access Expansion | +0.8% | Global, with early gains in North America, APAC, and Western Europe | Short term (≤ 2 years) |

| Snackification Of Meals And On-The-Go Wellness | +1.0% | Global, strongest in North America and APAC, with spillover to MEA urban markets | Short term (≤ 2 years) |

| Premiumization Via Functional, Plant-Based, And High-Protein Formats | +0.9% | North America and Europe core, expanding to APAC premium segments | Medium term (2-4 years) |

| Regenerative And Traceable Sourcing As Conversion Lever | +0.6% | North America and Western Europe, nascent in APAC | Long term (≥ 4 years) |

| Private-Label Organic Snack Expansion Broadening Price Access | +0.5% | North America and Europe core, with spillover to APAC modern trade | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health-led trading up into organic and clean-label snacks

Ingredient transparency is accelerating the journey from awareness to purchase in the organic snacks market. Younger consumers are increasingly wary of synthetic pesticides, artificial dyes, and GMOs. As a result, certified organic labels and straightforward ingredient lists have become paramount in their snack choices. This shift reflects a growing preference for products that align with health-conscious and environmentally friendly lifestyles. Moreover, this heightened demand isn't confined to a single weekly grocery run; organic snacks are now being integrated into daily eating habits, such as mid-morning snacks, post-workout bites, and evening treats. The FDA's revamped definition of "healthy," effective from 2025, is steering food companies towards formulations that emphasize both health benefits and clearer ingredient transparency[2]Source: Food and Drug Administration, " Use of the 'Healthy' Claim on Food Labeling", fda.gov. This regulatory change is encouraging brands to innovate and reformulate their products to meet evolving consumer expectations. Consequently, in the organic snacks arena, mere certification is losing its shelf appeal. To remain competitive, brands must prioritize concise ingredient lists, prominent nutritional cues, and overall label clarity, ensuring they resonate with the informed and discerning modern consumer.

E-commerce and omnichannel access expansion

Digital retail has empowered smaller brands to reach consumers in the organic snacks market, reducing their reliance on traditional store listings. In Germany, organic products now account for 26% to 28% of purchases on online grocery platforms, indicating that digital channels have evolved from mere conveniences to integral parts of shopping habits. Direct-to-consumer subscriptions enhance demand forecasting and mitigate the risks associated with underperforming stock-keeping units. Following this trend, major players are making significant investments; for instance, Mars inaugurated a USD 240 million Nature’s Bakery facility in Salt Lake City in July 2025, aiming to ramp up production to meet growing brand demand. As online and brick-and-mortar retail converge, competition intensifies across premium, mainstream, and value segments in the organic snacks market, diminishing the exclusive edge that specialty organic brands once enjoyed in natural food outlets.

Snackification of meals and on-the-go wellness

Across both developed and rapidly growing economies, the organic snacks market is thriving as consumers transition from fixed meals to multiple daily eating occasions. Today's consumers are leaning towards portable foods that are lighter, easier to portion, and fit seamlessly into their work, travel, and on-the-go lifestyles. This shift favors products that strike a balance between indulgence and practical nutrition, including bars, crackers, crisps, and bite-sized bakery items. Convenience has emerged as a significant value driver, leading to snack formats capturing spending that traditionally went to formal meals. Additionally, the growing awareness of health and wellness has further amplified the demand for organic snacks, as consumers increasingly prioritize clean-label products free from artificial additives. This trend is particularly pivotal in the organic snacks market, as it legitimizes premium pricing when consumers perceive these snacks as functional substitutes for small meals. Consequently, this has broadened the demand base, bolstering both everyday purchases and higher-value niche formats.

Premiumization via functional, plant-based, and high-protein formats

In the organic snacks market, functional layering is carving out a premium segment. Ingredients like protein, fiber, probiotics, and plant-based components are enabling brands to transcend basic organic offerings, allowing them to command higher prices for added benefits. Functional layering not only enhances the nutritional profile of products but also aligns with evolving consumer preferences for health and wellness. Projections indicate that organic protein snack variants will grow at a robust 9.1% CAGR through 2031, outpacing the broader category. This growth reflects the increasing demand for snacks that combine convenience with functional benefits. In February 2025, Nature’s Path Foods debuted its Love Crunch Protein Granola, boasting 10 grams of pea protein per serving. Notably, the product was aimed at widespread retail distribution, moving beyond just natural channels to reach a broader audience. Opting for plant-based protein not only simplifies the complexities associated with animal-protein processing but also accelerates brands' entry into new product launches. Additionally, plant-based protein aligns with sustainability trends, appealing to environmentally conscious consumers. This strategy sustains the premiumization trend in the organic snacks market, even as consumers remain conscious of prices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Organic Price Premium Versus Conventional Snacks | -0.9% | Global, most acute in price-sensitive emerging markets and lower-income households in North America and Europe | Medium term (2-4 years) |

| Certified Organic Ingredient Scarcity And Co-Manufacturing Bottlenecks | -0.7% | Global, with structural severity in North America and Europe due to constrained certified farmland | Medium term (2-4 years) |

| EUDR And Farm-Level Traceability Burdens On Cocoa And Tropical Inputs | -0.5% | Europe core, with compliance cost spillover to North American exporters supplying EU-listed commodities | Short term (≤ 2 years) |

| Shelf-Life And Fragile Texture Constraints In Minimally Processed Formats | -0.4% | Global, particularly in hot and humid APAC markets, less acute in North America and Northern Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Organic price premium versus conventional snacks

Price remains the primary constraint on demand in the organic snacks market. The disparity between certified organic and conventional snacks significantly influences household purchasing behavior, including how frequently they buy, the variety of stock-keeping units they explore, and their likelihood of opting for cheaper alternatives when budgets tighten. This growth, supported by stable pricing and increased volume movement, highlights the ongoing value sensitivity, even in well-established organic markets. While private-label expansion is making organic snacks more accessible to a broader audience, it is also redefining the price ceiling for branded products. This is particularly challenging for brands that cannot convincingly demonstrate superior taste, enhanced functionality, or sustainable sourcing. Such dynamics are especially critical in the organic snacks market, where frequent purchases expose consumers to repeated price comparisons. In lower-income households and price-sensitive emerging markets, the premium pricing of organic snacks continues to limit the category's reach, thereby restricting its penetration and growth potential.

Certified organic ingredient scarcity and co-manufacturing bottlenecks

As demand for organic snacks surges, the supply side grapples with structural challenges. Certified farmland, specialized inputs, and compliant manufacturing capacities aren't keeping pace with the burgeoning demand. Furthermore, the number of facilities that can simultaneously meet organic certification and stringent food safety standards is limited compared to their conventional counterparts. This discrepancy not only extends lead times but also amplifies production risks, particularly for smaller brands. Highlighting the strategic value of manufacturing capacity, Hershey's acquisition of LesserEvil in November 2025 underscored the importance of both brand access and production capability. Additionally, the European Union's Deforestation Regulation (EUDR) mandates heightened traceability for cocoa and palm oil entering its borders by December 30, 2026[3]Source: European Commission, "Regulation (EU) 2023/1115", eur-lex.europa.eu. This requirement, set by the European Commission, imposes additional compliance burdens on brands that use these tropical inputs. Managing shelf-life and texture in minimally processed formats poses challenges, especially in warmer, humid markets. This difficulty exacerbates waste and intensifies formulation pressures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Savory Volume Stays Largest While Bakery Gains Speed

In 2025, chips and crisps clinched the top spot in the organic snacks market, commanding a 28.3% share. Their dominance stems from deep-rooted consumer familiarity, impressive repeat purchase rates, and their ubiquitous presence in mainstream retail. The category's appeal spans a wide price spectrum, from basic kettle chips to upscale vegetable and seed-based crisps. This versatility not only solidifies chips and crisps as market mainstays but also ensures they thrive alongside emerging snack formats. Additionally, their ability to cater to diverse consumer preferences, including those seeking healthier options or indulgent treats, has further strengthened their position. Consequently, they remain pivotal to the category's growth, catering to both budget-conscious and premium consumers.

Bakery snacks are set to lead the pack, with projections indicating a robust 9% CAGR growth rate through 2031. This surge is fueled by a rising appetite for ancient-grain crackers, seed-infused biscuits, and clean-label, portion-controlled cookies. The segment skillfully marries indulgence with functional nutrition, especially with enticing protein and fiber claims. Innovative premium bakery snacks are attracting health-savvy consumers who prioritize both flavor and nutrition. Furthermore, the growing trend of on-the-go snacking and the increasing availability of bakery snacks in convenient formats are driving their popularity. This blend of health-centric positioning, product creativity, and convenience is propelling the bakery segment's ascent in the organic snacks arena.

By Packaging Type: Pouches Dominate While Secondary Formats Add Premium Options

In 2025, bags and pouches dominated the organic snacks market, capturing 55.3% of total revenue. Their versatility spans a range of products, from chips and nuts to dried fruits and bakery snacks. Health-conscious consumers appreciate the resealability of these packages, aligning with their on-the-go lifestyles and boosting convenience while minimizing waste. Additionally, the lightweight nature of bags and pouches makes them easy to transport and store, further enhancing their appeal. Furthermore, bags and pouches offer manufacturers and retailers both shelf efficiency and cost savings, as they require less material and space compared to rigid packaging formats. This blend of practicality and adaptability solidifies their central role in the organic snacks packaging landscape.

Cans are set to emerge as the fastest-growing packaging format, with a projected CAGR of 8.1% through 2031. Their premium appeal, coupled with enhanced product protection and a heightened perception of freshness, especially for nuts, crisps, and functional snack mixes, fuels this growth. Canisters, with their upscale presentation, are not only popular for pantry stocking but also for gifting. The durability of cans also ensures better protection during transportation, reducing the risk of product damage. Concurrently, a heightened emphasis on sustainability, particularly in Northern Europe, is driving innovations across all packaging types. This includes a push for recyclable and compostable solutions, transforming packaging into a pivotal product-differentiation tool rather than a mere functional afterthought.

By Consumer Group: Adults Hold the Base While Kids Drive the Faster Growth Curve

In 2025, adults led the organic snacks market, capturing 67.2% of total revenue. Their dominance stems from increased disposable incomes, a growing familiarity with organic products, and a trend of snacking during work, travel, and fitness. Adults are now on the lookout for multiple benefits in their snacks, such as high protein, reduced sugar, gut health advantages, and straightforward ingredients. These preferences reflect a broader shift toward health-conscious and functional eating habits, where consumers prioritize both nutritional value and ingredient transparency. Additionally, the demand for clean-label products aligns with the growing awareness of the long-term health impacts of processed foods. These shifting preferences not only complicate product formulations but also justify premium pricing. Consequently, adults remain the cornerstone of both demand and value growth in the organic snacks arena.

Meanwhile, the segment of kids and children is set to be the market's fastest-growing demographic, with an anticipated CAGR of 9.6% extending to 2031. This surge is largely attributed to parents prioritizing allergen-free, school-appropriate, and certified organic snacks that align with heightened safety and nutritional standards. In markets like the U.S., there's a heightened scrutiny on artificial additives, further driving the demand for purer products for children. In response, brands are adopting a strategy of using common base formulations for both adult and child products, but tweaking packaging and portion sizes for cost efficiency. This approach allows manufacturers to cater to the wellness-centric demands of adults and the safety-conscious preferences of parents, all while broadening their innovation scope for various consumption moments.

By Distribution Channel: Physical Retail Keeps Scale While Online Builds the Growth Edge

In 2025, supermarkets and hypermarkets dominated the organic snacks market, capturing 35.5% of total revenue. These outlets remain the go-to destination for household shopping, enabling consumers to discover brands, compare prices, and make informed purchases. Their prominence is bolstered by strong shelf visibility, frequent promotions, and an expanding range of private-label programs. Supermarkets and hypermarkets also benefit from their ability to cater to a wide demographic, offering convenience and accessibility to urban and suburban consumers alike. Additionally, their established supply chain networks and partnerships with organic snack manufacturers ensure consistent product availability. Consequently, these channels play a pivotal role in driving volume sales and enhancing brand visibility in the organic snacks arena.

Online retail stores are set to emerge as the fastest-growing channel, with a projected CAGR of 9.8% through 2031. This growth is fueled by subscription models, bundled offerings, and compelling brand narratives that boost repeat purchases. Digital platforms excel in promoting organic products, evident in markets like Germany, where a significant portion of online grocery baskets comprises organic items. Moreover, online retail offers brands a unique opportunity to engage directly with consumers, highlighting product differentiation. As e-commerce gains traction, online retail is solidifying its position as a key growth driver for the organic snacks market.

Geography Analysis

In 2025, North America dominated the organic snacks market, accounting for 38.1% of the market. The U.S. led the charge, boasting organic sales of USD 76.6 billion and a robust 6.8% growth. This growth rate was more than double the conventional food market's 3.4% increase, underscoring the region's mainstream acceptance of organic products. North America's prominence in the organic snacks arena is bolstered by its mature retail infrastructure, widespread label recognition, and a robust mix of natural and mass retail outlets. The region benefits from a well-established supply chain that ensures consistent availability of organic products, further driving consumer trust and repeat purchases. While Canada bolsters the region with its organic-centric brands expanding into the U.S., Mexico is broadening the market's reach through modern trade, introducing organic snacks to a wider audience and increasing accessibility.

Europe is the second-largest player in the organic snacks market, buoyed by established regulations and deep-rooted consumer trust in certified labels. Germany's organic food market saw a 6.7% year-on-year (YoY) growth. Supermarkets, by expanding their assortments, ensured organic products became a staple in routine shopping. Additionally, the region's focus on sustainability and eco-friendly practices aligns with consumer preferences, further strengthening the organic snacks market. With the EUDR set to fully enforce traceability demands for cocoa and palm oil in organic snacks by December 30, 2026, Europe remains a lucrative market. However, this also underscores the need for stringent compliance and disciplined sourcing to ensure profitable growth. Companies operating in the region are expected to invest in transparent supply chains and certifications to meet these evolving regulatory requirements.

Asia-Pacific is emerging as the fastest-growing region in the organic snacks market, with projections of an 11.2% CAGR through 2031. Factors such as rising disposable incomes, heightened urban health awareness, and a digital-first distribution approach are driving demand in nations like China, India, South Korea, and Indonesia. The region's growing middle class and increasing penetration of e-commerce platforms are further accelerating the adoption of organic snacks. Japan, with its emphasis on traceability and premium quality, stands out as a high-value market, ensuring repeat purchases. While South America and the Middle East and Africa currently hold a smaller share, nations like Brazil, Argentina, and South Africa are steadily expanding their consumer bases, thanks to modern retail advancements and growing urban affluence. These regions are also witnessing increased promotional activities and awareness campaigns, which are educating consumers about the benefits of organic snacks. This landscape paints a clear picture: North America and Europe showcase mature demand, while Asia-Pacific and select emerging urban markets are on a rapid ascent.

Competitive Landscape

The organic snacks market remains moderately fragmented, with specialists and large food companies competing across overlapping usage occasions and price bands. Nature’s Path Foods, MadeGood, LesserEvil, Rhythm Superfoods, Annie’s, and retailer private labels all compete for space in the same broad shelf set. While larger companies leverage their manufacturing scale and extensive distribution networks, specialist brands carve out their niche through cleaner brand positioning, compelling sourcing narratives, and faster product cycles. This dynamic not only keeps switching costs low for consumers but also ensures a competitive landscape where no single entity holds sway over the organic snacks market.

In a strategic move, The Hershey Company finalized its acquisition of LesserEvil in November 2025, bolstering its foothold in the certified organic popcorn and puffs segment and enhancing its organic manufacturing capabilities. Meanwhile, Mars inaugurated a USD 240 million Nature’s Bakery facility in Salt Lake City in July 2025, marking a significant milestone in its broader USD 2 billion U.S. manufacturing commitment, which extends through 2026. Additionally, Hain Celestial divested its North American snacks division to Snackruptors in March 2026, sealing the deal at USD 115 million. These strategic maneuvers underscore the diverse strategies at play: some companies are amplifying their capacities, others are making acquisitions, and a few are divesting from non-core snack assets.

Retailers are taking a more hands-on approach in the organic snacks arena, especially as private-label offerings gain traction in mainstream grocery and club channels. This expansion not only narrows the price disparity for consumers but also elevates the standards for branded suppliers aiming to maintain their premium margins. Notably, there's a significant opportunity in functional adult snacks, allergy-conscious products for children, and offerings that emphasize traceability or regenerative practices backed by credible sourcing claims. Brands that successfully merge a reliable certified supply with robust repeat-purchase metrics are poised to secure and retain coveted listings. Given these dynamics, the organic snacks market is set to remain fiercely competitive through 2031, with growth leaning towards companies adept at balancing certification rigor, pricing strategies, and distinct product positioning.

Organic Snacks Industry Leaders

-

Mars Incorporated

-

General Mills, Inc

-

The Hain Celestial Group

-

Nature's Path Foods

-

Made In Nature

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Earth’s Best launched a new nationwide organic snack line for children aged 4 to 8, featuring Crispy Sticks and Veggie Waves, now available at major retailers like Target and Walmart.

- March 2026: Frankie’s Organic Snacks launched its Organic Puffcorn Variety Pack as part of its first major national retail expansion in the U.S., making it available in over 600 Sam’s Club locations nationwide.

- June 2025: Calbee America launched Weston’s Family Farms organic potato chips, expanding its organic snack portfolio with USDA-certified, gluten-free, non-GMO chips made from single-source potatoes.

- April 2025: That’s it. launched Organic Fruit Crunchables, a clean-label toddler snack made with 100% real fruit and just one to two ingredients. The product, free from added sugar, juices, purees, concentrates, and artificial additives, debuted nationwide at Walmart, with availability also at Sam’s Club and online.

Global Organic Snacks Market Report Scope

A snack is a small portion of food eaten between meals. The scope of the report includes organic certified snacks. Snacks come in various forms and shapes, including packaged snack foods and other processed foods.

The organic snacks market is segmented by product type into frozen snacks, chips and crisps, fruit snacks, confectionery snacks, bakery snacks, meat snacks, and others. By packaging type, the market is segmented into bags/pouches, cans, and others. By consumer group, the market is segmented into adults and kids/children. Based on distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other retail stores. Also, the report offers a detailed analysis of major economies across North America, Europe, Asia-Pacific, South America and Middle East, and Africa.

| Frozen Snacks |

| Chips and Crisps |

| Fruit Snacks |

| Confectionery Snacks |

| Bakery Snacks |

| Meat Snacks |

| Others |

| Bags/Pouches |

| Cans |

| Others |

| Adults |

| Kids/Children |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Frozen Snacks | |

| Chips and Crisps | ||

| Fruit Snacks | ||

| Confectionery Snacks | ||

| Bakery Snacks | ||

| Meat Snacks | ||

| Others | ||

| By Packaging Type | Bags/Pouches | |

| Cans | ||

| Others | ||

| By Consumer Group | Adults | |

| Kids/Children | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the organic snacks space?

The organic snacks market stood at USD 15.1 billion in 2025 and is estimated at USD 15.9 billion in 2026, with forecasts reaching USD 20.6 billion by 2031 at a 5.3% CAGR.

Which region leads global revenue and which region is growing the fastest?

North America led with 38.1% of 2025 revenue, while Asia-Pacific is projected to record the fastest growth at 11.2% CAGR through 2031.

Which product category leads sales in organic snacking?

Chips and Crisps held the largest share at 28.3% in 2025, which shows that savory formats still define the largest demand pool.

What is the fastest-growing product type through 2031?

Bakery Snacks is projected to grow at 9% CAGR, supported by premium crackers, seed-based products, and portion-controlled clean-label formats.

Page last updated on: