Natural Skin Care Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

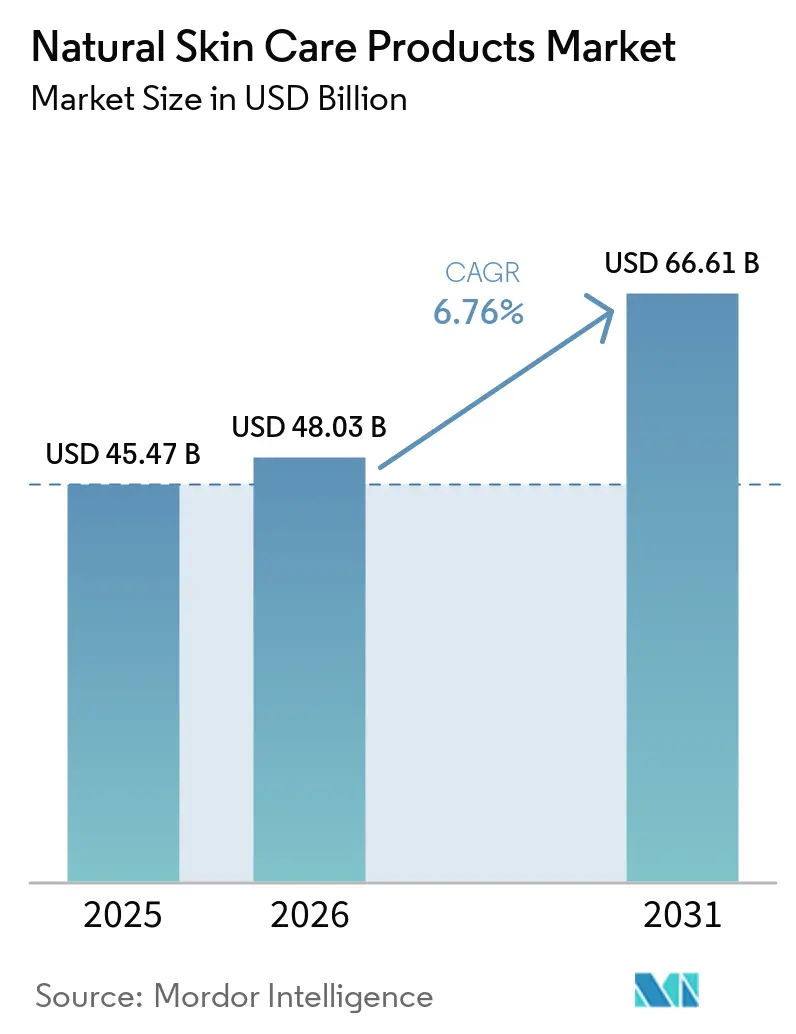

| Market Size (2026) | USD 48.03 Billion |

| Market Size (2031) | USD 66.61 Billion |

| Growth Rate (2026 - 2031) | 6.76% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Natural Skin Care Products Market Analysis by Mordor Intelligence

The natural skin care products market size is projected to expand from USD 45.5 billion in 2025 and USD 48 billion in 2026 to USD 66.6 billion by 2031, registering a CAGR of 6.8% between 2026 and 2031. The natural skin care products market is growing because ingredient scrutiny has become a mainstream buying habit, and consumers now check for the absence of petrochemical-derived compounds before purchase. Tighter claim standards in Europe are reinforcing this shift, and they are making it harder for brands to market products as natural without proof. The natural skin care products market is also gaining from premium routine building, where buyers are willing to pay more for certified formulas, traceable sourcing, and stronger efficacy positioning. At the same time, digital-first selling models are widening access for newer brands and changing how discovery happens across the natural skin care products market. Cost pressure remains a real constraint because botanical supply volatility, reformulation needs, and the higher stability burden of natural preservative systems still weigh on margins across the natural skin care products market.

Key Report Takeaways

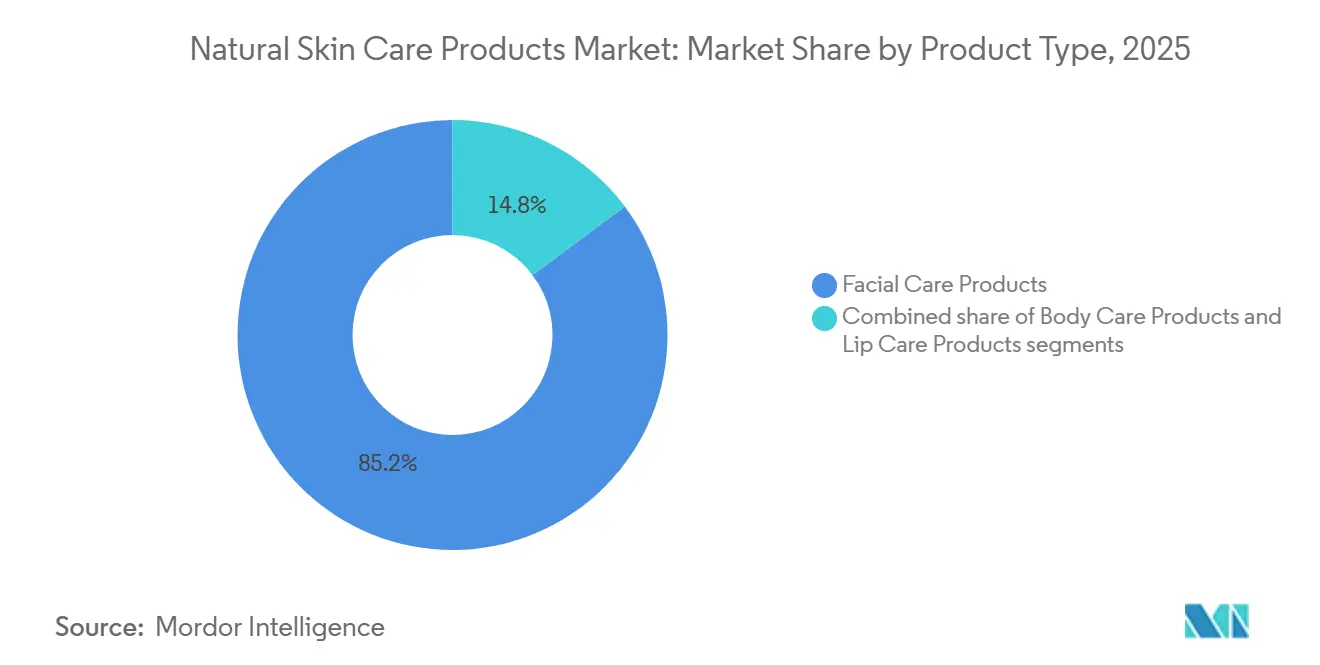

- By product type, facial care products accounted for the largest share of the skincare market, at 85.2% in 2025, and are projected to grow at a CAGR of 7.3% through 2031.

- By category, mass products accounted for the largest share of the skincare market, at 53.5% in 2025, while luxury or premium products are projected to grow at the fastest CAGR of 8.1% during 2026-2031.

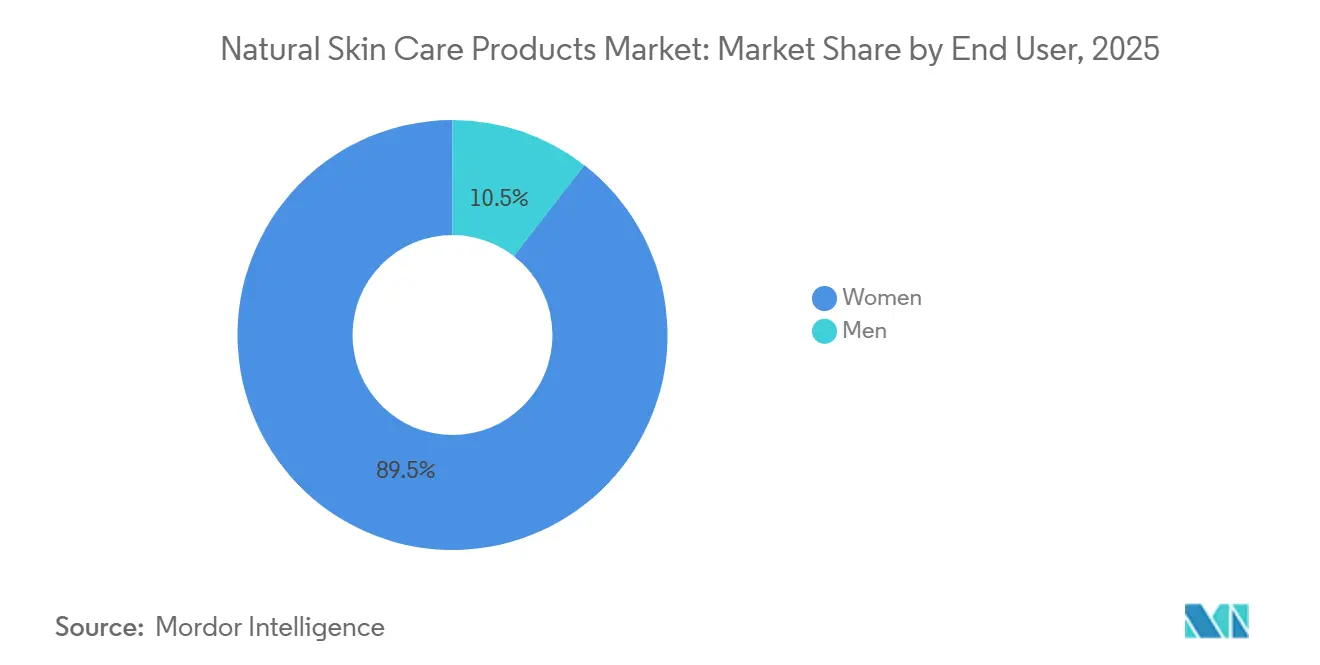

- By end user, women accounted for the largest share of the skincare market, at 89.3% in 2025, while men are projected to grow at the fastest CAGR of 8.3% during 2026-2031.

- By distribution channel, health and beauty stores accounted for the largest share of the skincare market, at 35.1% in 2025, while online retail stores are projected to grow at the fastest CAGR of 7.5% during 2026-2031.

- By geography, Asia-Pacific accounted for the largest share of the skincare market, at 37.4% in 2025, and is projected to grow at a CAGR of 7.8% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Natural Skin Care Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Demand for Chemical-Free Skin Care | +2.1% | Global: highest intensity in North America, Europe, and East Asia | Short term (≤ 2 years) |

| Expansion of Clean Beauty Retail and E-Commerce Channels | +1.4% | Global, accelerating gains in APAC and South America | Medium term (2–4 years) |

| Premiumization of Natural and Organic Skin Care Routines | +1.2% | North America, Europe, China; spill-over to the United Arab Emirates and South Korea | Medium term (2–4 years) |

| Ingredient Transparency and Label-Trust Requirements | +0.7% | Europe, North America, Australia | Medium term (2–4 years) |

| Microbiome-Friendly and Sensitive-Skin Positioning | +0.5% | North America, the United Kingdom, Japan, and South Korea | Long term (≥ 4 years) |

| Regulatory Push Against Undisclosed Synthetic Additives | +0.4% | Europe core; spill-over to the Asia-Pacific and Middle East, and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer demand for chemical-free skin care

Millennials and Gen Z, now the dominant forces in global beauty spending, have transitioned from casually avoiding certain synthetic compounds to making it a primary filter in their purchases. These compounds include parabens, phthalates, formaldehyde-releasing preservatives, and synthetic fragrances. However, not all natural product categories enjoy the same level of demand. For instance, formulations that credibly tout a "chemical-free" label and back it with clinical mechanisms, like a ceramide-rich botanical serum referencing peer-reviewed skin barrier science, see significantly higher repeat purchase rates than those that merely list ingredients. In 2025, NATRUE highlighted the rapid ascent of men's natural skincare as one of the industry's fastest-growing sub-segments. This trend is self-perpetuating: as brands become more transparent, consumers engage in comparison shopping. This heightened scrutiny on synthetic alternatives complicates matters for conventional brands, making it challenging to retain customers who've transitioned to verified-natural products. Moreover, brands that secure dermatologist endorsements and present published clinical evidence are carving out robust competitive advantages, especially in the lucrative facial care market.

Premiumization of natural and organic skin care routines

As the organic and luxury skincare categories converge, a new premium-natural segment emerges, where certification integrity increasingly dictates pricing power, overshadowing traditional brand heritage. Weleda AG's 2025 annual results underscore this trend: the company celebrated a record turnover with a 9.2% sales growth, buoyed by the October 2025 debut of its premium face care line, Cell Longevity, and the Booster Drops serum range, which clinched the title of the year's top skincare launch in Germany[1]Source: “2025 Annual Results and 2026 Product Launch Updates,” Weleda, weleda.com. Notably, Weleda also highlighted a significant leap in its sustainability efforts: recycled primary packaging in its natural cosmetics surged to 77% in 2025, up from 65% the previous year. This shift underscores that in the premium-natural segment, sustainability is now a baseline expectation rather than a distinguishing feature. Continuing this trajectory, Weleda made waves in the UV protection arena with its UV Glow Fluid launch in Q1 2026, mirroring the robust growth of 2025. This momentum suggests that the push towards premiumization in the natural category is not a fleeting trend but a sustained movement. Meanwhile, brands attempting to carve a niche in the luxury skincare realm, yet lacking verifiable supply chain traceability and endorsements from third-party certifiers like NATRUE, COSMOS, or USDA Organic, find themselves grappling with regulatory challenges and consumer doubts, jeopardizing their desired pricing premiums.

Expansion of clean beauty retail and e-commerce channels

Natural skincare's shift towards e-commerce and direct-to-consumer (DTC) channels is reshaping the landscape, challenging traditional retail dynamics. L'Oréal's June 2026 move to acquire a majority stake in Innovist, known for its clean brands Bare Anatomy and Chemist at Play, highlights this trend. These brands, primarily selling through D2C and e-commerce platforms in India, signal how multinationals are pivoting to harness the digital-first natural beauty boom. In a significant regulatory shift, South Korea's MFDS, as of August 1, 2025, scrapped its government certification for natural cosmetics[2]Source: “Abolition of Government Certification System for Natural and Organic Cosmetics,” Ministry of Food and Drug Safety, mfds.go.kr. Now, the onus of "natural" claims lies with e-commerce listings, allowing for tighter regulatory oversight than traditional sales points. This evolution is diminishing the edge that health and beauty specialty stores once enjoyed in product discovery. AI-driven skin assessment tools on DTC platforms are enhancing product matching, leveling the playing field. However, regional nuances persist: while Germany and France uphold pharmacy-based skincare counseling, India's rapid adoption of premium natural products is fueled by swift quick-commerce deliveries, sometimes in under 10 minutes. Brands merging DTC data insights with selective specialty retail are reaping the rewards, showcasing enhanced customer lifetime value metrics.

Microbiome-friendly and sensitive-skin positioning

As the skin microbiome gains traction, both consumers and dermatologists are shifting their focus from "anti-bacterial" to "microbiome-supportive" formulations. This shift in perspective offers a structural advantage to natural skincare brands. Central to these microbiome-targeted formulations are probiotic and prebiotic actives. These actives, primarily derived from fermentation or plants, bolster the brands' natural claims. Notably, they sidestep the intricate agricultural supply chain challenges faced by traditional botanical materials. In April 2026, South Korea's MFDS rolled out a Cosmetic Safety Assessment Support Program. This initiative, aimed at 1,500 small and medium-sized enterprises, prepares them for mandatory safety assessments set to begin in 2028. This compliance framework gives an edge to formulations that are microbiome-tested and clinically validated, overshadowing those that lean on generic ingredient-origin claims. Japan presents a unique regulatory twist: while the nation boasts a JAS certification for food, it lacks a legal definition of "organic" for cosmetics. This ambiguity in "organic" labeling amplifies the credibility of COSMOS-certified microbiome products, which benefit from independent third-party verification. A significant and expanding demographic, the sensitive-skin sub-population, is increasingly influenced by urban pollution and lifestyle stressors. This group is particularly receptive to microbiome-supportive claims, often willing to pay a premium for dermatologically validated formulations. Brands that champion human microbiome clinical trials and publicize their findings are crafting a unique competitive edge, one that transcends mere ingredient transparency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Stability and Shelf-Life Constraints Versus Conventional Formulations | -0.4% | Global; acute in high-humidity markets across APAC and South America | Short term (≤ 2 years) |

| Ingredient Traceability and Certification Costs | -0.3% | Global, with the highest burden on SMEs in North America and Europe | Medium term (2–4 years) |

| Counterfeit, Greenwashing, and Brand-Trust Risk | -0.3% | Asia-Pacific and Middle East and Africa; growing in South America | Medium term (2–4 years) |

| Supply Volatility in Botanicals and Natural Actives | -0.4% | Global sourcing regions in Eastern Europe, Southeast Asia, and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher stability and shelf-life constraints versus conventional formulations

Natural preservation systems like rosemary extract, vitamin E, and fermented actives face formulation challenges due to their inherent instability compared to parabens or phenoxyethanol. This instability is particularly pronounced in water-based formulations, such as toners and hydrating serums. Under ambient storage, these natural products risk microbial contamination, potentially shortening their shelf life to 12–18 months, while conventionally preserved items can last 24–36 months. As a result, natural skincare brands grapple with tough choices: accept the higher risk of a shorter shelf life, invest in more complex waterless or anhydrous formulations, or pivot to biotechnology-derived preservatives, each with its own certification and supply chain challenges. The financial stakes are heightened by MoCRA's recall framework. According to draft guidance from December 18, 2025, brands are primarily liable for adulteration, meaning a widespread stability failure could have dire regulatory and reputational repercussions. Meanwhile, established players with robust research and development teams are pulling ahead of indie brands, hinting at mounting consolidation pressures in the water-based natural product segment.

Supply volatility in botanicals and natural actives

Unlike synthetic ingredient supply chains, the botanical supply chain faces mounting threats from climate disruptions, geopolitical conflicts, and agricultural cycles. In 2024-2025, Ukraine and Russia, major players in global sunflower oil production, faced disruptions due to conflict. This oil, a popular natural emollient in skin formulations, saw persistent shortages and price hikes, pressuring brands to reformulate. The Union for Ethical BioTrade (UEBT) highlighted in its 2025 report that biodiversity loss in traditional sourcing regions is worsening climate-driven harvest inconsistencies[3]Source: “Resilience Rooted in Nature Report,” Union for Ethical BioTrade, uebt.org. This reality pushes brands to forge long-term partnerships with farmers and diversify their sourcing strategies, moving away from mere spot procurement. The EU Deforestation Regulation imposes additional compliance costs on suppliers sourcing from regions at high risk of deforestation. This regulation poses challenges for small-scale producers lacking documentation and shrinks the certified supply of essential ingredients. Brands like Forest Essentials, with a locally integrated Ayurvedic ingredient network, have seen their value soar. Their supply resilience, showcased by The Estée Lauder Companies' full acquisition in March 2026, is now as prized as their brand equity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Facial Care Dominance Anchors Formulation Innovation

In 2025, Facial Care Products dominated the revenue landscape, commanding a significant 85.21% share. This dominance underscores the pivotal role facial skincare plays in shaping a brand's scientific credibility and pricing strategy. Within the Facial Care realm, not all sub-categories exhibit the same dynamism. Cleansers and moisturizers cater to a high-volume, moderately premium audience. In contrast, serums and essences, where consumers are willing to pay a premium per milliliter, emerge as the forefront of ingredient innovation. Weleda, a brand with a century-old legacy, made headlines in April 2026 by unveiling its first face serums in over a hundred years. The Serum Booster Drops collection, featuring six variants focused on hydration, vitamin C, anti-aging, and radiance, underscores the brand's strategic pivot towards premium-natural positioning. Meanwhile, toners and face masks serve as crucial discovery tools, facilitating trials for emerging natural brands, especially via online retail platforms.

Body Care Products, which include body lotions, foot and hand creams, and other formats, currently hold a smaller market share. However, they're witnessing growth as consumers increasingly adopt natural formulation standards beyond just facial products. Lip Care Products are buzzing with innovation. In February 2026, Burt's Bees ventured into the lip oil segment, harnessing jojoba, sweet almond, and meadowfoam seed oils. This move not only underscores the brand's commitment to its natural heritage but also its adaptability to trend-driven formats, now available at major retailers like Target, Amazon, Walmart, and CVS Pharmacy. Looking ahead, the Facial Care Products segment is projected to grow at a robust 7.31% CAGR through 2031, outpacing the overall market's 6.76% growth rate. This trend highlights the industry's continued investment in clinically validated botanical actives, especially as the serum and essence sub-categories reach maturity.

By Category: Mass Holds Volume, Luxury/Premium Claims the Growth

In 2025, the Mass category dominated, capturing 53.54% of total category revenue, underscoring its pivotal role as the go-to choice for consumers seeking easily accessible natural skincare through widespread retail channels. The natural skincare landscape showcases two distinct growth trajectories: mass formats, buoyed by price accessibility, and the Luxury/Premium tier, where the allure lies in certification credibility and ingredient traceability, ensuring robust pricing power. L'Occitane en Provence's April 2026 comeback of its Amande Sublime collection, now boasting 97% natural-origin ingredients, fully biodegradable components, and a refillable format, underscores how legacy brands are bolstering their natural credentials to fend off competition from purer-positioned indie rivals.

Projected to expand at an 8.12% CAGR until 2031, the Luxury/Premium segment is set to outpace both the Mass category and the broader market. While consumers loyal to natural formulations are eager to invest more for verified organic certifications and heightened bioactive concentrations, their expectations are climbing. Under EU Regulation No 655/2013, claims of "natural" in cosmetics must be substantiated, elevating the compliance bar for all premium-tier brands in Europe. Meanwhile, in markets like the United States, the United Kingdom, Germany, and Japan, brands lacking COSMOS or NATRUE certification are grappling to maintain premium pricing as consumer awareness sharpens.

By End User: Women Lead, Men Accelerate

In 2025, women accounted for a dominant 89.32% of end-user revenue, underscoring the historical trend where brands, marketing strategies, and retail setups predominantly catered to female consumers. Forecasts indicate that the Men's segment will lead all end-user categories with an 8.33% CAGR through 2031. This surge is attributed to a cultural shift linking male skincare to themes of wellbeing, sustainability, and personal authenticity. Furthermore, as societal grooming taboos fade, the global men's facial skincare market witnesses a notable uptick, especially with Gen Z men gravitating towards natural formulations for oil control, sensitivity, and post-shave care.

This burgeoning interest in men's skincare is reshaping formulation trends. There's a rising demand for lighter textures, non-greasy finishes, and multifunctional products, think moisturizer-SPF combos and cleanser-toner hybrids. These innovations stand in contrast to traditional female facial care offerings. Brands that craft men's skincare with a unique product architecture, rather than merely tweaking female-centric products, are carving out a stronghold in this burgeoning market. The strategic importance is undeniable: buying choices are heavily swayed by certifications like NATRUE or COSMOS and specific ingredient exclusions, marking it as the most certification-sensitive segment in the category.

By Distribution Channel: Specialty Retail Leads, Digital Commerce Accelerates

In 2025, Health and Beauty Stores commanded 35.13% of the distribution channel revenue, underscoring their pivotal role as the primary venue for discovering and trying natural skincare products. Here, elements like sensory evaluation, texture, scent, and skin feel play a crucial role in driving purchase decisions. Supermarkets and Hypermarkets cater to the mass market, facilitating volume distribution for well-established brands. Meanwhile, Other Channels, encompassing natural food retailers, pharmacies, and airport travel retail, target specific consumer segments. In Germany and France, pharmacy channels hold particular significance. Here, natural formulations, often positioned alongside dermatological solutions, command a credibility premium that's hard to find in broader grocery settings.

Online Retail Stores are projected to lead the pack, with a forecasted growth rate of 7.51% CAGR through 2031. This surge is attributed to the rise of DTC brand architectures, the discovery potential of social commerce, and AI-driven skin assessment tools, all of which are diminishing the once-dominant guided-selling edge of specialty retail. L'Oréal's strategic acquisition of Innovist in June 2026 was a clear nod to this trend. The acquisition zeroed in on Innovist's diverse channels, seamlessly blending D2C, e-commerce, quick commerce, and traditional retail. This move is seen as a blueprint for a digital-first approach to natural skincare distribution, especially in rapidly growing emerging markets. Furthermore, the merging of health and beauty specialty formats with pharmacy channels is birthing hybrid retail spaces. In these environments, natural skincare products are vying directly with clinical dermocosmetics for prime shelf space.

Geography Analysis

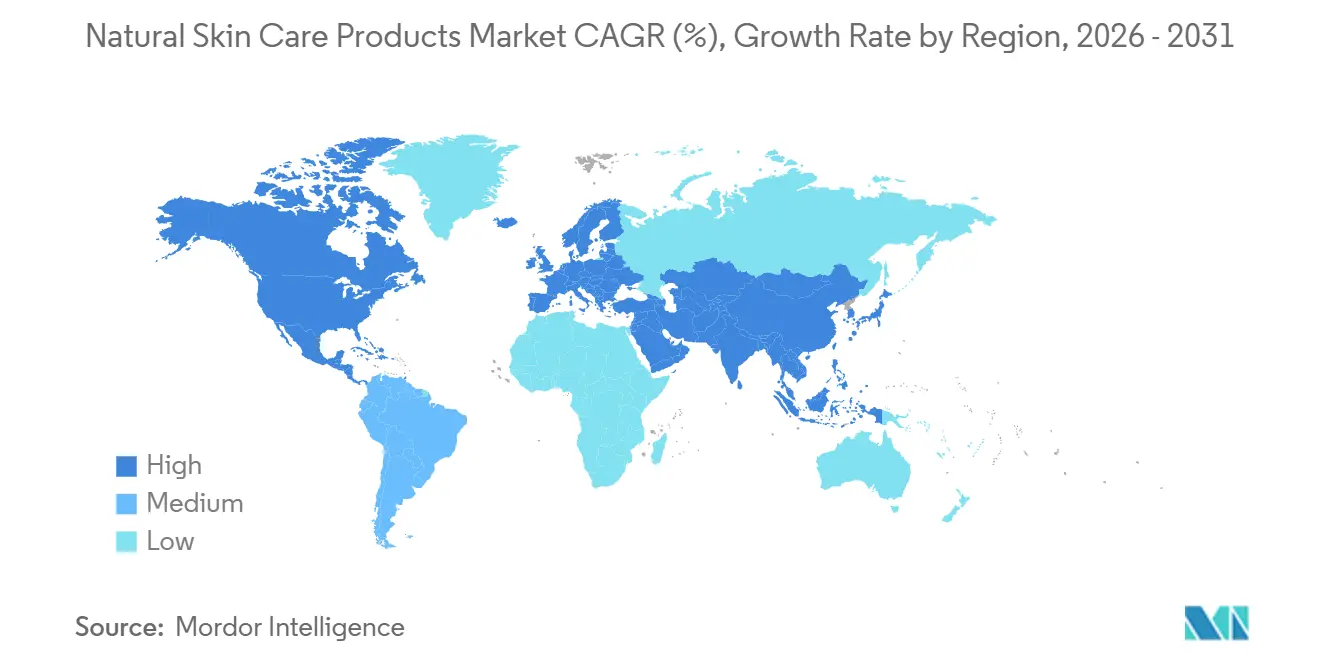

In 2025, Asia-Pacific commanded a dominant 37.4% share of the global revenue, solidifying its position as the leading market for natural skin care products. Forecasts predict Asia-Pacific will not only maintain its status as the largest regional market but also emerge as the fastest-growing, with an anticipated CAGR of 7.8% through 2031. China, bolstered by a growing demand for ingredient transparency and the emergence of digital-first local brands like Winona and Proya, stands as the region's primary revenue driver. Meanwhile, India is carving out a niche as the fastest-growing national market, both in Asia-Pacific and on the global stage. UEBT attributes this growth to India's pivotal role as a vertically integrated botanical sourcing hub, especially for Ayurvedic formulations. Reinforcing this perspective, The Estée Lauder Companies, in March 2026, took a significant step by acquiring full ownership of Forest Essentials, a prestigious natural skincare brand rooted in integrated Ayurvedic sourcing.

South Korea is reshaping the credibility landscape of the natural skin care products market. On August 1, 2025, the Ministry of Food and Drug Safety abolished its government certification system for natural and organic cosmetics. This pivotal shift placed the onus of disclosure squarely on brands. As a result, many companies are gravitating towards globally recognized standards like COSMOS and NATRUE, especially when marketing in Korea or using it as a benchmark for exports. Meanwhile, as consumer awareness deepens, smaller markets in the Asia-Pacific, such as Thailand, Singapore, Indonesia, and Australia, are also making strides. Indonesia, in 2026, introduced an added layer of compliance with mandatory halal certification for cosmetics, a move that resonates with the rising demand for cleaner ingredient profiles.

North America and Europe continue to wield significant influence over the regulatory and pricing dynamics of the natural skin care products market. Europe, in particular, holds a pivotal role: Germany, France, and the UK account for a substantial portion of the certified-organic demand. Germany's pharmacy-centric skincare culture further bolsters brands that meld botanical traditions with clinical credibility. The EU has tightened its grip on ingredient controls. Notably, in April 2026, Commission Regulation (EU) 2026/909 imposed new restrictions on certain cosmetic substances, amplifying the reformulation challenges for products reliant on synthetic fragrance systems. While South America, the Middle East, and Africa are still in the nascent stages, they hold significance in the market. Brazil, with Natura's Amazonian sourcing model, leads the charge in South America. In the Middle East, the UAE and Saudi Arabia blend luxury demand with preferences for halal formulations. Meanwhile, Africa's rich botanical offerings, from shea butter to baobab extract, present a long-term sourcing opportunity, allowing brands to fortify their local procurement capabilities.

Competitive Landscape

Multinational groups dominate the natural skin care products market, leveraging advantages in distribution, portfolio breadth, and research budgets. Yet, there's ample space for indie and DTC brands, which carve out their niche through ingredient transparency, deep certifications, and active community engagement. Major players like The Procter & Gamble Company, The Estée Lauder Companies, Unilever, and L'Oréal view natural skincare as a means to broaden their portfolios, rather than as a standalone venture. While this strategy bolsters their financial clout, it also introduces friction; traditional manufacturing and preservative methods often clash with the expectations of the natural skincare market. This discord underscores why acquisitions are a favored growth strategy.

In March 2026, The Estée Lauder Companies fully acquired Forest Essentials, highlighting a global beauty giant's strategy to tap into a trusted, established natural brand. Similarly, L'Oréal's June 2026 move to secure a majority stake in Innovist underscored a focus on digital distribution and India's burgeoning clean beauty market. Such maneuvers indicate that the natural skincare market values authenticity, a trait challenging to cultivate within traditional brand frameworks. Among established names, Weleda AG and WALA Heilmittel GmbH are recognized for their certification credibility and rich botanical heritage. Weleda's 2026 foray into premium serums and UV protection signals that heritage brands are venturing beyond niche markets into lucrative segments.

Emerging premium brands like Tata Harper Skincare, Herbivore Botanicals, True Botanicals, Pai Skincare, and KORA Organics are challenging industry giants with compelling ingredient narratives and a dedicated DTC following. Opportunities abound in men's natural skincare, certified-organic products for children, and microbiome-supportive formulas, with no dominant global player yet emerging. While gaining shelf access has become increasingly challenging, the natural skincare market remains receptive to new leaders. Success now hinges less on a brand's beauty legacy and more on proof of claims, resilient sourcing, disciplined marketing, and the capacity to foster trust across both digital and physical platforms.

Natural Skin Care Products Industry Leaders

The Procter & Gamble Company

Unilever PLC

The Estée Lauder Companies Inc.

L'Oréal S.A.

Weleda AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: L'Oréal acquired a majority stake in Innovist, an Indian digital-first personal care company whose brands, Bare Anatomy and Chemist at Play, are built on clean, transparent formulations. The deal marks a major step in L'Oréal's India expansion strategy and accelerates penetration of the country's fast-growing digital-first beauty market; transaction close is expected within months, pending regulatory approvals.

- April 2026: Weleda launched Serum Booster Drops and UV Glow Fluid: Weleda entered two new product categories, face serums and UV protection, maintaining the same high growth trajectory as 2025. The NATRUE-approved, vegan Serum Booster Drops target six distinct skin concerns and represent the brand's most significant portfolio expansion in a generation.

- March 2026: The Estée Lauder Companies acquired Forest Essentials (India): ELC agreed to acquire the remaining interests in India's top-ranked prestige natural skincare brand, building on a partnership dating to 2008 and a 49% stake held since 2020. Forest Essentials' vertically integrated Ayurvedic research and development, local botanical sourcing, and in-house manufacturing are central to the strategic rationale.

Global Natural Skin Care Products Market Report Scope

Natural skin care products are topical formulations made primarily from ingredients sourced from nature, such as plants, roots, flowers, essential oils, and minerals. The global natural skin care products market is segmented by product type, category, end user, distribution channel, and geography. By product type, the market is segmented into facial care products, body care products, and lip care products. The Facial care products segment is further sub-segmented into cleansers, moisturizers and creams, serums and essence, toners, face masks, and other facial care products. Similarly, the Body care products segment is further sub-segmented into body lotion, foot and hand cream, and other body care products. By category, the market is segmented into mass and luxury/premium. By end user, the market is segmented into men and women. By distribution channel, the market is segmented into supermarkets/hypermarkets, health and beauty stores, online retail stores, and other channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Facial Care Products | Cleansers |

| Moisturizers and creams | |

| Serums and Essence | |

| Toners | |

| Face Masks | |

| Other Facial Care Products | |

| Body Care Products | Body Lotion |

| Foot and Hand Cream | |

| Other Body Care Products | |

| Lip Care Products |

| Mass |

| Luxury/Premium |

| Men |

| Women |

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Facial Care Products | Cleansers |

| Moisturizers and creams | ||

| Serums and Essence | ||

| Toners | ||

| Face Masks | ||

| Other Facial Care Products | ||

| Body Care Products | Body Lotion | |

| Foot and Hand Cream | ||

| Other Body Care Products | ||

| Lip Care Products | ||

| Category | Mass | |

| Luxury/Premium | ||

| End User | Men | |

| Women | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Health and Beauty Stores | ||

| Online Retail Stores | ||

| Other Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current outlook for natural skin care products through 2031?

The natural skin care products market is projected to rise from USD 48 billion in 2026 to USD 66.6 billion by 2031 at a 6.8% CAGR. Growth is being supported by stronger ingredient scrutiny, premiumization, and wider digital reach.

Which region is leading global demand for natural skin care products?

Asia-Pacific led with 37.4% of global revenue in 2025 and is also forecast to post the fastest growth at 7.8% CAGR through 2031. China, India, and South Korea are central to that regional momentum.

Which product area is driving the most value in natural skincare?

Facial care is the core value pool, holding 85.2% of revenue in 2025 and growing at a 7.3% CAGR through 2031. Serums, moisturizers, and cleansers remain the main formats shaping premium positioning.

Why are premium natural formulations growing faster than mass offerings?

Luxury and premium products are projected to grow at an 8.1% CAGR because buyers are paying more for verified certifications, traceable sourcing, stronger bioactive positioning, and better sustainability credentials.

Page last updated on: