Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

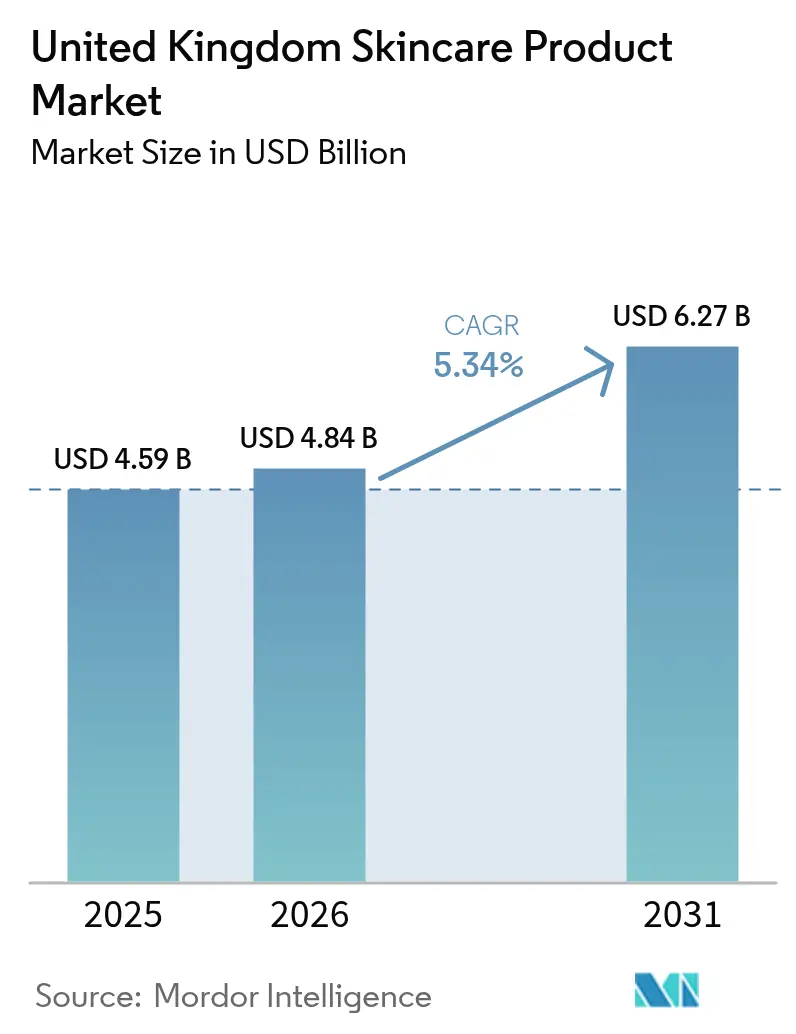

| Base Year Market Size (2025) | USD 4.59 Billion |

| Market Size (2026) | USD 4.84 Billion |

| Market Size (2031) | USD 6.27 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

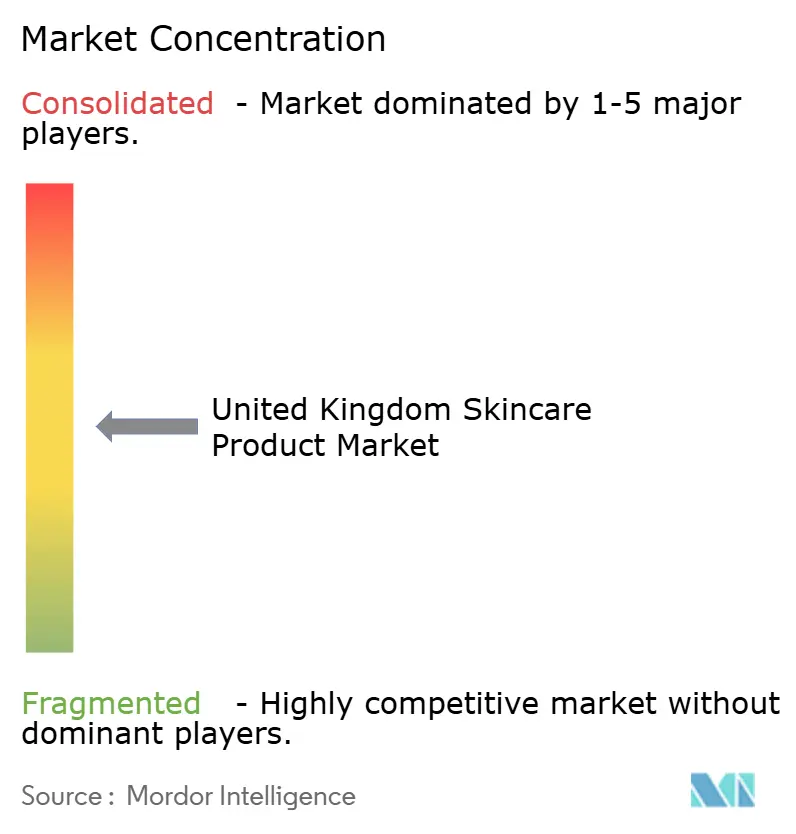

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Skincare Product Market Analysis by Mordor Intelligence

The United Kingdom skincare product market size is expected to grow from USD 4.59 billion in 2025 to USD 4.84 billion in 2026 and is forecast to reach USD 6.27 billion by 2031 at 5.34% CAGR over 2026-2031. Resilient consumer demand, expanding clean-beauty portfolios, and widespread integration of AI-powered personalization engines continue to reinforce market fundamentals. Facial care leads category expansion as anti-aging actives with clinical validation win consumer trust, while regulatory tightening post-Brexit is steering the industry toward higher ingredient safety standards. Premium players are outgrowing mass brands because efficacy-driven shoppers are willing to pay more for science-backed formulations, even in an inflationary environment. Online channels remain the fastest route to market, owing to data-rich purchase journeys that amplify shopper education and retention.

Key Report Takeaways

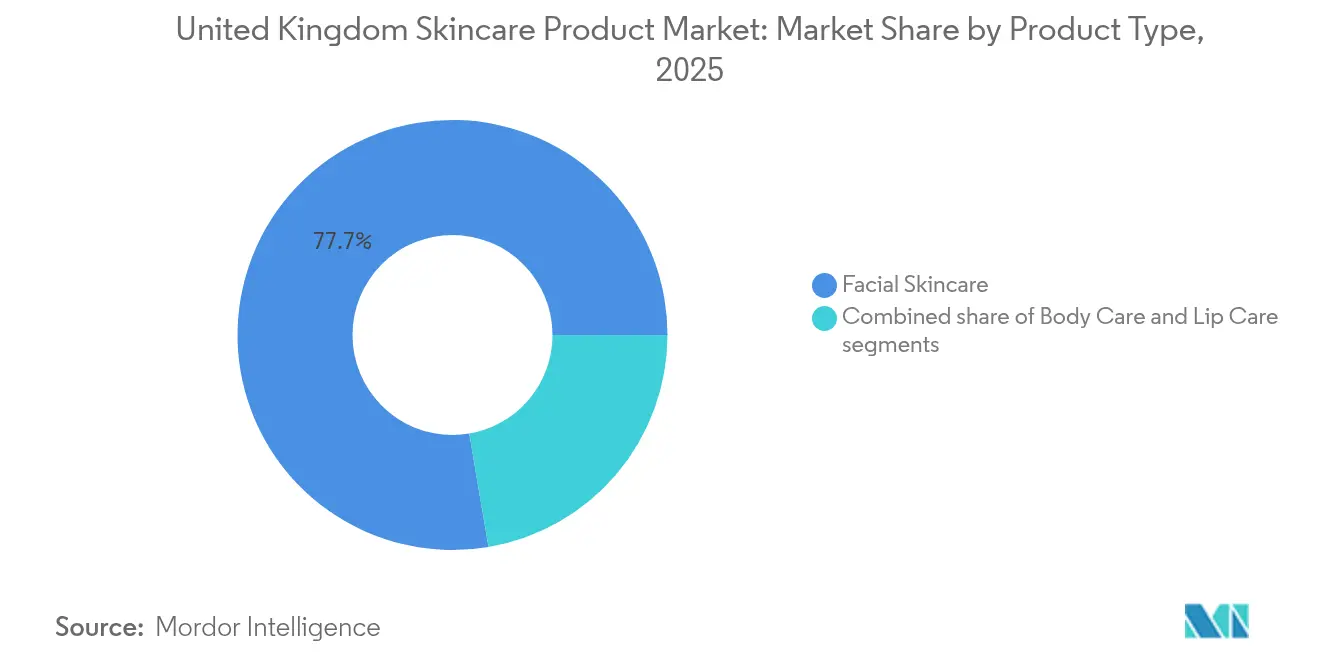

- By product type, facial care captured 77.68% of the United Kingdom skincare market share in 2025; the same segment is forecast to expand at a 5.74% CAGR through 2031.

- By category, the mass segment held 64.72% of the United Kingdom skincare market share in 2025, while the premium/luxury segment is projected to expand at a 6.29% CAGR through 2031.

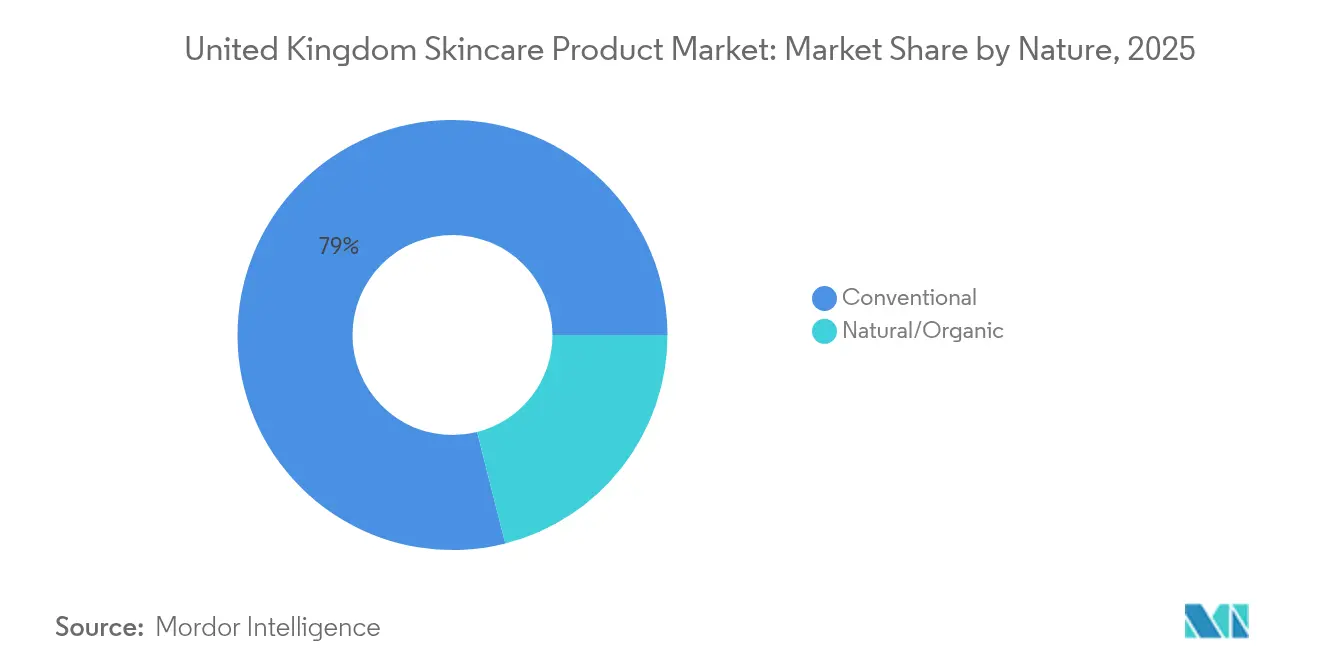

- By nature, conventional formulations retained 78.95% revenue share in 2025, yet the natural/organic segment is poised for the highest 6.82% CAGR through 2031.

- By distribution channel, online retail outlets held 45.12% revenue share in 2025 and are expected to advance at a 6.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Skincare Product Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased focus on skin health | +1.2% | England, Scotland, Wales, Northern Ireland | Medium term (2-4 years) |

| Growing demand for anti-ageing and dermatologist-backed claims | +1.0% | England primarily, expanding to Scotland and Wales | Long term (≥ 4 years) |

| Trend toward clean and sustainable skincare | +0.8% | England and Scotland leading, Wales and Northern Ireland following | Medium term (2-4 years) |

| Influence of social media and beauty influencers | +0.7% | England dominant, significant in Scotland | Short term (≤ 2 years) |

| Personalized skincare solutions owing to usage of advanced technologies | +0.6% | England and Scotland early adopters | Long term (≥ 4 years) |

| Dominance of specialty clinics offering targeted products | +0.5% | England concentrated, expanding to other regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increased focus on skin health

The focus in the United Kingdom skincare market is shifting from cosmetic enhancement to prioritizing skin health, driving changes in consumer expectations and product innovation. Avon’s Future of Beauty Report 2024 highlights that 97% of women now prioritize skincare for hydration and overall skin health over traditional anti-aging benefits, signaling a significant move towards a health-centric approach [1]Source: Avon Products, Inc, "Future of Beauty Report 2024", avonworldwide.com. This shift is fueling demand for dermatologist-formulated products and clinical-grade ingredients. Leading brands are responding by forming strategic collaborations, such as Boots and No7 Beauty Company, renewing their 20-year research partnership with the University of Manchester in April 2024 to support evidence-based formulations. Besides, younger consumers in the United Kingdom are adopting preventative skincare routines earlier, ensuring consistent demand for products that promote long-term skin health. Brands like CeraVe and Eucerin are leveraging this trend by focusing on dermatologist-approved ingredients that strengthen the skin barrier. Additionally, AI-driven tools are gaining traction, with Boots’ SmartSkin Checker achieving 95% diagnostic accuracy for skin conditions, enabling consumers to address specific skin health needs with precision. This evolution is anchoring product development in scientific validation, establishing efficacy, safety, and partnerships with medical research institutions as critical standards for market leadership in the skincare industry.

Growing demand for anti-ageing and dermatologist-backed claims

The skincare product market in the United Kingdom is increasingly focusing on anti-ageing innovations, driven by scientific advancements and a growing consumer demand for dermatologist-backed efficacy. L’Oréal's March 2024 launch of Melasyl, a groundbreaking ingredient developed over 18 years and backed by 121 scientific studies, underscores the industry's commitment to substantiated anti-ageing results, setting a new standard for evidence-based product development. This consumer demand for tangible clinical results is mirrored in the surging popularity of med spas throughout the United Kingdom. More individuals are opting for aesthetic procedures in regulated medical environments, highlighting a distinct preference for clinical expertise and safety over conventional beauty treatments. Regulatory changes, like the newly imposed 0.3% limit on over-the-counter retinol concentrations for facial products, bolster this trend towards dermatologist-supervised methods. Yet, they ensure continued access to potent prescription-strength treatments through medical avenues. Collaborative efforts are speeding up ingredient discovery and innovation. A prime example is the University of Birmingham's research into PEPITEM-derived peptides, which have shown effectiveness on par with steroid creams for psoriasis, highlighting academia's pivotal role in the future of skincare. In tandem with L’Oréal, brands such as SkinCeuticals are adapting to this shifting landscape, curating portfolios that emphasize clinical validation and dermatologist endorsement. This move reaffirms the market's dedication to scientific integrity and the pursuit of safe, effective anti-ageing solutions.

Trend toward clean and sustainable skincare

Sustainability is increasingly influencing consumer behavior, with 78% of United Kingdom consumers now prioritizing environmental credentials in their skincare purchases, according to Avon’s Future of Beauty Report 2024. This shift, largely driven by the clean beauty movement, underscores the growing importance of environmentally conscious practices. Brands are taking strategic actions. For instance, NIVEA has committed to a 50% reduction in plastic packaging and has transitioned to 100% renewable energy for production since 2019, often surpassing regulatory requirements. Meanwhile, industry-wide initiatives, such as the CTPA’s “Driving Towards a Net Positive Cosmetics Industry” strategy, seek to uplift the environmental performance across the board. However, independent evaluations by organizations such as the Carbon Trust indicate that none of the top 10 global beauty companies have attained validated Net Zero targets. This gap between soaring consumer expectations and corporate actions presents lucrative opportunities for emerging brands. Evolve Organic Beauty stands out, boasting both B Corp certification and Carbon Neutral status. They've also introduced groundbreaking innovations like water-free formulations and sugarcane-based packaging, significantly reducing their environmental footprint. These concerted efforts not only set brands apart in a competitive landscape but also foster industry accountability, empowering United Kingdom consumers to favor brands with genuine sustainability commitments over mere green claims.

Influence of social media and beauty influencers

In 2024, social media and beauty influencers are driving significant changes in the United Kingdom skincare product market. According to the World Population Review, the United Kingdom has 56.2 million social media users this year [2]Source: World Population Review, "Social Media Users by Country 2025", worldpopulationreview.com. Platforms like Instagram and TikTok are not only enabling real-time product discovery and instant purchases but are also reshaping product development processes. Brands are increasingly leveraging user-generated feedback to inform decisions on product formulation and packaging design. The rapid growth of the K-beauty trend exemplifies this shift, with Korean skincare products selling every 15 seconds at major retailers like Boots, a surge fueled by viral content and influencer endorsements. Digital-native brands, such as SkinCupid, are capitalizing on this momentum by transitioning from e-commerce to physical retail, as seen with their flagship store near Oxford Street, driven by strong social media-driven demand. Consumer behavior trends, such as "skinimalism," which emphasizes multifunctional products and simplified routines, are gaining popularity. Avon’s Future of Beauty Report 2024 highlights that 63% of United Kingdom consumers now prefer skincare routines with no more than three products. In this dynamic digital environment, influencers are increasingly collaborating with brands in co-creation efforts. This approach fosters authentic connections, strengthens customer loyalty, enhances engagement, and drives sales conversions, key factors shaping the strategies and success of businesses in the United Kingdom skincare market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse reactions to synthetic actives | -0.4% | England and Scotland primarily | Medium term (2-4 years) |

| Strict regulatory compliance creating cost hurdles | -0.6% | England, Scotland, Wales, Northern Ireland | Long term (≥ 4 years) |

| Impact of brand fatigue on consumer behavior | -0.5% | England dominant, Scotland and Wales moderate | Short term (≤ 2 years) |

| Challenges in building consumer loyalty | -0.3% | England, Scotland, Wales, Northern Ireland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adverse reactions to synthetic actives

Rising consumer concerns over ingredient safety, particularly regarding synthetic actives linked to adverse reactions, are impacting the United Kingdom skincare market. In response to this growing awareness, regulatory measures have been introduced, such as the United Kingdom's recent cap on over-the-counter retinol concentrations at 0.3% for facial products. This move reflects formal recognition of increasing reports that undermine confidence in conventional synthetic ingredients. To adapt, brands are reformulating their offerings, shifting toward gentler, biotech-derived alternatives like naringenin from L’Oréal-backed Deinde, which delivers anti-inflammatory benefits without the risks associated with synthetic components. This transition aligns with the accelerating growth of the natural and organic skincare segments, which are outperforming conventional product lines in the United Kingdom. However, the shift is not without challenges, as natural ingredients can also cause sensitivities. This highlights the critical need for brands to prioritize safe ingredient sourcing, rigorous safety testing, and transparent communication. These efforts are essential to educate consumers and maintain trust in a market where ingredient-related concerns can quickly influence purchasing decisions. These dynamics reflect a broader trend prioritizing skin health and safety alongside efficacy, driving innovation while challenging brands to balance effectiveness, gentleness, and consumer reassurance.

Strict regulatory compliance creating cost hurdles

Skincare manufacturers in the United Kingdom are grappling with heightened compliance demands stemming from a complex post-Brexit regulatory landscape. With the enactment of 65 newly banned substances and stricter concentration limits, companies are under pressure to reformulate and test their products, all while racing against tight compliance deadlines [3]Source: HM Government, "The Cosmetic Products (Restriction of Chemical Substances) (No. 2) Regulations 2024", legislation.gov.uk. This regulatory divergence has led to an estimated USD 850 million drop in United Kingdom beauty exports to the EU in 2023, underscoring the challenges of fragmented market access. Brands operating in both Great Britain and Northern Ireland face added complexities, needing separate United Kingdom Responsible Persons and distinct product information files, which translates to increased administrative burdens and costs. Compounding these challenges, U.S. trade tariffs impose a 10% levy on United Kingdom cosmetic imports, impacting millions in annual exports. The Office for Product Safety and Standards signals even stricter enforcement and upcoming regulatory changes, suggesting that compliance costs will continue to escalate. This creates a daunting landscape, especially for smaller brands that lack the resources to navigate such complexities. As a result, these challenges could hasten market consolidation, benefiting larger players equipped to absorb rising costs and ensure compliance, thereby altering the competitive landscape of the United Kingdom skincare sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Facial Dominance Drives Innovation

Facial care holds a dominant 77.68% market share in 2025 and is projected to lead growth with a 5.74% CAGR through 2031. This performance reflects consumers' increasing focus on facial routines and a shift towards premium products. The segment's prominence is driven by rising anti-aging demands, the pervasive influence of social media, and advancements in product formulations. A notable example of this innovation is No7's Future Renew Night Serum, co-developed with the University of Manchester, which demonstrates 100% efficacy in reversing visible skin damage, as confirmed by clinical studies. Body care products, including washes, scrubs, lotions, and creams, maintain steady demand, supported by hygiene essentials and seasonal trends. Artificial tan products, in particular, are experiencing a sales boost in 2024. Although lip care represents the smallest segment, it remains resilient due to multi-functional products that combine treatment and cosmetic benefits.

Facial care's competitive edge is further strengthened by continuous innovation in delivery systems. Research into dissolvable microneedle patches has shown an 83.3% reduction in acne-related inflammatory signs within four weeks. Within the facial care category, serums and essences are achieving the highest growth rates, driven by their concentrated active ingredient delivery and compatibility with layered skincare routines promoted on social media. Cleansers and toners continue to see stable demand as routine essentials, while face masks and packs benefit from the self-care trend and social media-driven usage occasions. Regulatory compliance, supported by MHRA oversight and Trading Standards enforcement, ensures product safety and bolsters consumer confidence in facial applications.

By Category: Premium Segment Outpaces Mass Market

In 2025, the mass market category holds a dominant 64.72% share of the skincare product market in the United Kingdom, driven by its extensive accessibility and distribution network catering to price-sensitive consumers. However, the premium/luxury segment is surpassing overall market growth, achieving a strong 6.29% CAGR. This growth is attributed to consumers' increasing willingness to spend on higher-priced products that promise superior efficacy and brand prestige, even in the face of economic challenges. The premium segment supports its elevated price points through access to exclusive ingredients, rigorous clinical testing, and strategic marketing initiatives. Brands such as Medik8 exemplify this trend by leveraging evidence-based philosophies and professional endorsements to justify premium pricing, a growth area that has attracted strategic acquisitions, including one by L’Oréal.

Meanwhile, mass market brands are enhancing their competitiveness by incorporating premium ingredients and advanced technologies, increasingly narrowing the gap between the two segments. This evolution is further driven by the rise of premium private label offerings from retailers, which deliver professional-grade formulations at more affordable prices, intensifying competition across price tiers. The premium segment's growth is further bolstered by specialty retailers and advanced online platforms, which provide consumers with detailed product information and user reviews. These tools enable brands to effectively communicate their superior benefits, reinforcing the value of premium pricing. Together, these factors are shaping a dynamic market landscape in the United Kingdom, where both mass and premium categories are evolving to align with shifting consumer expectations.

By Nature: Natural/Organic Segment Accelerates

In 2025, conventional products hold a 78.95% market share, yet they face increasing competition from natural and organic alternatives, which are growing at a strong 6.82% CAGR, the fastest rate among all segments. This growth reflects rising consumer awareness, with 78% of buyers prioritizing sustainability in their purchasing decisions, as highlighted in Avon's "Future of Beauty Report 2024". The natural and organic segment capitalizes on clean beauty trends, regulatory pressures on synthetic ingredients, and the premiumization of natural formulations enabled by advanced extraction and processing technologies. For instance, the University of Bradford's partnership with Coegin Pharma to develop peptide-based self-tanning products illustrates how natural innovations can create new market categories while avoiding synthetic chemicals. However, the segment faces challenges related to efficacy perception and shelf stability, prompting investments in natural preservation systems and bioactive ingredient research.

Conventional products continue to dominate due to their established efficacy profiles, cost advantages, and extensive research supporting synthetic actives. However, the segment is adapting by introducing hybrid formulations that combine synthetic efficacy with natural positioning and by improving the sustainability profiles of conventional ingredients. The regulatory environment increasingly favors natural alternatives, with stricter restrictions on synthetic substances creating opportunities for natural substitutes. To remain competitive, brands are investing in sustainable sourcing and transparent supply chains while retaining the benefits of conventional formulations. The growth disparity between the segments indicates a long-term shift toward natural products, although conventional formulations are expected to retain a majority share due to their performance advantages in specific applications and cost considerations for price-sensitive consumers.

By Distribution Channel: Online Retail Dominates Growth

In 2025, online retail stores capture a commanding 45.12% of the market share, leading the charge with a robust 6.55% CAGR. This growth is fueled by their ability to offer superior personalization, comprehensive product information, and unmatched convenience, all of which resonate with today's consumers. The online dominance in the skincare category is evident, as shoppers relish the opportunity to delve into ingredient research, peruse reviews, and scrutinize product details before making a purchase. A testament to this trend is Trinny London's Digital Skincare Advisor, an AI-driven tool crafted in collaboration with Revieve and Google Cloud, showcasing how online platforms are revolutionizing the shopping journey with tailored skin analysis recommendations. Furthermore, online channels are reaping the rewards of subscription models, auto-replenishment services, and direct-to-consumer strategies, all of which not only amplify customer lifetime value but also yield invaluable consumer insights for product innovation.

Health and beauty stores carve out a notable market presence, offering expert consultations and product testing, services that online platforms struggle to match. Superdrug's impressive double-digit growth and profit surge underscore the enduring significance of brick-and-mortar beauty retail, especially when bolstered by robust omnichannel strategies. While supermarkets/hypermarkets provide convenient access to everyday skincare items and capitalize on impulse purchases, they grapple with the challenge of delivering in-depth product education. The "other distribution channels" segment, encompassing specialty clinics and professional avenues, is witnessing growth, driven by the rising medicalization of skincare and a consumer tilt towards professional insights on active ingredients. The distribution landscape is shifting towards hybrid models, exemplified by brands like SkinCupid, which are transitioning from exclusive online platforms to establishing physical flagship stores, aiming to craft immersive brand experiences.

Geography Analysis

England commands the largest share of the United Kingdom's skincare market in 2025, driven by higher disposable incomes, concentrated urban populations, and early adoption of beauty trends. The region benefits from the presence of major retailers, flagship stores, and the highest concentration of specialty clinics and med spas. London's Oxford Street corridor has become a battleground for beauty retail expansion, with SkinCupid's flagship store opening reflecting the area's importance for brand visibility and consumer engagement. The region shows the highest growth rates through 2031, supported by continued urbanization, tourism recovery, and the concentration of high-income demographics who prioritize premium skincare products. England's regulatory environment, governed by MHRA and Trading Standards, provides a stable framework that encourages innovation while ensuring consumer safety.

Scotland demonstrates strong growth potential in the forecast period, driven by increasing beauty consciousness and expanding retail infrastructure in major cities like Edinburgh and Glasgow. The region shows particular strength in natural and organic product adoption, aligning with cultural values around environmental stewardship and authenticity. Wales and Northern Ireland represent smaller but growing markets, with consumers increasingly adopting skincare routines influenced by social media trends and improved product accessibility through online channels. These regions benefit from the United Kingdom's unified regulatory framework while maintaining distinct consumer preferences that favor value-oriented products and trusted brands.

The geographic distribution reflects broader economic patterns, with higher-income regions showing greater adoption of premium products and advanced skincare technologies. Rural areas across all regions are experiencing growth through improved e-commerce infrastructure and targeted marketing by brands seeking to expand beyond urban centers. The regional analysis indicates that while England will maintain market leadership, growth opportunities exist across all United Kingdom regions as skincare adoption becomes more universal and less concentrated in traditional beauty hubs. Brexit's impact on supply chains has been managed effectively across regions, with brands adapting distribution networks to maintain product availability and competitive pricing throughout the United Kingdom market.

Regulatory Landscape

The United Kingdom skincare market operates under the assimilated UK Cosmetics Regulation framework, with the Office for Product Safety and Standards (OPSS) as the competent authority in Great Britain. Before placing products on the market, a UK Responsible Person must notify OPSS via the Submit Cosmetic Product Notifications (SCPN) service, complete a safety assessment by a qualified assessor, and maintain a Product Information File (PIF) in line with GOV.UK guidance.

Post-Brexit chemical-controls tightening continues through statutory instruments amending restricted and prohibited substance annexes. The Cosmetic Products (Restriction of Chemical Substances) (No. 2) Regulations 2024 (SI 2024/1334) came into force on 31 January 2025, adding additional CMR-linked substance bans and concentration limits. More recently, SI 2026/23 (in force 15 July 2026) prohibited 3-(4'-methylbenzylidene)-camphor and updated warning labelling thresholds for formaldehyde-releasing preservatives. Transitional sell-through windows generally run into January or February 2027 depending on the specific restriction, which influences reformulation, testing, and inventory planning for brands selling in Great Britain and Northern Ireland.

Competitive Landscape

The United Kingdom skincare industry demonstrates moderate fragmentation, with large multinational corporations competing alongside agile local and digital-native brands. This dynamic enables global players to capitalize on economies of scale while specialized companies quickly adapt to shifting consumer trends and evolving regulatory frameworks. L’Oréal's acquisition of the British brand Medik8 highlights how global firms are strengthening their United Kingdom presence by leveraging local expertise and established consumer trust.

Competitive success increasingly depends on a brand’s ability to integrate scientific innovation with advanced digital marketing strategies. For example, No7 collaborates with universities for product development while maintaining strong partnerships with major retail channels, showcasing the importance of combining research credibility with consumer accessibility. Furthermore, technological advancements are becoming key differentiators, as companies invest in AI-driven personalization, virtual consultations, and sophisticated skin analysis tools to enhance customer engagement and justify premium pricing.

Strategic collaborations are reshaping competitive dynamics, as evidenced by the August 2024 partnership between Galderma and L’Oréal, which focuses on advancing dermatology research through shared expertise. The ability to navigate complex post-Brexit regulations is also critical for market positioning, favoring companies with robust compliance teams capable of managing increased operational challenges. This environment supports both consolidation, such as Bridgepoint’s private equity acquisition of RoC Skincare, and the rise of new entrants leveraging digital channels and sustainability to challenge established market shares.

United Kingdom Skincare Product Industry Leaders

-

L'Oréal SA

-

The Estée Lauder Companies Inc.

-

Unilever PLC

-

Procter & Gamble Company

-

Groupe Clarins

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory divergence between the United Kingdom and the EU is creating room for compliance-led innovation and service models. Frequent UK annex updates, including SI 2024/1334 (effective 31 January 2025) and SI 2026/23 (effective 15 July 2026), push manufacturers toward reformulation roadmaps, stronger safety substantiation, and faster label and PIF updates. The OPSS notification requirement via SCPN also keeps UK Responsible Persons and specialist compliance support central to operating cycles. For active-led facial care and sensitive-skin products, brands that can run repeatable UK-specific regulatory workflows can reduce time-to-shelf friction when concentration limits and warning-label thresholds force portfolio rationalization.

On the supply side, investment into UK manufacturing and supply-chain capability supports agility in adjacent beauty formats that affect skincare retail space and omnichannel execution. In May 2026, Unilever completed a GBP 150 million upgrade at its Port Sunlight campus, adding high-tech manufacturing upgrades and a new automated distribution centre connected to three factories by 2,000 metres of conveyors, improving throughput and logistics efficiency. In June 2026, The Estee Lauder Companies announced an investment to strengthen its Whitman manufacturing network in Petersfield by integrating luxury candle and home fragrance capabilities from Contract Candles, along with added R&D and quality capabilities. While not skincare-specific, these UK capability build-outs can help enable faster launches, tighter compliance control, and improved retailer service levels for premium portfolios sold through UK omnichannel partners.

Recent Industry Developments

- July 2026: The Very Group added The Estee Lauder Companies to its online beauty offer, listing about 440 skincare and makeup products across the Very and Littlewoods platforms. The expansion widens distribution reach in UK online retail and increases competitive pressure on incumbent skincare brands that rely on a narrower set of e-commerce partners.

- July 2025: The Ordinary expanded its United Kingdom digital distribution through a partnership with Amazon, opening a dedicated storefront on Amazon Premium Beauty UK. This strengthens access to science-led skincare at mass-premium price points and raises the bar for product education, reviews, and price transparency in online channels.

- April 2024: Boots and No7 Beauty Company renewed their long-running research partnership with the University of Manchester. The renewal reinforces clinical substantiation as a route to differentiation for facial care and supports continued pipeline development of evidence-backed actives and claims in a tightening UK compliance environment.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers professional skincare products sold and used through professional channels in the UK, where purchase is tied to a service setting or professional recommendation, and value is measured as product sales revenue.

Scope exclusions: We exclude mass retail only skincare ranges that are not positioned, distributed, or used as professional grade products.

Segmentation Overview

-

By Product Type

-

Facial Care

- Cleansers/Toners

- Moisturizers

- Serums and Essence

- Face Masks and Packs

- Other Facial Care Products

-

Body Care

- Body Wash and Scrubs

- Body Lotions and Creams

- Lip Care

-

Facial Care

-

By Category

- Mass

- Premium/Luxury

-

By Nature

- Conventional

- Natural/Organic

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Health and Beauty Stores

- Online Retail Stores

- Other Distribution Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping what counts as professional skincare in the UK and how products move through clinics, salons, and specialized distributors. We lean on public health and trade signals to anchor the demand environment, such as UK Office for National Statistics household spend series, NHS and public health guidance that influences skin health behavior, and Medicines and Healthcare products Regulatory Agency updates that affect product claims.

To keep assumptions grounded, we also review sources such as the British Beauty Council and other UK beauty association publications, HMRC trade statistics for relevant personal care import and export movements, peer-reviewed dermatology and cosmetic science journals for active ingredient adoption patterns, and brand and distributor websites with product positioning and channel statements. Company filings, investor presentations, and reputable press are used to cross-check pricing moves and portfolio mix, and a paid subscription covering company financials and news helps validate reported revenues where public reporting is limited. These sources are illustrative only, and many other references were used to collect, validate, and clarify data points during the study.

Primary Interviews and Surveys

Primary work is used to confirm what is truly sold as professional skincare in the UK and to validate pricing steps, channel margins, and mix shifts. We speak with brand and distributor-side leaders, clinic and salon operators, and specialist retailers, so desk assumptions on volumes, price bands, and adoption are tested against real buying and replenishment behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 18% | |

| Mid tier: 43% | Functional/Unit leaders: 36% | |

| Smaller Players: 21% | Managers: 46% |

Market-Sizing & Forecasting

Sizing is built mainly with a top-down approach, where the UK beauty and skincare value pool is narrowed into professional-only demand using channel participation, service-linked purchasing, and product positioning checks. The totals are then corroborated with selective bottom-up approximations, such as sampled clinic and salon replenishment patterns, distributor sell-in ranges, and average selling price (ASP) times indicative throughput, which are used to adjust outliers rather than to build the whole market.

Key inputs that shape the model include professional channel share by setting (clinic versus salon), typical service attach rates for skincare homecare, price architecture by category (cleansers, exfoliators, treatment serums, moisturizers, masks, and sun care), mix shifts between premium and entry professional lines, and promotional intensity that moves realized ASPs. Where point data is missing for smaller players, gaps are handled through conservative banding based on comparable portfolios and confirmed margin and pricing ranges from interviews.

Forecasting uses scenario analysis supported by a light regression check on drivers like consumer spend direction, professional service activity, and price inflation, so the forward view stays realistic when a single driver changes faster than expected. Assumptions for category growth and ASP progression are reviewed with primary respondents before the final curve is locked.

Data Validation & Update Cycle

Outputs are validated by comparing model results against independent demand signals, pricing movements, and channel commentary, and then checking whether implied per-site sales and ASP ranges look reasonable. Variances are flagged, worked through, and re-tested, and when a mismatch persists, we re-contact sources to confirm whether the change is real or only a timing effect.

Before sign-off, a second analyst reviews key assumptions and the calculation flow so the logic can be repeated and audited. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major pricing resets, channel disruptions, or regulatory changes affecting claims. Right before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's UK Professional Skincare Product Market Size Versus Other Published Estimates

Published numbers for UK professional skincare can look far apart because the boundary between professional-only products and broader skincare is not applied the same way, and because price and timing choices can shift the value even when volumes are similar.

In our work, the estimate is kept aligned to the period being measured by refreshing ASPs with current year price steps and promotional dilution, and then running variance checks against channel signals before release, which is also why the 2026 figure on Mordor Intelligence can sit away from sources that keep older exchange rates or use list prices without a realized ASP adjustment.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.84 B (2026) | |

| Industry Publisher A | USD 1.20 B (2024) | This figure is positioned around professional-grade products only and appears to exclude adjacent premium skincare sold through specialist retail, and the year base can also compress the value when later price resets are not carried forward. |

| Trade Aggregator B | USD 4.14 B (2024) | This estimate is for the wider UK skincare market, so it can blend mass and premium retail sales with professional-channel activity, which changes the scope and reduces the ability to isolate service-linked demand. |

Taken together, the spread is mainly explained by whether the scope is professional-only or total skincare, and by how ASPs are timed and converted for the stated year. By keeping scope rules explicit and re-checking price realization against channel feedback, the final number stays traceable to clear inputs and can be repeated when the market moves.

Key Questions Answered in the Report

What is the current value of the UK skincare product sector and its expected CAGR to 2031?

The sector is valued at USD 4.84 billion in 2026 and is projected to reach USD 6.27 billion by 2031, reflecting a 5.34% CAGR.

Which product category holds the largest share of UK skincare product sales?

Facial skincare leads with a 77.68% share in 2025 and is forecast to remain dominant through 2031.

Why are premium skincare brands outpacing mass labels in the UK?

Shoppers prioritize science-backed efficacy and are willing to pay for clinically validated actives, enabling the premium segment to grow at a 6.29% CAGR versus slower gains for mass products.

Which sales channel is forecast to grow fastest for UK skincare?

Online retail, already holding 45.12% share in 2025, is expected to advance at a 6.55% CAGR due to personalized shopping experiences.

Page last updated on: