Dermocosmetics Skin Care Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

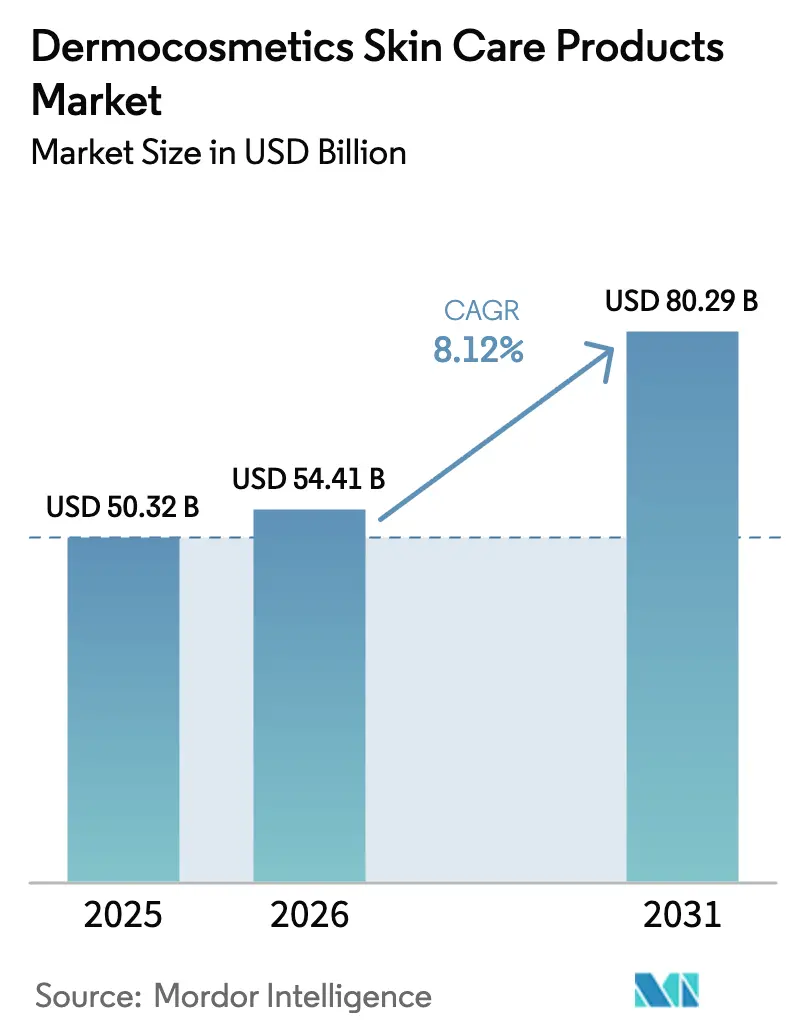

| Market Size (2026) | USD 54.41 Billion |

| Market Size (2031) | USD 80.29 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

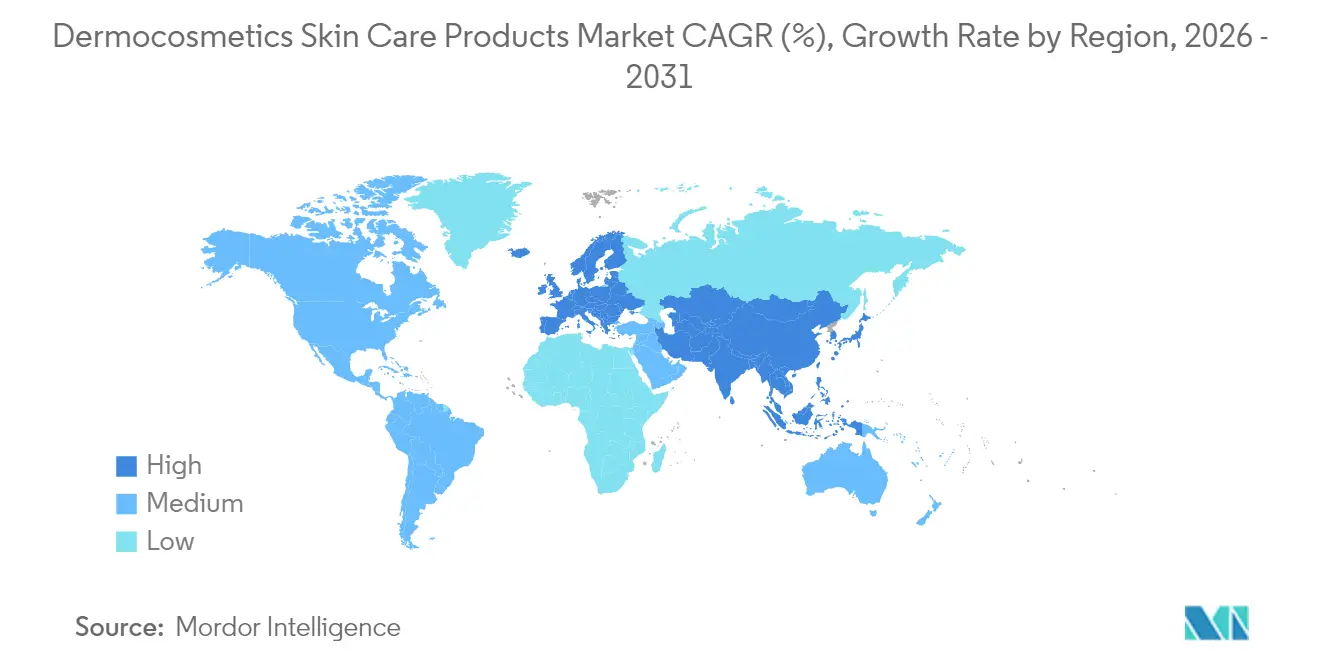

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dermocosmetics Skin Care Products Market Analysis by Mordor Intelligence

The dermocosmetics skin care products market size is expected to grow from USD 50.32 billion in 2025 to USD 54.41 billion in 2026 and is forecast to reach USD 80.29 billion by 2031 at 8.12% CAGR over 2026-2031. The dermocosmetics market, encompassing facial, lip, nail, and body care, is witnessing steady growth, fueled by a surge in consumer demand for scientifically-backed, dermatologically-tested solutions. Facial care leads the pack, bolstered by heightened awareness of issues like rosacea, eczema, and photodamage. Meanwhile, body and lip care are gaining prominence, driven by rising concerns over dryness and the need for barrier repair. Europe stands at the forefront, both in terms of innovation and consumption. However, the Asia-Pacific region is rapidly catching up, spurred by urbanization, heightened pollution exposure, and better access to dermatologists. Technological innovations, including microbiome-based formulations, encapsulated actives, and AI-driven skin assessments, are revolutionizing product development. Brands such as Eucerin and Avène are harnessing pharmaceutical research and developments to craft targeted treatments, bolstering consumer trust. Today's consumers are increasingly prioritizing sustainability, ingredient transparency, and minimalist routines, with a marked shift towards fragrance-free and hypoallergenic formulations.

Key Report Takeaways

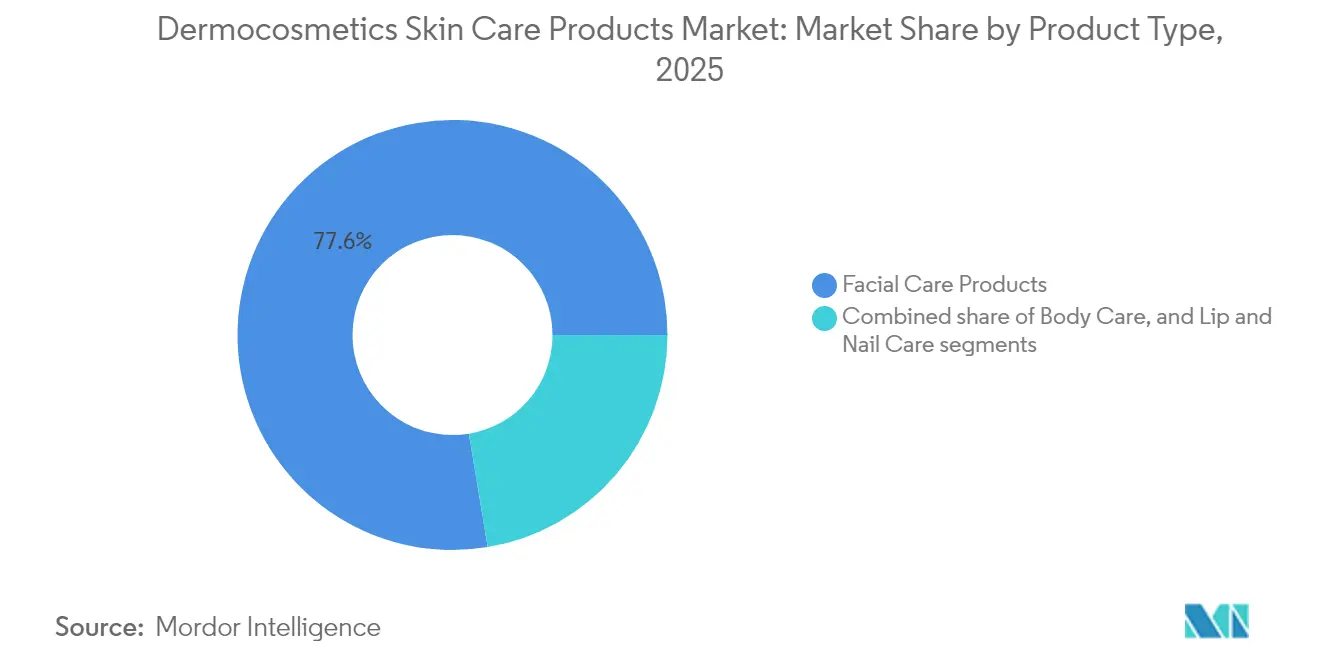

- By product type, facial care led with a 77.62% dermocosmetics skin care products market share in 2025, while lip care is projected to post the fastest 9.55% CAGR through 2031.

- By active ingredient, hyaluronic acid products accounted for 31.62% of the dermocosmetics skin care products market size in 2025; peptides form the fastest-expanding group at an 11.02% CAGR to 2031.

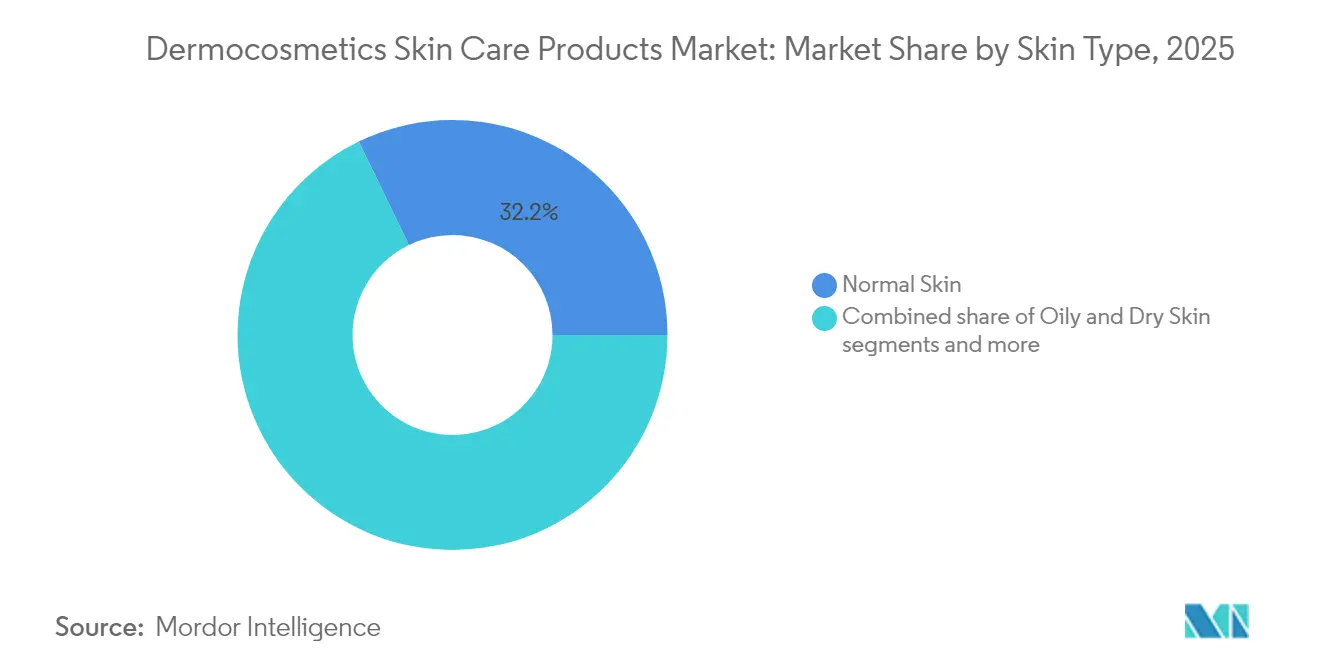

- By skin type, formulations for sensitive skin are advancing at a 9.86% CAGR between 2026-2031, whereas normal skin products remained the revenue cornerstone with 32.18% share in 2025.

- By distribution channel, health and beauty stores commanded 44.91% of sales in 2025, yet online retail is set to accelerate at a 10.05% CAGR over the same horizon.

- By geography, Europe retained leadership with a 34.42% share in 2025; Asia-Pacific is expected to register the quickest 8.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dermocosmetics Skin Care Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased awareness of sensitive skin needs | +1.8% | North America, Europe, global spill-over | Medium term (2-4 years) |

| Active-ingredient transparency and evidence-based demand | +2.1% | Asia-Pacific core, global spill-over | Long term (≥4 years) |

| Premiumization and willingness to pay for quality | +1.5% | Developed markets worldwide | Medium term (2-4 years) |

| AI-driven personalized skincare solutions | +0.9% | North America and Asia-Pacific | Long term (≥4 years) |

| Innovative microbiome-friendly formulations | +1.2% | Early adoption in North America | Medium term (2-4 years) |

| Celebrity endorsements with dermatology claims | +0.7% | Global, strongest in North America and Asia-Pacific | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Increased Awareness of Sensitive Skin Needs

As consumers become more aware of the needs of sensitive skin, their behavior in the dermocosmetics market is shifting, leading to a rising demand for products that prioritize both safety and effectiveness. Aveeno’s 2024 State of Skin Sensitivity report reveals that 71% of global consumers now recognize themselves as having sensitive skin [1] Source: Aveeno, “State of Skin Sensitivity,”aveeno.com. This growing acknowledgment has heightened the demand for formulations that are gentle, fragrance-free, and backed by clinical testing. In response to this trend, brands are rolling out scientifically-backed innovations. For instance, L’Oréal’s La Roche-Posay, in 2024, broadened its Toleriane range with formulations enriched with neurosensine. This move was bolstered by a 2023 EADV study, which highlighted a 28-day reduction in itching, redness, and burning for users with sensitive and allergy-prone skin. On another front, Aveeno’s Calm + Restore line, featuring oat-based actives for barrier repair, is being promoted through dermatology-led campaigns that stress ingredient transparency and minimalism. Such strategies underscore a market shift where functionality is prioritized over mere aesthetic claims. Tools like digital skin assessments and personalized platforms such as SkinSAFE further amplify this shift. The industry is now leaning towards products that are friendly to the microbiome and light on preservatives, as consumers take proactive steps to sidestep irritants.

Consumer Demand for Active Ingredient Transparency and Evidence-Based Products

The consumers are increasingly demanding transparency in active ingredients and evidence-based claims. This shift is reshaping the dermocosmetics skincare market. L’Oréal’s 2024 launch of Melasyl™, underpinned by 121 scientific studies, underscores the industry's pivot towards clinically validated actives, justifying their premium positioning. The Ordinary, eschewing emotional narratives, has ascended by championing transparent, single-ingredient formulations with clinically validated efficacy. Brands are now prioritizing biotechnology-led innovations, investing in lab-developed molecules and peer-reviewed testing to align with rising consumer expectations. Regulatory frameworks, like the California Department of Public Health’s Cosmetic Safety Program, which mandates a minimum of 70% organic content for products labeled as organic, are bolstering this trend, promoting genuine clean beauty claims [2]Source: California Department of Public Health, “Cosmetic Safety Program,” cdph.ca.gov. . A March 2025 NSF survey further highlights this shift, revealing that 74% of consumers deem organic ingredients crucial in personal care products [3]Source: NSF International, “Global Consumer Insights on Personal Care,”nsf.org . As consumers become more discerning, brands that prioritize science and align with regulations are gaining prominence.

Premiumization and Willingness to Pay for Quality

As consumers increasingly view skincare as a long-term health investment rather than a mere luxury, the premiumization trend in beauty is propelling growth in the dermocosmetics market. This evolving mindset is influencing purchasing behaviors across various price tiers. Consumers are gravitating towards clinical-grade formulations that come with dermatological validation. This demonstrates that clinical credibility can evoke a premium perception, even in the absence of luxury branding. The swift rise of the masstige segment, driven by brands offering reasonably priced products infused with active ingredients like niacinamide and ceramides, underscores consumers' readiness to 'trade up' when the formulation warrants it. In the realms of prestige and luxury, brands such as SkinCeuticals and La Mer bolster their value propositions by spotlighting patented actives, backing their claims with clinical studies, and forging partnerships with dermatologists. Meanwhile, Dr. Barbara Sturm flourishes by championing anti-inflammatory science and bespoke routines. This shift in consumer behavior is putting pressure on mid-tier brands that struggle with differentiation, pushing consumers to either invest in scientifically validated products or settle for basic, utilitarian choices.

Celebrity Endorsements and Dermatologically Backed Claims

Celebrity endorsements and influencer marketing, now intertwined with dermatologist-backed claims, are rapidly driving younger, digitally-savvy consumers towards dermocosmetic skincare. In 2023, Hailey Bieber’s Rhode Skin, with its minimalist messaging centered on skin barrier health and dermatologist consultations, gained significant traction. This underscores the potent combination of celebrity allure and clinical validation in swaying consumer choices. Gwyneth Paltrow’s Goop Beauty, on the other hand, marries expert endorsements with wellness narratives, resonating with health-focused premium buyers. On platforms like TikTok and Instagram, derm-influencers such as Dr. Shereene Idriss and Dr. Shah break down skincare ingredients and advocate for evidence-based routines, often sparking viral interest in brands like La Roche-Posay and Vichy. A 2024 survey from the University of Portsmouth underscores this trend: 60% of consumers place trust in influencer recommendations, with nearly half of all purchasing decisions influenced by them [4]Source: University of Porth, “New Research Unveils the "Dark Side" of Social Media Influencers and Their Impact on Marketing and Consumer Behaviour”, port.ac.uk.. This highlights the rising clout of digital voices in shaping skincare preferences. Dermocosmetic brands aligning with medically credible influencers and celebrities are not only garnering heightened attention but also fostering brand loyalty, propelling their market growth through trust, education, and visibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity and competition from conventional skincare | −1.4% | Emerging markets global | Short term (≤2 years) |

| Competition from home and professional dermatological treatments | −0.8% | North America, Europe | Medium term (2-4 years) |

| Supply chain challenges in specialty actives | −1.1% | Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Regulatory compliance costs and certification hurdles | −0.6% | Europe, North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity and High Competition from Conventional Skincare Products

As consumers increasingly weigh cost against perceived value, rising price sensitivity is constraining the growth of the dermocosmetics skincare market. In emerging markets, brands such as Pond’s and Nivea are gaining traction by offering moisturizers and serums infused with familiar actives like hyaluronic acid and vitamin C, but at a fraction of the price of premium dermocosmetic lines. This shift has led consumers to reevaluate the cost-benefit ratio of higher-end products, especially when the efficacy claims seem comparable. Adding to the complexity, mass beauty giants like Unilever and L’Oréal have launched premium lines, such as L’Oréal Revitalift Clinical and Simple Booster Serums. These products blur the lines between conventional and dermocosmetic skincare by emphasizing narratives of dermatologist co-creation and clinical testing. On the other hand, traditional skincare brands like Vaseline and Dove, which lack strong clinical claims, still maintain consumer trust in routine care categories. They offer dependable performance without the premium pricing or science-driven branding. This overlap in competition diminishes the unique positioning of traditional dermocosmetics.

Competition from Home and Dermatological Skin Treatments

As advanced at-home devices and professional dermatological treatments gain traction, the dermocosmetics skincare market finds itself in a tightening competitive squeeze. Brands such as Dr. Dennis Gross and CurrentBody are revolutionizing consumer habits, introducing LED masks and microcurrent tools. These innovations are being hailed as high-tech substitutes for traditional topical serums, particularly in the realms of anti-aging and skin firming. Not only do these devices promise visible results, but they also resonate with tech-savvy consumers eager for swift outcomes without the commitment of daily applications. Concurrently, the burgeoning field of aesthetic dermatology, encompassing injectables and laser treatments, has nudged consumers towards options that promise instant skin enhancements. This shift has lessened the dependence on dermocosmetics for corrective purposes. Platforms like Skintap and Curology are streamlining access to prescription-strength solutions via virtual consultations, steering consumers away from standard over-the-counter products and towards clinically endorsed regimens. In response to this evolving landscape, dermocosmetics brands are recalibrating their strategies. Brands like La Roche-Posay and Avene are capitalizing on this trend, championing formulations tailored for use in tandem with dermatological treatments, thus redefining their significance in a landscape increasingly driven by treatment interventions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Facial Care Dominance Drives Innovation

In 2025, facial care products command a dominant 77.62% share of the market, underscoring consumers' focus on visible skin areas as the primary entry point for dermocosmetic adoption. Given the heightened sensitivity and visibility of facial skin, consumers are increasingly turning to scientifically validated solutions. Capitalizing on this trend, brands like La Roche-Posay and The Ordinary have broadened their serum and moisturizer lines, emphasizing high-concentration actives. Serums, in particular, have garnered attention for their perceived clinical benefits. Additionally, the rise of Dr. Jart+ masks and toners, propelled by social media, is ushering in new facial skincare rituals, further cementing the segment's dominance.

The lip care segment is emerging as the fastest-growing category, with projections indicating a CAGR of 9.55% from 2026 to 2031. This surge is driven by consumers' growing awareness of the lips' unique physiological needs. Responding to this trend, brands like Laneige, with its popular Lip Sleeping Mask, and Eucerin are broadening their dermocosmetic lip offerings. While lip care gains momentum, body care products are also making strides, incorporating active ingredients once reserved for facial treatments. Notable examples include CeraVe's SA Body Wash and Augustinus Bader's Body Cream. As brands navigate this evolving landscape, they are ensuring consistent ingredient quality while tailoring formulations for varied applications to maintain consumer trust and loyalty.

By Active Ingredients: Hyaluronic Acid Leadership Faces Peptide Challenge

In 2025, hyaluronic acid commands a dominant 31.62% share of the dermocosmetics active ingredient market, owing to its renowned deep hydration properties, compatibility with skin, and widespread regulatory endorsement. Its versatility spans a range of formulations from serums to creams with tweaks in molecular weight, allowing tailored penetration at varying skin depths. This adaptability has cemented its status as a cornerstone ingredient for brands like La Roche-Posay, with its Hyalu B5 Serum, and The Ordinary’s Hyaluronic Acid 2% + B5, appealing to both mainstream and upscale consumers. Moreover, advancements in sustainable microbial fermentation not only bolster production economics but also champion environmental sustainability, paving the way for its expansive adoption.

Peptides are emerging as the fastest-growing ingredient category, projected to surge at a CAGR of 11.02% through 2031. Their ascent is fueled by their proven benefits in anti-aging, collagen production, and fortifying the skin barrier. Cutting-edge innovations, like bioengineered peptides and PFAS-free formulations from Croda Beauty, are drawing in consumers who prioritize clinical results but with a diminished risk compared to conventional actives. Meanwhile, retinoids, despite their established reputation in the anti-aging realm, grapple with growth challenges stemming from consumer sensitivities and heightened global regulatory oversight.These consumers, while seeking pronounced wrinkle-reduction results, acknowledge the necessity for a gradual acclimatization and formulations that bolster tolerance.

By Skin Type: Normal Skin Foundation Enables Sensitive Skin Growth

In 2025, the normal skin segment commands a dominant 32.18% share, anchoring the dermocosmetics skincare market. Its universal appeal makes it a prime target for new product introductions. Brands like CeraVe and Neutrogena capitalize on this segment, offering formulations that not only balance the skin but also highlight innovative active ingredients. The segment's vastness ensures steady revenue streams for companies, which subsequently fuels research and development for specialized products. Moreover, it's a proving ground for next-gen technologies, often before they're tailored for more sensitive or intricate skin types.

Meanwhile, the sensitive skin segment is on an upward trajectory, projected to expand at a 9.86% CAGR from 2026 to 2031. As concerns over pollution, stress, and allergies rise, consumers are increasingly turning to this segment. Brands like La Roche-Posay's Toleriane and Avene's Tolérance Control, backed by dermatologists, are leading the charge. They emphasize minimalist, hypoallergenic formulations, often backed by stringent clinical validation. This not only establishes high entry barriers but also cultivates deep consumer trust. In contrast, other skin types, dry, oily, and combination, are pushing the envelope with innovations. Products like Gallinée’s prebiotic creams and Dr. Jart+’s zonal treatments underscore the industry's pivot towards personalized skincare solutions.

By Distribution Channel: Online Acceleration Challenges Traditional Retail

In 2025, health and beauty stores command the distribution landscape with a 44.91% market share. Their success stems from offering personalized consultations, employing trained staff, and curating selections of dermocosmetics. Retail giants like Ulta Beauty and Watsons bolster consumer trust by adopting diagnostic tools and featuring dermatologist-endorsed brands, including CeraVe and La Roche-Posay, known for their efficacy on sensitive and acne-prone skin. By creating a professional retail atmosphere, these stores bridge the gap between clinical expertise and consumer skincare needs, solidifying their leading status.

Online retail stores are emerging as the fastest-growing channel, with projections indicating a robust 10.05% CAGR from 2026 to 2031. This surge is largely attributed to platforms like TikTok Shop, where skincare trends go viral and swiftly shape purchasing decisions. Additionally, direct-to-consumer sites like The Ordinary and Dr. Jart+ leverage targeted content and ingredient-focused narratives to boost sales. Amazon's rising foothold in the European beauty sector highlights the power of competitive pricing and customer reviews, serving as trust substitutes when in-person consultations are absent. On another front, supermarkets and hypermarkets, including Carrefour and Tesco, cater to budget-conscious shoppers by broadening their dermocosmetic offerings.

Geography Analysis

In 2025, Europe dominates the dermocosmetics skincare market, holding a 34.42% share. This leadership is attributed to Europe's stringent regulatory frameworks, a high consumer trust in clinically validated products, and a robust pharmacy-based distribution network. France stands at the forefront, with brands such as La Roche-Posay and Avène receiving endorsements from both dermatologists and pharmacists, seamlessly integrating into the nation's healthcare system. The region's mature market benefits from widespread consumer education on ingredient safety and effectiveness, fostering a preference for dermocosmetic products over general skincare, especially for conditions like rosacea and eczema.

Asia-Pacific emerges as the fastest-growing region, boasting a projected CAGR of 8.97% from 2026 to 2031. A rising digital influence, a convergence in regulations, and a consumer pivot towards science-backed skincare fuel this growth. In South Korea, brands like Dr. Jart+ and Mediheal meld dermatological science with the allure of K-beauty, establishing themselves as essentials in both local and global skincare routines. Chinese consumers, increasingly swayed by derm-influencers on platforms like Xiaohongshu, are gravitating towards ingredients such as niacinamide and peptides, sidelining traditional luxury cosmetics. In Japan, consumers lean towards minimalist, clinically-proven formulations, with pharmacy shelves dominated by brands like Hada Labo and Curel. Meanwhile, in India, there's a burgeoning demand for dermocosmetics addressing local concerns, such as pollution-related skin issues and pigmentation, propelling brands like Cipla's Ciphands and The Derma Co. into the spotlight.

North America, South America, and the Middle East and Africa, though smaller markets, are witnessing notable evolution. In North America, specialty retailers like Sephora are championing the rise of clinical skincare, prominently featuring brands such as The Ordinary, SkinCeuticals, and Murad. Brazil is witnessing a surge in dermatologist-recommended skincare, with brands like Adcos becoming go-to solutions for acne and sun damage.

Competitive Landscape

The market exhibits a moderate consolidation. In the dermocosmetics market, industry giants such as L'Oréal, Beiersdorf, and Kenvue leverage their extensive backgrounds in pharmaceuticals and cosmetics. These leaders utilize robust multi-channel marketing strategies, emphasizing clinical endorsements, collaborations with dermatologists, and a science-driven approach to product messaging. For instance, L'Oréal's CeraVe prominently showcases dermatological endorsements, while La Roche-Posay focuses its messaging on sensitive skin, underpinned by clinical research.

Technology is becoming a pivotal differentiator in this arena. Companies are leveraging AI-driven diagnostic tools, teledermatology platforms, and biofermentation processes to boost personalization and sustainability. For example, Shiseido and Procter & Gamble utilize AI skin analysis apps to refine product recommendations and enhance consumer trust. Biotech firms such as Codex Labs and Mother Dirt lead the charge, incorporating microbiome-friendly actives and postbiotic innovations, frequently through bioengineered fermentation. This approach not only guarantees product effectiveness but also reduces environmental impact.

Strategically, industry players are adopting both vertical and horizontal integration to solidify their growth and credibility. Pharmaceutical giants like Galderma and Nestlé Skin Health are partnering with aesthetic clinics and dermatology networks, enhancing their clinical significance and accessing premium distribution channels. On the horizontal front, L'Oréal's collaborations with biotech firms like Verily and Carbios highlight its dedication to ingredient innovation, green chemistry, and advanced formulation platforms.

Dermocosmetics Skin Care Products Industry Leaders

-

L’Oréal Group

-

Beiersdorf AG

-

Galderma SA

-

Pierre Fabre SA

-

Johnson and Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: L’Oréal completed the acquisition of Medik8 for GBP 50.4 billion, adding high-potency vitamin A serums and algorithm-guided regimens to its active cosmetics division.

- April 2025: Dove unveiled a dermatologist-tested facial portfolio featuring ceramide lipids and niacinamide, signalling Unilever’s elevated commitment to clinically validated skincare

- March 2025: L’Oréal and the WHO Foundation launched the EUR 20 million “Act for Dermatology” program aimed at reducing the global treatment gap for skin diseases

- August 2024: L’Oréal purchased a 10% stake in Galderma for USD 450 million to synergize dermal-filler expertise with topical dermatology portfolio

Global Dermocosmetics Skin Care Products Market Report Scope

| Facial Care Products | Cleansers |

| Masks | |

| Moisturizers and Creams | |

| Toner | |

| Serums and Oils | |

| Other Facial Care Products | |

| Body Care Products | Body Wash |

| Body Scrubs | |

| Body Lotion | |

| Other Body Care Products | |

| Lip and Nail Care Products | Lip Balms |

| Lip Scrubs | |

| Nail Care | |

| Others |

| Vitamins |

| Retinoids |

| Peptides |

| Hyaluronic Acid |

| Combination |

| Others |

| Dry Skin |

| Oily Skin |

| Sensitive Skin |

| Normal Skin |

| Combination Skin |

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Others Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Facial Care Products | Cleansers |

| Masks | ||

| Moisturizers and Creams | ||

| Toner | ||

| Serums and Oils | ||

| Other Facial Care Products | ||

| Body Care Products | Body Wash | |

| Body Scrubs | ||

| Body Lotion | ||

| Other Body Care Products | ||

| Lip and Nail Care Products | Lip Balms | |

| Lip Scrubs | ||

| Nail Care | ||

| Others | ||

| By Active Ingredients | Vitamins | |

| Retinoids | ||

| Peptides | ||

| Hyaluronic Acid | ||

| Combination | ||

| Others | ||

| By Skin Type | Dry Skin | |

| Oily Skin | ||

| Sensitive Skin | ||

| Normal Skin | ||

| Combination Skin | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Health and Beauty Stores | ||

| Online Retail Stores | ||

| Others Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the dermocosmetics skin care products market in 2026?

The market is valued at USD 54.41 billion in 2026 and is projected to reach USD 80.29 billion by 2031.

Which product category generates the most revenue?

Facial care products hold 77.62% of global revenue, far surpassing body and lip care.

What ingredient category is growing fastest?

Peptides are forecast to expand at an 11.02% CAGR through 2031 due to advances in sustainable bio-synthesis.

Which region will add the greatest incremental sales?

Asia-Pacific, supported by e-commerce penetration and regulatory harmonization, is expected to grow at a 8.97% CAGR.

Page last updated on: