South Africa Skincare Product Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

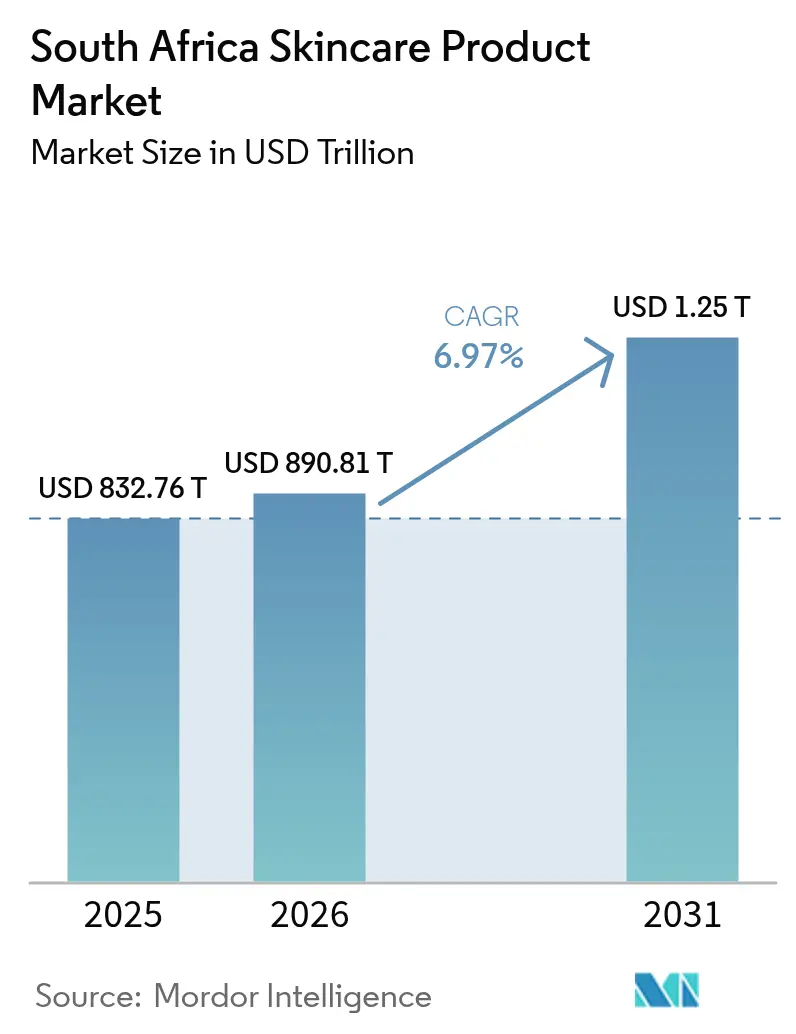

| Base Year Market Size (2025) | USD 832.76 Billion |

| Market Size (2026) | USD 890.81 Billion |

| Market Size (2031) | USD 1248.38 Billion |

| Growth Rate (2026 - 2031) | 6.97% CAGR |

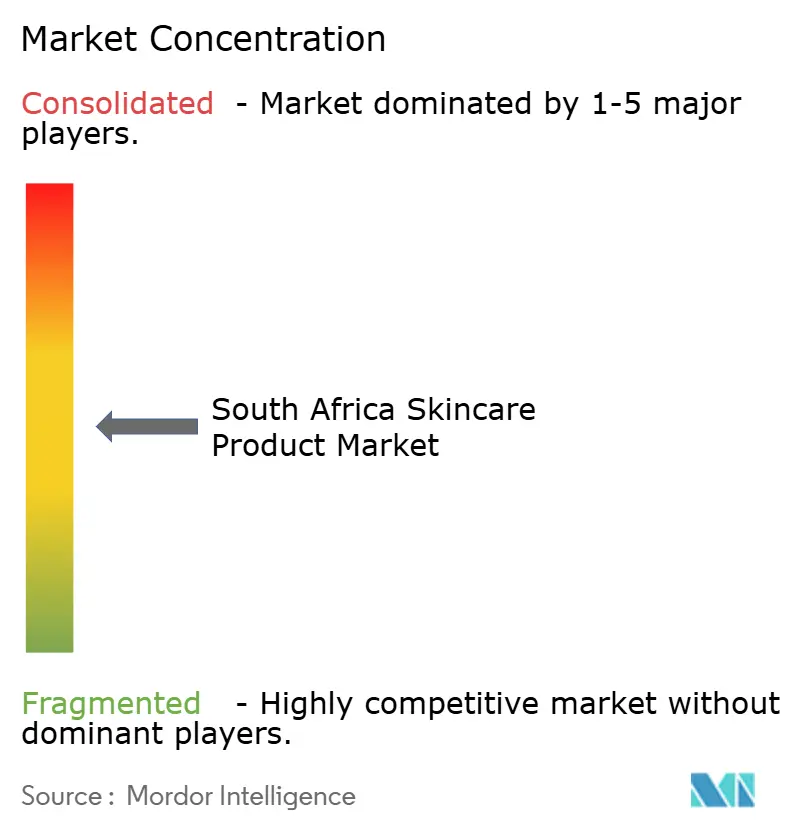

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Africa Skincare Product Market Analysis by Mordor Intelligence

The South Africa skin care market size is expected to grow from USD 832.76 million in 2025 to USD 890.81 million in 2026 and is forecast to reach USD 1,248.38 million by 2031 at 6.97% CAGR over 2026-2031. The decline in inflation, has improved real wages and revitalized discretionary spending. This change enables consumers to choose premium formulations and adopt new digital shopping behaviors. Growing health and environmental awareness is driving demand for skin care products with natural ingredients, fostering innovation in clean-label, eco-friendly formulations. The growth of South Africa's skin care market is supported by premiumization, increasing demand for clinically-backed dermacosmetics, the expansion of organized retail chains, and a thriving e-commerce sector. Evolving societal trends have led to a rising demand for male-focused skin care, with products designed for men gaining visibility through influencer and celebrity endorsements. International brands leverage extensive distribution networks, while agile local brands incorporate indigenous botanicals and sustainability elements to build loyal customer bases. Although challenges such as raw-material price volatility and counterfeit risks remain, urbanization and higher per-capita spending in Gauteng and Western Cape offer significant growth opportunities for suppliers in South Africa's skin care market

Key Report Takeaways

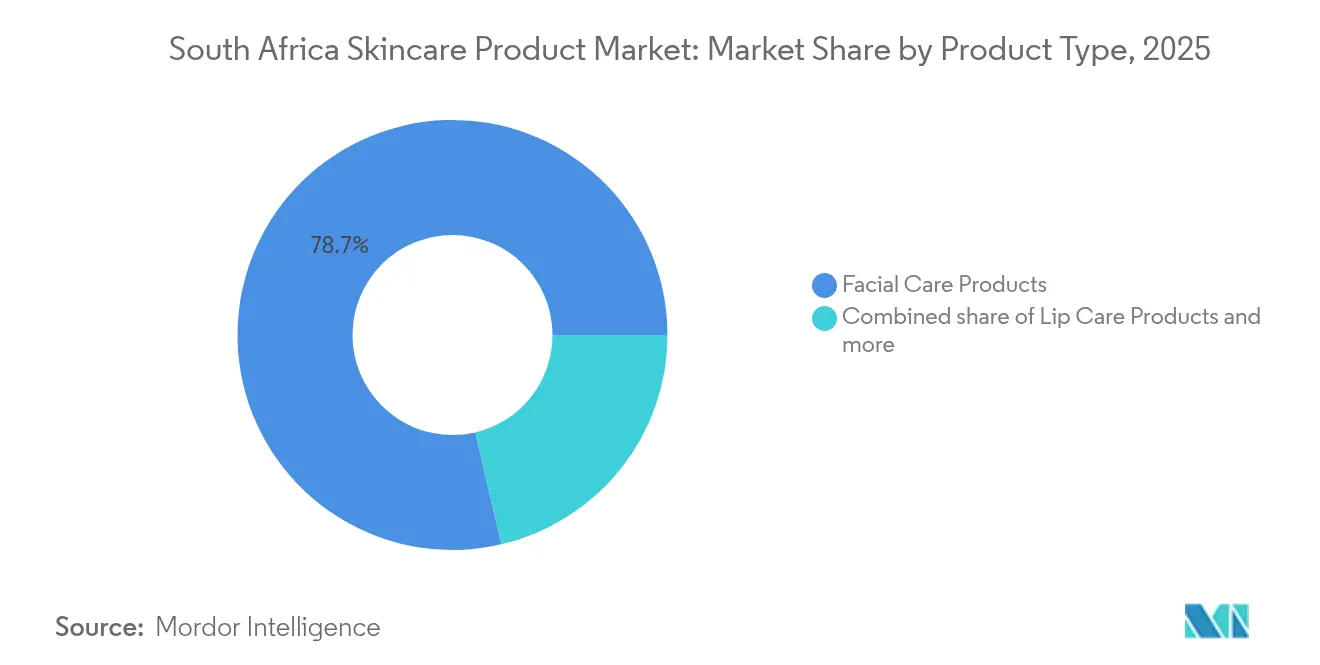

- By product type, Facial Care Products led with 78.65% revenue share in 2025; Lip Care Products are forecast to post the fastest 7.18% CAGR through 2031.

- By category, the Mass segment held 65.72% of the South Africa skin care market share in 2025, while the Luxury/Premium segment is expected to expand at a 7.82% CAGR to 2031.

- By end user, Women accounted for 88.35% of sales in 2025; the Men’s segment is projected to grow the quickest at an 7.97% CAGR to 2031.

- By ingredient type, Conventional inputs commanded 70.63% of the South Africa skin care market size in 2025, and Natural/Organic formulations are on track for a 7.74% CAGR through 2031.

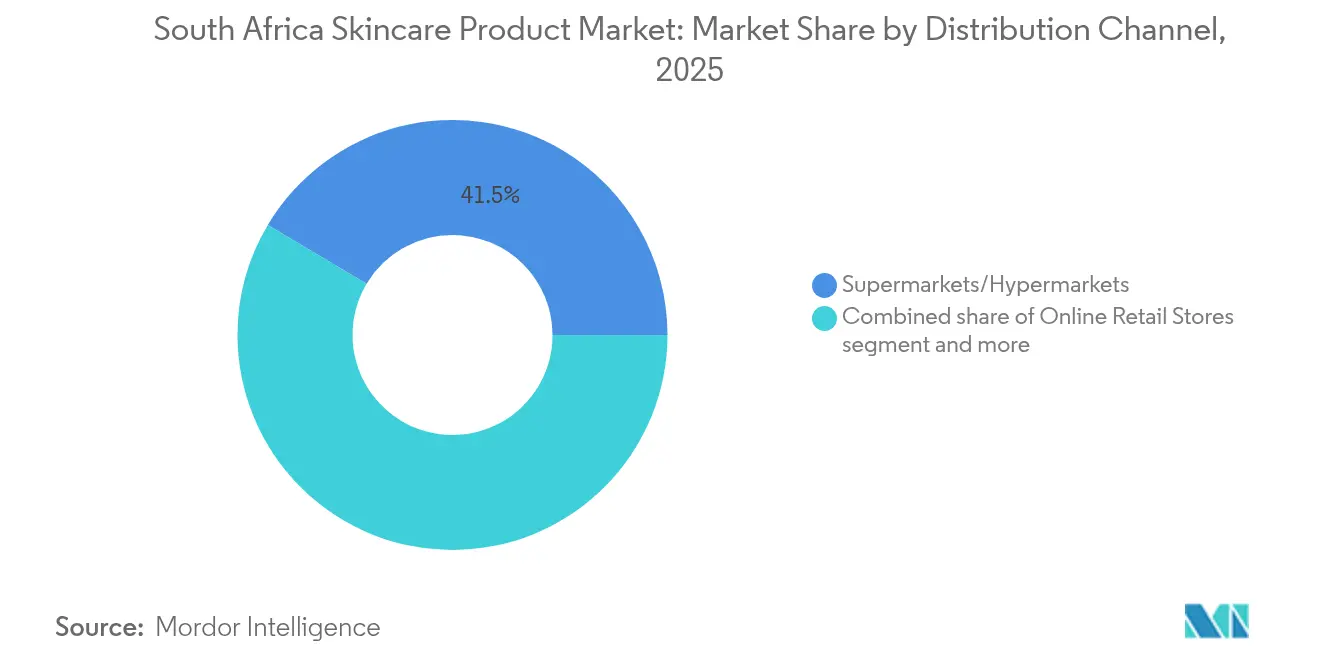

- By distribution channel, Supermarkets/Hypermarkets captured 41.45% share in 2025, whereas Online Retail Stores are set to grow at an 7.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Skincare Product Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for dermacosmetics | +1.5% | National, with concentration in Gauteng and Western Cape metros | Medium term (2-4 years) |

| Consumer Inclination Towards Organic and Natural Products | +1.2% | Urban areas, particularly Cape Town and Johannesburg affluent suburbs | Long term (≥ 4 years) |

| Influence of Social Media and Celebrity Endorsement | +0.8% | National, with higher impact in urban millennials and Gen Z demographics | Short term (≤ 2 years) |

| Increasing Demand for Anti-Aging Products | +0.9% | Metro areas, concentrated among higher-income households | Medium term (2-4 years) |

| Growing Awareness Regarding Skin-Related Issues | +1.1% | National, accelerated by healthcare accessibility improvements | Medium term (2-4 years) |

| Growing preference for multifunctional 'hybrid' products | +0.7% | Urban consumers, driven by time-pressed lifestyles | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for dermacosmetics

The South African skin care market is experiencing growth in value and innovation, driven by increasing demand for dermacosmetics. Consumers are showing a stronger preference for products that combine dermatological effectiveness with cosmetic benefits. This evolving trend is influencing shopper behavior and expanding the scope of traditional skin care. The integration of skincare and pharmaceutical science is fueling notable market growth as South Africans increasingly opt for clinically-proven formulations. Urban professionals are at the forefront of this shift, prioritizing efficacy over conventional beauty marketing. Retailers like Dis-Chem, focusing on 37 stores, demonstrate confidence in this segment by prominently offering premium dermacosmetic brands such as Avène, La Roche-Posay, and Eucerin. Additionally, local brands like DrK Dermal Health Care are gaining traction by providing premium-priced dermatological solutions for specific skin conditions. The segment's expansion is further supported by SAHPRA's rigorous regulatory framework under the Medicines and Related Substances Act, which ensures product safety and strengthens consumer trust in medical-grade formulations.

Consumer inclination towards organic and natural products

South African consumers are increasingly gravitating toward organic and natural skin care products. This shift is driving market growth, fostering product innovation, and expanding category offerings. As global sustainability trends influence South African consumers, natural and organic formulations are gaining momentum. However, conventional products still hold a dominant 71.19% market share in 2024. Norse Organics exemplifies this transition, leveraging social media to promote its plant-based formulations, which appeal to environmentally-conscious buyers. This trend is particularly evident in affluent areas of Cape Town and Johannesburg, where household spending is significantly higher. According to Statistics South Africa, in 2023, Cape Town households recorded the highest average consumption expenditure at ZAR 248,539, with a median of ZAR 140,523[1]Source: Statistics South Africa, "Income & Expenditure Survey (IES)", statssa.gov.za. Local brands are capitalizing on this opportunity by incorporating indigenous South African botanicals like rooibos and marula oil to create authentic, locally-sourced products. Additionally, updated cannabis regulations are redirecting hemp cultivation toward medicinal and cosmetic applications, especially in light of the food ban scheduled for March 2025.

Influence of social media and celebrity endorsement

In South Africa, YouTube beauty vlogs are transforming the purchasing decisions of Gen Y female consumers. According to the World Bank, 76% of individuals in South Africa were internet users in 2023[2]Source: World Bank, "Individuals using the Internet", worldbank.org. This increasing digital connectivity provides brands with instant access to a broad audience. Brands are leveraging platforms like Instagram, TikTok, and YouTube by partnering with celebrity ambassadors and influencers to promote products, thereby boosting awareness and appeal across various demographics. For example, L'Oréal's collaboration with Bonang Matheba at SA Fashion Week in April 2024 expanded their brand reach and generated significant social media engagement. Influencers such as Mihlali Ndamase (partnering with Kenvue), Nomzamo Mbatha (Neutrogena ambassador), and Linda Mtoba (collaborating with Vaseline) achieve high follower engagement, which directly drives sales for their partnered brands. This approach is particularly effective among urban millennials and Gen Z, who frequently use social platforms to discover and research products before purchasing. Additionally, as e-commerce continues to grow, brands are increasingly investing in social media marketing, utilizing influencer content to drive online sales conversions.

Increasing demand for anti-aging products

In South Africa's major metropolitan areas, a growing middle class is increasingly embracing anti-aging products, driven by demographic changes and greater longevity awareness. L'Oréal's March 2024 launch of Melasyl™, designed to address pigmentation issues common in diverse skin tones, highlights how brands cater to local market demands. Similarly, NIVEA's anti-aging guidance, combined with localized pricing strategies, makes premium formulations more accessible, extending their reach beyond traditional luxury consumers. As of 2024, Statistics South Africa reports a significant aging population: 4,475,803 individuals aged 40-44 and 3,462,953 aged 45-49[3]Source: Statistics South Africa, "Mid-year population estimates", statssa.gov.za. Rising awareness of skin aging, influenced by UV exposure, pollution, stress, and lifestyle factors, has shifted consumer priorities toward longevity, prevention, and self-care. As a result, products targeting fine lines, wrinkles, uneven textures, and other aging signs are increasingly regarded as everyday essentials. This segment benefits from growing healthcare awareness and a recovery in disposable incomes. Driving further innovation, L'Oréal's CES 2025 unveiling of Cell BioPrint introduces personalized skin analysis, enhancing anti-aging product recommendations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-driven trading-down behaviour | -0.9% | National, with higher impact in lower-income households | Short term (≤ 2 years) |

| Health Concerns Over Chemical Ingredients | -0.6% | National, Urban educated consumers, particularly in metros | Medium term (2-4 years) |

| Counterfeit and grey-market inflow | -0.8% | National, concentrated in informal retail channels | Long term (≥ 4 years) |

| Fluctuating Raw Material Prices | -0.5% | National, affecting all price segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inflation-driven trading-down behaviour

Inflation is altering consumer behavior in South Africa's skincare market, driving a preference for essential, cost-effective products over premium and specialty items. This trend limits volume growth and puts pressure on brands' pricing and profit margins. Consumers are focusing on basic skincare routines, such as cleansing and moisturizing, while showing reluctance to invest in higher-priced specialty products like anti-aging treatments and serums. Economic challenges are steering consumers toward value-oriented purchases. Rising household debt relative to disposable income is constraining discretionary spending, particularly in the premium skincare segment. This shift benefits mass-market and private-label brands while creating challenges for mid-tier and luxury segments. Retailers are responding by expanding value product lines and increasing promotional efforts to sustain sales volumes despite tighter margins.

Counterfeit and grey-market inflow

Counterfeit products infiltrate markets, posing risks to consumer safety and damaging brand reputations. These products, often sold at lower prices, divert sales from genuine brands, resulting in significant revenue losses for legitimate manufacturers and retailers. This reduces profitability and discourages investment in product development. Counterfeiters exploit lower production costs and avoid taxes and regulatory compliance, creating an unfair competitive environment that hampers growth and innovation for legitimate businesses. Although the Counterfeit Goods Act 37 of 1997 provides a legal framework for enforcement, implementation challenges persist, particularly in informal retail and online marketplaces. For instance, in April 2025, fake Rhode Beauty pop-up scams at Mall of Africa showcased how counterfeiters leverage brand popularity and consumer demand. With cosmetics being a high-risk category for counterfeiting, it is crucial to enhance supply chain verification and consumer education to protect market integrity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Facial Care Dominance Drives Innovation

Facial care Products dominate the market with a commanding 78.65% share in 2025, underscoring the South African consumers' commitment to facial skincare and a shift towards premium formulations. This segment's prominence is largely attributed to heightened awareness of UV protection, an essential consideration in sun-drenched South Africa, and the rising trend of multi-step skincare routines, echoing global beauty movements. Within this realm, cleansers enjoy daily usage, while serums and essences command premium prices, thanks to their concentrated ingredients addressing specific skin issues. Meanwhile, moisturizers and creams see consistent demand across demographics, a testament to South Africa's varied climate and its diverse hydration needs.

While lip care products hold a modest market share, they are on an upward trajectory, boasting a 7.18% CAGR through 2031. This surge is fueled by a growing trend in male grooming and the allure of premium lip treatments. Body care products see tempered growth, as consumers channel their spending towards more visible facial areas. Yet, niche products like foot and hand creams are carving out a space, especially in professional and healthcare environments. A notable trend in this segment is the embrace of local ingredients. Brands are increasingly turning to indigenous botanicals, such as marula oil and rooibos extracts, not just to stand out but to resonate with consumers seeking authenticity.

By Category: Premium Segment Accelerates Despite Mass Market Dominance

The Mass category holds a significant 65.72% market share in 2025, driven by its extensive availability in supermarkets and pharmacies. The mass market thrives on effective distribution networks, with key players such as Shoprite, Pick'n Pay, and Woolworths playing crucial roles. Notably, in September 2024, Woolworths strategically launched its first standalone beauty store in Somerset West to capitalize on the rising demand for beauty products. On the other hand, the Luxury/Premium segment is experiencing robust growth, with a 7.82% CAGR projected through 2031, highlighting a clear shift towards premiumization. This segmentation reflects South Africa's income inequality, where affluent consumers in Gauteng and Western Cape metros drive demand for premium products, while price-sensitive consumers focus on value-driven offerings.

The luxury/premium segment's growth is fueled by several factors, including increased disposable income among higher-earning households, the influence of social media in promoting aspirational beauty standards, and improved product accessibility through e-commerce platforms. Brands like Clarins are achieving notable success in South Africa by leveraging localized marketing strategies and positioning their products to appeal to affluent consumers who value both efficacy and prestige. Furthermore, the segment benefits from the recovery of tourism, as international visitors contribute to luxury beauty sales at major retail locations.

By End User: Male Grooming Emerges as Growth Engine

Women constitute 88.35% of skincare consumers in 2025, highlighting their continued dominance in the market. Skincare brands primarily target women, offering a variety of products such as anti-aging creams, moisturizers, serums, makeup-related skincare, and natural/organic options. Women's regular use of multiple products significantly boosts their market share. On the other hand, the men's segment is expected to grow at an 7.97% CAGR through 2031, reflecting changing perceptions of masculinity and the normalization of grooming. The increasing adoption of male skincare is driven by targeted marketing efforts, celebrity endorsements, and products specifically formulated for men's skin. Additionally, social media serves as a key channel, particularly in engaging younger males who now view skincare as an essential part of self-care rather than vanity.

At the same time, the kids/children's segment is experiencing steady growth, driven by greater parental awareness of skincare and sun protection in South Africa's high-UV environment. Recommendations from pediatric dermatologists and the development of gentle, hypoallergenic products for sensitive skin further enhance this segment's growth. Compliance with SAHPRA guidelines ensures the safety of children's skincare products, strengthening parental confidence in these specialized offerings.

By Ingredient Type: Clean Beauty Movement Gains Momentum

Conventional ingredients command a dominant 70.63% market share in 2025, bolstered by established supply chains, proven efficacy, and cost-effectiveness that resonates with price-sensitive consumers. While synthetic ingredients are favored for their extended shelf life and stable formulations, appealing to manufacturers and retailers prioritizing product reliability, natural and organic formulations are on a robust trajectory, projected to grow at a 7.74% CAGR through 2031. This surge is fueled by rising health consciousness, heightened environmental awareness, and strategic premium positioning. Notably, this growth mirrors global clean beauty trends, with a distinct local flavor: South African consumers are becoming more discerning, closely examining ingredient lists and demanding brand transparency.

The pivot towards natural formulations not only underscores changing consumer preferences but also opens avenues for local ingredient sourcing, spotlighting indigenous plants traditionally used in skincare. Brands such as Frøya Organics are at the forefront, championing clean beauty formulations that eschew controversial chemicals, yet harness the potency of botanical actives. This trend is further bolstered by supply chain advancements, exemplified by companies like Givaudan, which have cemented their presence in South Africa, offering sustainable ingredient solutions tailored for local manufacturers. Moreover, the Foodstuffs, Cosmetics and Disinfectants Act's regulatory framework not only safeguards the safety of natural products but also fosters innovation in botanical formulations.

By Distribution Channel: Digital Commerce Transforms Retail Landscape

Supermarkets and hypermarkets hold a 41.45% market share in 2025, leveraging their convenience, competitive pricing, and wide geographic presence to effectively serve a diverse consumer base. These channels capitalize on established shopping habits and use promotional pricing to attract value-conscious customers. Major chains, such as Shoprite, are expanding their beauty sections and enhancing digital capabilities, as seen with the launch of their Sixty60 delivery service in March 2025, to meet the growing demand for omnichannel shopping.

Online retail stores are expected to grow at a CAGR of 7.88% through 2031, driven by improvements in internet infrastructure, increased smartphone adoption, and evolving consumer preferences favoring digital-first shopping. E-commerce leaders like Takealot.com are achieving strong performance in the beauty category, while niche platforms like Bash.com are offering curated shopping experiences for skincare enthusiasts. Specialist Stores remain relevant by providing expert consultations and collaborating with premium brands. At the same time, Convenience Stores effectively cater to impulse purchases and offer essential skincare products for busy urban consumers.

Geography Analysis

In South Africa, Gauteng stands out as the top province for household consumption expenditure on skincare, while the Western Cape contributes a relatively smaller portion. Combined, these two provinces account for more than half of the nation's total skincare spending. Gauteng and the Western Cape drive market growth due to their higher average household incomes, widespread adoption of urban lifestyles, and significant exposure to international beauty trends through strong business and tourism connections. Cape Town, in particular, reports the highest metro average spending, creating an ideal environment for premium skincare brands to thrive and for the launch of new products. The concentration of affluent consumers in these metropolitan areas allows brands to optimize their marketing budgets and distribution investments, while simultaneously enhancing their brand equity.

As of 2024, urban areas dominate the skincare market, contributing 81.5% of total household consumption expenditure, according to Statistics South Africa. This underscores the market's strong metropolitan focus and the limited opportunities for penetration in rural regions. Skincare brands have aligned their distribution strategies with this urban concentration by prioritizing retail presence in shopping malls, pharmacy chains, and e-commerce platforms that effectively serve city-based consumers. Although rural and traditional areas currently show lower average expenditure, they represent untapped potential for basic skincare product adoption as infrastructure development advances and income levels rise. This geographic disparity creates an opportunity for brands to implement tiered product strategies, offering premium products to metro consumers while introducing value-oriented lines to cater to emerging rural markets.

The South African Health Products Regulatory Authority (SAHPRA) plays a vital role in enhancing regulatory oversight of cosmetic safety standards across the country. This ensures consistent product quality in all provinces, building consumer trust in both locally manufactured and imported skincare brands. The regulatory framework supports market expansion by providing clear and detailed guidelines for product registration, labeling requirements, and safety compliance. These measures enable brands to scale their operations effectively while navigating South Africa's diverse geographic markets with greater confidence and efficiency.

Regulatory Landscape

South Africa's skincare and cosmetics products are primarily governed by the Foodstuffs, Cosmetics and Disinfectants Act, 1972 (Act No. 54 of 1972), with the National Department of Health (NDoH) as the lead authority. For products that sit at the cosmetic-medicine interface, SAHPRA provides a pathway through its Borderline Products Working Group and related guidance, and products making therapeutic claims may be regulated under the Medicines and Related Substances Act (Act 101 of 1965).

In industry practice, compliance is reinforced through self-regulation and codes of practice promoted by the Cosmetic, Toiletry & Fragrance Association of South Africa (CTFA), alongside voluntary South African National Standards (SANS) developed under the SABS standards system for cosmetics and personal care. Market participants continue to monitor draft regulations linked to labelling, advertising, and composition that have been in public-comment processes since 2017, because these influence claim substantiation, on-pack communication, and documentation readiness for both local listings and cross-border trade.

Competitive Landscape

The South African skincare market is moderately fragmented, with international giants maintaining a strong presence alongside emerging local players. This dynamic creates competitive tensions across various price segments and distribution channels. Global leaders like L'Oréal, Unilever, and Estée Lauder utilize their extensive research and development capabilities, broad distribution networks, and significant marketing budgets to retain market share. Meanwhile, local brands such as Norse Organics and Celltone capitalize on their agility, cultural authenticity, and niche positioning to target specific consumer groups. A key trend is the focus on omnichannel distribution, with brands heavily investing in e-commerce and social media marketing to engage digitally-savvy consumers who increasingly research and purchase skincare products online.

Major players in the market include Beiersdorf SA, Unilever Plc, L’Oréal SA, Kenvue Inc., and Environ Skin Care (Pty) Ltd. Strategic expansion through omnichannel distribution networks, particularly partnerships with specialty stores and online platforms, has emerged as a significant trend. The industry has seen a rise in customized and personalized skincare solutions, with companies leveraging digital technologies to provide tailored product recommendations and enhance customer engagement. Additionally, manufacturers are strengthening their market presence by collaborating with dermatologists and skincare specialists to boost product credibility and expand their reach.

White-space opportunities are emerging in areas such as male grooming products designed for South African skin types and climate, affordable dermacosmetic formulations for mass-market consumers, and premium natural products featuring indigenous botanical ingredients. Technology adoption is driving competitive differentiation, as demonstrated by L'Oréal's Cell BioPrint personalized skin analysis platform, unveiled at CES 2025, which highlights how brands are using AI and data analytics to deliver customized product recommendations and improve customer engagement. Emerging disruptors are focusing on direct-to-consumer models, sustainable packaging solutions, and ingredient transparency, appealing to environmentally-conscious consumers seeking authentic brand connections beyond traditional marketing methods.

South Africa Skincare Product Industry Leaders

-

Beiersdorf SA

-

UnileverPlc

-

L’Oréal SA

-

Environ Skin Care (Pty) Ltd

-

Kenvue Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Dermacosmetics and other clinically positioned skincare are a key whitespace area in South Africa, especially for brands that need to balance efficacy claims with compliant classification at the cosmetic-medicine boundary. SAHPRA's borderline-product guidance creates an operational need for claim and evidence strategies, supporting opportunities for manufacturers and brand owners that build clinically backed portfolios while keeping products within cosmetic frameworks where appropriate (and shifting to medicines or devices where required).

Distribution and manufacturing capability expansion also create room for faster product iteration and wider assortment localization. In March 2026, Prime Product Manufacturing's acquisition of L'Oreal South Africa's Midrand production facility pointed to growing local contract manufacturing capacity, which can support shorter lead times, localized SKUs, and new entrants seeking South African-made supply without building greenfield plants. On the demand side, named retail partnerships and new launches, including Altruist entering via Clicks and Sel:pH Skincare launching through Truworths, support opportunities for curated pharmacy and fashion retail channels. At the ingredient level, indigenous botanicals such as rooibos and marula remain a practical route for local brands to premiumize and for multinationals to localize.

Recent Industry Developments

- June 2026: NtryMed launched a new face serum in South Africa, expanding its range around barrier-supporting, non-irritating formulations tailored to local climate conditions. The new product adds competitive pressure in clinically positioned facial care, where consumers compare actives, tolerability, and routine compatibility rather than brand heritage alone.

- April 2025: Unilever expanded its skincare adjacency with the launch of the Vaseline Cera-Glow body care range in South Africa, featuring Pro-Ceramide Technology. The rollout reinforces active-led mass-market innovation and supports wider on-shelf differentiation in body care beyond basic moisturization.

- September 2024: Woolworths opened its first standalone beauty store in Somerset West, Western Cape, expanding dedicated retail space for premium beauty and skincare alongside consultation-led service. The format strengthens premium distribution in an affluent metro catchment and raises the bar for in-store experience among organized retailers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers professional skincare products sold and used through professional and advised channels in South Africa, and it is measured in value terms in USD for the study years.

Scope exclusions: We exclude professional services and procedure revenues (such as facials and in-clinic treatments) and count only product sales.

Segmentation Overview

-

Product Type

-

Facial Care Products

- Cleansers

- Moisturizers and creams

- Serums and Essence

- Toners

- Face Masks

- Other Facial Care Products

-

Body Care Products

- Body Lotion

- Foot and Hand Cream

- Other Body Care Products

- Lip Care Products

-

Facial Care Products

-

Category

- Mass

- Luxury/Premium

-

End User

- Men

- Women

- Kids/Children

-

Ingredient Type

- Conventional

- Natural/Organic

-

Distribution Channels

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialist Stores

- Online Retail Stores

- Other Distribution Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building the South Africa country context and demand anchors that can be checked year over year. We use public sources such as Statistics South Africa releases, SARS trade statistics, South African Reserve Bank inflation and exchange-rate series, and international references such as UN Comtrade and World Bank indicators to understand import exposure and consumer conditions.

On the supply and channel side, we review company annual reports, investor decks, product catalogs, retailer and pharmacy website listings, and reputable press for launch timelines and pricing bands. Where needed, we also use paid subscriptions for company financials and for shipment-level import and export reads, which helps us test whether local sales direction is consistent with trade movement. The sources listed here are illustrative, and many other public documents and datasets were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focuses on converting desk assumptions into realistic shares and price ranges for professional skincare products, especially where public data is broad for total skincare. We interview and survey a mix of brand owners, distributors, salon and clinic decision-makers, and retail channel operators across key provinces, and then we recheck any large variance points before locking the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 12% | |

| Mid tier: 40% | Functional/Unit leaders: 40% | |

| Smaller Players: 22% | Managers: 48% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where the total skincare value pool is reconstructed for South Africa and then filtered into the professional-only portion using channel and product mapping. To keep the totals realistic, we corroborate results with selective bottom-up approximations, such as sampled price-per-unit times estimated sell-out volumes by channel, followed by distributor and salon throughput checks.

Inputs that materially shape the model include professional-channel penetration within skincare, product mix between face care and body care, observed retail and professional price ladders, packaging mix (tubes, bottles, jars) that influences typical pack sizes, and channel split between offline and online. When a data gap appears, we apply conservative proxy shares that are then stress-tested in interviews and adjusted only when a consistent story is heard across respondent groups.

For forecasting, scenario analysis is used with a base case built around inflation and currency timing, expected premiumization within advised skincare, and channel expansion pace for pharmacies, specialist stores, and e-commerce. Assumptions are kept simple and traceable so each annual step can be recreated and explained without relying on inaccessible data.

Data Validation & Update Cycle

Outputs are checked against independent signals such as import value trends, observed pricing movement, and channel expansion announcements so the direction and scale stay consistent. Any sharp jumps trigger an analyst review that revisits the mix, pricing, and penetration assumptions, and we may re-contact sources when a variance cannot be explained by a known market event.

Before sign-off, the model is reviewed in multiple steps, including cross-checking calculation logic and verifying that the scope rules are applied consistently across years. The report is refreshed annually, and interim updates are made when material events occur, after which a final pre-delivery pass is completed so clients receive an up-to-date view.

Mordor Intelligence's South Africa Professional Skincare Product Market Sizing Compared With Other Published Estimates

Published numbers for this market can look far apart because the term skincare is sometimes treated as a broad consumer category and sometimes narrowed to products sold through salons and clinics. Differences also come from how pricing is averaged, which exchange rate timing is used, and whether online channels are counted as professional when they sell similar items.

Some external estimates roll up the overall South Africa skincare products market regardless of whether sales are professional-advised or mass retail. In Mordor Intelligence sizing, value is counted only for professional skincare products in South Africa, and procedure or service revenues are excluded, with the 2026 total anchored to channel splits and packaging-linked price bands that were checked in primary calls.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 890.81 M (2026) | |

| Industry Publisher A | USD 301.77 M (2026) | This figure appears to emphasize clinic and medispa routed sales and may undercount professional products sold through broader offline retail and online channels, which compresses the addressable value pool. |

| Industry Publisher B | USD 24.91 M (2023) | This estimate is stated for the wider skin care products market but at a much smaller scale, which suggests a narrower product basket, different currency conversion timing, or partial channel coverage that does not capture professional price points and mix. |

The spread is mainly explained by how strictly the professional channel is defined and whether only a subset of outlets is treated as eligible. By keeping the scope tied to product sales, applying consistent USD conversion timing, and validating channel shares through interviews, the model stays balanced and repeatable year to year.

Key Questions Answered in the Report

What is the projected value of South Africa’s skin care market by 2031?

The market is forecast to reach USD 1,248.38 million by 2031.

Which product segment is expected to grow the fastest through 2031?

Lip Care Products are set to record the highest growth at a 7.18% CAGR.

How quickly will online retail sales for skin care expand in South Africa?

Sales through online retail channels are projected to advance at an 7.88% CAGR to 2031.

What share of current South African skin care spending comes from female consumers?

Women account for 88.35% of total spending as of 2025.

Page last updated on: