Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 34.73 Billion |

| Market Size (2026) | USD 36.17 Billion |

| Market Size (2031) | USD 44.32 Billion |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Skin Care Products Market Analysis by Mordor Intelligence

The Europe skin care products market size was valued at USD 34.73 billion in 2025 and estimated to grow from USD 36.17 billion in 2026 to reach USD 44.32 billion by 2031, at a CAGR of 4.15% during the forecast period (2026-2031). This steady growth is attributed to a combination of factors, including an aging population that drives demand for anti-aging and specialized skin care solutions, the implementation of stricter European Union (EU) safety regulations ensuring product quality and consumer protection, and a rising preference for clinically validated and environmentally sustainable formulations. Despite the market's maturity, facial care continues to dominate as the largest revenue segment, while the increasing adoption of e-commerce platforms contributes to incremental sales growth. Additionally, initiatives promoting refillable packaging are fostering consumer trust, particularly in response to Directive 2024/825, which aims to curb misleading greenwashing practices. Although the market remains fragmented, mergers and acquisitions and advancements in artificial intelligence (AI)-driven research and development are elevating innovation standards. However, challenges such as the infiltration of counterfeit products and heightened price sensitivity in Southern and Eastern Europe are tempering the pace of expansion. Germany leads the market with a 22.56% share of the Europe skin care products market, while Poland is emerging as the fastest-growing market in the region.

Key Report Takeaways

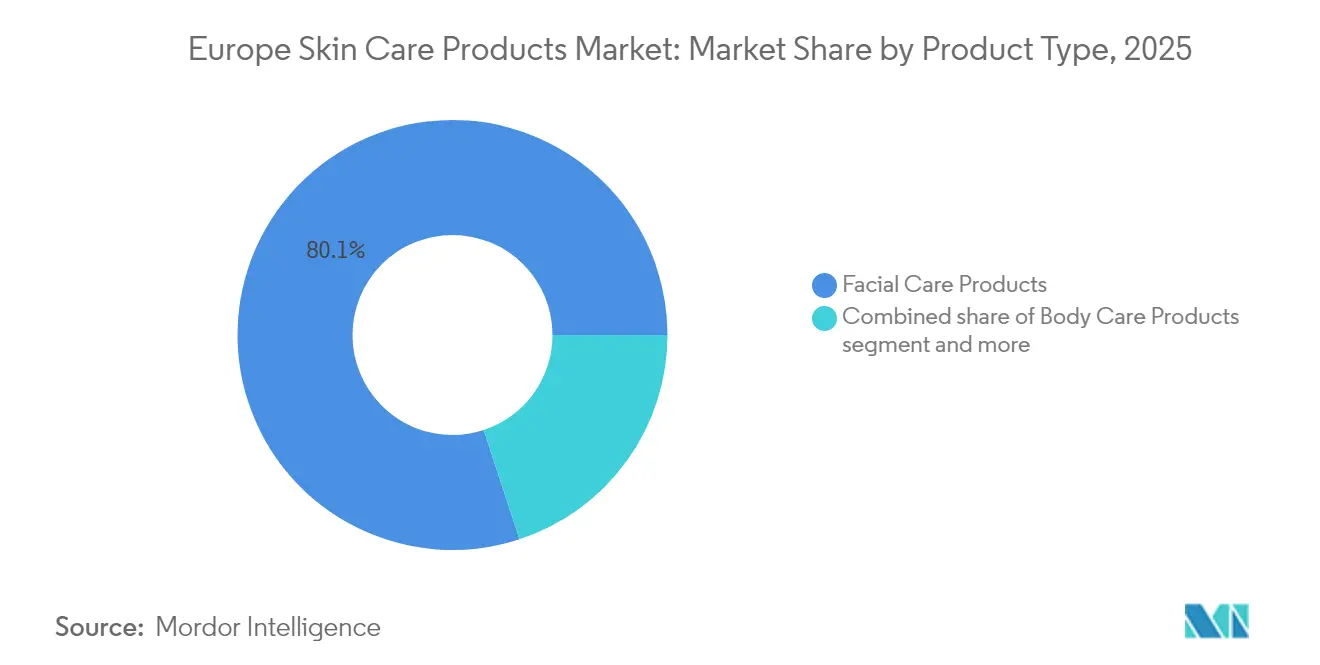

- By product type, facial care products accounted for 80.05% of Europe skin care products market share in 2025 and is set to expand at a 5.63% CAGR through 2031.

- By category, the mass segment held 66.74% of the Europe skin care products market size in 2025, while luxury/premium is forecast to grow at a 5.12% CAGR.

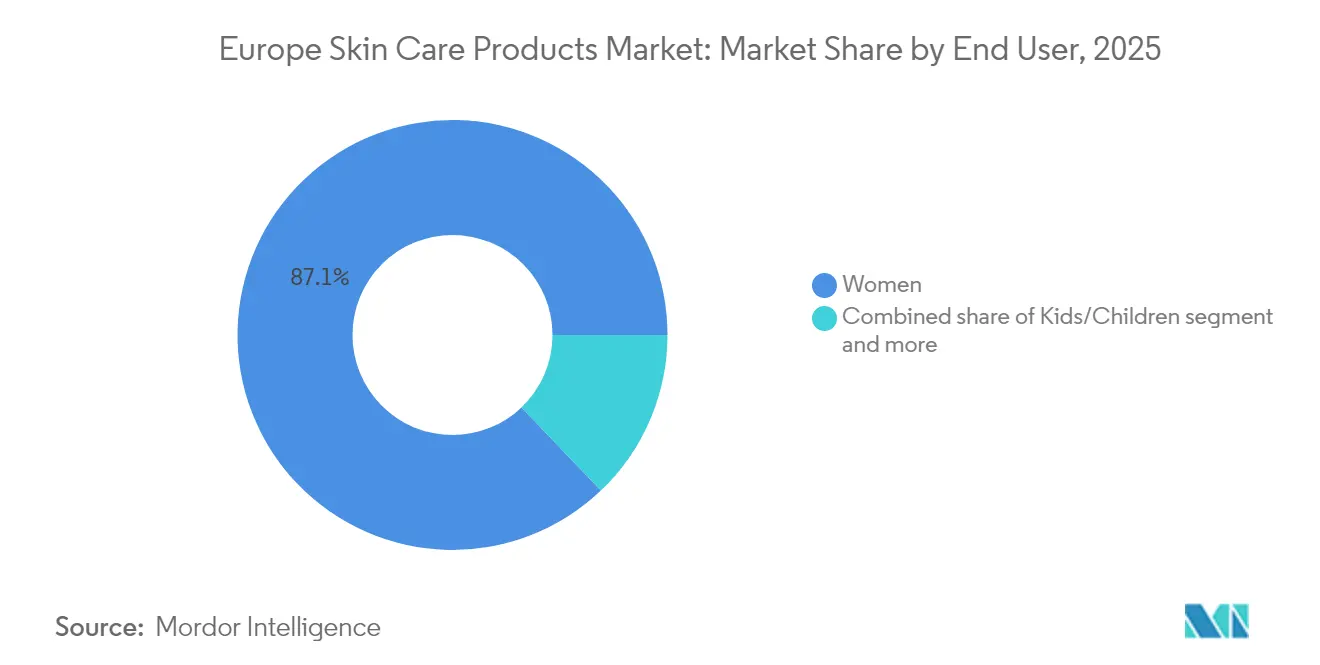

- By end user, women generated 87.12% of 2025 sales, yet the kids/children cohort is projected to rise at a 6.63% CAGR to 2031

- By ingredient type, conventional and synthetic formulations represented 69.88% of 2025 value, and natural and organic ingredients are slated to grow at a 6.74% CAGR.

- By distribution channel, health and beauty stores captured 34.92% of 2025 spending, whereas online retail is climbing at a 6.21% CAGR.

- By geography, Germany accounts for 22.31% of 2025 spending, while Poland is experiencing a CAGR of 6.91%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Skin Care Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population driving anti-ageing demand | +1.2% | Germany, Italy, France, Spain (highest median ages); broader Euroean Union (EU 27) + United Kingdom | Long term (≥ 4 years) |

| Rising consumer shift to natural and organic products | +0.9% | Germany, Netherlands, Sweden, France (strong green consumer base) | Medium term (2-4 years) |

| Growth of refillable and solid formats amid packaging-waste rules | +0.6% | France, Germany, Netherlands (early adopters of circular economy mandates) | Medium term (2-4 years) |

| Rising male grooming and Gen Z skin care adoption | +0.8% | United Kingdom, Germany, France, Spain (urban centers with younger demographics) | Short term (≤ 2 years) |

| E-commerce and DTC acceleration | +1.0% | Germany (20% online penetration), United Kingdom, Poland, Spain (high growth rates) | Short term (≤ 2 years) |

| Increasing demand for clinically and dermatologically tested skin care products | +0.7% | Global, with strongest uptake in Germany, France, Italy (pharmacy-channel heritage) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ageing population driving anti-ageing demand

Europe's demographic profile, with 21.6% of the population aged 65 or older and a median age of 44.7 years, continues to drive consistent demand for anti-aging formulations that address key concerns such as wrinkle depth, loss of skin elasticity, and hyperpigmentation [1]Source: Eurostat, “Demography of Europe – 2024 edition,” ec.europa.eu. Vichy's upcoming November 2025 launch of LiftActiv Derm Source, a product developed over a decade of research and protected by seven patents, underscores the increasing emphasis on pharmaceutical-grade active ingredients. The formulation, containing a 5% concentration of rhamnose, demonstrated significant efficacy in a consumer trial involving 800 women over two months, achieving a 20% reduction in forehead and crow ''s-feet wrinkles and a 17% reduction in glabellar lines. Notably, within the 65-plus age group, the over-80 demographic is growing at the fastest rate, fueling demand for advanced skin care solutions such as barrier-repair ceramides and peptides that cater to thinning skin and impaired wound healing. Additionally, L'Oréal's June 2025 announcement of its Longevity Integrative Science platform, which includes the innovative Cell BioPrint lab-on-a-chip technology capable of analyzing over 260 skin longevity biomarkers in under five minutes, signals a strategic shift from corrective treatments to preventive care. This approach has the potential to unlock new revenue streams in wellness-adjacent categories, reflecting the evolving priorities of the aging population.

Rising consumer shift to natural and organic products

The demand for natural and organic skin care ingredients is experiencing significant growth, with a compound annual growth rate (CAGR) of 7.12% projected through 2030, notably outpacing the market average of 4.35%. This trend is largely driven by shifting consumer preferences, as 64% of European consumers indicate a willingness to pay a premium for eco-friendly products, and 78% report that sustainability plays a key role in their purchasing decisions. The COSMOS (COSMetic Organic and Natural Standard) certification has become the recognized benchmark in the industry, with over 34,000 products now certified under this standard. However, the introduction and enforcement of Directive 2024/825 on greenwashing are compelling brands to validate their sustainability claims through rigorous lifecycle assessments and third-party audits. In response to these evolving demands, Givaudan is set to launch RetiLife in May 2025, marking the debut of the first 100% natural-origin retinol, produced through the fermentation of plant sugars with sunflower oil as a carrier. This innovation addresses the concerns of clean-beauty advocates who often "blacklist" synthetic retinol, positioning biotech-derived actives as a viable and scalable alternative to petrochemical-based ingredients. Additionally, Chemyunion's Ecoffea Citrus, an upcycled botanical extract sourced from coffee and lemon, exemplifies the growing intersection of circularity and efficacy. This ingredient, which has been shown to enhance collagen types I, III, IV, and fibronectin within 28 days, resonates strongly with German and Dutch consumers who prioritize transparency in ingredient sourcing and sustainability in their skin care choices.

Growth of refillable and solid formats amid packaging-waste rules

Guerlain's Orchidée Impériale refill system, crafted from 90% cellulose combined with a protective polymer film, exemplifies how luxury brands are addressing sustainability challenges. This system reduces material usage by over 40% from the first refill cycle and decreases environmental impact by 50% over a year, showcasing sustainability as a viable strategy to enhance profit margins. Similarly, Bioderma's December 2025 launch of Hydrabio Eau de Soin, a water-based facial mist with SPF (Sun Protection Factor) 30, delivered through a perfume-style pump that eliminates the need for aerosol propellants, reflects a commitment to innovative, low-waste packaging solutions. This approach aligns with the preferences of environmentally conscious consumers in France and Germany, who value environmental impact as much as product efficacy. Furthermore, solid formats, including bar cleansers, shampoo bars, and concentrated serums, are becoming increasingly popular in markets like the Netherlands and Sweden, where zero-waste retail concepts have shifted from niche offerings to mainstream adoption. Compliance with ISO (International Organization for Standardization) 14021 standards for environmental claims is now a critical requirement for securing shelf space in leading drugstore chains, compelling brands to prioritize transparent supply-chain documentation and third-party verification to meet these evolving standards.

Rising male grooming and Gen Z skincare adoption

Male grooming and the increasing adoption of skin care by Generation Z (Gen Z) are driving significant growth in the market's compound annual growth rate (CAGR). Notably, 68% of Gen Z men in the United States now use facial skin care products, a behavioral shift that is also evident in urban centers across the United Kingdom (UK), Germany, France, and Spain. Yves Rocher has announced plans to launch an on-site marketplace in September 2024, featuring Monsieur Barbier, a specialist in men's grooming. This initiative reflects a strategic approach to expanding complementary product categories, thereby increasing the average basket size. The platform is set to host 50 brands and aims to expand its reach to Asian and U.S. markets within three years. Similarly, GIVET is preparing to introduce SKINSOO, a Korean dermocosmetics brand, in July 2025 across 27 European markets. This launch is designed to appeal to "K-beauty enthusiasts, results-focused and ingredient-literate consumers of all genders and ages," signaling a shift toward efficacy-driven formulations that challenge traditional gender-based segmentation in the skin care category. Furthermore, Gen Z's preference for minimalist skin care routines, with 62% of them favoring a maximum of three products, is reshaping product development trends. For instance, Dior's Capture Crème Regard combines anti-dark-circle ingredients such as Chaga mushroom extract and caffeine with Micro-Light Diffusing technology, which incorporates 100% natural-origin pearlescent particles. Additionally, social-commerce platforms are playing a pivotal role in product discovery, with 70% of Gen Z purchasing beauty products online or through mobile applications. This shift presents significant opportunities for direct-to-consumer brands to bypass traditional retail intermediaries and engage directly with their target audience.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent European Union safety and claim regulations | -0.5% | European Union 27 (harmonized enforcement under Regulation 1223/2009 and amendments) | Long term (≥ 4 years) |

| Counterfeit products and parallel imports affecting brand trust | -0.4% | Italy, Spain, Poland (higher incidence of grey-market channels) | Medium term (2-4 years) |

| Consumer skepticism over greenwashing claims | -0.3% | Germany, Netherlands, Sweden (high environmental literacy) | Short term (≤ 2 years) |

| Premium pricing of organic and natural products | -0.6% | Southern and Eastern Europe (price-sensitive markets: Spain, Poland, Italy) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent European Union safety and claim regulations

The European Union's (EU) Regulation 1223/2009, along with its amendments, enforces comprehensive safety assessments, imposes restrictions on ingredients, and requires substantiation of product claims. These measures extend product development timelines by 12 to 18 months and increase compliance costs by an estimated 15% to 20%. Furthermore, Regulation 2025/877, which bans carcinogenic, mutagenic, and reprotoxic (CMR) substances in cosmetics, and the upcoming 2025 prohibition of titanium dioxide (TiO₂) in leave-on products, compel manufacturers to reformulate thousands of stock-keeping units (SKUs), with sunscreens and color cosmetics being particularly affected. Adding to these challenges, Directive 2024/825 on greenwashing introduces mandatory lifecycle assessments and third-party audits for environmental claims, raising the standards for labeling products as "natural," "organic," or "eco-friendly" and exposing brands that rely on ambiguous marketing language. Highlighting the innovation demands in this regulatory environment, Skinosive announced in April 2025 the development of bio-adhesive UV filters, which have been validated to extend sunscreen efficacy up to eight hours while minimizing environmental release. The company plans to submit its first regulatory file to the European Commission in June 2025 but acknowledges that navigating the EU's lengthy and complex regulatory processes remains a significant barrier to market entry. These regulatory pressures disproportionately impact smaller brands and independent disruptors, as they face higher compliance costs relative to their resources, thereby creating a competitive advantage for multinational corporations equipped with dedicated regulatory teams and advanced testing infrastructure.

Counterfeit products and parallel imports are affecting brand trust

The European Union Intellectual Property Office (EUIPO) estimates that counterfeit cosmetics lead to significant annual losses of EUR 3 billion (USD 3.3 billion). Alarmingly, 16% of cosmetics seized at borders are identified as counterfeit, posing serious risks to brand equity and consumer safety [2]Source: European Union Intellectual Property Service, “Economic impact of counterfeiting in the clothing, cosmetics, and toy sectors in the EU,” euipo.europa.eu. These counterfeit products often contain unregulated formulations with potentially harmful contaminants. Additionally, the issue of parallel imports, where legitimate products are diverted from lower-priced markets into premium geographies, further disrupts authorized pricing structures and weakens brand positioning. This challenge is particularly pronounced in countries like Italy, Spain, and Poland, where grey-market channels are estimated to account for 10% to 15% of luxury skin care sales. Online marketplaces, such as Amazon, have amplified these challenges. The platform’s rapid growth in beauty sales has attracted third-party sellers who list counterfeit or diverted products alongside authorized inventory, complicating enforcement efforts and creating confusion for consumers. To combat these issues, brands are increasingly turning to serialization technologies, including QR codes, blockchain-based provenance tracking, and tamper-evident packaging. However, the high costs associated with implementing these measures remain a barrier for mid-tier companies. Furthermore, the rise of social-commerce platforms like TikTok Shop and Instagram Checkout has introduced new avenues for counterfeit distribution. Influencer-driven sales on these platforms often bypass traditional gatekeepers and regulatory oversight, adding another layer of complexity to the fight against counterfeit products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Facial Care Dominance Fueled by Anti-Ageing Innovation

Facial care products accounted for 80.05% of 2025 revenue and are projected to grow at a rate of 5.63% through 2031, surpassing the market average growth rate of 4.15%. This growth is driven by consumer demand for serums, essences, and targeted treatments addressing concerns such as wrinkle depth, hyperpigmentation, and skin barrier integrity. While cleansers and moisturizers continue to lead in volume, serums and essences are the fastest-growing sub-segments. This trend is fueled by high-concentration active ingredients like peptides, retinoids, and hyaluronic acid, which offer measurable results. For instance, Vichy's November 2025 launch of LiftActiv Derm Source, containing 5% rhamnose and protected by seven patents, demonstrated a 20% reduction in forehead and crow's-feet wrinkles in a consumer trial involving 800 women. This highlights the growing credibility of pharma-derived actives as alternatives to injectables.

Lip care remains a stable category, with SPF-infused balms and tinted treatments gaining incremental market share as consumers increasingly prefer multifunctional products that combine hydration, sun protection, and color correction in a single SKU. Additionally, the European Union's ban on titanium dioxide (TiO₂) in leave-on products, effective from 2025, is driving reformulation efforts in lip balms and sunscreens. This regulatory change is creating opportunities for mineral-based alternatives like zinc oxide and innovative UV filters, such as Skinosive's bio-adhesive molecules.

By Category: Mass Holds Ground While Luxury/Premium Gains via Dermatological Credibility

The mass segment accounted for 66.74% of 2025 revenue, driven by drugstore chains such as DM-Drogerie Markt, Rossmann, and Müller in Germany, as well as Boots and Superdrug in the United Kingdom. These retailers focus on private-label dermatological products and value-oriented assortments. Beiersdorf's planned mid-2025 launch of NIVEA Cellular Epigenetics, incorporating the patented Epicelline active ingredient previously exclusive to the luxury Eucerin line, reflects a strategic effort to make longevity science more accessible and protect its mass-segment market share from premium competition.

The luxury/premium segment is projected to grow at a rate of 5.12% through 2031, supported by factors such as dermatological credibility, experiential retail formats, and refillable packaging that resonate with affluent consumers prioritizing sustainability and product efficacy over cost. Sephora's approximately 860 European stores generate EUR 4.16 million (USD 4.6 million) in revenue per location, the highest productivity among specialty retailers. This performance is attributed to exclusive brand offerings, loyalty programs, and in-store consultations that enhance customer differentiation.

By End User: Women Dominate, Yet Kids/Children Segment Accelerates on Safety Concerns

Women accounted for 87.12% of the end-user demand in 2025, aligning with established historical trends in the category. However, the kids/children segment is witnessing significant growth, expanding at a compound annual growth rate (CAGR) of 6.63% through 2031, making it the fastest-growing end-user group. This growth is primarily driven by increasing parental preference for hypoallergenic and fragrance-free formulations that comply with the European Union (EU) cosmetics safety standards. The EU's upcoming 2025 ban on titanium dioxide (TiO₂) in leave-on products, alongside Regulation 2025/877, which prohibits the use of carcinogenic, mutagenic, and reprotoxic (CMR) substances, is compelling brands to reformulate products such as children's sunscreens, moisturizers, and cleansers. Leading brands like Mustela, Weleda, and Bioderma are at the forefront of this category.

Furthermore, Yves Rocher's September 2024 launch of Ouate, a product line dedicated to children's and baby hygiene, underscores a strategic initiative to diversify into complementary categories. This approach aims to enhance basket size and capture lifecycle value as parents transition from baby care to toddler and pre-teen skin care products. The men's segment, while not individually quantified in the approved metrics, is integrated within the broader end-user mix and is experiencing notable growth, driven by the increasing adoption of skin care routines among Generation Z (Gen Z). For instance, 68% of Gen Z men in the United States now use facial skin care products, reflecting a significant behavioral shift. This trend is also mirrored in urban centers across key European markets, including the United Kingdom (UK), Germany, France, and Spain, highlighting a growing opportunity within this demographic.

By Ingredient Type: Conventional Holds Majority, Yet Natural/Organic Gains via Biotech Breakthroughs

Natural and organic ingredients are projected to grow at a compound annual growth rate (CAGR) of 6.74% through 2031, marking the fastest growth among all ingredient types. Despite this rapid expansion, conventional and synthetic formulations are expected to maintain a significant market share, accounting for 69.88% of 2025 revenue. This highlights the continued reliance on established chemistries due to their proven efficacy and cost-effectiveness. Givaudan's planned launch of RetiLife in May 2025, the first 100% natural-origin retinol produced through the fermentation of plant sugars, addresses the concerns of clean-beauty advocates who have criticized synthetic retinol. This innovation positions biotechnology-derived actives as a viable and scalable alternative to petrochemical-based ingredients, aligning with the increasing demand for sustainable solutions. Similarly, Chemyunion's Peptid4 B-Like, a synthetic tetrapeptide that mimics the mechanism of botulinum toxin, demonstrated a 20% reduction in periorbital (around the eye) wrinkles during clinical trials. This product showcases the successful integration of green chemistry principles with high-performance actives, appealing to consumers who prioritize visible results over ingredient origin.

According to the Soil Association, organic health and beauty product sales in the United Kingdom (UK) reached GBP 136 million in 2023, encompassing skin care, cosmetics, and wellness items . This growth reflects the increasing consumer preference for organic and sustainable products, further driving innovation in the natural and organic segment. Conventional and synthetic ingredients continue to dominate formulations in the mass-market segment, where cost efficiency and shelf stability are critical factors. Beiersdorf's Epicelline, a patented epigenetic active developed over 15 years of research, exemplifies how synthetic actives can transcend price tiers when supported by robust clinical validation. This active ingredient is featured in both the premium Eucerin product line and the more affordable NIVEA Cellular Epigenetics serum, demonstrating its versatility and broad consumer appeal. The ability of synthetic actives like Epicelline to deliver scientifically validated benefits ensures their continued relevance across diverse market segments, from luxury to mass-market offerings.

By Distribution Channel: Health and Beauty Stores Lead, Yet Online Retail Surges

Health and beauty stores accounted for 34.92% of the 2025 distribution, driven by Germany's leading drugstore chains: DM Drogerie Markt (DM), Rossmann, and Müller. DM operates approximately 4,000 stores, generating EUR 12 billion in revenue with a per-store productivity of EUR 3.0 million. Rossmann, with around 4,700 stores, reports EUR 10 billion in revenue and a per-store productivity of EUR 2.13 million. Müller, which operates approximately 900 stores, achieves EUR 4 billion in revenue and a per-store productivity of EUR 4.44 million. These retailers focus on offering private-label dermatological products and emphasize sustainability in their branding and messaging, which resonates strongly with environmentally conscious consumers.

Online retail stores are expected to grow at a compound annual growth rate (CAGR) of 6.21% through 2031, which is nearly 50% faster than the overall market growth rate. Amazon has reported significant growth in its beauty and personal care segment, with a 43% increase in sales in France during the first quarter of 2025. Germany continues to lead the European market with a 20% online penetration rate for beauty and personal care products, reflecting the increasing consumer preference for the convenience and variety offered by e-commerce platforms.

Geography Analysis

Germany held 22.31% of the 2025 market share, making it the largest single-country contributor. This leadership is supported by a robust network of drugstore chains, including DM-Drogerie Markt, Rossmann, and Müller, which collectively operate over 9,000 stores. These retailers focus on private-label dermatological products and emphasize sustainability in their messaging. Additionally, Germany's 20% online penetration rate in beauty and personal care, the highest in Europe, reflects advanced digital infrastructure and consumer confidence in e-commerce. German consumers, known for their high environmental literacy, scrutinize ingredient sourcing, carbon footprints, and product disposal. Brands that provide detailed sustainability data gain consumer trust, while those with vague claims face challenges.

Poland is the fastest-growing market, with a projected compound annual growth rate (CAGR) of 6.91% through 2031. This growth is fueled by rising disposable incomes, an 18% year-on-year increase in online health and beauty orders, and localized product launches by multinational brands aiming to capture Central European demand before market saturation. Spain, the Netherlands, Belgium, and Sweden also contribute to the market, each showcasing distinct consumer preferences and regulatory landscapes. The Netherlands and Sweden lead in zero-waste retail concepts and solid-format product adoption, driven by high environmental awareness and government incentives promoting circular-economy initiatives. Belgium's 100% increase in Korean beauty (K-beauty) imports in 2024 highlights a growing demand for innovative formulations and ingredient transparency, areas where domestic brands have been slower to respond. The Rest of Europe category, encompassing smaller markets such as Austria, Portugal, Greece, and the Nordics, exhibits a fragmented landscape. Achieving success in these markets necessitates localized distribution partnerships and strict compliance with regulatory requirements. The European Union's (EU) harmonized cosmetics regulations under Regulation 1223/2009 facilitate cross-border expansion. However, cultural preferences differ notably across regions. Southern European consumers emphasize sun protection and brightening products, whereas Northern Europeans prioritize barrier repair and anti-pollution solutions. Developing tailored product portfolios and marketing strategies is crucial to effectively address these regional variations.

Regulatory Landscape

Skin care products marketed across Europe are primarily governed by EU Cosmetics Regulation (EC) No 1223/2009, which sets rules for product safety, labeling, responsible person obligations, and the substance lists in Annexes II to VI. In 2026, compliance requirements tightened further through Commission Regulation (EU) 2026/78 (published January 2026, applicable from May 1, 2026), updating multiple annexes and reinforcing restrictions linked to substances classified as carcinogenic, mutagenic, or toxic for reproduction (CMR). This increases the reformulation and dossier-maintenance burden for affected products.

Ingredient-specific conditions were also updated via Commission Regulation (EU) 2026/909 (published April 27, 2026), amending the cosmetics framework for ingredients including Benzyl Salicylate, Aluminium compounds, Citral, and DHHB. Scientific Committee on Consumer Safety (SCCS) opinions continue to anchor many of these changes, and the cadence of annex updates raises the need for continuous regulatory surveillance and faster change control across formulation, packaging, and claims substantiation workflows.

Competitive Landscape

The Europe skin care products market is moderately fragmented, with global leaders such as L'Oréal, Beiersdorf, Unilever, Estée Lauder, Procter & Gamble, and Shiseido dominating the landscape. These companies coexist with regional players such as Clarins, Pierre Fabre, and Galderma, as well as independent brands that leverage direct-to-consumer models and social-commerce platforms. L'Oréal's acquisition of a 10% stake in Galderma in August 2024 underscores its strategic focus on injectable aesthetics and prescription dermatology, complementing its over-the-counter skin care offerings and positioning the company to capture opportunities across the beauty-to-medical spectrum.

The fastest-growing segment includes innovations in longevity science, microbiome modulation, and bio-adhesive delivery systems. For example, Skinosive's bio-adhesive UV (ultraviolet) filters, which extend sunscreen efficacy up to eight hours, highlight advancements where regulatory approval timelines provide a competitive edge for early movers. Similarly, disruptors like GIVET, which launched SKINSOO Korean dermocosmetics across 27 European markets in July 2025, are capitalizing on K-beauty expertise, plant-based exosomes, and liposomal delivery systems to challenge incumbents slower to adopt biotech-derived actives.

Other factors influencing the market include the integration of technology and the challenge of counterfeit products. AI-powered formulation platforms, such as Shiseido's VOYAGER, L'Oréal's Longevity AI (Artificial Intelligence) Cloud analyzing over 260 skin biomarkers, and Estée Lauder's AI Innovation Lab in collaboration with Microsoft, are transforming research and development processes and enabling hyper-personalized product recommendations. Meanwhile, counterfeit products and parallel imports remain significant risks. The European Union Intellectual Property Office (EUIPO) estimates annual losses of EUR 3 billion (USD 3.3 billion) due to counterfeit cosmetics, with 16% of seized cosmetics at borders identified as fake. To address these issues, brands are investing in serialization technologies, blockchain-based provenance tracking, and tamper-evident packaging to protect their products and maintain consumer trust.

Europe Skin Care Products Industry Leaders

Beiersdorf AG

L'Oréal S.A.

Unilever plc

The Procter & Gamble Company

The Estée Lauder Companies Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory-driven reformulation and claims substantiation are creating whitespace for suppliers and brands that can industrialize compliant alternatives, especially in sensitive areas such as facial care, sun protection, and fragrance-allergen-adjacent positioning. Directive (EU) 2024/825, binding across the EU from September 27, 2026, raises the bar for environmental and sustainability messaging, increasing the value of third-party verification, lifecycle evidence, and packaging choices that can be defended across retail and online channels.

Capacity additions and upstream investments also point to opportunities in localized, resilient supply chains for skin care actives and bases. In July 2026, BASF inaugurated a new specialty emollients production plant in Dusseldorf, Germany, supporting skin care and sun protection formulations, while Pierre Fabre announced a EUR 50 million investment (May 2026) to double production capacity at its Avène skin care plant in southern France by 2029. Alongside these moves, large beauty groups are strengthening science-led positioning, such as L'Oréal's longevity-focused biomarker approach, reinforcing demand for clinically validated products and ingredient transparency in major markets including Germany and France.

Recent Industry Developments

- January 2026: Beiersdorf launched NIVEA Creme Natural Touch in Germany as a line extension of the iconic blue tin, featuring a vegan formula with 99% natural-origin ingredients. The company targeted shoppers actively trading into natural-origin propositions while staying within a high-volume mass brand franchise. This approach supports shelf competitiveness in core European drugstore channels.

- September 2025: Doré introduced two new skin care products in partnership with Evolved By Nature, integrating peptide biotechnology into a simplified, clinically positioned routine. The collaboration highlights how biotech-derived actives are being used to differentiate in crowded facial care segments where efficacy claims and ingredient narratives influence conversion. It also reinforces a clearer clinical angle within clean-beauty positioning.

- August 2024: L'Oréal acquired a 10% stake in Galderma, adding deeper exposure to prescription dermatology and injectable aesthetics adjacent to its over-the-counter skin care portfolio. The investment strengthens L'Oréal's ability to connect medical-grade credibility with mainstream skin care innovation. It shapes competitive positioning across premium and dermocosmetic channels in Europe.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers retail and professional sales value of skin care products purchased and used in Europe, across common formats meant to cleanse, treat, protect, and moisturize the skin.

Scope exclusions: Color cosmetics, fragrances, and hair care products are not counted in this market value.

Segmentation Overview

- By Product Type

- Facial Care Products

- Cleansers

- Moisturizers and Creams

- Serums and Essences

- Toners

- Face Masks

- Other Facial Care Products

- Body Care Products

- Body Lotions

- Foot and Hand Creams

- Other Body Care Products

- Lip Care Products

- Facial Care Products

- By Category

- Mass

- Luxury/Premium

- By End User

- Men

- Women

- Kids/Children

- By Ingredient Type

- Natural and Organic

- Conventional and Synthetic

- By Distribution Channel

- Supermarkets/Hypermarkets

- Health and Beauty Stores

- Online Retail Stores

- Other Channels

- By Geography

- Germany

- United Kingdom

- Italy

- Spain

- France

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping the demand environment for skin care in Europe, and then narrowing it into a usable sizing scope. We rely on public, non-paywalled sources such as Eurostat consumption and trade indicators, European Commission publications on cosmetics rules and compliance, and national statistics offices for household spending signals.

To keep assumptions realistic, we also cross-check with sources such as Cosmetics Europe category snapshots, customs trade series where relevant, and peer-reviewed dermatology and formulation journals for product usage and ingredient trends. Company filings, investor presentations, and reputable business press are then used to understand price positioning and distribution shifts (online versus store-led), as well as new product launches. In a few places, paid subscriptions for company financials and patent databases are used to fill gaps on private players and pipeline activity. The sources listed here are illustrative, and many other public references were also used for clarification and validation throughout the work.

Primary Interviews and Surveys

Primary work is used to pressure-test what desk signals imply, especially for mix, pricing, and channel dynamics that are not visible in public data. Interviews covered distributors, brand and category managers, retail channel leads, and ingredient and formulation specialists across major European markets. Follow-up surveys then confirmed typical price bands, promotion intensity, and category growth pockets.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 15% | |

| Mid tier: 48% | Functional/Unit leaders: 33% | |

| Smaller Players: 20% | Managers: 52% |

Market-Sizing & Forecasting

Sizing begins with a top-down approach where category value is reconstructed from country-level beauty and personal care consumption signals, and then filtered into skin care using share splits that are checked by channel and format. Once that structure is in place, selective bottom-up approximations are used to validate totals, such as sampled brand revenue roll-ups, retailer and distributor checks on volume movement, and an average selling price by format multiplied by estimated units for key countries.

Key inputs that shape the model include skin care category share within personal care, online penetration for skin care, mass versus premium mix, typical price-per-ml shifts by format, and promotional intensity that changes realized pricing. To reduce overstatement in smaller countries, gaps are handled using proxy ratios from comparable markets (similar income levels and retail structure), and then adjusted after interview feedback. Forecasting is completed using scenario analysis supported by short-run trend smoothing, where variables like inflation pressure on discretionary spend, premiumization, and regulatory compliance costs are stress-tested before the final range is set.

Data Validation & Update Cycle

Validation is done through repeated cross-checks, where modeled totals are compared against independent signals such as reported category growth, import patterns for key skin care inputs, and channel share movements. If a country output looks too high or too low versus these signals, the drivers are re-opened and the interview pool is re-contacted to confirm whether pricing, mix, or distribution assumptions have shifted.

Before sign-off, the file goes through multi-step analyst review, including variance checks across countries and a sanity check on implied per-capita spend. Reports are refreshed annually, and interim updates are made when a material event changes pricing, regulation, or retail availability. Right before delivery, we perform a fresh pass so clients receive the most current view that can be supported by traceable inputs.

Mordor Intelligence's Europe Skin Care Products Market Size Versus Other Published Estimates

Published market sizes for Europe skin care can look far apart, even when the topic sounds similar at first glance. The spread usually comes from what products are counted, whether the figure is retail sales or manufacturer revenue, and how price inflation and currency timing are handled.

Some outside estimates widen the scope by rolling skin care into wider personal care baskets, or by mixing in adjacent categories like hair care and toiletries, which can push the total up quickly. In Mordor Intelligence's model, the value is counted only for skin care products sold in Europe, and the country totals are built using consistent category splits, channel checks, and price progression rules that are re-validated during updates.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 34.73 B (2025) | |

| Trade Journal A | USD 33.90 B (2024) | Uses retail-sales reporting in euros for a broader cosmetics and personal care context, and the skin care value can reflect a different channel mix and currency conversion timing versus a country-modeled USD build. |

| Regional Consultancy B | USD 35.79 B (2025) | Applies a faster growth arc and a wider product basket in parts of the definition, which can lift the 2025 level when premiumization and online-led pricing are assumed to rise uniformly across Europe. |

The table shows that most of the difference is explained by category scope choices and how the current year price level is constructed. When the same geography and product set are enforced, and pricing is tied back to channel mix and format-level ASP ranges, the market total becomes easier to reproduce and compare year to year.

Key Questions Answered in the Report

How large is the Europe skin care products market in 2026?

The market is valued at USD 36.17 billion in 2026, with a forecast to reach USD 44.32 billion by 2031.

What is the expected CAGR for European skin care through 2031?

The Europe skin care products market is projected to grow at a 4.15% CAGR during 2026-2031.

Which product category leads sales in Europe?

Facial care products commands 80.05% of 2025 revenue and is set to remain the dominant segment through 2031.

Which European country shows the highest market growth?

Poland posts the fastest growth at a 6.91% CAGR, driven by rising incomes and online adoption.

How important is e-commerce for skin care sales in Europe?

Online retail stores is growing 6.21% annually, with Germany already at a 20% penetration rate.

Page last updated on: