Europe Hair And Skin Care Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

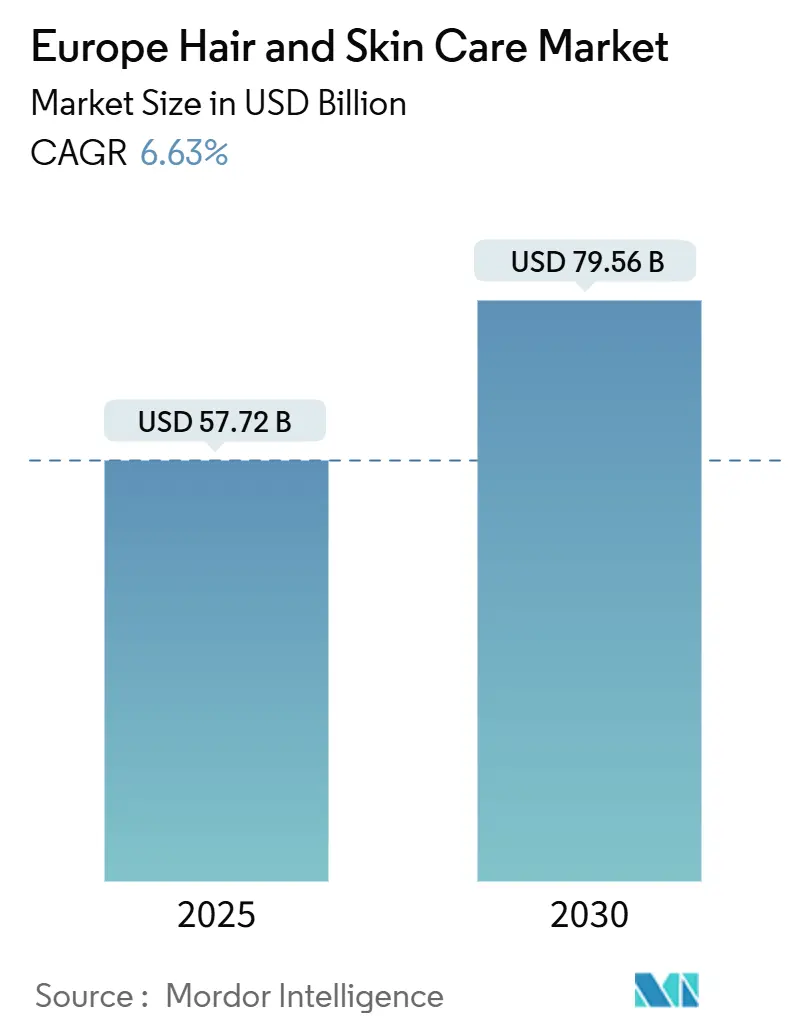

| Market Size (2025) | USD 57.72 Billion |

| Market Size (2030) | USD 79.56 Billion |

| Growth Rate (2025 - 2030) | 6.63% CAGR |

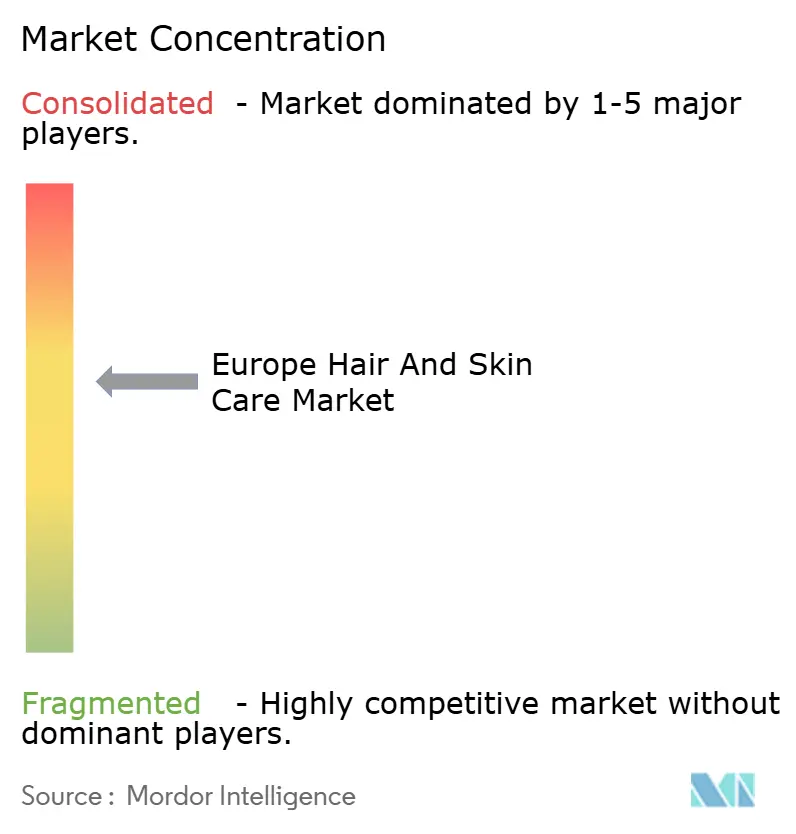

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Hair And Skin Care Market Analysis by Mordor Intelligence

The Europe hair and skin care market is estimated to be USD 57.72 billion in 2025 and is projected to reach USD 79.56 billion by 2030, reflecting a 6.63% CAGR during the forecast period. This growth trajectory is bolstered by demographic ageing in the European Union, a steadfast regulatory focus on ingredient safety, and the swift embrace of beauty-tech solutions. Anti-ageing formulas are now straddling the realms of preventive healthcare and cosmetics, leading consumers to invest in clinically validated products. The rising demand for clean labels is not only reformulating products but also driving investments in biotechnology-derived actives. Furthermore, personalization technologies, ranging from AI-driven consultations to IoT devices, are reshaping purchasing journeys and enhancing consumer loyalty. While some markets remain price-sensitive, brands that meld credible science, transparent sourcing, and omnichannel strategies are seizing significant opportunities across Europe.

Key Report Takeaways

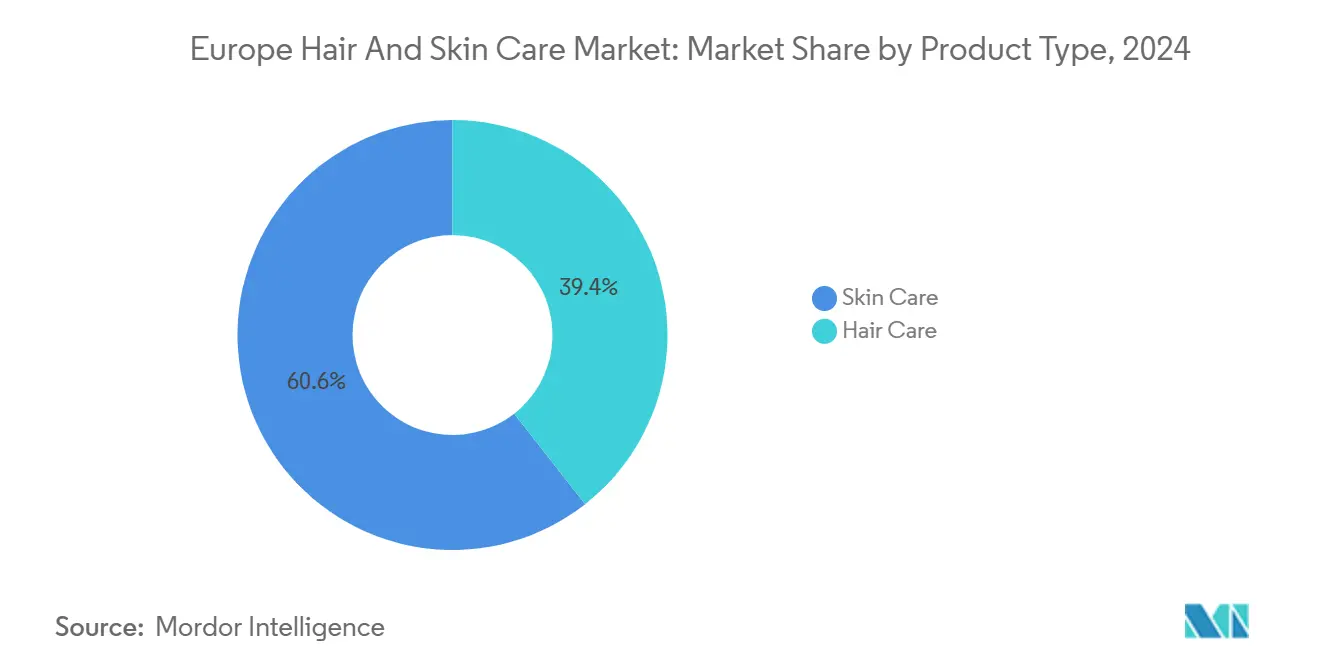

- By product type, skin care held 60.59% of the Europe hair and skin care market share in 2024 and is expanding at a 6.85% CAGR through 2030.

- By category, mass products accounted for 67.45% of the market in 2024, while premium offerings are forecast to grow at a 7.25% CAGR through 2030.

- By ingredients, conventional/synthetic formulations retained 71.65% share in 2024, whereas natural/organic alternatives are growing at a 7.54% CAGR.

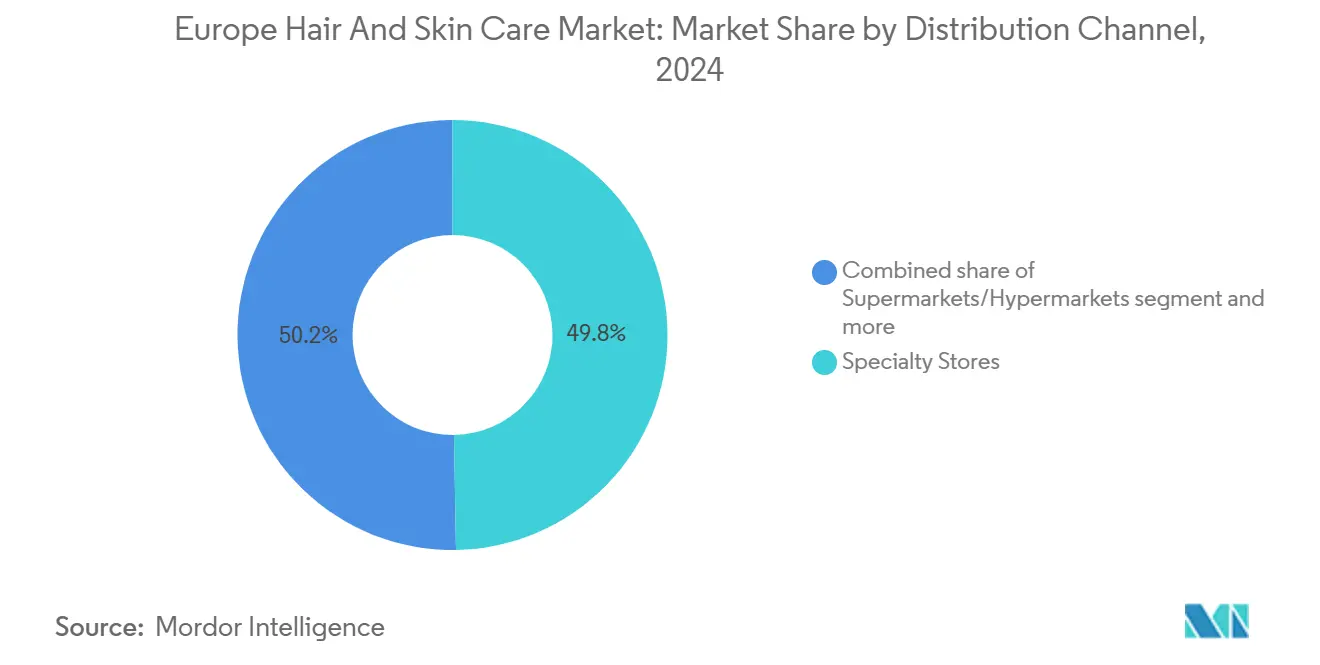

- By distribution channel, specialty stores captured 49.75% share in 2024, whereas online retail stores are growing at a 7.85% CAGR through 2030.

- By geography, Germany led with an 18.65% share in 2024, whereas Italy is forecast to grow at an 8.25% CAGR to 2030.

Europe Hair And Skin Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population fueling anti-ageing skin care | +1.8% | European Union-wide, highest in Italy, Germany | Long term (≥ 4 years) |

| Technological advancements driving the market growth | +1.2% | Germany, France, Nordic countries | Medium term (2-4 years) |

| Rising demand for products formulated with clean label ingredients | +1.0% | Western Europe, spreading to Eastern Europe | Medium term (2-4 years) |

| Growing demand for personalized hair care solutions | +0.8% | Urban centers across European Union | Short term (≤ 2 years) |

| Growing male grooming and skincare segment | +0.6% | United Kingdom, Germany, Scandinavia | Medium term (2-4 years) |

| Influence of social media and beauty influencers | +0.5% | European Union-wide, strongest in younger demographics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ageing population fueling anti-ageing skin care

In 2024, Europe's median age reaches 44.7 years, creating significant opportunities for anti-aging skincare innovations. According to Eurostat, the European population aged 80 and above has grown substantially, reaching 6.1% in 2024 [1]Source: Eurostat, “Population change-Demographic balance,” ec.europa.eu/Eurostat. This demographic not only holds considerable purchasing power but also demands specialized skincare solutions that traditional products often fail to provide. Italy leads this demographic shift with a median age of 48.7 years, followed by Germany and other major European markets. Consumers in these regions increasingly treat skincare as a proactive approach to healthcare rather than a focus on cosmetic enhancement. This evolving perspective drives the demand for scientifically proven formulations that address age-related skin concerns. Brands that demonstrate clinical efficacy are seizing this opportunity to cater to these needs. The aging population's readiness to invest in high-quality skincare products is reshaping industry priorities. Companies are actively developing products with ingredients like retinoids, peptides, and advanced delivery systems, ensuring measurable anti-aging benefits and meeting the expectations of this growing consumer segment.

Technological advancements driving the market growth

In the European hair and skin care market, technological advancements play a crucial role in driving growth. Innovations in product formulations, such as the incorporation of natural and organic ingredients, have gained significant traction among consumers. Additionally, advancements in manufacturing processes and packaging technologies have enhanced product quality and shelf life, further boosting market demand. The integration of digital tools, including artificial intelligence and augmented reality, has also revolutionized the consumer experience by enabling personalized product recommendations and virtual try-ons. Furthermore, the development of smart skincare devices, such as facial cleansing brushes and skin analyzers, has provided consumers with at-home solutions for professional-grade care. The use of biotechnology in creating customized skincare solutions tailored to individual skin types and concerns has also emerged as a significant trend. These technological developments, combined with the growing adoption of e-commerce platforms and digital marketing strategies, continue to shape the market, catering to evolving consumer preferences and fostering sustained growth.

Rising demand for products formulated with clean label ingredients

Consumers increasingly seek products made with clean label ingredients, driving growth in the Europe hair and skin care market. Clean label ingredients refer to natural, minimally processed, and transparent components that align with consumer preferences for health-conscious and environmentally friendly products. This trend is fueled by rising awareness of ingredient safety, sustainability, and the potential adverse effects of synthetic additives. In 2024, more than 210 cosmetic products and 15 licenses obtained the EU Ecolabel certification, according to the European Commission [2]Source: European Commission, "EU Ecolabel grows as nearly 100,000 products certified", environment.ec.europa.eu. This increase demonstrates growing regulatory support for environmentally responsible beauty products. The Europe hair and skin care market exhibits increased adoption of ecolabel-certified products, specifically those incorporating biodegradable formulations and non-toxic active ingredients. The certification enables brands to maintain regulatory compliance while addressing consumer requirements for sustainable and transparent products. Manufacturers in the region are responding by reformulating products to meet these demands, incorporating plant-based, organic, and non-toxic ingredients. This shift not only enhances product appeal but also strengthens brand trust and loyalty among consumers.

Growing male grooming and skincare segment

The growing male grooming and skincare segment is a significant driver of the European hair and skincare market. Increasing awareness among men about personal grooming and skincare routines, coupled with the rising availability of specialized products tailored for male consumers, is fueling this growth. Recently, younger consumers in the region have gravitated towards shaving foams, creams, and gels, valuing their quick application and minimal fuss. Typically packaged in aerosol cans, these products are designed for a seamless shaving experience. For instance, as per Cosmetica Italia in 2023, Italy's men's cosmetics market saw soaps, shaving foams, and gels leading with a consumption value. This shift in consumer preferences highlights the growing demand for convenience-oriented grooming products among men. Furthermore, the influence of social media, celebrity endorsements, and evolving societal norms around male grooming are contributing to the expansion of this segment. The increasing focus of manufacturers on innovative product formulations and packaging to cater to male consumers is also driving market growth. This trend is expected to continue shaping the market dynamics during the forecast period.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit products | -1.2% | European Union-wide, highest impact in online channels | Medium term (2-4 years) |

| Adoption of traditional at-home hair care solutions | -0.8% | Eastern Europe, rural areas | Long term (≥ 4 years) |

| High cost of premium and organic products | -0.6% | Price-sensitive segments across European Union | Short term (≤ 2 years) |

| Consumer skepticism about product efficacy claims | -0.4% | European Union-wide, significant in urban areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit products

Counterfeit products proliferate, posing a significant restraint in the market. The increasing availability of counterfeit hair and skin care products undermines consumer trust and impacts the revenue of genuine brands. These counterfeit items often mimic the packaging and branding of established companies, making it challenging for consumers to differentiate between authentic and fake products. Additionally, counterfeit products may contain harmful ingredients, leading to potential health risks for consumers. This issue not only affects market growth but also compels companies to invest heavily in anti-counterfeiting measures, further increasing operational costs. The prevalence of counterfeit goods remains a critical challenge for the market, necessitating stringent regulatory actions and consumer awareness campaigns to mitigate its impact. The rise of e-commerce platforms has further exacerbated the issue, as counterfeit products are often sold online through unregulated channels. This makes it easier for counterfeiters to reach a broader audience while evading detection. The lack of stringent monitoring mechanisms on some online platforms allows these products to flourish, creating a significant barrier for legitimate brands.

Adoption of traditional at-home hair care solutions

The adoption of traditional at-home hair care solutions acts as a significant restraint in the Europe hair and skin care market. Consumers are increasingly turning to these solutions, which often include natural and DIY remedies, as they seek cost-effective and chemical-free alternatives to commercial products. This shift is driven by growing awareness of the potential side effects of synthetic ingredients and a preference for personalized care routines. Additionally, the availability of online tutorials, social media platforms, and blogs offering step-by-step guidance on creating homemade hair care products has further encouraged this trend. Many consumers perceive these traditional solutions as safer and more sustainable, aligning with the growing demand for eco-friendly and organic options. Furthermore, the rising costs of premium hair care products and the economic uncertainties in the region have pushed consumers to explore more affordable alternatives. This trend poses a challenge for manufacturers and brands in the market, as they face increasing competition from these at-home solutions, which are often perceived as equally effective. Consequently, the demand for conventional hair care products in the market is facing challenges, impacting the overall growth potential of the sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Skin Care Dominates Through Innovation

In 2024, the European beauty market sees the skin care segment at the forefront, commanding a 60.59% share. Projections suggest it will not only maintain this dominance but also lead with the highest growth rate of 6.85% CAGR from 2025 to 2030. This leadership is bolstered by relentless innovations in the segment, particularly in anti-aging and customized solutions tailored to diverse consumer needs. The growing consumer demand for effective and science-backed products has further fueled the segment's expansion. Within the skin care realm, face care emerges as the frontrunner, driven by premium serums and treatments that leverage cutting-edge active ingredients and advanced delivery systems for enhanced efficacy, meeting the rising expectations for visible results.

Body care is on the rise, with formulations extending skincare benefits beyond the face, tackling concerns like hydration, firming, and other body-specific needs. This growth is supported by increasing awareness of holistic skincare routines that address the entire body. Lip care, while a high-margin category, experiences pronounced seasonal fluctuations swayed by weather and shifting consumer preferences, such as heightened demand during colder months. Technological advancements are reshaping the skin care landscape, with L'Oréal's Cell BioPrint technology leading the charge. This innovation emphasizes a shift towards personalized diagnostics, assessing skin's biological age and its response to specific ingredients, paving the way for more targeted and effective solutions that align with individual consumer profiles.

By Category: Premium Segment Accelerates Despite Economic Headwinds

In 2024, mass products dominate the European skin and hair care market, accounting for a significant 67.45% share. These products cater to a broad and diverse consumer base, offering affordability and accessibility. The mass segment's stronghold in the market is driven by high demand for cost-effective solutions that address everyday skin and hair care needs, making it a preferred choice for the majority of consumers. Additionally, the availability of mass products across various distribution channels, including supermarkets, hypermarkets, and online platforms, further strengthens their market presence. The segment benefits from continuous product innovation, such as the introduction of natural and organic ingredients, which appeals to environmentally conscious consumers while maintaining affordability.

Meanwhile, the premium segment is steadily gaining traction, carving out a niche within the market. This segment is projected to grow at a robust CAGR of 7.25% from 2025 to 2030. The growth is fueled by increasing consumer inclination toward high-quality, luxury products that promise superior efficacy and exclusive formulations. Premium products often feature advanced technologies, unique ingredients, and personalized solutions, which resonate with consumers seeking enhanced performance and a premium experience. As disposable incomes rise and consumer preferences shift toward premium offerings, this segment is expected to play a pivotal role in shaping the future of the European skin and hair care market. Furthermore, the growing influence of social media and endorsements by celebrities and influencers are driving awareness and demand for premium products, particularly among younger demographics.

By Distribution Channel: Online Growth Challenges Specialty Store Dominance

In 2024, specialty stores dominate the market, holding a significant 49.75% share. Their success stems from their ability to provide personalized consultations and immersive brand experiences, which resonate strongly with consumers seeking tailored solutions. Specialty stores, such as Sephora, exemplify this trend by offering a curated selection of high-quality products and creating a shopping environment that prioritizes customer engagement. These stores often employ trained professionals who guide customers in selecting products best suited to their needs, enhancing the overall shopping experience. Additionally, the focus on premium and niche products allows specialty stores to attract a loyal customer base, particularly among beauty enthusiasts who value exclusivity and quality.

Meanwhile, online retail is emerging as a rapidly growing channel in the market, with a projected growth rate of 7.85% CAGR from 2025-2030. The rise of e-commerce is driven by its convenience, extensive product offerings, and the integration of advanced digital engagement tools. Online platforms provide consumers with the flexibility to shop anytime and anywhere, making premium beauty products more accessible, even in remote areas beyond major urban centers. Furthermore, the use of virtual try-on tools, personalized recommendations, and targeted marketing campaigns enhances the online shopping experience, attracting a diverse customer base. The ability to compare products, read reviews, and access exclusive online discounts further contributes to the growing popularity of this channel. As digital infrastructure continues to improve across Europe, online retail is expected to play an increasingly pivotal role in the distribution of hair and skincare products.

By Ingredients: Natural/Organic Outpaces Conventional Options

In 2024, conventional/synthetic ingredients dominate the European hair and skincare market, accounting for a significant 71.65% market share. These ingredients are widely preferred due to their consistent performance, stability, and cost-effectiveness, which are critical for mass-market products. Their ability to deliver reliable results at competitive prices ensures their continued dominance among manufacturers targeting a broad consumer base. Furthermore, synthetic formulations have seen continuous advancements, enhancing their efficacy, shelf life, and compatibility with various product types. This has allowed brands to cater to diverse consumer needs while maintaining affordability, making conventional and synthetic ingredients a cornerstone of the market. Despite growing interest in natural alternatives, the scalability and cost advantages of synthetic ingredients remain unmatched, ensuring their strong position in the market.

On the other hand, the natural and organic segment is experiencing rapid growth, with a robust 7.54% CAGR projected from 2025 to 2030. This growth underscores a significant shift in consumer preferences toward sustainable and transparent formulations. According to the Soil Association, organic health and beauty product sales in the United Kingdom totaled GBP 136 million in 2023, comprising skincare, cosmetics, and wellness items [3]Source: Soil Association, "The Organic Beauty and Wellbeing Market", soilassociation.org. Growing consumer awareness of environmental and health risks linked to conventional ingredients drives market expansion. The rising demand for natural and organic formulations has increased sales of products with clean-label ingredients. The hair and skin care segments demonstrate consumer preference for botanical extracts, biodegradable materials, and sustainably sourced active ingredients, reflecting market requirements for safety, transparency, and environmental compliance.

Geography Analysis

In 2024, Germany holds an 18.65% share of the European beauty market, leveraging its position as the continent's largest economy and most populous country. This dominance spans all beauty segments, from mass-market products to premium offerings. The strength of the German market is supported by consumers' high purchasing power, an advanced retail infrastructure, and the success of domestic brands like Beiersdorf, which effectively address both local preferences and global competition. Germany's market leadership is further reinforced by its emphasis on sustainability and innovation, with brands increasingly adopting eco-friendly practices and utilizing advanced technologies to meet evolving consumer expectations.

Italy is experiencing the fastest growth among European beauty markets, with a projected CAGR of 8.25% through 2030. This growth reflects a market transformation driven by rising disposable incomes and evolving beauty standards. International brands are contributing to this expansion by investing in local distribution networks, implementing targeted digital marketing strategies, and customizing product formulations to align with regional preferences and climatic conditions. The growth of Italy's beauty market is influenced by urbanization, increased exposure to global beauty trends through social media, and a generational shift in consumer behavior. Furthermore, the availability of affordable yet high-quality products is encouraging wider adoption, while collaborations with local influencers and retailers are helping brands strengthen their presence in this rapidly expanding market.

France, the United Kingdom, and Spain are key players in the European beauty market, each reflecting distinct consumer preferences and retail dynamics shaped by cultural attitudes toward beauty and personal care. These mature markets are characterized by a discerning consumer base that values product quality and is willing to invest in premium offerings. This is particularly evident in the skincare segment, where product efficacy and brand heritage significantly influence purchasing decisions. Additionally, these markets benefit from a strong presence of luxury beauty brands and a well-established e-commerce infrastructure, enhancing accessibility and consumer engagement.

Competitive Landscape

The Europe skin and hair care market exhibits moderate consolidation among key industry players such as L'Oréal S.A., Unilever plc, Beiersdorf AG, The Procter & Gamble Company, among others. This score highlights a competitive landscape where established multinationals share the stage with nimble, specialized brands. Such a setup allows larger entities to reap the benefits of scale economies, leveraging their extensive resources, distribution networks, and brand recognition to maintain a strong foothold in the market. Meanwhile, smaller, innovation-centric companies capitalize on their agility and niche expertise to introduce unique products and cater to specific consumer demands, carving out defensible positions in the market.

A notable trend shaping the market is the rising vertical integration among industry leaders. These companies are not only securing proprietary ingredient sources to ensure consistent quality and cost efficiency but are also enhancing their manufacturing capabilities to reduce dependency on third-party suppliers. This dual approach aims to fortify their supply chains against disruptions and align with growing consumer demand for sustainable and ethically sourced products, thereby strengthening their sustainability credentials.

For instance, L'Oréal is setting the pace with its technological investments and strategic initiatives. The company has embraced advanced bioprinted skin technology for product testing, which reduces the need for animal testing and accelerates product development cycles. Additionally, L'Oréal is leveraging AI-powered content creation systems to deliver personalized marketing campaigns and improve consumer engagement. These innovations not only enhance operational efficiency but also create significant barriers to entry for potential competitors, solidifying L'Oréal's position as a market leader.

Europe Hair And Skin Care Industry Leaders

-

Beiersdorf AG

-

L'Oréal S.A.

-

Unilever plc

-

The Procter & Gamble Company

-

The Estée Lauder Companies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Grabity, an anti-hair loss K-beauty brand developed by scientists from MIT and KAIST under Professor Haeshin Lee's leadership, entered the European market at FOIRE DE PARIS 2025, France's largest consumer goods exhibition.

- April 2025: KinKind launched its updated "Make me SHINE!" shampoo and conditioner bars. The improved formula included a seaweed complex that repaired damaged hair cuticles, retained moisture, enhanced curl definition, controlled frizz, and increased shine. The bars also contained glycolic acid, which strengthened hydrogen bonds, removed calcium deposits and impurities, and firmed the hair fiber, creating a smooth cuticle surface.

- March 2025: Slick Gorilla's product line expansion included the Daily 2in1 Shampoo & Conditioner, complementing their existing offerings such as the Hairstyling Powder. The combined shampoo and conditioner formula supported scalp and hair health while providing a practical solution for men's daily grooming needs. The product was suitable for both daily and occasional use, adapting to individual hair care routines.

Europe Hair And Skin Care Market Report Scope

| Skin Care | Face Care |

| Body Care | |

| Lip Care | |

| Hair Care | Shampoo |

| Conditioner | |

| Hair Colorants | |

| Hair Styling Products | |

| Other Product Types |

| Mass |

| Premium |

| Conventional/Synthetic |

| Natural/Organic |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Channels |

| Germany |

| United Kingdom |

| Italy |

| Spain |

| France |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Skin Care | Face Care |

| Body Care | ||

| Lip Care | ||

| Hair Care | Shampoo | |

| Conditioner | ||

| Hair Colorants | ||

| Hair Styling Products | ||

| Other Product Types | ||

| By Category | Mass | |

| Premium | ||

| By Ingredients | Conventional/Synthetic | |

| Natural/Organic | ||

| By Distribution Channel | Specialty Stores | |

| Supermarkets/Hypermarkets | ||

| Online Retail Stores | ||

| Other Channels | ||

| By Geography | Germany | |

| United Kingdom | ||

| Italy | ||

| Spain | ||

| France | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe hair and skin care market?

The market stands at USD 57.72 billion in 2025 and is forecast to reach USD 79.56 billion by 2030.

Which segment holds the largest Europe hair and skincare market share?

Skin care leads with 60.59% share in 2024 and is also the fastest-growing segment at a 6.85% CAGR to 2030.

How fast are premium products growing within the Europe hair and skincare market?

Premium offerings are expanding at a 7.25% CAGR, outpacing the mass segment’s stable base.

What role do natural ingredients play in market growth?

Natural and organic formulations are growing 7.54% per year, driven by EU regulation and consumer demand for clean labels.

Why is Germany the largest market in Europe?

High disposable income, advanced retail infrastructure, and strong local brands give Germany an 18.65% share of regional sales.

Page last updated on: