US Organic Skin Care Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 9.09 Billion |

| Market Size (2026) | USD 9.48 Billion |

| Market Size (2031) | USD 11.7 Billion |

| Growth Rate (2026 - 2031) | 4.30% CAGR |

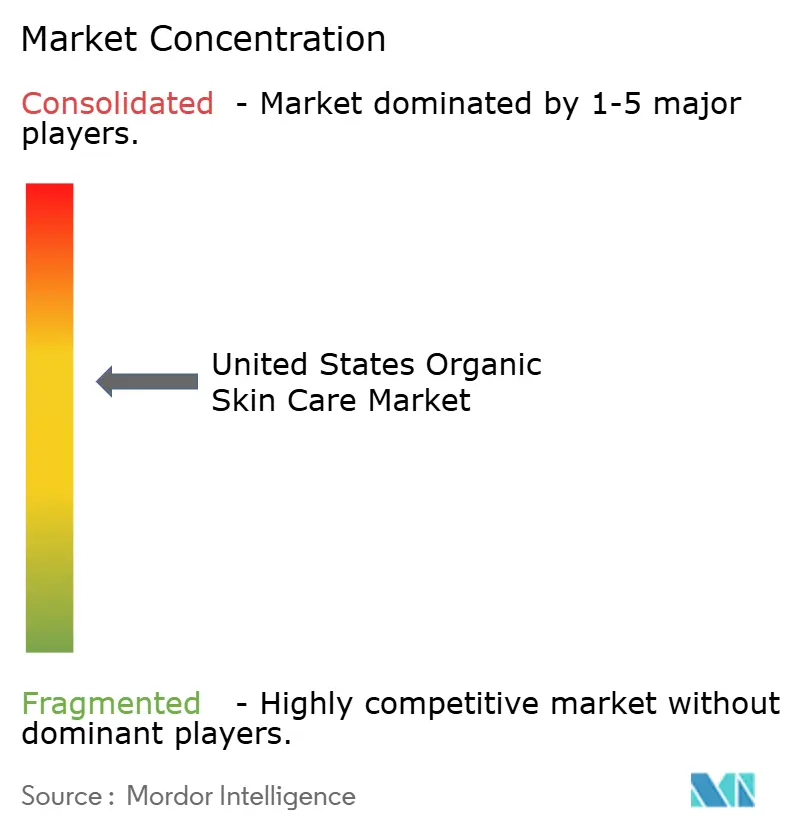

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Organic Skin Care Market Analysis by Mordor Intelligence

The US organic skincare market size was valued at USD 9.09 billion in 2025 and estimated to grow from USD 9.48 billion in 2026 to reach USD 11.7 billion by 2031, at a CAGR of 4.30% during the forecast period (2026-2031). In the U.S. organic skincare market, rising consumer scrutiny over product ingredients and tighter regulatory oversight under MoCRA are driving expansion. Facial care, aligning with premium positioning and a heightened demand for ingredient transparency, stands out as the dominant and fastest-growing category. Digital engagement, bolstered by influencer advocacy, is pivotal in accelerating online adoption, making it the leading distribution route. While tariffs and fragmented chemical regulations present sourcing challenges, they inadvertently bolster the competitive edge of certified organic producers who can validate their purity and safety claims. While mass-market products dominate in volume, premium-tier offerings, buoyed by biotechnology-led innovation and supply chain traceability, are on the rise. Adults are the primary users, but the children's segment, spurred by parental safety concerns, is expanding even more rapidly. As major players grow through acquisitions and direct-to-consumer brands like Youth to the People and Honest Company broaden their reach, they increasingly depend on regulatory adaptability and investments in clean-label infrastructure.

Key Report Takeaways

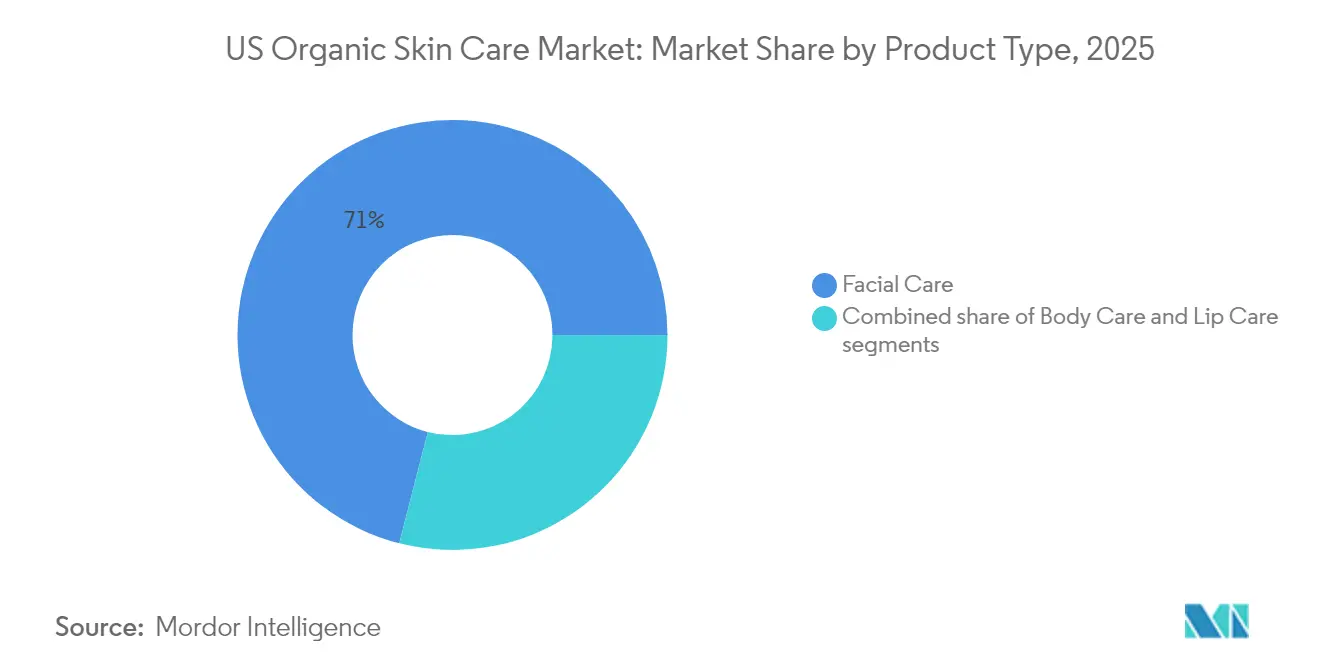

- By product type, the facial care segment commanded 71.02% of the US organic skincare market share in 2025 and is set to grow at a 4.66% CAGR through 2031.

- By category, the mass products segment led with 67.71% revenue share in 2025, whereas the premium products segment is forecast to expand at a 4.84% CAGR between 2026-2031.

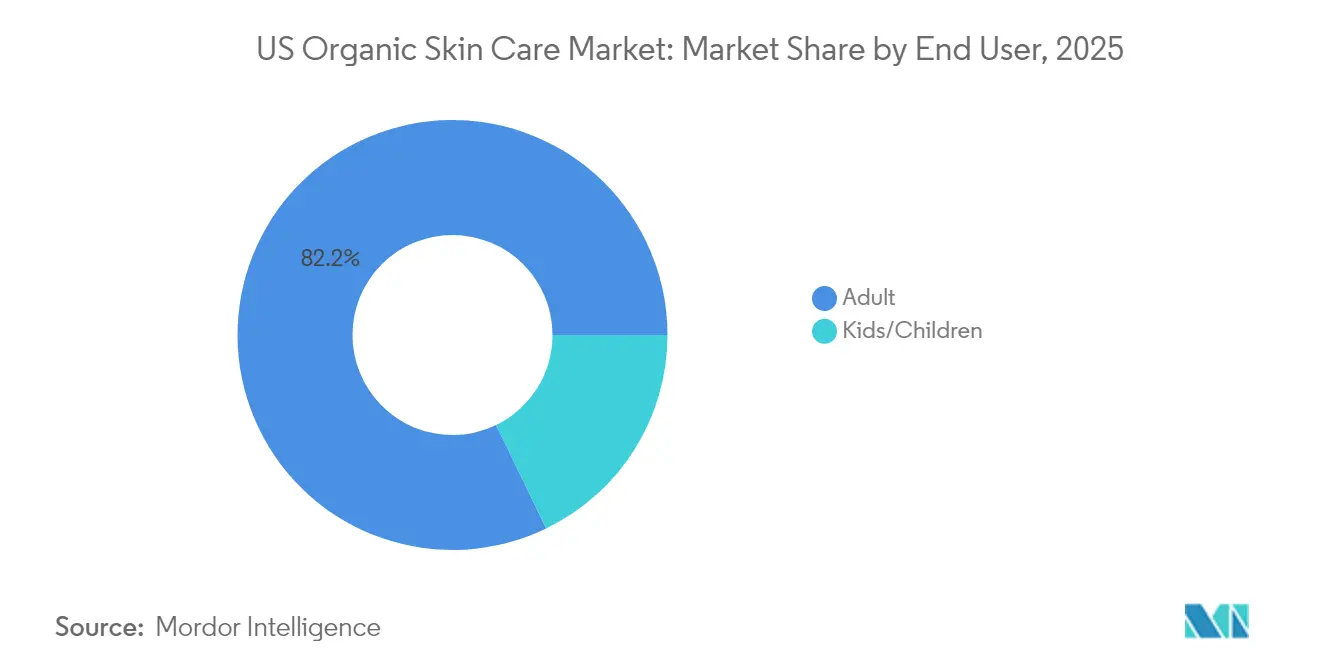

- By end user, the adult segment accounted for 82.18% of the US organic skincare market size in 2025, but the kid/children products segment represents the fastest trajectory, advancing at a 5.09% CAGR to 2031.

- By distribution channel, online retail captured 49.02% share of the US organic skincare market in 2025 and is projected to progress at a 5.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with United states representing one among them. The global report on organic skin care market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

US Organic Skin Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing awareness about environmental sustainability | +0.8% | Global, with strongest impact in coastal United States | Medium term (2-4 years) |

| Influence of social media platforms on purchasing decisions | +1.2% | National, concentrated in urban areas with high Gen Z population | Short term (≤ 2 years) |

| Growing concerns over the effects of synthetic products on the body | +0.9% | National, with premium segments leading adoption | Medium term (2-4 years) |

| Growth of organic skincare in men's and gender-neutral categories | +0.4% | National, with early gains in metropolitan areas | Long term (≥ 4 years) |

| Millennial and Gen Z preference for ethical products | +0.7% | National, strongest in college towns and tech hubs | Short term (≤ 2 years) |

| Awareness of vegan and cruelty-free beauty products | +0.5% | National, with higher penetration in California and Northeast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Awareness About Environmental Sustainability

Environmental consciousness has evolved beyond surface-level marketing to drive fundamental purchasing decisions, with consumers willing to pay more for personal care products with natural ingredients. This shift reflects deeper concerns about climate change and resource depletion, prompting brands to invest heavily in sustainable sourcing and circular economy principles. L'Oréal's commitment to source 95% of its formula ingredients from bio-based sources by 2030 exemplifies this transformation, supported by partnerships with biotechnology firms like Abolis to develop next-generation sustainable ingredients [1] Source: L’Oréal Groupe, “L’Oréal Sets Targets for 95% Bio-Based Ingredients by 2030,” loreal.com. The sustainability imperative is reshaping supply chains, with companies like Unilever investing USD 120 million in joint ventures to create plant-based alternatives to palm oil derivatives. This trend extends beyond ingredients to packaging innovation, where brands are adopting biodegradable materials and refillable containers to address consumer demands for comprehensive environmental responsibility. The regulatory landscape is reinforcing this shift, with Extended Producer Responsibility laws in multiple states requiring companies to manage packaging waste disposal, creating additional incentives for sustainable practices.

Influence of Social Media Platforms on Purchasing Decisions

Social media platforms have transformed how consumers discover and purchase products, with TikTok becoming a significant influence on organic skincare preferences among younger consumers. According to the Organic Trade Association, social media's impact has helped drive a 7% increase in sustainable personal care product sales, reaching USD 1.3 billion [2] Source: Organic Trade Association, “Social Media Boosts Sustainable Personal Care Sales,” ota.com. These platforms facilitate rapid trend dissemination and enable consumers to share authentic product experiences. TikTok's algorithm-based content distribution system allows smaller organic brands to gain widespread visibility without substantial marketing investments, creating more market access opportunities and increasing competition for established companies. Research indicates that social media engagement directly influences purchase decisions for organic cosmetics by enhancing consumer perception of product quality and value. A 2024 University of Portsmouth survey indicated that 60% of consumers trusted influencer recommendations, while nearly half of all purchasing decisions were influenced by these endorsements [3]Source: University of Portsmouth, “New Research Unveils the Dark Side of Social Media Influencers and Their Impact on Marketing and Consumer Behaviour,”port.ac.uk.Consumer preference for genuine, relatable influencer content over traditional brand messaging has prompted companies to revise their marketing approaches. This shift has created a market environment where effective social media presence and influencer partnerships have become essential factors alongside product quality in determining market position.

Growing Concerns Over the Effects of Synthetic Products on the Body

Concerns over harmful chemicals such as parabens, sulfates, and artificial fragrances, which are linked to skin irritation, allergic reactions, and possible long-term health risks, are prompting consumers to seek safer, natural alternatives. This concern is driving demand for transparency in ingredient sourcing and formulation, with consumers actively seeking products free from parabens, sulfates, and artificial fragrances. The trend reflects broader health consciousness where skincare is viewed as an extension of wellness routines rather than purely cosmetic enhancement. Research indicates that consumers are increasingly educated about ingredient safety, with many using apps and online resources to verify product compositions before purchase. According to the NSF survey 2025, 74% of U.S. consumers consider organic ingredients important in personal care products such as skincare, soaps, and shampoos. Additionally, 45% are willing to pay more for certified organic products, rising to 62% among those aged 18–29 [4]Source: NSF, “74 % of U.S. Consumers Consider Organic Ingredients Important in Personal Care Products,”nsf.org. This knowledge empowerment is forcing brands to reformulate existing products and invest in cleaner alternatives, creating opportunities for organic brands positioned as safer options. The regulatory response is evident in state-level chemical bans, with California, Colorado, and Minnesota prohibiting cosmetics containing intentional PFAS, while Washington State's Toxic-Free Cosmetics Act bans lead and other harmful substances. These regulatory changes are accelerating the shift toward organic formulations as brands seek to avoid compliance complexities associated with synthetic ingredients.

Growth of Organic Skincare in Men's and Gender-Neutral Categories

In the U.S., the surge in organic skincare, particularly in men's and gender-neutral categories, is driven by evolving social norms and a growing appetite for inclusive, natural personal care. As grooming expectations shift, an increasing number of men and non-binary individuals are gravitating towards skincare products that prioritize their needs and eschew harsh synthetic ingredients. The men's skincare market is witnessing a rapid expansion, significantly propelled by platforms like TikTok and Instagram, where influencers and dermatologists are championing skincare routines for male audiences. Brands such as Bevel and Ursa Major are capitalizing on this trend, rolling out clean, gender-inclusive skincare lines that cater to a spectrum of skin concerns. This demographic evolution is presenting fresh avenues for organic brands, especially as consumers lean towards health-conscious and sustainable choices. In alignment with this trend, companies are debuting unisex formulations and adopting minimalist packaging, underscoring both inclusivity and organic authenticity. The shifting perceptions of masculinity, now embracing self-care and grooming, further bolster the sustained demand for organic men's skincare. Together, these developments signal a significant cultural shift in the U.S. personal care market, championing inclusivity, wellness, and sustainability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory gaps fuel growth of uncertified organic and natural products | -0.6% | National, with varying state-level enforcement | Long term (≥ 4 years) |

| Strong penetration of synthetic products in the retail shelves | -0.8% | National, concentrated in mass retail channels | Medium term (2-4 years) |

| Competitive pressure from "naturally inspired" but non-organic brands | -0.5% | National, strongest in premium and mass market segments | Short term (≤ 2 years) |

| Scalability issues for certified organic ingredient supply chains | -0.7% | Global supply chains affecting United States market | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Gaps Fuel Growth of Uncertified Organic and Natural Products

The personal care sector operates with less stringent regulations compared to the food industry regarding organic certification, which allows brands to market products as organic or natural without formal certification. This regulatory environment has resulted in a significant increase of uncertified products that specifically target the growing consumer demand for clean beauty alternatives without meeting verified organic standards, leading to potential market distortions and authenticity concerns in the industry. The lack of a legal definition for "natural" in US cosmetics regulations creates substantial market ambiguity and uncertainty. This regulatory gap enables non-organic products to compete using unclear claims, which significantly affects the premium positioning of certified organic brands. Companies frequently use terms like "naturally inspired" or "natural-based" without meeting organic certification requirements, creating intense price competition that impacts authentic organic brands in the marketplace. The United States Department of Agriculture (USDA)'s National Organic Program faces considerable resource constraints for comprehensive market oversight, delegating much of the regulation to organic certifiers and trade associations. This delegation results in inconsistent enforcement across the market segments. The widespread confusion between organic and natural claims reduces consumer willingness to pay premium prices for certified products, as many consumers continue to struggle with differentiating between genuine organic formulations and marketing-based natural claims in the personal care sector.

Strong Penetration of Synthetic Products in the Retail Shelves

Established synthetic skincare products maintain dominant shelf space in mass retail channels through long-standing relationships with major retailers and superior marketing budgets, creating significant barriers for organic brand visibility and consumer trial. The entrenched position of synthetic products is reinforced by their lower production costs and longer shelf life, enabling aggressive pricing strategies that challenge organic alternatives on value perception. Major retailers often prioritize high-turnover synthetic products due to established consumer habits and proven sales performance, limiting shelf space allocation for organic alternatives despite growing consumer interest. The distribution challenge is particularly acute for smaller organic brands lacking the resources to compete for premium shelf positioning or fund extensive marketing campaigns required to educate consumers about organic benefits. Supply chain disruptions and rising costs from tariffs are exacerbating this challenge, with beauty brands facing tough choices between absorbing increased costs or raising prices, potentially making organic products less competitive against synthetic alternatives. The competitive pressure is intensified by synthetic brands' ability to quickly reformulate and launch new products, while organic brands face longer development cycles due to ingredient sourcing constraints and certification requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Facial Care Dominance Drives Innovation

In 2025, facial care products took the lead in the organic skincare market, capturing a dominant 71.02% share. Projections indicate a steady growth at a CAGR of 4.66% through 2031. This dominance underscores a shift in consumer behavior, with face-specific formulations now viewed as daily essentials. The influence of social media is evident, promoting multi-step skincare regimens and boosting the demand for potent organic cleansers, moisturizers, and serums. Brands like Juice Beauty and OSEA are at the forefront, offering clinically backed natural solutions targeting acne, aging, and sensitive skin, in tune with rising consumer expectations. Meanwhile, body care products, including organic lotions and washes, enjoy consistent demand due to their everyday utility. Lip care, though a niche, remains steady, with seasonal lip balms and natural tints riding the wave of clean cosmetic trends.

Personalized skincare is rapidly emerging as the industry's fastest-growing segment, driven by technological advancements and a surge in demand for bespoke, clean formulations. Innovations like L’Oréal’s Cell BioPrint device, which delivers rapid skin diagnostics through proteomic analysis, are reshaping the engagement strategies of organic skincare brands. This evolution is fueling a heightened demand for smart, ingredient-focused formulations that promise visible results. Brands such as Typology and Herbivore Botanicals are pioneering this shift, seamlessly blending organic ingredients with scientific precision to cater to individual skin concerns. With consumers placing a premium on transparency, safety, and customization, this segment is set for explosive growth, mirroring a broader industry trend towards efficacy-driven organic beauty solutions that harmonize wellness with performance.

By Category: Mass Market Leadership Amid Premium Growth

In 2025, mass-market organic skincare products captured a commanding 67.71% market share, underscoring their widespread availability and seamless integration into daily retail outlets. This surge in dominance is largely attributed to mass retailers, such as Walmart, broadening their organic selections. By introducing a variety of certified, affordable brands, these retailers have made organic skincare more accessible, especially to budget-conscious consumers. Heightened awareness regarding ingredient safety has bolstered this segment, with brands like Burt’s Bees and Avalon Organics leading the charge, offering effective yet wallet-friendly formulations. A notable shift in retail dynamics sees mass-premium and mid-range brands eclipsing traditional luxury lines, further propelling this trend. As the appetite for clean and transparent products grows, mass-market organic brands are leveraging expansive retail collaborations. They manage to uphold their organic ethos and competitive pricing, positioning them as pivotal players in the category's growth.

Premium organic skincare is emerging as the fastest-growing segment, boasting a 4.84% CAGR. Digital advancements, a commitment to sustainable sourcing, and a brand focus on transparency drive this growth. U.S. consumers are increasingly gravitating towards high-performance products that resonate with their wellness ideals. In response, premium brands are bolstering their omnichannel approaches. A testament to this trend, Origins unveiled over 70 products on Amazon’s Premium Beauty platform in May 2025, illustrating how digital avenues can enhance visibility while maintaining a luxury allure. Brands such as Herbivore Botanicals and True Botanicals are at the forefront of this expansion, presenting clinically validated organic solutions paired with compelling brand narratives. Certifications in clean beauty and eco-conscious packaging amplify consumer confidence. With a pronounced shift towards online shopping and an emphasis on product integrity, the premium organic segment is poised for rapid acceleration, harmonizing elegance, efficacy, and environmental mindfulness.

By End User: Adult Dominance with Kids/Children's Segment Acceleration

Adult consumers accounted for 82.18% of the organic skincare market in 2025, maintaining dominance due to well-established routines, higher disposable income, and growing demand for premium, health-conscious formulations. Millennials and Gen Z are driving this segment through values-based purchasing, seeking products that align with sustainability, wellness, and ingredient transparency. Social media continues to influence skincare habits, reinforcing trends like anti-aging, hydration, and preventive care. Organic brands targeting adults have responded with clinically backed, natural formulations that deliver visible results without synthetic additives. The integration of skincare into broader wellness lifestyles alongside fitness, diet, and mental health has also supported premium pricing and brand loyalty, making the adult segment the cornerstone of category revenue and innovation.

The kids/children’s organic skincare segment is the fastest-growing, expanding at a 5.09% CAGR through 2031, driven by parents' increasing awareness of ingredient safety and long-term skin health. Modern parenting emphasizes clean, non-toxic personal care, fueling demand for certified organic products suitable for sensitive, developing skin. Regulatory tightening around children’s product safety further boosts consumer preference for vetted, trustworthy brands. This shift has created fertile ground for niche players like Earth Mama Organics and prompted adult-focused companies to diversify into child-friendly lines. From gentle cleansers to fragrance-free moisturizers, the segment is seeing innovation in formulation and packaging that appeals to health-conscious parents. As education and label scrutiny grow, this category represents a high-potential growth avenue for organic skincare brands committed to safety, purity, and performance.

By Distribution Channel: Online Retail Transformation

Online retail channels hold 49.02% market share in 2025 and are projected to grow at 5.38% CAGR through 2031, reflecting shifts in consumer shopping preferences and beauty retail digitalization. The dominance of online channels stems from their convenience, extensive product selection, and transparent ingredient information that helps consumers make informed decisions about organic products. E-commerce enables brands to implement direct-to-consumer approaches, resulting in better profit margins and stronger customer relationships through personalized experiences and subscription offerings. Social commerce integration on platforms like TikTok and Instagram has enhanced online channel growth by creating direct paths from product discovery to purchase, particularly benefiting organic brands that use influencer collaborations and consumer-created content.

While specialty stores and supermarkets/hypermarkets continue to serve important roles through hands-on shopping experiences and professional guidance, their growth rates remain below online channels. The distribution landscape is shifting toward hybrid approaches, with brands maintaining digital presence while forming strategic partnerships with physical retailers that complement their organic values and consumer base. This evolution in distribution channels helps organic brands by lowering market entry costs and facilitating direct consumer education about product benefits and sustainability initiatives. The transformation of retail channels continues to provide organic brands with expanded opportunities to reach and educate consumers while optimizing their distribution strategies for maximum market penetration and growth.

Geography Analysis

Affluent consumers, stringent regulations, and a health-conscious populace fuel the dominance of California, New York, and Massachusetts in the U.S. premium organic skincare market. California’s Toxic-Free Cosmetics Act and Proposition 65 not only shape local brands but also set a nationwide gold standard, compelling companies to embrace safer, non-toxic formulations. Leading the charge in eco-conscious trends, these states witness a surging demand for carbon-neutral logistics, refillable packaging, and locally sourced botanicals. Manufacturers often tap into native ingredients like cedar, lavender, and seaweed, appealing to both eco-tourists and wellness aficionados. For example, OSEA Malibu from California, which crafts ocean-inspired, certified-organic skincare using locally harvested seaweed, underscoring the region's leadership in clean beauty innovation.

Outdoor enthusiasts in the Pacific Northwest and Mountain West, who prioritize skincare and environmental stewardship, are driving rapid growth in these regions. Cities like Seattle, Portland, and Denver are witnessing a notable uptick in sales of certified organic products, signaling a rising consumer interest. Local brands are not just sourcing nearby botanicals but are also creating products that resonate with wellness principles and regional heritage. Wildcraft Skincare in Portland, for instance, champions eco-consciousness by utilizing locally foraged ingredients and sustainable practices. This intensified commitment to sustainability and environmental consciousness is transforming product design, packaging, and brand narratives, facilitating wider acceptance in both direct-to-consumer and retail arenas.

Though the South and Midwest are still emerging in the organic skincare landscape, they hold significant promise as awareness and accessibility expand. National retailers are broadening their organic offerings, and social media is instrumental in educating budget-conscious consumers about ingredient safety and the advantages of clean beauty. Additionally, agricultural tech hubs in states like Missouri and Georgia are delving into localized ingredient sourcing, aiming to cut production and logistics costs and bolster regional competitiveness. Brands like Farmstead Apothecary, which utilize fruit-based, vegan ingredients from U.S. farms, exemplify the growing resonance of clean skincare in these developing regions.

Competitive Landscape

The U.S. organic skincare market is witnessing a blend of established giants and a surge of independent, direct-to-consumer brands. Historically, multinationals like L'Oréal, Unilever, and Clorox have dominated through acquisitions. However, the current landscape boasts a robust presence of companies such as Dr. Bronner’s, Beautycounter, Juice Beauty, The Honest Company, and Youth to the People. These brands, with their niche positioning and innovative approaches, enhance the market's diversity. They prioritize transparent ingredient sourcing, certified organic formulations, and clean-label ethics, fostering trust and loyalty among consumers.

Independent players like Dr. Bronner’s and Weleda utilize vertically integrated operations and established certification frameworks to not only meet MoCRA requirements but also to achieve environmental benchmarks. These benchmarks include standards like cruelty-free, carbon-neutral, and biodegradable. Meanwhile, digital-first brands such as OSEA, Indie Lee, and True Botanicals are revolutionizing distribution. By harnessing the power of social media and e-commerce, they're tapping into high-growth consumer segments and broadening their reach, all without the need for traditional retail channels.

In response to trade instability and escalating tariffs on Asian botanical extracts, companies are diversifying their supply chains. Many are pivoting to Latin American sources or pouring investments into U.S.-based biotechnology fermentation. Brands like Tata Harper, Phyt’s, and Thesis Beauty are making strides by adopting low-carbon, traceable ingredient systems. They often achieve this through collaborations in synthetic biology or direct sourcing. In this dynamic landscape, success hinges on the ability to meld product innovation, sustainable practices, and regulatory adherence with the values of health-conscious consumers.

US Organic Skin Care Industry Leaders

Dr. Bronner’s Magic Soaps, Inc.

The Honest Company, Inc.

Juice Beauty, Inc.

Beautycounter (Counter Brands, LLC)

Weleda Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Rhug Wild Beauty, a luxury COSMOS-certified organic skincare brand from North Wales' Rhug Estate, entered the U.S. market through Amazon. The brand's portfolio includes cleansers, serums, masks, and creams featuring wild-foraged, sustainable botanicals. All products are vegan, cruelty-free, halal, and certified organic.

- May 2025: Natural Grocers, a family-owned natural and organic grocery retailer based in Lakewood, Colorado, has introduced a luxury vegan skincare collection under its private label. The product range comprises body washes, sugar scrubs, butters, and body creams. These products are manufactured in small batches using selected vegan-friendly ingredients, including essential oils and acacia-derived phyto-collagen, while excluding parabens, synthetic fragrances, phthalates, petroleum, gluten, and palm oil.

- January 2025: Real Skin Care has expanded its organic skincare product line to meet the increasing demand for natural beauty solutions from consumers. The company introduced new United States Department of Agriculture-certified organic products focusing on sustainability, purity, and performance. The expanded portfolio addresses consumer preferences for plant-based ingredients and environmentally responsible formulations, aligning with the company's established focus on holistic wellness and skin health.

- October 2024: KORA Organics, a certified-organic skincare line, debuted on QVC (U.S.), marking the first time a certified organic line was featured live on the network. The launch featured products including Noni Glow Face Oil, Turmeric Moisturizer, Kakadu Plum Vitamin C Serum, Berry Bright Eye Cream, and exclusive skincare bundles. All products contain United States Department of Agriculture (USDA) and Cosmetic Organic and Natural Standard (COSMOS)-certified organic ingredients.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States organic skin care market as finished facial, body, and lip care formulations that carry certified-organic claims under USDA or equivalent standards and reach consumers through retail, professional, or direct-to-consumer channels.

(Scope Exclusions) The estimate omits spa service revenue, cosmeceuticals positioned for therapeutic outcomes, and DIY raw ingredients.

Segmentation Overview

- By Product Type

- Skin Care

- Facial Care

- Cleansers

- Moisturizers and Oils/Serums

- Other Facial Care Product

- Body Care

- Body Lotions

- Body Wash

- Other Body Care Products

- Lip Care

- Facial Care

- Skin Care

- By Category

- Premium Products

- Mass Products

- By End User

- Adult

- Kids/Children

- By Distribution Channel

- Supermarkets/Hypermarket

- Specialty Stores

- Online Retail Stores

- Others Distribution Channel

Detailed Research Methodology and Data Validation

Primary Research

We complemented desk work with interviews and surveys covering brand founders, contract formulators, dermatologists, ingredient suppliers, and specialty retailers in California, Texas, New York, and Illinois, gaining firsthand checks on average selling prices, certification costs, and channel velocity.

Desk Research

Mordor Intelligence analysts began with public sources such as USDA National Organic Program certificate lists, FDA Voluntary Cosmetic Registration data, BEA consumer-spend tables, and US ITC trade codes to size domestic availability and imports. Industry voices like the Organic Trade Association, Personal Care Products Council, and dermatology journals clarified adoption triggers, while American Academy of Dermatology prevalence studies quantified sensitive-skin cohorts. Select paid libraries, D&B Hoovers for company splits and Questel for patent flow on plant-based actives, supplied competitive and innovation clues. This roster is illustrative; many further references informed data collection and validation.

Market-Sizing & Forecasting

A top-down build starts from total US skin-care expenditure, applies verified organic penetration from retail audits, and adjusts for export-import balances to fix 2024 volume, which our team prices with weighted average shelf ASPs. Supplier roll-ups and e-commerce channel checks offer bottom-up reasonableness. Key variables tracked include USDA certificate counts, MoCRA enforcement milestones, online share of beauty sales, premium price uplifts, and female-millennial purchase propensity. Five-year forecasts blend multivariate regression with ARIMA and scenario analysis to reflect ingredient cost swings and policy shifts flagged during field work.

Data Validation & Update Cycle

Outputs pass peer review, variance checks against dermatologist-visit statistics, and reconciliation with shipment records before sign-off. Reports refresh annually, and analysts trigger interim revisions after material recalls, regulatory changes, or sizeable M&A.

Why Our US Organic Skin Care Baseline Stands Out for Decision-Makers

Published estimates often diverge because firms interpret "organic" differently, fold broader product baskets into totals, or refresh figures on uneven schedules.

Key gap drivers include inclusion of hair and oral care in some counts, reliance on single-channel retail scans, and omission of MoCRA-related compliance costs that our model captures.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.09 B (2025) | Mordor Intelligence | |

| USD 6.88 B (2025) | Global Consultancy A | Bundles all organic personal care items, diluting skin-only focus |

| USD 2.56 B (2024) | Trade Dataset B | Tracks natural-label retail SKUs only; omits online and certification premium |

| USD 1.80 B (2023) | Industry Forecast C | Relies on factory shipment values; overlooks direct-to-consumer and prestige channels |

Mordor Intelligence pegs the market at USD 9.09 billion for 2025. Other public references range from USD 6.88 billion to USD 1.80 billion, largely due to the scope and data limitations noted above. These comparisons show that our disciplined scope, variable mix, and recurring validation deliver a balanced, transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the US organic skincare market?

The market is valued at USD 9.48 billion in 2026 and is forecast to reach USD 11.7 billion by 2031.

Which product segment leads US organic skincare sales?

Facial care products hold 71.02% share and should grow at a 4.66% CAGR through 2031.

How fast is online retail growing in organic skincare

Online channels are advancing at a 5.38% CAGR, the fastest among all distribution options.

What regulations most influence organic skincare in the US?

MoCRA’s facility registration rules and state-level bans on PFAS and lead drive formulation and compliance decisions.

Page last updated on: