Mobile Banking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

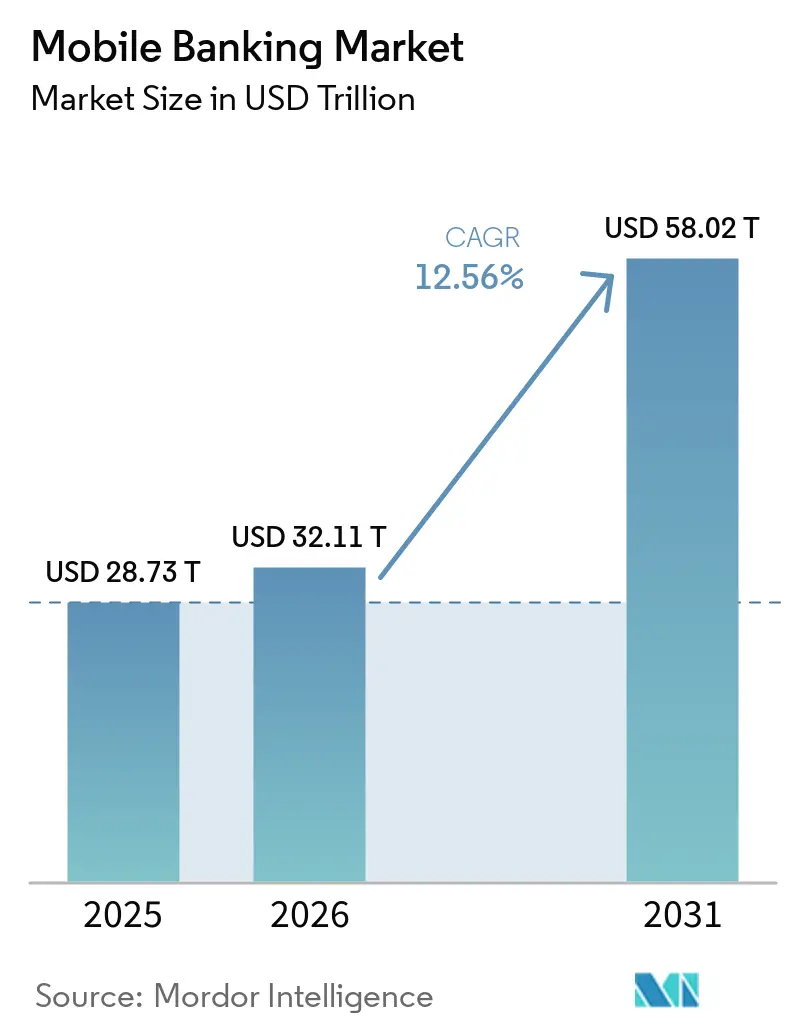

| Market Size (2026) | USD 32.11 Trillion |

| Market Size (2031) | USD 58.02 Trillion |

| Growth Rate (2026 - 2031) | 12.56% CAGR |

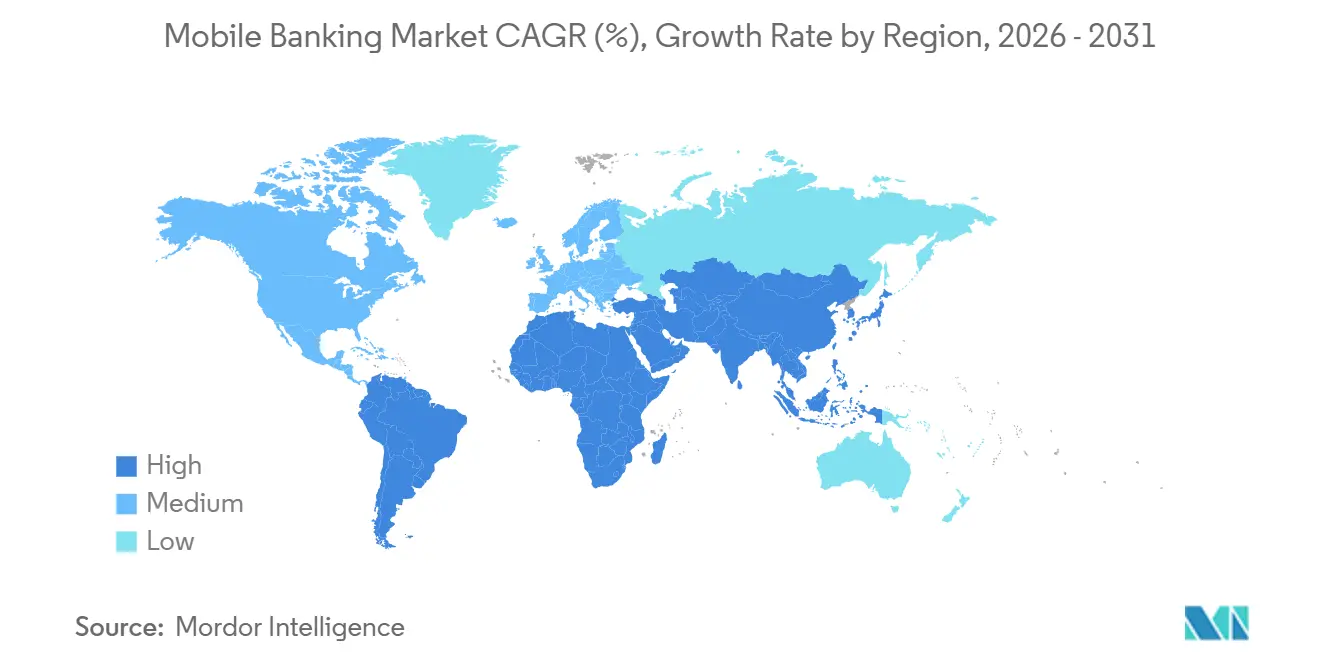

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Banking Market Analysis by Mordor Intelligence

The Mobile Banking Market size was valued at USD 28.73 trillion in 2025 and is estimated to grow from USD 32.11 trillion in 2026 to reach USD 58.02 trillion by 2031, at a CAGR of 12.56% during the forecast period (2026-2031).

The expansion reflects a durable shift in customer behavior, as routine banking activity is moving into apps and staying there for payments, account access, service requests, and product discovery. Bank of America reported 30 billion client interactions in 2025, including 16.6 billion digital logins, which shows how large banks now handle a major share of customer engagement through digital channels. Growth is also supported by financial inclusion, as the World Bank reported that mobile-phone technology is helping adults in developing economies save more through formal accounts than before. Security, authentication quality, and app reliability are now central to adoption, as a larger share of financial activity occurs on mobile devices each year. Competition in the mobile banking market is therefore moving beyond simple account access and toward stronger engagement, wider product coverage, and better transaction execution across both retail and business use cases.

Key Report Takeaways

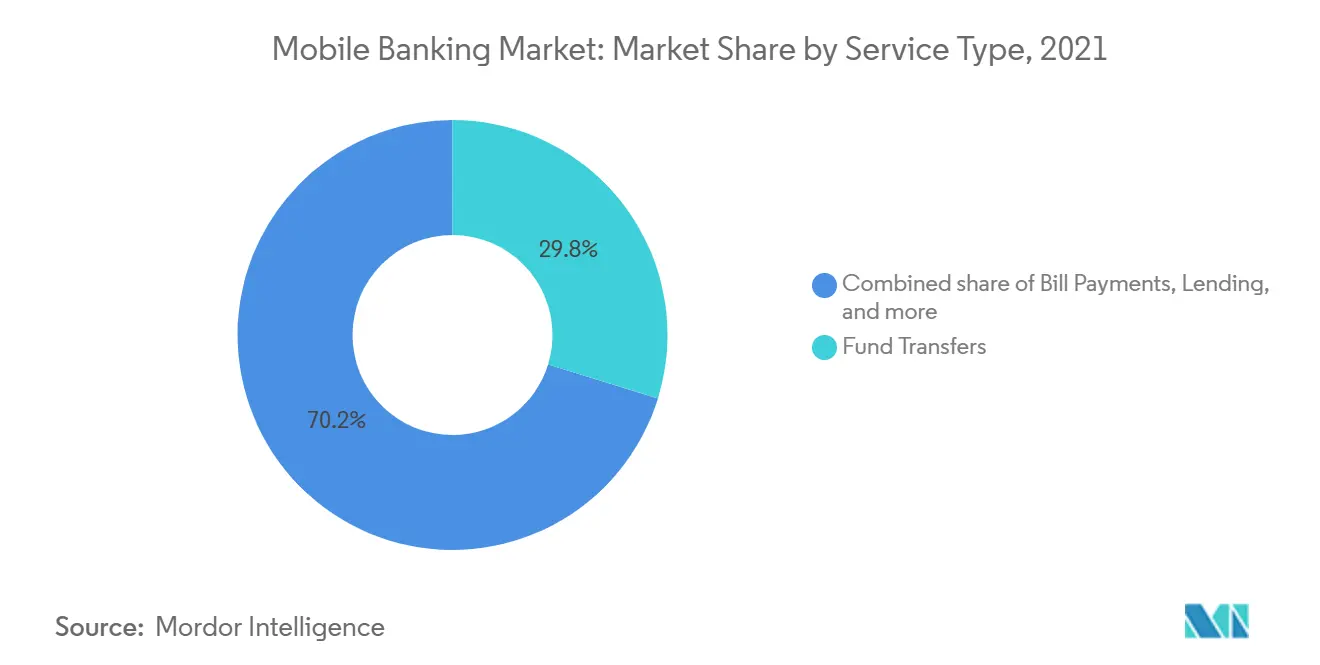

- By service type, fund transfers held 29.8% of the mobile banking market share in 2025, while investments and wealth management are projected to grow at 16.2% CAGR through 2031.

- By transaction type, consumer-to-business accounted for 54.1% of the mobile banking market share in 2025, while business-to-business is projected to grow at a 15.3% CAGR through 2031.

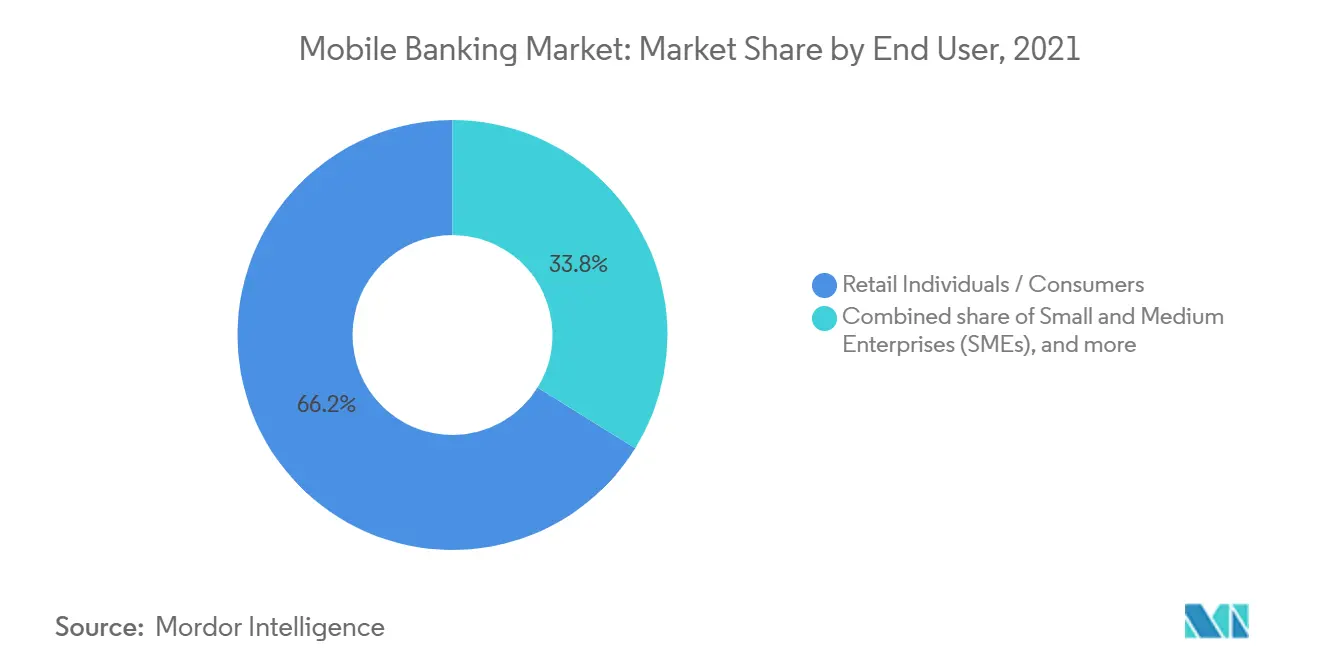

- By end user, retail individuals and consumers accounted for 66.2% of the mobile banking market share in 2025, while small and medium enterprises are projected to grow at 14.9% CAGR through 2031.

- By geography, Asia-Pacific held 46.6% of the mobile banking market share in 2025, while the Middle East and Africa are projected to grow at 15.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mobile Banking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile-First Primary Banking Becomes The Default Channel | +2.4% | Global, with highest depth in North America, EU, and East Asia | Medium term (2-4 years) |

| Rising Demand For Real-Time P2P And Bill Payment Journeys | +2.0% | Global, with peak intensity in South Asia, Southeast Asia, and Sub-Saharan Africa | Short term (≤ 2 years) |

| Biometric And Passkey Authentication Reduces Friction | +1.5% | Global, with regulatory acceleration in UAE, India, EU, and Philippines | Short term (≤ 2 years) |

| Embedded Finance Expands In-App Banking Frequency | +1.8% | Asia-Pacific core, spill-over to Latin America and MEA | Medium term (2-4 years) |

| AI-Personalized Financial Guidance Improves Retention | +1.2% | North America and the EU, early gains in Asia-Pacific urban centers | Medium term (2-4 years) |

| Rural And Underserved Access Via Lightweight And USSD-Enabled Experiences | +1.0% | Sub-Saharan Africa, South Asia, Southeast Asia rural markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mobile-First Primary Banking Becomes the Default Channel

Mobile is now the primary access point for routine banking activity across many large institutions. Bank of America reported 59 million verified digital users in 2025, along with 16.6 billion digital logins and digital engagement across 81% of its consumer and small business households[1]BANKOFAMERICA.COM BofA AI and Digital Innovations Fuel 30 Billion Client Interactions | Press Releases | Newsroom | Bank of America. JPMorgan Chase said its mobile platform serves nearly 63 million active users, and its 2026 app redesign focused on faster access to Zelle, the digital wallet, and savings prompts for younger customers. This level of usage changes the app's role, making it the primary surface for customer service, payments, and product discovery. As a result, banks that make the mobile journey simpler and more reliable can deepen engagement and retain a greater share of the customer relationship in the mobile banking market.

Rising Demand for Real-Time P2P and Bill Payment Journeys

Real-time settlement has become a basic customer expectation in the mobile banking market. Bank of America said Zelle users completed 1.8 billion transactions worth USD 556 billion in 2025, while small business Zelle payments reached USD 126 billion and grew 23% year over year. GSMA also reported that mobile money transactions reached USD 2 trillion in 2025 and that active 30-day accounts rose 15% to 593 million, indicating that mobile-led transaction habits are widening across emerging markets[2]GSMA.COM Mobile Money accounted for $2 trillion in transactions in 2025, doubling since 2021 as active accounts continue to grow - Newsroom. Frequent payment activity keeps users returning to the same app, thereby increasing the value of the mobile channel for banks and financial platforms. Once that payment behavior is established, customers are more likely to adopt adjacent features, such as savings, borrowing, and investment tools, within the same mobile banking environment.

Biometric and Passkey Authentication Reduces Friction

Authentication quality is becoming a direct growth lever in the mobile banking market because it affects both trust and transaction completion. FIDO Alliance reported that 5 billion passkeys were in use worldwide by May 2026, 75% of global consumers had enabled a passkey on at least one account, and 49% used them regularly[3]FIDOALLIANCE.ORG Five Billion Passkeys: FIDO Alliance Reports Mainstream Global Usage on World Passkey Day 2026 | FIDO Alliance. FIDO Alliance also documented that Banesco Banco Universal deployed passkeys to 2.2 million users for high-value transactions and fast P2P payments. Organizations that adopted passkeys reported 32% fewer phishing-related incidents and a 35% drop in password reset requests, indicating lower friction and lower service costs. In practical terms, better authentication lets mobile banking platforms reduce login drop-off, cut recovery effort, and support higher-value activities with less customer hesitation.

Embedded Finance Expands In-App Banking Frequency

Embedded finance is expanding how often users return to a banking app and how many needs they can handle within a single interface. Freedom Holding said its SuperApp model, which bundles banking, insurance, and lifestyle services, contributed to a 46% increase in deposits and a 29% increase in loans in its banking segment in 2025. That result shows why platforms are expanding beyond transfers and balances into lending, protection, and investment features that naturally fit within the same session. The user relationship becomes more valuable when the app supports multiple financial tasks rather than just a single recurring transaction. This is helping the mobile banking market shift from a utility model toward a broader platform model where product depth and engagement frequency rise together.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Fraud Losses From Social Engineering And Account Takeover | -1.8% | Global; Asia-Pacific login attack rate grew 21% YoY in 2025, against a global decline | Short term (≤ 2 years) |

| Legacy Core Integration Slows Feature Rollout | -1.5% | North America, Europe, South Asia—markets with large incumbent bank bases | Medium term (2-4 years) |

| Fragmented Data-Residency And App Store Compliance Burdens | -1.0% | Asia-Pacific and MEA, particularly multi-jurisdiction digital bank operators | Medium term (2-4 years) |

| Low-Trust User Segments Limit Migration To Full App Banking | -0.7% | Sub-Saharan Africa, South Asia, and rural Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Fraud Losses from Social Engineering and Account Takeover

Fraud remains a meaningful drag on confidence in the mobile banking market because the phone has become a central financial device for millions of users. The FBI reported more than 5,100 account takeover fraud complaints since January 2025, with losses exceeding USD 262 million, and it identified impersonation of financial institution support staff through calls, texts, and emails as the primary method[4]FBI.GOV Account Takeover Fraud via Impersonation of Financial Institution Support — FBI. This makes the risk difficult to solve through interface design alone because customers can still be manipulated outside the app. Banks, therefore, have to invest in stronger authentication, clearer alerts, and tighter transaction monitoring while still keeping the experience usable. If trust weakens, some users delay higher-value transactions or limit their activity, slowing the pace of expansion in the mobile banking market.

Legacy Core Integration Slows Feature Rollout

Legacy core architecture continues to limit how quickly many incumbents can improve their mobile offers. Older batch-based systems were not built for real-time event handling, which can leave mobile channels working with stale data states and narrow integration options. Large banks also have many third-party links and legacy processes, so even small product changes can require extensive remediation across several systems. During transition periods, institutions often have to run legacy and modern environments in parallel, which raises operating costs and reduces room for discretionary digital spending. This slows feature rollout in the mobile banking market, giving faster-moving cloud-native competitors an opening in areas such as embedded finance, API-based services, and business banking workflows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Wealth Management Disrupting the Fund Transfer Incumbent

Fund Transfers held 29.8% of the mobile banking market share in 2025, keeping this category in the lead, as payment movement remains the most frequent banking task in a mobile session. Bill Payments and Lending followed as large use cases because users increasingly expect one-touch access to recurring obligations and fast credit decisions inside the same app. Investments and Wealth Management is the fastest-growing sub-segment, projected to expand at a 16.2% CAGR between 2026 and 2031. This shift shows that the mobile banking market is no longer defined solely by transaction utility, as banks are increasingly bringing more complex financial decisions into the mobile environment. Insurance and deposit-related services also remain part of the service mix as institutions build more complete financial journeys within a single application.

Investments and Wealth Management is gaining momentum as mobile users become more comfortable making higher-value financial decisions without leaving the banking app. TD Bank launched a fully redesigned mobile-first TD Easy Trade app in Q1 2026, which shows how established institutions are now treating investing as a core mobile experience rather than a separate digital add-on. That product direction matters because investment activity can deepen customer retention and raise the value of the relationship beyond payments alone. It also reflects a wider change in the mobile banking industry, where banks and digital players are expanding into advisory, self-directed trading, and broader personal finance management. Over time, this changes the service mix by making wealth activity a more regular part of mobile banking behavior instead of a niche extension.

By Transaction Type: B2B Channels Rewiring Corporate Treasury on Mobile

Consumer-to-Business accounted for 54.1% of the mobile banking market in 2025, supported by the high volume of retail commerce, utility payments, and government-related payments that now run through mobile channels. Consumer-to-Consumer activity also remains important because person-to-person transfers create repeat usage and keep customers anchored to a specific banking app. Business-to-Business is the fastest-growing transaction type and is set to drive the fastest expansion in the mobile banking market, with a 15.3% CAGR between 2026 and 2031. This pattern shows that the mobile banking market is extending from consumer convenience into business-critical treasury activity. As firms become more comfortable approving payments and managing cash flows on smartphones, the role of mobile changes from an access channel to an execution channel.

The business side of the mobile banking industry is being reshaped by tools that once sat only in desktop treasury systems. Bank of America said its CashPro platform processed a record USD 1.2 trillion in mobile payment approvals in 2025, while mobile sign-ins rose 20% across a network serving corporates in 145 jurisdictions. Maybank also launched its next-generation Maybank2E enterprise banking platform in June 2026 after processing MYR 3 trillion, (USD 680 billion) across 122 million transactions in Malaysia in 2025 These moves show that corporate approval flows, cash visibility, and multi-user controls are now being rebuilt around mobile use rather than added later as a secondary layer. That gives B2B mobile banking a stronger long-term role in transaction mix growth.

By End User: SME Adoption Challenging the Retail-Only Value Model

Retail Individuals and Consumers held 66.2% of the mobile banking market in 2025, which confirms that the broadest user base still comes from everyday personal banking activity. The World Bank reported a 5-percentage-point increase in 2021 in the share of adults across developing economies who used mobile-money accounts to save, indicating that retail adoption is still widening in lower- and middle-income countries. Small and Medium Enterprises are the fastest-growing end-user group, and this segment of the mobile banking market is projected to expand at a 14.9% CAGR between 2026 and 2031. Large corporates remain important users, but the stronger growth rate in SMEs points to a change in where new digital value is being created. The mobile banking market is therefore broadening from a retail-heavy model toward a more balanced structure where business users matter more.

SME demand is rising because smaller firms now expect mobile access to functions that once required branch support or desktop banking. Chime said its Workday partnership reached First Student in Q1 2026, showing how mobile-first financial platforms are connecting more directly to employer and payroll ecosystems. That matters because business users tend to return to the app for time-sensitive actions such as payroll checks, payment approvals, and working capital decisions. It also changes competitive behavior in the mobile banking industry, as banks that can combine business controls with simple mobile design become more attractive to smaller firms. As this functionality improves, SME adoption is likely to keep narrowing the gap between consumer and business engagement in the mobile banking market.

Geography Analysis

Asia-Pacific held 46.6% of the mobile banking market share in 2025, which made it the largest regional base by a wide margin. The region combines very large user populations with strong mobile-led payment behavior and a fast transition toward app-based account use. The World Bank reported that mobile-phone technology is supporting greater formal savings in developing economies, which helps explain why large parts of Asia continue to add depth and scale to mobile financial activity. This keeps Asia-Pacific at the center of the mobile banking market, as the region encompasses both mature digital behavior and large pools of newly engaged users. The result is a geography where daily transaction use, broader product adoption, and financial inclusion are advancing simultaneously.

North America and Europe remain the most mature parts of the mobile banking market, as many customers already rely on apps as their primary banking interface. Bank of America reported 59 million verified digital users in 2025, while JPMorgan Chase said its mobile platform serves nearly 63 million active users, which shows the scale now present among major United States institutions. Chime reached 10.2 million active members in Q1 2026 and raised its full-year revenue guidance, indicating that digital-first challengers still have room to expand in a mature market. In Europe, ING reported a mobile primary customer base of 15.4 million in FY2025, which confirms that mobile-led growth remains relevant even in established banking systems. Together, these conditions keep North America and Europe important to the mobile banking market as centers of app refinement, product depth, and competitive intensity.

The Middle East and Africa is the fastest-growing regional segment in the mobile banking market and is forecast to expand at 15.0% CAGR between 2026 and 2031. GSMA reported that mobile money transactions reached USD 2 trillion in 2025 and active 30-day accounts rose to 593 million, with much of the momentum coming from Sub-Saharan Africa. This region benefits from strong demand for mobile-first access because branch infrastructure is uneven and handset-based finance solves a real access gap. Growth is also supported by the fact that mobile channels can handle low-value, high-frequency activity at large scale, which fits many customer needs in the region. That makes the Middle East and Africa a key expansion zone for the mobile banking market over the forecast period.

Competitive Landscape

The mobile banking market shows moderate concentration because a group of very large banks has substantial customer reach, but competitive pressure remains active across regions and user segments. Bank of America reported 59 million verified digital users in 2025, and JPMorgan Chase said its mobile platform serves nearly 63 million active users, which illustrates the scale advantage held by major incumbents. These institutions benefit from broad customer bases, established trust, and large transaction data pools that can support personalization and service expansion. At the same time, digital-first challengers continue to compete by focusing on speed, targeted user groups, and simpler app journeys. This keeps the mobile banking market competitive even though scale remains an important advantage.

Strategic execution is increasingly centered on product depth and engagement quality rather than on basic mobile access alone. JPMorgan Chase launched a redesigned app in May 2026, co-created with users aged 18 to 24 and built around streamlined payments, wallet access, and savings prompts. Bank of America expanded business-side mobile functionality, with CashPro processing USD 1.2 trillion in mobile payment approvals in 2025, which shows how incumbents are turning mobile into a serious enterprise workflow tool. Chime launched its Chime Prime premium membership tier as it reported its first quarter of GAAP profitability in Q1 2026, which signals a push toward broader monetization and deeper customer engagement. These moves show that leadership in the mobile banking market depends on retaining users through relevance, convenience, and broader in-app value.

The next competitive layer is forming around security, business use cases, and cross-product integration. FIDO Alliance data on passkey adoption and phishing reduction shows why authentication has moved from a technical feature to a strategic differentiator for banks serving higher-value mobile activity. Maybank’s rollout of Maybank2E and TD Bank’s redesign of TD Easy Trade also show how banks are widening the mobile proposition into enterprise banking and investing rather than treating those functions as stand-alone channels. Institutions that can combine secure access, routine transactions, advisory tools, and business controls in one app are likely to hold stronger customer relationships over time. That is why competition in the mobile banking market is moving toward integrated app ecosystems rather than single-feature digital offerings.

Mobile Banking Industry Leaders

JPMorgan Chase and Co.

Bank of America Corporation

Wells Fargo and Company

Citigroup Inc.

HSBC Holdings plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Maybank launched the next-generation Maybank2E enterprise banking platform, an integrated regional business mobile banking solution processing approximately MYR 3 trillion (approximately USD 680 billion) across 122 million transactions in Malaysia in 2025, with planned expansion to Singapore and Indonesia in 2026, directly targeting the fast-growing B2B mobile banking segment

- May 2026: JPMorgan Chase launched a redesigned mobile app co-created with users aged 18-24, featuring streamlined Zelle access, a reimagined digital wallet, and automatic savings prompts, reinforcing a Gen Z-focused mobile-first acquisition strategy across its nearly 63 million active mobile users.

- May 2026: Chime reported its first quarter of GAAP profitability in Q1 2026, reaching 10.2 million active members and raising full-year 2026 revenue guidance to USD 2.66-2.69 billion (22-23% year-on-year growth), with the launch of its Chime Prime premium membership tier.

- March 2026: Bank of America reported that its CashPro corporate mobile platform processed a record USD 1.2 trillion in payment approvals in 2025, approximately USD 38,000 per second, up 15% year-on-year, with mobile sign-ins growing 20%, affirming mobile's centrality in large-enterprise treasury.

Global Mobile Banking Market Report Scope

| Fund Transfers |

| Bill Payments |

| Lending |

| Deposits and Withdrawals |

| Investments and Wealth Management |

| Insurance |

| Others |

| Consumer-to-Consumer |

| Consumer-to-Business |

| Business-to-Business |

| Retail Individuals / Consumers |

| Small and Medium Enterprises (SMEs) |

| Large Corporates and Businesses |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Service Type | Fund Transfers | |

| Bill Payments | ||

| Lending | ||

| Deposits and Withdrawals | ||

| Investments and Wealth Management | ||

| Insurance | ||

| Others | ||

| By Transaction Type | Consumer-to-Consumer | |

| Consumer-to-Business | ||

| Business-to-Business | ||

| By End User | Retail Individuals / Consumers | |

| Small and Medium Enterprises (SMEs) | ||

| Large Corporates and Businesses | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 value outlook for mobile banking?

The sector is forecast to reach USD 58.0 trillion by 2031, up from USD 32.1 trillion in 2026, which reflects sustained app-led expansion across retail and business banking.

How fast is mobile banking expected to grow through 2031?

The forecast calls for a 12.6% CAGR between 2026 and 2031, supported by rising digital engagement, broader product use, and stronger financial inclusion.

Which region leads global mobile banking activity?

Asia-Pacific led with 46.6% share in 2025, making it the largest regional base for app-led banking activity and mobile financial engagement.

Which region is growing the fastest in mobile-led banking services?

The Middle East and Africa is expected to expand at a 15.0% CAGR through 2031, helped by strong mobile money adoption and limited branch dependence in many markets.

Which service area is growing fastest on banking apps?

Investments and Wealth Management is the fastest-growing service type, with a 16.2% CAGR projected between 2026 and 2031 as users shift more complex financial activity into mobile channels.

Why are SMEs becoming more important to banking apps?

SMEs are the fastest-growing end-user group at 14.9% CAGR because mobile tools now support payment approvals, payroll-linked activity, and day-to-day business cash management in one interface.

Page last updated on: