Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

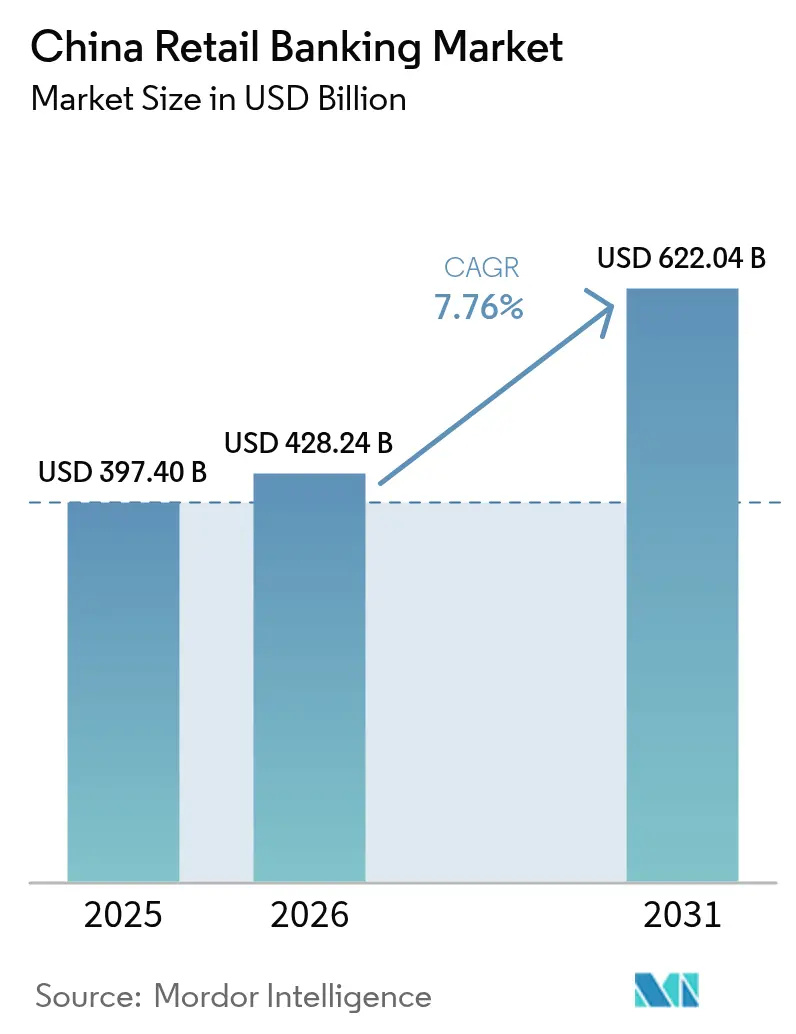

| Base Year Market Size (2025) | USD 397.4 Billion |

| Market Size (2026) | USD 428.24 Billion |

| Market Size (2031) | USD 622.04 Billion |

| Growth Rate (2026 - 2031) | 7.76% CAGR |

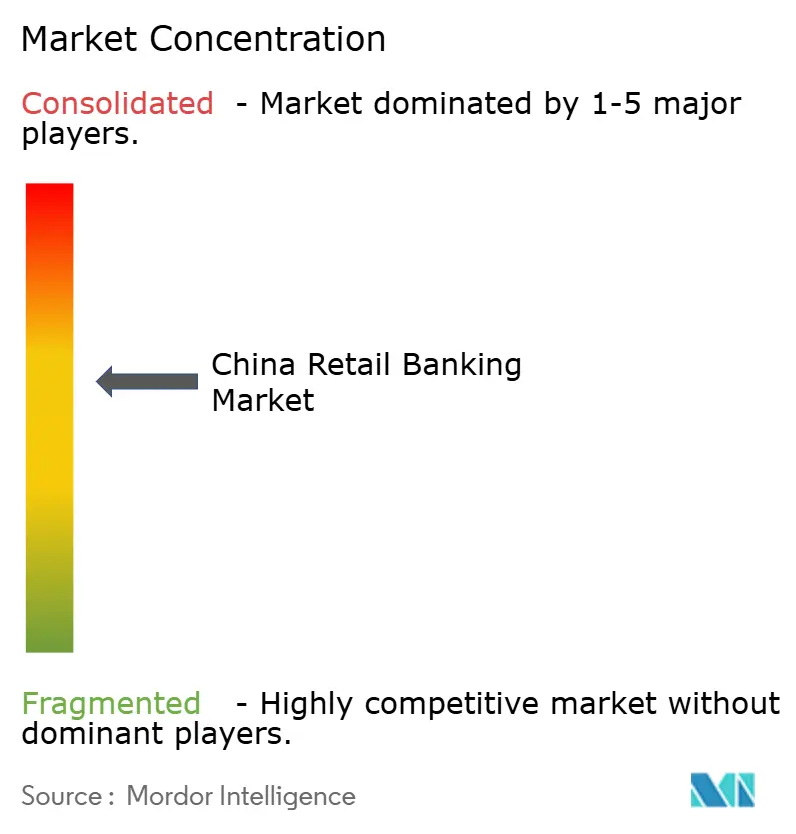

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Retail Banking Market Analysis by Mordor Intelligence

China retail banking market size in 2026 is estimated at USD 428.24 billion, growing from 2025 value of USD 397.4 billion with 2031 projections showing USD 622.04 billion, growing at 7.76% CAGR over 2026-2031. The expansion quickens as mobile payments, open-banking APIs, and biometric onboarding push traditional institutions to re-architect service delivery around digital channels. Government mandates on rural inclusion increase the addressable base, while green finance programs create fresh lending categories. Competition from super-apps compresses fee margins, so banks lean on data-driven cross-selling to defend profitability. Intensifying capital standards encourage a pivot toward fee income and asset-light advisory services, and the rising mass-affluent population supports demand for higher-yield investment products.

Key Report Takeaways

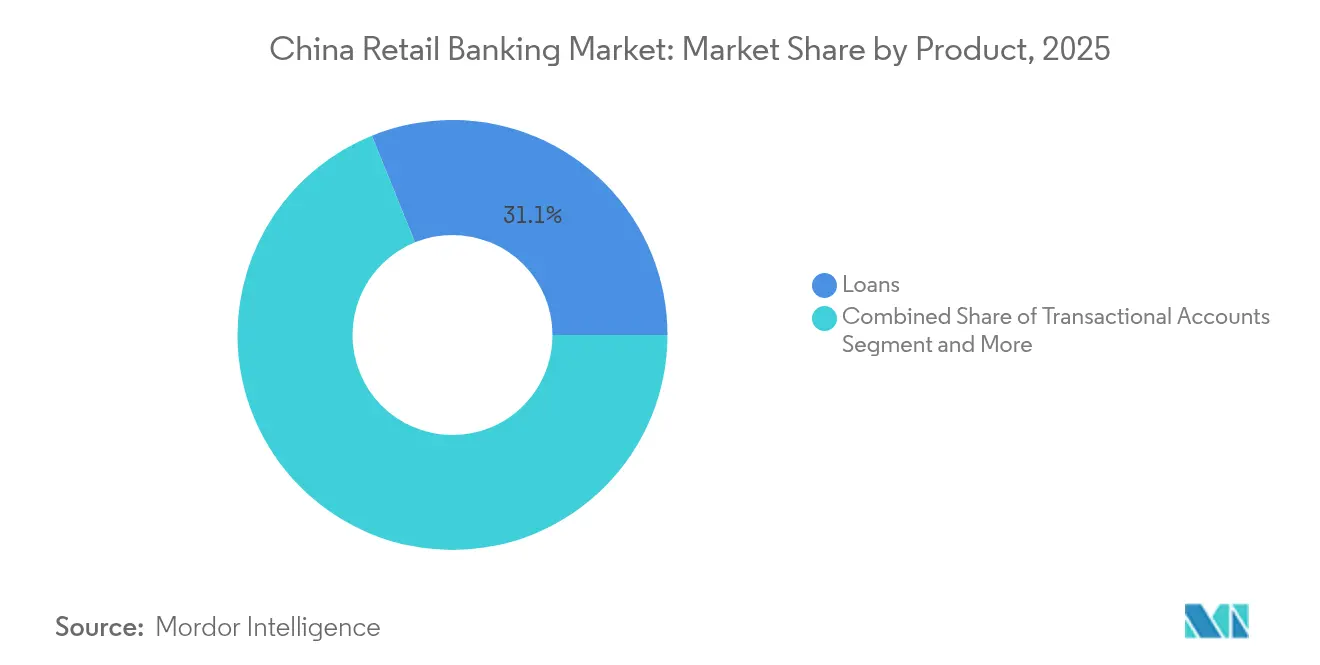

- By product, loans held 31.12% of China retail banking market share in 2025; credit cards are forecasted to expand at a 8.95% CAGR through 2031.

- By channel, online banking led with a 64.02% share of the China retail banking market in 2025, while mobile-first platforms are projected to grow at a 10.35% CAGR to 2031.

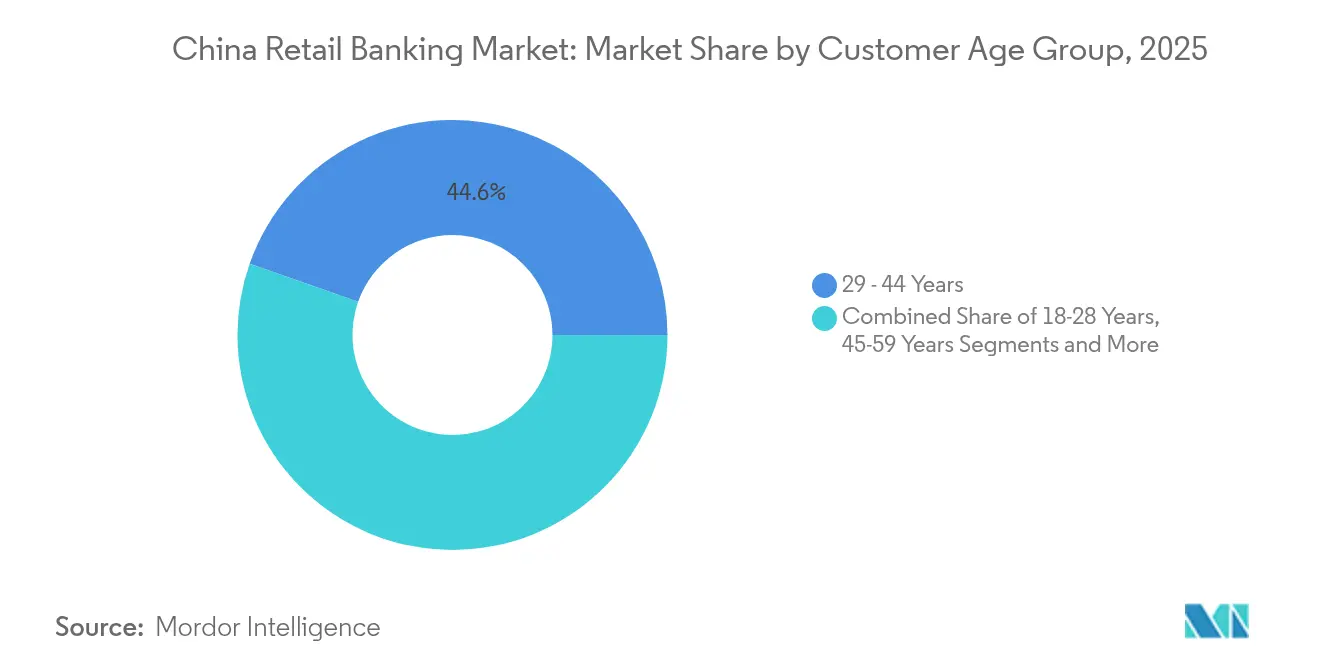

- By customer age group, the 29-44 cohort accounted for 44.62% of the China retail banking market size in 2025; the 18-28 cohort is projected to advance at a 9.55% CAGR between 2026-2031.

- By bank type, national banks commanded 67.15% of the market in 2025, whereas neobanks registered the highest projected CAGR at 11.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Retail Banking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile-payment ecosystem integration | +1.2% | Tier-1 cities (Beijing, Shanghai, Guangzhou, Shenzhen); expanding to Tier-2 | Short term (≤ 2 years) |

| Rural financial-inclusion push | +0.5% | Central and western rural provinces | Medium term (2-4 years) |

| Mass-affluent income growth | +1.8% | Eastern coastal provinces (Yangtze and Pearl River Deltas) | Short term (≤ 2 years) |

| Open-banking API adoption | +2.1% | National; strongest in technology hubs (Beijing, Shanghai, Hangzhou, Shenzhen) | Medium term (2-4 years) |

| Biometric authentication uptake | +1.7% | National; early adoption in urban centers | Short term (≤ 2 years) |

| Green-finance lending mandates | +1.0% | National; heightened in economically advanced regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Mobile Payment Ecosystem Integration

Transaction volumes on mobile platforms surpassed USD 12.8 trillion in 2024, and Alipay plus WeChat Pay captured 90% of that flow[1]National Bureau of Statistics of China, “Statistical Communiqué on the 2024 National Economic and Social Development,” stats.gov.cn. Banks that embed current-account, lending, and investment functions into these super-apps gain access to granular spending data that improves risk scoring and personalization. QR payments now dominate Tier-1 city point-of-sale environments, so branch and ATM usage continue to decline. Institutions unable to plug into these ecosystems risk losing visibility, prompting accelerated partnership activity and white-label wallet launches. The shift positions smartphones as the default branch for China's retail banking market and compresses legacy interchange revenues.

Regulatory Push for Rural Financial Inclusion

Village banks backed by large institutions extend basic deposit and micro-credit services deep into rural counties, aided by low-bandwidth mobile interfaces and biometrics that simplify know-your-customer compliance. Digital benefit disbursement platforms streamline welfare payments, raising household income stability and thus loan eligibility. While provincial gaps persist in fiber and 5G coverage, targeted infrastructure subsidies aim to narrow the divide by 2027. The initiative adds millions of new customers to China's retail banking market, though profitability hinges on low-cost digital servicing models that offset smaller ticket sizes.

High Disposable Income Growth Propelling Mass Affluent Segment

Average disposable income reached CNY 54,188 for urban households in 2024, creating a sizable tier seeking yield above basic deposit returns. Banks respond with tiered wealth-management centres that bundle funds, brokerage links, and robo-advice under premium loyalty plans. Relationship managers push structured deposits and ESG funds that align with green-lending priorities. Competition intensifies as securities firms and big-tech platforms court the same demographic, compelling banks to integrate lifestyle benefits within accounts. Mass-affluent dynamics increasingly shape product roadmaps across China's retail banking market.

Emergence of Open Banking APIs Facilitating Collaboration

Standardized APIs accelerate digital-product launches from years to months, enabling community banks to distribute third-party robo-advisors, buy-now-pay-later widgets, and insurance modules without large IT overhauls. The People’s Bank pilot on integrated cash pooling shows regulators embracing data-sharing under strict security rules[2]People’s Bank of China, “Notice on Pilot Cash Pooling for Multinational Corporations,” pbc.gov.cn. Technology hubs such as Shenzhen host vibrant sandbox programs where fintechs test niche propositions before nationwide scale-up. API ecosystems democratize innovation yet raise cyber-risk, so banks bolster tokenization and zero-trust architectures to protect customer assets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Super-app competition | -1.3% | National; greatest in Tier-1 and Tier-2 cities | Medium term (2-4 years) |

| Capital-adequacy reforms | -0.9% | National; sharper effect on smaller regional lenders | Medium term (2-4 years) |

| Aging population curbing mortgage demand | -0.4% | Lower-tier cities and rural areas, especially in northeastern China | Long term (≥ 4 years) |

| Cybersecurity breach incidents | -0.3% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intensifying Competition from Super-Apps

Alipay and WeChat Pay surround users with embedded wealth, micro-loan, and insurance tabs that displace bank mobile apps. Banks face a strategic crossroads: partner and pay referral fees or invest heavily in standalone digital experiences. The distraction pulls fee income away from card interchange, remittances, and FX spreads. Younger customers open accounts passively within super-apps, never setting foot in a physical branch. Defensive strategies include loyalty programs that tie rate boosts to broader product bundling, but margins tighten across China's retail banking market.

Stringent Capital Adequacy Reforms

The 2025 TLAC rollout requires higher buffers, constraining balance-sheet capacity for unsecured consumer loans. Large state-owned lenders tap domestic bond markets for fresh Tier-2 capital, whereas regional banks curb card issuance and pivot to brokered deposits. Fee-based services such as asset custody and credit-risk transfer gain traction because they consume minimal capital. Credit rationing opens a window for fintech lenders that operate under lighter rules, prompting regulators to consider a level-playing-field framework.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Loans Drive Profitability Despite Digital Shift

The loans segment contributed 31.12% to China's retail banking market share in 2025 and remains the primary earnings engine even as digital competition rises. Mortgage growth cooled with property-sector stress, yet mortgages still anchor relationship banking by generating stable funding and cross-sell flows. Rural revitalization policies push consumption and agricultural loans, while green lending balances jumped to CNY 30.1 trillion in 2024. Major banks package carbon-reduction mortgages that offer rate discounts when homes meet efficiency benchmarks, aligning product design with national sustainability goals.

Credit cards, though smaller in absolute volume, are projected to record a 8.95% CAGR, making them the fastest expanding line within China's retail banking market. Digital-issuance journeys now take under five minutes with near-instant biometric verification, sharply reducing acquisition costs. Revolving-credit margins offset interchange pressure from super-apps, and gamified cashback schemes resonate with digital natives. Savings and current accounts continue to anchor deposit franchises but face leakage to money-market funds marketed inside super-apps. As yields stay compressed, fee-bearing bundles that include wealth portals and lifestyle perks maintain account stickiness.

By Channel: Digital Dominance Reshapes Distribution

Online channels captured 64.02% of the market share in 2025, and mobile sessions eclipse desktop use by a five-to-one ratio. Industrial and Commercial Bank of China reported 260 million active mobile users, showing the centrality of handheld devices to customer engagement. Branch networks are being retooled into advisory lounges that focus on complex wealth and SME financing discussions rather than routine cash handling. Self-service kiosks and AI chatbots migrate simple service tasks out of branches, lowering cost-to-serve across China's retail banking market.

Offline distribution still matters for trust-building in high-ticket wealth or mortgage consultations. Large state-owned banks deploy smaller “light” outlets in remote towns to satisfy inclusion targets while avoiding full-service overhead. Fintech adoption has created a substitution effect for teller-based transactions in saturated metros and a complementary role in under-banked counties, illustrating a nuanced geographic interplay. The hybrid model balances digital convenience with human reassurance, keeping retention high among older customers and mass affluent segments.

By Customer Age Group: Demographic Shifts Drive Strategy

The 29-44 demographic held 44.62% of the China retail banking market size in 2025 and anchors profitability due to multi-product uptake covering housing, education, and investment needs. Banks segment this cohort further by life-stage triggers such as childbirth or entrepreneurship, pushing tailored bundles that combine insurance, loans, and asset-management plans. Digital service expectations are high, but personal advisory still influences complex decisions such as overseas education funding.

Youth aged 18-28 represent the fastest-growing slice, expanding at 9.55% CAGR through 2031. These digital natives open accounts entirely online, use QR codes for daily spend, and gravitate toward buy-now-pay-later modules embedded in e-commerce checkouts. Gamified savings pots and social-media badges boost engagement, while micro-investment features introduce wealth habits early. Banks that master personalized nudges and zero-fee student cards win early mind-share, laying the foundation for future wallet-share as incomes rise.

By Bank Type: National Champions Face Digital Challengers

National players controlled 67.15% of the China retail banking market in 2025, leveraging extensive branch grids and privileged policy roles. They channel significant credit toward strategic sectors and rural revitalization, reinforcing systemic importance. To stay relevant, these incumbents invest heavily in proprietary cloud cores and AI-driven risk engines that shorten loan approvals.

Neobanks clock an 11.05% forecast CAGR and carve niches with fee-free accounts, AI chatbots, and algorithmic credit scoring. Backed by tech giants, they deploy super-app distribution that on-boards customers in seconds and cross-sells merchant services. Regional banks adopt a hyper-local angle, emphasizing community ties and supply-chain finance for local SMEs. Cooperative models emerge as smaller lenders plug into open APIs from large banks, gaining scale in payments while retaining brand identity. The coexistence of these models enriches product diversity and accelerates digital standards across the China retail banking market.

Geography Analysis

Eastern coastal provinces, particularly the Yangtze and Pearl River Deltas, host the most mature slice of the China retail banking market. Urbanization reached 67.00% in 2024, and disposable incomes exceed the national average, fueling sophisticated demand for wealth management and foreign-currency services. Digital adoption is near universal in top-tier cities where mobile payments dominate daily life, and super-app ecosystems generate intense rivalry for customer attention.

Central provinces represent a second-wave growth corridor as inland city clusters industrialize and household incomes rise. Government stimulus funnels infrastructure spending into these regions, spurring SME formation and consumer-credit appetite. Banks strengthen branch-plus-digital hybrids here, pairing local relationship managers with mobile self-service platforms to expand reach cost-effectively. The China retail banking market experiences rapid gains in these zones, particularly in small-ticket consumer loans and first-time investment products.

Western and remote areas remain the frontier for inclusion. Sparse populations once made full branches uneconomic, yet satellite broadband and 5G are changing the equation. Village banks and fintech partnerships deliver micro-savings accounts and agricultural loans via simplified mobile apps. Regulatory subsidies lower network-deployment costs, and biometric KYC removes paperwork barriers for residents lacking traditional IDs. Successful penetration of these territories could add millions of new accounts, materially lifting the overall China retail banking market size.

Competitive Landscape

Four state-owned giants—ICBC, CCB, ABC, and BOC—account for a significant share of total banking assets, making the market structurally concentrated. Their scale affords funding cost advantages and positions them as primary conduits for policy lending. To counter digital disintermediation, each has launched proprietary super-apps, rolled out voice assistants, and migrated core systems to cloud-native stacks.

Mid-tier joint-stock and city commercial banks differentiate through regional specialization and niche verticals such as supply-chain finance for local manufacturers. Capital constraints limit expansive tech investment, so many subscribe to banking-as-a-service platforms that provide digital wallets, robo-advice, and risk models on demand. Strategic alliances with fintechs accelerate product cycles, allowing mid-tiers to defend share in the China retail banking market without large capex.

Neobanks backed by internet titans leverage vast social and e-commerce ecosystems to amass customers at low marginal cost. AI-driven credit engines enable near-instant micro-loans, and open-loop QR payment rails encourage embedded finance starts. They are moving upstream into wealth and SME lending, challenging incumbents beyond entry-level accounts. The competitive mix elevates customer expectations for seamless, contextual, and personalized services across the China retail banking market.

China Retail Banking Industry Leaders

Industrial and Commercial Bank of China Ltd.

China Construction Bank Corp.

Agricultural Bank of China Ltd.

Bank of China Ltd.

Bank of Communications Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The government injected RMB 520 billion into major banks, including ICBC and ABC, to offset property-sector stress, while BOC and CCB raised additional equity.

- April 2025: Fitch Ratings revised the outlook for ICBC, CCB, BOC, ABC, BOCOM, and China Merchants Bank to Stable, citing continued government support.

- January 2025: The People’s Bank of China and SAFE launched pilot cash-pooling rules for multinationals, while the National Financial Regulatory Administration issued first-ever data-security measures for banking and insurance.

- December 2024: The National Development and Reform Commission tightened foreign-debt approvals, with major syndicated loans such as RMB 75 billion for Guangzhou Metro Group.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines China's retail banking market as the value of fee and interest income generated from mass-market and mass-affluent customers through deposits, payment cards, personal loans, mortgages, and wealth-type savings products that are booked by licensed banks and regulated neobanks in mainland China.

Income from corporate banking, investment banking, and offshore bookkeeping is excluded to keep the retail focus clear.

Segmentation Overview

- By Product

- Transactional Accounts

- Savings Accounts

- Debit Cards

- Credit Cards

- Loans

- Other Products

- By Channel

- Online Banking

- Offline Banking

- By Customer Age Group

- 18-28 Years

- 29-44 Years

- 45-59 Years

- 60 Years and Above

- By Bank Type

- National Banks

- Regional Banks

- Neobanks & Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed branch managers, digital-channel heads, fintech association spokespeople, and former CBIRC officers across Beijing, Shanghai, Guangdong, and Sichuan. These discussions verified fee schedules, mobile-only account uptake, and risk appetite shifts, letting us fine-tune growth drivers and stress-test early model outputs.

Desk Research

We collated macro and banking-level indicators from reputable public sources such as the People's Bank of China, the China Banking and Insurance Regulatory Commission, the National Bureau of Statistics, OECD country tables, and IMF Financial Access Surveys, which give base figures for deposits, loan balances, branch counts, and digital usage. Company filings and investor decks augmented customer mix and pricing data, while D&B Hoovers supplied hard-to-find income splits for unlisted regional banks. News archives on Dow Jones Factiva helped us trace regulatory events that move retail spreads. The sources cited here are illustrative; many other public documents and databases were reviewed for validation and context.

Market-Sizing & Forecasting

A top-down build starts with household deposit stock, consumer loan outstandings, and card spending reported by regulators. These pools are forecast through multivariate regression that blends disposable income, urbanization, smartphone penetration, policy rates, and open-banking API adoption. Results are cross-checked with selective bottom-up cues, average revenue per customer and sampled branch counts, to ensure plausibility. Gaps in smaller provincial data are bridged by applying peer ratios adjusted for per-capita GDP. The baseline is then rolled forward using scenario ranges generated by ARIMA to capture cyclical swings.

Data Validation & Update Cycle

Each iteration passes two analyst reviews where variance triggers above three percentage points prompt source re-checks. We refresh models annually; material events such as sudden policy rate moves or pandemic waves initiate an interim update so clients always receive the latest view.

Why Mordor's China Retail Banking Baseline Commands Credibility

Published estimates often diverge because firms adopt different product baskets, pricing assumptions, and refresh cadences.

Key gap drivers include: some studies track only urban deposit income, others fold in corporate cash-management fees, and a few extrapolate from limited city surveys without reconciling with national regulator releases. Mordor's scope and dual-check process minimize those skews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 397.4 B (2025) | Mordor Intelligence | - |

| USD 170.5 B (2024) | Regional Consultancy A | Narrow urban scope and static FX conversion |

| USD 1.32 T (2025) | Trade Journal B | Includes corporate and treasury income; single-factor growth extrapolation |

These comparisons show that our disciplined variable selection, timely updates, and balanced top-down with bottom-up corroboration give decision-makers a dependable, transparent baseline.

Key Questions Answered in the Report

What is the current size of the China retail banking market?

The market stands at USD 428.24 billion in 2026 and is projected to grow to USD 622.04 billion by 2031.

Which product segment is the largest within China’s retail banking?

Loans dominate with a 31.12% market share in 2025, driven mainly by mortgages and inclusive-finance lending.

How fast is online banking growing in China?

Online channels already handle 64.02% of revenue and are forecast to expand at a 10.35% CAGR through 2031.

Which customer group is expanding fastest?

The 18-28 age cohort is growing at a 9.55% CAGR, propelled by digital-first banking habits and rising incomes.

What impact do super-apps have on traditional banks?

Super-apps like Alipay and WeChat Pay erode fee income and intercept customer relationships, reducing bank margins and forcing deeper digital integration.

How significant is green finance in Chinese retail banking?

Major banks reported green-loan balances rising more than 20% in 2024, underscoring sustainable lending as a key growth theme.

Page last updated on: